UK Income Tax Obligations for Individuals

VerifiedAdded on 2020/02/05

|13

|3354

|46

Report

AI Summary

This assignment delves into UK income tax regulations applicable to individuals. It focuses specifically on Emma's tax obligations for the 2014-15 accounting year. The analysis examines relevant HMRC standards and emphasizes the timely payment of taxes to avoid penalties. The document cites various legal texts, journals, and online resources to support its arguments.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Business and

taxation

taxation

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

Introduction .....................................................................................................................................3

Task A..............................................................................................................................................3

Tax implications of the commercial transactions........................................................................3

Task B..............................................................................................................................................6

Extraction of profits from a company and its implications.........................................................6

Tax calculations...........................................................................................................................7

Conclusion ....................................................................................................................................10

References......................................................................................................................................11

2

Introduction .....................................................................................................................................3

Task A..............................................................................................................................................3

Tax implications of the commercial transactions........................................................................3

Task B..............................................................................................................................................6

Extraction of profits from a company and its implications.........................................................6

Tax calculations...........................................................................................................................7

Conclusion ....................................................................................................................................10

References......................................................................................................................................11

2

INDEX OF TABLES

Table 1: Computation of NIC for 2014-15......................................................................................8

Table 2: Statement showing adjustment profit of Emma's company...............................................9

Table 3: Statement showing chargeable profit of Emma's company...............................................9

Table 4: Statement showing tax payable Emma's company............................................................9

Table 5: Statement showing computation of capital allowance.......................................................9

Table 6: Statement showing computation of capital gain tax of Emma........................................10

Table 7: Statement showing computation of capital gain by incorporation .................................11

Table 8: Statement showing computation of income tax ..............................................................11

3

Table 1: Computation of NIC for 2014-15......................................................................................8

Table 2: Statement showing adjustment profit of Emma's company...............................................9

Table 3: Statement showing chargeable profit of Emma's company...............................................9

Table 4: Statement showing tax payable Emma's company............................................................9

Table 5: Statement showing computation of capital allowance.......................................................9

Table 6: Statement showing computation of capital gain tax of Emma........................................10

Table 7: Statement showing computation of capital gain by incorporation .................................11

Table 8: Statement showing computation of income tax ..............................................................11

3

INTRODUCTION

Taxation can be defined as act of legal authorities of imposition of tax on commercial and

non-commercial transactions. Individuals and business entities are liable to pay tax charges for

the profit or benefit earned by them through operational activities in timely manner. Tax is levied

in UK on the basis of statutory norms described by HMRC. Taxes is payable in UK at minimum

three different level i.e. central government, local government and devolved national government

(Citron, 2010). Present study is focused on description of tax obligation of Emma by considering

operational activities of her business. For this aspect description of major taxes will be provided

such as NIC, corporation tax, capital gains tax, VAT and personal tax. In addition to this, various

methods for the tax planning will be discussed through which reduction can be made in tax

obligations.

TASK A

Tax implications of the commercial transactions

In accordance with the given case situation Emma is planning for the incorporation of

business for the purpose of expansion. For this aspect, she has option to either rent out the

building in the Europe or to purchase building by taking loan from the financial institutions. By

considering the provisions of corporate tax she is recommended to the rent out the premises in

Europe. It is because; he will be able to make deduction of the rent from the chargeable profits of

the company. However, similar benefit will not be provided in situation where loan is taken. It is

because; loan is taken prior to the incorporation. In addition to this, loan will make increase in

his financial obligation. Further, implications of the incorporation from the taxation point of

view is enumerated as below:

National Insurance contribution (NIC)

An individual or business entity is required to pay national insurance contribution in

situation where they have age more than equal to 16. Further, if employee is earning above £155

a week or in case of self employed their profit must be more than equal to £5,965 in a year. In

accordance with the UK taxation law, NI is the amount payable by workers and employers

towards the cost of certain state benefits (Henrekson and Sanandaji, 2011). These contributions

are collected by HMRC on the basis of PAYE system along with the income tax or repayment of

4

Taxation can be defined as act of legal authorities of imposition of tax on commercial and

non-commercial transactions. Individuals and business entities are liable to pay tax charges for

the profit or benefit earned by them through operational activities in timely manner. Tax is levied

in UK on the basis of statutory norms described by HMRC. Taxes is payable in UK at minimum

three different level i.e. central government, local government and devolved national government

(Citron, 2010). Present study is focused on description of tax obligation of Emma by considering

operational activities of her business. For this aspect description of major taxes will be provided

such as NIC, corporation tax, capital gains tax, VAT and personal tax. In addition to this, various

methods for the tax planning will be discussed through which reduction can be made in tax

obligations.

TASK A

Tax implications of the commercial transactions

In accordance with the given case situation Emma is planning for the incorporation of

business for the purpose of expansion. For this aspect, she has option to either rent out the

building in the Europe or to purchase building by taking loan from the financial institutions. By

considering the provisions of corporate tax she is recommended to the rent out the premises in

Europe. It is because; he will be able to make deduction of the rent from the chargeable profits of

the company. However, similar benefit will not be provided in situation where loan is taken. It is

because; loan is taken prior to the incorporation. In addition to this, loan will make increase in

his financial obligation. Further, implications of the incorporation from the taxation point of

view is enumerated as below:

National Insurance contribution (NIC)

An individual or business entity is required to pay national insurance contribution in

situation where they have age more than equal to 16. Further, if employee is earning above £155

a week or in case of self employed their profit must be more than equal to £5,965 in a year. In

accordance with the UK taxation law, NI is the amount payable by workers and employers

towards the cost of certain state benefits (Henrekson and Sanandaji, 2011). These contributions

are collected by HMRC on the basis of PAYE system along with the income tax or repayment of

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

the Student loan. Mainly there are three type of contribution classes in NIC. In this aspect,

employers and employees are covered in class 1, self employed is covered in class 2 and

voluntary payers are covered in class 3.

In accordance with the given information of Emma, she is self employed and planning for

the incorporation of business. On the basis of this aspect, it can be said that she is employer and

will be covered in class 1A. NIC of directors of company are computed on the annual basis. In

accordance with the provisions described by the HMRC rate of NIC will be 13.8%. Emma is in

position to deduct this amount from the payable salary of employees and further she is required

to submit this amount to the government authorities. In accordance with the given information

his salary is 60000 i.e. 1153 per week. Thus, he is required to pay NIC.

Corporation tax

Scope of corporation tax

Business formed as corporate entity are required to pay corporate tax on the earned profit

in accounting year. Taxable profits for the purpose of corporation tax is inclusive of money made

by company from doing business, investments and selling assets (Sungdoo, 2014). Rate of

corporation tax is as follows:

Particulars 2015 2014

Small companies (having profit less than £300000) 20%

Main rate companies (having profit more than £300000) 21%

Main rate on all profits exclusive of ring fence profits 20%

Marginal relief £300,000

Accounting period

Generally, tax is charged on corporate entities for the period of 12 months. However, in

the given case accounting period will be of 9 months because Emma would incorporate business

on 1 April 2014 and change the year end by 31st December 2014.

Chargeable profits

Corporation tax rate is applicable on amount of computed chargeable profits. This

amount is calculated by considering disallowed expenses and income of the business. Further,

adjustment of tax relief is made on the basis of provisions described by the HMRC.

5

employers and employees are covered in class 1, self employed is covered in class 2 and

voluntary payers are covered in class 3.

In accordance with the given information of Emma, she is self employed and planning for

the incorporation of business. On the basis of this aspect, it can be said that she is employer and

will be covered in class 1A. NIC of directors of company are computed on the annual basis. In

accordance with the provisions described by the HMRC rate of NIC will be 13.8%. Emma is in

position to deduct this amount from the payable salary of employees and further she is required

to submit this amount to the government authorities. In accordance with the given information

his salary is 60000 i.e. 1153 per week. Thus, he is required to pay NIC.

Corporation tax

Scope of corporation tax

Business formed as corporate entity are required to pay corporate tax on the earned profit

in accounting year. Taxable profits for the purpose of corporation tax is inclusive of money made

by company from doing business, investments and selling assets (Sungdoo, 2014). Rate of

corporation tax is as follows:

Particulars 2015 2014

Small companies (having profit less than £300000) 20%

Main rate companies (having profit more than £300000) 21%

Main rate on all profits exclusive of ring fence profits 20%

Marginal relief £300,000

Accounting period

Generally, tax is charged on corporate entities for the period of 12 months. However, in

the given case accounting period will be of 9 months because Emma would incorporate business

on 1 April 2014 and change the year end by 31st December 2014.

Chargeable profits

Corporation tax rate is applicable on amount of computed chargeable profits. This

amount is calculated by considering disallowed expenses and income of the business. Further,

adjustment of tax relief is made on the basis of provisions described by the HMRC.

5

Due dates

Corporation tax is required to be paid by director prior to 9 months of completion of

financial year. Further, return is required to be filed before 12 months from the date of closing of

accounting year.

Capital gain tax

Scope of tax

Capital gain tax can be defined as tax charges arises on the sale of a non-inventory assets

which was purchased at lower amount in comparison to its sales amount. Generally, two types of

capital gain tax rate is applied on individuals and business entities i.e. 18% and 28% on the basis

of their taxable income. Seller is chargeable for the payment of CGT on the sale of each

chargeable assets of the business. In accordance with the provisions of UK taxation law

chargeable assets are comprises of business premises, trademark and patent, goodwill and other

fixed assets (Terra and Wattèl, 2005 ). However, it will not include assets such as inventory or

debtors. Emma will be required to pay capital gain tax as properties of her business will be

transferred to the incorporation. For this property, consideration is paid by incorporation in form

of cash and equity.

Chargeable persons

Chargeable person in capital gain tax provisions is an individual who has liability for the

payment of tax charges on the profit occurred on the sale of asset. In the cited situation tax

obligation is payable by Emma thus he will be considered as chargeable person.

Assets and disposals

Provisions of capital gain tax are applicable only on the equipment having capital nature.

Further, HMRC had declared various assets exempt for the tax purpose. These assets are

comprises of government securities, shares related to NISA, PEP or ISA, car, investment in

personal equity plan etc (Oh, 2010). In addition to this, Emma will be required for the payment

of capital gain tax only if sales value of disposal asset is more than equal to £6,000.

Payment dates

Emma is required to pay tax charges on 5th April arising after the completion of financial

year of incorporation. In situation of self employed, capital gain tax will be payable on 31st

January.

6

Corporation tax is required to be paid by director prior to 9 months of completion of

financial year. Further, return is required to be filed before 12 months from the date of closing of

accounting year.

Capital gain tax

Scope of tax

Capital gain tax can be defined as tax charges arises on the sale of a non-inventory assets

which was purchased at lower amount in comparison to its sales amount. Generally, two types of

capital gain tax rate is applied on individuals and business entities i.e. 18% and 28% on the basis

of their taxable income. Seller is chargeable for the payment of CGT on the sale of each

chargeable assets of the business. In accordance with the provisions of UK taxation law

chargeable assets are comprises of business premises, trademark and patent, goodwill and other

fixed assets (Terra and Wattèl, 2005 ). However, it will not include assets such as inventory or

debtors. Emma will be required to pay capital gain tax as properties of her business will be

transferred to the incorporation. For this property, consideration is paid by incorporation in form

of cash and equity.

Chargeable persons

Chargeable person in capital gain tax provisions is an individual who has liability for the

payment of tax charges on the profit occurred on the sale of asset. In the cited situation tax

obligation is payable by Emma thus he will be considered as chargeable person.

Assets and disposals

Provisions of capital gain tax are applicable only on the equipment having capital nature.

Further, HMRC had declared various assets exempt for the tax purpose. These assets are

comprises of government securities, shares related to NISA, PEP or ISA, car, investment in

personal equity plan etc (Oh, 2010). In addition to this, Emma will be required for the payment

of capital gain tax only if sales value of disposal asset is more than equal to £6,000.

Payment dates

Emma is required to pay tax charges on 5th April arising after the completion of financial

year of incorporation. In situation of self employed, capital gain tax will be payable on 31st

January.

6

Value added tax (VAT)

Business organization operating in UK are required to pay VAT charges in situation

where they are dealing in chargeable goods and services. For this aspect, individuals are required

to take their registration number in order to pay chargeable amount (Rates and thresholds for

employers 2015 to 2016, 2015). It is a form of indirect as it is borne by another person and paid

by another person. VAT rates for goods and services is as follows:

Rate % of VAT Applicability on goods and

services

Standard 20% On most of the goods and

services

Reduced Rate 5% Some goods and services, such

as home energy and children’s

car seats.

Zero rate 0% On zero rated goods and

services

By incorporation of business Emma will be required to get registered under the

provisions of VAT. In addition to this, he will be entitled to charge tax from the customers and

get relief for the VAT paid to the sellers. In accordance with the provided business information,

previously he was not capable to get relief of the VAT paid.

Impact on Emma’s personal taxation position

From the above described transaction there will be various changes in taxation position of

the Emma. In accordance with the provisions described by the HMRC initially change will be in

his taxation status. Initially he was required to pay tax charges under the provisions of the self

employer but after the incorporation tax will be charged as per the provisions described for the

corporation entity (Income Tax rates and Personal Allowances, 2015). In addition to this, he will

be required for the payment of capital gain tax for the transfer of business assets from sole trader

to the company.

Emma will have legal obligation for getting registration under the provisions of VAT. It

is because, VAT number of incorporation is different in comparison to the self individual. Thus,

new VAT registration number should be taken on the name of the company. Contribution rate for

the pension will also differ in the cited scenario regarding national insurance on Emma.

7

Business organization operating in UK are required to pay VAT charges in situation

where they are dealing in chargeable goods and services. For this aspect, individuals are required

to take their registration number in order to pay chargeable amount (Rates and thresholds for

employers 2015 to 2016, 2015). It is a form of indirect as it is borne by another person and paid

by another person. VAT rates for goods and services is as follows:

Rate % of VAT Applicability on goods and

services

Standard 20% On most of the goods and

services

Reduced Rate 5% Some goods and services, such

as home energy and children’s

car seats.

Zero rate 0% On zero rated goods and

services

By incorporation of business Emma will be required to get registered under the

provisions of VAT. In addition to this, he will be entitled to charge tax from the customers and

get relief for the VAT paid to the sellers. In accordance with the provided business information,

previously he was not capable to get relief of the VAT paid.

Impact on Emma’s personal taxation position

From the above described transaction there will be various changes in taxation position of

the Emma. In accordance with the provisions described by the HMRC initially change will be in

his taxation status. Initially he was required to pay tax charges under the provisions of the self

employer but after the incorporation tax will be charged as per the provisions described for the

corporation entity (Income Tax rates and Personal Allowances, 2015). In addition to this, he will

be required for the payment of capital gain tax for the transfer of business assets from sole trader

to the company.

Emma will have legal obligation for getting registration under the provisions of VAT. It

is because, VAT number of incorporation is different in comparison to the self individual. Thus,

new VAT registration number should be taken on the name of the company. Contribution rate for

the pension will also differ in the cited scenario regarding national insurance on Emma.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK B

Extraction of profits from a company and its implications

Entire profits of the limited company is chargeable at the rate of 20%. Remaining profits

after the payment of tax charges is available for distribution to the owner as they have position of

director and shareholder. There are various ways through which profit of company can be

extracted by Emma. Description of these methods along with their impact is as follows:

Directors' fee

As a director of the limited company, Emma is in position to take directors' fee. For the

purpose of tax this fee will be similar to the drawing of salary. In accordance with the provisions

described by the HMRC directors' fee for most people is £192.30 per week. By making use of

this provisions Emma will be able to make optimum utilization of her personal allowance in

order to save the maximum amount of tax and contribution of NIC payable to the stated pension.

Dividends

Drawing dividends from company is generally more tax effective in comparison to the

director's fee. It is because, national insurance contribution is not payable on the amount of

dividend (Preshaw, 2015). In addition to this, tax on dividend is 10% while rate of corporation

tax is 20%. Thus, by extracting dividend from the profits of the company Emma can make

reduction in the oveall obligation.

Benefits in kind

Profits of the company can also be extracted in non-monetary manner. In this aspect,

Emma can make use of business property for the personal use. In the given case scenario, he is

provided with the car for the personal use as well as commercial use.

Pension

Contribution of pension can be paid at personal level and by the company. In addition to

this, contribution are tax efficient because it provides benefit of saving at the time of retirement

(Dowell, 2013). Pension payment can be made by company net of tax to the recognized pension

scheme in order to make reduction in the higher potential rate that can be incurred at that point of

time.

8

Extraction of profits from a company and its implications

Entire profits of the limited company is chargeable at the rate of 20%. Remaining profits

after the payment of tax charges is available for distribution to the owner as they have position of

director and shareholder. There are various ways through which profit of company can be

extracted by Emma. Description of these methods along with their impact is as follows:

Directors' fee

As a director of the limited company, Emma is in position to take directors' fee. For the

purpose of tax this fee will be similar to the drawing of salary. In accordance with the provisions

described by the HMRC directors' fee for most people is £192.30 per week. By making use of

this provisions Emma will be able to make optimum utilization of her personal allowance in

order to save the maximum amount of tax and contribution of NIC payable to the stated pension.

Dividends

Drawing dividends from company is generally more tax effective in comparison to the

director's fee. It is because, national insurance contribution is not payable on the amount of

dividend (Preshaw, 2015). In addition to this, tax on dividend is 10% while rate of corporation

tax is 20%. Thus, by extracting dividend from the profits of the company Emma can make

reduction in the oveall obligation.

Benefits in kind

Profits of the company can also be extracted in non-monetary manner. In this aspect,

Emma can make use of business property for the personal use. In the given case scenario, he is

provided with the car for the personal use as well as commercial use.

Pension

Contribution of pension can be paid at personal level and by the company. In addition to

this, contribution are tax efficient because it provides benefit of saving at the time of retirement

(Dowell, 2013). Pension payment can be made by company net of tax to the recognized pension

scheme in order to make reduction in the higher potential rate that can be incurred at that point of

time.

8

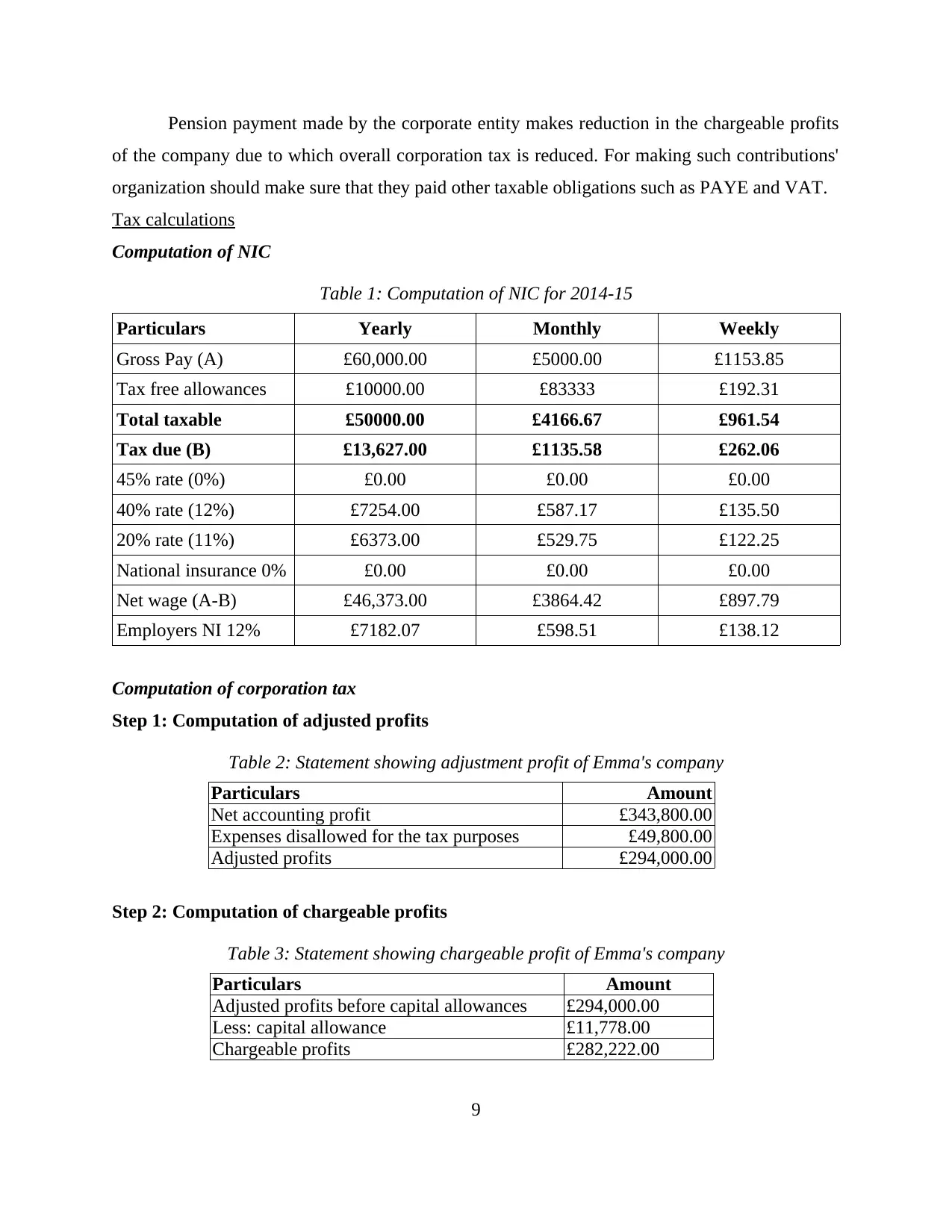

Pension payment made by the corporate entity makes reduction in the chargeable profits

of the company due to which overall corporation tax is reduced. For making such contributions'

organization should make sure that they paid other taxable obligations such as PAYE and VAT.

Tax calculations

Computation of NIC

Table 1: Computation of NIC for 2014-15

Particulars Yearly Monthly Weekly

Gross Pay (A) £60,000.00 £5000.00 £1153.85

Tax free allowances £10000.00 £83333 £192.31

Total taxable £50000.00 £4166.67 £961.54

Tax due (B) £13,627.00 £1135.58 £262.06

45% rate (0%) £0.00 £0.00 £0.00

40% rate (12%) £7254.00 £587.17 £135.50

20% rate (11%) £6373.00 £529.75 £122.25

National insurance 0% £0.00 £0.00 £0.00

Net wage (A-B) £46,373.00 £3864.42 £897.79

Employers NI 12% £7182.07 £598.51 £138.12

Computation of corporation tax

Step 1: Computation of adjusted profits

Table 2: Statement showing adjustment profit of Emma's company

Particulars Amount

Net accounting profit £343,800.00

Expenses disallowed for the tax purposes £49,800.00

Adjusted profits £294,000.00

Step 2: Computation of chargeable profits

Table 3: Statement showing chargeable profit of Emma's company

Particulars Amount

Adjusted profits before capital allowances £294,000.00

Less: capital allowance £11,778.00

Chargeable profits £282,222.00

9

of the company due to which overall corporation tax is reduced. For making such contributions'

organization should make sure that they paid other taxable obligations such as PAYE and VAT.

Tax calculations

Computation of NIC

Table 1: Computation of NIC for 2014-15

Particulars Yearly Monthly Weekly

Gross Pay (A) £60,000.00 £5000.00 £1153.85

Tax free allowances £10000.00 £83333 £192.31

Total taxable £50000.00 £4166.67 £961.54

Tax due (B) £13,627.00 £1135.58 £262.06

45% rate (0%) £0.00 £0.00 £0.00

40% rate (12%) £7254.00 £587.17 £135.50

20% rate (11%) £6373.00 £529.75 £122.25

National insurance 0% £0.00 £0.00 £0.00

Net wage (A-B) £46,373.00 £3864.42 £897.79

Employers NI 12% £7182.07 £598.51 £138.12

Computation of corporation tax

Step 1: Computation of adjusted profits

Table 2: Statement showing adjustment profit of Emma's company

Particulars Amount

Net accounting profit £343,800.00

Expenses disallowed for the tax purposes £49,800.00

Adjusted profits £294,000.00

Step 2: Computation of chargeable profits

Table 3: Statement showing chargeable profit of Emma's company

Particulars Amount

Adjusted profits before capital allowances £294,000.00

Less: capital allowance £11,778.00

Chargeable profits £282,222.00

9

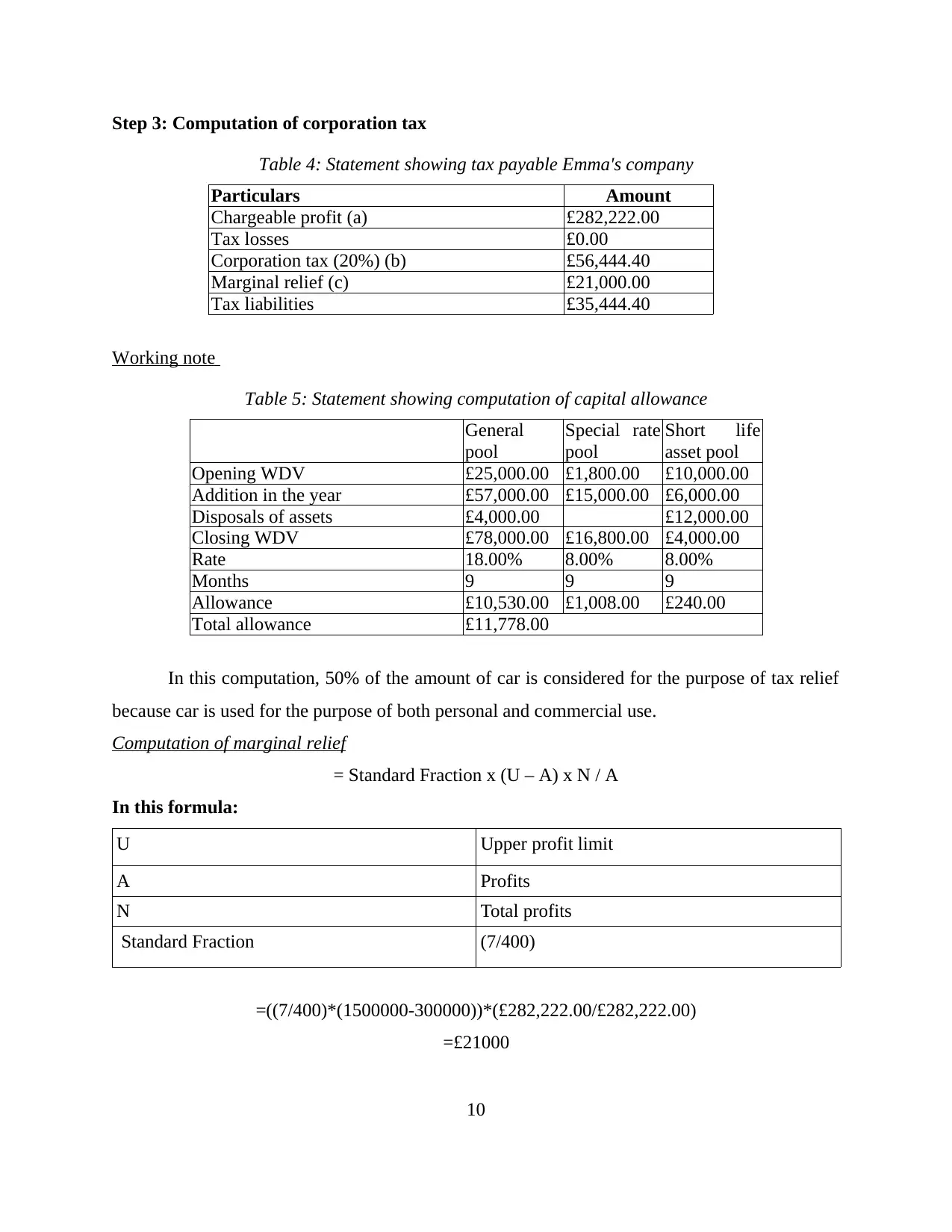

Step 3: Computation of corporation tax

Table 4: Statement showing tax payable Emma's company

Particulars Amount

Chargeable profit (a) £282,222.00

Tax losses £0.00

Corporation tax (20%) (b) £56,444.40

Marginal relief (c) £21,000.00

Tax liabilities £35,444.40

Working note

Table 5: Statement showing computation of capital allowance

General

pool

Special rate

pool

Short life

asset pool

Opening WDV £25,000.00 £1,800.00 £10,000.00

Addition in the year £57,000.00 £15,000.00 £6,000.00

Disposals of assets £4,000.00 £12,000.00

Closing WDV £78,000.00 £16,800.00 £4,000.00

Rate 18.00% 8.00% 8.00%

Months 9 9 9

Allowance £10,530.00 £1,008.00 £240.00

Total allowance £11,778.00

In this computation, 50% of the amount of car is considered for the purpose of tax relief

because car is used for the purpose of both personal and commercial use.

Computation of marginal relief

= Standard Fraction x (U – A) x N / A

In this formula:

U Upper profit limit

A Profits

N Total profits

Standard Fraction (7/400)

=((7/400)*(1500000-300000))*(£282,222.00/£282,222.00)

=£21000

10

Table 4: Statement showing tax payable Emma's company

Particulars Amount

Chargeable profit (a) £282,222.00

Tax losses £0.00

Corporation tax (20%) (b) £56,444.40

Marginal relief (c) £21,000.00

Tax liabilities £35,444.40

Working note

Table 5: Statement showing computation of capital allowance

General

pool

Special rate

pool

Short life

asset pool

Opening WDV £25,000.00 £1,800.00 £10,000.00

Addition in the year £57,000.00 £15,000.00 £6,000.00

Disposals of assets £4,000.00 £12,000.00

Closing WDV £78,000.00 £16,800.00 £4,000.00

Rate 18.00% 8.00% 8.00%

Months 9 9 9

Allowance £10,530.00 £1,008.00 £240.00

Total allowance £11,778.00

In this computation, 50% of the amount of car is considered for the purpose of tax relief

because car is used for the purpose of both personal and commercial use.

Computation of marginal relief

= Standard Fraction x (U – A) x N / A

In this formula:

U Upper profit limit

A Profits

N Total profits

Standard Fraction (7/400)

=((7/400)*(1500000-300000))*(£282,222.00/£282,222.00)

=£21000

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

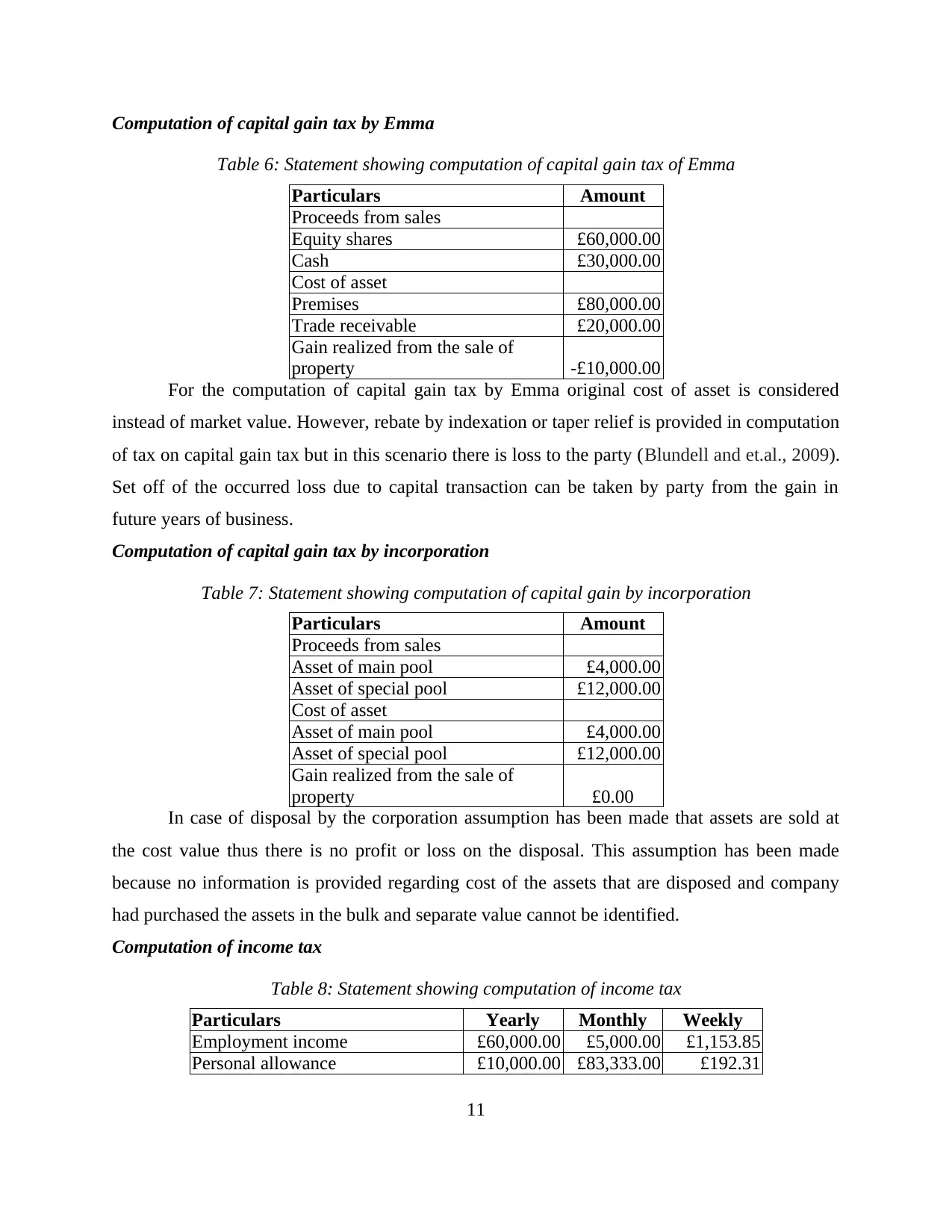

Computation of capital gain tax by Emma

Table 6: Statement showing computation of capital gain tax of Emma

Particulars Amount

Proceeds from sales

Equity shares £60,000.00

Cash £30,000.00

Cost of asset

Premises £80,000.00

Trade receivable £20,000.00

Gain realized from the sale of

property -£10,000.00

For the computation of capital gain tax by Emma original cost of asset is considered

instead of market value. However, rebate by indexation or taper relief is provided in computation

of tax on capital gain tax but in this scenario there is loss to the party (Blundell and et.al., 2009).

Set off of the occurred loss due to capital transaction can be taken by party from the gain in

future years of business.

Computation of capital gain tax by incorporation

Table 7: Statement showing computation of capital gain by incorporation

Particulars Amount

Proceeds from sales

Asset of main pool £4,000.00

Asset of special pool £12,000.00

Cost of asset

Asset of main pool £4,000.00

Asset of special pool £12,000.00

Gain realized from the sale of

property £0.00

In case of disposal by the corporation assumption has been made that assets are sold at

the cost value thus there is no profit or loss on the disposal. This assumption has been made

because no information is provided regarding cost of the assets that are disposed and company

had purchased the assets in the bulk and separate value cannot be identified.

Computation of income tax

Table 8: Statement showing computation of income tax

Particulars Yearly Monthly Weekly

Employment income £60,000.00 £5,000.00 £1,153.85

Personal allowance £10,000.00 £83,333.00 £192.31

11

Table 6: Statement showing computation of capital gain tax of Emma

Particulars Amount

Proceeds from sales

Equity shares £60,000.00

Cash £30,000.00

Cost of asset

Premises £80,000.00

Trade receivable £20,000.00

Gain realized from the sale of

property -£10,000.00

For the computation of capital gain tax by Emma original cost of asset is considered

instead of market value. However, rebate by indexation or taper relief is provided in computation

of tax on capital gain tax but in this scenario there is loss to the party (Blundell and et.al., 2009).

Set off of the occurred loss due to capital transaction can be taken by party from the gain in

future years of business.

Computation of capital gain tax by incorporation

Table 7: Statement showing computation of capital gain by incorporation

Particulars Amount

Proceeds from sales

Asset of main pool £4,000.00

Asset of special pool £12,000.00

Cost of asset

Asset of main pool £4,000.00

Asset of special pool £12,000.00

Gain realized from the sale of

property £0.00

In case of disposal by the corporation assumption has been made that assets are sold at

the cost value thus there is no profit or loss on the disposal. This assumption has been made

because no information is provided regarding cost of the assets that are disposed and company

had purchased the assets in the bulk and separate value cannot be identified.

Computation of income tax

Table 8: Statement showing computation of income tax

Particulars Yearly Monthly Weekly

Employment income £60,000.00 £5,000.00 £1,153.85

Personal allowance £10,000.00 £83,333.00 £192.31

11

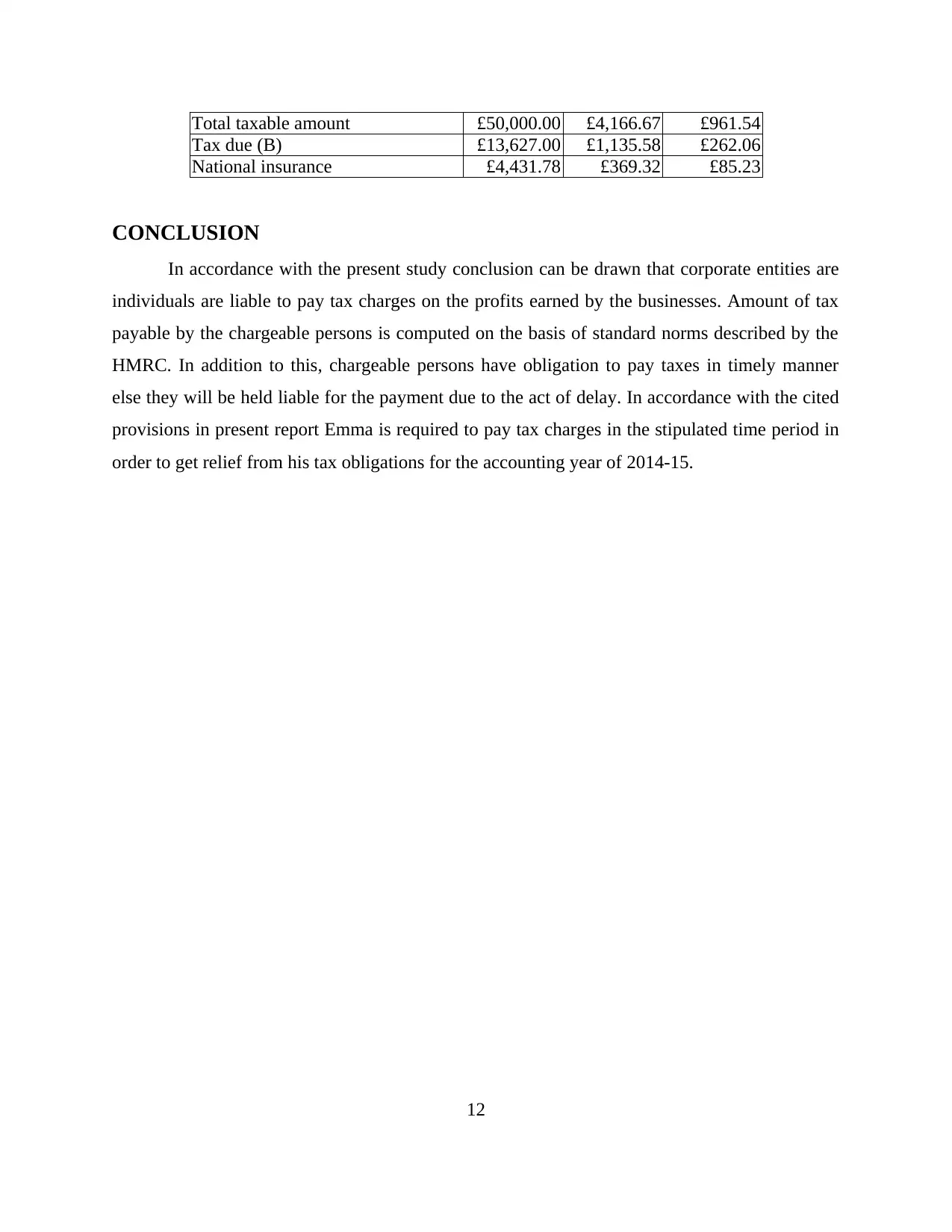

Total taxable amount £50,000.00 £4,166.67 £961.54

Tax due (B) £13,627.00 £1,135.58 £262.06

National insurance £4,431.78 £369.32 £85.23

CONCLUSION

In accordance with the present study conclusion can be drawn that corporate entities are

individuals are liable to pay tax charges on the profits earned by the businesses. Amount of tax

payable by the chargeable persons is computed on the basis of standard norms described by the

HMRC. In addition to this, chargeable persons have obligation to pay taxes in timely manner

else they will be held liable for the payment due to the act of delay. In accordance with the cited

provisions in present report Emma is required to pay tax charges in the stipulated time period in

order to get relief from his tax obligations for the accounting year of 2014-15.

12

Tax due (B) £13,627.00 £1,135.58 £262.06

National insurance £4,431.78 £369.32 £85.23

CONCLUSION

In accordance with the present study conclusion can be drawn that corporate entities are

individuals are liable to pay tax charges on the profits earned by the businesses. Amount of tax

payable by the chargeable persons is computed on the basis of standard norms described by the

HMRC. In addition to this, chargeable persons have obligation to pay taxes in timely manner

else they will be held liable for the payment due to the act of delay. In accordance with the cited

provisions in present report Emma is required to pay tax charges in the stipulated time period in

order to get relief from his tax obligations for the accounting year of 2014-15.

12

REFERENCES

Books and journals

Blundell, R. and et.al., 2009. Optimal Income Taxation of Lone Mothers: An Empirical

Comparison of the UK and Germany. The Economic Journal.119(535). Pp.101-121.

Citron, D. B., 2010. The valuation of deferred taxation: Evidence from the UK partial provision

approach. Journal of Business Finance & Accounting. 28(7‐8). Pp.821-852.

Dowell, S., 2013. History of Taxation and Taxes in England. Routledge.

Henrekson, M. and Sanandaji, T., 2011. Entrepreneurship and the theory of taxation. Small

Business Economics. 37(2). pp. 167-185.

McGuire, E. B., 2013. The British tariff system. Routledge.

Oh, Y., 2010. Consolidated Tax Return System and Corporate Tax Act.Seoultaxlawreview. 16(3).

pp.256-288.

Sungdoo, J., 2014. Review of 2013 “Income Tax Law” and “Inheritance and Gift Tax Law”

Cases.seoultaxlawreview. 20(1). pp.325-373.

Terra, B. and Wattèl, P., 2005. European tax law. The Hague: Kluwer Law International.

Online

Income Tax rates and Personal Allowances. 2015. [Online]. Available

at:<https://www.gov.uk/income-tax-rates>. [Accessed on 23rd March 2016].

Preshaw, J., 2015. Management of Taxes Sub-Committee. [Online]. Available through

<https://www.tax.org.uk/tax-policy/remit-of-technical-committee/ManagementofTaxes>

. [Accessed on 23rd March 2016].

Rates and thresholds for employers 2015 to 2016. 2015. [Online]. Available

at:<https://www.gov.uk/guidance/rates-and-thresholds-for-employers-2015-to-2016>.

[Accessed on 23rd March 2016].

13

Books and journals

Blundell, R. and et.al., 2009. Optimal Income Taxation of Lone Mothers: An Empirical

Comparison of the UK and Germany. The Economic Journal.119(535). Pp.101-121.

Citron, D. B., 2010. The valuation of deferred taxation: Evidence from the UK partial provision

approach. Journal of Business Finance & Accounting. 28(7‐8). Pp.821-852.

Dowell, S., 2013. History of Taxation and Taxes in England. Routledge.

Henrekson, M. and Sanandaji, T., 2011. Entrepreneurship and the theory of taxation. Small

Business Economics. 37(2). pp. 167-185.

McGuire, E. B., 2013. The British tariff system. Routledge.

Oh, Y., 2010. Consolidated Tax Return System and Corporate Tax Act.Seoultaxlawreview. 16(3).

pp.256-288.

Sungdoo, J., 2014. Review of 2013 “Income Tax Law” and “Inheritance and Gift Tax Law”

Cases.seoultaxlawreview. 20(1). pp.325-373.

Terra, B. and Wattèl, P., 2005. European tax law. The Hague: Kluwer Law International.

Online

Income Tax rates and Personal Allowances. 2015. [Online]. Available

at:<https://www.gov.uk/income-tax-rates>. [Accessed on 23rd March 2016].

Preshaw, J., 2015. Management of Taxes Sub-Committee. [Online]. Available through

<https://www.tax.org.uk/tax-policy/remit-of-technical-committee/ManagementofTaxes>

. [Accessed on 23rd March 2016].

Rates and thresholds for employers 2015 to 2016. 2015. [Online]. Available

at:<https://www.gov.uk/guidance/rates-and-thresholds-for-employers-2015-to-2016>.

[Accessed on 23rd March 2016].

13

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.