Finance Report: Business Calculations for Dominoz and Retail

VerifiedAdded on 2020/12/24

|15

|3619

|500

Report

AI Summary

This report presents a comprehensive financial analysis of Dominoz Pizza Enterprises Limited and Retail Food Group Limited, focusing on key business calculations and performance metrics. It begins by calculating holding period returns for both companies over a five-year period, followed by the determination of expected returns using probability distributions. The report then computes total returns to shareholders, considering both share price changes and dividends. A significant portion of the analysis is dedicated to examining the share price fluctuations and their impact on company performance, highlighting the contrasting trends between Dominoz, which shows positive growth, and Retail Food Group, which exhibits a decline. The analysis further delves into a detailed ratio analysis, including earnings per share, net profit margin, asset turnover, leverage, return on equity, quick ratio, and debt-to-equity ratio for both companies. A comparative and contrastive analysis of the performance of both companies, with a focus on growth in different financial ratios, is presented, highlighting the strengths and weaknesses of each company based on profitability, efficiency, and liquidity ratios. The report concludes with an evaluation of the factors influencing the financial performance of both companies and their implications for stakeholders.

Business Calculations

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

TASK 1............................................................................................................................................1

Question 1....................................................................................................................................1

Question 2....................................................................................................................................1

Question 3....................................................................................................................................2

Question 4....................................................................................................................................3

Question 5....................................................................................................................................3

Question 6....................................................................................................................................7

TASK 2............................................................................................................................................8

Question 1....................................................................................................................................8

Question 2....................................................................................................................................9

Question 3....................................................................................................................................9

Question 4..................................................................................................................................10

Question 5..................................................................................................................................11

Question 6..................................................................................................................................11

Question 7..................................................................................................................................11

Question 8..................................................................................................................................11

REFERENCES..............................................................................................................................13

TASK 1............................................................................................................................................1

Question 1....................................................................................................................................1

Question 2....................................................................................................................................1

Question 3....................................................................................................................................2

Question 4....................................................................................................................................3

Question 5....................................................................................................................................3

Question 6....................................................................................................................................7

TASK 2............................................................................................................................................8

Question 1....................................................................................................................................8

Question 2....................................................................................................................................9

Question 3....................................................................................................................................9

Question 4..................................................................................................................................10

Question 5..................................................................................................................................11

Question 6..................................................................................................................................11

Question 7..................................................................................................................................11

Question 8..................................................................................................................................11

REFERENCES..............................................................................................................................13

TASK 1

Question 1

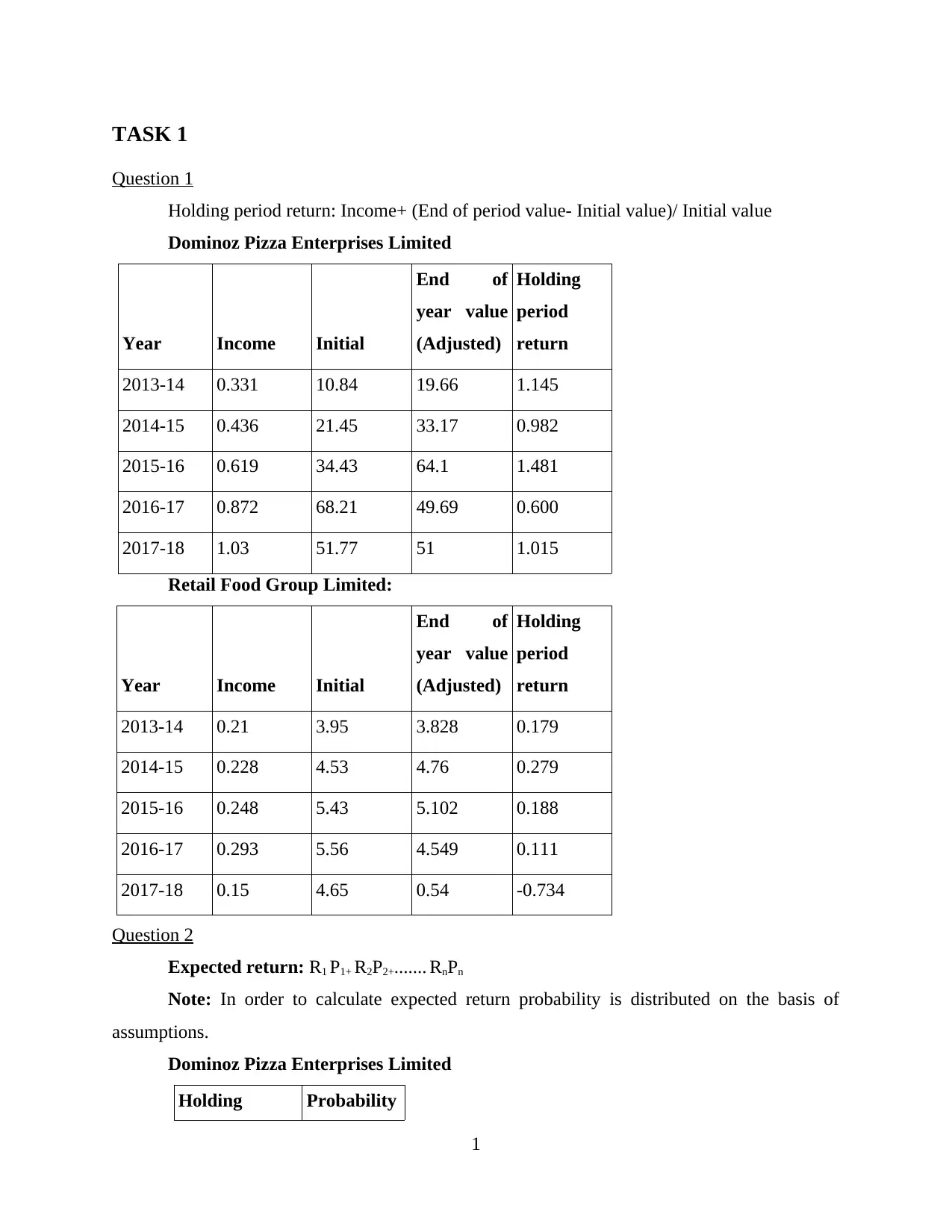

Holding period return: Income+ (End of period value- Initial value)/ Initial value

Dominoz Pizza Enterprises Limited

Year Income Initial

End of

year value

(Adjusted)

Holding

period

return

2013-14 0.331 10.84 19.66 1.145

2014-15 0.436 21.45 33.17 0.982

2015-16 0.619 34.43 64.1 1.481

2016-17 0.872 68.21 49.69 0.600

2017-18 1.03 51.77 51 1.015

Retail Food Group Limited:

Year Income Initial

End of

year value

(Adjusted)

Holding

period

return

2013-14 0.21 3.95 3.828 0.179

2014-15 0.228 4.53 4.76 0.279

2015-16 0.248 5.43 5.102 0.188

2016-17 0.293 5.56 4.549 0.111

2017-18 0.15 4.65 0.54 -0.734

Question 2

Expected return: R1 P1+ R2P2+....... RnPn

Note: In order to calculate expected return probability is distributed on the basis of

assumptions.

Dominoz Pizza Enterprises Limited

Holding Probability

1

Question 1

Holding period return: Income+ (End of period value- Initial value)/ Initial value

Dominoz Pizza Enterprises Limited

Year Income Initial

End of

year value

(Adjusted)

Holding

period

return

2013-14 0.331 10.84 19.66 1.145

2014-15 0.436 21.45 33.17 0.982

2015-16 0.619 34.43 64.1 1.481

2016-17 0.872 68.21 49.69 0.600

2017-18 1.03 51.77 51 1.015

Retail Food Group Limited:

Year Income Initial

End of

year value

(Adjusted)

Holding

period

return

2013-14 0.21 3.95 3.828 0.179

2014-15 0.228 4.53 4.76 0.279

2015-16 0.248 5.43 5.102 0.188

2016-17 0.293 5.56 4.549 0.111

2017-18 0.15 4.65 0.54 -0.734

Question 2

Expected return: R1 P1+ R2P2+....... RnPn

Note: In order to calculate expected return probability is distributed on the basis of

assumptions.

Dominoz Pizza Enterprises Limited

Holding Probability

1

You're viewing a preview

Unlock full access by subscribing today!

period return

1.145 0.2

0.982 0.2

1.481 0.2

0.600 0.2

1.015 0.2

= (1.145*0.2) + (0.982*0.2) + (0.1481*0.2) + (0.600*0.2) + (0.1015*0.2)

=1.0447

Retail Food Group Limited:

Holding period

return Probability

0.179 0.2

0.279 0.2

0.188 0.2

0.111 0.2

-0.734 0.2

= (0.179*0.2) + (0.279*0.2) + (0.188*0.2) +(0.111*0.2) + (-0.734*0.2)

= 0.0045551789

Question 3

Total return to shareholders for Dominos: [P5+D1-5/P0](1/5)-1

[51+ (0.331-1.03) /40.40] (1/5 )-1

= [51-0.699 /40.40] (1/5 )-1

= [1.245] (1/5) -1

= [1.245]0.20 -1

= 1.044-1

= 0.044

Total return to shareholders for Retail: [P5+D1-5/P0](1/5)-1

[0.54+ (0.21-0.15) /0.19] (1/5)- 1

2

1.145 0.2

0.982 0.2

1.481 0.2

0.600 0.2

1.015 0.2

= (1.145*0.2) + (0.982*0.2) + (0.1481*0.2) + (0.600*0.2) + (0.1015*0.2)

=1.0447

Retail Food Group Limited:

Holding period

return Probability

0.179 0.2

0.279 0.2

0.188 0.2

0.111 0.2

-0.734 0.2

= (0.179*0.2) + (0.279*0.2) + (0.188*0.2) +(0.111*0.2) + (-0.734*0.2)

= 0.0045551789

Question 3

Total return to shareholders for Dominos: [P5+D1-5/P0](1/5)-1

[51+ (0.331-1.03) /40.40] (1/5 )-1

= [51-0.699 /40.40] (1/5 )-1

= [1.245] (1/5) -1

= [1.245]0.20 -1

= 1.044-1

= 0.044

Total return to shareholders for Retail: [P5+D1-5/P0](1/5)-1

[0.54+ (0.21-0.15) /0.19] (1/5)- 1

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

= [0.54+ 0.06 /0.19] (1/5)- 1

= [3.158] (1/5)- 1

= [3.158]0.20 -1

= 1.259-1

= 0.259

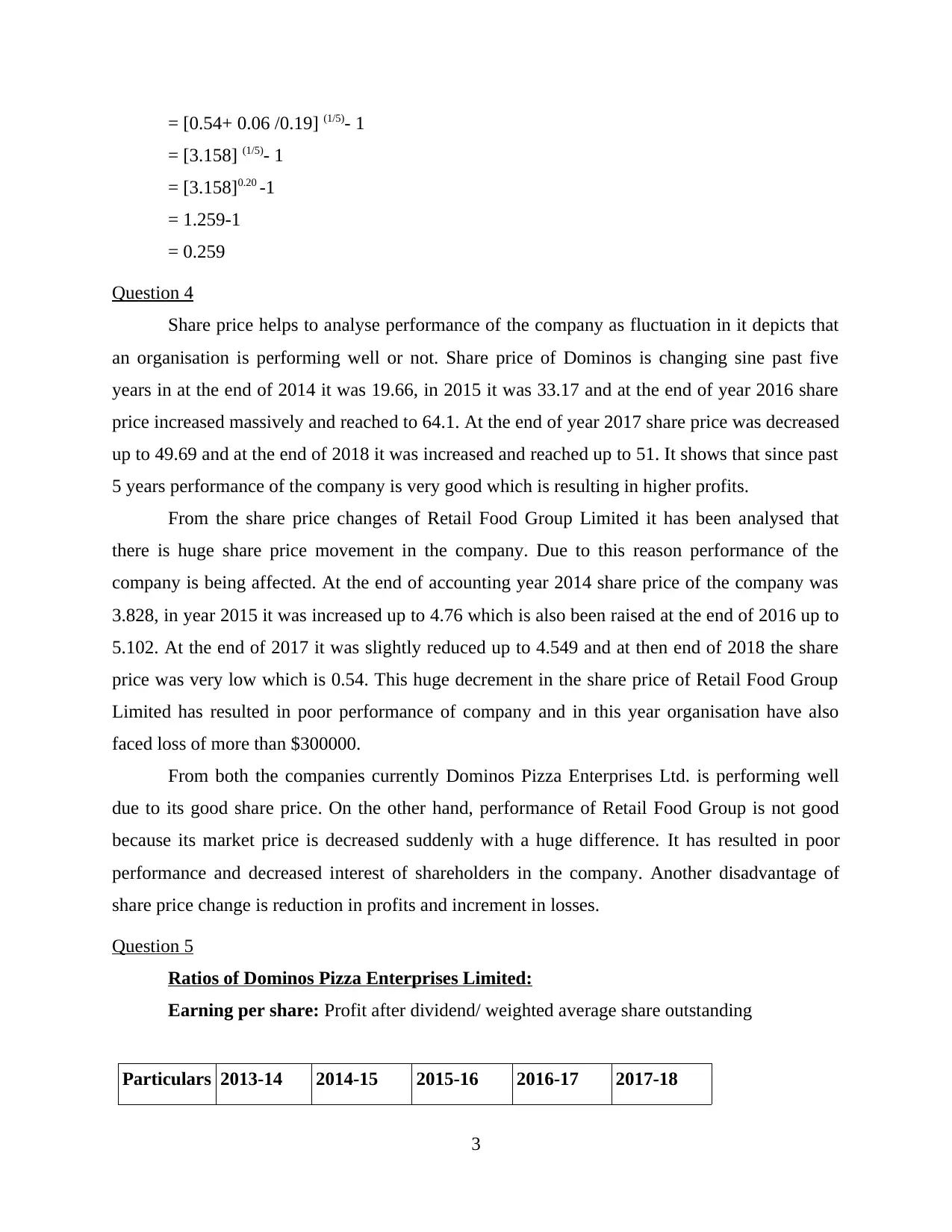

Question 4

Share price helps to analyse performance of the company as fluctuation in it depicts that

an organisation is performing well or not. Share price of Dominos is changing sine past five

years in at the end of 2014 it was 19.66, in 2015 it was 33.17 and at the end of year 2016 share

price increased massively and reached to 64.1. At the end of year 2017 share price was decreased

up to 49.69 and at the end of 2018 it was increased and reached up to 51. It shows that since past

5 years performance of the company is very good which is resulting in higher profits.

From the share price changes of Retail Food Group Limited it has been analysed that

there is huge share price movement in the company. Due to this reason performance of the

company is being affected. At the end of accounting year 2014 share price of the company was

3.828, in year 2015 it was increased up to 4.76 which is also been raised at the end of 2016 up to

5.102. At the end of 2017 it was slightly reduced up to 4.549 and at then end of 2018 the share

price was very low which is 0.54. This huge decrement in the share price of Retail Food Group

Limited has resulted in poor performance of company and in this year organisation have also

faced loss of more than $300000.

From both the companies currently Dominos Pizza Enterprises Ltd. is performing well

due to its good share price. On the other hand, performance of Retail Food Group is not good

because its market price is decreased suddenly with a huge difference. It has resulted in poor

performance and decreased interest of shareholders in the company. Another disadvantage of

share price change is reduction in profits and increment in losses.

Question 5

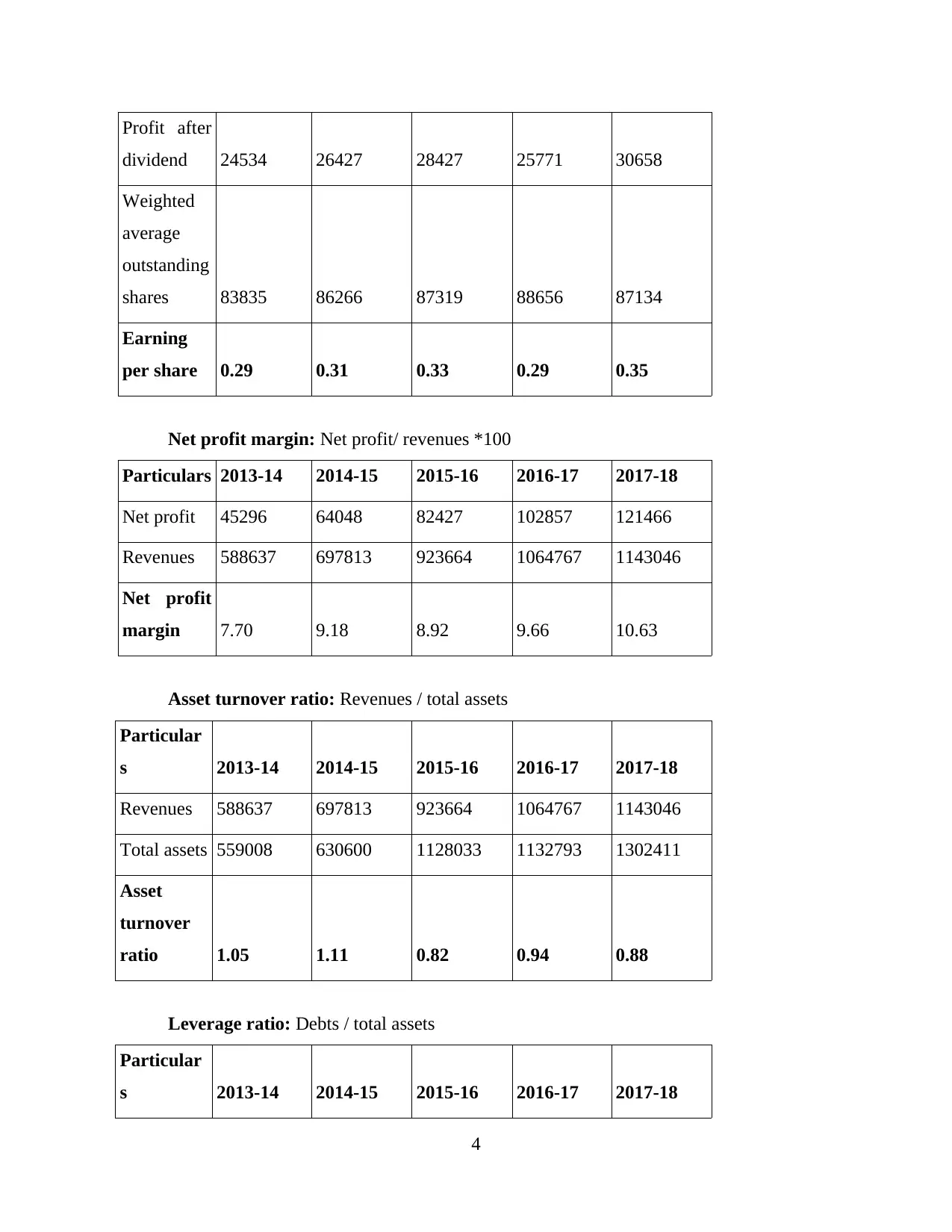

Ratios of Dominos Pizza Enterprises Limited:

Earning per share: Profit after dividend/ weighted average share outstanding

Particulars 2013-14 2014-15 2015-16 2016-17 2017-18

3

= [3.158] (1/5)- 1

= [3.158]0.20 -1

= 1.259-1

= 0.259

Question 4

Share price helps to analyse performance of the company as fluctuation in it depicts that

an organisation is performing well or not. Share price of Dominos is changing sine past five

years in at the end of 2014 it was 19.66, in 2015 it was 33.17 and at the end of year 2016 share

price increased massively and reached to 64.1. At the end of year 2017 share price was decreased

up to 49.69 and at the end of 2018 it was increased and reached up to 51. It shows that since past

5 years performance of the company is very good which is resulting in higher profits.

From the share price changes of Retail Food Group Limited it has been analysed that

there is huge share price movement in the company. Due to this reason performance of the

company is being affected. At the end of accounting year 2014 share price of the company was

3.828, in year 2015 it was increased up to 4.76 which is also been raised at the end of 2016 up to

5.102. At the end of 2017 it was slightly reduced up to 4.549 and at then end of 2018 the share

price was very low which is 0.54. This huge decrement in the share price of Retail Food Group

Limited has resulted in poor performance of company and in this year organisation have also

faced loss of more than $300000.

From both the companies currently Dominos Pizza Enterprises Ltd. is performing well

due to its good share price. On the other hand, performance of Retail Food Group is not good

because its market price is decreased suddenly with a huge difference. It has resulted in poor

performance and decreased interest of shareholders in the company. Another disadvantage of

share price change is reduction in profits and increment in losses.

Question 5

Ratios of Dominos Pizza Enterprises Limited:

Earning per share: Profit after dividend/ weighted average share outstanding

Particulars 2013-14 2014-15 2015-16 2016-17 2017-18

3

Profit after

dividend 24534 26427 28427 25771 30658

Weighted

average

outstanding

shares 83835 86266 87319 88656 87134

Earning

per share 0.29 0.31 0.33 0.29 0.35

Net profit margin: Net profit/ revenues *100

Particulars 2013-14 2014-15 2015-16 2016-17 2017-18

Net profit 45296 64048 82427 102857 121466

Revenues 588637 697813 923664 1064767 1143046

Net profit

margin 7.70 9.18 8.92 9.66 10.63

Asset turnover ratio: Revenues / total assets

Particular

s 2013-14 2014-15 2015-16 2016-17 2017-18

Revenues 588637 697813 923664 1064767 1143046

Total assets 559008 630600 1128033 1132793 1302411

Asset

turnover

ratio 1.05 1.11 0.82 0.94 0.88

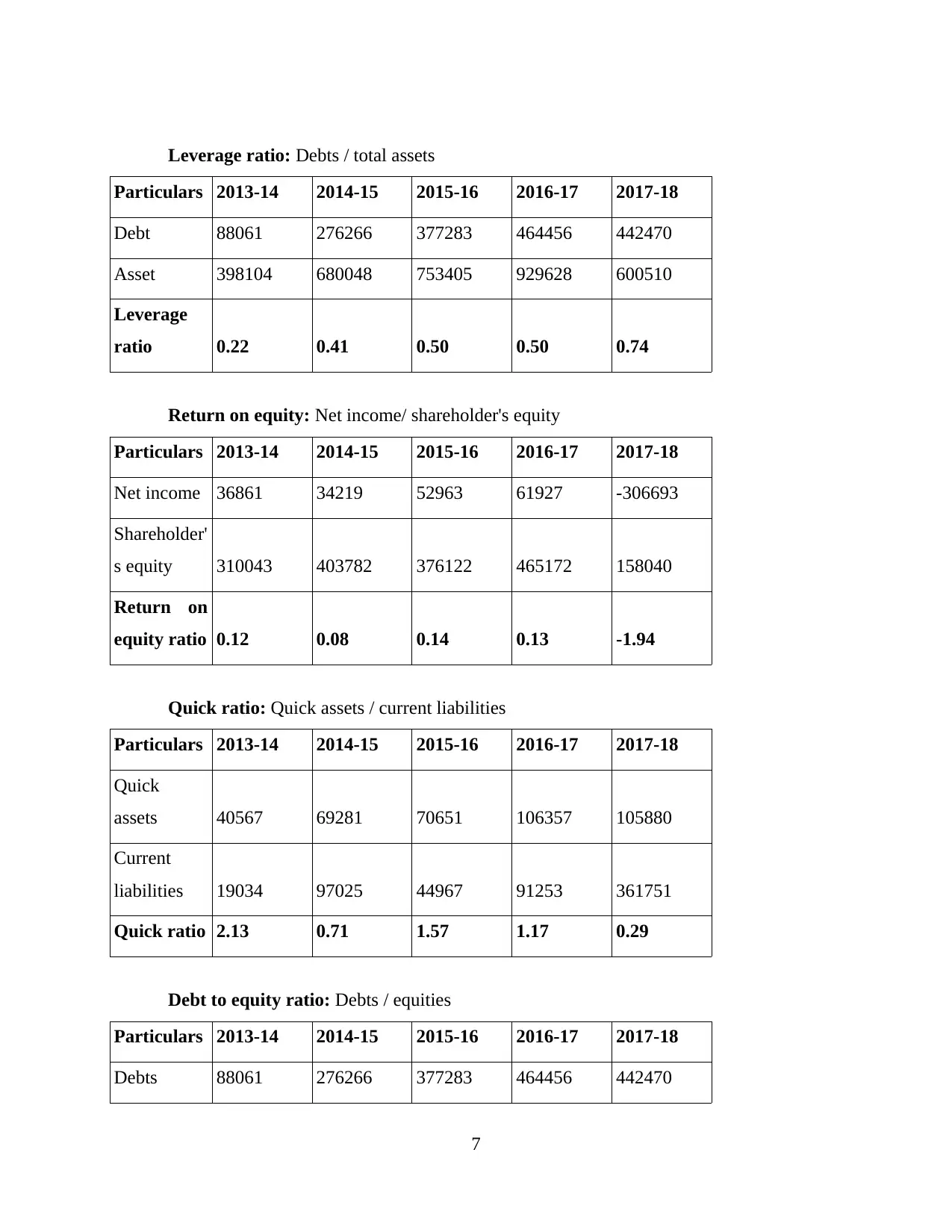

Leverage ratio: Debts / total assets

Particular

s 2013-14 2014-15 2015-16 2016-17 2017-18

4

dividend 24534 26427 28427 25771 30658

Weighted

average

outstanding

shares 83835 86266 87319 88656 87134

Earning

per share 0.29 0.31 0.33 0.29 0.35

Net profit margin: Net profit/ revenues *100

Particulars 2013-14 2014-15 2015-16 2016-17 2017-18

Net profit 45296 64048 82427 102857 121466

Revenues 588637 697813 923664 1064767 1143046

Net profit

margin 7.70 9.18 8.92 9.66 10.63

Asset turnover ratio: Revenues / total assets

Particular

s 2013-14 2014-15 2015-16 2016-17 2017-18

Revenues 588637 697813 923664 1064767 1143046

Total assets 559008 630600 1128033 1132793 1302411

Asset

turnover

ratio 1.05 1.11 0.82 0.94 0.88

Leverage ratio: Debts / total assets

Particular

s 2013-14 2014-15 2015-16 2016-17 2017-18

4

You're viewing a preview

Unlock full access by subscribing today!

Debt 299619 325544 733487 717729 994747

Asset 559008 630600 1128033 1132793 1302411

Leverage

ratio 0.54 0.52 0.65 0.63 0.76

Return on equity: Net income/ shareholder's equity

Particulars 2013-14 2014-15 2015-16 2016-17 2017-18

Net income 45296 64048 82427 102857 121466

Shareholder'

s equity 259389 305056 394546 415064 307664

Return on

equity 0.17 0.21 0.21 0.25 0.39

Quick ratio: Quick assets / current liabilities

Particulars 2013-14 2014-15 2015-16 2016-17 2017-18

Quick

assets 91437 103641 165862 165914 207545

Current

liabilities 112597 13131 266250 230146 201045

Quick ratio 0.81 7.89 0.62 0.72 1.03

Debt to equity ratio: Debts / equities

Particulars 2013-14 2014-15 2015-16 2016-17 2017-18

Debts 299619 325544 733487 717729 994747

Equities 259389 305056 394546 415064 307664

Debt to

equity ratio 1.16 1.07 1.86 1.73 3.23

5

Asset 559008 630600 1128033 1132793 1302411

Leverage

ratio 0.54 0.52 0.65 0.63 0.76

Return on equity: Net income/ shareholder's equity

Particulars 2013-14 2014-15 2015-16 2016-17 2017-18

Net income 45296 64048 82427 102857 121466

Shareholder'

s equity 259389 305056 394546 415064 307664

Return on

equity 0.17 0.21 0.21 0.25 0.39

Quick ratio: Quick assets / current liabilities

Particulars 2013-14 2014-15 2015-16 2016-17 2017-18

Quick

assets 91437 103641 165862 165914 207545

Current

liabilities 112597 13131 266250 230146 201045

Quick ratio 0.81 7.89 0.62 0.72 1.03

Debt to equity ratio: Debts / equities

Particulars 2013-14 2014-15 2015-16 2016-17 2017-18

Debts 299619 325544 733487 717729 994747

Equities 259389 305056 394546 415064 307664

Debt to

equity ratio 1.16 1.07 1.86 1.73 3.23

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

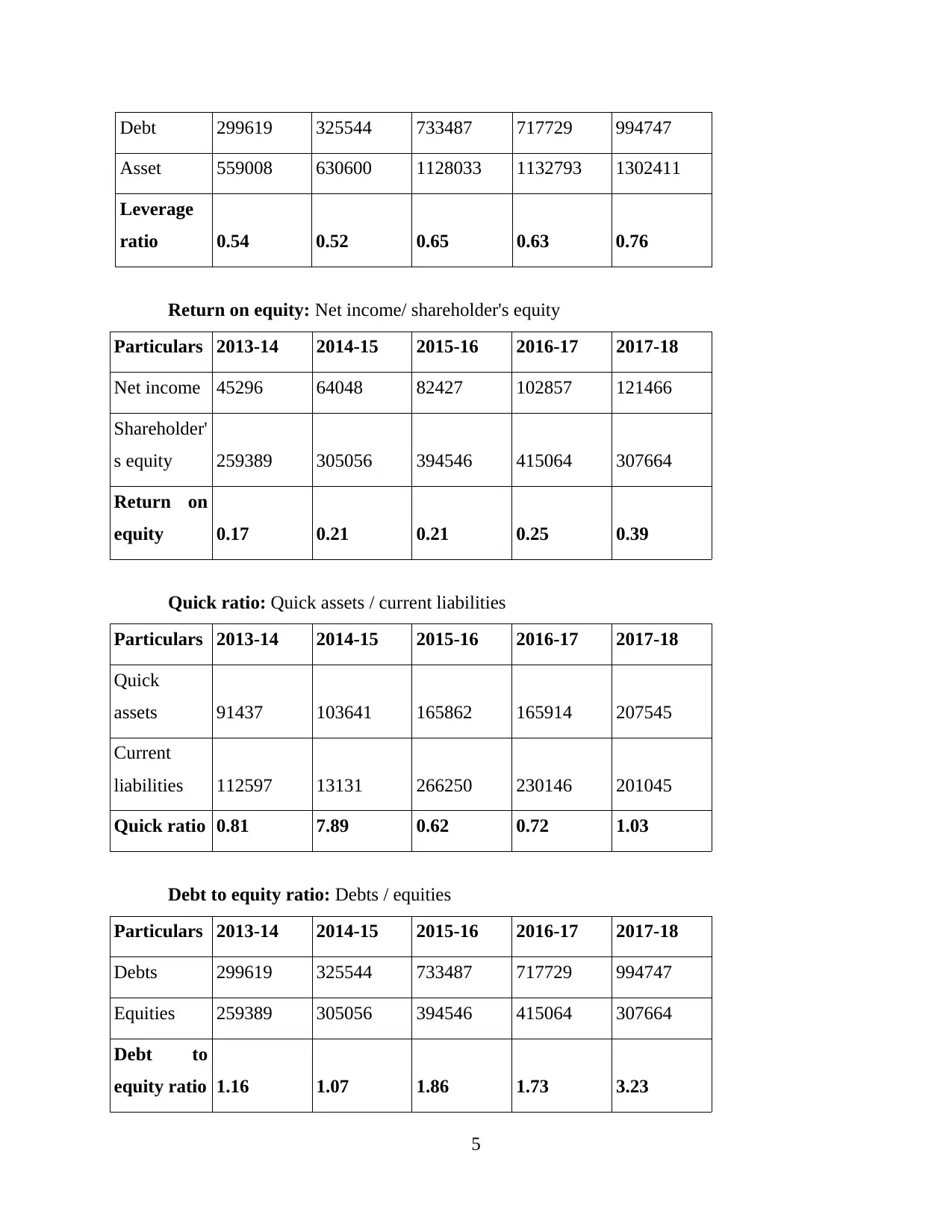

Ratios of Retail Food Group Limited:

Earning per share: Profit after dividend/ weighted average share outstanding

Particulars 2013-14 2014-15 2015-16 2016-17 2017-18

Profit after

dividend 11517 10097 21507 19039 -328673

Weighted

average

outstanding

shares 139185 154876 164099 173441 180951

Earning

per share 0.08 0.07 0.13 0.11 -1.82

Net profit margin: Net profit/ revenues *100

Particulars 2013-14 2014-15 2015-16 2016-17 2017-18

Net profit 36861 34219 52963 61927 -306693

Revenues 56247 120768 164840 245873 297719

Net profit

margin

ratio 65.53 28.33 32.13 25.19 -103.01

Asset turnover ratio: Revenues / total assets

Particulars 2013-14 2014-15 2015-16 2016-17 2017-18

Revenues 56247 120768 164840 245873 297719

Total assets 398104 680048 753405 929628 600510

Asset

turnover

ratio 0.14 0.18 0.22 0.26 0.50

6

Earning per share: Profit after dividend/ weighted average share outstanding

Particulars 2013-14 2014-15 2015-16 2016-17 2017-18

Profit after

dividend 11517 10097 21507 19039 -328673

Weighted

average

outstanding

shares 139185 154876 164099 173441 180951

Earning

per share 0.08 0.07 0.13 0.11 -1.82

Net profit margin: Net profit/ revenues *100

Particulars 2013-14 2014-15 2015-16 2016-17 2017-18

Net profit 36861 34219 52963 61927 -306693

Revenues 56247 120768 164840 245873 297719

Net profit

margin

ratio 65.53 28.33 32.13 25.19 -103.01

Asset turnover ratio: Revenues / total assets

Particulars 2013-14 2014-15 2015-16 2016-17 2017-18

Revenues 56247 120768 164840 245873 297719

Total assets 398104 680048 753405 929628 600510

Asset

turnover

ratio 0.14 0.18 0.22 0.26 0.50

6

Leverage ratio: Debts / total assets

Particulars 2013-14 2014-15 2015-16 2016-17 2017-18

Debt 88061 276266 377283 464456 442470

Asset 398104 680048 753405 929628 600510

Leverage

ratio 0.22 0.41 0.50 0.50 0.74

Return on equity: Net income/ shareholder's equity

Particulars 2013-14 2014-15 2015-16 2016-17 2017-18

Net income 36861 34219 52963 61927 -306693

Shareholder'

s equity 310043 403782 376122 465172 158040

Return on

equity ratio 0.12 0.08 0.14 0.13 -1.94

Quick ratio: Quick assets / current liabilities

Particulars 2013-14 2014-15 2015-16 2016-17 2017-18

Quick

assets 40567 69281 70651 106357 105880

Current

liabilities 19034 97025 44967 91253 361751

Quick ratio 2.13 0.71 1.57 1.17 0.29

Debt to equity ratio: Debts / equities

Particulars 2013-14 2014-15 2015-16 2016-17 2017-18

Debts 88061 276266 377283 464456 442470

7

Particulars 2013-14 2014-15 2015-16 2016-17 2017-18

Debt 88061 276266 377283 464456 442470

Asset 398104 680048 753405 929628 600510

Leverage

ratio 0.22 0.41 0.50 0.50 0.74

Return on equity: Net income/ shareholder's equity

Particulars 2013-14 2014-15 2015-16 2016-17 2017-18

Net income 36861 34219 52963 61927 -306693

Shareholder'

s equity 310043 403782 376122 465172 158040

Return on

equity ratio 0.12 0.08 0.14 0.13 -1.94

Quick ratio: Quick assets / current liabilities

Particulars 2013-14 2014-15 2015-16 2016-17 2017-18

Quick

assets 40567 69281 70651 106357 105880

Current

liabilities 19034 97025 44967 91253 361751

Quick ratio 2.13 0.71 1.57 1.17 0.29

Debt to equity ratio: Debts / equities

Particulars 2013-14 2014-15 2015-16 2016-17 2017-18

Debts 88061 276266 377283 464456 442470

7

You're viewing a preview

Unlock full access by subscribing today!

Equities 310043 403782 376122 465172 158040

Debt to

equity ratio 0.28 0.68 1.00 1.00 2.80

Question 6

Comparison and contrasting of performance of Dominos and Retail according to growth

in different ratios:

Profitability ratios: From the growth in EPS and net profit margin of Dominos it has

been analysed that profitability of the company good and and its is stable. In year 2014 growth

was 29% and in year 2017 it has decreased up to 24%. Net profit margin of the company has

increased in year 2017 up to 13% as compare to 10% which is related to 2014. Profitability of

Retail Food Group Limited is not good according to its growth in EPS and net profit margin

(Share price and final accounts of Retail Food Group Ltd., 2019). In 2014 the growth in EPS

was 2% which was decreased in 2015 up to -17% which has affected organisation's profits. In

2016 massive growth in being recorded in this ratio and in 2017 the growth was decreased. There

is huge fluctuation in the profits of the company. Due to this reason its profitability is very low.

Growth in net profit margin is also not stable and fluctuations in this ratio has resulted in bad

performance of company (Ashalatha, Agarkhed and Patil, 2016).

Efficiency ratio: Growth in asset turnover ratio of Dominos is very high but it is

continuously decreasing. On the other hand, growth in efficiency ratio of Retail Food Group is

increasing continuously since 2014 to 2017. If growth are compared with each other then it

shows that Dominos is having huge growth as compare to Retail Food Group which has resulted

in good performance of Dominos (Share price and final accounts of Dominos Pizza Enterprises

Ltd., 2019).

Liquidity ratio: Growth in quick ratio shows that company is having higher liquidity or

not. With the help of it investors can make decision regarding making investment in the

company. Growth in quick ratio of Dominos Pizza Enterprises Limited is very low as compare to

Retail Food group Limited. Growth of Dominos is 81%, 80%, 63% and 72% for year 2014 to

2017 respectively. On the other hand, growth of Retail Food Group Ltd. In quick ratio is 213%,

75%, 157% and 117%. for the period of 2014 to 2017. It affects performance of company

8

Debt to

equity ratio 0.28 0.68 1.00 1.00 2.80

Question 6

Comparison and contrasting of performance of Dominos and Retail according to growth

in different ratios:

Profitability ratios: From the growth in EPS and net profit margin of Dominos it has

been analysed that profitability of the company good and and its is stable. In year 2014 growth

was 29% and in year 2017 it has decreased up to 24%. Net profit margin of the company has

increased in year 2017 up to 13% as compare to 10% which is related to 2014. Profitability of

Retail Food Group Limited is not good according to its growth in EPS and net profit margin

(Share price and final accounts of Retail Food Group Ltd., 2019). In 2014 the growth in EPS

was 2% which was decreased in 2015 up to -17% which has affected organisation's profits. In

2016 massive growth in being recorded in this ratio and in 2017 the growth was decreased. There

is huge fluctuation in the profits of the company. Due to this reason its profitability is very low.

Growth in net profit margin is also not stable and fluctuations in this ratio has resulted in bad

performance of company (Ashalatha, Agarkhed and Patil, 2016).

Efficiency ratio: Growth in asset turnover ratio of Dominos is very high but it is

continuously decreasing. On the other hand, growth in efficiency ratio of Retail Food Group is

increasing continuously since 2014 to 2017. If growth are compared with each other then it

shows that Dominos is having huge growth as compare to Retail Food Group which has resulted

in good performance of Dominos (Share price and final accounts of Dominos Pizza Enterprises

Ltd., 2019).

Liquidity ratio: Growth in quick ratio shows that company is having higher liquidity or

not. With the help of it investors can make decision regarding making investment in the

company. Growth in quick ratio of Dominos Pizza Enterprises Limited is very low as compare to

Retail Food group Limited. Growth of Dominos is 81%, 80%, 63% and 72% for year 2014 to

2017 respectively. On the other hand, growth of Retail Food Group Ltd. In quick ratio is 213%,

75%, 157% and 117%. for the period of 2014 to 2017. It affects performance of company

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

because when an organisation is not having sufficient funds then it can result in inappropriate

business operations. Due to low liquidity performance of Dominos may get affected in future and

also result in losses for the company (Kruppe and Scholz, 2014).

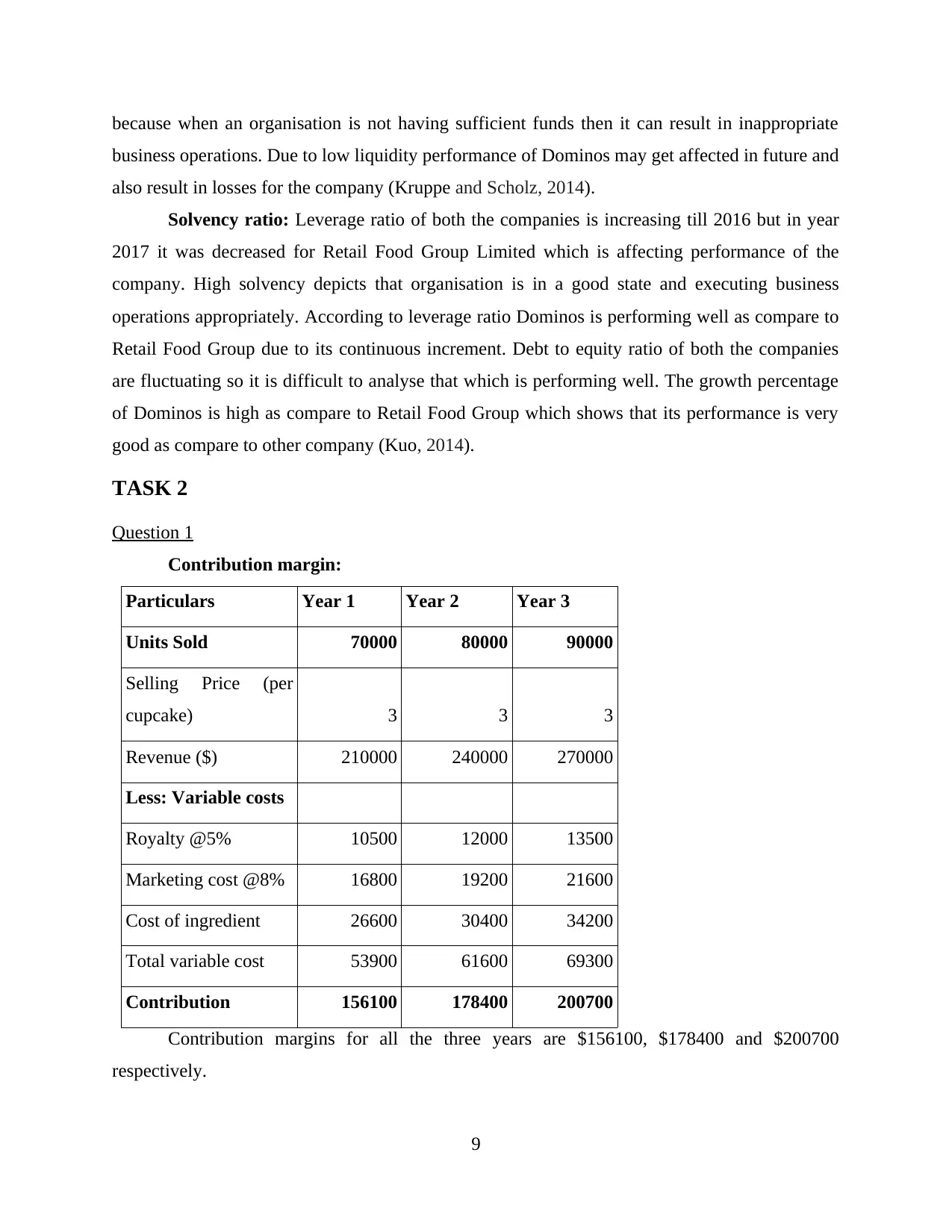

Solvency ratio: Leverage ratio of both the companies is increasing till 2016 but in year

2017 it was decreased for Retail Food Group Limited which is affecting performance of the

company. High solvency depicts that organisation is in a good state and executing business

operations appropriately. According to leverage ratio Dominos is performing well as compare to

Retail Food Group due to its continuous increment. Debt to equity ratio of both the companies

are fluctuating so it is difficult to analyse that which is performing well. The growth percentage

of Dominos is high as compare to Retail Food Group which shows that its performance is very

good as compare to other company (Kuo, 2014).

TASK 2

Question 1

Contribution margin:

Particulars Year 1 Year 2 Year 3

Units Sold 70000 80000 90000

Selling Price (per

cupcake) 3 3 3

Revenue ($) 210000 240000 270000

Less: Variable costs

Royalty @5% 10500 12000 13500

Marketing cost @8% 16800 19200 21600

Cost of ingredient 26600 30400 34200

Total variable cost 53900 61600 69300

Contribution 156100 178400 200700

Contribution margins for all the three years are $156100, $178400 and $200700

respectively.

9

business operations. Due to low liquidity performance of Dominos may get affected in future and

also result in losses for the company (Kruppe and Scholz, 2014).

Solvency ratio: Leverage ratio of both the companies is increasing till 2016 but in year

2017 it was decreased for Retail Food Group Limited which is affecting performance of the

company. High solvency depicts that organisation is in a good state and executing business

operations appropriately. According to leverage ratio Dominos is performing well as compare to

Retail Food Group due to its continuous increment. Debt to equity ratio of both the companies

are fluctuating so it is difficult to analyse that which is performing well. The growth percentage

of Dominos is high as compare to Retail Food Group which shows that its performance is very

good as compare to other company (Kuo, 2014).

TASK 2

Question 1

Contribution margin:

Particulars Year 1 Year 2 Year 3

Units Sold 70000 80000 90000

Selling Price (per

cupcake) 3 3 3

Revenue ($) 210000 240000 270000

Less: Variable costs

Royalty @5% 10500 12000 13500

Marketing cost @8% 16800 19200 21600

Cost of ingredient 26600 30400 34200

Total variable cost 53900 61600 69300

Contribution 156100 178400 200700

Contribution margins for all the three years are $156100, $178400 and $200700

respectively.

9

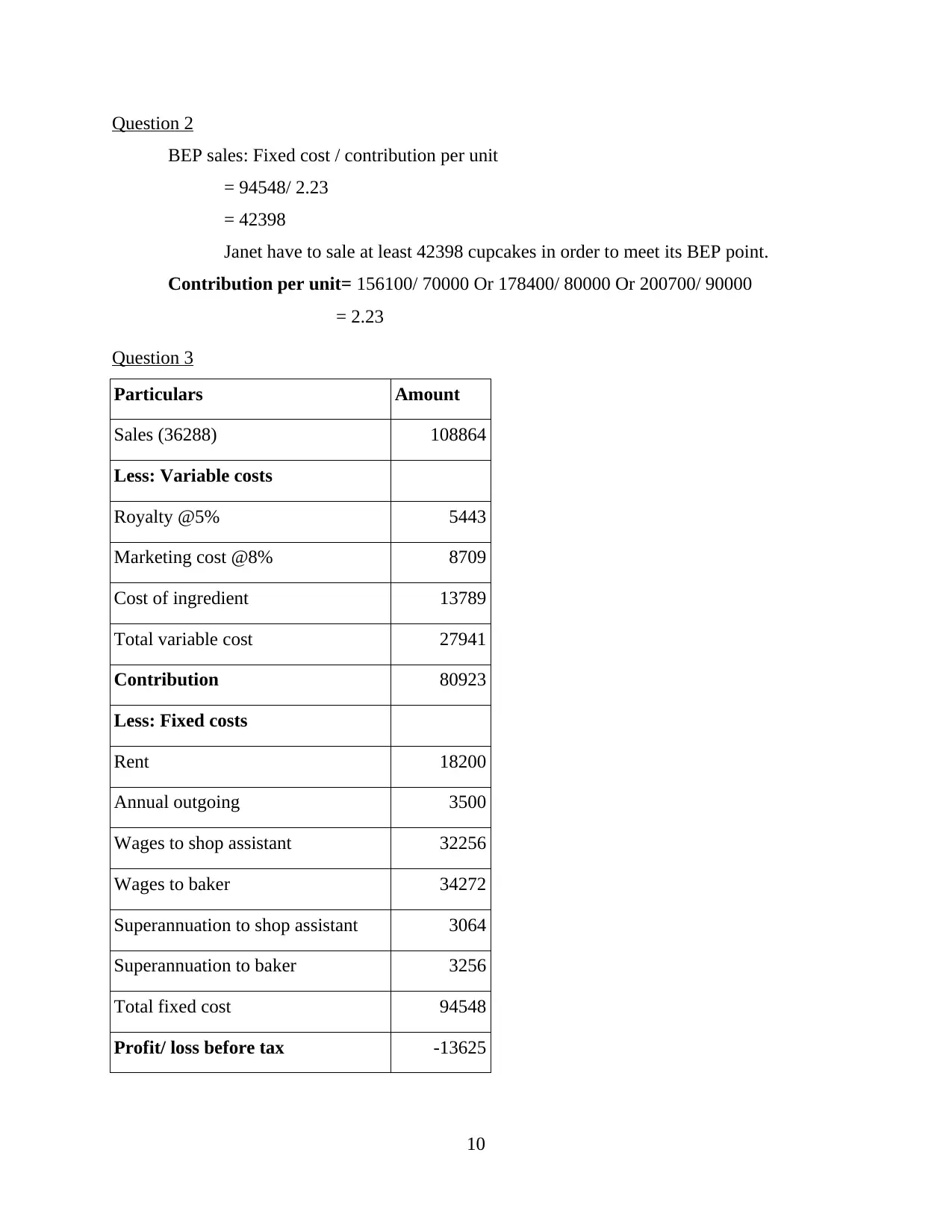

Question 2

BEP sales: Fixed cost / contribution per unit

= 94548/ 2.23

= 42398

Janet have to sale at least 42398 cupcakes in order to meet its BEP point.

Contribution per unit= 156100/ 70000 Or 178400/ 80000 Or 200700/ 90000

= 2.23

Question 3

Particulars Amount

Sales (36288) 108864

Less: Variable costs

Royalty @5% 5443

Marketing cost @8% 8709

Cost of ingredient 13789

Total variable cost 27941

Contribution 80923

Less: Fixed costs

Rent 18200

Annual outgoing 3500

Wages to shop assistant 32256

Wages to baker 34272

Superannuation to shop assistant 3064

Superannuation to baker 3256

Total fixed cost 94548

Profit/ loss before tax -13625

10

BEP sales: Fixed cost / contribution per unit

= 94548/ 2.23

= 42398

Janet have to sale at least 42398 cupcakes in order to meet its BEP point.

Contribution per unit= 156100/ 70000 Or 178400/ 80000 Or 200700/ 90000

= 2.23

Question 3

Particulars Amount

Sales (36288) 108864

Less: Variable costs

Royalty @5% 5443

Marketing cost @8% 8709

Cost of ingredient 13789

Total variable cost 27941

Contribution 80923

Less: Fixed costs

Rent 18200

Annual outgoing 3500

Wages to shop assistant 32256

Wages to baker 34272

Superannuation to shop assistant 3064

Superannuation to baker 3256

Total fixed cost 94548

Profit/ loss before tax -13625

10

You're viewing a preview

Unlock full access by subscribing today!

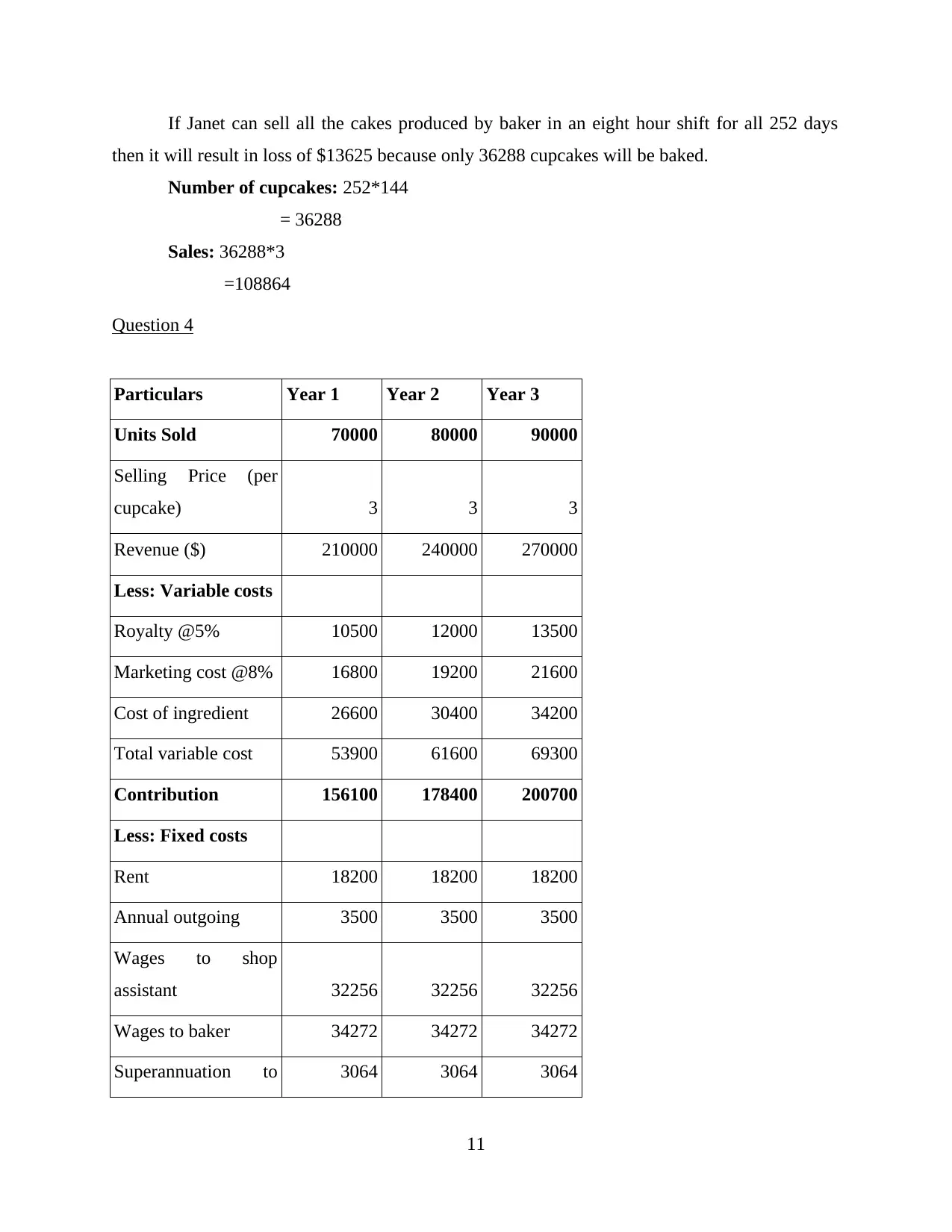

If Janet can sell all the cakes produced by baker in an eight hour shift for all 252 days

then it will result in loss of $13625 because only 36288 cupcakes will be baked.

Number of cupcakes: 252*144

= 36288

Sales: 36288*3

=108864

Question 4

Particulars Year 1 Year 2 Year 3

Units Sold 70000 80000 90000

Selling Price (per

cupcake) 3 3 3

Revenue ($) 210000 240000 270000

Less: Variable costs

Royalty @5% 10500 12000 13500

Marketing cost @8% 16800 19200 21600

Cost of ingredient 26600 30400 34200

Total variable cost 53900 61600 69300

Contribution 156100 178400 200700

Less: Fixed costs

Rent 18200 18200 18200

Annual outgoing 3500 3500 3500

Wages to shop

assistant 32256 32256 32256

Wages to baker 34272 34272 34272

Superannuation to 3064 3064 3064

11

then it will result in loss of $13625 because only 36288 cupcakes will be baked.

Number of cupcakes: 252*144

= 36288

Sales: 36288*3

=108864

Question 4

Particulars Year 1 Year 2 Year 3

Units Sold 70000 80000 90000

Selling Price (per

cupcake) 3 3 3

Revenue ($) 210000 240000 270000

Less: Variable costs

Royalty @5% 10500 12000 13500

Marketing cost @8% 16800 19200 21600

Cost of ingredient 26600 30400 34200

Total variable cost 53900 61600 69300

Contribution 156100 178400 200700

Less: Fixed costs

Rent 18200 18200 18200

Annual outgoing 3500 3500 3500

Wages to shop

assistant 32256 32256 32256

Wages to baker 34272 34272 34272

Superannuation to 3064 3064 3064

11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

shop assistant

Superannuation to

baker 3256 3256 3256

Total fixed cost 94548 94548 94548

Profit before tax 61552 83852 106152

Less: tax @ 30% 18466 25156 31846

Profit after tax/ Net

profit 43086 58696 74306

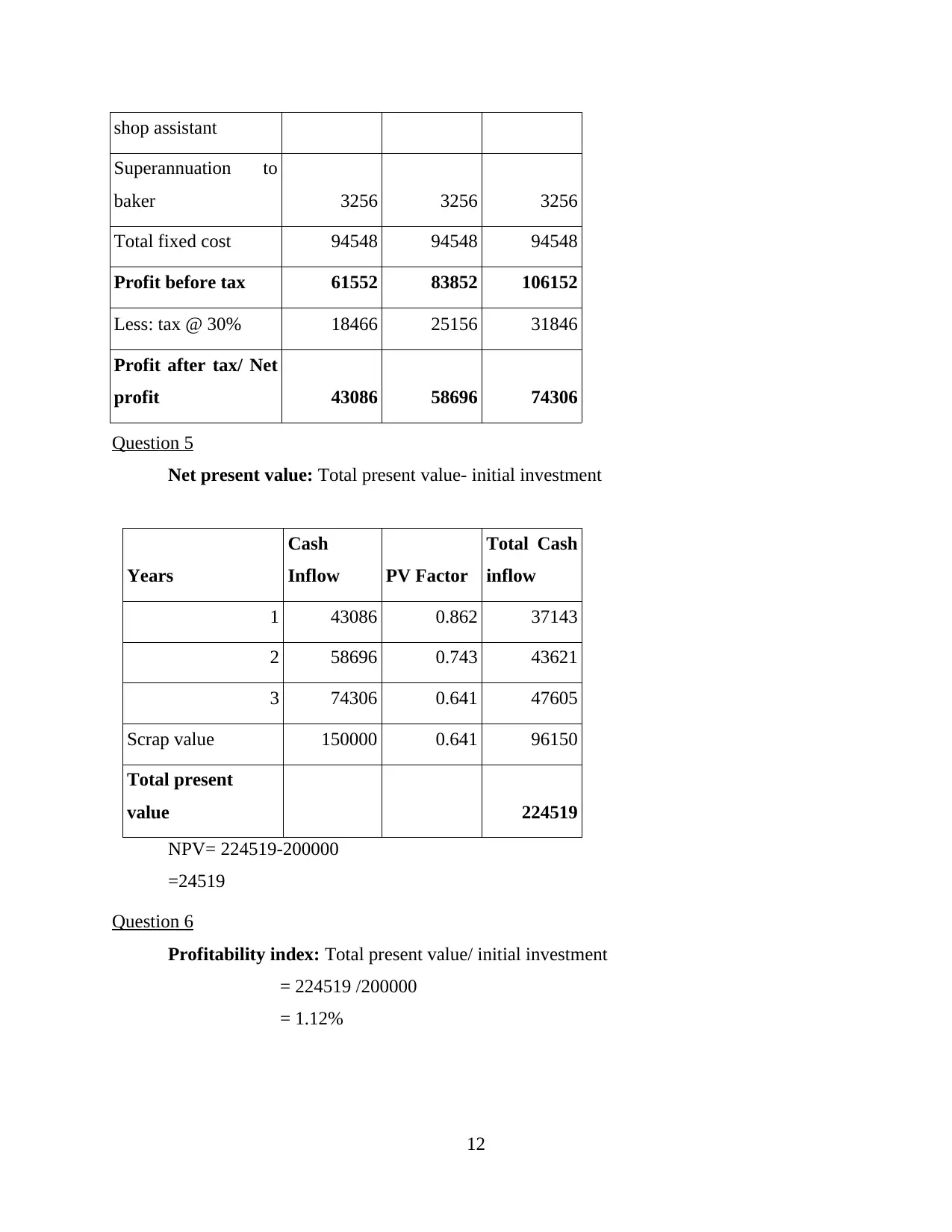

Question 5

Net present value: Total present value- initial investment

Years

Cash

Inflow PV Factor

Total Cash

inflow

1 43086 0.862 37143

2 58696 0.743 43621

3 74306 0.641 47605

Scrap value 150000 0.641 96150

Total present

value 224519

NPV= 224519-200000

=24519

Question 6

Profitability index: Total present value/ initial investment

= 224519 /200000

= 1.12%

12

Superannuation to

baker 3256 3256 3256

Total fixed cost 94548 94548 94548

Profit before tax 61552 83852 106152

Less: tax @ 30% 18466 25156 31846

Profit after tax/ Net

profit 43086 58696 74306

Question 5

Net present value: Total present value- initial investment

Years

Cash

Inflow PV Factor

Total Cash

inflow

1 43086 0.862 37143

2 58696 0.743 43621

3 74306 0.641 47605

Scrap value 150000 0.641 96150

Total present

value 224519

NPV= 224519-200000

=24519

Question 6

Profitability index: Total present value/ initial investment

= 224519 /200000

= 1.12%

12

Question 7

From the net present value of the investment it has been analysed that the investment

which is being made by Janet is financially viable because when it will be sold by Janet then it

will result in profit of $24519. It has been recommended to Janet to make investment in this

project as it can help to attain profits in future (Schröder, Falk and Schmitt, 2015).

Question 8

There are various types of risks may take place while establishing a cup cake business.

All the risks which may affect business of Janet are as follows:

In cup cake business there is no exclusivity because it is not possible to patent a cup cake.

There are end number of competitors in this market because very low amount of

investment is required to enter (YU, YU and LAN, 2017).

Anyone can make cupcakes in order to attract customers creativity and innovation is

required.

Price of cup cakes is very high and it is not possible for all the customers to buy them.

Taste of customers changes with time which affects their buying behaviour against things

such as cup cakes.

In order to deal with all the above described challenges Janet can use following ways to

modify the business plan and reduce possibility of such types of risks:

Janet can use innovative techniques to bake cup cakes which can help to attract large

number of customers. For example, cup cakes which are carrying low calories could be

produced by Janet which will result in large number of clients because now a days people

are becoming health conscious.

As the market is saturated and pricing of the cupcakes is very high Janet can set prices to

the cup cakes according to market segment. Different types of cup cakes could be baked

for all type of customers whether they are from middle or upper class. It will help to

reach large number of clients and fulfil their needs (Sen and Sen, 2014).

Keeping detailed information regarding latest trends in baking could also help to deal

with above described risks because when cup cakes will be baked according to customer's

requirements then it can help to generate higher profits.

13

From the net present value of the investment it has been analysed that the investment

which is being made by Janet is financially viable because when it will be sold by Janet then it

will result in profit of $24519. It has been recommended to Janet to make investment in this

project as it can help to attain profits in future (Schröder, Falk and Schmitt, 2015).

Question 8

There are various types of risks may take place while establishing a cup cake business.

All the risks which may affect business of Janet are as follows:

In cup cake business there is no exclusivity because it is not possible to patent a cup cake.

There are end number of competitors in this market because very low amount of

investment is required to enter (YU, YU and LAN, 2017).

Anyone can make cupcakes in order to attract customers creativity and innovation is

required.

Price of cup cakes is very high and it is not possible for all the customers to buy them.

Taste of customers changes with time which affects their buying behaviour against things

such as cup cakes.

In order to deal with all the above described challenges Janet can use following ways to

modify the business plan and reduce possibility of such types of risks:

Janet can use innovative techniques to bake cup cakes which can help to attract large

number of customers. For example, cup cakes which are carrying low calories could be

produced by Janet which will result in large number of clients because now a days people

are becoming health conscious.

As the market is saturated and pricing of the cupcakes is very high Janet can set prices to

the cup cakes according to market segment. Different types of cup cakes could be baked

for all type of customers whether they are from middle or upper class. It will help to

reach large number of clients and fulfil their needs (Sen and Sen, 2014).

Keeping detailed information regarding latest trends in baking could also help to deal

with above described risks because when cup cakes will be baked according to customer's

requirements then it can help to generate higher profits.

13

You're viewing a preview

Unlock full access by subscribing today!

1 out of 15

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.