ACC00716 S1 2019: DuoLever Limited Financial Case Study Report

VerifiedAdded on 2023/03/17

|8

|1456

|86

Report

AI Summary

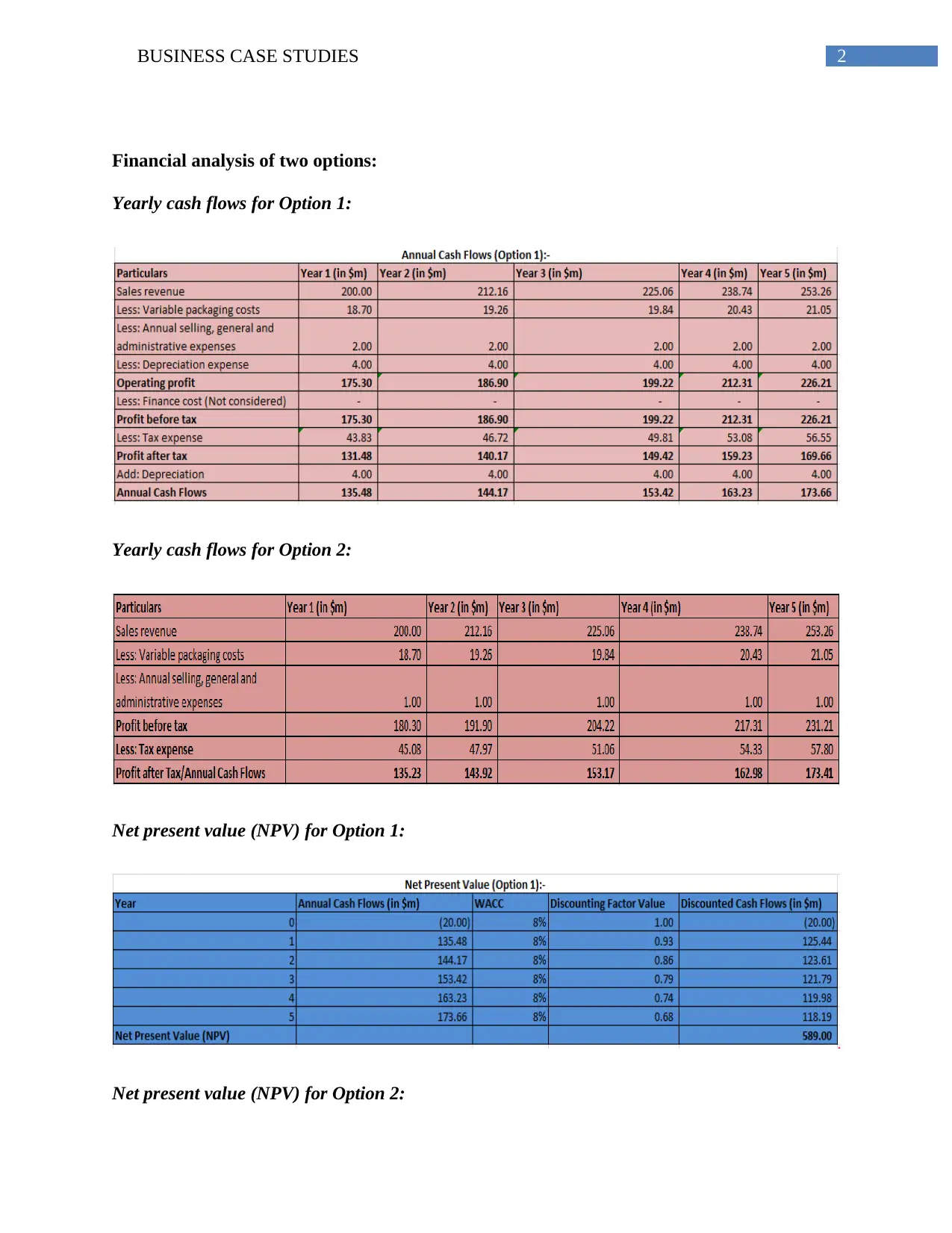

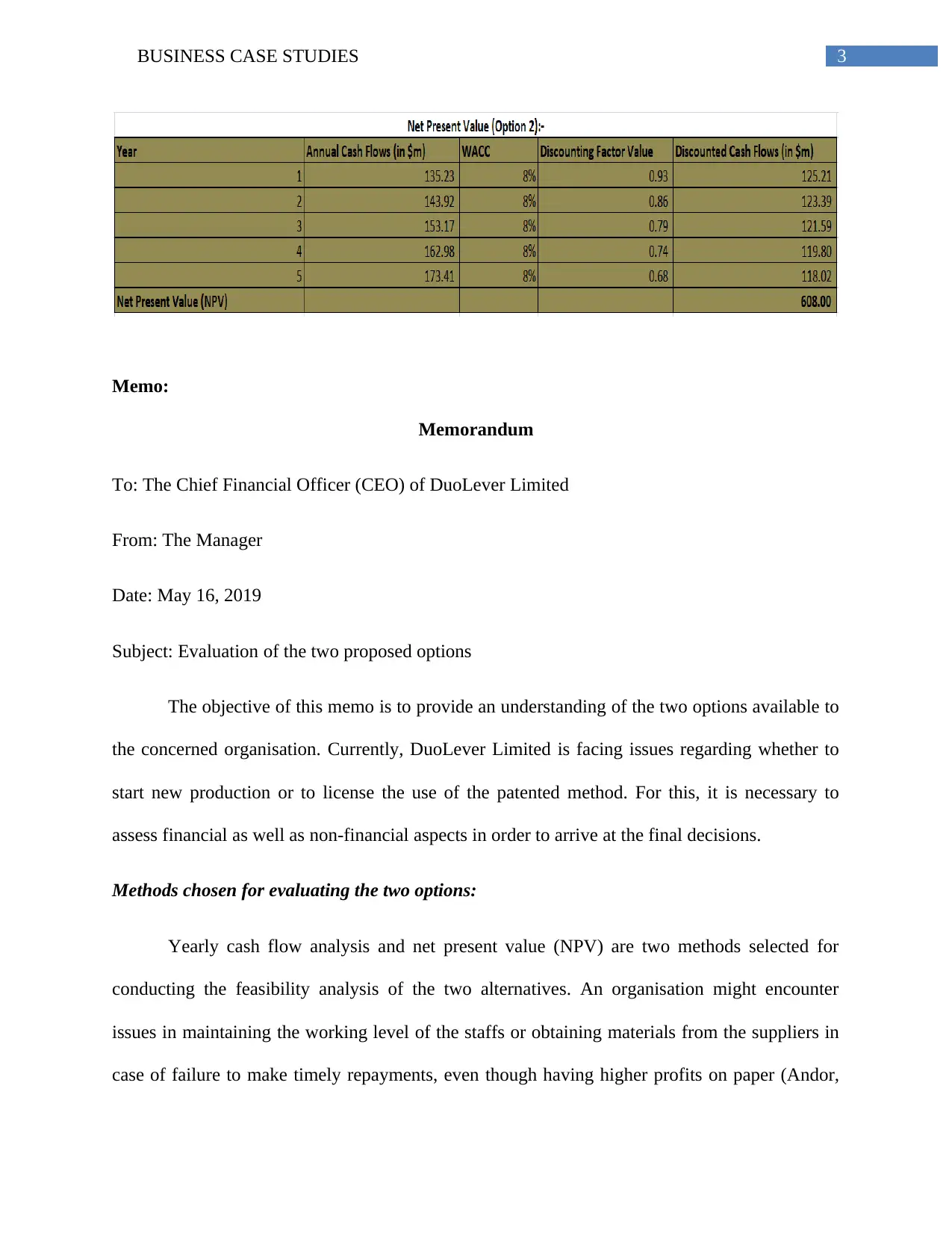

This report presents a financial analysis of two investment options for DuoLever Limited, a company in the personal care industry. The analysis evaluates the feasibility of starting new production versus licensing a patented method, considering both financial and non-financial aspects. The methods used include yearly cash flow analysis and net present value (NPV) calculations. The report includes a memo to the Chief Financial Officer summarizing the findings, which favor licensing the patented method due to higher cash flows and a greater NPV. The analysis considers assumptions about sales revenue, costs, depreciation, and tax rates. It also suggests follow-up measures to mitigate risks associated with the chosen option. The report provides detailed yearly cash flow and NPV calculations, supporting the recommendation for DuoLever Limited to choose the second option for increased profit margin.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.