Business Decision-Making Report: Project Analysis and Recommendations

VerifiedAdded on 2022/11/29

|8

|1519

|188

Report

AI Summary

This report focuses on business decision-making, particularly for DDK plc, a garment manufacturer. It analyzes two project choices using capital budgeting techniques like payback period and net present value (NPV). The report calculates the payback period for both projects, finding Project B has a s...

Business decision

Making

Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction-...............................................................................................................................................3

Calculation of Payback Period-....................................................................................................................3

Calculation of Net Present Value-................................................................................................................4

Financial and Non-financial Factors-............................................................................................................6

Financial Factors-.....................................................................................................................................6

Non-financial Factors-..............................................................................................................................7

Conclusion-..................................................................................................................................................7

REFERENCES............................................................................................................................................9

Introduction-...............................................................................................................................................3

Calculation of Payback Period-....................................................................................................................3

Calculation of Net Present Value-................................................................................................................4

Financial and Non-financial Factors-............................................................................................................6

Financial Factors-.....................................................................................................................................6

Non-financial Factors-..............................................................................................................................7

Conclusion-..................................................................................................................................................7

REFERENCES............................................................................................................................................9

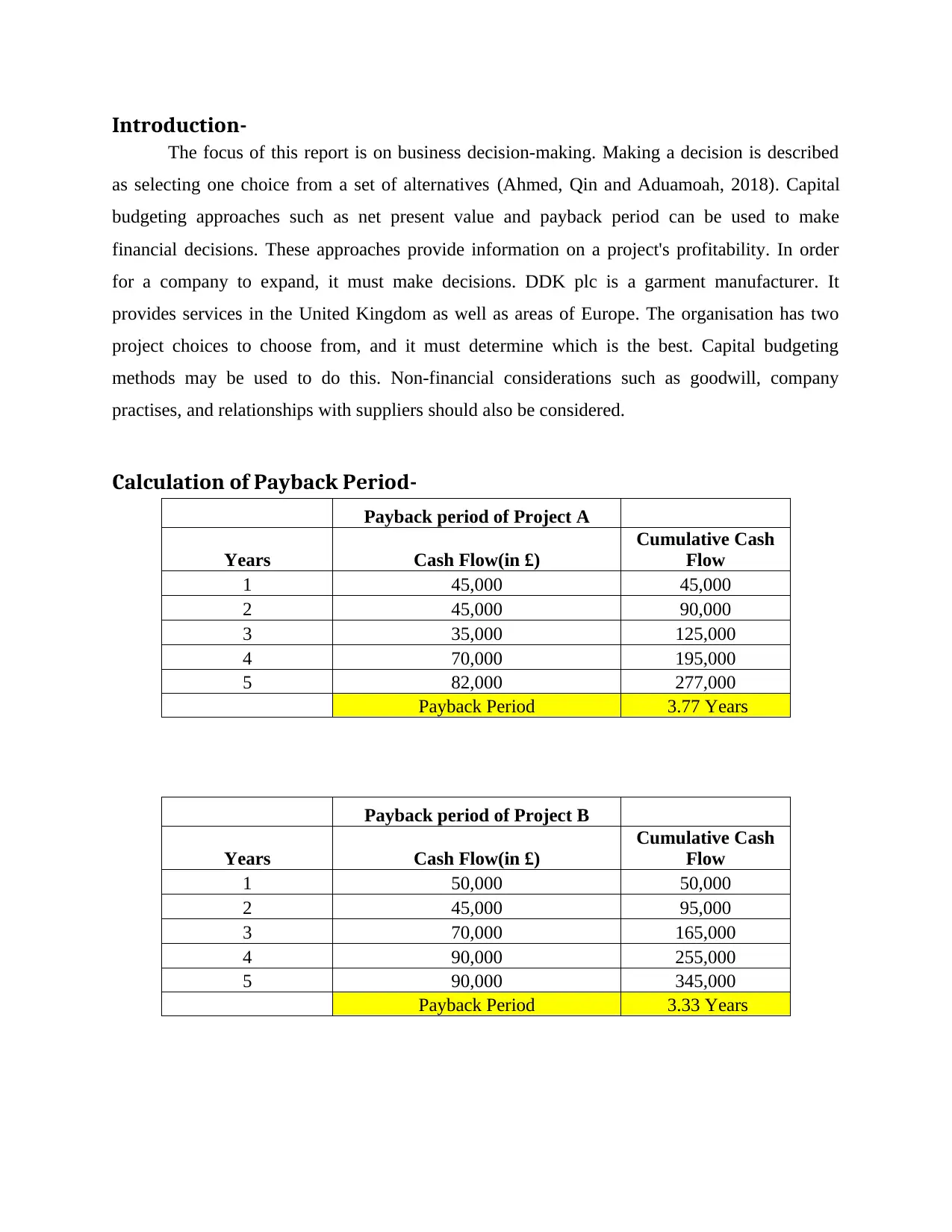

Introduction-

The focus of this report is on business decision-making. Making a decision is described

as selecting one choice from a set of alternatives (Ahmed, Qin and Aduamoah, 2018). Capital

budgeting approaches such as net present value and payback period can be used to make

financial decisions. These approaches provide information on a project's profitability. In order

for a company to expand, it must make decisions. DDK plc is a garment manufacturer. It

provides services in the United Kingdom as well as areas of Europe. The organisation has two

project choices to choose from, and it must determine which is the best. Capital budgeting

methods may be used to do this. Non-financial considerations such as goodwill, company

practises, and relationships with suppliers should also be considered.

Calculation of Payback Period-

Payback period of Project A

Years Cash Flow(in £)

Cumulative Cash

Flow

1 45,000 45,000

2 45,000 90,000

3 35,000 125,000

4 70,000 195,000

5 82,000 277,000

Payback Period 3.77 Years

Payback period of Project B

Years Cash Flow(in £)

Cumulative Cash

Flow

1 50,000 50,000

2 45,000 95,000

3 70,000 165,000

4 90,000 255,000

5 90,000 345,000

Payback Period 3.33 Years

The focus of this report is on business decision-making. Making a decision is described

as selecting one choice from a set of alternatives (Ahmed, Qin and Aduamoah, 2018). Capital

budgeting approaches such as net present value and payback period can be used to make

financial decisions. These approaches provide information on a project's profitability. In order

for a company to expand, it must make decisions. DDK plc is a garment manufacturer. It

provides services in the United Kingdom as well as areas of Europe. The organisation has two

project choices to choose from, and it must determine which is the best. Capital budgeting

methods may be used to do this. Non-financial considerations such as goodwill, company

practises, and relationships with suppliers should also be considered.

Calculation of Payback Period-

Payback period of Project A

Years Cash Flow(in £)

Cumulative Cash

Flow

1 45,000 45,000

2 45,000 90,000

3 35,000 125,000

4 70,000 195,000

5 82,000 277,000

Payback Period 3.77 Years

Payback period of Project B

Years Cash Flow(in £)

Cumulative Cash

Flow

1 50,000 50,000

2 45,000 95,000

3 70,000 165,000

4 90,000 255,000

5 90,000 345,000

Payback Period 3.33 Years

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

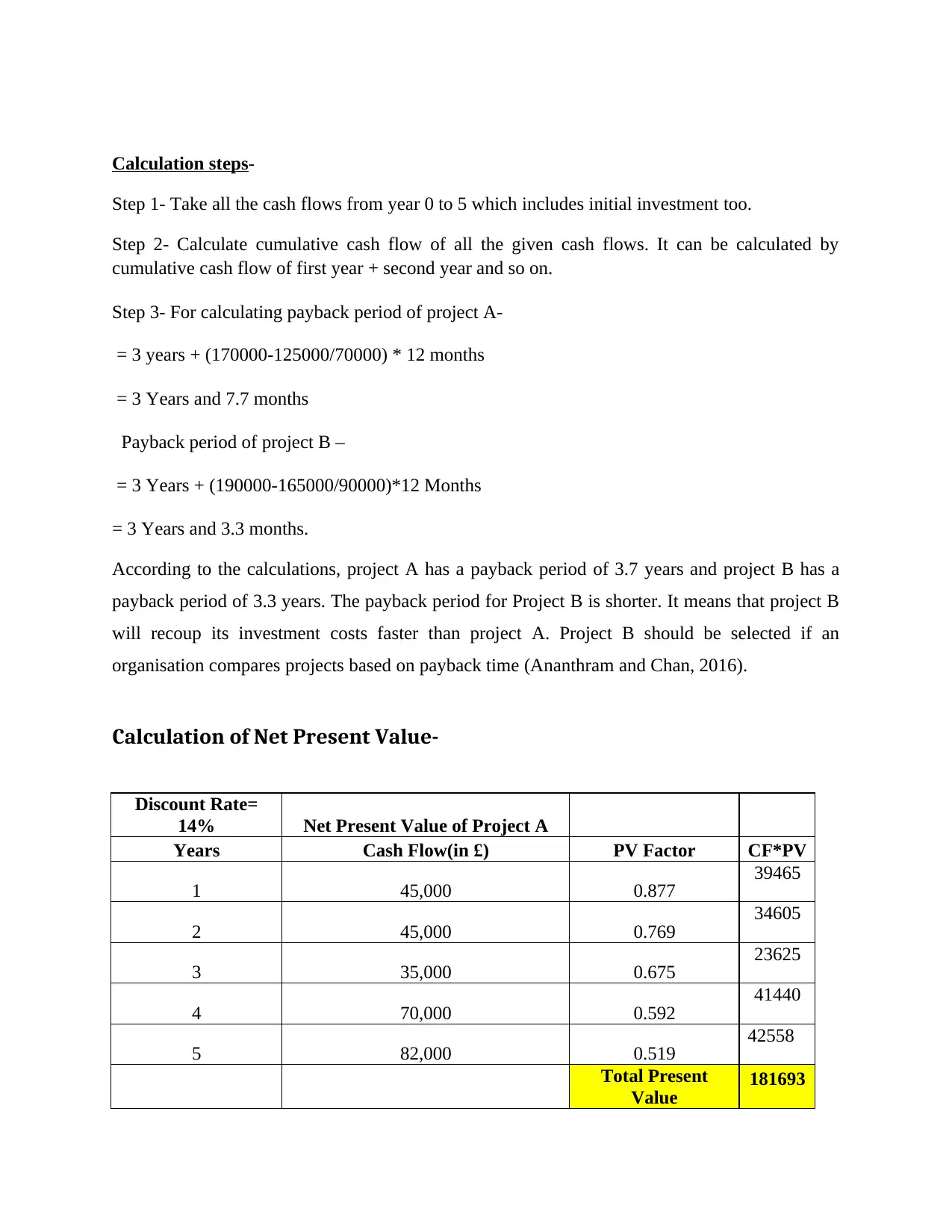

Calculation steps-

Step 1- Take all the cash flows from year 0 to 5 which includes initial investment too.

Step 2- Calculate cumulative cash flow of all the given cash flows. It can be calculated by

cumulative cash flow of first year + second year and so on.

Step 3- For calculating payback period of project A-

= 3 years + (170000-125000/70000) * 12 months

= 3 Years and 7.7 months

Payback period of project B –

= 3 Years + (190000-165000/90000)*12 Months

= 3 Years and 3.3 months.

According to the calculations, project A has a payback period of 3.7 years and project B has a

payback period of 3.3 years. The payback period for Project B is shorter. It means that project B

will recoup its investment costs faster than project A. Project B should be selected if an

organisation compares projects based on payback time (Ananthram and Chan, 2016).

Calculation of Net Present Value-

Discount Rate=

14% Net Present Value of Project A

Years Cash Flow(in £) PV Factor CF*PV

1 45,000 0.877 39465

2 45,000 0.769 34605

3 35,000 0.675 23625

4 70,000 0.592 41440

5 82,000 0.519 42558

Total Present

Value 181693

Step 1- Take all the cash flows from year 0 to 5 which includes initial investment too.

Step 2- Calculate cumulative cash flow of all the given cash flows. It can be calculated by

cumulative cash flow of first year + second year and so on.

Step 3- For calculating payback period of project A-

= 3 years + (170000-125000/70000) * 12 months

= 3 Years and 7.7 months

Payback period of project B –

= 3 Years + (190000-165000/90000)*12 Months

= 3 Years and 3.3 months.

According to the calculations, project A has a payback period of 3.7 years and project B has a

payback period of 3.3 years. The payback period for Project B is shorter. It means that project B

will recoup its investment costs faster than project A. Project B should be selected if an

organisation compares projects based on payback time (Ananthram and Chan, 2016).

Calculation of Net Present Value-

Discount Rate=

14% Net Present Value of Project A

Years Cash Flow(in £) PV Factor CF*PV

1 45,000 0.877 39465

2 45,000 0.769 34605

3 35,000 0.675 23625

4 70,000 0.592 41440

5 82,000 0.519 42558

Total Present

Value 181693

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

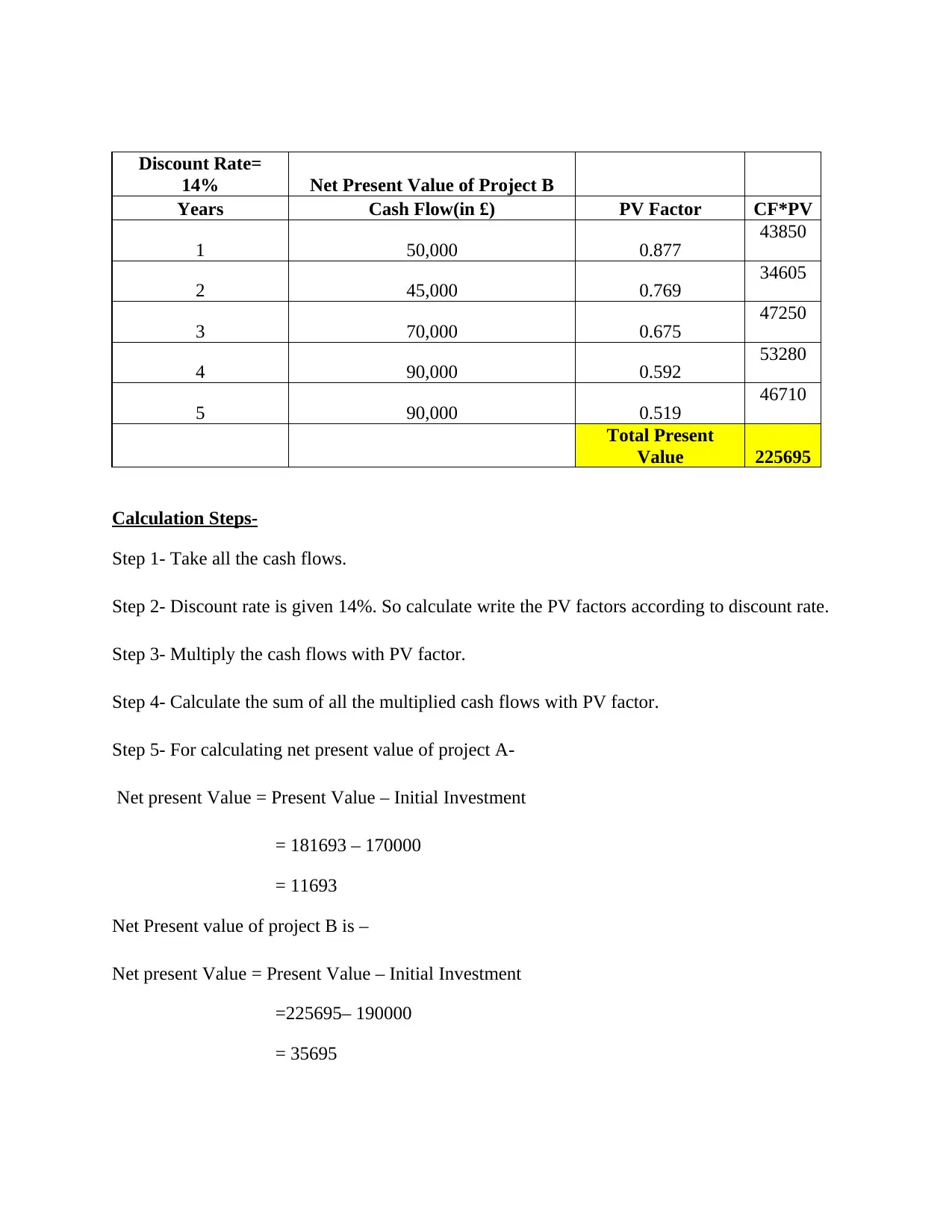

Discount Rate=

14% Net Present Value of Project B

Years Cash Flow(in £) PV Factor CF*PV

1 50,000 0.877 43850

2 45,000 0.769 34605

3 70,000 0.675 47250

4 90,000 0.592 53280

5 90,000 0.519 46710

Total Present

Value 225695

Calculation Steps-

Step 1- Take all the cash flows.

Step 2- Discount rate is given 14%. So calculate write the PV factors according to discount rate.

Step 3- Multiply the cash flows with PV factor.

Step 4- Calculate the sum of all the multiplied cash flows with PV factor.

Step 5- For calculating net present value of project A-

Net present Value = Present Value – Initial Investment

= 181693 – 170000

= 11693

Net Present value of project B is –

Net present Value = Present Value – Initial Investment

=225695– 190000

= 35695

14% Net Present Value of Project B

Years Cash Flow(in £) PV Factor CF*PV

1 50,000 0.877 43850

2 45,000 0.769 34605

3 70,000 0.675 47250

4 90,000 0.592 53280

5 90,000 0.519 46710

Total Present

Value 225695

Calculation Steps-

Step 1- Take all the cash flows.

Step 2- Discount rate is given 14%. So calculate write the PV factors according to discount rate.

Step 3- Multiply the cash flows with PV factor.

Step 4- Calculate the sum of all the multiplied cash flows with PV factor.

Step 5- For calculating net present value of project A-

Net present Value = Present Value – Initial Investment

= 181693 – 170000

= 11693

Net Present value of project B is –

Net present Value = Present Value – Initial Investment

=225695– 190000

= 35695

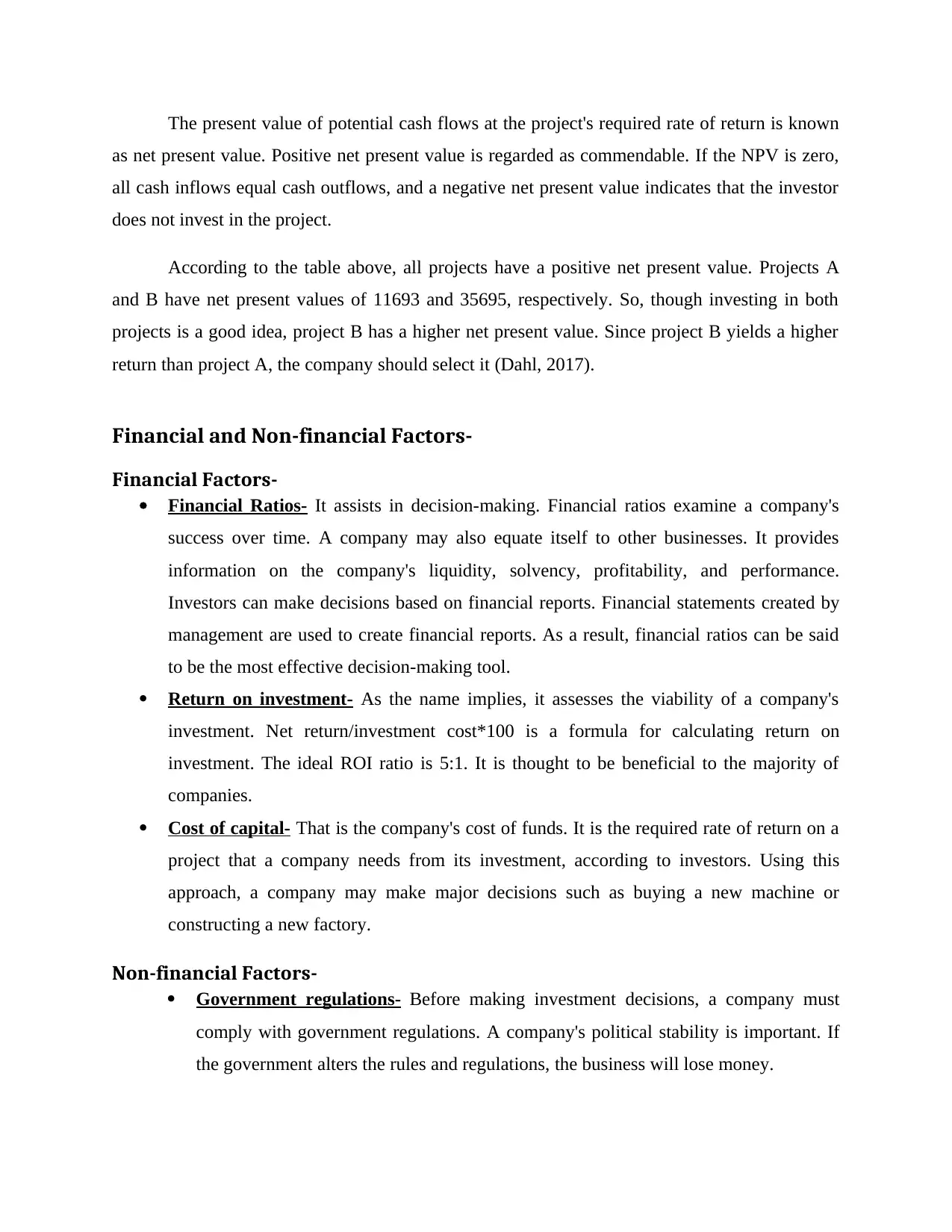

The present value of potential cash flows at the project's required rate of return is known

as net present value. Positive net present value is regarded as commendable. If the NPV is zero,

all cash inflows equal cash outflows, and a negative net present value indicates that the investor

does not invest in the project.

According to the table above, all projects have a positive net present value. Projects A

and B have net present values of 11693 and 35695, respectively. So, though investing in both

projects is a good idea, project B has a higher net present value. Since project B yields a higher

return than project A, the company should select it (Dahl, 2017).

Financial and Non-financial Factors-

Financial Factors-

Financial Ratios- It assists in decision-making. Financial ratios examine a company's

success over time. A company may also equate itself to other businesses. It provides

information on the company's liquidity, solvency, profitability, and performance.

Investors can make decisions based on financial reports. Financial statements created by

management are used to create financial reports. As a result, financial ratios can be said

to be the most effective decision-making tool.

Return on investment- As the name implies, it assesses the viability of a company's

investment. Net return/investment cost*100 is a formula for calculating return on

investment. The ideal ROI ratio is 5:1. It is thought to be beneficial to the majority of

companies.

Cost of capital- That is the company's cost of funds. It is the required rate of return on a

project that a company needs from its investment, according to investors. Using this

approach, a company may make major decisions such as buying a new machine or

constructing a new factory.

Non-financial Factors-

Government regulations- Before making investment decisions, a company must

comply with government regulations. A company's political stability is important. If

the government alters the rules and regulations, the business will lose money.

as net present value. Positive net present value is regarded as commendable. If the NPV is zero,

all cash inflows equal cash outflows, and a negative net present value indicates that the investor

does not invest in the project.

According to the table above, all projects have a positive net present value. Projects A

and B have net present values of 11693 and 35695, respectively. So, though investing in both

projects is a good idea, project B has a higher net present value. Since project B yields a higher

return than project A, the company should select it (Dahl, 2017).

Financial and Non-financial Factors-

Financial Factors-

Financial Ratios- It assists in decision-making. Financial ratios examine a company's

success over time. A company may also equate itself to other businesses. It provides

information on the company's liquidity, solvency, profitability, and performance.

Investors can make decisions based on financial reports. Financial statements created by

management are used to create financial reports. As a result, financial ratios can be said

to be the most effective decision-making tool.

Return on investment- As the name implies, it assesses the viability of a company's

investment. Net return/investment cost*100 is a formula for calculating return on

investment. The ideal ROI ratio is 5:1. It is thought to be beneficial to the majority of

companies.

Cost of capital- That is the company's cost of funds. It is the required rate of return on a

project that a company needs from its investment, according to investors. Using this

approach, a company may make major decisions such as buying a new machine or

constructing a new factory.

Non-financial Factors-

Government regulations- Before making investment decisions, a company must

comply with government regulations. A company's political stability is important. If

the government alters the rules and regulations, the business will lose money.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

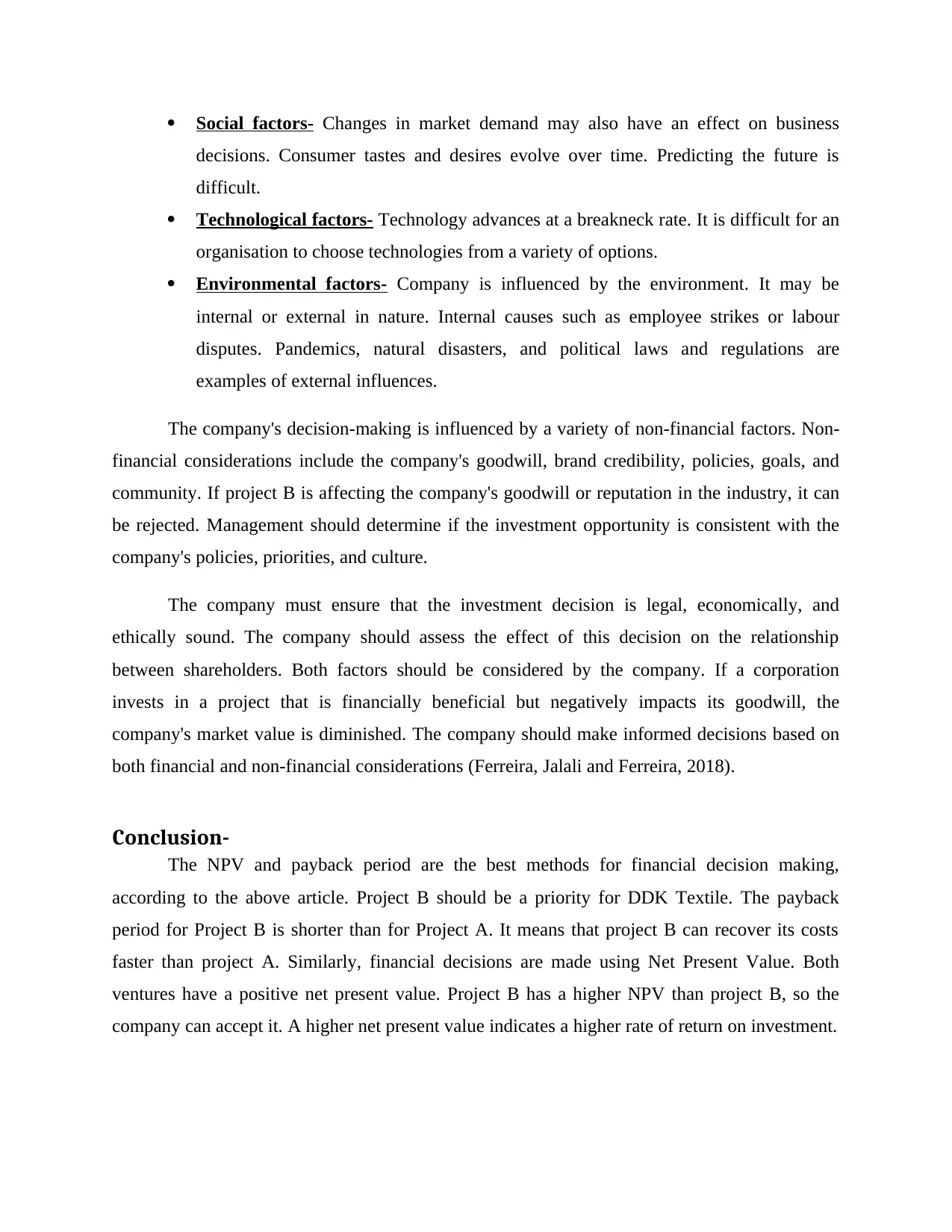

Social factors- Changes in market demand may also have an effect on business

decisions. Consumer tastes and desires evolve over time. Predicting the future is

difficult.

Technological factors- Technology advances at a breakneck rate. It is difficult for an

organisation to choose technologies from a variety of options.

Environmental factors- Company is influenced by the environment. It may be

internal or external in nature. Internal causes such as employee strikes or labour

disputes. Pandemics, natural disasters, and political laws and regulations are

examples of external influences.

The company's decision-making is influenced by a variety of non-financial factors. Non-

financial considerations include the company's goodwill, brand credibility, policies, goals, and

community. If project B is affecting the company's goodwill or reputation in the industry, it can

be rejected. Management should determine if the investment opportunity is consistent with the

company's policies, priorities, and culture.

The company must ensure that the investment decision is legal, economically, and

ethically sound. The company should assess the effect of this decision on the relationship

between shareholders. Both factors should be considered by the company. If a corporation

invests in a project that is financially beneficial but negatively impacts its goodwill, the

company's market value is diminished. The company should make informed decisions based on

both financial and non-financial considerations (Ferreira, Jalali and Ferreira, 2018).

Conclusion-

The NPV and payback period are the best methods for financial decision making,

according to the above article. Project B should be a priority for DDK Textile. The payback

period for Project B is shorter than for Project A. It means that project B can recover its costs

faster than project A. Similarly, financial decisions are made using Net Present Value. Both

ventures have a positive net present value. Project B has a higher NPV than project B, so the

company can accept it. A higher net present value indicates a higher rate of return on investment.

decisions. Consumer tastes and desires evolve over time. Predicting the future is

difficult.

Technological factors- Technology advances at a breakneck rate. It is difficult for an

organisation to choose technologies from a variety of options.

Environmental factors- Company is influenced by the environment. It may be

internal or external in nature. Internal causes such as employee strikes or labour

disputes. Pandemics, natural disasters, and political laws and regulations are

examples of external influences.

The company's decision-making is influenced by a variety of non-financial factors. Non-

financial considerations include the company's goodwill, brand credibility, policies, goals, and

community. If project B is affecting the company's goodwill or reputation in the industry, it can

be rejected. Management should determine if the investment opportunity is consistent with the

company's policies, priorities, and culture.

The company must ensure that the investment decision is legal, economically, and

ethically sound. The company should assess the effect of this decision on the relationship

between shareholders. Both factors should be considered by the company. If a corporation

invests in a project that is financially beneficial but negatively impacts its goodwill, the

company's market value is diminished. The company should make informed decisions based on

both financial and non-financial considerations (Ferreira, Jalali and Ferreira, 2018).

Conclusion-

The NPV and payback period are the best methods for financial decision making,

according to the above article. Project B should be a priority for DDK Textile. The payback

period for Project B is shorter than for Project A. It means that project B can recover its costs

faster than project A. Similarly, financial decisions are made using Net Present Value. Both

ventures have a positive net present value. Project B has a higher NPV than project B, so the

company can accept it. A higher net present value indicates a higher rate of return on investment.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and journals

Ahmed, F., Qin, Y. and Aduamoah, M., 2018, March. Employee readiness for acceptance of

decision support systems as a new technology in E-business environments; A proposed

research agenda. In 2018 7th International Conference on Industrial Technology and

Management (ICITM) (pp. 209-212). IEEE.

Ananthram, S. and Chan, C., 2016. Religiosity, spirituality and ethical decision-making:

Perspectives from executives in Indian multinational enterprises. Asia Pacific Journal of

Management, 33(3), pp.843-880.

Dahl, R.A., 2017. Decision-making in a democracy: The Supreme Court as a national policy-

maker (pp. 137-154). Routledge.

Ferreira, J.J., Jalali, M.S. and Ferreira, F.A., 2018. Enhancing the decision-making virtuous cycle

of ethical banking practices using the Choquet integral. Journal of Business Research,

88, pp.492-497.

Books and journals

Ahmed, F., Qin, Y. and Aduamoah, M., 2018, March. Employee readiness for acceptance of

decision support systems as a new technology in E-business environments; A proposed

research agenda. In 2018 7th International Conference on Industrial Technology and

Management (ICITM) (pp. 209-212). IEEE.

Ananthram, S. and Chan, C., 2016. Religiosity, spirituality and ethical decision-making:

Perspectives from executives in Indian multinational enterprises. Asia Pacific Journal of

Management, 33(3), pp.843-880.

Dahl, R.A., 2017. Decision-making in a democracy: The Supreme Court as a national policy-

maker (pp. 137-154). Routledge.

Ferreira, J.J., Jalali, M.S. and Ferreira, F.A., 2018. Enhancing the decision-making virtuous cycle

of ethical banking practices using the Choquet integral. Journal of Business Research,

88, pp.492-497.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.