Financial Statement Analysis and Business Decision-Making Report

VerifiedAdded on 2023/06/18

|13

|2648

|432

Report

AI Summary

This report provides a comprehensive analysis of financial statements and their role in business decision-making. It discusses the importance of financial statements, including the Profit and Loss (P&L) statement and Balance Sheet, in assessing a company's financial health. The report includes a practical example of P&L and Balance Sheet preparation, highlighting key components such as revenue, cost of sales, gross profit, expenses, assets, liabilities, and equity. It also examines the limitations of both the P&L account and Balance Sheet, such as the implication of the accrual concept, difficulty in comparison, overlooking non-monetary assets, and the use of historical values. Furthermore, the report delves into ratio analysis, explaining its use in determining a company's liquidity, efficiency, and capacity. It calculates and interprets key ratios such as inventory days, trade payable days, and trade receivable days, providing recommendations for improvement. The conclusion emphasizes the significance of financial analysis in making informed business decisions.

BUSINESS DECISION-

MAKING

MAKING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

TASK-1............................................................................................................................................3

TASK-2 ...........................................................................................................................................4

TASK-3............................................................................................................................................6

TASK-4............................................................................................................................................6

TASK-5............................................................................................................................................7

CONCLUSION................................................................................................................................9

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

TASK-1............................................................................................................................................3

TASK-2 ...........................................................................................................................................4

TASK-3............................................................................................................................................6

TASK-4............................................................................................................................................6

TASK-5............................................................................................................................................7

CONCLUSION................................................................................................................................9

REFERENCES................................................................................................................................1

INTRODUCTION

Business decision is one of the important task and aspect with regard to any company. It

plays a major role with regard to company and from investor perspective too. Financial

statements including P&L, Balance sheet plays a major role in this (Krylov, 2021). Likewise,

with the analysis of the ratio with the concerned company based on financial statements,

company's financial health can be determined and analysed. This report will discuss about the

concept of financial statement including Balance sheet, P&L with its practical implication and

preparation. Likewise, an analysis of ratio and its use in the business decision is also presented in

this report.

MAIN BODY

TASK-1

Financial statements:

Financial statements are the report that enable the entity's financial information, including

the assets, liabilities, profits, financial position, cash flows and various other (Osadchy and et.al.,

2018). With the help of financial statements company can measure its performance in terms of

determination of loopholes and on that basis taking of corrective actions.

P&L Statement:

It refers to a statement that outline the revenue, cost, expenses and net profit that is being

earned by company within the financial year. It is one of the important financial statement which

is used by company to determine their financial health and performance (Oncioiu, Calotă and

Tănase, 2021). As this statement shows the amount of profit which is earned by company so

through this statement company can determine its financial health along with plan its future

strategies. Likewise, this statement also shows the amount of gross profit that is a reflection of

profit after making deduction of cost element.

Particular Amount

Sales 290357

Less: Cost of sales -150060

Business decision is one of the important task and aspect with regard to any company. It

plays a major role with regard to company and from investor perspective too. Financial

statements including P&L, Balance sheet plays a major role in this (Krylov, 2021). Likewise,

with the analysis of the ratio with the concerned company based on financial statements,

company's financial health can be determined and analysed. This report will discuss about the

concept of financial statement including Balance sheet, P&L with its practical implication and

preparation. Likewise, an analysis of ratio and its use in the business decision is also presented in

this report.

MAIN BODY

TASK-1

Financial statements:

Financial statements are the report that enable the entity's financial information, including

the assets, liabilities, profits, financial position, cash flows and various other (Osadchy and et.al.,

2018). With the help of financial statements company can measure its performance in terms of

determination of loopholes and on that basis taking of corrective actions.

P&L Statement:

It refers to a statement that outline the revenue, cost, expenses and net profit that is being

earned by company within the financial year. It is one of the important financial statement which

is used by company to determine their financial health and performance (Oncioiu, Calotă and

Tănase, 2021). As this statement shows the amount of profit which is earned by company so

through this statement company can determine its financial health along with plan its future

strategies. Likewise, this statement also shows the amount of gross profit that is a reflection of

profit after making deduction of cost element.

Particular Amount

Sales 290357

Less: Cost of sales -150060

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

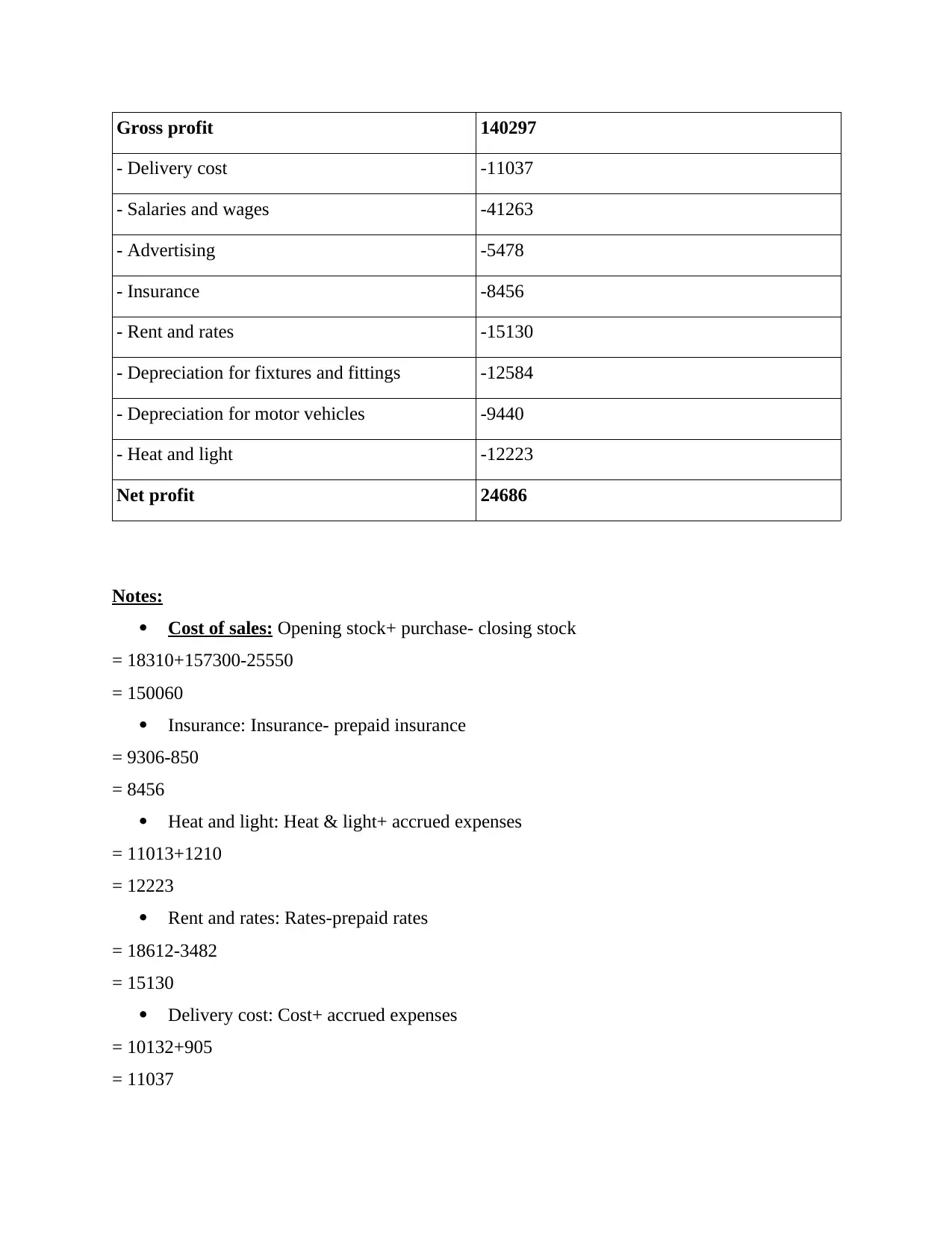

Gross profit 140297

- Delivery cost -11037

- Salaries and wages -41263

- Advertising -5478

- Insurance -8456

- Rent and rates -15130

- Depreciation for fixtures and fittings -12584

- Depreciation for motor vehicles -9440

- Heat and light -12223

Net profit 24686

Notes:

Cost of sales: Opening stock+ purchase- closing stock

= 18310+157300-25550

= 150060

Insurance: Insurance- prepaid insurance

= 9306-850

= 8456

Heat and light: Heat & light+ accrued expenses

= 11013+1210

= 12223

Rent and rates: Rates-prepaid rates

= 18612-3482

= 15130

Delivery cost: Cost+ accrued expenses

= 10132+905

= 11037

- Delivery cost -11037

- Salaries and wages -41263

- Advertising -5478

- Insurance -8456

- Rent and rates -15130

- Depreciation for fixtures and fittings -12584

- Depreciation for motor vehicles -9440

- Heat and light -12223

Net profit 24686

Notes:

Cost of sales: Opening stock+ purchase- closing stock

= 18310+157300-25550

= 150060

Insurance: Insurance- prepaid insurance

= 9306-850

= 8456

Heat and light: Heat & light+ accrued expenses

= 11013+1210

= 12223

Rent and rates: Rates-prepaid rates

= 18612-3482

= 15130

Delivery cost: Cost+ accrued expenses

= 10132+905

= 11037

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Here, it is to be noted that the prepaid expenses are reduced and charged from the profit

and loss account because of the concept of the Generally Accepted Accounting Principles

which shows that the expenses are to be changed in the same accounting period as the

benefit will be generated from related assets.

In the same manner accrued expenses are those that are recognized at the time of incur

even though payment is not being made. Thus, in order to meet the matching concept it is

to be deducted in the same accounting period.

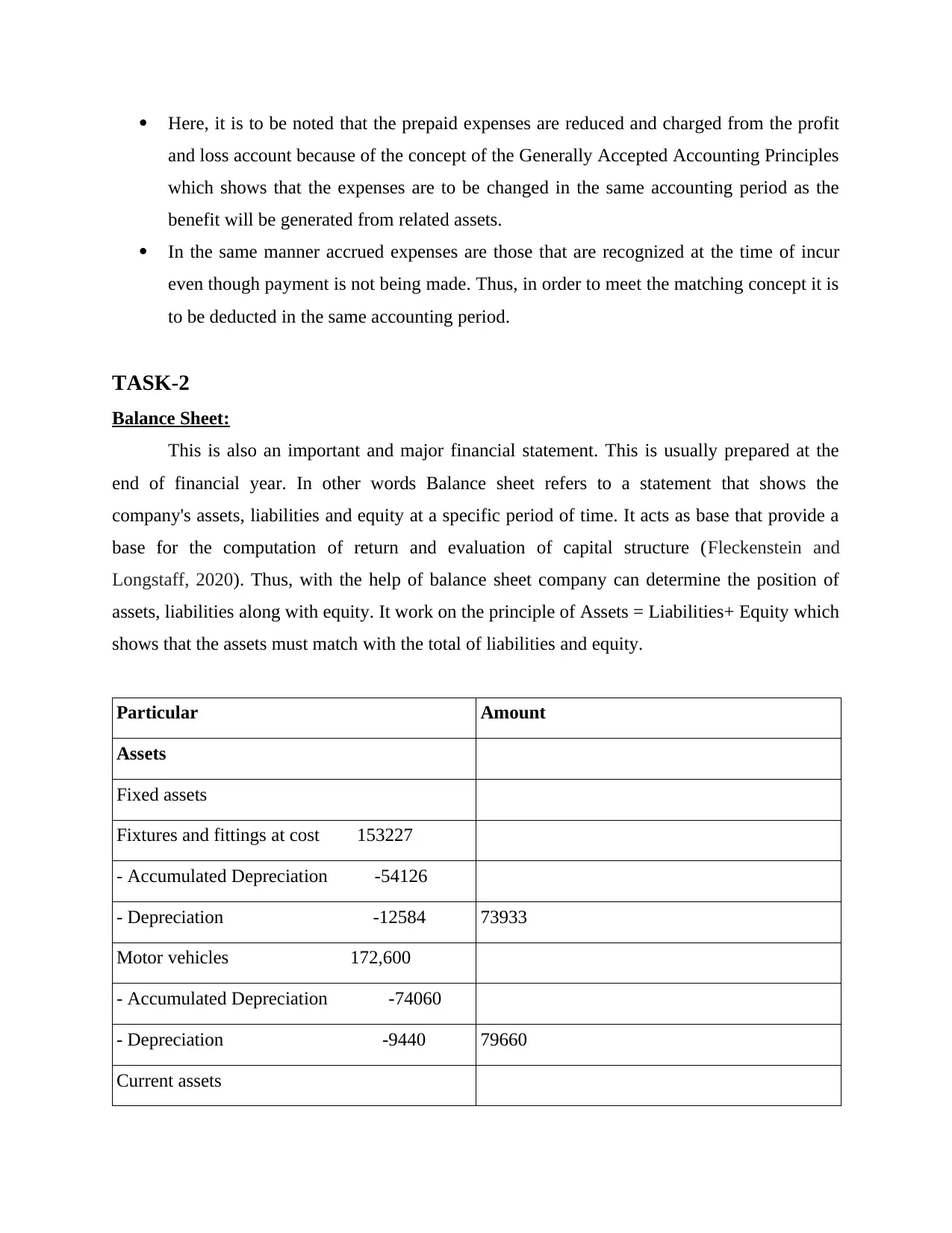

TASK-2

Balance Sheet:

This is also an important and major financial statement. This is usually prepared at the

end of financial year. In other words Balance sheet refers to a statement that shows the

company's assets, liabilities and equity at a specific period of time. It acts as base that provide a

base for the computation of return and evaluation of capital structure (Fleckenstein and

Longstaff, 2020). Thus, with the help of balance sheet company can determine the position of

assets, liabilities along with equity. It work on the principle of Assets = Liabilities+ Equity which

shows that the assets must match with the total of liabilities and equity.

Particular Amount

Assets

Fixed assets

Fixtures and fittings at cost 153227

- Accumulated Depreciation -54126

- Depreciation -12584 73933

Motor vehicles 172,600

- Accumulated Depreciation -74060

- Depreciation -9440 79660

Current assets

and loss account because of the concept of the Generally Accepted Accounting Principles

which shows that the expenses are to be changed in the same accounting period as the

benefit will be generated from related assets.

In the same manner accrued expenses are those that are recognized at the time of incur

even though payment is not being made. Thus, in order to meet the matching concept it is

to be deducted in the same accounting period.

TASK-2

Balance Sheet:

This is also an important and major financial statement. This is usually prepared at the

end of financial year. In other words Balance sheet refers to a statement that shows the

company's assets, liabilities and equity at a specific period of time. It acts as base that provide a

base for the computation of return and evaluation of capital structure (Fleckenstein and

Longstaff, 2020). Thus, with the help of balance sheet company can determine the position of

assets, liabilities along with equity. It work on the principle of Assets = Liabilities+ Equity which

shows that the assets must match with the total of liabilities and equity.

Particular Amount

Assets

Fixed assets

Fixtures and fittings at cost 153227

- Accumulated Depreciation -54126

- Depreciation -12584 73933

Motor vehicles 172,600

- Accumulated Depreciation -74060

- Depreciation -9440 79660

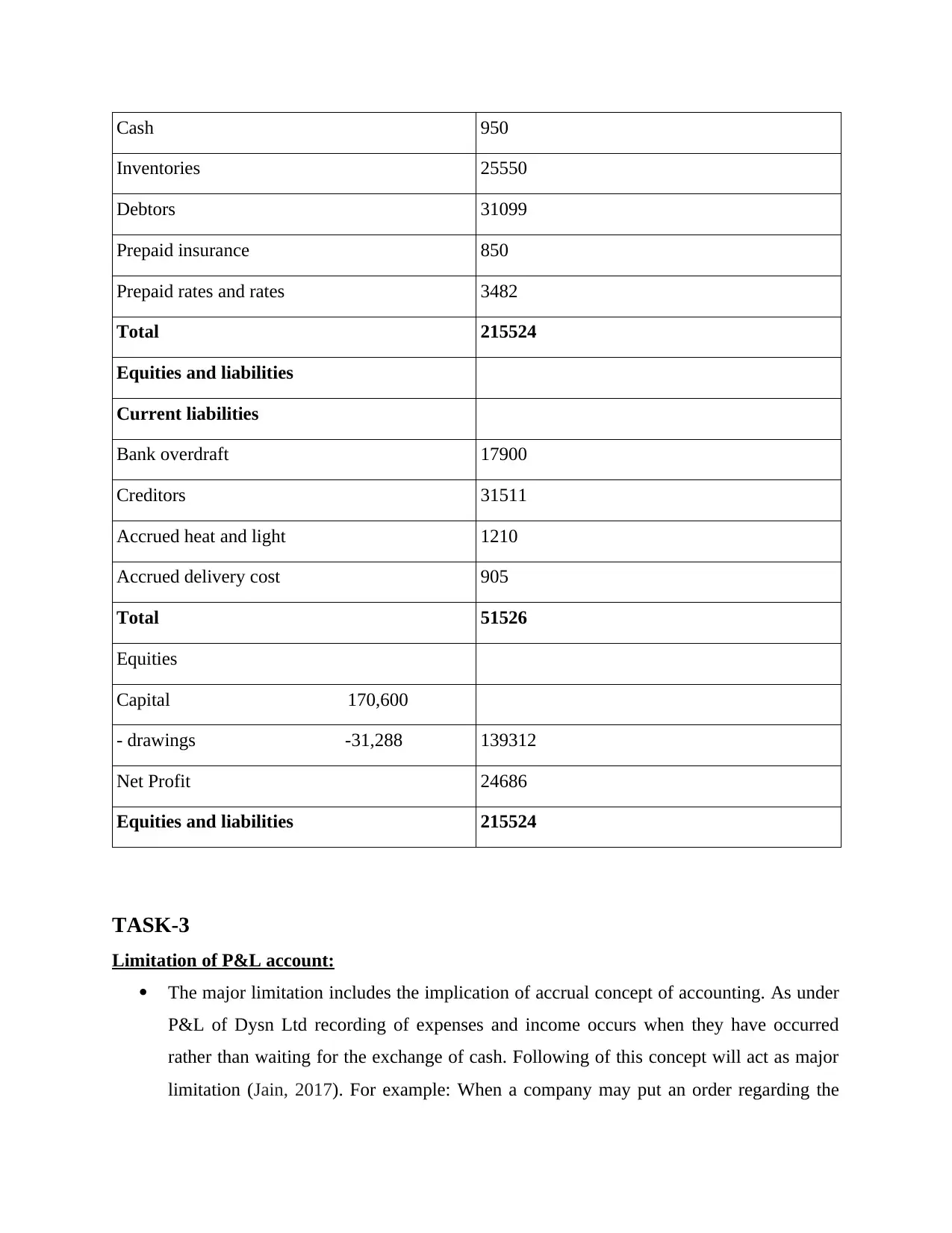

Current assets

Cash 950

Inventories 25550

Debtors 31099

Prepaid insurance 850

Prepaid rates and rates 3482

Total 215524

Equities and liabilities

Current liabilities

Bank overdraft 17900

Creditors 31511

Accrued heat and light 1210

Accrued delivery cost 905

Total 51526

Equities

Capital 170,600

- drawings -31,288 139312

Net Profit 24686

Equities and liabilities 215524

TASK-3

Limitation of P&L account:

The major limitation includes the implication of accrual concept of accounting. As under

P&L of Dysn Ltd recording of expenses and income occurs when they have occurred

rather than waiting for the exchange of cash. Following of this concept will act as major

limitation (Jain, 2017). For example: When a company may put an order regarding the

Inventories 25550

Debtors 31099

Prepaid insurance 850

Prepaid rates and rates 3482

Total 215524

Equities and liabilities

Current liabilities

Bank overdraft 17900

Creditors 31511

Accrued heat and light 1210

Accrued delivery cost 905

Total 51526

Equities

Capital 170,600

- drawings -31,288 139312

Net Profit 24686

Equities and liabilities 215524

TASK-3

Limitation of P&L account:

The major limitation includes the implication of accrual concept of accounting. As under

P&L of Dysn Ltd recording of expenses and income occurs when they have occurred

rather than waiting for the exchange of cash. Following of this concept will act as major

limitation (Jain, 2017). For example: When a company may put an order regarding the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

supply of inventory and records it as an expense in its financial statements. But on the

due date if the supplier didn't make supply of inventory then this entire transaction with

regard to expenditure will be wrong and unnecessarily company's profit decline

irrespective of occurrence of transaction.

As the financial statements are prepared at the end of financial period. But this will lead

to difficulty in comparison of different company's financial position because every

company have different preparation time (Barth, 2018). This will lead to difficult

comparison and thus analysis of the financial position would be wrongly predicted.

As the Dysn Ltd follows matching concept while preparing P&L under which revenue

must match with expenses. But in case if they do not match then it will lead to difficulty

in its preparation. Likewise following of this concept will also have chances to be not

practically equal because of the existence of difference between revenue and expenses.

TASK-4

Limitation of Balance Sheet:

Overlooking of non monetary asset is the major limitation with respect to the Balance

sheet of Dysn Ltd. As non-monetary assets like intelligence are also an important element

with respect to company and its business so its non recording emerges as a main

disadvantage. In order words overlooking and ignorance of non monetary assets

irrespective of its major role with regard to company success itself act as a disadvantage

with regard to balance sheet.

Dysn limited records its assets at its historical value which itself act as a disadvantage. As

the value of assets changes with time but is non-consideration itself emerge as its

limitation (Kausar and Lennox, 2017). However, depreciation is calculated and deducted

from asset value but it is calculated just for tax purpose and it does not reflect the wear

and tear of assets.

As the balance sheet depicts the financial position of the company of a particular date, but

this is a major disadvantage because companies usually make payment of their debts on

last date and clear their debts. This will lead to the presence of healthy financial health of

the company but it will be wrong with the perspective of investors. This is also counted

due date if the supplier didn't make supply of inventory then this entire transaction with

regard to expenditure will be wrong and unnecessarily company's profit decline

irrespective of occurrence of transaction.

As the financial statements are prepared at the end of financial period. But this will lead

to difficulty in comparison of different company's financial position because every

company have different preparation time (Barth, 2018). This will lead to difficult

comparison and thus analysis of the financial position would be wrongly predicted.

As the Dysn Ltd follows matching concept while preparing P&L under which revenue

must match with expenses. But in case if they do not match then it will lead to difficulty

in its preparation. Likewise following of this concept will also have chances to be not

practically equal because of the existence of difference between revenue and expenses.

TASK-4

Limitation of Balance Sheet:

Overlooking of non monetary asset is the major limitation with respect to the Balance

sheet of Dysn Ltd. As non-monetary assets like intelligence are also an important element

with respect to company and its business so its non recording emerges as a main

disadvantage. In order words overlooking and ignorance of non monetary assets

irrespective of its major role with regard to company success itself act as a disadvantage

with regard to balance sheet.

Dysn limited records its assets at its historical value which itself act as a disadvantage. As

the value of assets changes with time but is non-consideration itself emerge as its

limitation (Kausar and Lennox, 2017). However, depreciation is calculated and deducted

from asset value but it is calculated just for tax purpose and it does not reflect the wear

and tear of assets.

As the balance sheet depicts the financial position of the company of a particular date, but

this is a major disadvantage because companies usually make payment of their debts on

last date and clear their debts. This will lead to the presence of healthy financial health of

the company but it will be wrong with the perspective of investors. This is also counted

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

and considered as unethical because it will lead to make playing with the decision and

perspective of the stakeholders.

TASK-5

Ratio analysis:

It is a quantitative method that can be used to make analysis of the financial health of the

company. With the help of ratio analysis the company's liquidity, efficiency, capacity and

various aspects can be determined that will again act as base for business decision-making

because both the customer and the investor will make their decision on the outcome of this

analysis (Hasanaj and Kuqi, 2019). However, it will also assist the company to determine the

future strategies along with taking of corrective actions in case of finding of adverse results.

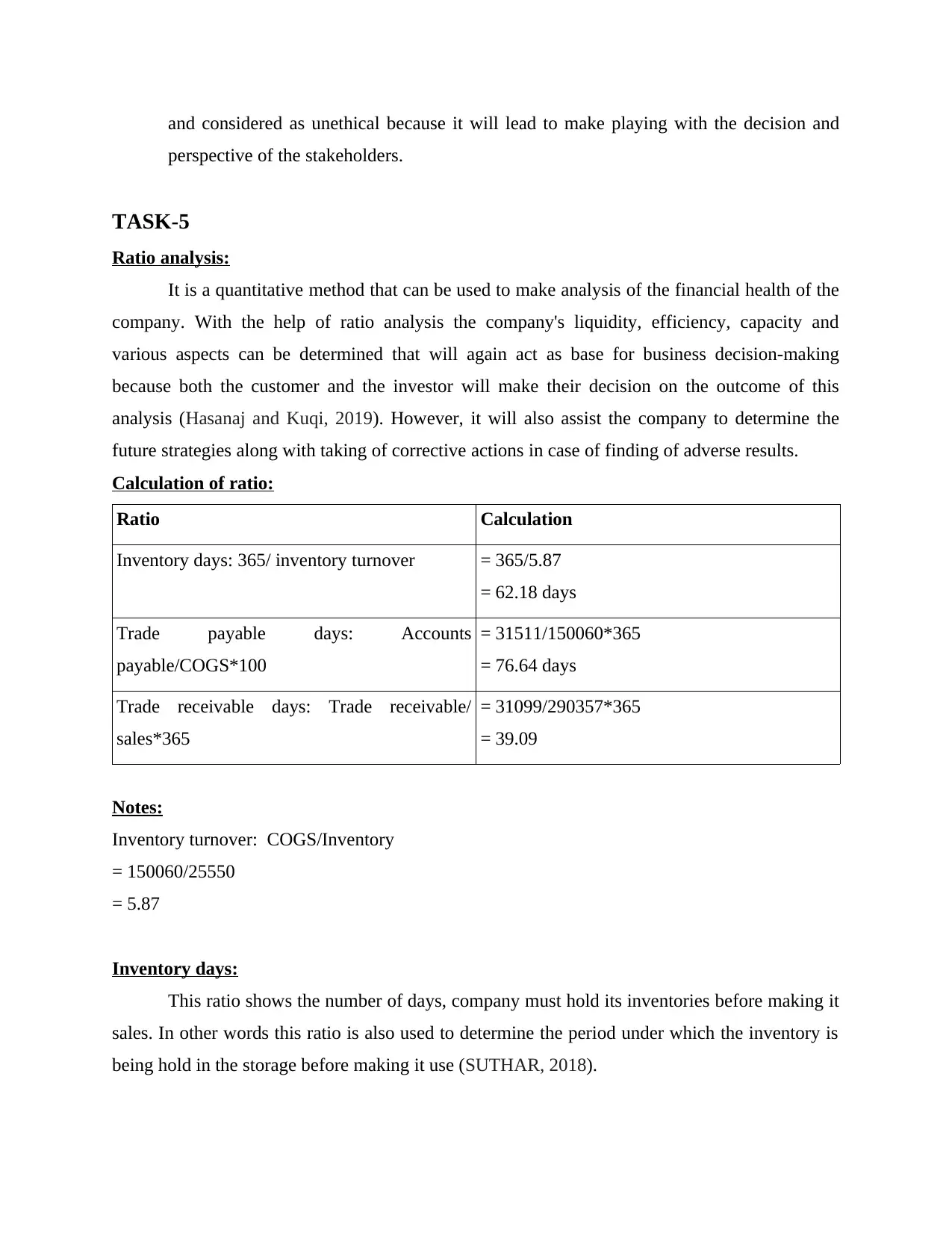

Calculation of ratio:

Ratio Calculation

Inventory days: 365/ inventory turnover = 365/5.87

= 62.18 days

Trade payable days: Accounts

payable/COGS*100

= 31511/150060*365

= 76.64 days

Trade receivable days: Trade receivable/

sales*365

= 31099/290357*365

= 39.09

Notes:

Inventory turnover: COGS/Inventory

= 150060/25550

= 5.87

Inventory days:

This ratio shows the number of days, company must hold its inventories before making it

sales. In other words this ratio is also used to determine the period under which the inventory is

being hold in the storage before making it use (SUTHAR, 2018).

perspective of the stakeholders.

TASK-5

Ratio analysis:

It is a quantitative method that can be used to make analysis of the financial health of the

company. With the help of ratio analysis the company's liquidity, efficiency, capacity and

various aspects can be determined that will again act as base for business decision-making

because both the customer and the investor will make their decision on the outcome of this

analysis (Hasanaj and Kuqi, 2019). However, it will also assist the company to determine the

future strategies along with taking of corrective actions in case of finding of adverse results.

Calculation of ratio:

Ratio Calculation

Inventory days: 365/ inventory turnover = 365/5.87

= 62.18 days

Trade payable days: Accounts

payable/COGS*100

= 31511/150060*365

= 76.64 days

Trade receivable days: Trade receivable/

sales*365

= 31099/290357*365

= 39.09

Notes:

Inventory turnover: COGS/Inventory

= 150060/25550

= 5.87

Inventory days:

This ratio shows the number of days, company must hold its inventories before making it

sales. In other words this ratio is also used to determine the period under which the inventory is

being hold in the storage before making it use (SUTHAR, 2018).

With respect to Dysn Ltd the inventory days are 62 days which is almost 2 months. Since

the ideal inventories days are around 1 to 2 months which means holding of stock in the

company will not need to be extended to more than 2 months. And in case of Dysn Ltd this

period is around 2 months which shows the company's good policies with regard to stock

holding.

However, it can further be improved with the adoption of the practice of proper

forecasting regarding the requirement of inventory, focus over the sales of old stock, smart

pricing, encourage the customers for making pre order, negotiate the prices regularly and various

other. This will lead to have improvement in the inventories days along with enabling the

business not to bind the resources and investment. Adoption and implementation of these

practices are also important because it will lead to have better earning of profits and adequate

distribution and making of investment of funds.

Trade payable days:

This is an important ratio which shows the number of days company take in order to

make the payment of its creditors. As no company can survive its business without credit, so it is

an important ratio which shows the time period taken by company in order to make repayment to

its creditors (Ilter, 2019). Longer the period would be more efficiently the funds will be invested

by company in some other sources and earn revenue.

From the above analysis of table it can be determined that the trade payable days with

regard to Dysn Ltd is 76 days. As the ideal days are 20 with regard to making payment to

suppliers, however, in Dysn Ltd it is 76 days which are more than ideal days. On the one side it

would be right in terms of making further investment and earn good revenue. But being

possessing such a long period of credit will lead to adversely impacts the company in terms of

affecting relation between suppliers and company. Hence, it needs to be maintained so that the

company may arrange the funds from market without affecting any worry.

In order to manage the Trade payable period, Dysn Ltd can adopt the practice of tracking

its creditors. Likewise, making change in the credit period can also be opt by the company in

order to make payment with the creditors. Making adequate and timely arrangement of funds and

setting of credit automated reminder period will also help the company in order to make timely

payment to creditors. Thus, with these practices and strategies Dysn Ltd can improve its period.

the ideal inventories days are around 1 to 2 months which means holding of stock in the

company will not need to be extended to more than 2 months. And in case of Dysn Ltd this

period is around 2 months which shows the company's good policies with regard to stock

holding.

However, it can further be improved with the adoption of the practice of proper

forecasting regarding the requirement of inventory, focus over the sales of old stock, smart

pricing, encourage the customers for making pre order, negotiate the prices regularly and various

other. This will lead to have improvement in the inventories days along with enabling the

business not to bind the resources and investment. Adoption and implementation of these

practices are also important because it will lead to have better earning of profits and adequate

distribution and making of investment of funds.

Trade payable days:

This is an important ratio which shows the number of days company take in order to

make the payment of its creditors. As no company can survive its business without credit, so it is

an important ratio which shows the time period taken by company in order to make repayment to

its creditors (Ilter, 2019). Longer the period would be more efficiently the funds will be invested

by company in some other sources and earn revenue.

From the above analysis of table it can be determined that the trade payable days with

regard to Dysn Ltd is 76 days. As the ideal days are 20 with regard to making payment to

suppliers, however, in Dysn Ltd it is 76 days which are more than ideal days. On the one side it

would be right in terms of making further investment and earn good revenue. But being

possessing such a long period of credit will lead to adversely impacts the company in terms of

affecting relation between suppliers and company. Hence, it needs to be maintained so that the

company may arrange the funds from market without affecting any worry.

In order to manage the Trade payable period, Dysn Ltd can adopt the practice of tracking

its creditors. Likewise, making change in the credit period can also be opt by the company in

order to make payment with the creditors. Making adequate and timely arrangement of funds and

setting of credit automated reminder period will also help the company in order to make timely

payment to creditors. Thus, with these practices and strategies Dysn Ltd can improve its period.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Trade receivable period:

This is related with the number of days company take in order to make recovery of its

debtors. As every company perform its transactions with the enabling of credit sales and thus this

ratio play its role because it shows the number of days taken by company debtors in order to

make repayment to company (Jones, 2019). The shorter the period would be company will be

benefited because it will raise the funds and company can make investment in some other modes.

With regard to above calculation and analysis it can be interpreted that the trade

receivable period for Dysn Ltd is 39 days. As the ideal period of trade receivable days should

always be low so that the company can make faster recovery and make investment of funds in

some other alternatives. However, in case of Dysn Ltd this period is 39 days which is almost 1

month, this means that the company will make arrangement and recovery of its debt within a

period of 1 month,

In order to manage the trade receivable period, Dysn limited can make diversification of

its clients. Likewise, it can also opt discounting policy under which it will entitle discounts to its

clients in order to make early repayment. Timely invoicing and reducing the payback period will

also be helpful for Dysn Ltd in order to reduce the period. Similarly, creation of AR report and

make demand of AR will also be helpful to Dysn Ltd in order to perform faster recovery of its

debtors.

CONCLUSION

From the above report it would be concluded that financial statements in the form of

Profit and loss, Balance sheet plays an important role with regard to business decision-making.

These acts as self evaluator that enable the company to make analysis of its financial health and

performance. Likewise, investors and other stakeholders can also take decision on the basis of

the analysis of the financial statements. This report also summarizes the ratio analysis which will

also plays a major role in business decision-making that will allows the investors and concerned

stakeholders to determine company's financial position and thereby taking adequate decision of

making investment.

This is related with the number of days company take in order to make recovery of its

debtors. As every company perform its transactions with the enabling of credit sales and thus this

ratio play its role because it shows the number of days taken by company debtors in order to

make repayment to company (Jones, 2019). The shorter the period would be company will be

benefited because it will raise the funds and company can make investment in some other modes.

With regard to above calculation and analysis it can be interpreted that the trade

receivable period for Dysn Ltd is 39 days. As the ideal period of trade receivable days should

always be low so that the company can make faster recovery and make investment of funds in

some other alternatives. However, in case of Dysn Ltd this period is 39 days which is almost 1

month, this means that the company will make arrangement and recovery of its debt within a

period of 1 month,

In order to manage the trade receivable period, Dysn limited can make diversification of

its clients. Likewise, it can also opt discounting policy under which it will entitle discounts to its

clients in order to make early repayment. Timely invoicing and reducing the payback period will

also be helpful for Dysn Ltd in order to reduce the period. Similarly, creation of AR report and

make demand of AR will also be helpful to Dysn Ltd in order to perform faster recovery of its

debtors.

CONCLUSION

From the above report it would be concluded that financial statements in the form of

Profit and loss, Balance sheet plays an important role with regard to business decision-making.

These acts as self evaluator that enable the company to make analysis of its financial health and

performance. Likewise, investors and other stakeholders can also take decision on the basis of

the analysis of the financial statements. This report also summarizes the ratio analysis which will

also plays a major role in business decision-making that will allows the investors and concerned

stakeholders to determine company's financial position and thereby taking adequate decision of

making investment.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and journals

Barth, M.E., 2018. The future of financial reporting: Insights from research. Abacus. 54(1).

pp.66-78.

Fleckenstein, M. and Longstaff, F.A., 2020. Renting balance sheet space: Intermediary balance

sheet rental costs and the valuation of derivatives. The Review of Financial

Studies. 33(11). pp.5051-5091.

Hasanaj, P. and Kuqi, B., 2019. Analysis of financial statements. Humanities and Social Science

Research. 2(2). pp.p17-p17.

Ilter, C., 2019. A Discussion Paper on Accounts Payable Ratio. Acta Oeconomica

Pragensia. 2019(3-4). pp.85-94.

Jones, S.A., 2019. Trade and Receivables Finance. In The Trade and Receivables Finance

Companion (pp. 389-419). Palgrave Macmillan, Cham.

Kausar, A. and Lennox, C., 2017. Balance sheet conservatism and audit reporting

conservatism. Journal of Business Finance & Accounting. 44(7-8). pp.897-924.

Krylov, S., 2021. The Content of Contemporary Analysis of Financial Statements. Available at

SSRN 3845542.

Oncioiu, I.V., Calotă, T.O. and Tănase, A.E., 2021. An Overview of Diversities in the Use of the

Profit and Loss Statement. Encyclopedia of Organizational Knowledge, Administration,

and Technology, pp.124-134.

Osadchy, and et.al., 2018. Financial statements of a company as an information base for

decision-making in a transforming economy.

SUTHAR, K., 2018. Financial Ratio Analysis: A Theoretical Study. International Journal of

Research in all Subjects in Multi Languages, Gujarat, India.

Online references

Jain, P., 2017. The disadvantages of profit and loss accounts. [Online]. Available through

<https://www.pocketpence.co.uk/disadvantages-profit-loss-accounts-8543243.html>

1

Books and journals

Barth, M.E., 2018. The future of financial reporting: Insights from research. Abacus. 54(1).

pp.66-78.

Fleckenstein, M. and Longstaff, F.A., 2020. Renting balance sheet space: Intermediary balance

sheet rental costs and the valuation of derivatives. The Review of Financial

Studies. 33(11). pp.5051-5091.

Hasanaj, P. and Kuqi, B., 2019. Analysis of financial statements. Humanities and Social Science

Research. 2(2). pp.p17-p17.

Ilter, C., 2019. A Discussion Paper on Accounts Payable Ratio. Acta Oeconomica

Pragensia. 2019(3-4). pp.85-94.

Jones, S.A., 2019. Trade and Receivables Finance. In The Trade and Receivables Finance

Companion (pp. 389-419). Palgrave Macmillan, Cham.

Kausar, A. and Lennox, C., 2017. Balance sheet conservatism and audit reporting

conservatism. Journal of Business Finance & Accounting. 44(7-8). pp.897-924.

Krylov, S., 2021. The Content of Contemporary Analysis of Financial Statements. Available at

SSRN 3845542.

Oncioiu, I.V., Calotă, T.O. and Tănase, A.E., 2021. An Overview of Diversities in the Use of the

Profit and Loss Statement. Encyclopedia of Organizational Knowledge, Administration,

and Technology, pp.124-134.

Osadchy, and et.al., 2018. Financial statements of a company as an information base for

decision-making in a transforming economy.

SUTHAR, K., 2018. Financial Ratio Analysis: A Theoretical Study. International Journal of

Research in all Subjects in Multi Languages, Gujarat, India.

Online references

Jain, P., 2017. The disadvantages of profit and loss accounts. [Online]. Available through

<https://www.pocketpence.co.uk/disadvantages-profit-loss-accounts-8543243.html>

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.