Business Decision Making

VerifiedAdded on 2023/01/13

|7

|1367

|47

AI Summary

This study focuses on business decision making, specifically on calculating payback period and net present value for Project A and Project B. It analyzes the drawbacks and benefits of using payback period and NPV, and provides implications for better management decision. The study also discusses the advantages and disadvantages of payback period and NPV.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Business Decision Making

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................3

1. COMPUTATION OF PAYBACK PERIOD...............................................................................3

2. CALCULATION OF NET PRESENT VALUE (NPV)..............................................................4

3. ANALYSIS..................................................................................................................................4

4. PRACTICAL IMPLICATION....................................................................................................5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

INTRODUCTION...........................................................................................................................3

1. COMPUTATION OF PAYBACK PERIOD...............................................................................3

2. CALCULATION OF NET PRESENT VALUE (NPV)..............................................................4

3. ANALYSIS..................................................................................................................................4

4. PRACTICAL IMPLICATION....................................................................................................5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

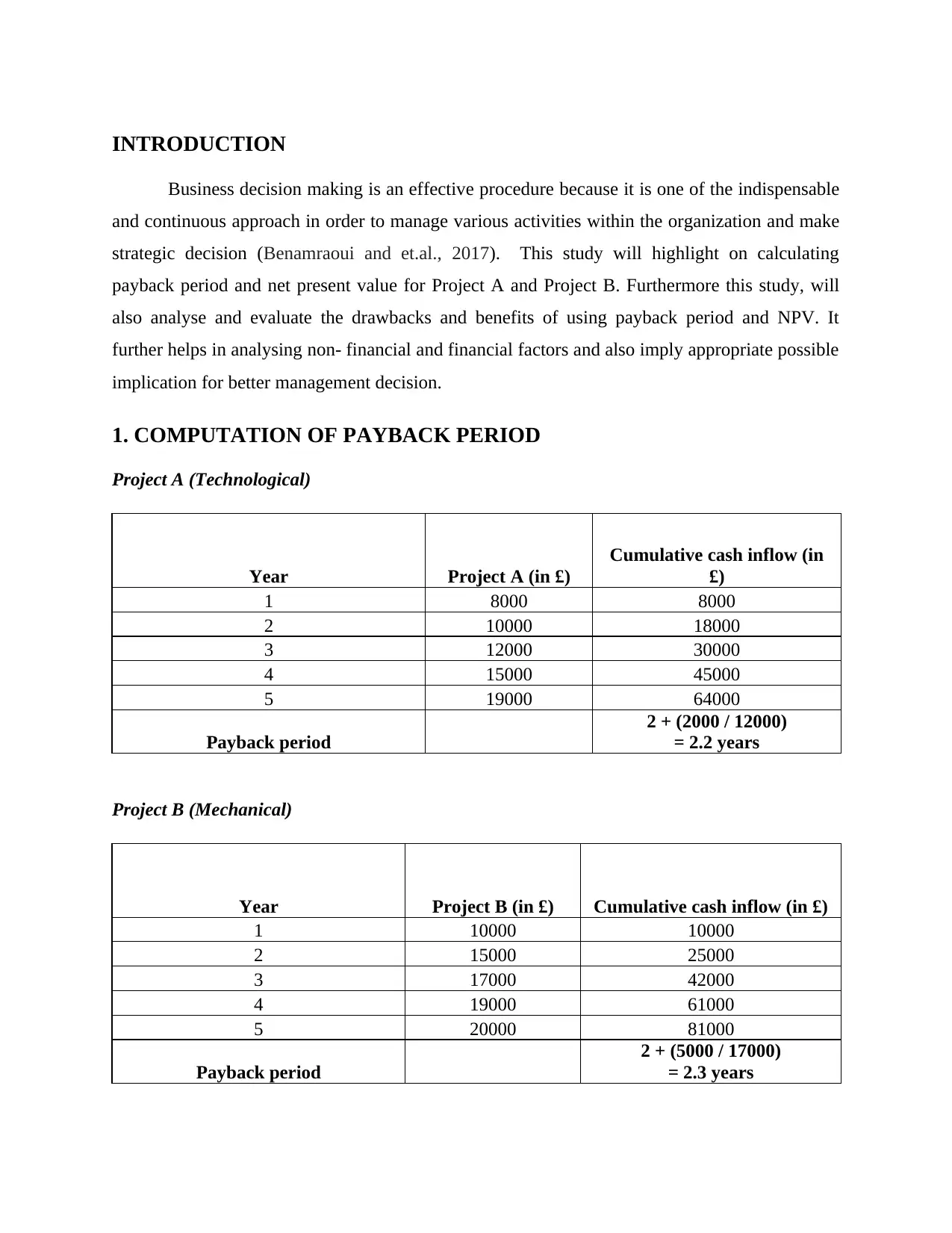

INTRODUCTION

Business decision making is an effective procedure because it is one of the indispensable

and continuous approach in order to manage various activities within the organization and make

strategic decision (Benamraoui and et.al., 2017). This study will highlight on calculating

payback period and net present value for Project A and Project B. Furthermore this study, will

also analyse and evaluate the drawbacks and benefits of using payback period and NPV. It

further helps in analysing non- financial and financial factors and also imply appropriate possible

implication for better management decision.

1. COMPUTATION OF PAYBACK PERIOD

Project A (Technological)

Year Project A (in £)

Cumulative cash inflow (in

£)

1 8000 8000

2 10000 18000

3 12000 30000

4 15000 45000

5 19000 64000

Payback period

2 + (2000 / 12000)

= 2.2 years

Project B (Mechanical)

Year Project B (in £) Cumulative cash inflow (in £)

1 10000 10000

2 15000 25000

3 17000 42000

4 19000 61000

5 20000 81000

Payback period

2 + (5000 / 17000)

= 2.3 years

Business decision making is an effective procedure because it is one of the indispensable

and continuous approach in order to manage various activities within the organization and make

strategic decision (Benamraoui and et.al., 2017). This study will highlight on calculating

payback period and net present value for Project A and Project B. Furthermore this study, will

also analyse and evaluate the drawbacks and benefits of using payback period and NPV. It

further helps in analysing non- financial and financial factors and also imply appropriate possible

implication for better management decision.

1. COMPUTATION OF PAYBACK PERIOD

Project A (Technological)

Year Project A (in £)

Cumulative cash inflow (in

£)

1 8000 8000

2 10000 18000

3 12000 30000

4 15000 45000

5 19000 64000

Payback period

2 + (2000 / 12000)

= 2.2 years

Project B (Mechanical)

Year Project B (in £) Cumulative cash inflow (in £)

1 10000 10000

2 15000 25000

3 17000 42000

4 19000 61000

5 20000 81000

Payback period

2 + (5000 / 17000)

= 2.3 years

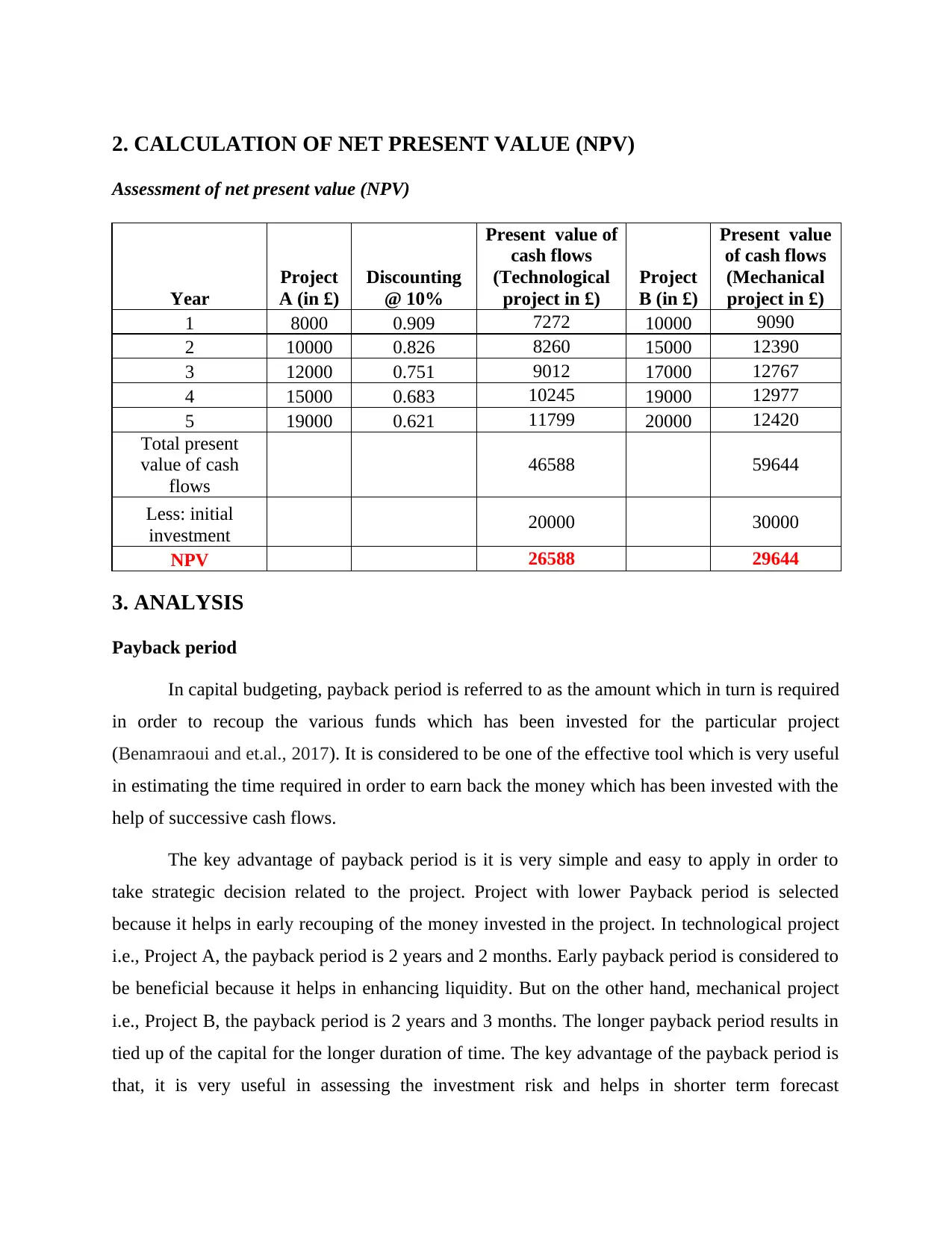

2. CALCULATION OF NET PRESENT VALUE (NPV)

Assessment of net present value (NPV)

Year

Project

A (in £)

Discounting

@ 10%

Present value of

cash flows

(Technological

project in £)

Project

B (in £)

Present value

of cash flows

(Mechanical

project in £)

1 8000 0.909 7272 10000 9090

2 10000 0.826 8260 15000 12390

3 12000 0.751 9012 17000 12767

4 15000 0.683 10245 19000 12977

5 19000 0.621 11799 20000 12420

Total present

value of cash

flows

46588 59644

Less: initial

investment 20000 30000

NPV 26588 29644

3. ANALYSIS

Payback period

In capital budgeting, payback period is referred to as the amount which in turn is required

in order to recoup the various funds which has been invested for the particular project

(Benamraoui and et.al., 2017). It is considered to be one of the effective tool which is very useful

in estimating the time required in order to earn back the money which has been invested with the

help of successive cash flows.

The key advantage of payback period is it is very simple and easy to apply in order to

take strategic decision related to the project. Project with lower Payback period is selected

because it helps in early recouping of the money invested in the project. In technological project

i.e., Project A, the payback period is 2 years and 2 months. Early payback period is considered to

be beneficial because it helps in enhancing liquidity. But on the other hand, mechanical project

i.e., Project B, the payback period is 2 years and 3 months. The longer payback period results in

tied up of the capital for the longer duration of time. The key advantage of the payback period is

that, it is very useful in assessing the investment risk and helps in shorter term forecast

Assessment of net present value (NPV)

Year

Project

A (in £)

Discounting

@ 10%

Present value of

cash flows

(Technological

project in £)

Project

B (in £)

Present value

of cash flows

(Mechanical

project in £)

1 8000 0.909 7272 10000 9090

2 10000 0.826 8260 15000 12390

3 12000 0.751 9012 17000 12767

4 15000 0.683 10245 19000 12977

5 19000 0.621 11799 20000 12420

Total present

value of cash

flows

46588 59644

Less: initial

investment 20000 30000

NPV 26588 29644

3. ANALYSIS

Payback period

In capital budgeting, payback period is referred to as the amount which in turn is required

in order to recoup the various funds which has been invested for the particular project

(Benamraoui and et.al., 2017). It is considered to be one of the effective tool which is very useful

in estimating the time required in order to earn back the money which has been invested with the

help of successive cash flows.

The key advantage of payback period is it is very simple and easy to apply in order to

take strategic decision related to the project. Project with lower Payback period is selected

because it helps in early recouping of the money invested in the project. In technological project

i.e., Project A, the payback period is 2 years and 2 months. Early payback period is considered to

be beneficial because it helps in enhancing liquidity. But on the other hand, mechanical project

i.e., Project B, the payback period is 2 years and 3 months. The longer payback period results in

tied up of the capital for the longer duration of time. The key advantage of the payback period is

that, it is very useful in assessing the investment risk and helps in shorter term forecast

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

(Advantages & Disadvantages of Payback Capital Budgeting Method, 2019). The major

disadvantage of the payback period is that, it ignores TMV i.e., time value of money. Another

major key limitation of the payback period is it ignores the timing of the cash inflows at the time

of payback period.

Net Present Value

The net present value is considered to be the present value of the certain sum of money.

The projected cash flow is intended to be discounted each year by the certain rate (Gorshkov,

Murgul and Oliynyk, 2016). This in turn helps in determining the expected return on the

investment is considered to be positive or negative.

Positive net present value states that, the projected earnings which in turn are generated

through specific project tends to exceed the anticipated cost (Namanda, 2017). The net present

value for the technological project i.e., Project A, is estimated to be £26588. On the other hand,

the net present value for the mechanical project i.e., Project B, is estimated to be £29644. It has

been examined that, the NPV of the Project B is higher when compared with Project A. this

means that Project B is going to give higher returns in the future and greater profitability

(Hopkinson, 2017). The major advantage of the NPV is that, it helps in maximizing the wealth

by gaining higher returns as compared to the cost of capital.

Non- financial factors mainly includes improve morale of employees to retain and recruit

talented employees, improved relationship, mitigating future and current legislation, etc. On the

other hand, financial factors includes rates, cash flows, expenditures, revenue, capital, cost of the

goods, etc. in order to take strategic decision for the particular project (Zis and et.al., 2016).

4. PRACTICAL IMPLICATION

Management of the company uses various financial factors like initial investment,

projected cash flows in order to measure the projected payback period for the Project A and

Project B. In order to implicate project B the financial factors which influence the net present

value of the project is estimated to be discount rate, projected returns, investment cost,

unforeseen expenditure, additional expenditure in order to assess the real estimated profitability

of the project B. The payback period is considered to be very useful in getting back the initial

investment by estimating the time of recouping the money invested through payback period.

disadvantage of the payback period is that, it ignores TMV i.e., time value of money. Another

major key limitation of the payback period is it ignores the timing of the cash inflows at the time

of payback period.

Net Present Value

The net present value is considered to be the present value of the certain sum of money.

The projected cash flow is intended to be discounted each year by the certain rate (Gorshkov,

Murgul and Oliynyk, 2016). This in turn helps in determining the expected return on the

investment is considered to be positive or negative.

Positive net present value states that, the projected earnings which in turn are generated

through specific project tends to exceed the anticipated cost (Namanda, 2017). The net present

value for the technological project i.e., Project A, is estimated to be £26588. On the other hand,

the net present value for the mechanical project i.e., Project B, is estimated to be £29644. It has

been examined that, the NPV of the Project B is higher when compared with Project A. this

means that Project B is going to give higher returns in the future and greater profitability

(Hopkinson, 2017). The major advantage of the NPV is that, it helps in maximizing the wealth

by gaining higher returns as compared to the cost of capital.

Non- financial factors mainly includes improve morale of employees to retain and recruit

talented employees, improved relationship, mitigating future and current legislation, etc. On the

other hand, financial factors includes rates, cash flows, expenditures, revenue, capital, cost of the

goods, etc. in order to take strategic decision for the particular project (Zis and et.al., 2016).

4. PRACTICAL IMPLICATION

Management of the company uses various financial factors like initial investment,

projected cash flows in order to measure the projected payback period for the Project A and

Project B. In order to implicate project B the financial factors which influence the net present

value of the project is estimated to be discount rate, projected returns, investment cost,

unforeseen expenditure, additional expenditure in order to assess the real estimated profitability

of the project B. The payback period is considered to be very useful in getting back the initial

investment by estimating the time of recouping the money invested through payback period.

The key role of the net present value is that, it helps managers and investors of the

company to only invest in the projects which tends to have positive NPV (Madichie and et.al.,

2017). The key factors which tends to affect the profitability of the business is that, high discount

rate tends to result in low present value of expenditure on the future date.

CONCLUSION

From the above conducted study it has been concluded that, the management of the

company will choose Project A because the Payback period calculated is 2.2 years which is

lower as compared to the Project B. On the contrary, this study summarizes that, the

management of the company will choose Project B because the Net present value is higher when

compared with Project A. This results in higher growth and profitability.

company to only invest in the projects which tends to have positive NPV (Madichie and et.al.,

2017). The key factors which tends to affect the profitability of the business is that, high discount

rate tends to result in low present value of expenditure on the future date.

CONCLUSION

From the above conducted study it has been concluded that, the management of the

company will choose Project A because the Payback period calculated is 2.2 years which is

lower as compared to the Project B. On the contrary, this study summarizes that, the

management of the company will choose Project B because the Net present value is higher when

compared with Project A. This results in higher growth and profitability.

REFERENCES

Books and Journals

Benamraoui, A and et.al., 2017. Net Present Value Analysis and the Wealth Creation Process: A

Case Illustration. The Accounting Educators' Journal.26.

Gorshkov, A., Murgul, V. and Oliynyk, O., 2016. Forecasted Payback Period in the Case of

Energy-Efficient Activities. In MATEC Web of Conferences(Vol. 53, p. 01045). EDP

Sciences.

Hopkinson, M., 2017. Net Present value and risk modelling for projects. Routledge.

Madichie, N.O and et.al., 2017. Net Present Value Analysis and the Wealth Creation Process: A

Case Illustration. The Accounting Educators' Journal.26.

Namanda, M., 2017. Capital Budgeting, Net Present Value and other Business Decision Making

Tools.

Zis, T and et.al., 2016. Payback period for emissions abatement alternatives: Role of regulation

and fuel prices. Transportation Research Record. 2549(1), pp.37-44.

Online

Advantages & Disadvantages of Payback Capital Budgeting Method. 2019. [ONLINE].

Available through<https://smallbusiness.chron.com/advantages-disadvantages-payback-

capital-budgeting-method-14206.html>

Books and Journals

Benamraoui, A and et.al., 2017. Net Present Value Analysis and the Wealth Creation Process: A

Case Illustration. The Accounting Educators' Journal.26.

Gorshkov, A., Murgul, V. and Oliynyk, O., 2016. Forecasted Payback Period in the Case of

Energy-Efficient Activities. In MATEC Web of Conferences(Vol. 53, p. 01045). EDP

Sciences.

Hopkinson, M., 2017. Net Present value and risk modelling for projects. Routledge.

Madichie, N.O and et.al., 2017. Net Present Value Analysis and the Wealth Creation Process: A

Case Illustration. The Accounting Educators' Journal.26.

Namanda, M., 2017. Capital Budgeting, Net Present Value and other Business Decision Making

Tools.

Zis, T and et.al., 2016. Payback period for emissions abatement alternatives: Role of regulation

and fuel prices. Transportation Research Record. 2549(1), pp.37-44.

Online

Advantages & Disadvantages of Payback Capital Budgeting Method. 2019. [ONLINE].

Available through<https://smallbusiness.chron.com/advantages-disadvantages-payback-

capital-budgeting-method-14206.html>

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.