Business Decision Making Essay: Investment Appraisal for DDK plc

VerifiedAdded on 2022/12/09

|7

|1412

|119

Essay

AI Summary

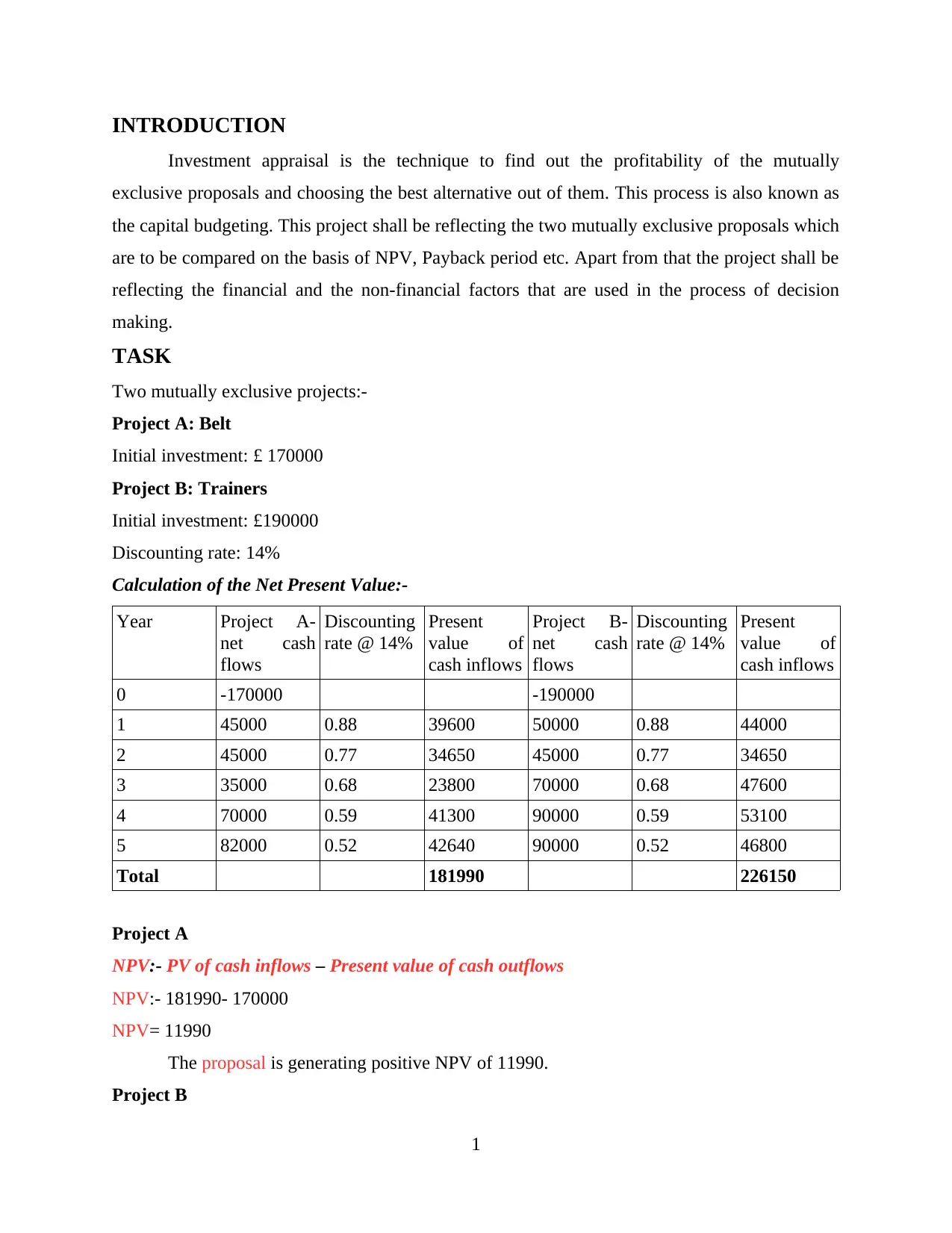

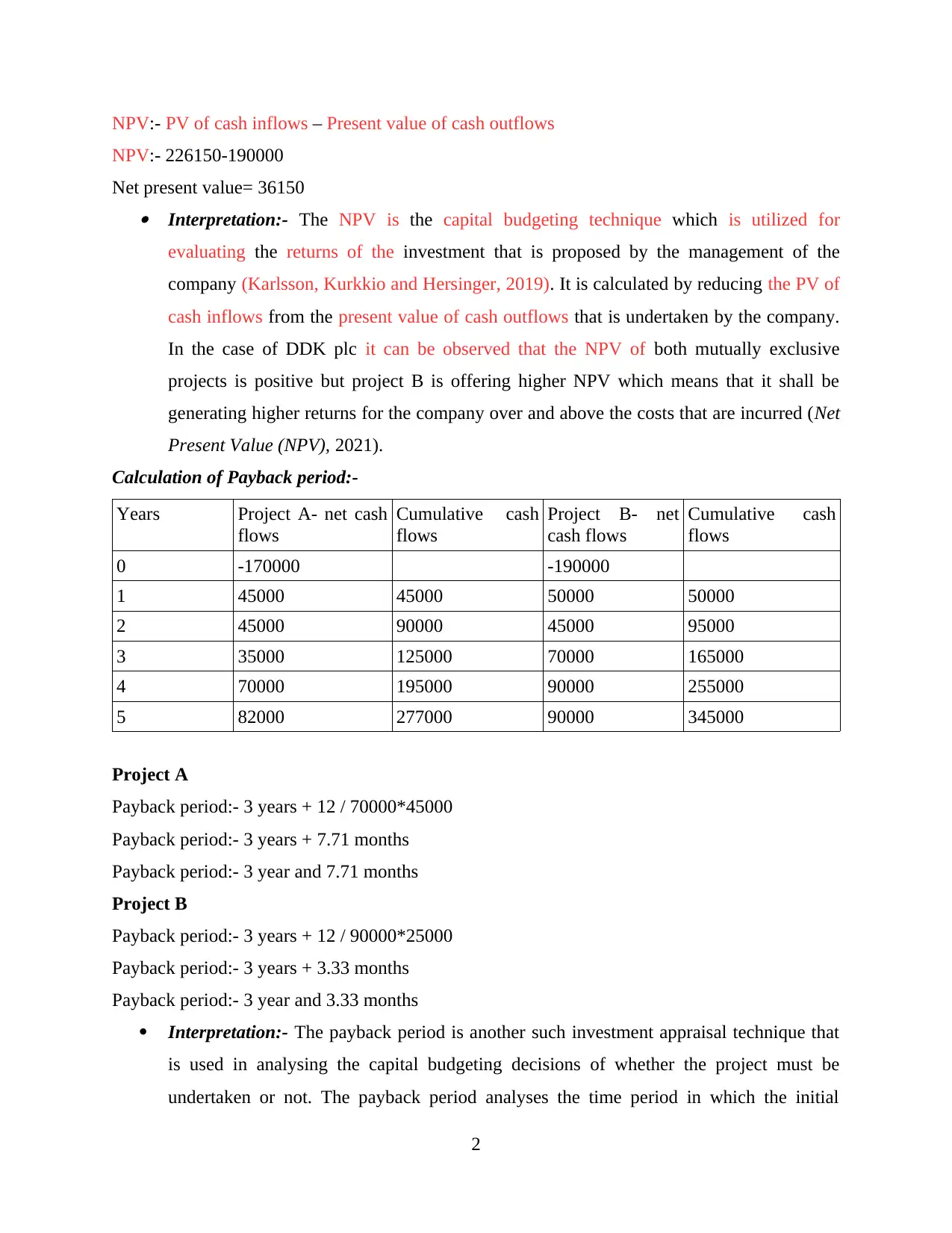

This essay analyzes investment appraisal techniques, specifically focusing on Net Present Value (NPV) and payback period, to evaluate mutually exclusive projects for DDK plc. The assignment calculates and interprets NPV and payback periods for two projects (Belt and Trainers), determining the more feasible investment based on financial metrics. The essay also explores financial factors like net cash inflows and potential rate of return, alongside non-financial factors such as human resources and technology, that influence capital budgeting decisions. The conclusion emphasizes the importance of comprehensive evaluation using investment appraisal techniques before executing investment plans, considering both financial and non-financial aspects.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.