BA4008QA: Business Decision Making - Financial Statement Analysis

VerifiedAdded on 2023/06/15

|10

|1987

|231

Report

AI Summary

This report provides a detailed analysis of financial statements for business decision-making, focusing on London Ventures. It includes the preparation of an income statement and statement of financial position, along with calculations and recommendations for managing inventory days, trade payable days, and trade receivable days. The report also discusses the limitations of income statements and balance sheets, offering insights into how London Ventures can effectively manage its financial performance and improve its business operations. The analysis incorporates working notes for clarity and references relevant academic sources.

BA4008QA BUSINESS

DECISION MAKING

DECISION MAKING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

(a) Preparation of Income Statement for the year ended 31st March 2021................................3

(b) Preparation of Statement of financial position as at 31st March 2021..................................4

TASK 2............................................................................................................................................6

Three possible limitations of the Income Statement for Ventures..............................................6

TASK 3............................................................................................................................................6

Three possible limitations of statement financial position for ventures.....................................6

TASK 4............................................................................................................................................7

Explanation of how London venture company effective manage following efficiency ratios:. .7

CONCLUSION................................................................................................................................8

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

(a) Preparation of Income Statement for the year ended 31st March 2021................................3

(b) Preparation of Statement of financial position as at 31st March 2021..................................4

TASK 2............................................................................................................................................6

Three possible limitations of the Income Statement for Ventures..............................................6

TASK 3............................................................................................................................................6

Three possible limitations of statement financial position for ventures.....................................6

TASK 4............................................................................................................................................7

Explanation of how London venture company effective manage following efficiency ratios:. .7

CONCLUSION................................................................................................................................8

REFERENCES..............................................................................................................................10

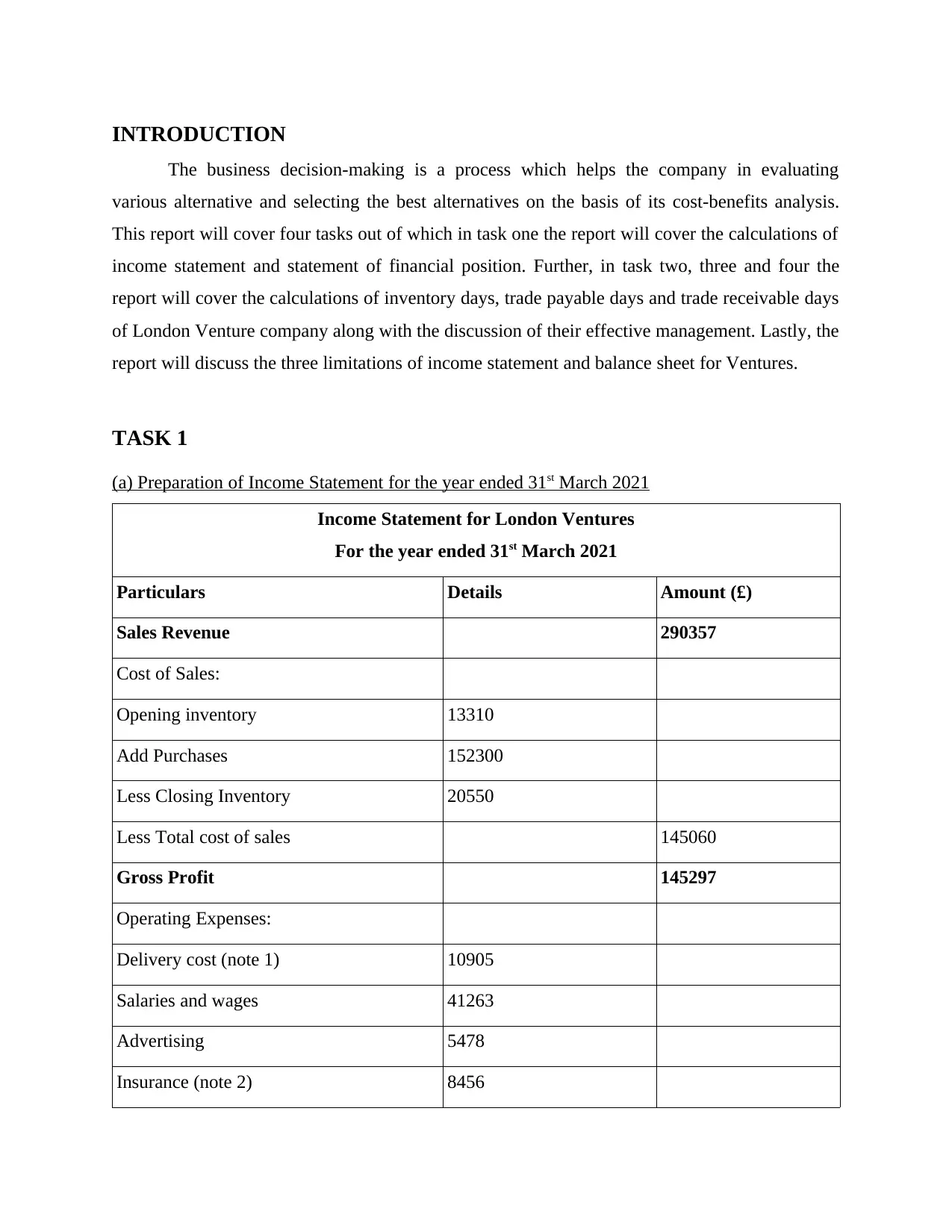

INTRODUCTION

The business decision-making is a process which helps the company in evaluating

various alternative and selecting the best alternatives on the basis of its cost-benefits analysis.

This report will cover four tasks out of which in task one the report will cover the calculations of

income statement and statement of financial position. Further, in task two, three and four the

report will cover the calculations of inventory days, trade payable days and trade receivable days

of London Venture company along with the discussion of their effective management. Lastly, the

report will discuss the three limitations of income statement and balance sheet for Ventures.

TASK 1

(a) Preparation of Income Statement for the year ended 31st March 2021

Income Statement for London Ventures

For the year ended 31st March 2021

Particulars Details Amount (£)

Sales Revenue 290357

Cost of Sales:

Opening inventory 13310

Add Purchases 152300

Less Closing Inventory 20550

Less Total cost of sales 145060

Gross Profit 145297

Operating Expenses:

Delivery cost (note 1) 10905

Salaries and wages 41263

Advertising 5478

Insurance (note 2) 8456

The business decision-making is a process which helps the company in evaluating

various alternative and selecting the best alternatives on the basis of its cost-benefits analysis.

This report will cover four tasks out of which in task one the report will cover the calculations of

income statement and statement of financial position. Further, in task two, three and four the

report will cover the calculations of inventory days, trade payable days and trade receivable days

of London Venture company along with the discussion of their effective management. Lastly, the

report will discuss the three limitations of income statement and balance sheet for Ventures.

TASK 1

(a) Preparation of Income Statement for the year ended 31st March 2021

Income Statement for London Ventures

For the year ended 31st March 2021

Particulars Details Amount (£)

Sales Revenue 290357

Cost of Sales:

Opening inventory 13310

Add Purchases 152300

Less Closing Inventory 20550

Less Total cost of sales 145060

Gross Profit 145297

Operating Expenses:

Delivery cost (note 1) 10905

Salaries and wages 41263

Advertising 5478

Insurance (note 2) 8456

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

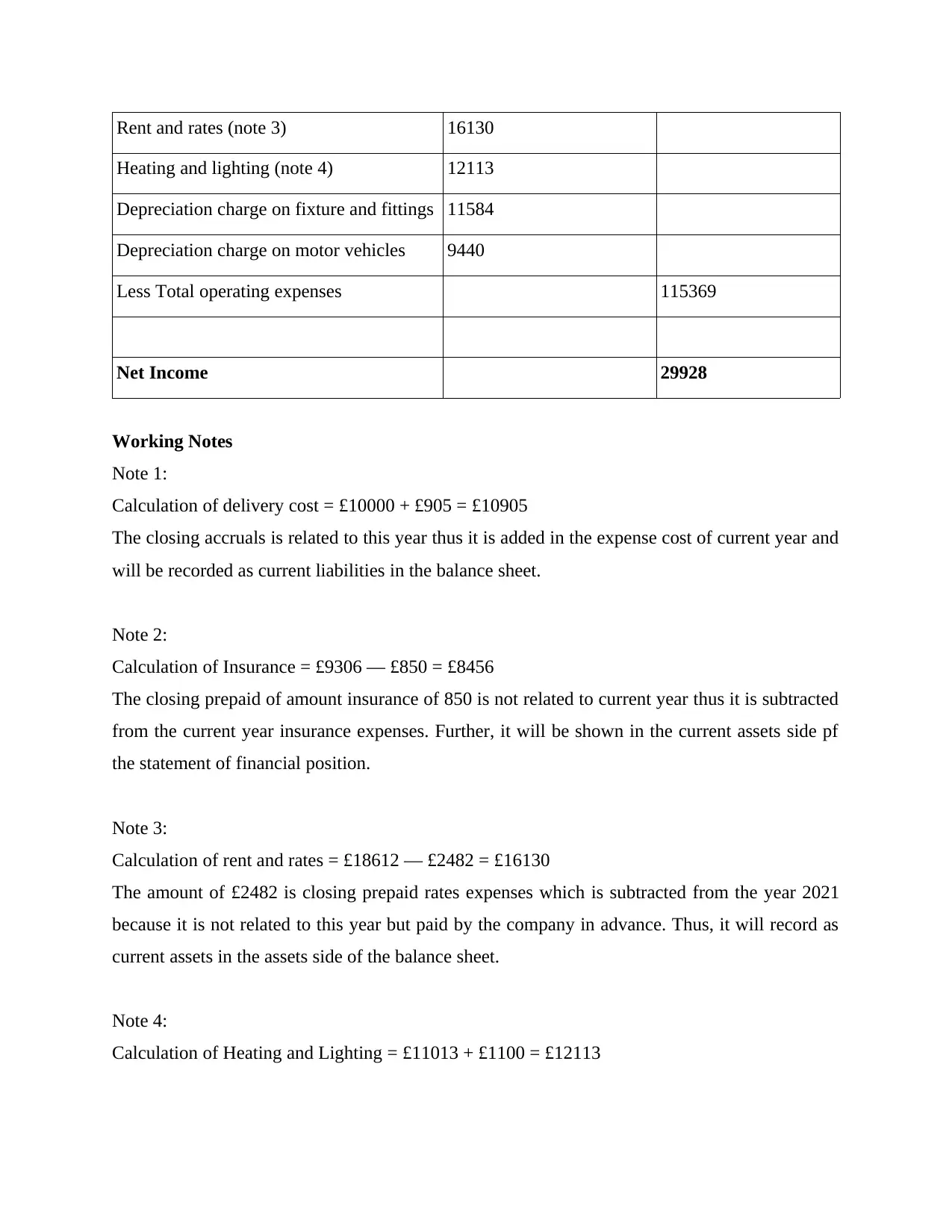

Rent and rates (note 3) 16130

Heating and lighting (note 4) 12113

Depreciation charge on fixture and fittings 11584

Depreciation charge on motor vehicles 9440

Less Total operating expenses 115369

Net Income 29928

Working Notes

Note 1:

Calculation of delivery cost = £10000 + £905 = £10905

The closing accruals is related to this year thus it is added in the expense cost of current year and

will be recorded as current liabilities in the balance sheet.

Note 2:

Calculation of Insurance = £9306 — £850 = £8456

The closing prepaid of amount insurance of 850 is not related to current year thus it is subtracted

from the current year insurance expenses. Further, it will be shown in the current assets side pf

the statement of financial position.

Note 3:

Calculation of rent and rates = £18612 — £2482 = £16130

The amount of £2482 is closing prepaid rates expenses which is subtracted from the year 2021

because it is not related to this year but paid by the company in advance. Thus, it will record as

current assets in the assets side of the balance sheet.

Note 4:

Calculation of Heating and Lighting = £11013 + £1100 = £12113

Heating and lighting (note 4) 12113

Depreciation charge on fixture and fittings 11584

Depreciation charge on motor vehicles 9440

Less Total operating expenses 115369

Net Income 29928

Working Notes

Note 1:

Calculation of delivery cost = £10000 + £905 = £10905

The closing accruals is related to this year thus it is added in the expense cost of current year and

will be recorded as current liabilities in the balance sheet.

Note 2:

Calculation of Insurance = £9306 — £850 = £8456

The closing prepaid of amount insurance of 850 is not related to current year thus it is subtracted

from the current year insurance expenses. Further, it will be shown in the current assets side pf

the statement of financial position.

Note 3:

Calculation of rent and rates = £18612 — £2482 = £16130

The amount of £2482 is closing prepaid rates expenses which is subtracted from the year 2021

because it is not related to this year but paid by the company in advance. Thus, it will record as

current assets in the assets side of the balance sheet.

Note 4:

Calculation of Heating and Lighting = £11013 + £1100 = £12113

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

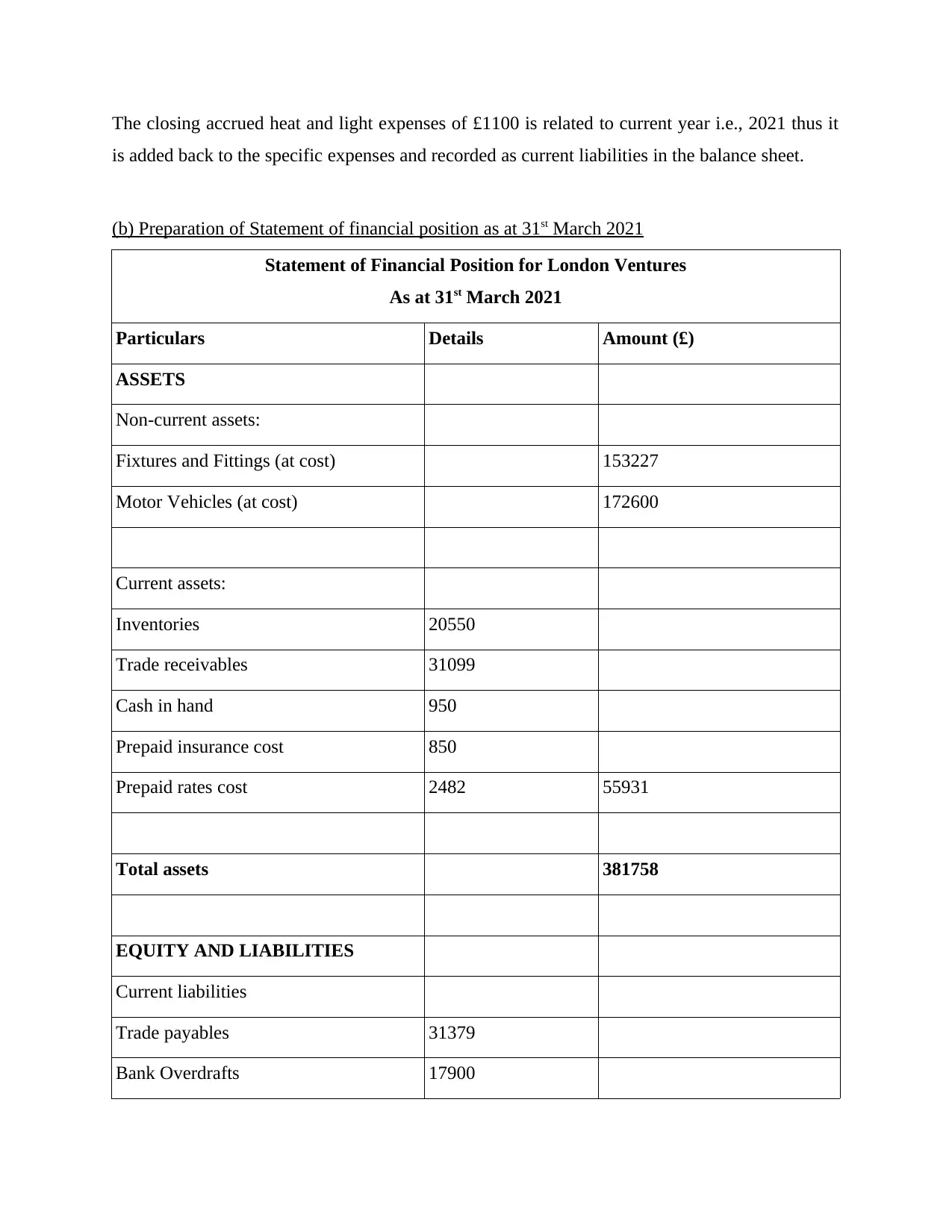

The closing accrued heat and light expenses of £1100 is related to current year i.e., 2021 thus it

is added back to the specific expenses and recorded as current liabilities in the balance sheet.

(b) Preparation of Statement of financial position as at 31st March 2021

Statement of Financial Position for London Ventures

As at 31st March 2021

Particulars Details Amount (£)

ASSETS

Non-current assets:

Fixtures and Fittings (at cost) 153227

Motor Vehicles (at cost) 172600

Current assets:

Inventories 20550

Trade receivables 31099

Cash in hand 950

Prepaid insurance cost 850

Prepaid rates cost 2482 55931

Total assets 381758

EQUITY AND LIABILITIES

Current liabilities

Trade payables 31379

Bank Overdrafts 17900

is added back to the specific expenses and recorded as current liabilities in the balance sheet.

(b) Preparation of Statement of financial position as at 31st March 2021

Statement of Financial Position for London Ventures

As at 31st March 2021

Particulars Details Amount (£)

ASSETS

Non-current assets:

Fixtures and Fittings (at cost) 153227

Motor Vehicles (at cost) 172600

Current assets:

Inventories 20550

Trade receivables 31099

Cash in hand 950

Prepaid insurance cost 850

Prepaid rates cost 2482 55931

Total assets 381758

EQUITY AND LIABILITIES

Current liabilities

Trade payables 31379

Bank Overdrafts 17900

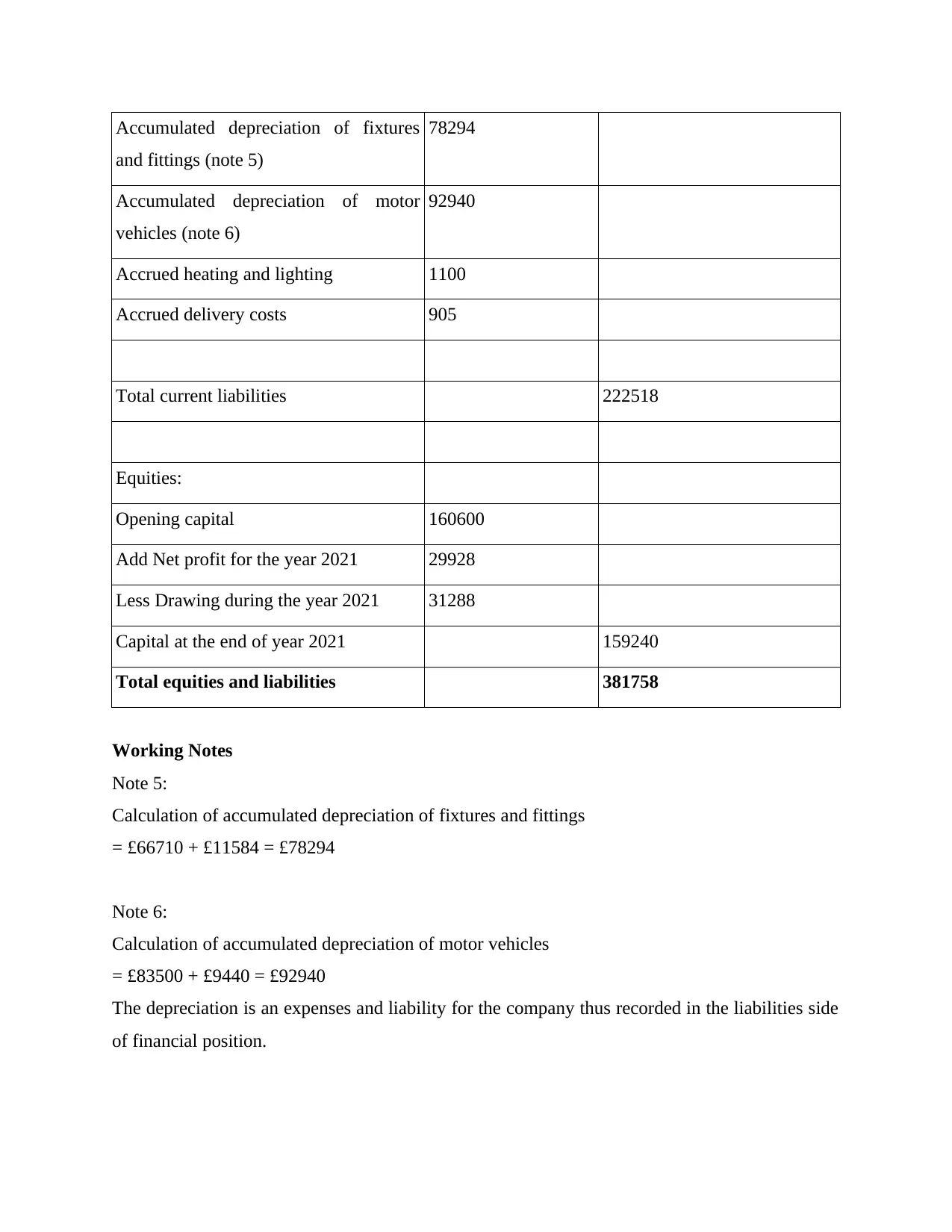

Accumulated depreciation of fixtures

and fittings (note 5)

78294

Accumulated depreciation of motor

vehicles (note 6)

92940

Accrued heating and lighting 1100

Accrued delivery costs 905

Total current liabilities 222518

Equities:

Opening capital 160600

Add Net profit for the year 2021 29928

Less Drawing during the year 2021 31288

Capital at the end of year 2021 159240

Total equities and liabilities 381758

Working Notes

Note 5:

Calculation of accumulated depreciation of fixtures and fittings

= £66710 + £11584 = £78294

Note 6:

Calculation of accumulated depreciation of motor vehicles

= £83500 + £9440 = £92940

The depreciation is an expenses and liability for the company thus recorded in the liabilities side

of financial position.

and fittings (note 5)

78294

Accumulated depreciation of motor

vehicles (note 6)

92940

Accrued heating and lighting 1100

Accrued delivery costs 905

Total current liabilities 222518

Equities:

Opening capital 160600

Add Net profit for the year 2021 29928

Less Drawing during the year 2021 31288

Capital at the end of year 2021 159240

Total equities and liabilities 381758

Working Notes

Note 5:

Calculation of accumulated depreciation of fixtures and fittings

= £66710 + £11584 = £78294

Note 6:

Calculation of accumulated depreciation of motor vehicles

= £83500 + £9440 = £92940

The depreciation is an expenses and liability for the company thus recorded in the liabilities side

of financial position.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

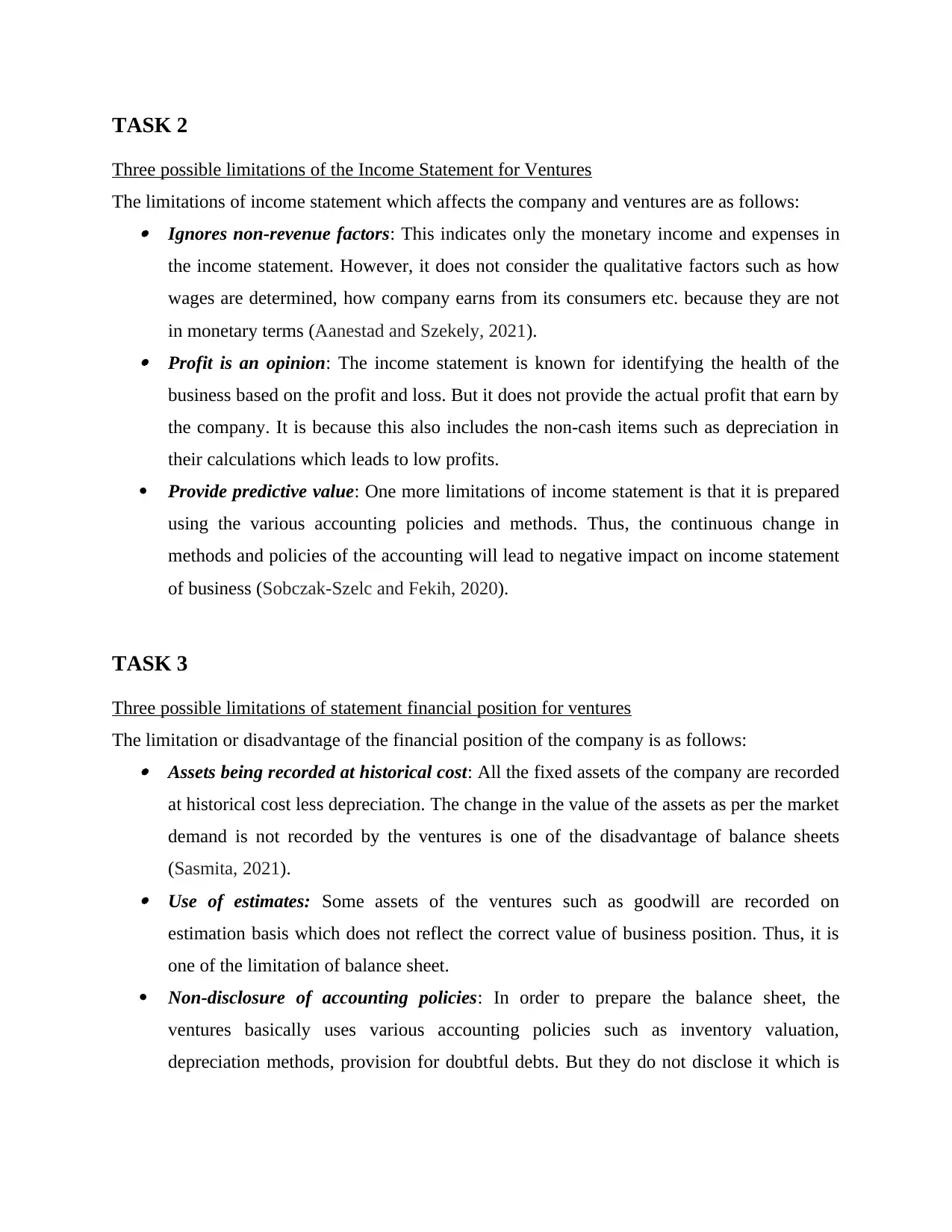

TASK 2

Three possible limitations of the Income Statement for Ventures

The limitations of income statement which affects the company and ventures are as follows: Ignores non-revenue factors: This indicates only the monetary income and expenses in

the income statement. However, it does not consider the qualitative factors such as how

wages are determined, how company earns from its consumers etc. because they are not

in monetary terms (Aanestad and Szekely, 2021). Profit is an opinion: The income statement is known for identifying the health of the

business based on the profit and loss. But it does not provide the actual profit that earn by

the company. It is because this also includes the non-cash items such as depreciation in

their calculations which leads to low profits.

Provide predictive value: One more limitations of income statement is that it is prepared

using the various accounting policies and methods. Thus, the continuous change in

methods and policies of the accounting will lead to negative impact on income statement

of business (Sobczak-Szelc and Fekih, 2020).

TASK 3

Three possible limitations of statement financial position for ventures

The limitation or disadvantage of the financial position of the company is as follows: Assets being recorded at historical cost: All the fixed assets of the company are recorded

at historical cost less depreciation. The change in the value of the assets as per the market

demand is not recorded by the ventures is one of the disadvantage of balance sheets

(Sasmita, 2021). Use of estimates: Some assets of the ventures such as goodwill are recorded on

estimation basis which does not reflect the correct value of business position. Thus, it is

one of the limitation of balance sheet.

Non-disclosure of accounting policies: In order to prepare the balance sheet, the

ventures basically uses various accounting policies such as inventory valuation,

depreciation methods, provision for doubtful debts. But they do not disclose it which is

Three possible limitations of the Income Statement for Ventures

The limitations of income statement which affects the company and ventures are as follows: Ignores non-revenue factors: This indicates only the monetary income and expenses in

the income statement. However, it does not consider the qualitative factors such as how

wages are determined, how company earns from its consumers etc. because they are not

in monetary terms (Aanestad and Szekely, 2021). Profit is an opinion: The income statement is known for identifying the health of the

business based on the profit and loss. But it does not provide the actual profit that earn by

the company. It is because this also includes the non-cash items such as depreciation in

their calculations which leads to low profits.

Provide predictive value: One more limitations of income statement is that it is prepared

using the various accounting policies and methods. Thus, the continuous change in

methods and policies of the accounting will lead to negative impact on income statement

of business (Sobczak-Szelc and Fekih, 2020).

TASK 3

Three possible limitations of statement financial position for ventures

The limitation or disadvantage of the financial position of the company is as follows: Assets being recorded at historical cost: All the fixed assets of the company are recorded

at historical cost less depreciation. The change in the value of the assets as per the market

demand is not recorded by the ventures is one of the disadvantage of balance sheets

(Sasmita, 2021). Use of estimates: Some assets of the ventures such as goodwill are recorded on

estimation basis which does not reflect the correct value of business position. Thus, it is

one of the limitation of balance sheet.

Non-disclosure of accounting policies: In order to prepare the balance sheet, the

ventures basically uses various accounting policies such as inventory valuation,

depreciation methods, provision for doubtful debts. But they do not disclose it which is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

one of the biggest disadvantage of balance sheet that need to be removed by the company

(Plosser, 2018).

TASK 4

Explanation of how London venture company effective manage following efficiency ratios:

(a) Inventory Days

Formula = Total Inventory / Cost of goods sold * 365 days

= £20550 / 145060 × 365 days = 52 days

Recommendation on management of inventory days:

On the basis of calculation of inventory days, it is indicated that the company will hold its

inventory for 52 days in the warehouse. In order to further manage stock holding days, it is

advisable to the London venture that they have to adopt the efficient restocking system such as

EOQ and Just-in-time inventory (Brambilla and et.al., 2018). Along with this, it is also

recommended to the company that they should also use the appropriate marketing strategies

because it helps them in attracting more and more customers which further increase the sales of

the company. One of the key area where the company need to improve its system is delivery or

shipping. It is because delay in shipment of goods and services to the ultimate customers will

leave negative comments on the social media sites and online shopping channels. Proper

forecasting is also one step which helps the London Venture in managing inventory days.

(b) Trade Payable Days

Formula = Trade payable / COGS * 365 days

= £31379 / 145060 × 365 days = 79 days

Recommendation on management of trade payable days:

The high trade payable days will affect the credit worthiness of the London Venture thus

they need to manage and control it. In order to manage trade payable days, it is advisable to the

company that they should negotiate the payment terms with the supplier. Also, the company have

to build the strong relation with its supplier in which they have to make sure that they are paying

them timely (Alarussi, 2021). For this, the company can arrange money from the sale of the

(Plosser, 2018).

TASK 4

Explanation of how London venture company effective manage following efficiency ratios:

(a) Inventory Days

Formula = Total Inventory / Cost of goods sold * 365 days

= £20550 / 145060 × 365 days = 52 days

Recommendation on management of inventory days:

On the basis of calculation of inventory days, it is indicated that the company will hold its

inventory for 52 days in the warehouse. In order to further manage stock holding days, it is

advisable to the London venture that they have to adopt the efficient restocking system such as

EOQ and Just-in-time inventory (Brambilla and et.al., 2018). Along with this, it is also

recommended to the company that they should also use the appropriate marketing strategies

because it helps them in attracting more and more customers which further increase the sales of

the company. One of the key area where the company need to improve its system is delivery or

shipping. It is because delay in shipment of goods and services to the ultimate customers will

leave negative comments on the social media sites and online shopping channels. Proper

forecasting is also one step which helps the London Venture in managing inventory days.

(b) Trade Payable Days

Formula = Trade payable / COGS * 365 days

= £31379 / 145060 × 365 days = 79 days

Recommendation on management of trade payable days:

The high trade payable days will affect the credit worthiness of the London Venture thus

they need to manage and control it. In order to manage trade payable days, it is advisable to the

company that they should negotiate the payment terms with the supplier. Also, the company have

to build the strong relation with its supplier in which they have to make sure that they are paying

them timely (Alarussi, 2021). For this, the company can arrange money from the sale of the

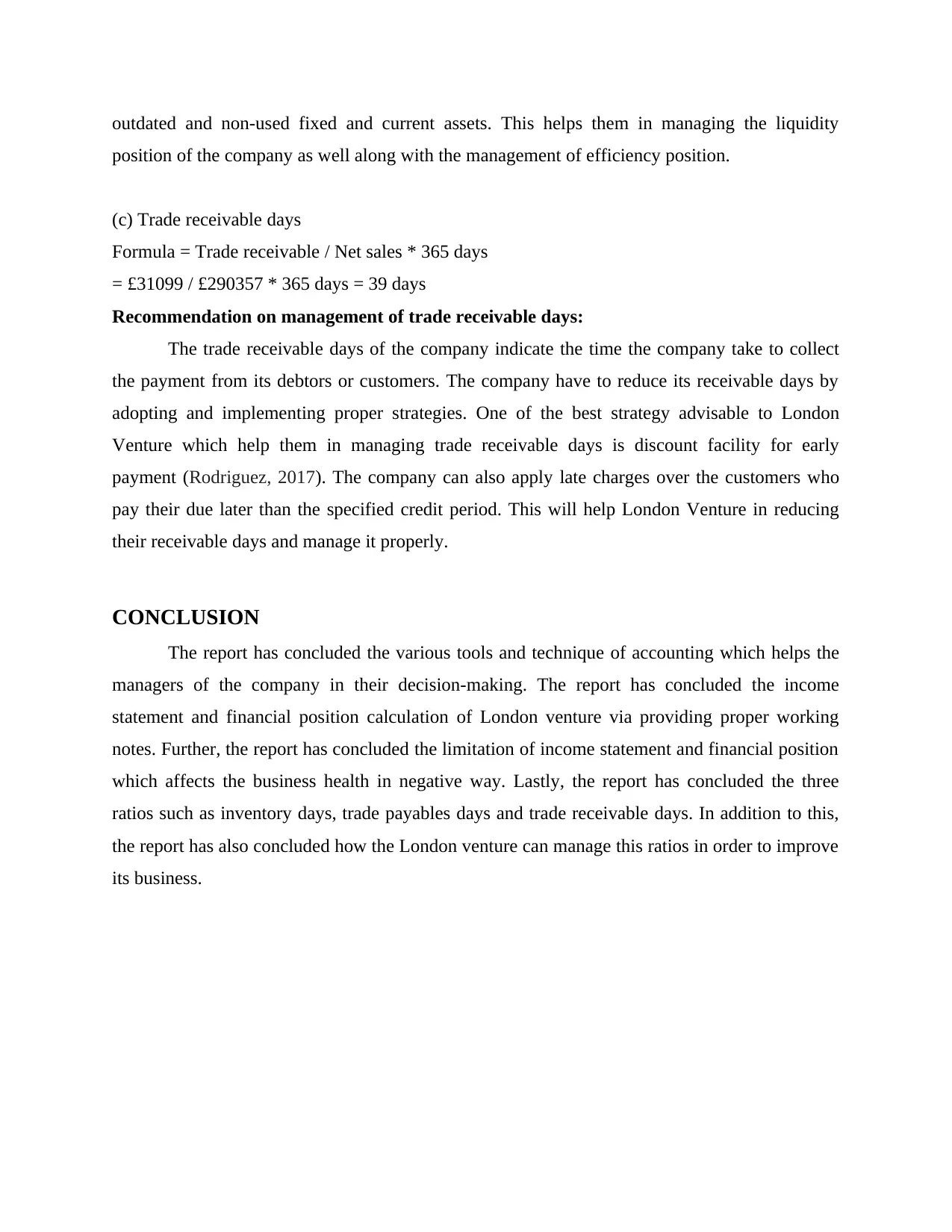

outdated and non-used fixed and current assets. This helps them in managing the liquidity

position of the company as well along with the management of efficiency position.

(c) Trade receivable days

Formula = Trade receivable / Net sales * 365 days

= £31099 / £290357 * 365 days = 39 days

Recommendation on management of trade receivable days:

The trade receivable days of the company indicate the time the company take to collect

the payment from its debtors or customers. The company have to reduce its receivable days by

adopting and implementing proper strategies. One of the best strategy advisable to London

Venture which help them in managing trade receivable days is discount facility for early

payment (Rodriguez, 2017). The company can also apply late charges over the customers who

pay their due later than the specified credit period. This will help London Venture in reducing

their receivable days and manage it properly.

CONCLUSION

The report has concluded the various tools and technique of accounting which helps the

managers of the company in their decision-making. The report has concluded the income

statement and financial position calculation of London venture via providing proper working

notes. Further, the report has concluded the limitation of income statement and financial position

which affects the business health in negative way. Lastly, the report has concluded the three

ratios such as inventory days, trade payables days and trade receivable days. In addition to this,

the report has also concluded how the London venture can manage this ratios in order to improve

its business.

position of the company as well along with the management of efficiency position.

(c) Trade receivable days

Formula = Trade receivable / Net sales * 365 days

= £31099 / £290357 * 365 days = 39 days

Recommendation on management of trade receivable days:

The trade receivable days of the company indicate the time the company take to collect

the payment from its debtors or customers. The company have to reduce its receivable days by

adopting and implementing proper strategies. One of the best strategy advisable to London

Venture which help them in managing trade receivable days is discount facility for early

payment (Rodriguez, 2017). The company can also apply late charges over the customers who

pay their due later than the specified credit period. This will help London Venture in reducing

their receivable days and manage it properly.

CONCLUSION

The report has concluded the various tools and technique of accounting which helps the

managers of the company in their decision-making. The report has concluded the income

statement and financial position calculation of London venture via providing proper working

notes. Further, the report has concluded the limitation of income statement and financial position

which affects the business health in negative way. Lastly, the report has concluded the three

ratios such as inventory days, trade payables days and trade receivable days. In addition to this,

the report has also concluded how the London venture can manage this ratios in order to improve

its business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Aanestad, H. and Szekely, N., 2021. Understanding the Norwegian additive manufacturing

market: Its attractive aspects, limitations, potential and future opportunities within a

circular framework (Master's thesis, uis).

Sobczak-Szelc, K. and Fekih, N., 2020. Migration as one of several adaptation strategies for

environmental limitations in Tunisia: evidence from El Faouar. Comparative Migration

Studies. 8(1). pp.1-20.

Sasmita, R. P. H., 2021. Off-Balance Sheet Analysis Toward Risk-Adjusted Performance. The

Indonesian Journal of Accounting Research. 24(1).

Plosser, C. I., 2018. The risks of a Fed balance sheet unconstrained by monetary policy. The

Structural Foundations of Monetary Policy, pp.1-16.

Brambilla, A. and et.al., 2018. Life cycle efficiency ratio: A new performance indicator for a life

cycle driven approach to evaluate the potential of ventilative cooling and thermal

inertia. Energy and Buildings. 163. pp.22-33.

Alarussi, A. S. A., 2021. Financial ratios and efficiency in Malaysian listed companies. Asian

Journal of Economics and Banking.

Rodriguez, I. F., 2017. Music Tempo and Manufacturing Efficiency Ratio: An Experimental

Research. J Glob Econ. 4(232). p.2.

Books and Journals

Aanestad, H. and Szekely, N., 2021. Understanding the Norwegian additive manufacturing

market: Its attractive aspects, limitations, potential and future opportunities within a

circular framework (Master's thesis, uis).

Sobczak-Szelc, K. and Fekih, N., 2020. Migration as one of several adaptation strategies for

environmental limitations in Tunisia: evidence from El Faouar. Comparative Migration

Studies. 8(1). pp.1-20.

Sasmita, R. P. H., 2021. Off-Balance Sheet Analysis Toward Risk-Adjusted Performance. The

Indonesian Journal of Accounting Research. 24(1).

Plosser, C. I., 2018. The risks of a Fed balance sheet unconstrained by monetary policy. The

Structural Foundations of Monetary Policy, pp.1-16.

Brambilla, A. and et.al., 2018. Life cycle efficiency ratio: A new performance indicator for a life

cycle driven approach to evaluate the potential of ventilative cooling and thermal

inertia. Energy and Buildings. 163. pp.22-33.

Alarussi, A. S. A., 2021. Financial ratios and efficiency in Malaysian listed companies. Asian

Journal of Economics and Banking.

Rodriguez, I. F., 2017. Music Tempo and Manufacturing Efficiency Ratio: An Experimental

Research. J Glob Econ. 4(232). p.2.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.