Business Decision Making Essay: Investment Appraisal at XYZ plc

VerifiedAdded on 2023/01/11

|8

|1313

|24

Essay

AI Summary

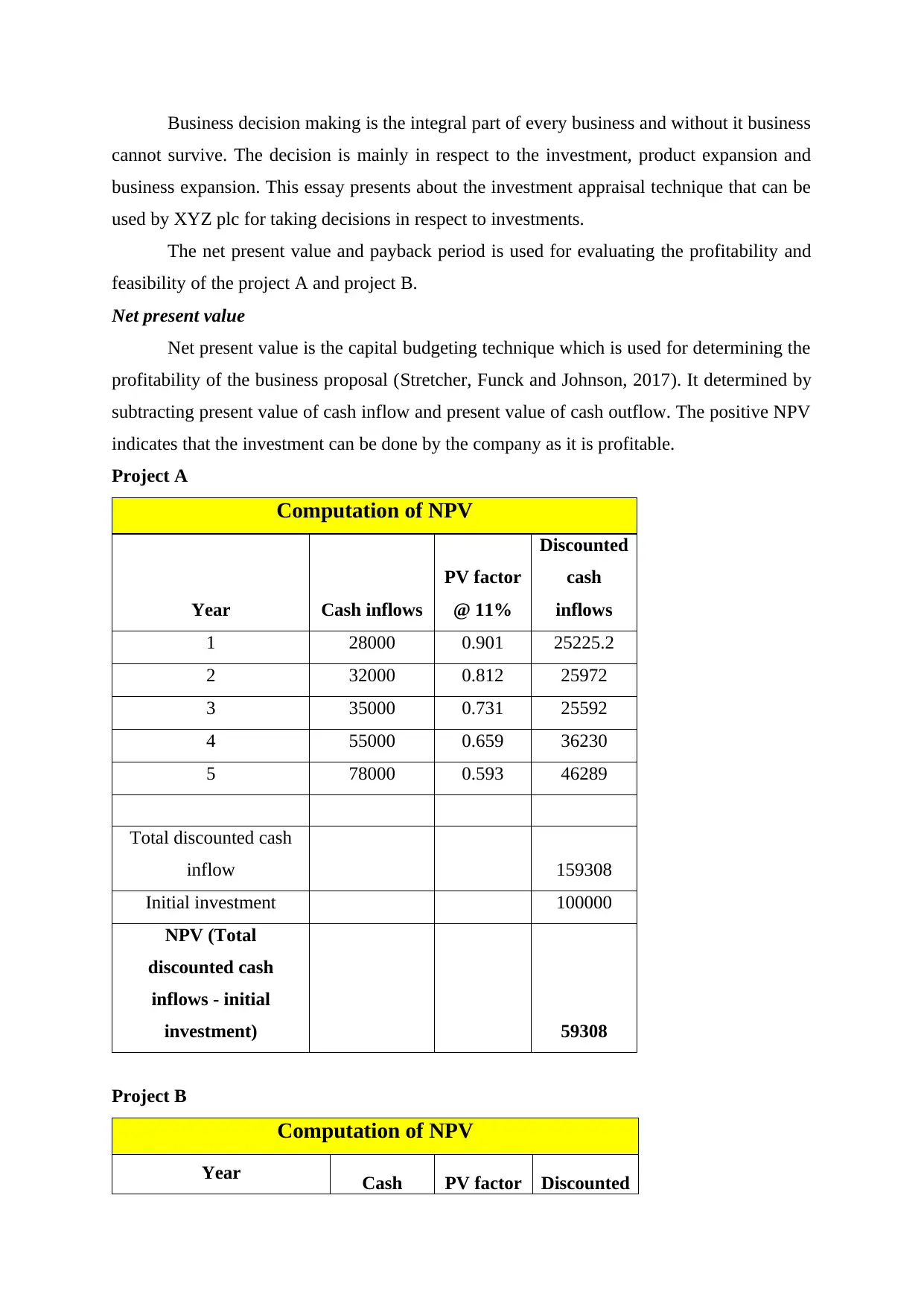

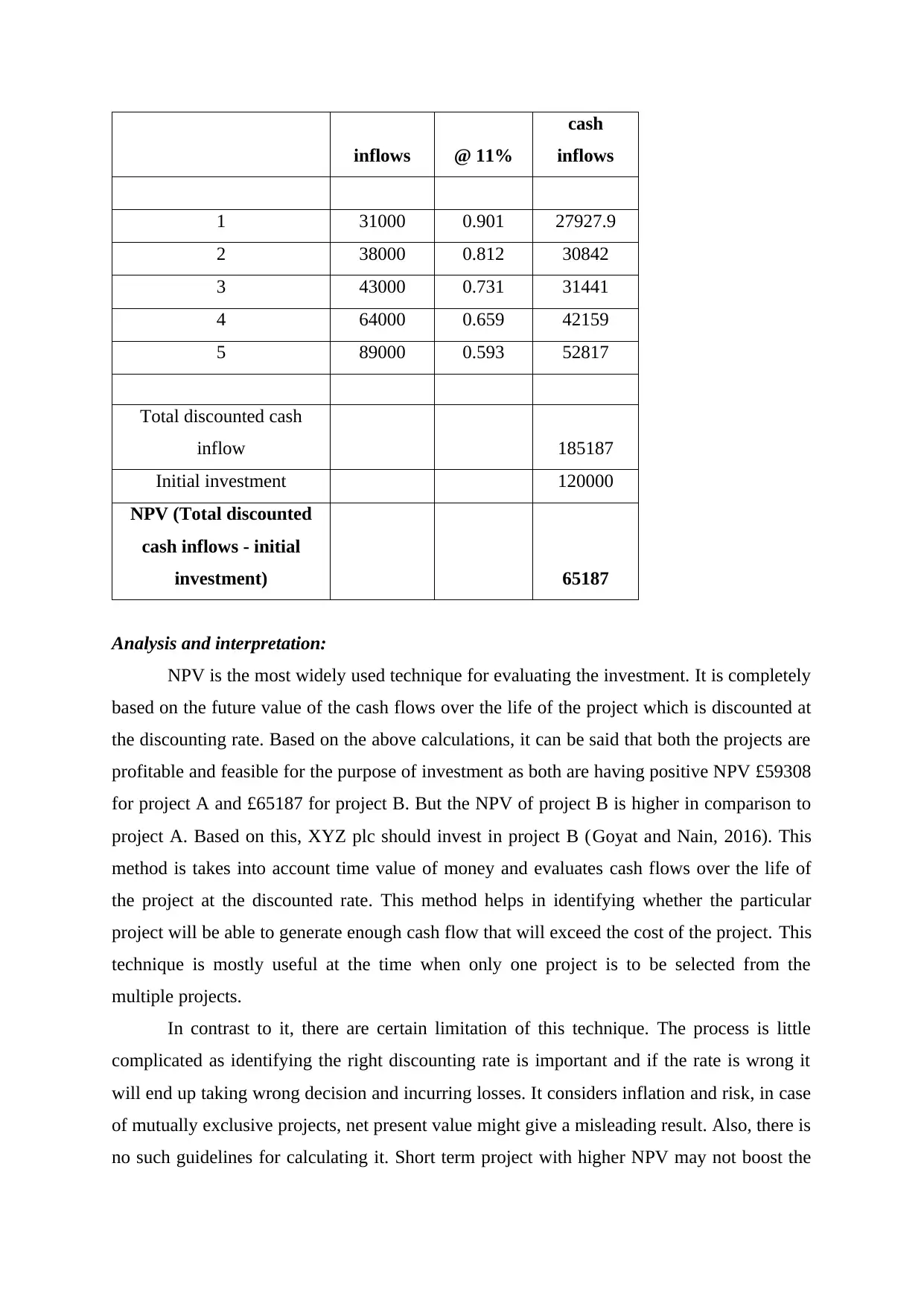

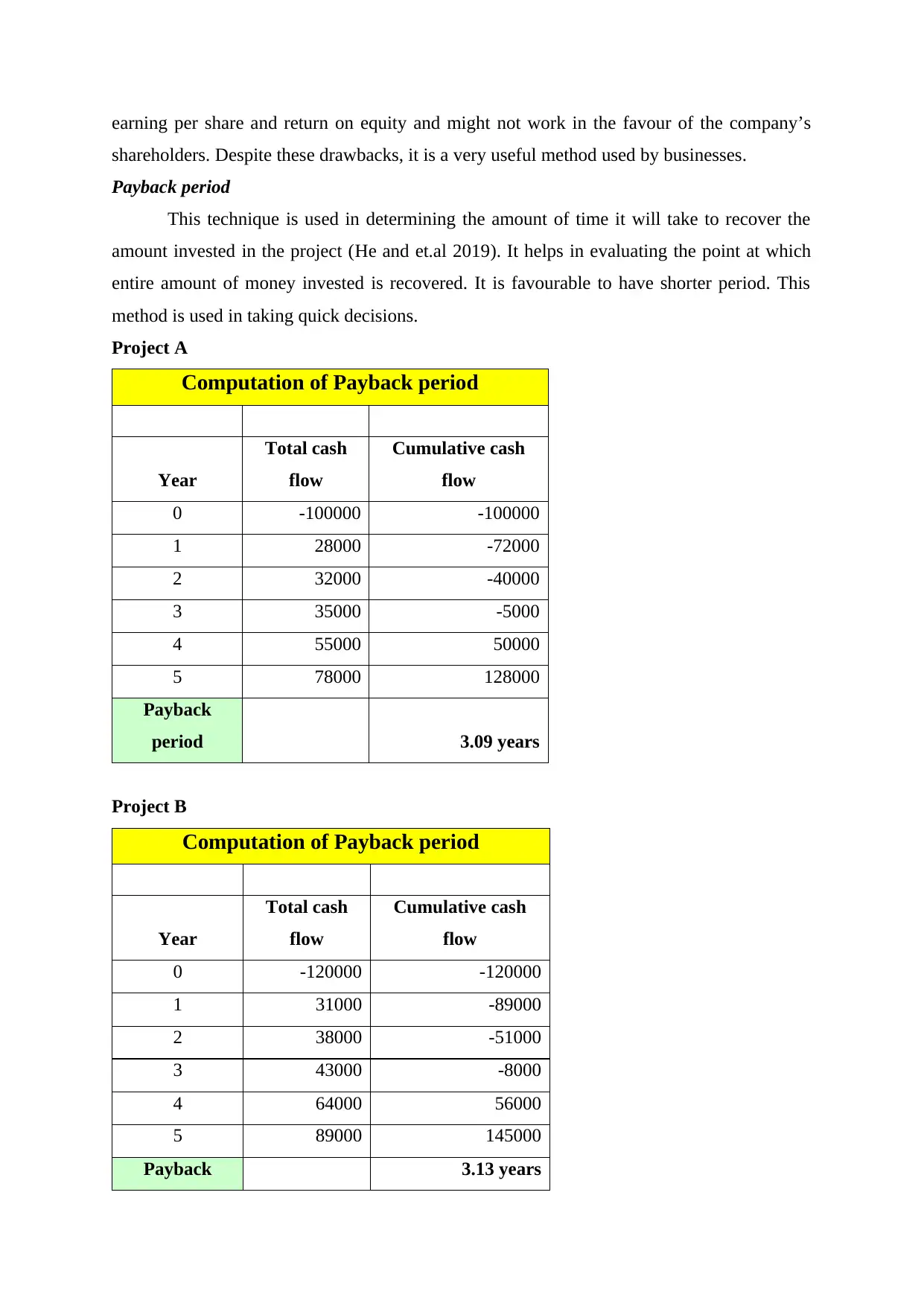

This essay examines the crucial role of business decision-making in the success of companies. It focuses on investment appraisal techniques, specifically net present value (NPV) and payback period, to evaluate the profitability and feasibility of potential projects. The essay presents a case study of XYZ plc, analyzing two projects, A and B, using these techniques. The NPV analysis reveals that both projects are profitable, with project B showing a higher NPV. The payback period analysis indicates project A is more feasible. However, the essay highlights the limitations of the payback period and concludes that, based on the NPV, project B is the better investment. Furthermore, the essay discusses the importance of non-financial factors, such as compliance with regulations, industry standards, community relations, market conditions, and staff morale, in comprehensive business decision-making. The essay emphasizes that while financial metrics are vital, a holistic approach considering both financial and non-financial aspects is essential for sound investment decisions.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.