Business Finance: Investment Appraisal and Ratio Analysis Case Study

VerifiedAdded on 2023/06/10

|10

|2584

|421

Case Study

AI Summary

This case study provides a comprehensive financial analysis of Jessica Ltd's investment opportunity and Omega Ltd's financial performance. It includes calculations of the payback period, net present value (NPV), and internal rate of return (IRR) to advise Jessica Ltd on the suitability of an online market investment. Furthermore, it calculates and interprets accounting ratios such as current ratio, quick ratio, debt-equity ratio, interest coverage ratio, stock turnover ratio, debtors turnover ratio, creditors turnover ratio and net profit ratio for Omega Ltd, accompanied by a risk assessment based on these ratios. The study also identifies and evaluates non-financial performance indicators like customer satisfaction, retention, and brand reputation for Omega Ltd, and discusses the impact of Salesforce's price skimming strategy on its performance. Desklib provides access to this and many other solved assignments for students.

Business Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

MAIN BODY..................................................................................................................................3

2: A Case Study...............................................................................................................................3

Advising Jessica Ltd regarding the suitability of the investment opportunity............................4

b.......................................................................................................................................................5

Calculation of accounting ratios..................................................................................................5

Report of Risk Assessment..........................................................................................................6

Identifying and evaluating non-financial performance indicators for Omega Ltd......................7

Impact of Pricing Strategy on the performance of Salesforce.....................................................8

REFERENCES................................................................................................................................1

MAIN BODY..................................................................................................................................3

2: A Case Study...............................................................................................................................3

Advising Jessica Ltd regarding the suitability of the investment opportunity............................4

b.......................................................................................................................................................5

Calculation of accounting ratios..................................................................................................5

Report of Risk Assessment..........................................................................................................6

Identifying and evaluating non-financial performance indicators for Omega Ltd......................7

Impact of Pricing Strategy on the performance of Salesforce.....................................................8

REFERENCES................................................................................................................................1

MAIN BODY

2: A Case Study

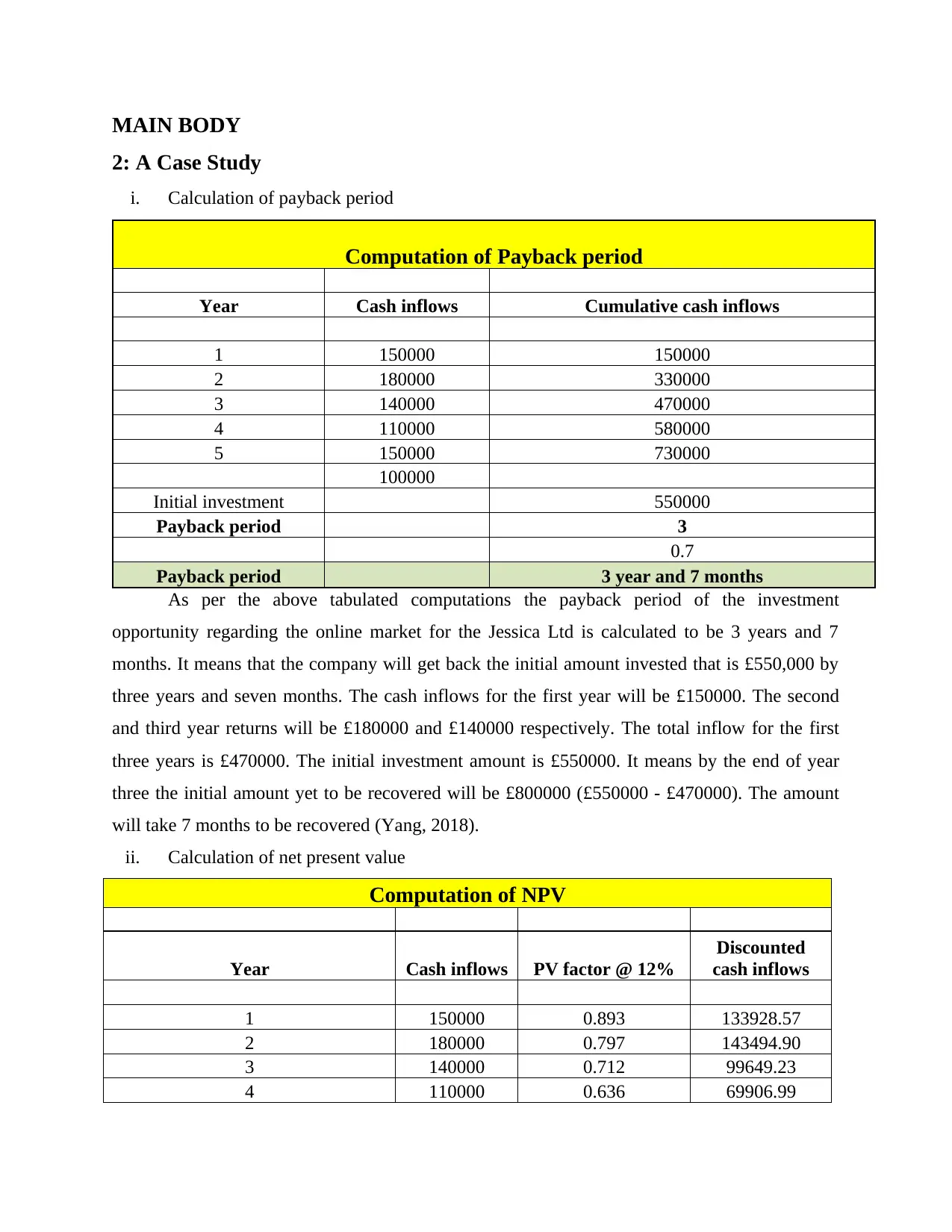

i. Calculation of payback period

Computation of Payback period

Year Cash inflows Cumulative cash inflows

1 150000 150000

2 180000 330000

3 140000 470000

4 110000 580000

5 150000 730000

100000

Initial investment 550000

Payback period 3

0.7

Payback period 3 year and 7 months

As per the above tabulated computations the payback period of the investment

opportunity regarding the online market for the Jessica Ltd is calculated to be 3 years and 7

months. It means that the company will get back the initial amount invested that is £550,000 by

three years and seven months. The cash inflows for the first year will be £150000. The second

and third year returns will be £180000 and £140000 respectively. The total inflow for the first

three years is £470000. The initial investment amount is £550000. It means by the end of year

three the initial amount yet to be recovered will be £800000 (£550000 - £470000). The amount

will take 7 months to be recovered (Yang, 2018).

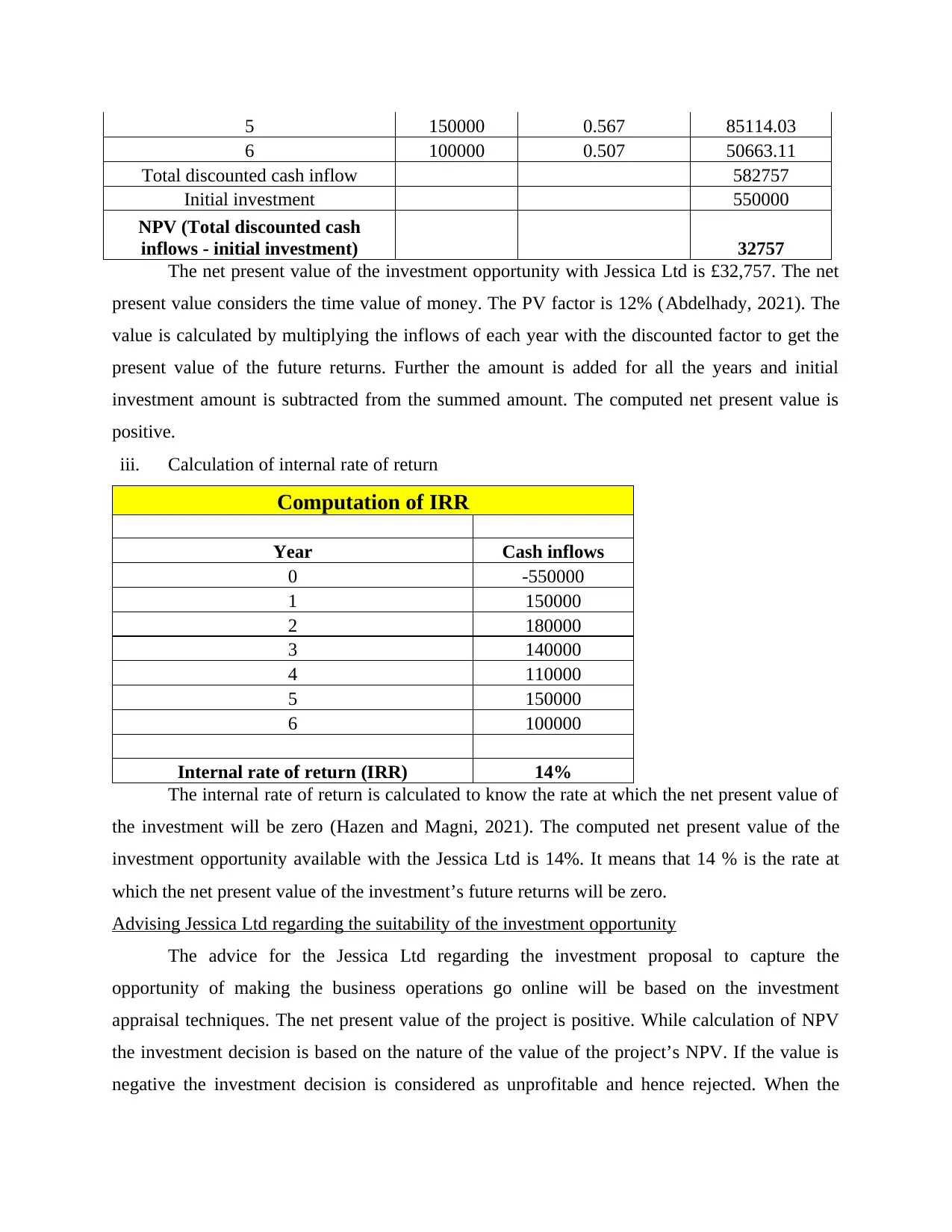

ii. Calculation of net present value

Computation of NPV

Year Cash inflows PV factor @ 12%

Discounted

cash inflows

1 150000 0.893 133928.57

2 180000 0.797 143494.90

3 140000 0.712 99649.23

4 110000 0.636 69906.99

2: A Case Study

i. Calculation of payback period

Computation of Payback period

Year Cash inflows Cumulative cash inflows

1 150000 150000

2 180000 330000

3 140000 470000

4 110000 580000

5 150000 730000

100000

Initial investment 550000

Payback period 3

0.7

Payback period 3 year and 7 months

As per the above tabulated computations the payback period of the investment

opportunity regarding the online market for the Jessica Ltd is calculated to be 3 years and 7

months. It means that the company will get back the initial amount invested that is £550,000 by

three years and seven months. The cash inflows for the first year will be £150000. The second

and third year returns will be £180000 and £140000 respectively. The total inflow for the first

three years is £470000. The initial investment amount is £550000. It means by the end of year

three the initial amount yet to be recovered will be £800000 (£550000 - £470000). The amount

will take 7 months to be recovered (Yang, 2018).

ii. Calculation of net present value

Computation of NPV

Year Cash inflows PV factor @ 12%

Discounted

cash inflows

1 150000 0.893 133928.57

2 180000 0.797 143494.90

3 140000 0.712 99649.23

4 110000 0.636 69906.99

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

5 150000 0.567 85114.03

6 100000 0.507 50663.11

Total discounted cash inflow 582757

Initial investment 550000

NPV (Total discounted cash

inflows - initial investment) 32757

The net present value of the investment opportunity with Jessica Ltd is £32,757. The net

present value considers the time value of money. The PV factor is 12% (Abdelhady, 2021). The

value is calculated by multiplying the inflows of each year with the discounted factor to get the

present value of the future returns. Further the amount is added for all the years and initial

investment amount is subtracted from the summed amount. The computed net present value is

positive.

iii. Calculation of internal rate of return

Computation of IRR

Year Cash inflows

0 -550000

1 150000

2 180000

3 140000

4 110000

5 150000

6 100000

Internal rate of return (IRR) 14%

The internal rate of return is calculated to know the rate at which the net present value of

the investment will be zero (Hazen and Magni, 2021). The computed net present value of the

investment opportunity available with the Jessica Ltd is 14%. It means that 14 % is the rate at

which the net present value of the investment’s future returns will be zero.

Advising Jessica Ltd regarding the suitability of the investment opportunity

The advice for the Jessica Ltd regarding the investment proposal to capture the

opportunity of making the business operations go online will be based on the investment

appraisal techniques. The net present value of the project is positive. While calculation of NPV

the investment decision is based on the nature of the value of the project’s NPV. If the value is

negative the investment decision is considered as unprofitable and hence rejected. When the

6 100000 0.507 50663.11

Total discounted cash inflow 582757

Initial investment 550000

NPV (Total discounted cash

inflows - initial investment) 32757

The net present value of the investment opportunity with Jessica Ltd is £32,757. The net

present value considers the time value of money. The PV factor is 12% (Abdelhady, 2021). The

value is calculated by multiplying the inflows of each year with the discounted factor to get the

present value of the future returns. Further the amount is added for all the years and initial

investment amount is subtracted from the summed amount. The computed net present value is

positive.

iii. Calculation of internal rate of return

Computation of IRR

Year Cash inflows

0 -550000

1 150000

2 180000

3 140000

4 110000

5 150000

6 100000

Internal rate of return (IRR) 14%

The internal rate of return is calculated to know the rate at which the net present value of

the investment will be zero (Hazen and Magni, 2021). The computed net present value of the

investment opportunity available with the Jessica Ltd is 14%. It means that 14 % is the rate at

which the net present value of the investment’s future returns will be zero.

Advising Jessica Ltd regarding the suitability of the investment opportunity

The advice for the Jessica Ltd regarding the investment proposal to capture the

opportunity of making the business operations go online will be based on the investment

appraisal techniques. The net present value of the project is positive. While calculation of NPV

the investment decision is based on the nature of the value of the project’s NPV. If the value is

negative the investment decision is considered as unprofitable and hence rejected. When the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

NPV is equivalent to zero the investment decision is neither advantageous nor disadvantageous.

In such a case the project is rejected and the project that is profitable is considered for making

investment. The NPV of the investment opportunity with Jessica Ltd is positive it means that the

profit is profitable (Investment Appraisal Techniques, 2022). The internal rate of return is

considered good if it is higher. IRR of the investment opportunity is 14 % which is high. Also,

the payback period calculation represents that the project’s initial amount invested will be

recovered with a duration of less than four years. So as per the computed results of the payback

period, net present value and internal rate of return it is recommended for the Jessica Ltd to

undertake the investment opportunity.

b.

Calculation of accounting ratios

Particulars Formula 2021

Current Ratio Current Assets/Current Liabilities 2.27

Current Assets 111000

Current Liabilities 49000

Quick Ratio Liquid Assets/Current Liabilities 1.04

Liquid Assets

Current Assets - inventories - prepaid

expenses 51000

Inventories 60000

Prepaid Expenses 0

Current Liabilities 49000

Debt Equity Ratio

Total Long Term Debts / Shareholders

Fund 1.14

Total Long Term Debts 400000

Shareholders Fund

Equity Share Capital + Reserves and

Surpluses + 5% preference share

capital 352000

Equity Share Capital 210000

Reserves and Surpluses 90000

5% preference share capital 52000

Interest Coverage Ratio

Earnings before Interest, Taxes,

Depreciation, and Amortization /

Interest Expense 53.75

Earnings before Interest, Taxes,

Depreciation, and Amortization

Gross Profit - Rent Expense -

Administration Expenses 215000

Interest Expense 4000

Gross Profit 300000

Rent Expense 60000

Administration Expenses 25000

In such a case the project is rejected and the project that is profitable is considered for making

investment. The NPV of the investment opportunity with Jessica Ltd is positive it means that the

profit is profitable (Investment Appraisal Techniques, 2022). The internal rate of return is

considered good if it is higher. IRR of the investment opportunity is 14 % which is high. Also,

the payback period calculation represents that the project’s initial amount invested will be

recovered with a duration of less than four years. So as per the computed results of the payback

period, net present value and internal rate of return it is recommended for the Jessica Ltd to

undertake the investment opportunity.

b.

Calculation of accounting ratios

Particulars Formula 2021

Current Ratio Current Assets/Current Liabilities 2.27

Current Assets 111000

Current Liabilities 49000

Quick Ratio Liquid Assets/Current Liabilities 1.04

Liquid Assets

Current Assets - inventories - prepaid

expenses 51000

Inventories 60000

Prepaid Expenses 0

Current Liabilities 49000

Debt Equity Ratio

Total Long Term Debts / Shareholders

Fund 1.14

Total Long Term Debts 400000

Shareholders Fund

Equity Share Capital + Reserves and

Surpluses + 5% preference share

capital 352000

Equity Share Capital 210000

Reserves and Surpluses 90000

5% preference share capital 52000

Interest Coverage Ratio

Earnings before Interest, Taxes,

Depreciation, and Amortization /

Interest Expense 53.75

Earnings before Interest, Taxes,

Depreciation, and Amortization

Gross Profit - Rent Expense -

Administration Expenses 215000

Interest Expense 4000

Gross Profit 300000

Rent Expense 60000

Administration Expenses 25000

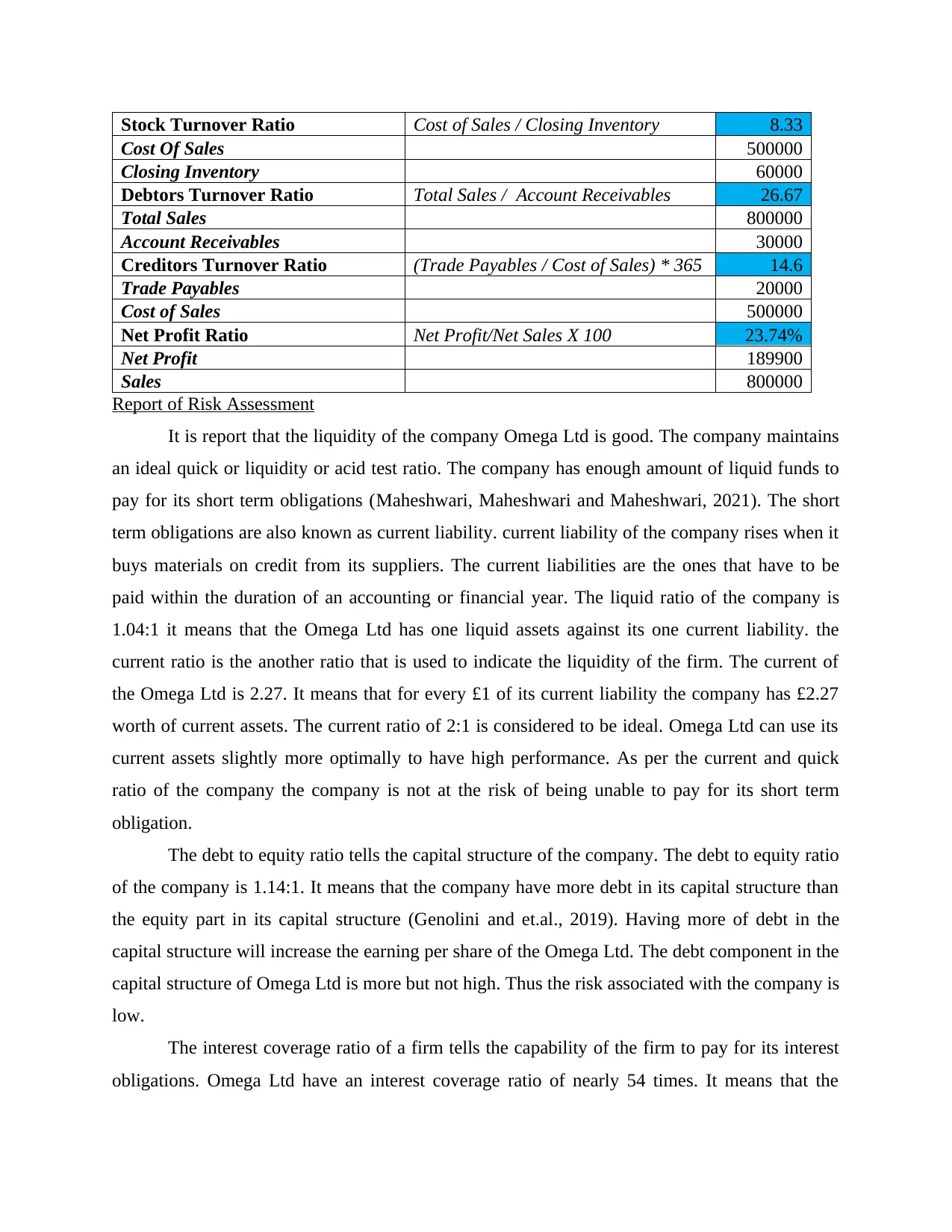

Stock Turnover Ratio Cost of Sales / Closing Inventory 8.33

Cost Of Sales 500000

Closing Inventory 60000

Debtors Turnover Ratio Total Sales / Account Receivables 26.67

Total Sales 800000

Account Receivables 30000

Creditors Turnover Ratio (Trade Payables / Cost of Sales) * 365 14.6

Trade Payables 20000

Cost of Sales 500000

Net Profit Ratio Net Profit/Net Sales X 100 23.74%

Net Profit 189900

Sales 800000

Report of Risk Assessment

It is report that the liquidity of the company Omega Ltd is good. The company maintains

an ideal quick or liquidity or acid test ratio. The company has enough amount of liquid funds to

pay for its short term obligations (Maheshwari, Maheshwari and Maheshwari, 2021). The short

term obligations are also known as current liability. current liability of the company rises when it

buys materials on credit from its suppliers. The current liabilities are the ones that have to be

paid within the duration of an accounting or financial year. The liquid ratio of the company is

1.04:1 it means that the Omega Ltd has one liquid assets against its one current liability. the

current ratio is the another ratio that is used to indicate the liquidity of the firm. The current of

the Omega Ltd is 2.27. It means that for every £1 of its current liability the company has £2.27

worth of current assets. The current ratio of 2:1 is considered to be ideal. Omega Ltd can use its

current assets slightly more optimally to have high performance. As per the current and quick

ratio of the company the company is not at the risk of being unable to pay for its short term

obligation.

The debt to equity ratio tells the capital structure of the company. The debt to equity ratio

of the company is 1.14:1. It means that the company have more debt in its capital structure than

the equity part in its capital structure (Genolini and et.al., 2019). Having more of debt in the

capital structure will increase the earning per share of the Omega Ltd. The debt component in the

capital structure of Omega Ltd is more but not high. Thus the risk associated with the company is

low.

The interest coverage ratio of a firm tells the capability of the firm to pay for its interest

obligations. Omega Ltd have an interest coverage ratio of nearly 54 times. It means that the

Cost Of Sales 500000

Closing Inventory 60000

Debtors Turnover Ratio Total Sales / Account Receivables 26.67

Total Sales 800000

Account Receivables 30000

Creditors Turnover Ratio (Trade Payables / Cost of Sales) * 365 14.6

Trade Payables 20000

Cost of Sales 500000

Net Profit Ratio Net Profit/Net Sales X 100 23.74%

Net Profit 189900

Sales 800000

Report of Risk Assessment

It is report that the liquidity of the company Omega Ltd is good. The company maintains

an ideal quick or liquidity or acid test ratio. The company has enough amount of liquid funds to

pay for its short term obligations (Maheshwari, Maheshwari and Maheshwari, 2021). The short

term obligations are also known as current liability. current liability of the company rises when it

buys materials on credit from its suppliers. The current liabilities are the ones that have to be

paid within the duration of an accounting or financial year. The liquid ratio of the company is

1.04:1 it means that the Omega Ltd has one liquid assets against its one current liability. the

current ratio is the another ratio that is used to indicate the liquidity of the firm. The current of

the Omega Ltd is 2.27. It means that for every £1 of its current liability the company has £2.27

worth of current assets. The current ratio of 2:1 is considered to be ideal. Omega Ltd can use its

current assets slightly more optimally to have high performance. As per the current and quick

ratio of the company the company is not at the risk of being unable to pay for its short term

obligation.

The debt to equity ratio tells the capital structure of the company. The debt to equity ratio

of the company is 1.14:1. It means that the company have more debt in its capital structure than

the equity part in its capital structure (Genolini and et.al., 2019). Having more of debt in the

capital structure will increase the earning per share of the Omega Ltd. The debt component in the

capital structure of Omega Ltd is more but not high. Thus the risk associated with the company is

low.

The interest coverage ratio of a firm tells the capability of the firm to pay for its interest

obligations. Omega Ltd have an interest coverage ratio of nearly 54 times. It means that the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

profit of the firm before it pays of its interest and tax obligations and provide for the depreciation

and amortization charges is sufficient enough to pay for the interest obligations fifty-four times.

The company is at low risk.

The stock turnover ratio of the company tells about the number of times the entire

inventory of the company gets replaced within an accounting year (Accounting Ratios, 2022).

The computed stock turnover ratio of the Omega Ltd is 8 times approximately. This indicates

high sales are being held by the company. The company is capable of selling in large volumes

through the year. The risk of low sales is low for the company.

Debtors turnover ratio give the computed result in number of days or months. In this

report it has been calculated in the number of days. The debtors’ turnover ratio of the Omega Ltd

is 27 days. It means that the company get back the sales revenue for the goods sold to its

customers within the duration of 27 days that is less than a month. It means that the risk of

Omega Ltd.’s debtors converting into bad debtors is low. The company is efficient enough to get

the due amount from its debtors against the credit purchases made by them timely.

The creditor turnover ratio of a company gives information about the average time taken

by the company to pay back its suppliers for the materials purchased on credit. The creditors

turnover ratio of Omega Ltd is around 15 days. It means that when the company purchase

materials on credit from the suppliers it pays the amount back to its suppliers within 15 days. The

risk of default in payments is also low for the company.

The net profit ratio of the company is 24% approximately. Omega Ltd holds a good

profitability. Net profit ratio is the percentage of sales revenue left with the company after paying

for all of its expenses.

Identifying and evaluating non-financial performance indicators for Omega Ltd.

Non-financial indicators are those indicators that reflects the performance of the company

on the basis of the factors that cannot be expressed in the monetary terms but affects the financial

performance of the company. The non-financial factors that can be assessed for knowing the

performance of Omega Ltd are:

Customer Satisfaction and Retention: The non-financial performance indicator of

customer satisfaction and retention is linked to each other. A company having higher level of

customer satisfaction and high customer retention rates is considered to be performing well. The

consumer satisfaction is higher when the experience it has with the usage of product is high (Al-

and amortization charges is sufficient enough to pay for the interest obligations fifty-four times.

The company is at low risk.

The stock turnover ratio of the company tells about the number of times the entire

inventory of the company gets replaced within an accounting year (Accounting Ratios, 2022).

The computed stock turnover ratio of the Omega Ltd is 8 times approximately. This indicates

high sales are being held by the company. The company is capable of selling in large volumes

through the year. The risk of low sales is low for the company.

Debtors turnover ratio give the computed result in number of days or months. In this

report it has been calculated in the number of days. The debtors’ turnover ratio of the Omega Ltd

is 27 days. It means that the company get back the sales revenue for the goods sold to its

customers within the duration of 27 days that is less than a month. It means that the risk of

Omega Ltd.’s debtors converting into bad debtors is low. The company is efficient enough to get

the due amount from its debtors against the credit purchases made by them timely.

The creditor turnover ratio of a company gives information about the average time taken

by the company to pay back its suppliers for the materials purchased on credit. The creditors

turnover ratio of Omega Ltd is around 15 days. It means that when the company purchase

materials on credit from the suppliers it pays the amount back to its suppliers within 15 days. The

risk of default in payments is also low for the company.

The net profit ratio of the company is 24% approximately. Omega Ltd holds a good

profitability. Net profit ratio is the percentage of sales revenue left with the company after paying

for all of its expenses.

Identifying and evaluating non-financial performance indicators for Omega Ltd.

Non-financial indicators are those indicators that reflects the performance of the company

on the basis of the factors that cannot be expressed in the monetary terms but affects the financial

performance of the company. The non-financial factors that can be assessed for knowing the

performance of Omega Ltd are:

Customer Satisfaction and Retention: The non-financial performance indicator of

customer satisfaction and retention is linked to each other. A company having higher level of

customer satisfaction and high customer retention rates is considered to be performing well. The

consumer satisfaction is higher when the experience it has with the usage of product is high (Al-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Mamary and et.al., 2020). High customer satisfaction means that the quality of the product

offerings of the company is of superior quality and also at the competitive price, it is available to

the customer. When the customer treatment during the purchase is of standard expectations and

also the satisfaction derived by the buyer from the using of product or experiencing of service

offered is high the customers tends to make repeated sales from the company. This indicates that

the performance of the company is excellent.

Brand Reputation: Brand reputation is the major non-financial factor that represents the

performance of the company. The reputation of the company gets improved when the company

works with a major or broader point of view. The basic perspective of the company behind its

working is to earn profits (Gousgounis and Neubert, 2020). When the company, aims at earning

the profit along with keeping in mind the impact of its operations over the environment from

which it gathers all the required resources and the society to which it ultimately sells its products

and who forms the base for its profit earnings, it is said to be working with a broader perspective.

This increases the reputation of the company in the minds of the society.

Impact of Pricing Strategy on the performance of Salesforce

The pricing strategy used by the Salesforce, a cloud based software company is price

skimming. In price skimming strategy the price of the product or service is set high at the initial

level and then the price is reduced at a steady pace when the product becomes less popular. The

motive of the company behind the price skimming strategy is to reduce the price constantly to

keep its sales at a rising trend by attracting different sections of society with every change in the

price level (10 Examples of Non-Financial KPIs that Make Money Now, 2022). The strategy

offers varied benefits to the company. The company with this pricing strategy enjoys the

advantage of high return on the investment it makes on the product. Further the pricing strategy

helps the company to create a brand image and main it over the time. The image of the brand

becomes more prestigious with the time. Company effectively segments the market in

accordance with its prices. The requirement for effective working of this policy is that the

demand curve should be inelastic. The new products launched by the company gets further

tested by the early purchasers of the product. Other companies using price skimming strategies

are Apple, Samsung etc.

offerings of the company is of superior quality and also at the competitive price, it is available to

the customer. When the customer treatment during the purchase is of standard expectations and

also the satisfaction derived by the buyer from the using of product or experiencing of service

offered is high the customers tends to make repeated sales from the company. This indicates that

the performance of the company is excellent.

Brand Reputation: Brand reputation is the major non-financial factor that represents the

performance of the company. The reputation of the company gets improved when the company

works with a major or broader point of view. The basic perspective of the company behind its

working is to earn profits (Gousgounis and Neubert, 2020). When the company, aims at earning

the profit along with keeping in mind the impact of its operations over the environment from

which it gathers all the required resources and the society to which it ultimately sells its products

and who forms the base for its profit earnings, it is said to be working with a broader perspective.

This increases the reputation of the company in the minds of the society.

Impact of Pricing Strategy on the performance of Salesforce

The pricing strategy used by the Salesforce, a cloud based software company is price

skimming. In price skimming strategy the price of the product or service is set high at the initial

level and then the price is reduced at a steady pace when the product becomes less popular. The

motive of the company behind the price skimming strategy is to reduce the price constantly to

keep its sales at a rising trend by attracting different sections of society with every change in the

price level (10 Examples of Non-Financial KPIs that Make Money Now, 2022). The strategy

offers varied benefits to the company. The company with this pricing strategy enjoys the

advantage of high return on the investment it makes on the product. Further the pricing strategy

helps the company to create a brand image and main it over the time. The image of the brand

becomes more prestigious with the time. Company effectively segments the market in

accordance with its prices. The requirement for effective working of this policy is that the

demand curve should be inelastic. The new products launched by the company gets further

tested by the early purchasers of the product. Other companies using price skimming strategies

are Apple, Samsung etc.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Abdelhady, S., 2021. Performance and cost evaluation of solar dish power plant: sensitivity

analysis of levelized cost of electricity (LCOE) and net present value (NPV). Renewable

Energy. 168. pp.332-342.

Al-Mamary, Y. H. and et.al., 2020. The effect of entrepreneurial orientation on financial and

non-financial performance in Saudi SMES: a review. Journal of Critical Reviews. 7(14).

pp.270-278.

Genolini, Y. and et.al., 2019. Cosmic-ray transport from AMS-02 boron to carbon ratio data:

Benchmark models and interpretation. Physical Review D. 99(12). p.123028.

Gousgounis, Y. Y. L. and Neubert, M., 2020. Price-setting strategies and practice for medical

devices used by consumers. Journal of Revenue and Pricing Management. 19(3). pp.218-

226.

Hazen, G. and Magni, C. A., 2021. Average internal rate of return for risky projects. The

Engineering Economist. 66(2). pp.90-120.

Maheshwari, S. N., Maheshwari, S. K. and Maheshwari, M. S. K., 2021. Principles of

Management Accounting. Sultan Chand & Sons.

Rouskas, E., 2021. Skimming through search. German Economic Review. 22(2). pp.129-152.

Yang, M. H., 2018. Payback period investigation of the organic Rankine cycle with mixed

working fluids to recover waste heat from the exhaust gas of a large marine diesel

engine. Energy Conversion and Management. 162. pp.189-202.

Online

10 Examples of Non-Financial KPIs that Make Money Now. 2022. [Online]. Available through:

<https://dividendsdiversify.com/non-financial-performance-measures/>

Accounting Ratios. 2022. [Online]. Available through: <

https://corporatefinanceinstitute.com/resources/knowledge/accounting/accounting-

ratios/>

Investment Appraisal Techniques. 2022. [Online]. Available through: <

https://efinancemanagement.com/investment-decisions/investment-appraisal-techniques >

1

Books and Journals

Abdelhady, S., 2021. Performance and cost evaluation of solar dish power plant: sensitivity

analysis of levelized cost of electricity (LCOE) and net present value (NPV). Renewable

Energy. 168. pp.332-342.

Al-Mamary, Y. H. and et.al., 2020. The effect of entrepreneurial orientation on financial and

non-financial performance in Saudi SMES: a review. Journal of Critical Reviews. 7(14).

pp.270-278.

Genolini, Y. and et.al., 2019. Cosmic-ray transport from AMS-02 boron to carbon ratio data:

Benchmark models and interpretation. Physical Review D. 99(12). p.123028.

Gousgounis, Y. Y. L. and Neubert, M., 2020. Price-setting strategies and practice for medical

devices used by consumers. Journal of Revenue and Pricing Management. 19(3). pp.218-

226.

Hazen, G. and Magni, C. A., 2021. Average internal rate of return for risky projects. The

Engineering Economist. 66(2). pp.90-120.

Maheshwari, S. N., Maheshwari, S. K. and Maheshwari, M. S. K., 2021. Principles of

Management Accounting. Sultan Chand & Sons.

Rouskas, E., 2021. Skimming through search. German Economic Review. 22(2). pp.129-152.

Yang, M. H., 2018. Payback period investigation of the organic Rankine cycle with mixed

working fluids to recover waste heat from the exhaust gas of a large marine diesel

engine. Energy Conversion and Management. 162. pp.189-202.

Online

10 Examples of Non-Financial KPIs that Make Money Now. 2022. [Online]. Available through:

<https://dividendsdiversify.com/non-financial-performance-measures/>

Accounting Ratios. 2022. [Online]. Available through: <

https://corporatefinanceinstitute.com/resources/knowledge/accounting/accounting-

ratios/>

Investment Appraisal Techniques. 2022. [Online]. Available through: <

https://efinancemanagement.com/investment-decisions/investment-appraisal-techniques >

1

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.