Comprehensive Business Finance Report: Analysis and Budgeting

VerifiedAdded on 2023/01/06

|13

|3502

|55

Report

AI Summary

This report provides a comprehensive analysis of business finance, beginning with an examination of profit and loss statements and statements of financial position. It utilizes ratio analysis to assess liquidity and profitability, highlighting key performance indicators for a sample company. The report th...

BUSINESS FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

PART 1............................................................................................................................................3

Statement of profit and loss........................................................................................................3

Statement of financial position ..................................................................................................4

PART 2............................................................................................................................................5

Accrual Accounting & Cash Accounting....................................................................................5

Difference Between Profit & Cash Flow....................................................................................7

PART 3............................................................................................................................................8

Define Budget and explain purposes of preparing a budget......................................................8

Benefit of forming limited company and getting it registered on stock exchange.....................9

REFERENCES..............................................................................................................................11

APPENDIX....................................................................................................................................12

Ratio analysis calculation..........................................................................................................12

PART 1............................................................................................................................................3

Statement of profit and loss........................................................................................................3

Statement of financial position ..................................................................................................4

PART 2............................................................................................................................................5

Accrual Accounting & Cash Accounting....................................................................................5

Difference Between Profit & Cash Flow....................................................................................7

PART 3............................................................................................................................................8

Define Budget and explain purposes of preparing a budget......................................................8

Benefit of forming limited company and getting it registered on stock exchange.....................9

REFERENCES..............................................................................................................................11

APPENDIX....................................................................................................................................12

Ratio analysis calculation..........................................................................................................12

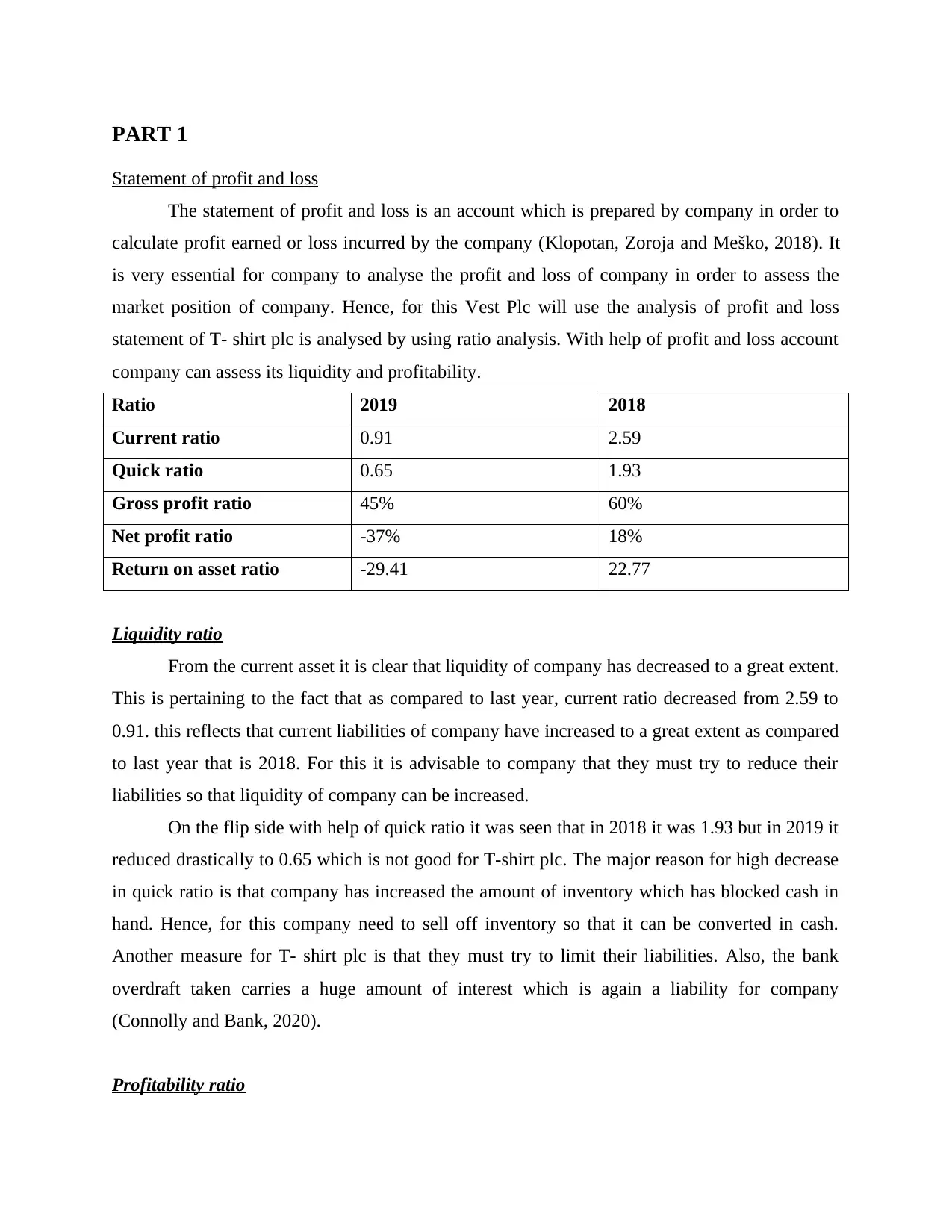

PART 1

Statement of profit and loss

The statement of profit and loss is an account which is prepared by company in order to

calculate profit earned or loss incurred by the company (Klopotan, Zoroja and Meško, 2018). It

is very essential for company to analyse the profit and loss of company in order to assess the

market position of company. Hence, for this Vest Plc will use the analysis of profit and loss

statement of T- shirt plc is analysed by using ratio analysis. With help of profit and loss account

company can assess its liquidity and profitability.

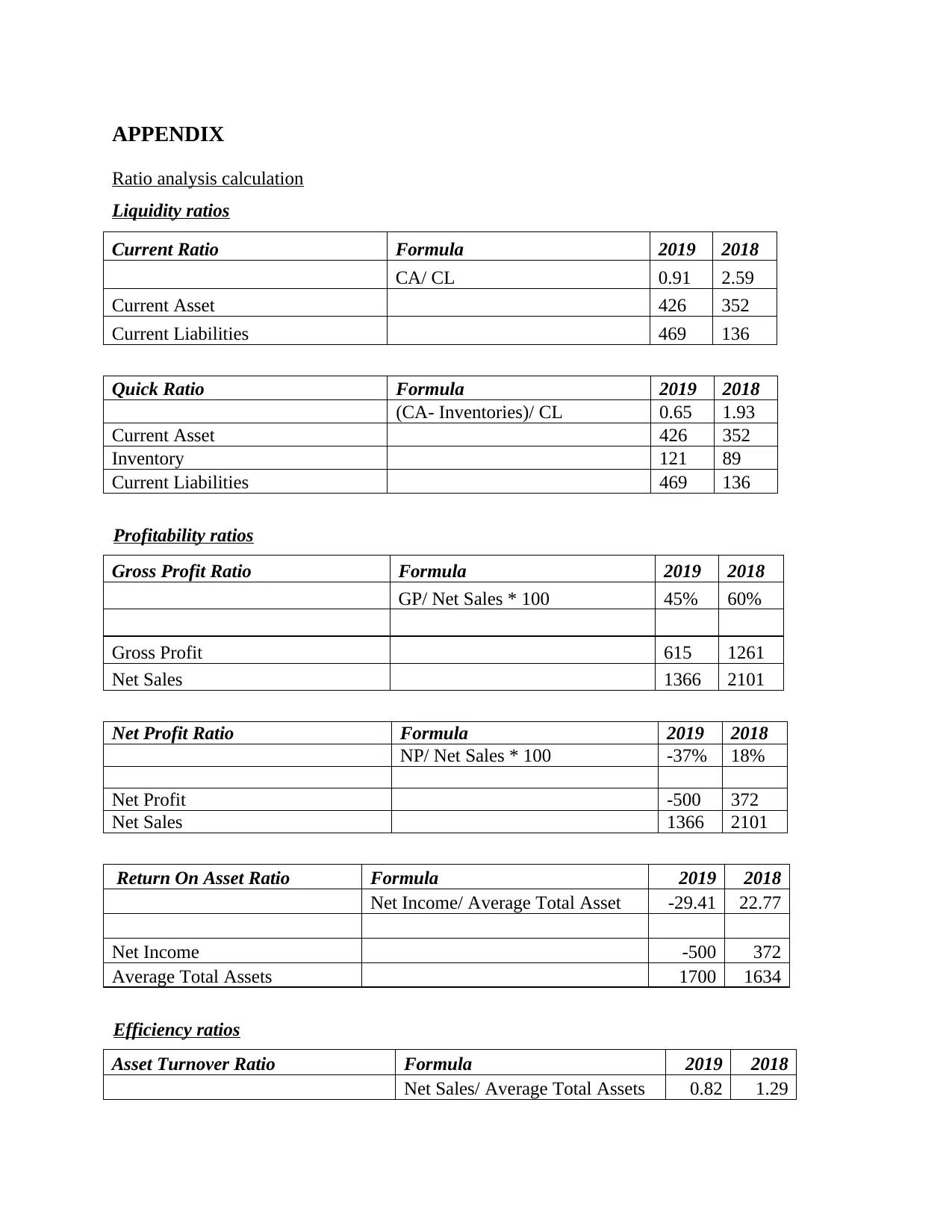

Ratio 2019 2018

Current ratio 0.91 2.59

Quick ratio 0.65 1.93

Gross profit ratio 45% 60%

Net profit ratio -37% 18%

Return on asset ratio -29.41 22.77

Liquidity ratio

From the current asset it is clear that liquidity of company has decreased to a great extent.

This is pertaining to the fact that as compared to last year, current ratio decreased from 2.59 to

0.91. this reflects that current liabilities of company have increased to a great extent as compared

to last year that is 2018. For this it is advisable to company that they must try to reduce their

liabilities so that liquidity of company can be increased.

On the flip side with help of quick ratio it was seen that in 2018 it was 1.93 but in 2019 it

reduced drastically to 0.65 which is not good for T-shirt plc. The major reason for high decrease

in quick ratio is that company has increased the amount of inventory which has blocked cash in

hand. Hence, for this company need to sell off inventory so that it can be converted in cash.

Another measure for T- shirt plc is that they must try to limit their liabilities. Also, the bank

overdraft taken carries a huge amount of interest which is again a liability for company

(Connolly and Bank, 2020).

Profitability ratio

Statement of profit and loss

The statement of profit and loss is an account which is prepared by company in order to

calculate profit earned or loss incurred by the company (Klopotan, Zoroja and Meško, 2018). It

is very essential for company to analyse the profit and loss of company in order to assess the

market position of company. Hence, for this Vest Plc will use the analysis of profit and loss

statement of T- shirt plc is analysed by using ratio analysis. With help of profit and loss account

company can assess its liquidity and profitability.

Ratio 2019 2018

Current ratio 0.91 2.59

Quick ratio 0.65 1.93

Gross profit ratio 45% 60%

Net profit ratio -37% 18%

Return on asset ratio -29.41 22.77

Liquidity ratio

From the current asset it is clear that liquidity of company has decreased to a great extent.

This is pertaining to the fact that as compared to last year, current ratio decreased from 2.59 to

0.91. this reflects that current liabilities of company have increased to a great extent as compared

to last year that is 2018. For this it is advisable to company that they must try to reduce their

liabilities so that liquidity of company can be increased.

On the flip side with help of quick ratio it was seen that in 2018 it was 1.93 but in 2019 it

reduced drastically to 0.65 which is not good for T-shirt plc. The major reason for high decrease

in quick ratio is that company has increased the amount of inventory which has blocked cash in

hand. Hence, for this company need to sell off inventory so that it can be converted in cash.

Another measure for T- shirt plc is that they must try to limit their liabilities. Also, the bank

overdraft taken carries a huge amount of interest which is again a liability for company

(Connolly and Bank, 2020).

Profitability ratio

You're viewing a preview

Unlock full access by subscribing today!

With help of gross profit ratio of T- shirt plc it is clearly evident that gross profit of

company has reduced to a great extent. The reduction was 15% that is from 60% to 45% from

2018 to 2019 respectively. This reduction was majorly due to the fact that sales of company has

reduced drastically from 2101 to 1366. This was the major reason for decrease in the gross profit.

Hence, for mitigating this issue that is to increase sales company is now providing more credit

period to their consumer and increased it to 60 from 30 days.

Along with this the net profit ratio depicted a downward trend in profit and loss account

of T- shirt plc. This was a very high change as company has incurred a loss of 500. This, because

of this NP ratio was -37% in 2019 which was earlier 18% in 2018. The major reason for this

reduction was that sales revenue decreased and along with this other expenses increased

(Ylhäinen, 2017). Thus, because of this increase in other expense and increase in finance cost the

expenses of company increased and as it was more than income so company suffered a loss.

In addition to return on asset ratio also company can assess it profitability. The return on

asset is a ratio which depicts ability of company in using its asset in order to generate revenue. In

2019 the return on asset was -29.41%, whereas in 2018 it was 22.77%. This reflects that

currently T- shirt is not in a position to optimally use its asset in order to generate finance from

the present asset.

Statement of financial position

The financial position of company is being reflected by balance sheet of company and for

analysing financial position of T- shirt plc it is very crucial to effectively assess the balance sheet

as well. For this company takes help of solvency and efficiency ratios to analyse balance sheet.

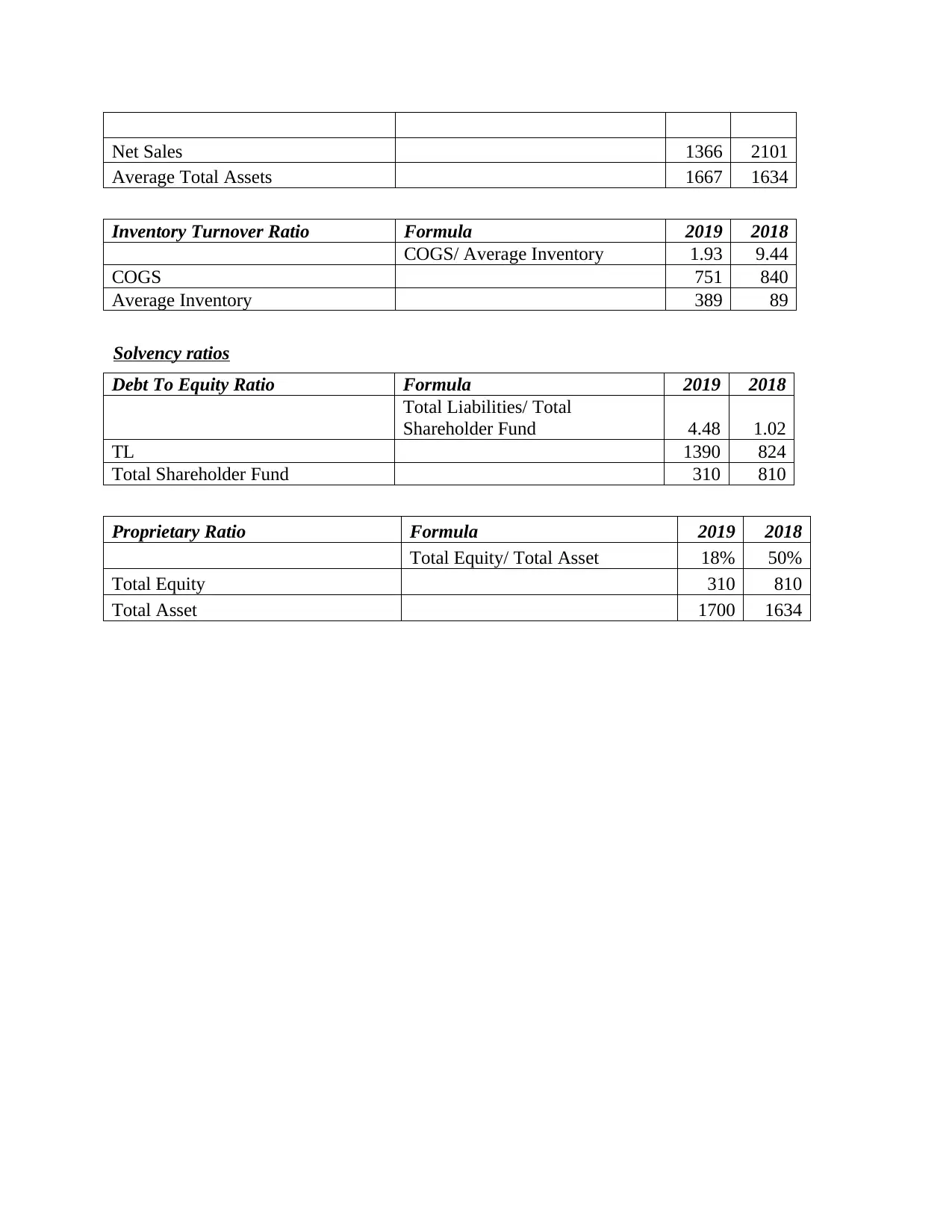

Ratio 2019 2018

Asset turnover ratio 0.82 1.29

Inventory turnover ratio 1.93 9.44

Debt to equity ratio 4.48 1.02

Proprietary ratio 18% 50%

Efficiency ratio

With help of asset turnover ratio, it was clearly visible that there was decrease in ratio

from 1.29 to 0.82 from the year 2018 to 2019 respectively. This reflects that company is not

making proper and efficient use of its asset in order to increase sales. For effective running of

company has reduced to a great extent. The reduction was 15% that is from 60% to 45% from

2018 to 2019 respectively. This reduction was majorly due to the fact that sales of company has

reduced drastically from 2101 to 1366. This was the major reason for decrease in the gross profit.

Hence, for mitigating this issue that is to increase sales company is now providing more credit

period to their consumer and increased it to 60 from 30 days.

Along with this the net profit ratio depicted a downward trend in profit and loss account

of T- shirt plc. This was a very high change as company has incurred a loss of 500. This, because

of this NP ratio was -37% in 2019 which was earlier 18% in 2018. The major reason for this

reduction was that sales revenue decreased and along with this other expenses increased

(Ylhäinen, 2017). Thus, because of this increase in other expense and increase in finance cost the

expenses of company increased and as it was more than income so company suffered a loss.

In addition to return on asset ratio also company can assess it profitability. The return on

asset is a ratio which depicts ability of company in using its asset in order to generate revenue. In

2019 the return on asset was -29.41%, whereas in 2018 it was 22.77%. This reflects that

currently T- shirt is not in a position to optimally use its asset in order to generate finance from

the present asset.

Statement of financial position

The financial position of company is being reflected by balance sheet of company and for

analysing financial position of T- shirt plc it is very crucial to effectively assess the balance sheet

as well. For this company takes help of solvency and efficiency ratios to analyse balance sheet.

Ratio 2019 2018

Asset turnover ratio 0.82 1.29

Inventory turnover ratio 1.93 9.44

Debt to equity ratio 4.48 1.02

Proprietary ratio 18% 50%

Efficiency ratio

With help of asset turnover ratio, it was clearly visible that there was decrease in ratio

from 1.29 to 0.82 from the year 2018 to 2019 respectively. This reflects that company is not

making proper and efficient use of its asset in order to increase sales. For effective running of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

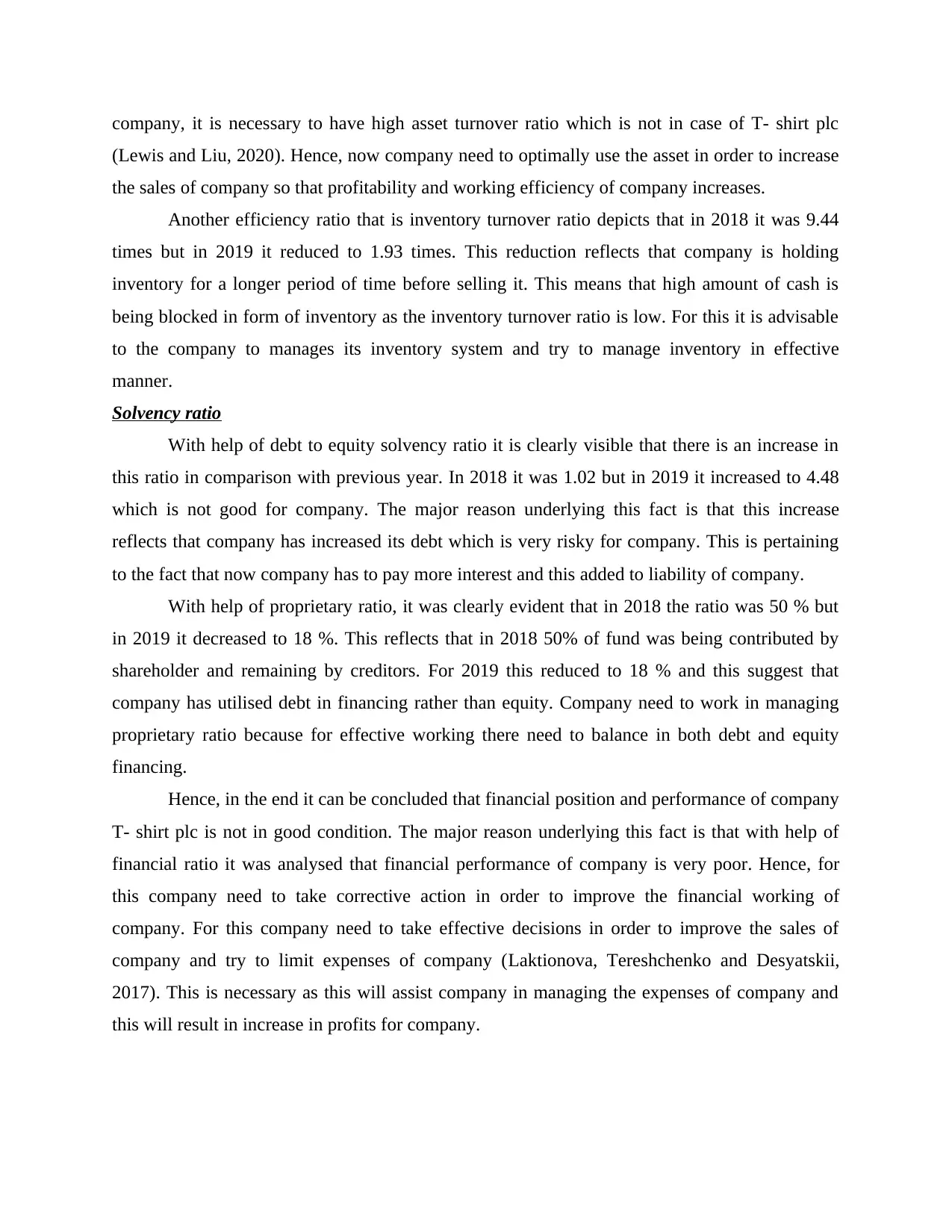

company, it is necessary to have high asset turnover ratio which is not in case of T- shirt plc

(Lewis and Liu, 2020). Hence, now company need to optimally use the asset in order to increase

the sales of company so that profitability and working efficiency of company increases.

Another efficiency ratio that is inventory turnover ratio depicts that in 2018 it was 9.44

times but in 2019 it reduced to 1.93 times. This reduction reflects that company is holding

inventory for a longer period of time before selling it. This means that high amount of cash is

being blocked in form of inventory as the inventory turnover ratio is low. For this it is advisable

to the company to manages its inventory system and try to manage inventory in effective

manner.

Solvency ratio

With help of debt to equity solvency ratio it is clearly visible that there is an increase in

this ratio in comparison with previous year. In 2018 it was 1.02 but in 2019 it increased to 4.48

which is not good for company. The major reason underlying this fact is that this increase

reflects that company has increased its debt which is very risky for company. This is pertaining

to the fact that now company has to pay more interest and this added to liability of company.

With help of proprietary ratio, it was clearly evident that in 2018 the ratio was 50 % but

in 2019 it decreased to 18 %. This reflects that in 2018 50% of fund was being contributed by

shareholder and remaining by creditors. For 2019 this reduced to 18 % and this suggest that

company has utilised debt in financing rather than equity. Company need to work in managing

proprietary ratio because for effective working there need to balance in both debt and equity

financing.

Hence, in the end it can be concluded that financial position and performance of company

T- shirt plc is not in good condition. The major reason underlying this fact is that with help of

financial ratio it was analysed that financial performance of company is very poor. Hence, for

this company need to take corrective action in order to improve the financial working of

company. For this company need to take effective decisions in order to improve the sales of

company and try to limit expenses of company (Laktionova, Tereshchenko and Desyatskii,

2017). This is necessary as this will assist company in managing the expenses of company and

this will result in increase in profits for company.

(Lewis and Liu, 2020). Hence, now company need to optimally use the asset in order to increase

the sales of company so that profitability and working efficiency of company increases.

Another efficiency ratio that is inventory turnover ratio depicts that in 2018 it was 9.44

times but in 2019 it reduced to 1.93 times. This reduction reflects that company is holding

inventory for a longer period of time before selling it. This means that high amount of cash is

being blocked in form of inventory as the inventory turnover ratio is low. For this it is advisable

to the company to manages its inventory system and try to manage inventory in effective

manner.

Solvency ratio

With help of debt to equity solvency ratio it is clearly visible that there is an increase in

this ratio in comparison with previous year. In 2018 it was 1.02 but in 2019 it increased to 4.48

which is not good for company. The major reason underlying this fact is that this increase

reflects that company has increased its debt which is very risky for company. This is pertaining

to the fact that now company has to pay more interest and this added to liability of company.

With help of proprietary ratio, it was clearly evident that in 2018 the ratio was 50 % but

in 2019 it decreased to 18 %. This reflects that in 2018 50% of fund was being contributed by

shareholder and remaining by creditors. For 2019 this reduced to 18 % and this suggest that

company has utilised debt in financing rather than equity. Company need to work in managing

proprietary ratio because for effective working there need to balance in both debt and equity

financing.

Hence, in the end it can be concluded that financial position and performance of company

T- shirt plc is not in good condition. The major reason underlying this fact is that with help of

financial ratio it was analysed that financial performance of company is very poor. Hence, for

this company need to take corrective action in order to improve the financial working of

company. For this company need to take effective decisions in order to improve the sales of

company and try to limit expenses of company (Laktionova, Tereshchenko and Desyatskii,

2017). This is necessary as this will assist company in managing the expenses of company and

this will result in increase in profits for company.

PART 2

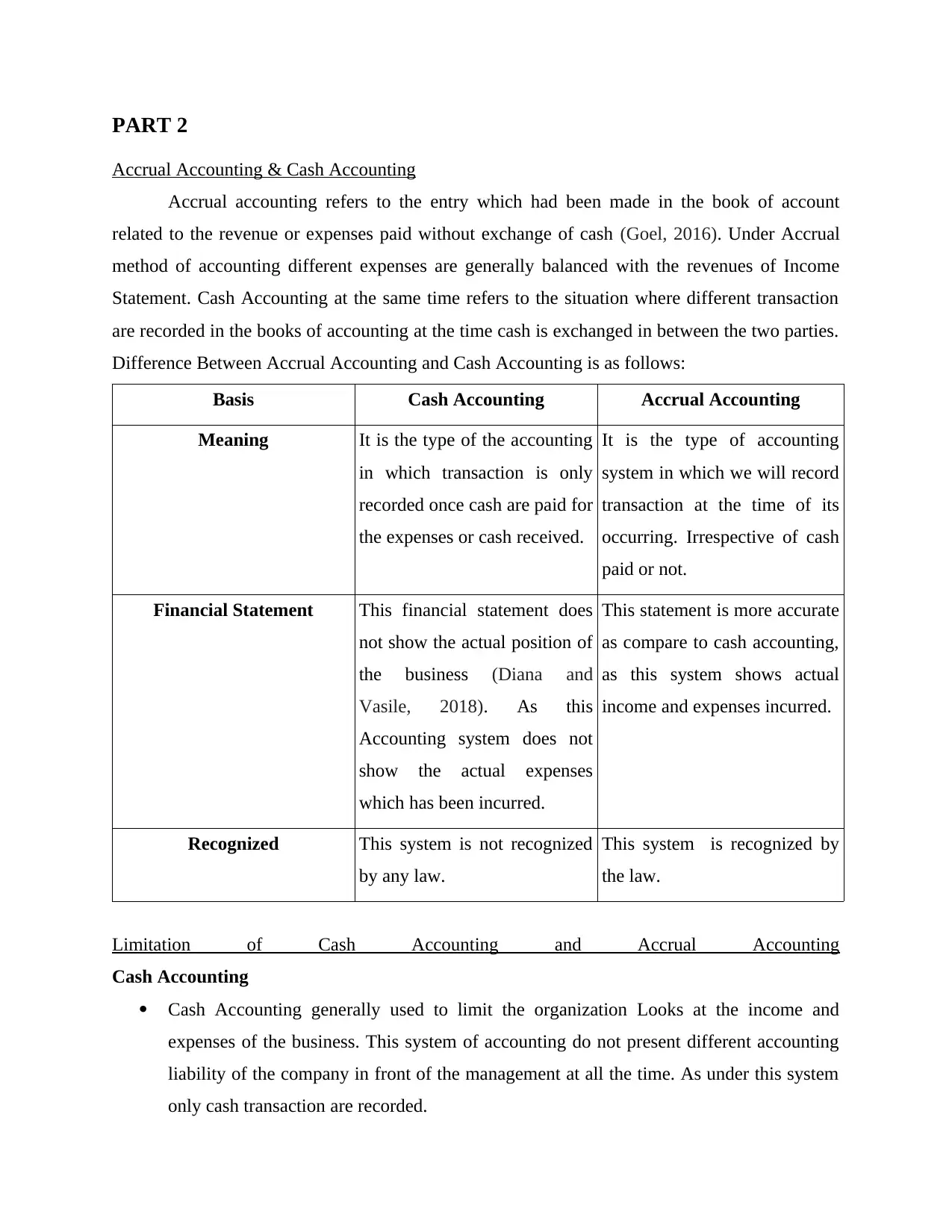

Accrual Accounting & Cash Accounting

Accrual accounting refers to the entry which had been made in the book of account

related to the revenue or expenses paid without exchange of cash (Goel, 2016). Under Accrual

method of accounting different expenses are generally balanced with the revenues of Income

Statement. Cash Accounting at the same time refers to the situation where different transaction

are recorded in the books of accounting at the time cash is exchanged in between the two parties.

Difference Between Accrual Accounting and Cash Accounting is as follows:

Basis Cash Accounting Accrual Accounting

Meaning It is the type of the accounting

in which transaction is only

recorded once cash are paid for

the expenses or cash received.

It is the type of accounting

system in which we will record

transaction at the time of its

occurring. Irrespective of cash

paid or not.

Financial Statement This financial statement does

not show the actual position of

the business (Diana and

Vasile, 2018). As this

Accounting system does not

show the actual expenses

which has been incurred.

This statement is more accurate

as compare to cash accounting,

as this system shows actual

income and expenses incurred.

Recognized This system is not recognized

by any law.

This system is recognized by

the law.

Limitation of Cash Accounting and Accrual Accounting

Cash Accounting

Cash Accounting generally used to limit the organization Looks at the income and

expenses of the business. This system of accounting do not present different accounting

liability of the company in front of the management at all the time. As under this system

only cash transaction are recorded.

Accrual Accounting & Cash Accounting

Accrual accounting refers to the entry which had been made in the book of account

related to the revenue or expenses paid without exchange of cash (Goel, 2016). Under Accrual

method of accounting different expenses are generally balanced with the revenues of Income

Statement. Cash Accounting at the same time refers to the situation where different transaction

are recorded in the books of accounting at the time cash is exchanged in between the two parties.

Difference Between Accrual Accounting and Cash Accounting is as follows:

Basis Cash Accounting Accrual Accounting

Meaning It is the type of the accounting

in which transaction is only

recorded once cash are paid for

the expenses or cash received.

It is the type of accounting

system in which we will record

transaction at the time of its

occurring. Irrespective of cash

paid or not.

Financial Statement This financial statement does

not show the actual position of

the business (Diana and

Vasile, 2018). As this

Accounting system does not

show the actual expenses

which has been incurred.

This statement is more accurate

as compare to cash accounting,

as this system shows actual

income and expenses incurred.

Recognized This system is not recognized

by any law.

This system is recognized by

the law.

Limitation of Cash Accounting and Accrual Accounting

Cash Accounting

Cash Accounting generally used to limit the organization Looks at the income and

expenses of the business. This system of accounting do not present different accounting

liability of the company in front of the management at all the time. As under this system

only cash transaction are recorded.

You're viewing a preview

Unlock full access by subscribing today!

Cash Accounting system does not provide the management with the actual position of the

business. This will create the situation where management think they have more money

than they actually have in hand. This will ultimately create the deficiency in presence of

cash and cash equivalent for the organization.

Accrual Accounting

The Biggest limitation of Accrual Accounting is that it is one of the complicated form of

accounting, this type of Accounting generally requires better amount of resources and

time to to be invested by the organization. Hence, it gets very difficult for small

organization to adopt the same (Ali, Ormal and Ahmad, 2018).

Another limitation of Accrual Accounting is that it sometime used to create the issue for

the organization in maintaining and managing the Cash flow statement of the

organization. As date of receiving the cash in the organization is ignored by the

organization. Hence, any issue occurred in cash flow statement can not be rectified with

the help of Accrual Accounting system.

Profit & Cash Flow

Profit in accounting is an income distributed to the owners in a profitable market

production process. In simple words profit is an amount left with the owner after deducting

production and operation cost from the amount earned.

Cash Flow at the same time is defined as a net amount of cash and cash equivalent

transferred into or out of the business (Rafi and et.al., 2020). If company is able to generate cash

flow way above their expenses then it is called as a positive cash flow. If company is not able to

generate cash flow to satisfy its expenses itself then is it is called as a negative cash flow.

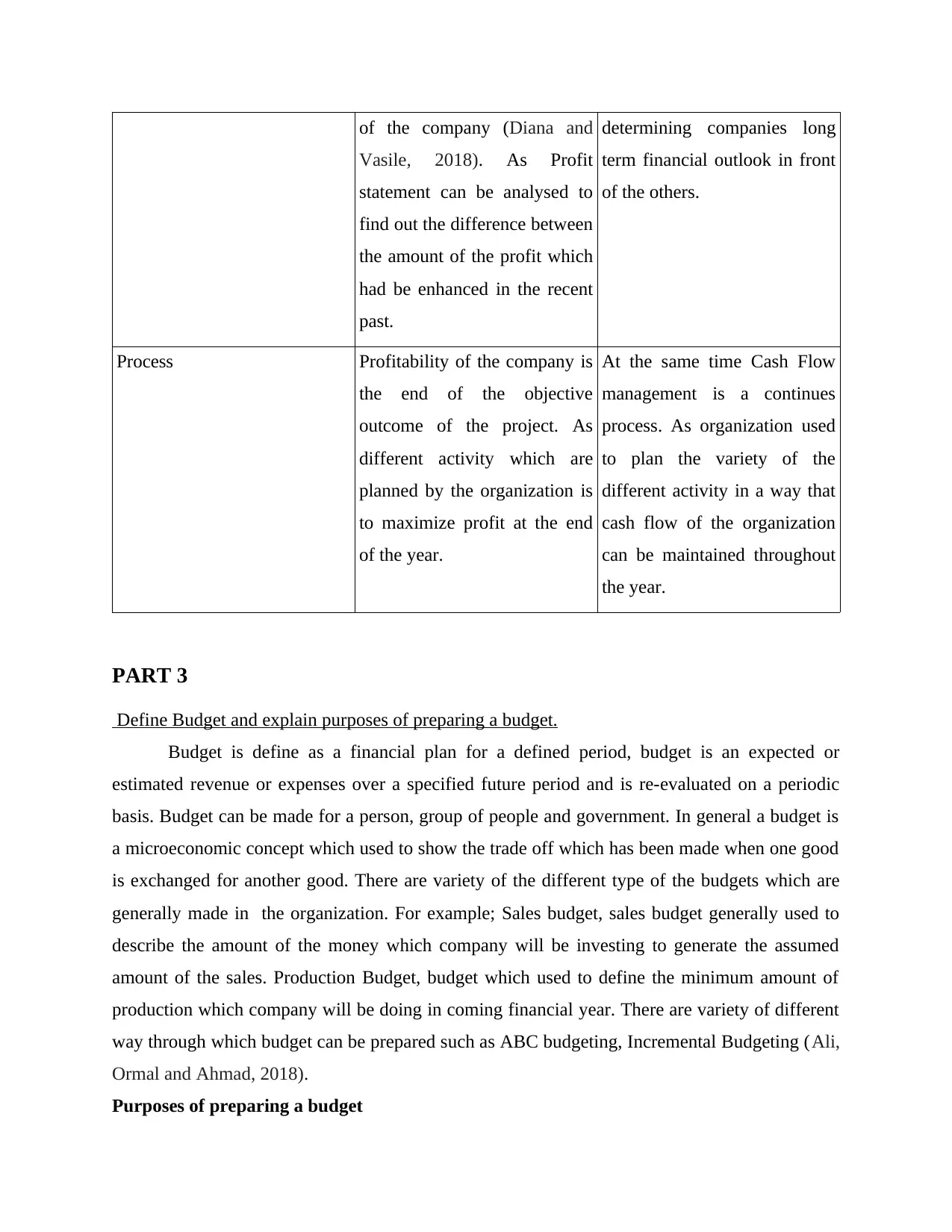

Difference Between Profit & Cash Flow

Basis Profit Cash Flow

Meaning Profit is defined as a positive

difference between Sales

revenues and total cost of the

company.

Cash Flow at the same time is

defined as total money that

flow in and out of a business

over a given year.

Purpose Profit statement generally

shows the immediate success

Cash Flow at the same time is

assured as a means of

business. This will create the situation where management think they have more money

than they actually have in hand. This will ultimately create the deficiency in presence of

cash and cash equivalent for the organization.

Accrual Accounting

The Biggest limitation of Accrual Accounting is that it is one of the complicated form of

accounting, this type of Accounting generally requires better amount of resources and

time to to be invested by the organization. Hence, it gets very difficult for small

organization to adopt the same (Ali, Ormal and Ahmad, 2018).

Another limitation of Accrual Accounting is that it sometime used to create the issue for

the organization in maintaining and managing the Cash flow statement of the

organization. As date of receiving the cash in the organization is ignored by the

organization. Hence, any issue occurred in cash flow statement can not be rectified with

the help of Accrual Accounting system.

Profit & Cash Flow

Profit in accounting is an income distributed to the owners in a profitable market

production process. In simple words profit is an amount left with the owner after deducting

production and operation cost from the amount earned.

Cash Flow at the same time is defined as a net amount of cash and cash equivalent

transferred into or out of the business (Rafi and et.al., 2020). If company is able to generate cash

flow way above their expenses then it is called as a positive cash flow. If company is not able to

generate cash flow to satisfy its expenses itself then is it is called as a negative cash flow.

Difference Between Profit & Cash Flow

Basis Profit Cash Flow

Meaning Profit is defined as a positive

difference between Sales

revenues and total cost of the

company.

Cash Flow at the same time is

defined as total money that

flow in and out of a business

over a given year.

Purpose Profit statement generally

shows the immediate success

Cash Flow at the same time is

assured as a means of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

of the company (Diana and

Vasile, 2018). As Profit

statement can be analysed to

find out the difference between

the amount of the profit which

had be enhanced in the recent

past.

determining companies long

term financial outlook in front

of the others.

Process Profitability of the company is

the end of the objective

outcome of the project. As

different activity which are

planned by the organization is

to maximize profit at the end

of the year.

At the same time Cash Flow

management is a continues

process. As organization used

to plan the variety of the

different activity in a way that

cash flow of the organization

can be maintained throughout

the year.

PART 3

Define Budget and explain purposes of preparing a budget.

Budget is define as a financial plan for a defined period, budget is an expected or

estimated revenue or expenses over a specified future period and is re-evaluated on a periodic

basis. Budget can be made for a person, group of people and government. In general a budget is

a microeconomic concept which used to show the trade off which has been made when one good

is exchanged for another good. There are variety of the different type of the budgets which are

generally made in the organization. For example; Sales budget, sales budget generally used to

describe the amount of the money which company will be investing to generate the assumed

amount of the sales. Production Budget, budget which used to define the minimum amount of

production which company will be doing in coming financial year. There are variety of different

way through which budget can be prepared such as ABC budgeting, Incremental Budgeting (Ali,

Ormal and Ahmad, 2018).

Purposes of preparing a budget

Vasile, 2018). As Profit

statement can be analysed to

find out the difference between

the amount of the profit which

had be enhanced in the recent

past.

determining companies long

term financial outlook in front

of the others.

Process Profitability of the company is

the end of the objective

outcome of the project. As

different activity which are

planned by the organization is

to maximize profit at the end

of the year.

At the same time Cash Flow

management is a continues

process. As organization used

to plan the variety of the

different activity in a way that

cash flow of the organization

can be maintained throughout

the year.

PART 3

Define Budget and explain purposes of preparing a budget.

Budget is define as a financial plan for a defined period, budget is an expected or

estimated revenue or expenses over a specified future period and is re-evaluated on a periodic

basis. Budget can be made for a person, group of people and government. In general a budget is

a microeconomic concept which used to show the trade off which has been made when one good

is exchanged for another good. There are variety of the different type of the budgets which are

generally made in the organization. For example; Sales budget, sales budget generally used to

describe the amount of the money which company will be investing to generate the assumed

amount of the sales. Production Budget, budget which used to define the minimum amount of

production which company will be doing in coming financial year. There are variety of different

way through which budget can be prepared such as ABC budgeting, Incremental Budgeting (Ali,

Ormal and Ahmad, 2018).

Purposes of preparing a budget

Optimum Utilization of Resources: It is one of the biggest purpose for which budget is

prepared in the organization. All the organization with the help of budget looks to allocate the

different resources in a way that organization is able to optimum utilize different resources.

Communication: Another purpose of drafting budget is to communicate clear message

to all the individual in regard to different resources which they are having to complete the task in

their hand. This ultimately help the company in maintaining good sort of the clarity in the long

run.

Achieve Financial Goal: First step in budget preparation is to set financial goal. After

budget is generally prepare in a way that it generally used to help the organization in achieving

the Financial goal of the business very efficiently.

Benefit of forming limited company and getting it registered on stock exchange

A limited company is a type of company which is formed or incorporated wherein the

liability of shareholders of company is limited (Canales, 2016). This includes a legal structure

which makes a provision that liability of members or shareholder is limited up to only their stake

in investment. Within the limited company all the asset and liabilities of company are separate

from that of shareholders. This can be limited by two methods that is limited by shares and

limited by guarantee. Listing is referred to as a process through which securities of company are

listed over the trading platform of different stock exchanges. It is very beneficial for a limited

company to get itself registered over stock exchange. The major benefits of forming a limited

company and getting it registered on stock exchange are as follows-

Minimising of personal liability- this is the major benefit of forming a limited company

as in this the personal liability of shareholder is not present. Thus, the shareholder will be liable

only to the extent to their money invested in company.

Limited risk- this is another major benefit of forming a limited company as under the

limited company the risk of the member or shareholder is very limited. The major reason

underlying this fact is that as company is separate from its owners hence, the risk is very

minimum and this is advantage for shareholders.

Enhanced visibility- another major benefit of getting the limited company listed over

stock exchange is that this increases the visibility of company. The major reason behind this is

that when company is listed over stock exchange then people can trade in shares of company and

this increases knowledge of people relating to the company.

prepared in the organization. All the organization with the help of budget looks to allocate the

different resources in a way that organization is able to optimum utilize different resources.

Communication: Another purpose of drafting budget is to communicate clear message

to all the individual in regard to different resources which they are having to complete the task in

their hand. This ultimately help the company in maintaining good sort of the clarity in the long

run.

Achieve Financial Goal: First step in budget preparation is to set financial goal. After

budget is generally prepare in a way that it generally used to help the organization in achieving

the Financial goal of the business very efficiently.

Benefit of forming limited company and getting it registered on stock exchange

A limited company is a type of company which is formed or incorporated wherein the

liability of shareholders of company is limited (Canales, 2016). This includes a legal structure

which makes a provision that liability of members or shareholder is limited up to only their stake

in investment. Within the limited company all the asset and liabilities of company are separate

from that of shareholders. This can be limited by two methods that is limited by shares and

limited by guarantee. Listing is referred to as a process through which securities of company are

listed over the trading platform of different stock exchanges. It is very beneficial for a limited

company to get itself registered over stock exchange. The major benefits of forming a limited

company and getting it registered on stock exchange are as follows-

Minimising of personal liability- this is the major benefit of forming a limited company

as in this the personal liability of shareholder is not present. Thus, the shareholder will be liable

only to the extent to their money invested in company.

Limited risk- this is another major benefit of forming a limited company as under the

limited company the risk of the member or shareholder is very limited. The major reason

underlying this fact is that as company is separate from its owners hence, the risk is very

minimum and this is advantage for shareholders.

Enhanced visibility- another major benefit of getting the limited company listed over

stock exchange is that this increases the visibility of company. The major reason behind this is

that when company is listed over stock exchange then people can trade in shares of company and

this increases knowledge of people relating to the company.

You're viewing a preview

Unlock full access by subscribing today!

Transparency- this is another major benefit of listing the company over stock exchange.

This is a benefit because when company list itself over stock exchange then they have to disclose

many of the fact sand information relating to company to its shareholders (Advantages and

disadvantages of private limited company, 2020). Thus, this calls for displaying all relevant

information to its shareholders which increases transparency among shareholders and company

which is a benefit.

This is a benefit because when company list itself over stock exchange then they have to disclose

many of the fact sand information relating to company to its shareholders (Advantages and

disadvantages of private limited company, 2020). Thus, this calls for displaying all relevant

information to its shareholders which increases transparency among shareholders and company

which is a benefit.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Canales, R., 2016. From ideals to institutions: Institutional entrepreneurship and the growth of

Mexican small business finance. Organization Science. 27(6). pp.1548-1573.

Connolly, E. and Bank, J., 2020. Access to small business finance. RBA Bulletin, September,

viewed. 10.

Klopotan, I., Zoroja, J. and Meško, M., 2018. Early warning system in business, finance, and

economics: Bibliometric and topic analysis. International Journal of Engineering Business

Management. 10. p.1847979018797013.

Laktionova, O.E., Tereshchenko, E.Y. and Desyatskii, S.P., 2017. Transformation of the

organization and management of small and medium-sized business' finance. Finansovaya

analitika: problemy i resheniya= Financial Analytics: Science and Experience. 10(7).

pp.767-789.

Lewis, M. and Liu, Q., 2020. The COVID-19 Outbreak and Access to Small Business

Finance. 1. 1 Managing the Risks of Holding Self-securitisations as Collateral 2. 11

Government Bond Market Functioning and COVID-19 3. The Economic Effects of Low

Interest Rates and Unconventional 21 Monetary Policy 4. Retail Central Bank Digital

Currency: Design Considerations, Rationales, p.58.

Ylhäinen, I., 2017. Life-cycle effects in small business finance. Journal of Banking &

Finance. 77. pp.176-196.

Goel, D., 2016. The earnings management motivation: Accrual accounting vs. cash

accounting. Australasian Accounting, Business and Finance Journal. 10(3). pp.48-66.

Gigli, S. and Mariani, L., 2018. Lost in the transition from cash to accrual

accounting. International Journal of Public Sector Management.

Diana, H. I. and Vasile, B., 2018. INTERFERENCE BETWEEN PROFIT AND CASH-FLOW

IN EVALUATING ECONOMIC PERFORMANCE. Annals of'Constantin

Brancusi'University of Targu-Jiu. Economy Series, (3).

Ali, U., Ormal, L. and Ahmad, F., 2018. Impact of free cash flow on profitability of the firms in

automobile sector of Germany. Journal of Economics and Management Sciences. 1(1).

pp.57-67.

Rafi, M and et.al., 2020. Budget harmonization and challenges: understanding the competence

of professionals in the budget process for structural and policy reforms in public

libraries. Performance Measurement and Metrics.

Online

Advantages and disadvantages of private limited company. 2020. [Online]. Available through: <

https://taxguru.in/company-law/advantages-disadvantages-private-limited-

company.html#:~:text=It%20can%20be%20registered%20with,family%20owned%20or

%20professionally%20managed. >

Books and Journals

Canales, R., 2016. From ideals to institutions: Institutional entrepreneurship and the growth of

Mexican small business finance. Organization Science. 27(6). pp.1548-1573.

Connolly, E. and Bank, J., 2020. Access to small business finance. RBA Bulletin, September,

viewed. 10.

Klopotan, I., Zoroja, J. and Meško, M., 2018. Early warning system in business, finance, and

economics: Bibliometric and topic analysis. International Journal of Engineering Business

Management. 10. p.1847979018797013.

Laktionova, O.E., Tereshchenko, E.Y. and Desyatskii, S.P., 2017. Transformation of the

organization and management of small and medium-sized business' finance. Finansovaya

analitika: problemy i resheniya= Financial Analytics: Science and Experience. 10(7).

pp.767-789.

Lewis, M. and Liu, Q., 2020. The COVID-19 Outbreak and Access to Small Business

Finance. 1. 1 Managing the Risks of Holding Self-securitisations as Collateral 2. 11

Government Bond Market Functioning and COVID-19 3. The Economic Effects of Low

Interest Rates and Unconventional 21 Monetary Policy 4. Retail Central Bank Digital

Currency: Design Considerations, Rationales, p.58.

Ylhäinen, I., 2017. Life-cycle effects in small business finance. Journal of Banking &

Finance. 77. pp.176-196.

Goel, D., 2016. The earnings management motivation: Accrual accounting vs. cash

accounting. Australasian Accounting, Business and Finance Journal. 10(3). pp.48-66.

Gigli, S. and Mariani, L., 2018. Lost in the transition from cash to accrual

accounting. International Journal of Public Sector Management.

Diana, H. I. and Vasile, B., 2018. INTERFERENCE BETWEEN PROFIT AND CASH-FLOW

IN EVALUATING ECONOMIC PERFORMANCE. Annals of'Constantin

Brancusi'University of Targu-Jiu. Economy Series, (3).

Ali, U., Ormal, L. and Ahmad, F., 2018. Impact of free cash flow on profitability of the firms in

automobile sector of Germany. Journal of Economics and Management Sciences. 1(1).

pp.57-67.

Rafi, M and et.al., 2020. Budget harmonization and challenges: understanding the competence

of professionals in the budget process for structural and policy reforms in public

libraries. Performance Measurement and Metrics.

Online

Advantages and disadvantages of private limited company. 2020. [Online]. Available through: <

https://taxguru.in/company-law/advantages-disadvantages-private-limited-

company.html#:~:text=It%20can%20be%20registered%20with,family%20owned%20or

%20professionally%20managed. >

APPENDIX

Ratio analysis calculation

Liquidity ratios

Current Ratio Formula 2019 2018

CA/ CL 0.91 2.59

Current Asset 426 352

Current Liabilities 469 136

Quick Ratio Formula 2019 2018

(CA- Inventories)/ CL 0.65 1.93

Current Asset 426 352

Inventory 121 89

Current Liabilities 469 136

Profitability ratios

Gross Profit Ratio Formula 2019 2018

GP/ Net Sales * 100 45% 60%

Gross Profit 615 1261

Net Sales 1366 2101

Net Profit Ratio Formula 2019 2018

NP/ Net Sales * 100 -37% 18%

Net Profit -500 372

Net Sales 1366 2101

Return On Asset Ratio Formula 2019 2018

Net Income/ Average Total Asset -29.41 22.77

Net Income -500 372

Average Total Assets 1700 1634

Efficiency ratios

Asset Turnover Ratio Formula 2019 2018

Net Sales/ Average Total Assets 0.82 1.29

Ratio analysis calculation

Liquidity ratios

Current Ratio Formula 2019 2018

CA/ CL 0.91 2.59

Current Asset 426 352

Current Liabilities 469 136

Quick Ratio Formula 2019 2018

(CA- Inventories)/ CL 0.65 1.93

Current Asset 426 352

Inventory 121 89

Current Liabilities 469 136

Profitability ratios

Gross Profit Ratio Formula 2019 2018

GP/ Net Sales * 100 45% 60%

Gross Profit 615 1261

Net Sales 1366 2101

Net Profit Ratio Formula 2019 2018

NP/ Net Sales * 100 -37% 18%

Net Profit -500 372

Net Sales 1366 2101

Return On Asset Ratio Formula 2019 2018

Net Income/ Average Total Asset -29.41 22.77

Net Income -500 372

Average Total Assets 1700 1634

Efficiency ratios

Asset Turnover Ratio Formula 2019 2018

Net Sales/ Average Total Assets 0.82 1.29

You're viewing a preview

Unlock full access by subscribing today!

Net Sales 1366 2101

Average Total Assets 1667 1634

Inventory Turnover Ratio Formula 2019 2018

COGS/ Average Inventory 1.93 9.44

COGS 751 840

Average Inventory 389 89

Solvency ratios

Debt To Equity Ratio Formula 2019 2018

Total Liabilities/ Total

Shareholder Fund 4.48 1.02

TL 1390 824

Total Shareholder Fund 310 810

Proprietary Ratio Formula 2019 2018

Total Equity/ Total Asset 18% 50%

Total Equity 310 810

Total Asset 1700 1634

Average Total Assets 1667 1634

Inventory Turnover Ratio Formula 2019 2018

COGS/ Average Inventory 1.93 9.44

COGS 751 840

Average Inventory 389 89

Solvency ratios

Debt To Equity Ratio Formula 2019 2018

Total Liabilities/ Total

Shareholder Fund 4.48 1.02

TL 1390 824

Total Shareholder Fund 310 810

Proprietary Ratio Formula 2019 2018

Total Equity/ Total Asset 18% 50%

Total Equity 310 810

Total Asset 1700 1634

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.