Cost Management and Budgeting in Business Finance

Added on 2022-12-14

17 Pages2668 Words203 Views

BUSINESS FINANCE

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

Part A...............................................................................................................................................3

Part B...............................................................................................................................................6

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................3

Part A...............................................................................................................................................3

Part B...............................................................................................................................................6

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

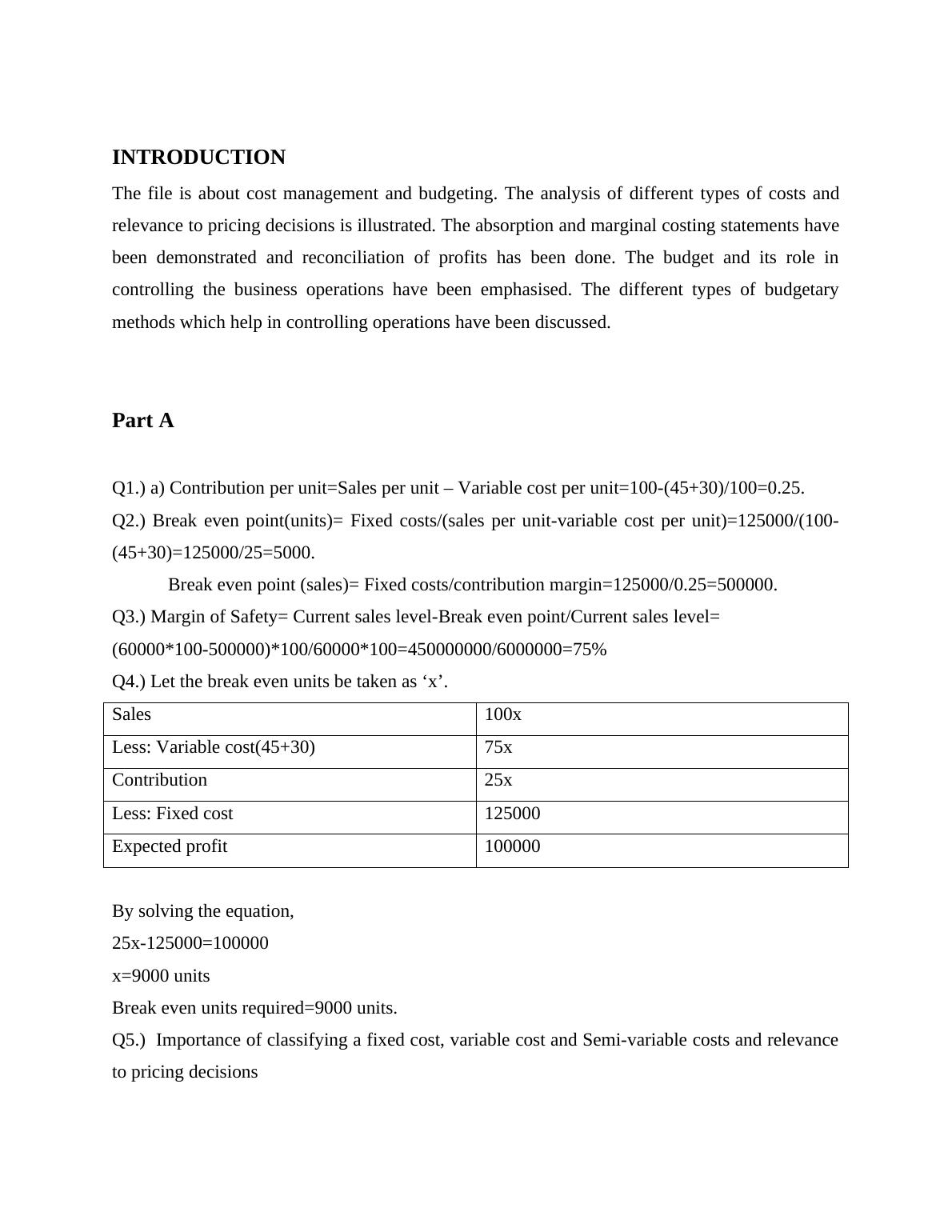

INTRODUCTION

The file is about cost management and budgeting. The analysis of different types of costs and

relevance to pricing decisions is illustrated. The absorption and marginal costing statements have

been demonstrated and reconciliation of profits has been done. The budget and its role in

controlling the business operations have been emphasised. The different types of budgetary

methods which help in controlling operations have been discussed.

Part A

Q1.) a) Contribution per unit=Sales per unit – Variable cost per unit=100-(45+30)/100=0.25.

Q2.) Break even point(units)= Fixed costs/(sales per unit-variable cost per unit)=125000/(100-

(45+30)=125000/25=5000.

Break even point (sales)= Fixed costs/contribution margin=125000/0.25=500000.

Q3.) Margin of Safety= Current sales level-Break even point/Current sales level=

(60000*100-500000)*100/60000*100=450000000/6000000=75%

Q4.) Let the break even units be taken as ‘x’.

Sales 100x

Less: Variable cost(45+30) 75x

Contribution 25x

Less: Fixed cost 125000

Expected profit 100000

By solving the equation,

25x-125000=100000

x=9000 units

Break even units required=9000 units.

Q5.) Importance of classifying a fixed cost, variable cost and Semi-variable costs and relevance

to pricing decisions

The file is about cost management and budgeting. The analysis of different types of costs and

relevance to pricing decisions is illustrated. The absorption and marginal costing statements have

been demonstrated and reconciliation of profits has been done. The budget and its role in

controlling the business operations have been emphasised. The different types of budgetary

methods which help in controlling operations have been discussed.

Part A

Q1.) a) Contribution per unit=Sales per unit – Variable cost per unit=100-(45+30)/100=0.25.

Q2.) Break even point(units)= Fixed costs/(sales per unit-variable cost per unit)=125000/(100-

(45+30)=125000/25=5000.

Break even point (sales)= Fixed costs/contribution margin=125000/0.25=500000.

Q3.) Margin of Safety= Current sales level-Break even point/Current sales level=

(60000*100-500000)*100/60000*100=450000000/6000000=75%

Q4.) Let the break even units be taken as ‘x’.

Sales 100x

Less: Variable cost(45+30) 75x

Contribution 25x

Less: Fixed cost 125000

Expected profit 100000

By solving the equation,

25x-125000=100000

x=9000 units

Break even units required=9000 units.

Q5.) Importance of classifying a fixed cost, variable cost and Semi-variable costs and relevance

to pricing decisions

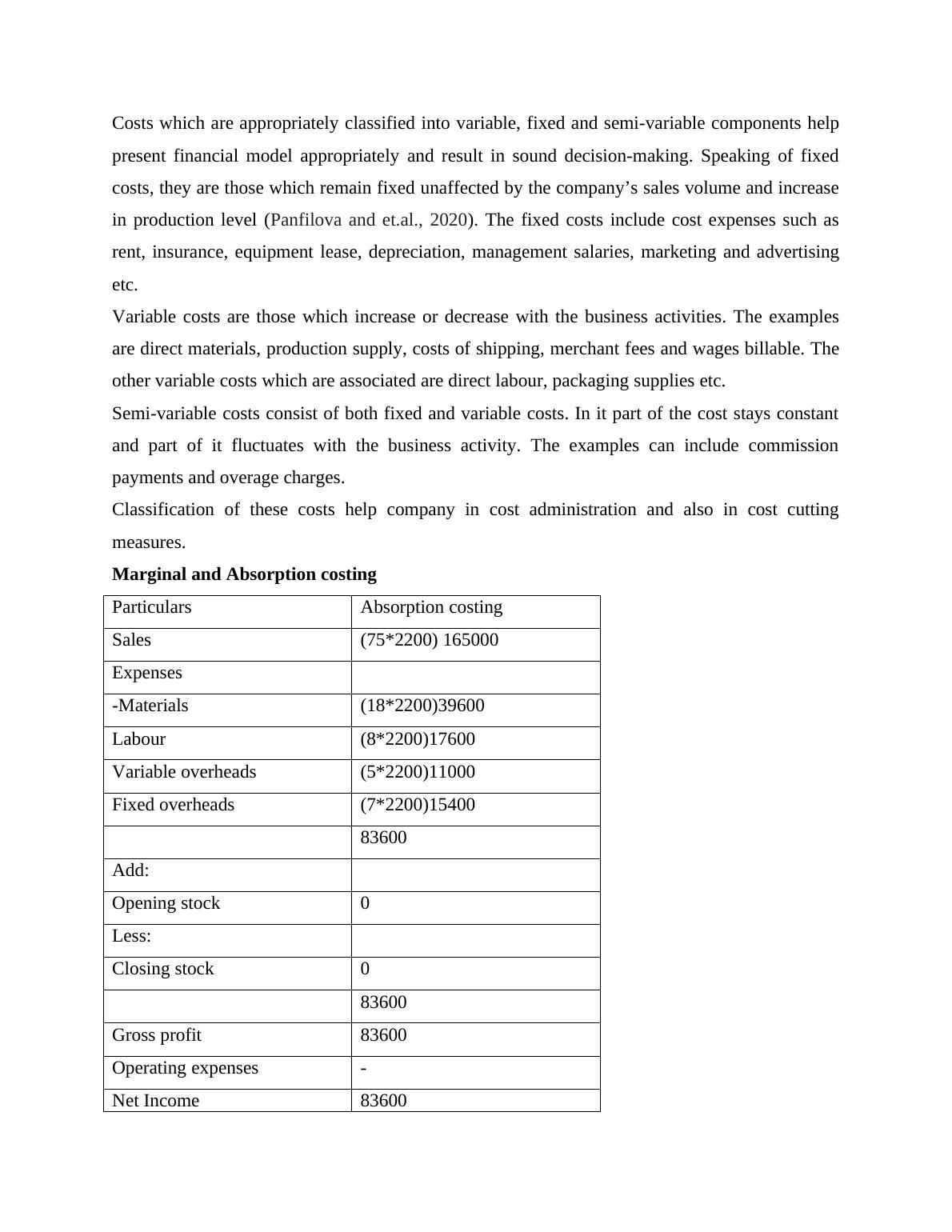

Costs which are appropriately classified into variable, fixed and semi-variable components help

present financial model appropriately and result in sound decision-making. Speaking of fixed

costs, they are those which remain fixed unaffected by the company’s sales volume and increase

in production level (Panfilova and et.al., 2020). The fixed costs include cost expenses such as

rent, insurance, equipment lease, depreciation, management salaries, marketing and advertising

etc.

Variable costs are those which increase or decrease with the business activities. The examples

are direct materials, production supply, costs of shipping, merchant fees and wages billable. The

other variable costs which are associated are direct labour, packaging supplies etc.

Semi-variable costs consist of both fixed and variable costs. In it part of the cost stays constant

and part of it fluctuates with the business activity. The examples can include commission

payments and overage charges.

Classification of these costs help company in cost administration and also in cost cutting

measures.

Marginal and Absorption costing

Particulars Absorption costing

Sales (75*2200) 165000

Expenses

-Materials (18*2200)39600

Labour (8*2200)17600

Variable overheads (5*2200)11000

Fixed overheads (7*2200)15400

83600

Add:

Opening stock 0

Less:

Closing stock 0

83600

Gross profit 83600

Operating expenses -

Net Income 83600

present financial model appropriately and result in sound decision-making. Speaking of fixed

costs, they are those which remain fixed unaffected by the company’s sales volume and increase

in production level (Panfilova and et.al., 2020). The fixed costs include cost expenses such as

rent, insurance, equipment lease, depreciation, management salaries, marketing and advertising

etc.

Variable costs are those which increase or decrease with the business activities. The examples

are direct materials, production supply, costs of shipping, merchant fees and wages billable. The

other variable costs which are associated are direct labour, packaging supplies etc.

Semi-variable costs consist of both fixed and variable costs. In it part of the cost stays constant

and part of it fluctuates with the business activity. The examples can include commission

payments and overage charges.

Classification of these costs help company in cost administration and also in cost cutting

measures.

Marginal and Absorption costing

Particulars Absorption costing

Sales (75*2200) 165000

Expenses

-Materials (18*2200)39600

Labour (8*2200)17600

Variable overheads (5*2200)11000

Fixed overheads (7*2200)15400

83600

Add:

Opening stock 0

Less:

Closing stock 0

83600

Gross profit 83600

Operating expenses -

Net Income 83600

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Management Accountinglg...

|13

|432

|59

Management Accounting Assignment - UCK furniturelg...

|12

|2724

|55

Management Accountinglg...

|10

|367

|55

Management Accounting Assignment : UCK Furniturelg...

|11

|2477

|168

Management Accounting Assignment: UCK Furniturelg...

|9

|2031

|262

Management Accounting: Marginal and Absorption Costing Techniqueslg...

|7

|838

|71