Business Finance

VerifiedAdded on 2023/01/04

|14

|3267

|51

AI Summary

make sure you follow the instructions from the assignment brief, thank you

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

BUSINESS FINANCE

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

MAIN BODY..................................................................................................................................3

Part 1................................................................................................................................................3

Part 2................................................................................................................................................7

Part3.................................................................................................................................................8

REFERENCES..............................................................................................................................12

MAIN BODY..................................................................................................................................3

Part 1................................................................................................................................................3

Part 2................................................................................................................................................7

Part3.................................................................................................................................................8

REFERENCES..............................................................................................................................12

MAIN BODY

Part 1

1.1 Statement of Profit or Loss

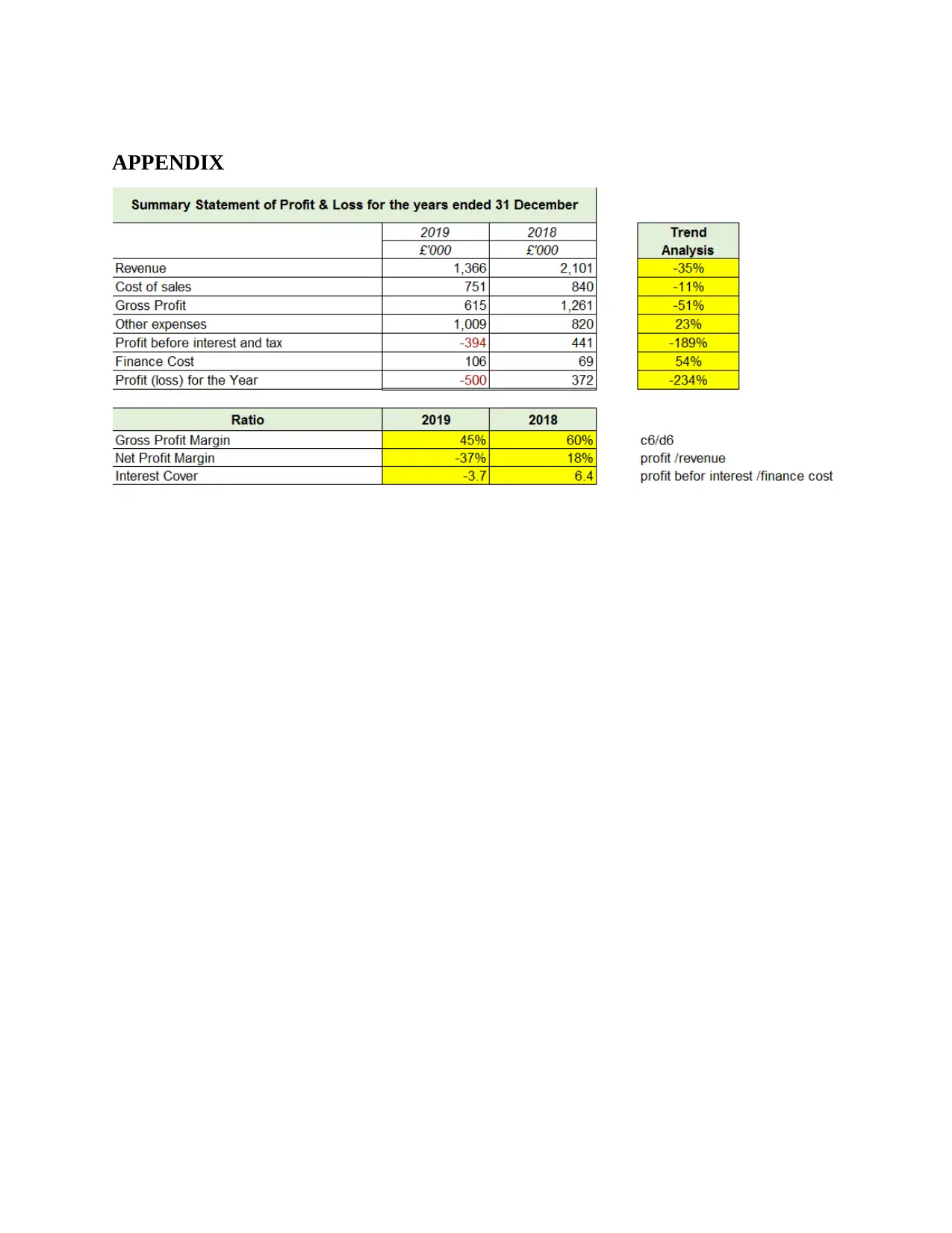

Revenue: Revenue is the profit that regular market operations produce which includes

restrictions and deductions for the stock registered. To calculate the gross pay, which is the key

line or estimate of the total wages through which costs are removed? Income is cash that an

entity puts into the company (Canales, 2016). Tender documents are considered income, an

addition to the expense-to-profit ratio that utilizes revenues in the nominator, as in the

negotiating cost ratio.

Based on the option of accounting utilized, there are distinct methods to calculate revenue.

Collaborative accounting involves investments made using a loan as revenue for the customer's

supplied goods or administrators. To analyze the competitiveness of a company collecting the

money owed, it is crucial to analyze the separate financial. The sales trend line is declining as its

sales have fallen by 35% since 2018. Either due to improvements in public taste or weak

marketing techniques, the cause may be low in consumer spending. As its Gross Margin has also

decreased amid the reduction in Cost of Revenue, price is not perceived as the factor.

Cost of Sales: Business sales expenses have also fallen by 11 percent since 2018, although this

drop is smaller than the downturn in revenue. This suggests a company's inability to manage its

expenses with a drop in sales. Here it is proposed that business should concentrate on steps of

cost management.

Gross Profit: As mentioned above, gross profit has been decreased by 51%. The cause for the

decline in income is an increase in the cost of revenues. Sales prices have risen by 24 percent due

to a 15 percent fall in gross margin since 2018. The organization has three options for growing

gross profit: increasing income, reducing sales time and boosting the price of the commodity.

Operating expenses: It is raised by 23 percent; owing to marketing strategy spending or hiring

additional sales team workers. It is a negative sign for the organization and can be managed by

removing needless marketing plan costs and paying additional workers wages.

Net Profit before tax: The key point is called Net Profit before tax when it first occurs in the

accounting description of a company. Brief expenses are included in maximum pay, also

Part 1

1.1 Statement of Profit or Loss

Revenue: Revenue is the profit that regular market operations produce which includes

restrictions and deductions for the stock registered. To calculate the gross pay, which is the key

line or estimate of the total wages through which costs are removed? Income is cash that an

entity puts into the company (Canales, 2016). Tender documents are considered income, an

addition to the expense-to-profit ratio that utilizes revenues in the nominator, as in the

negotiating cost ratio.

Based on the option of accounting utilized, there are distinct methods to calculate revenue.

Collaborative accounting involves investments made using a loan as revenue for the customer's

supplied goods or administrators. To analyze the competitiveness of a company collecting the

money owed, it is crucial to analyze the separate financial. The sales trend line is declining as its

sales have fallen by 35% since 2018. Either due to improvements in public taste or weak

marketing techniques, the cause may be low in consumer spending. As its Gross Margin has also

decreased amid the reduction in Cost of Revenue, price is not perceived as the factor.

Cost of Sales: Business sales expenses have also fallen by 11 percent since 2018, although this

drop is smaller than the downturn in revenue. This suggests a company's inability to manage its

expenses with a drop in sales. Here it is proposed that business should concentrate on steps of

cost management.

Gross Profit: As mentioned above, gross profit has been decreased by 51%. The cause for the

decline in income is an increase in the cost of revenues. Sales prices have risen by 24 percent due

to a 15 percent fall in gross margin since 2018. The organization has three options for growing

gross profit: increasing income, reducing sales time and boosting the price of the commodity.

Operating expenses: It is raised by 23 percent; owing to marketing strategy spending or hiring

additional sales team workers. It is a negative sign for the organization and can be managed by

removing needless marketing plan costs and paying additional workers wages.

Net Profit before tax: The key point is called Net Profit before tax when it first occurs in the

accounting description of a company. Brief expenses are included in maximum pay, also

recognized as authenticity. When the sales reach the expenditures, there is a benefit. A company

raises sales and lowers costs in order to optimize earnings, and thus the profits of each business

for investors. To assess corporate welfare, accounting analysts also separately consider the gross

revenue and benefits of an entity. Financial expenses will increase as long as, due to cost

savings, sales stay stable. Such a condition just doesn't seem good for an organization's growth.

The two most notable statistics considered are as governmental bodies announce quarterly

profits, revenue and net income ("profit" equals total). Making sure stock additional value largely

depends on whether a company is vastly outstrips or reducing each stock expert's revenue and

benefit.

Net Profit after tax: The Company faces a loss of £ 394,000; the cause for this is a strong 23

percent rise in operational expenses. Either rising net profits or reducing operating costs is the

only way to earn benefit by next year.

1.2 Statement of Financial Position

The balance sheet is also considered as a process to disclose all related details pertaining to the

financial status of the company. It is basically a definition of the financial condition of a person

or a corporation (Adhikary and Kutsuna, 2016). This may be a sole trader, a corporation, a

business group, a legal entity, or some other framework of an organization. This assertion is

important for all forms of being ready. That is useful as it provides a financial situation that is

important and fair. The balance sheet can describe any organization's different major elements,

including such cash, leverage, shares, etc.

Current ratio: The current ratio is a financial measure used inside one year to calculate the

willingness of a company to consider reasonable or due obligations. It guides investors and

lenders on how the business can maximise asset quality to fulfil current short-term obligations.

2018 2019

Current ratio 2.59 times 0.91 times

raises sales and lowers costs in order to optimize earnings, and thus the profits of each business

for investors. To assess corporate welfare, accounting analysts also separately consider the gross

revenue and benefits of an entity. Financial expenses will increase as long as, due to cost

savings, sales stay stable. Such a condition just doesn't seem good for an organization's growth.

The two most notable statistics considered are as governmental bodies announce quarterly

profits, revenue and net income ("profit" equals total). Making sure stock additional value largely

depends on whether a company is vastly outstrips or reducing each stock expert's revenue and

benefit.

Net Profit after tax: The Company faces a loss of £ 394,000; the cause for this is a strong 23

percent rise in operational expenses. Either rising net profits or reducing operating costs is the

only way to earn benefit by next year.

1.2 Statement of Financial Position

The balance sheet is also considered as a process to disclose all related details pertaining to the

financial status of the company. It is basically a definition of the financial condition of a person

or a corporation (Adhikary and Kutsuna, 2016). This may be a sole trader, a corporation, a

business group, a legal entity, or some other framework of an organization. This assertion is

important for all forms of being ready. That is useful as it provides a financial situation that is

important and fair. The balance sheet can describe any organization's different major elements,

including such cash, leverage, shares, etc.

Current ratio: The current ratio is a financial measure used inside one year to calculate the

willingness of a company to consider reasonable or due obligations. It guides investors and

lenders on how the business can maximise asset quality to fulfil current short-term obligations.

2018 2019

Current ratio 2.59 times 0.91 times

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Curr

ent

rati

o

In the year 2019, the following graph stated that the organization is struggling to meet an optimal

current ratio of 2:1 times. The corporation's ratio in 2018 was 2.59 times, while it was 0.91 times

in 2019. This means that the company is not in a position to expend its contract agreements on its

operating assets. There is also a need to control the specific issue so that the existing mix can be

optimized.

Receivable turnover ratio: It is a statistical metric used for both market growth and debt

accumulation to measure how profitable an organisation is (Jordà, Schularick and Taylor, 2016).

The turnover ratio of exchange accounts receivable is a useful ratio measuring how much the

organisation manages its funds.

2018 2019

Receivable turnover ratio 9.64 times 4.48 times

ent

rati

o

In the year 2019, the following graph stated that the organization is struggling to meet an optimal

current ratio of 2:1 times. The corporation's ratio in 2018 was 2.59 times, while it was 0.91 times

in 2019. This means that the company is not in a position to expend its contract agreements on its

operating assets. There is also a need to control the specific issue so that the existing mix can be

optimized.

Receivable turnover ratio: It is a statistical metric used for both market growth and debt

accumulation to measure how profitable an organisation is (Jordà, Schularick and Taylor, 2016).

The turnover ratio of exchange accounts receivable is a useful ratio measuring how much the

organisation manages its funds.

2018 2019

Receivable turnover ratio 9.64 times 4.48 times

Rec

eiva

ble

turn

over

rati

o

Above that the table implies that the firm successfully handled its obligations for the year 2018

although their ratio was 9.64 times, this implies that the liabilities were received at smaller

periods. It was lowered to 4.48 as it was in 2019, noting that in less years, the firm had been

unable to reclaim its debts. The sector has taken more in the year 2019 compared in 2018.

Payable turnover ratio- The turnover ratio of payable profits defines how easily a company

collects investments from lenders and suppliers who expand new loans (Babajide, Olokoyo and

Taiwo, 2016). The auditors evaluate the number of periods the company owes AP funding over a

specified period of time by calculating the cumulative amount of times.

2018 2019

Payable turnover ratio 15.45 times 9.05 times

eiva

ble

turn

over

rati

o

Above that the table implies that the firm successfully handled its obligations for the year 2018

although their ratio was 9.64 times, this implies that the liabilities were received at smaller

periods. It was lowered to 4.48 as it was in 2019, noting that in less years, the firm had been

unable to reclaim its debts. The sector has taken more in the year 2019 compared in 2018.

Payable turnover ratio- The turnover ratio of payable profits defines how easily a company

collects investments from lenders and suppliers who expand new loans (Babajide, Olokoyo and

Taiwo, 2016). The auditors evaluate the number of periods the company owes AP funding over a

specified period of time by calculating the cumulative amount of times.

2018 2019

Payable turnover ratio 15.45 times 9.05 times

Pay

able

turn

over

rati

o

The above table indicates that although the rate was 15.45 times, for 2018 the company handled

its liabilities in a positive way, meaning that their loans were met at fewer intervals. Although it

fell in 2019, in fewer years, this was 9.05 times that perhaps the company could not pay its

obligations. The sector has taken longer in the year 2019 compared in 2018.

Part 2

2.1. Explain the concept of accrual accounting versus cash accounting, including the benefits and

any limitations of each

There are primarily two categories of accounting, cash management and auditing base, since

these are fully checked approaches that are very applicable to the business and are also analyzed

in detail below in regards to T Shirt plc.

Accrual accounting method- A payment is registered, as per this financial accounting

framework, whether it can be calculated in sales for the same duration. Actual cash payments are

new administration in the area of sales directly after period (van der Schans, 2015). The

transaction can only be registered in the cash system at the moment that the cash trade requires it.

Where there is an opportunity for profit or expense on some purchase, the amount will be

recorded in the tax information for the following day. Since profits and expenses are registered

hand-to-hand rather than awaiting as the compensation period, it is very important and is also

done by multinational businesses and big firms. Its biggest advantage is that it is very quick and

easy to run and very useful in doing business with a lot of ease. While the main drawback of this

able

turn

over

rati

o

The above table indicates that although the rate was 15.45 times, for 2018 the company handled

its liabilities in a positive way, meaning that their loans were met at fewer intervals. Although it

fell in 2019, in fewer years, this was 9.05 times that perhaps the company could not pay its

obligations. The sector has taken longer in the year 2019 compared in 2018.

Part 2

2.1. Explain the concept of accrual accounting versus cash accounting, including the benefits and

any limitations of each

There are primarily two categories of accounting, cash management and auditing base, since

these are fully checked approaches that are very applicable to the business and are also analyzed

in detail below in regards to T Shirt plc.

Accrual accounting method- A payment is registered, as per this financial accounting

framework, whether it can be calculated in sales for the same duration. Actual cash payments are

new administration in the area of sales directly after period (van der Schans, 2015). The

transaction can only be registered in the cash system at the moment that the cash trade requires it.

Where there is an opportunity for profit or expense on some purchase, the amount will be

recorded in the tax information for the following day. Since profits and expenses are registered

hand-to-hand rather than awaiting as the compensation period, it is very important and is also

done by multinational businesses and big firms. Its biggest advantage is that it is very quick and

easy to run and very useful in doing business with a lot of ease. While the main drawback of this

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

financial statements is that it requires documenting and a customer's part spending is not

beneficial.

Cash basis accounting: According to this plan, if any cash payment transaction or rights were

made, transfers would only be reported in the accounting statements. Transactions which don't

have any money transfers will not be listed in the accounting period, such as impairment. This

technique is not used in big businesses, but is perfect for large businesses and their related

financial situation, where cash is perceived to be the main form of trade. For an organization

where transactions are sometimes done on the basis of currencies, it is very important. The

biggest value is that it represents in the long run the clear and equitable reputation of the

organization. The greatest downside; however is that it eliminates the employment and

operations of the business and thus has a detrimental effect.

2.2

The big distinction among cash flow and benefit is that the cash flow represents net cash flow,

even if income represents the receipts and expenditures after all payments have been made

(Macve,, 2015).

Business firms also find a measure for understanding a corporation's fitness. In order to see

whether they can spend or direct their market plan, they want to see what the specific amount can

look towards. As two crucial and interconnected profitability measures, revenue stream and

benefit are always at odds: which needs most?

This problem has no clear answer; both benefit and working capital are significant in their own

way. As an investment manager, company owner, key employee, or small businessman, if you

want to evaluate the financial health of a company, people have to comprehend both statistics

and also how those who communicate with one another.

In order to make informed strategic decisions, benefit and working capital are just several of the

many money perspective, indicators, and ratios that you should know. It is possible to pursue

progressively with a complete knowledge of core financial values become a more conservative

businessman or investor.

Part3: Budget techniques and Company Finance

3.1. Define Budget and explain purposes of preparing a budget.

beneficial.

Cash basis accounting: According to this plan, if any cash payment transaction or rights were

made, transfers would only be reported in the accounting statements. Transactions which don't

have any money transfers will not be listed in the accounting period, such as impairment. This

technique is not used in big businesses, but is perfect for large businesses and their related

financial situation, where cash is perceived to be the main form of trade. For an organization

where transactions are sometimes done on the basis of currencies, it is very important. The

biggest value is that it represents in the long run the clear and equitable reputation of the

organization. The greatest downside; however is that it eliminates the employment and

operations of the business and thus has a detrimental effect.

2.2

The big distinction among cash flow and benefit is that the cash flow represents net cash flow,

even if income represents the receipts and expenditures after all payments have been made

(Macve,, 2015).

Business firms also find a measure for understanding a corporation's fitness. In order to see

whether they can spend or direct their market plan, they want to see what the specific amount can

look towards. As two crucial and interconnected profitability measures, revenue stream and

benefit are always at odds: which needs most?

This problem has no clear answer; both benefit and working capital are significant in their own

way. As an investment manager, company owner, key employee, or small businessman, if you

want to evaluate the financial health of a company, people have to comprehend both statistics

and also how those who communicate with one another.

In order to make informed strategic decisions, benefit and working capital are just several of the

many money perspective, indicators, and ratios that you should know. It is possible to pursue

progressively with a complete knowledge of core financial values become a more conservative

businessman or investor.

Part3: Budget techniques and Company Finance

3.1. Define Budget and explain purposes of preparing a budget.

The budget can be defined as a standardized measurement of the cost and profits of a business to

calculate and measure productivity for this variable (Fraser, Bhaumik, and Wright, 2015). The

primary aim of creating a budget is to create a plan for long-term coordination, tracking and

growth of a company's profitability such that the aims and objectives of the company can be

fulfilled in an effective and sustainable manner, even within a limited period of time.

Budget's Reason:

In a continuing process, a carefully crafted budget allows a company to monitor where they will

be economically. This promotes long-term long term planning, from current running costs to

potential expansion, for all. Recognizing where the strategy lands sets up possibilities for

recruiting new employees, engaging in better types of goods, and setting earnings goals in

accordance with the firms' accounting spending needs.

Budgeting is a particularly critical aspect of organizational financial strategy. Chief executives

and management want to be able to foresee whether a company will earn a profit or not. The

purpose of budgeting is basically to provide a roadmap of how the company can work, if certain

strategies, practices, strategies, particularly economically, are pursued.

The purpose of a budget and to provide a financial basis for the decision process, i.e. the

proposed course for action is what firms are planned or not for. When running an enterprise

carefully, spending should be tightly controlled. The presumption that firms should spend money

in ads is likely to be " is probably to be no" before the advertising budget has been thoroughly

invested.

The purpose of budgeting is to allow actual operating productivity to be measured against the

expected financial results, i.e. the company that achieves our objectives (Finance, 2015). In the

equation inverse, the difference between budgeted expenditures and actual spending is

"variability".

Budgeting is highly essential for local managers, who always operate on a limited budget. Also

being slightly off on cost forecasts or profits in a small operation can have a disastrous impact. In

order to ensure that budgeting is carried out properly, it may be worth hiring an in-house or

outside accountant or a specific advisor who has expertise in company finance. This employee

will assist with establishing accounting, managing spending and producing reports to help major

corporations take strategic business decisions that are calculated and educated.

calculate and measure productivity for this variable (Fraser, Bhaumik, and Wright, 2015). The

primary aim of creating a budget is to create a plan for long-term coordination, tracking and

growth of a company's profitability such that the aims and objectives of the company can be

fulfilled in an effective and sustainable manner, even within a limited period of time.

Budget's Reason:

In a continuing process, a carefully crafted budget allows a company to monitor where they will

be economically. This promotes long-term long term planning, from current running costs to

potential expansion, for all. Recognizing where the strategy lands sets up possibilities for

recruiting new employees, engaging in better types of goods, and setting earnings goals in

accordance with the firms' accounting spending needs.

Budgeting is a particularly critical aspect of organizational financial strategy. Chief executives

and management want to be able to foresee whether a company will earn a profit or not. The

purpose of budgeting is basically to provide a roadmap of how the company can work, if certain

strategies, practices, strategies, particularly economically, are pursued.

The purpose of a budget and to provide a financial basis for the decision process, i.e. the

proposed course for action is what firms are planned or not for. When running an enterprise

carefully, spending should be tightly controlled. The presumption that firms should spend money

in ads is likely to be " is probably to be no" before the advertising budget has been thoroughly

invested.

The purpose of budgeting is to allow actual operating productivity to be measured against the

expected financial results, i.e. the company that achieves our objectives (Finance, 2015). In the

equation inverse, the difference between budgeted expenditures and actual spending is

"variability".

Budgeting is highly essential for local managers, who always operate on a limited budget. Also

being slightly off on cost forecasts or profits in a small operation can have a disastrous impact. In

order to ensure that budgeting is carried out properly, it may be worth hiring an in-house or

outside accountant or a specific advisor who has expertise in company finance. This employee

will assist with establishing accounting, managing spending and producing reports to help major

corporations take strategic business decisions that are calculated and educated.

3.2. What might be the main benefits of forming a limited company and listing it on a stock

exchange?

The greatest benefit of forming a limited company is there is no specific sum of money involved

and it is always possible to start a small volume of trade and property ownership is still feasible

and among the most important facets of it. In contrast to this ease of raising funds, it also helps

some kinds of companies (Pindado and Requejo, 2015). While the main advantage of having a

limited partnership listed on the stock exchange would be that additional capital can be added to

the business by using different kinds of equipment used in the market, and thus the business can

future better profitability and performance. Some primary benefits are discussed below in such a

way:

Many businesses have entered a point where it is important to infuse enhanced cash to fund

future planning for growth / expansion. Having it official however is a way of overcoming these

restrictions. The firm boosts the investor base by selling on a stock exchange and improving its

image.

Going public improves the union's visibility and credibility within companies and the purchasing

public as it satisfies numerous compliance standards and maintains transparency during

activities.

By listing, liquidity is enhanced, allowing owners the opportunity to consider the value of their

properties. It encourages participants to swap, share threats and benefit from the growth in

corporate value in the unpaid profits.

Listing provides transparency and utility to the business operations of the organization. The

management and administrative team of a public corporation are accountable to the shareholders.

In particular, the board members would need to allow rapid compliance by attributes that

contribute to the Exchange/shareholders as set out from the Listing Agreement or applicable

guidance.

Going public raises visibility and enhances the public reputation of the firm, thus growing

employees' value and efficiency. That can also lead to the recruiting of new employees and

facilitate stock-based purchases such as ESOPs, etc.

One of the greatest obstacles to market development is the lack of supply of cheap capital. Many

companies listed on the stock exchange are able to raise more attractive capital more quickly by

exchange?

The greatest benefit of forming a limited company is there is no specific sum of money involved

and it is always possible to start a small volume of trade and property ownership is still feasible

and among the most important facets of it. In contrast to this ease of raising funds, it also helps

some kinds of companies (Pindado and Requejo, 2015). While the main advantage of having a

limited partnership listed on the stock exchange would be that additional capital can be added to

the business by using different kinds of equipment used in the market, and thus the business can

future better profitability and performance. Some primary benefits are discussed below in such a

way:

Many businesses have entered a point where it is important to infuse enhanced cash to fund

future planning for growth / expansion. Having it official however is a way of overcoming these

restrictions. The firm boosts the investor base by selling on a stock exchange and improving its

image.

Going public improves the union's visibility and credibility within companies and the purchasing

public as it satisfies numerous compliance standards and maintains transparency during

activities.

By listing, liquidity is enhanced, allowing owners the opportunity to consider the value of their

properties. It encourages participants to swap, share threats and benefit from the growth in

corporate value in the unpaid profits.

Listing provides transparency and utility to the business operations of the organization. The

management and administrative team of a public corporation are accountable to the shareholders.

In particular, the board members would need to allow rapid compliance by attributes that

contribute to the Exchange/shareholders as set out from the Listing Agreement or applicable

guidance.

Going public raises visibility and enhances the public reputation of the firm, thus growing

employees' value and efficiency. That can also lead to the recruiting of new employees and

facilitate stock-based purchases such as ESOPs, etc.

One of the greatest obstacles to market development is the lack of supply of cheap capital. Many

companies listed on the stock exchange are able to raise more attractive capital more quickly by

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

offering new shares to consumers. They would use the funds they raise from issuing bonds to

grow their enterprises to pay for operating expenses.

Stocks also delay taxes of shareholder gains. When investing money, there is no need to file a

return on income if the stock valuation increases (Xiang, Worthington and Higgs, 2015). The

vendor only needs to report the stock changes before selling the stock. Furthermore, if the

investor makes a loss from the disposal of shares, the loss would be used to cover any such

increase in the portfolio through taxes. Interest-bearing liabilities, such as bank accounts or

bonds, are expected to pay tax on taxable profits.

grow their enterprises to pay for operating expenses.

Stocks also delay taxes of shareholder gains. When investing money, there is no need to file a

return on income if the stock valuation increases (Xiang, Worthington and Higgs, 2015). The

vendor only needs to report the stock changes before selling the stock. Furthermore, if the

investor makes a loss from the disposal of shares, the loss would be used to cover any such

increase in the portfolio through taxes. Interest-bearing liabilities, such as bank accounts or

bonds, are expected to pay tax on taxable profits.

REFERENCES

Canales, R., 2016. From ideals to institutions: Institutional entrepreneurship and the growth of

Mexican small business finance. Organization Science, 27(6), pp.1548-1573.

Adhikary, B. and Kutsuna, K., 2016. Small Business Finance in Bangladesh:

Can'Crowdfunding'Be an Alternative?. Review of Integrative Business and Economics

Research, 4, pp.1-21.

Jordà, Ò., Schularick, M. and Taylor, A.M., 2016. The great mortgaging: housing finance, crises

and business cycles. Economic policy, 31(85), pp.107-152.

Babajide, A.A., Olokoyo, F.O. and Taiwo, J.N., 2016. Evaluation of effects of banking

consolidation on small business finance in Nigeria. In Proceedings of the 23rd

International Business Information Management Association Conference (pp. 12522-

12540).

van der Schans, D., 2015. The British Business Bank's role in facilitating economic growth by

addressing imperfections in SME finance markets. Venture Capital, 17(1-2), pp.7-25.

Macve, R.H., 2015. Fair value vs conservatism? Aspects of the history of accounting, auditing,

business and finance from ancient Mesopotamia to modern China. The British

Accounting Review, 47(2), pp.124-141.

Fraser, S., Bhaumik, S.K. and Wright, M., 2015. What do we know about entrepreneurial finance

and its relationship with growth?. International Small Business Journal, 33(1), pp.70-88.

Finance, B., 2015. Business Finance.

Pindado, J. and Requejo, I., 2015. Family business performance from a governance perspective:

A review of empirical research. International Journal of Management Reviews, 17(3),

pp.279-311.

Xiang, D., Worthington, A.C. and Higgs, H., 2015. Discouraged finance seekers: An analysis of

Australian small and medium-sized enterprises. International Small Business

Journal, 33(7), pp.689-707.

Canales, R., 2016. From ideals to institutions: Institutional entrepreneurship and the growth of

Mexican small business finance. Organization Science, 27(6), pp.1548-1573.

Adhikary, B. and Kutsuna, K., 2016. Small Business Finance in Bangladesh:

Can'Crowdfunding'Be an Alternative?. Review of Integrative Business and Economics

Research, 4, pp.1-21.

Jordà, Ò., Schularick, M. and Taylor, A.M., 2016. The great mortgaging: housing finance, crises

and business cycles. Economic policy, 31(85), pp.107-152.

Babajide, A.A., Olokoyo, F.O. and Taiwo, J.N., 2016. Evaluation of effects of banking

consolidation on small business finance in Nigeria. In Proceedings of the 23rd

International Business Information Management Association Conference (pp. 12522-

12540).

van der Schans, D., 2015. The British Business Bank's role in facilitating economic growth by

addressing imperfections in SME finance markets. Venture Capital, 17(1-2), pp.7-25.

Macve, R.H., 2015. Fair value vs conservatism? Aspects of the history of accounting, auditing,

business and finance from ancient Mesopotamia to modern China. The British

Accounting Review, 47(2), pp.124-141.

Fraser, S., Bhaumik, S.K. and Wright, M., 2015. What do we know about entrepreneurial finance

and its relationship with growth?. International Small Business Journal, 33(1), pp.70-88.

Finance, B., 2015. Business Finance.

Pindado, J. and Requejo, I., 2015. Family business performance from a governance perspective:

A review of empirical research. International Journal of Management Reviews, 17(3),

pp.279-311.

Xiang, D., Worthington, A.C. and Higgs, H., 2015. Discouraged finance seekers: An analysis of

Australian small and medium-sized enterprises. International Small Business

Journal, 33(7), pp.689-707.

APPENDIX

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Summary Statement of Financial Position as at 31 December

2019 2018

ASSETS £'000 £'000

Non-current Assets Property

Plant and Equipment 1,274 1,282

Current Assets

Inventories 121 89

Trade and other receivables 305 218

Cash and cash equivalents - 45

Total Current Assets 426 352

Total Assets 1,700 1,634

EQUITY AND LIABILITIES

Equity

Share Capital 310 310

Retained Earnings - 500

Total Equity 310 810

Non-current Liabilities

Long-term borrowings 921 688

921 688

Current Liabilities

Trade payables 151 136

Bank overdraft 318 -

Total Current Liabilities 469 136

Total Liabilities 1,390 824

Total Equity and Liabilities 1,700 1,634

- -

Ratio 2019 2018

Current Ratio 0.908315565 2.5882352941 0.9 :1

Quick Ratio 0.7 1.9

Inventory Days 58.81 38.67 days

Trade Receivable Days 81 38 days

Trade Payable Days 73 59 days

Operating Cash Cycle 67 17 days

All Sales and Purchases are on Credit.

Use the COS for Payable Days Calculations

2019 2018

ASSETS £'000 £'000

Non-current Assets Property

Plant and Equipment 1,274 1,282

Current Assets

Inventories 121 89

Trade and other receivables 305 218

Cash and cash equivalents - 45

Total Current Assets 426 352

Total Assets 1,700 1,634

EQUITY AND LIABILITIES

Equity

Share Capital 310 310

Retained Earnings - 500

Total Equity 310 810

Non-current Liabilities

Long-term borrowings 921 688

921 688

Current Liabilities

Trade payables 151 136

Bank overdraft 318 -

Total Current Liabilities 469 136

Total Liabilities 1,390 824

Total Equity and Liabilities 1,700 1,634

- -

Ratio 2019 2018

Current Ratio 0.908315565 2.5882352941 0.9 :1

Quick Ratio 0.7 1.9

Inventory Days 58.81 38.67 days

Trade Receivable Days 81 38 days

Trade Payable Days 73 59 days

Operating Cash Cycle 67 17 days

All Sales and Purchases are on Credit.

Use the COS for Payable Days Calculations

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.