Business Finance Report: Cash Flow, Budgeting, and Working Capital

VerifiedAdded on 2023/01/18

|12

|3427

|29

Report

AI Summary

This report analyzes key aspects of business finance, focusing on cash flow, budgeting, and working capital management. Part 1 examines the relationship between profit and cash flow, highlighting their differences and the impact of working capital on cash flow. It includes an analysis of cash flow statements and recommends strategies for improving cash flow through effective working capital management, such as optimizing inventory, managing receivables and payables, and considering long-term financing. Part 2 explores budgeting techniques, comparing traditional and alternative methods like rolling and zero-based budgets. The report evaluates the purpose of budgeting, describes the application of these methods, and assesses the suitability of alternative versus traditional budgetary systems for BoatWorld Plc. The report emphasizes the importance of these financial tools for business performance and decision-making.

BUSINESS FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

TABLE OF CONTENTS................................................................................................................2

PART 1............................................................................................................................................1

Executive summary.....................................................................................................................1

I) Explanations.............................................................................................................................1

II) Analysis of Cash Flow statements..........................................................................................3

III) Steps to be taken for improving the cash flows by working capital management................4

PART 2............................................................................................................................................5

Executive Summary.....................................................................................................................5

I) Purpose of preparing budget and understanding traditional budgeting approach and

alternative budget methods..........................................................................................................5

II Describing the application of these methods for future...........................................................7

III) Analysing whether alternative budgetary system or traditional budgetary system is

appropriate...................................................................................................................................8

REFERENCES..............................................................................................................................10

TABLE OF CONTENTS................................................................................................................2

PART 1............................................................................................................................................1

Executive summary.....................................................................................................................1

I) Explanations.............................................................................................................................1

II) Analysis of Cash Flow statements..........................................................................................3

III) Steps to be taken for improving the cash flows by working capital management................4

PART 2............................................................................................................................................5

Executive Summary.....................................................................................................................5

I) Purpose of preparing budget and understanding traditional budgeting approach and

alternative budget methods..........................................................................................................5

II Describing the application of these methods for future...........................................................7

III) Analysing whether alternative budgetary system or traditional budgetary system is

appropriate...................................................................................................................................8

REFERENCES..............................................................................................................................10

PART 1

Executive summary

This part reveals the importance of cash flows and the profits. They help in determining how

cash flows could be negative even when the company is showing profits. There are various cases

where the profitability is shown. Working capital of the company could be used for managing

the cash flows and how they impact the cash flows. It will also recommend steps that could be

used for improving the cash flows.

Report to the shareholders

I) Explanations

a) Profit and Cash Flows and how they are different

Profits

Profits of a company describes financial benefits realized when revenues generated from

business activities exceeds costs, expenses and taxes that are involved in sustaining activity.

Profits earned by the business funnel back to its owners , who have the choice of using this profit

for their own benefits or to reinvest back into business. Profits are calculated as total revenues

less total expense. Profits refers to the money pulled by the business after all the expenses have

been accounted. Be it a sole proprietary business or a multinational company primary goal of

every business is of earning money, therefore performance of the business is measured based on

its profitability. Profits are of three types gross profits, operating profits and net profits and all of

these are shown in income statement of company (Williams and Dobelman, J.A., 2017). Every

profit gives different type of information that are used by the analysts according to their needs.

Cash Flow

Cash flow refers to the amount of net cash & cash equivalent that are being transferred in

and out of business. At basic fundamental level, cash flows determine the ability of company to

generate positive cash flows and create values for its shareholders. It is also aimed at maximising

the long term cash flows. Assessing amounts, timings and uncertainty in cash flows is also the

objective of financial reporting. For assessing the flexibility, liquidity and financial performance

of the company it is essential to have an understanding of the cash flows(Miao, Teoh and Zhu,

2016). Cash flows are important for recognising whether the company is utilising the cash funds

in an efficient manner or not.

1

Executive summary

This part reveals the importance of cash flows and the profits. They help in determining how

cash flows could be negative even when the company is showing profits. There are various cases

where the profitability is shown. Working capital of the company could be used for managing

the cash flows and how they impact the cash flows. It will also recommend steps that could be

used for improving the cash flows.

Report to the shareholders

I) Explanations

a) Profit and Cash Flows and how they are different

Profits

Profits of a company describes financial benefits realized when revenues generated from

business activities exceeds costs, expenses and taxes that are involved in sustaining activity.

Profits earned by the business funnel back to its owners , who have the choice of using this profit

for their own benefits or to reinvest back into business. Profits are calculated as total revenues

less total expense. Profits refers to the money pulled by the business after all the expenses have

been accounted. Be it a sole proprietary business or a multinational company primary goal of

every business is of earning money, therefore performance of the business is measured based on

its profitability. Profits are of three types gross profits, operating profits and net profits and all of

these are shown in income statement of company (Williams and Dobelman, J.A., 2017). Every

profit gives different type of information that are used by the analysts according to their needs.

Cash Flow

Cash flow refers to the amount of net cash & cash equivalent that are being transferred in

and out of business. At basic fundamental level, cash flows determine the ability of company to

generate positive cash flows and create values for its shareholders. It is also aimed at maximising

the long term cash flows. Assessing amounts, timings and uncertainty in cash flows is also the

objective of financial reporting. For assessing the flexibility, liquidity and financial performance

of the company it is essential to have an understanding of the cash flows(Miao, Teoh and Zhu,

2016). Cash flows are important for recognising whether the company is utilising the cash funds

in an efficient manner or not.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Difference in Cash flows and the profits

Profit and cash flows are separate financial parameters, and both are to be considered when

running business for keeping the track record. Companies are required to report over both profits

and cash holdings. Profit is accounting that is not measurable in cash inflow or outflow.

Operating Cash Flows

It is outcome of cash activities in business operation regardless, whether cash transactions

are generating earned revenues or incurred expenses at time of transaction. For instance when

when advance payments are received from customers it will increase the cash holdings of the

company but no effect would be seen on its reported profit (Sri, 2017).

Non Operating Cash Flows

Few cash flows may not be the outcome of operating activities of the company and may

not be related to the profitability. Along with operating activities cash flow from financing and

investing activities are also reported by the company. When investments are sold or funds are

obtained from financing , cash positions are increased, but they are not added to the revenues.

Similarly purchase of fixed assets will decrease the cash positions but the profits will not be

harmed. Heavy purchases can result in negative cash flows even when the company is showing

good profits (Gordon and et.al., 2017).

Non Cash Revenues

Non Cash revenues are the profit arising on sale of fixed assets, or the company recording

accrued profits this will increase the profits but no change in the cash holdings.

Non Cash Expenses

They decrease the profitability of the company but no impact is seen in cash holdings as

they do not result in any cash outflows like depreciation.

There are situation where company may show profits but do not have enough cash for meeting

the daily expenses. This may result in the break down of company operations. This sometimes

cause the company to liquidate due to non availability of cash.

b)Working Capital

Working Capital refers to difference between current asset like accounts receivables, cash

and inventories and the current liabilities like accounts payable. Working capital measures

operational efficiency, liquidity and short term financials health of the organisation. Company

2

Profit and cash flows are separate financial parameters, and both are to be considered when

running business for keeping the track record. Companies are required to report over both profits

and cash holdings. Profit is accounting that is not measurable in cash inflow or outflow.

Operating Cash Flows

It is outcome of cash activities in business operation regardless, whether cash transactions

are generating earned revenues or incurred expenses at time of transaction. For instance when

when advance payments are received from customers it will increase the cash holdings of the

company but no effect would be seen on its reported profit (Sri, 2017).

Non Operating Cash Flows

Few cash flows may not be the outcome of operating activities of the company and may

not be related to the profitability. Along with operating activities cash flow from financing and

investing activities are also reported by the company. When investments are sold or funds are

obtained from financing , cash positions are increased, but they are not added to the revenues.

Similarly purchase of fixed assets will decrease the cash positions but the profits will not be

harmed. Heavy purchases can result in negative cash flows even when the company is showing

good profits (Gordon and et.al., 2017).

Non Cash Revenues

Non Cash revenues are the profit arising on sale of fixed assets, or the company recording

accrued profits this will increase the profits but no change in the cash holdings.

Non Cash Expenses

They decrease the profitability of the company but no impact is seen in cash holdings as

they do not result in any cash outflows like depreciation.

There are situation where company may show profits but do not have enough cash for meeting

the daily expenses. This may result in the break down of company operations. This sometimes

cause the company to liquidate due to non availability of cash.

b)Working Capital

Working Capital refers to difference between current asset like accounts receivables, cash

and inventories and the current liabilities like accounts payable. Working capital measures

operational efficiency, liquidity and short term financials health of the organisation. Company

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

having positive working capital have the potential of investing and growing. If the current assets

are not exceeding current liabilities, company might face trouble in paying back to creditors or

growing it may even go bankrupt (Kopita, Charitou and Karamanou, 2017).

Receivables- It refers to the amount due from customers to whom goods have been sold on

credit.

Inventory- It refers to the stock of goods manufactured or traded by company. Inventory could

be of raw materials or the finished goods. Inventory of the company are current assets of

company.

Trade Payable- Like receivables, payables are the amount due to the supplier of the raw

materials from whom company have taken goods on credit. These are shown under head current

liabilities.

c) Effects of working capital on cash flows

Increases in working capital shows that more amount of cash is being invested in the working

capital, thereby reducing the cash flows. Those companies having significant requirements of

working capital finds that the working capital also grows and this would be reducing the cash

flows of company. There is a relationship between cash flows and the working capital,

companies that efficiently manage their working capital have high value as compared with firms

having high working capital requirements (Girish and Desai, 2017).

II) Analysis of Cash Flow statements

Analysing the cash flow statement of the company it could be said that the company is

not efficiently managing its cash flows. The operating profit of the company is just 5 million that

is 10% of the total turnover. The debts of the company have increased by 2 million that will

increase inflow in financing activities. Cash flows of 10 million will be considered in investing

activities where the 8 millions of advance will be increase the working capital. Company is

having current liability of 1.5 million, but this will not affect the cash flows of company. Cash

flows of the company will show positive results. The contingent liability of 2 million will affect

the cash flows. But the increase in cash flows will not be increasing the profitability of company.

3

are not exceeding current liabilities, company might face trouble in paying back to creditors or

growing it may even go bankrupt (Kopita, Charitou and Karamanou, 2017).

Receivables- It refers to the amount due from customers to whom goods have been sold on

credit.

Inventory- It refers to the stock of goods manufactured or traded by company. Inventory could

be of raw materials or the finished goods. Inventory of the company are current assets of

company.

Trade Payable- Like receivables, payables are the amount due to the supplier of the raw

materials from whom company have taken goods on credit. These are shown under head current

liabilities.

c) Effects of working capital on cash flows

Increases in working capital shows that more amount of cash is being invested in the working

capital, thereby reducing the cash flows. Those companies having significant requirements of

working capital finds that the working capital also grows and this would be reducing the cash

flows of company. There is a relationship between cash flows and the working capital,

companies that efficiently manage their working capital have high value as compared with firms

having high working capital requirements (Girish and Desai, 2017).

II) Analysis of Cash Flow statements

Analysing the cash flow statement of the company it could be said that the company is

not efficiently managing its cash flows. The operating profit of the company is just 5 million that

is 10% of the total turnover. The debts of the company have increased by 2 million that will

increase inflow in financing activities. Cash flows of 10 million will be considered in investing

activities where the 8 millions of advance will be increase the working capital. Company is

having current liability of 1.5 million, but this will not affect the cash flows of company. Cash

flows of the company will show positive results. The contingent liability of 2 million will affect

the cash flows. But the increase in cash flows will not be increasing the profitability of company.

3

Therefore it is essential to effectively manage the cash flows and working capital of the company

(Ketz, 2016).

III) Steps to be taken for improving the cash flows by working capital management.

Working capital means amount through which current asset of company exceeds the current

liabilities. Cash flows of the company could be improved by effectively managing the working

capital of company. Here the company is growing at constant pace with sufficient profits than

also the company may face negative cash flows. Therefore it is essential for company to manage

properly its cash flows.

Cash flows could be improved by managing the working capital.

Improving the Inventory

VLE should conduct inventory checks over short periods so that goods that are not moving at

same pace like other goods are identified. Company should offer more discounts for selling the

products that will increase the turnover and cash inflow to the company. It should not store

inventory that is unnecessary occupying space (Mathuva, 2015).

Trade Receivables

VLE should check the credibility of customers before selling goods to customer on credit.

Charge interest on delay over the specified limit in credit days. Reduce the credit days for

rotation of the cash flows.

Trade Payables

For the suppliers VLE should maintain friendly relations with them. This will help in bargaining

better trading terms. Ask for discounts from suppliers on early payments for the purchases.

Raising long term loans

Company for carrying out the working capital requirements should go for long term loans instead

of short term loans this will decrease the current liabilities of company (Aktas, Croci. and

Petmezas, 2015).

4

(Ketz, 2016).

III) Steps to be taken for improving the cash flows by working capital management.

Working capital means amount through which current asset of company exceeds the current

liabilities. Cash flows of the company could be improved by effectively managing the working

capital of company. Here the company is growing at constant pace with sufficient profits than

also the company may face negative cash flows. Therefore it is essential for company to manage

properly its cash flows.

Cash flows could be improved by managing the working capital.

Improving the Inventory

VLE should conduct inventory checks over short periods so that goods that are not moving at

same pace like other goods are identified. Company should offer more discounts for selling the

products that will increase the turnover and cash inflow to the company. It should not store

inventory that is unnecessary occupying space (Mathuva, 2015).

Trade Receivables

VLE should check the credibility of customers before selling goods to customer on credit.

Charge interest on delay over the specified limit in credit days. Reduce the credit days for

rotation of the cash flows.

Trade Payables

For the suppliers VLE should maintain friendly relations with them. This will help in bargaining

better trading terms. Ask for discounts from suppliers on early payments for the purchases.

Raising long term loans

Company for carrying out the working capital requirements should go for long term loans instead

of short term loans this will decrease the current liabilities of company (Aktas, Croci. and

Petmezas, 2015).

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

PART 2

Executive Summary

Budgeting techniques are an important part in determining what are the various expenditures and

sources of income for a business and in this part various budgeting techniques have been

evaluated to identify the best one for BoatWorld Plc.

I) Purpose of preparing budget and understanding traditional budgeting approach and alternative

budget methods

A budget is prepared by the organisations in order to predict initially what are the future

income and expenditure sources for the company and further it helps in determining what would

be the adequate number o f resources that need to be allocated amongst various activities that an

organisation needs to prefer (Opgenoord and Willcox, 2016). Further, it acts a s a decision

making tools for the company where they are able to determine how much expenditure will be

there and which tools or either assets are too be brought and which are not within the buying

range etc. are highlighted. In this budget reports, it also acts as a method and means to monitor

and evaluate the performance of the organization so that it can be ascertained whether the

standards that have been set up are being met or not and whether the work done is appropriate or

not.

The Traditional Budgeting Process is indeed a traditional and redundant process where

the budget that was prepared last year is taken as a base for the preparation of current year’s

budget. The figures and heads that were formulated in the budget of last year is kept same and

only the amount is incremented to the one that was allotted in the last year, i.e. there is no writing

off of the budget and it keeps on being carried forward in the organisation. Although it is an

extremely easy and quick method of budget preparation yet, in today’s context, it can be said that

this is not an adequate method since it does not highlight what was the individual years

performance and further, fails to take into purview various new factors that have emerged in the

market (Popesko and Šocová, 2016). At BoatWorld Plc as well, the recently appointed finance

director recognised that the current budgeting method that was being used in the company, i.e.

the traditional budgeting system is extremely redundant and was not depicting the true

performance of the company. He intends to change it and replace with other more efficient

budgeting technique. The alternative budgeting techniques that can be used are:

5

Executive Summary

Budgeting techniques are an important part in determining what are the various expenditures and

sources of income for a business and in this part various budgeting techniques have been

evaluated to identify the best one for BoatWorld Plc.

I) Purpose of preparing budget and understanding traditional budgeting approach and alternative

budget methods

A budget is prepared by the organisations in order to predict initially what are the future

income and expenditure sources for the company and further it helps in determining what would

be the adequate number o f resources that need to be allocated amongst various activities that an

organisation needs to prefer (Opgenoord and Willcox, 2016). Further, it acts a s a decision

making tools for the company where they are able to determine how much expenditure will be

there and which tools or either assets are too be brought and which are not within the buying

range etc. are highlighted. In this budget reports, it also acts as a method and means to monitor

and evaluate the performance of the organization so that it can be ascertained whether the

standards that have been set up are being met or not and whether the work done is appropriate or

not.

The Traditional Budgeting Process is indeed a traditional and redundant process where

the budget that was prepared last year is taken as a base for the preparation of current year’s

budget. The figures and heads that were formulated in the budget of last year is kept same and

only the amount is incremented to the one that was allotted in the last year, i.e. there is no writing

off of the budget and it keeps on being carried forward in the organisation. Although it is an

extremely easy and quick method of budget preparation yet, in today’s context, it can be said that

this is not an adequate method since it does not highlight what was the individual years

performance and further, fails to take into purview various new factors that have emerged in the

market (Popesko and Šocová, 2016). At BoatWorld Plc as well, the recently appointed finance

director recognised that the current budgeting method that was being used in the company, i.e.

the traditional budgeting system is extremely redundant and was not depicting the true

performance of the company. He intends to change it and replace with other more efficient

budgeting technique. The alternative budgeting techniques that can be used are:

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

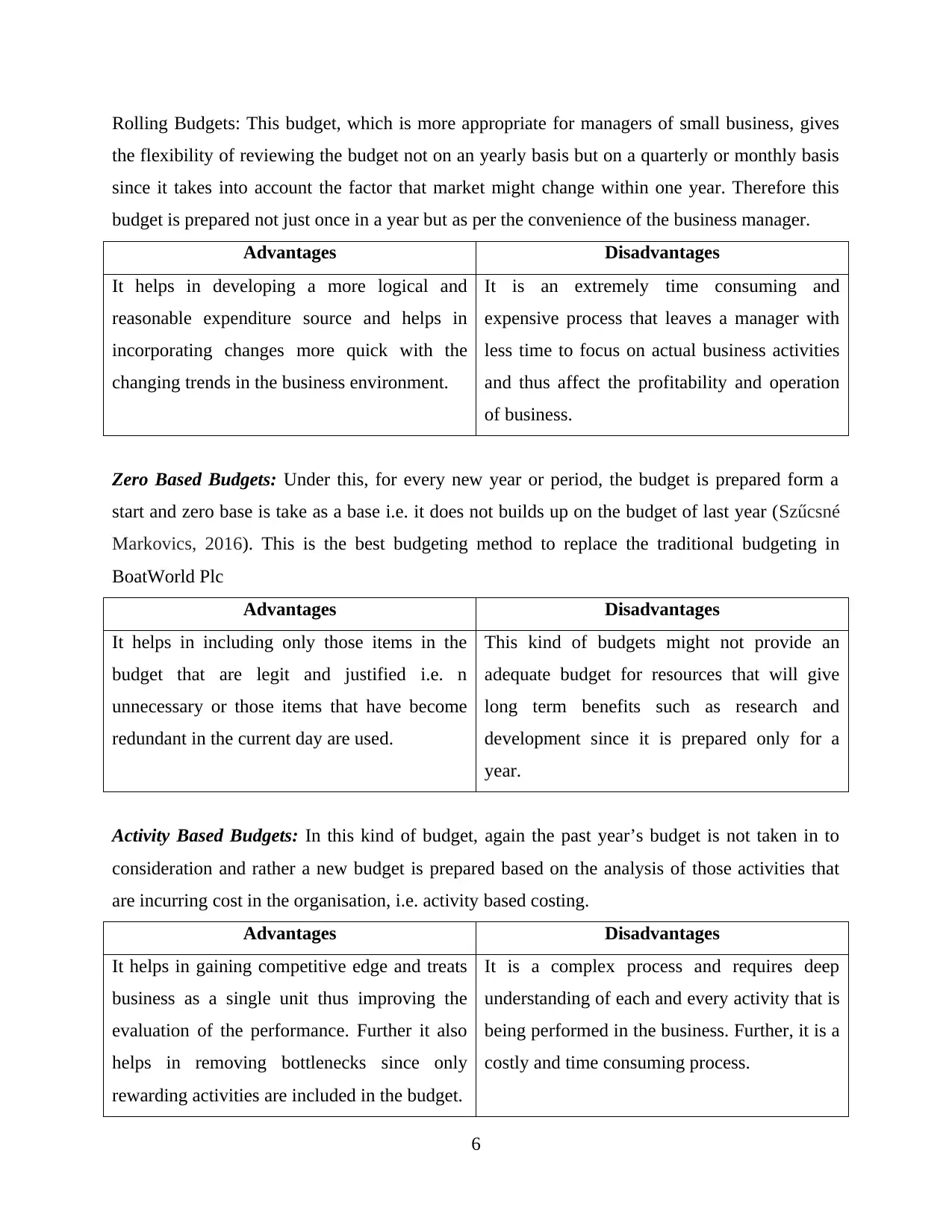

Rolling Budgets: This budget, which is more appropriate for managers of small business, gives

the flexibility of reviewing the budget not on an yearly basis but on a quarterly or monthly basis

since it takes into account the factor that market might change within one year. Therefore this

budget is prepared not just once in a year but as per the convenience of the business manager.

Advantages Disadvantages

It helps in developing a more logical and

reasonable expenditure source and helps in

incorporating changes more quick with the

changing trends in the business environment.

It is an extremely time consuming and

expensive process that leaves a manager with

less time to focus on actual business activities

and thus affect the profitability and operation

of business.

Zero Based Budgets: Under this, for every new year or period, the budget is prepared form a

start and zero base is take as a base i.e. it does not builds up on the budget of last year (Szűcsné

Markovics, 2016). This is the best budgeting method to replace the traditional budgeting in

BoatWorld Plc

Advantages Disadvantages

It helps in including only those items in the

budget that are legit and justified i.e. n

unnecessary or those items that have become

redundant in the current day are used.

This kind of budgets might not provide an

adequate budget for resources that will give

long term benefits such as research and

development since it is prepared only for a

year.

Activity Based Budgets: In this kind of budget, again the past year’s budget is not taken in to

consideration and rather a new budget is prepared based on the analysis of those activities that

are incurring cost in the organisation, i.e. activity based costing.

Advantages Disadvantages

It helps in gaining competitive edge and treats

business as a single unit thus improving the

evaluation of the performance. Further it also

helps in removing bottlenecks since only

rewarding activities are included in the budget.

It is a complex process and requires deep

understanding of each and every activity that is

being performed in the business. Further, it is a

costly and time consuming process.

6

the flexibility of reviewing the budget not on an yearly basis but on a quarterly or monthly basis

since it takes into account the factor that market might change within one year. Therefore this

budget is prepared not just once in a year but as per the convenience of the business manager.

Advantages Disadvantages

It helps in developing a more logical and

reasonable expenditure source and helps in

incorporating changes more quick with the

changing trends in the business environment.

It is an extremely time consuming and

expensive process that leaves a manager with

less time to focus on actual business activities

and thus affect the profitability and operation

of business.

Zero Based Budgets: Under this, for every new year or period, the budget is prepared form a

start and zero base is take as a base i.e. it does not builds up on the budget of last year (Szűcsné

Markovics, 2016). This is the best budgeting method to replace the traditional budgeting in

BoatWorld Plc

Advantages Disadvantages

It helps in including only those items in the

budget that are legit and justified i.e. n

unnecessary or those items that have become

redundant in the current day are used.

This kind of budgets might not provide an

adequate budget for resources that will give

long term benefits such as research and

development since it is prepared only for a

year.

Activity Based Budgets: In this kind of budget, again the past year’s budget is not taken in to

consideration and rather a new budget is prepared based on the analysis of those activities that

are incurring cost in the organisation, i.e. activity based costing.

Advantages Disadvantages

It helps in gaining competitive edge and treats

business as a single unit thus improving the

evaluation of the performance. Further it also

helps in removing bottlenecks since only

rewarding activities are included in the budget.

It is a complex process and requires deep

understanding of each and every activity that is

being performed in the business. Further, it is a

costly and time consuming process.

6

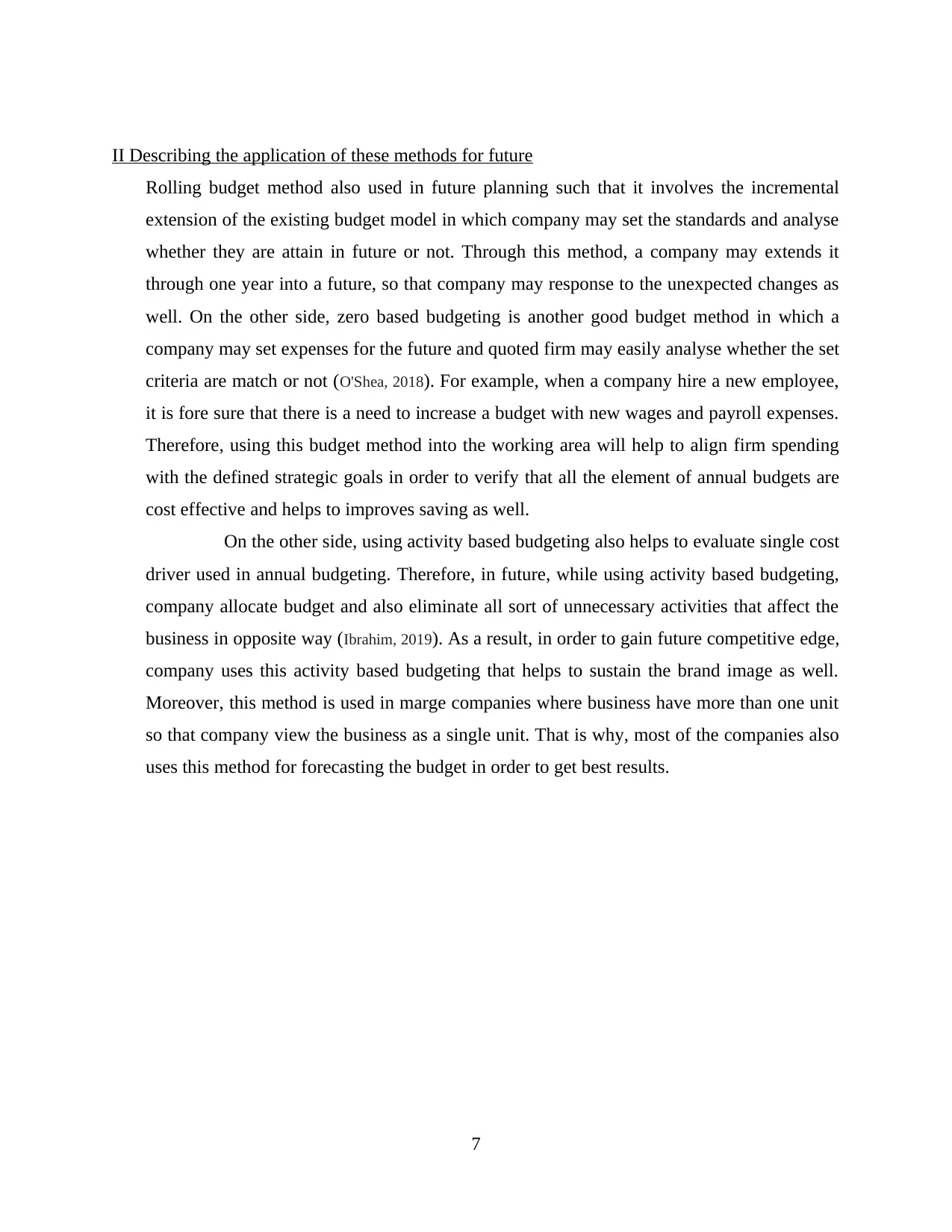

II Describing the application of these methods for future

Rolling budget method also used in future planning such that it involves the incremental

extension of the existing budget model in which company may set the standards and analyse

whether they are attain in future or not. Through this method, a company may extends it

through one year into a future, so that company may response to the unexpected changes as

well. On the other side, zero based budgeting is another good budget method in which a

company may set expenses for the future and quoted firm may easily analyse whether the set

criteria are match or not (O'Shea, 2018). For example, when a company hire a new employee,

it is fore sure that there is a need to increase a budget with new wages and payroll expenses.

Therefore, using this budget method into the working area will help to align firm spending

with the defined strategic goals in order to verify that all the element of annual budgets are

cost effective and helps to improves saving as well.

On the other side, using activity based budgeting also helps to evaluate single cost

driver used in annual budgeting. Therefore, in future, while using activity based budgeting,

company allocate budget and also eliminate all sort of unnecessary activities that affect the

business in opposite way (Ibrahim, 2019). As a result, in order to gain future competitive edge,

company uses this activity based budgeting that helps to sustain the brand image as well.

Moreover, this method is used in marge companies where business have more than one unit

so that company view the business as a single unit. That is why, most of the companies also

uses this method for forecasting the budget in order to get best results.

7

Rolling budget method also used in future planning such that it involves the incremental

extension of the existing budget model in which company may set the standards and analyse

whether they are attain in future or not. Through this method, a company may extends it

through one year into a future, so that company may response to the unexpected changes as

well. On the other side, zero based budgeting is another good budget method in which a

company may set expenses for the future and quoted firm may easily analyse whether the set

criteria are match or not (O'Shea, 2018). For example, when a company hire a new employee,

it is fore sure that there is a need to increase a budget with new wages and payroll expenses.

Therefore, using this budget method into the working area will help to align firm spending

with the defined strategic goals in order to verify that all the element of annual budgets are

cost effective and helps to improves saving as well.

On the other side, using activity based budgeting also helps to evaluate single cost

driver used in annual budgeting. Therefore, in future, while using activity based budgeting,

company allocate budget and also eliminate all sort of unnecessary activities that affect the

business in opposite way (Ibrahim, 2019). As a result, in order to gain future competitive edge,

company uses this activity based budgeting that helps to sustain the brand image as well.

Moreover, this method is used in marge companies where business have more than one unit

so that company view the business as a single unit. That is why, most of the companies also

uses this method for forecasting the budget in order to get best results.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

III) Analysing whether alternative budgetary system or traditional budgetary system is

appropriate.

Traditional budgeting refer to process of making projections for revenues & expenses of

the business for upcoming year reviewing the previous budgets. It involves projecting the sales

and revenues, estimation of expenses & predicting profits. They do not cover cover rate of

inflations in their budget. Traditional budget follows previous year's data for making the budget

The modern budgeting techniques are standing on the same foundation but with

modification with the time. They take into account all the adjustments required for making the

budget. Modern budgets are more flexible and could be modified according to the requirements

of company and specific activities. Modern budgeting technique provide for different budgets

that for different activities of different industry (Gordon and et.al., 2017).

Company should go for modern budgeting techniques as it includes more than one

budgeting technique that could be used by the Boat World Plc. Company has the business of

renting boats. Every year there are some or the other changes the that affect the tourism industry

in different countries. Budgets of previous year cannot be used by company for the current year

as the errors f previous year might occur in present year. Budgeting techniques like zero based

8

appropriate.

Traditional budgeting refer to process of making projections for revenues & expenses of

the business for upcoming year reviewing the previous budgets. It involves projecting the sales

and revenues, estimation of expenses & predicting profits. They do not cover cover rate of

inflations in their budget. Traditional budget follows previous year's data for making the budget

The modern budgeting techniques are standing on the same foundation but with

modification with the time. They take into account all the adjustments required for making the

budget. Modern budgets are more flexible and could be modified according to the requirements

of company and specific activities. Modern budgeting technique provide for different budgets

that for different activities of different industry (Gordon and et.al., 2017).

Company should go for modern budgeting techniques as it includes more than one

budgeting technique that could be used by the Boat World Plc. Company has the business of

renting boats. Every year there are some or the other changes the that affect the tourism industry

in different countries. Budgets of previous year cannot be used by company for the current year

as the errors f previous year might occur in present year. Budgeting techniques like zero based

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

budgeting and rolling budgets could be used. Company could use zero based budgeting that

requires the budgets to be prepared from the beginning taking base as zero. It will help company

in preparing budgets based for the every year that are not based on previous budgets.

9

requires the budgets to be prepared from the beginning taking base as zero. It will help company

in preparing budgets based for the every year that are not based on previous budgets.

9

REFERENCES

Books and Journals

Aktas, N., Croci, E. and Petmezas, D., 2015. Is working capital management value-enhancing?

Evidence from firm performance and investments. Journal of Corporate

Finance.30.pp.98-113.

Girish, S. and Desai, K., 2017. Impact of cash flow from operating and financial activities

information on share price: Empirical evidence from nifty Pharma index companies,

India. International Journal of Management Research and Reviews.7(11). pp.1029-1033.

Gordon, E.A. and et.al., 2017. Flexibility in cash-flow classification under IFRS: determinants

and consequences. Review of Accounting Studies.22(2). pp.839-872.

Ibrahim, M. M., 2019. Designing zero-based budgeting for public organizations. Problems and

Perspectives in Management. 17(2).

Ketz, J.E., 2016. Free Cash Flow and Business Combinations. The CPA Journal.86(11).pp.48-

53.

Kopita, A.S., Charitou, A. and Karamanou, I., 2017. The determinants and valuation effects of

classification choice on the statement of cash flows. Accounting and Business Research.

Mathuva, D., 2015. The Influence of working capital management components on corporate

profitability.

Miao, B., Teoh, S.H. and Zhu, Z., 2016. Limited attention, statement of cash flow disclosure, and

the valuation of accruals. Review of Accounting Studies.21(2). pp.473-515.

Opgenoord, M.M. and Willcox, K.E., 2016. Sensitivity analysis methods for uncertainty

budgeting in system design. AIAA Journal, pp.3134-3148.

O'Shea, J. P., 2018. Viability of Zero-Based Budgeting Methods in the City of Albuquerque.

Popesko, B. and Šocová, V., 2016. Current trends in budgeting and planning: Czech survey

initial results. International Advances in Economic Research, 22(1). pp.99-100.

Sri, B.P., 2017. An assignment on A study on cash flow statement analysis with special reference

to jet airways. Journal Homepage: http://www. ijmra. us, 7(11).

Szűcsné Markovics, K., 2016. Capital budgeting methods used in some European countries and

in the United States. Universal Journal of Management, 4(6). pp.348-360.

Williams, E.E. and Dobelman, J.A., 2017. Financial statement analysis. World Scientific Book

Chapters. pp.109-169.

10

Books and Journals

Aktas, N., Croci, E. and Petmezas, D., 2015. Is working capital management value-enhancing?

Evidence from firm performance and investments. Journal of Corporate

Finance.30.pp.98-113.

Girish, S. and Desai, K., 2017. Impact of cash flow from operating and financial activities

information on share price: Empirical evidence from nifty Pharma index companies,

India. International Journal of Management Research and Reviews.7(11). pp.1029-1033.

Gordon, E.A. and et.al., 2017. Flexibility in cash-flow classification under IFRS: determinants

and consequences. Review of Accounting Studies.22(2). pp.839-872.

Ibrahim, M. M., 2019. Designing zero-based budgeting for public organizations. Problems and

Perspectives in Management. 17(2).

Ketz, J.E., 2016. Free Cash Flow and Business Combinations. The CPA Journal.86(11).pp.48-

53.

Kopita, A.S., Charitou, A. and Karamanou, I., 2017. The determinants and valuation effects of

classification choice on the statement of cash flows. Accounting and Business Research.

Mathuva, D., 2015. The Influence of working capital management components on corporate

profitability.

Miao, B., Teoh, S.H. and Zhu, Z., 2016. Limited attention, statement of cash flow disclosure, and

the valuation of accruals. Review of Accounting Studies.21(2). pp.473-515.

Opgenoord, M.M. and Willcox, K.E., 2016. Sensitivity analysis methods for uncertainty

budgeting in system design. AIAA Journal, pp.3134-3148.

O'Shea, J. P., 2018. Viability of Zero-Based Budgeting Methods in the City of Albuquerque.

Popesko, B. and Šocová, V., 2016. Current trends in budgeting and planning: Czech survey

initial results. International Advances in Economic Research, 22(1). pp.99-100.

Sri, B.P., 2017. An assignment on A study on cash flow statement analysis with special reference

to jet airways. Journal Homepage: http://www. ijmra. us, 7(11).

Szűcsné Markovics, K., 2016. Capital budgeting methods used in some European countries and

in the United States. Universal Journal of Management, 4(6). pp.348-360.

Williams, E.E. and Dobelman, J.A., 2017. Financial statement analysis. World Scientific Book

Chapters. pp.109-169.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.