Critical Analysis of Financial Health of Harvey Norman Holdings Limited

VerifiedAdded on 2023/03/31

|12

|3168

|436

AI Summary

This report provides a critical analysis of the financial health of Harvey Norman Holdings Limited and offers financial advice to a big institutional investor. It includes an evaluation of the company's profitability and operating efficiency, as well as a comparison of share price movements.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: BUSINESS FINANCE

Business Finance

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Business Finance

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1BUSINESS FINANCE

Abstract:

The report would include critical analysis of the financial health of ASX listed firm in

order to provide financial advice to a big institutional investor. For this reason, Harvey

Norman Holdings Limited has been considered and the financial position of the firm

would be evaluated for providing recommendation to the client. It has been found that

the organisation is struggling in terms of profitability; however, it has managed to

maintain its operating efficiency over the years. However, from the share price

movement, it has been identified that Harvey Norman Holdings Limited would not

provide increased returns to the shareholders, as the returns would be much lower

compared to All Ordinaries Index. Hence, the investor is recommended not to invest in

the shares of Harvey Norman Holdings Limited, as the same would minimise the overall

return on investment.

Abstract:

The report would include critical analysis of the financial health of ASX listed firm in

order to provide financial advice to a big institutional investor. For this reason, Harvey

Norman Holdings Limited has been considered and the financial position of the firm

would be evaluated for providing recommendation to the client. It has been found that

the organisation is struggling in terms of profitability; however, it has managed to

maintain its operating efficiency over the years. However, from the share price

movement, it has been identified that Harvey Norman Holdings Limited would not

provide increased returns to the shareholders, as the returns would be much lower

compared to All Ordinaries Index. Hence, the investor is recommended not to invest in

the shares of Harvey Norman Holdings Limited, as the same would minimise the overall

return on investment.

2BUSINESS FINANCE

Table of Contents

I. Introduction:....................................................................................................................3

II. Financial analysis of Harvey Norman Limited:..............................................................3

2.1 Description of Harvey Norman Limited:...................................................................3

2.2 Calculation and analysis of financial ratios:.............................................................3

2.3 Graphs and comparison of share price movements:...............................................7

2.4 Calculation of cost of equity:....................................................................................8

2.5 Identification of the capital structure:.......................................................................8

III. Conclusion:...................................................................................................................9

IV. Recommendation:........................................................................................................9

References:......................................................................................................................11

Table of Contents

I. Introduction:....................................................................................................................3

II. Financial analysis of Harvey Norman Limited:..............................................................3

2.1 Description of Harvey Norman Limited:...................................................................3

2.2 Calculation and analysis of financial ratios:.............................................................3

2.3 Graphs and comparison of share price movements:...............................................7

2.4 Calculation of cost of equity:....................................................................................8

2.5 Identification of the capital structure:.......................................................................8

III. Conclusion:...................................................................................................................9

IV. Recommendation:........................................................................................................9

References:......................................................................................................................11

3BUSINESS FINANCE

I. Introduction:

The report would include critical analysis of the financial health of ASX listed firm

in order to provide financial advice to a big institutional investor. For this reason, Harvey

Norman Holdings Limited has been considered and the financial position of the firm

would be evaluated for providing recommendation to the client. The annual report of the

concerned firm would be analysed suitably for obtaining an insight of its existing

financial health by the application of different types of ratios. In this report, two types of

ratios are taken into consideration, which include profitability ratios along with operating

efficiency ratios. The stock prices of the organisation would be analysed in terms of

share price movements and they would be compared with those of the All Ordinaries

Index for determining the market volatility. Moreover, the capital structure of the

organisation would be considered in finding out the weighted average cost of capital

(WACC). Finally, the report would shed light on providing recommendations based on

the analysis of all possible aspects.

II. Financial analysis of Harvey Norman Limited:

2.1 Description of Harvey Norman Limited:

Harvey Norman Holdings Limited is a public firm, which is listed in ASX and its

core activities include integrated retail, property and digital enterprise and franchise. In

Australia, it operates within a franchise system and it provides consistent unparalleled

retail offerings to the Australian customers having effective product range, cutting edge

technology and leadership in the market in significant product categories. It is engaged

in granting franchises to the independent proprietors within three leading brands. They

include Harvey Norman, Joyce Mayne and Domayne. The products are sold under the

following categories:

Electrical products

Computerised communications

Furniture

Manchester and bedding

Small appliances

Kitchen appliances

Tiles and bathrooms

Flooring and carpets

Harvey Norman has launched Windows 95, which is considered to be one of the

biggest successes of the organisation in its entire history. Moreover, it has acquired

numerous small businesses by expanding its business operations and as a result, it has

assisted the organisation in gaining competitive supremacy in the market (Harvey

Norman Holdings 2019).

2.2 Calculation and analysis of financial ratios:

Operating efficiency and profitability are deemed to be the two crucial aspects in

order to determine the existing financial performance and standing of Harvey Norman

Holdings Limited (Brooks 2015). The below discussion reveals the evaluation of a

number of ratios within the profitability as well as operating efficiency of the concerned

organisation:

I. Introduction:

The report would include critical analysis of the financial health of ASX listed firm

in order to provide financial advice to a big institutional investor. For this reason, Harvey

Norman Holdings Limited has been considered and the financial position of the firm

would be evaluated for providing recommendation to the client. The annual report of the

concerned firm would be analysed suitably for obtaining an insight of its existing

financial health by the application of different types of ratios. In this report, two types of

ratios are taken into consideration, which include profitability ratios along with operating

efficiency ratios. The stock prices of the organisation would be analysed in terms of

share price movements and they would be compared with those of the All Ordinaries

Index for determining the market volatility. Moreover, the capital structure of the

organisation would be considered in finding out the weighted average cost of capital

(WACC). Finally, the report would shed light on providing recommendations based on

the analysis of all possible aspects.

II. Financial analysis of Harvey Norman Limited:

2.1 Description of Harvey Norman Limited:

Harvey Norman Holdings Limited is a public firm, which is listed in ASX and its

core activities include integrated retail, property and digital enterprise and franchise. In

Australia, it operates within a franchise system and it provides consistent unparalleled

retail offerings to the Australian customers having effective product range, cutting edge

technology and leadership in the market in significant product categories. It is engaged

in granting franchises to the independent proprietors within three leading brands. They

include Harvey Norman, Joyce Mayne and Domayne. The products are sold under the

following categories:

Electrical products

Computerised communications

Furniture

Manchester and bedding

Small appliances

Kitchen appliances

Tiles and bathrooms

Flooring and carpets

Harvey Norman has launched Windows 95, which is considered to be one of the

biggest successes of the organisation in its entire history. Moreover, it has acquired

numerous small businesses by expanding its business operations and as a result, it has

assisted the organisation in gaining competitive supremacy in the market (Harvey

Norman Holdings 2019).

2.2 Calculation and analysis of financial ratios:

Operating efficiency and profitability are deemed to be the two crucial aspects in

order to determine the existing financial performance and standing of Harvey Norman

Holdings Limited (Brooks 2015). The below discussion reveals the evaluation of a

number of ratios within the profitability as well as operating efficiency of the concerned

organisation:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4BUSINESS FINANCE

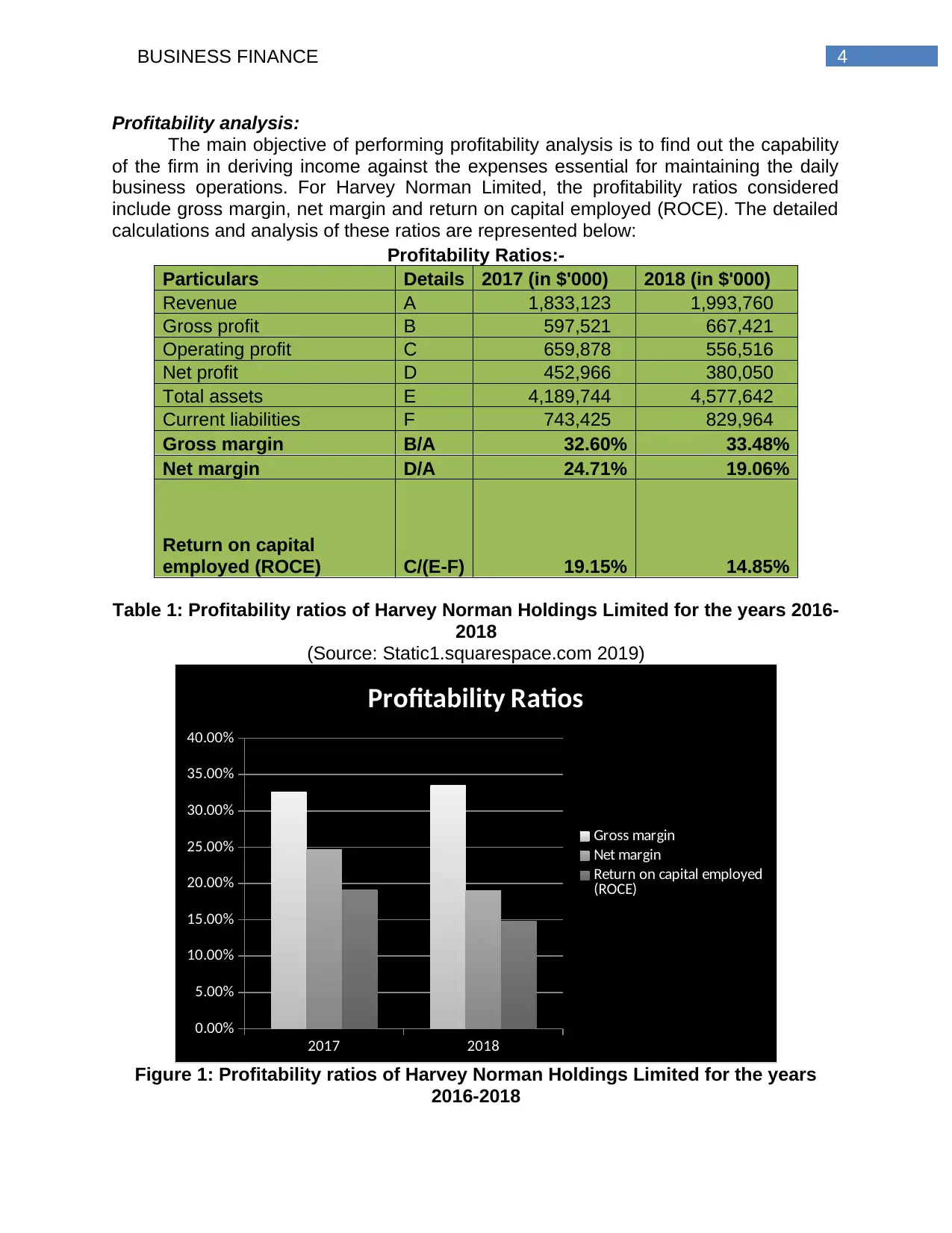

Profitability analysis:

The main objective of performing profitability analysis is to find out the capability

of the firm in deriving income against the expenses essential for maintaining the daily

business operations. For Harvey Norman Limited, the profitability ratios considered

include gross margin, net margin and return on capital employed (ROCE). The detailed

calculations and analysis of these ratios are represented below:

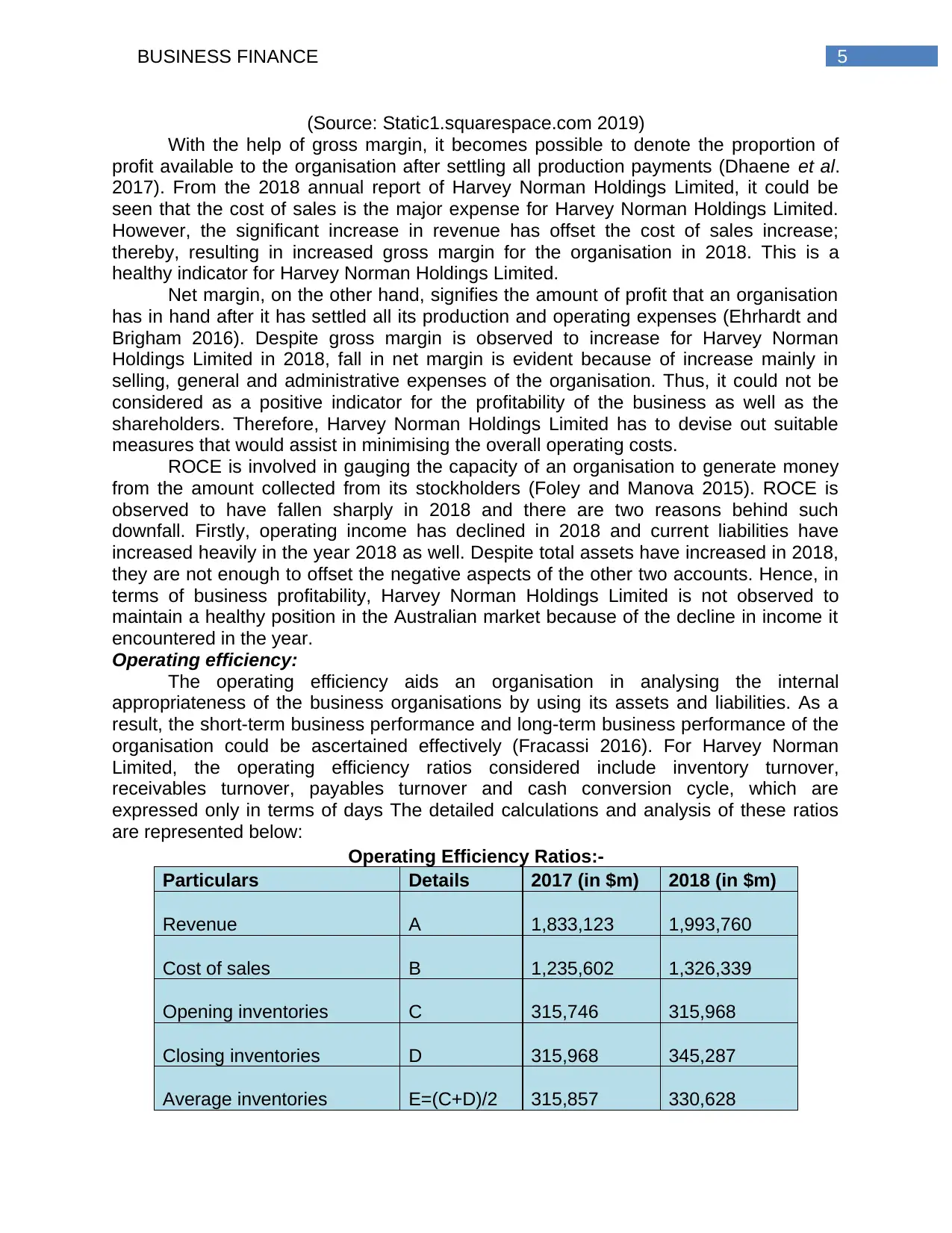

Profitability Ratios:-

Particulars Details 2017 (in $'000) 2018 (in $'000)

Revenue A 1,833,123 1,993,760

Gross profit B 597,521 667,421

Operating profit C 659,878 556,516

Net profit D 452,966 380,050

Total assets E 4,189,744 4,577,642

Current liabilities F 743,425 829,964

Gross margin B/A 32.60% 33.48%

Net margin D/A 24.71% 19.06%

Return on capital

employed (ROCE) C/(E-F) 19.15% 14.85%

Table 1: Profitability ratios of Harvey Norman Holdings Limited for the years 2016-

2018

(Source: Static1.squarespace.com 2019)

2017 2018

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

Profitability Ratios

Gross margin

Net margin

Return on capital employed

(ROCE)

Figure 1: Profitability ratios of Harvey Norman Holdings Limited for the years

2016-2018

Profitability analysis:

The main objective of performing profitability analysis is to find out the capability

of the firm in deriving income against the expenses essential for maintaining the daily

business operations. For Harvey Norman Limited, the profitability ratios considered

include gross margin, net margin and return on capital employed (ROCE). The detailed

calculations and analysis of these ratios are represented below:

Profitability Ratios:-

Particulars Details 2017 (in $'000) 2018 (in $'000)

Revenue A 1,833,123 1,993,760

Gross profit B 597,521 667,421

Operating profit C 659,878 556,516

Net profit D 452,966 380,050

Total assets E 4,189,744 4,577,642

Current liabilities F 743,425 829,964

Gross margin B/A 32.60% 33.48%

Net margin D/A 24.71% 19.06%

Return on capital

employed (ROCE) C/(E-F) 19.15% 14.85%

Table 1: Profitability ratios of Harvey Norman Holdings Limited for the years 2016-

2018

(Source: Static1.squarespace.com 2019)

2017 2018

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

Profitability Ratios

Gross margin

Net margin

Return on capital employed

(ROCE)

Figure 1: Profitability ratios of Harvey Norman Holdings Limited for the years

2016-2018

5BUSINESS FINANCE

(Source: Static1.squarespace.com 2019)

With the help of gross margin, it becomes possible to denote the proportion of

profit available to the organisation after settling all production payments (Dhaene et al.

2017). From the 2018 annual report of Harvey Norman Holdings Limited, it could be

seen that the cost of sales is the major expense for Harvey Norman Holdings Limited.

However, the significant increase in revenue has offset the cost of sales increase;

thereby, resulting in increased gross margin for the organisation in 2018. This is a

healthy indicator for Harvey Norman Holdings Limited.

Net margin, on the other hand, signifies the amount of profit that an organisation

has in hand after it has settled all its production and operating expenses (Ehrhardt and

Brigham 2016). Despite gross margin is observed to increase for Harvey Norman

Holdings Limited in 2018, fall in net margin is evident because of increase mainly in

selling, general and administrative expenses of the organisation. Thus, it could not be

considered as a positive indicator for the profitability of the business as well as the

shareholders. Therefore, Harvey Norman Holdings Limited has to devise out suitable

measures that would assist in minimising the overall operating costs.

ROCE is involved in gauging the capacity of an organisation to generate money

from the amount collected from its stockholders (Foley and Manova 2015). ROCE is

observed to have fallen sharply in 2018 and there are two reasons behind such

downfall. Firstly, operating income has declined in 2018 and current liabilities have

increased heavily in the year 2018 as well. Despite total assets have increased in 2018,

they are not enough to offset the negative aspects of the other two accounts. Hence, in

terms of business profitability, Harvey Norman Holdings Limited is not observed to

maintain a healthy position in the Australian market because of the decline in income it

encountered in the year.

Operating efficiency:

The operating efficiency aids an organisation in analysing the internal

appropriateness of the business organisations by using its assets and liabilities. As a

result, the short-term business performance and long-term business performance of the

organisation could be ascertained effectively (Fracassi 2016). For Harvey Norman

Limited, the operating efficiency ratios considered include inventory turnover,

receivables turnover, payables turnover and cash conversion cycle, which are

expressed only in terms of days The detailed calculations and analysis of these ratios

are represented below:

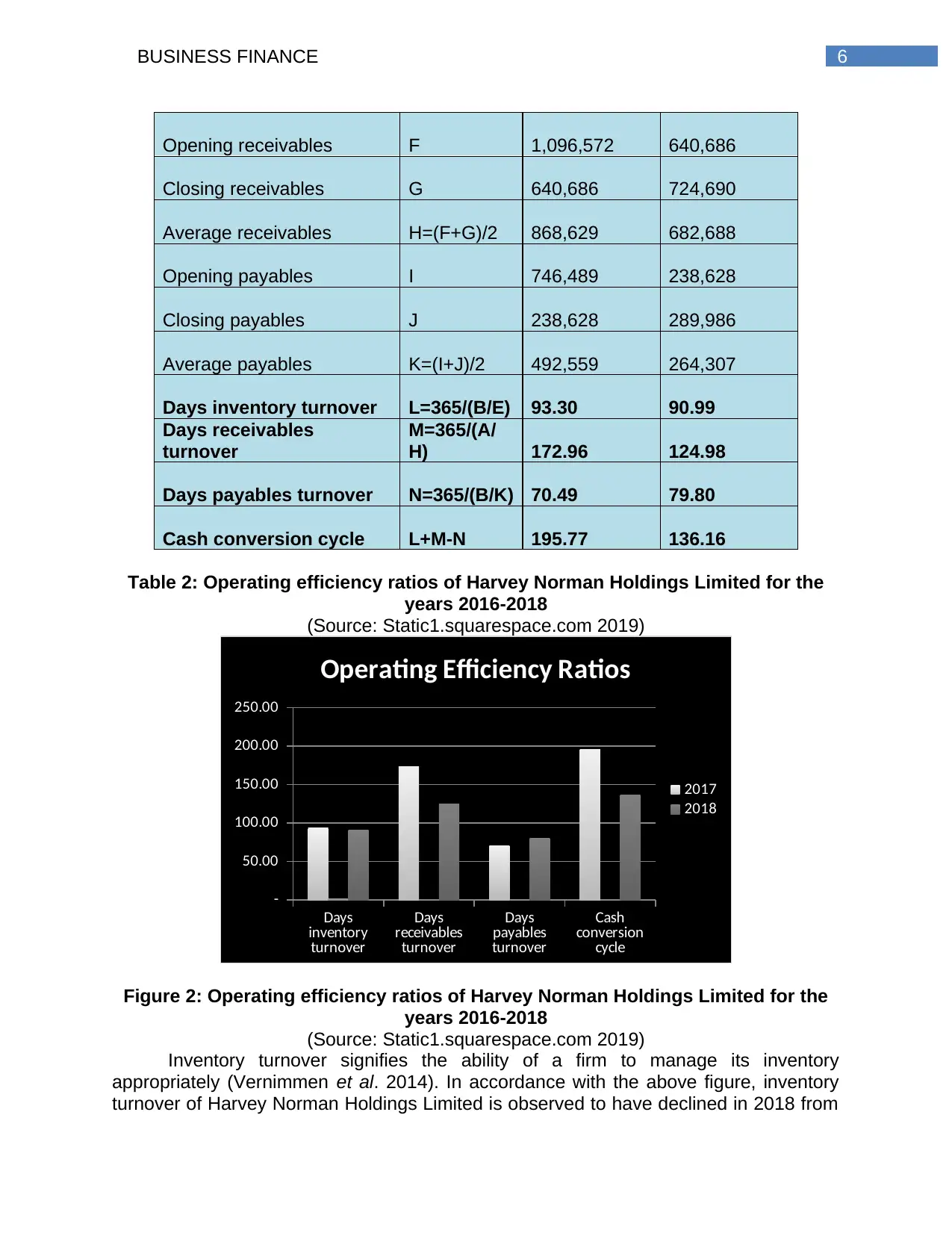

Operating Efficiency Ratios:-

Particulars Details 2017 (in $m) 2018 (in $m)

Revenue A 1,833,123 1,993,760

Cost of sales B 1,235,602 1,326,339

Opening inventories C 315,746 315,968

Closing inventories D 315,968 345,287

Average inventories E=(C+D)/2 315,857 330,628

(Source: Static1.squarespace.com 2019)

With the help of gross margin, it becomes possible to denote the proportion of

profit available to the organisation after settling all production payments (Dhaene et al.

2017). From the 2018 annual report of Harvey Norman Holdings Limited, it could be

seen that the cost of sales is the major expense for Harvey Norman Holdings Limited.

However, the significant increase in revenue has offset the cost of sales increase;

thereby, resulting in increased gross margin for the organisation in 2018. This is a

healthy indicator for Harvey Norman Holdings Limited.

Net margin, on the other hand, signifies the amount of profit that an organisation

has in hand after it has settled all its production and operating expenses (Ehrhardt and

Brigham 2016). Despite gross margin is observed to increase for Harvey Norman

Holdings Limited in 2018, fall in net margin is evident because of increase mainly in

selling, general and administrative expenses of the organisation. Thus, it could not be

considered as a positive indicator for the profitability of the business as well as the

shareholders. Therefore, Harvey Norman Holdings Limited has to devise out suitable

measures that would assist in minimising the overall operating costs.

ROCE is involved in gauging the capacity of an organisation to generate money

from the amount collected from its stockholders (Foley and Manova 2015). ROCE is

observed to have fallen sharply in 2018 and there are two reasons behind such

downfall. Firstly, operating income has declined in 2018 and current liabilities have

increased heavily in the year 2018 as well. Despite total assets have increased in 2018,

they are not enough to offset the negative aspects of the other two accounts. Hence, in

terms of business profitability, Harvey Norman Holdings Limited is not observed to

maintain a healthy position in the Australian market because of the decline in income it

encountered in the year.

Operating efficiency:

The operating efficiency aids an organisation in analysing the internal

appropriateness of the business organisations by using its assets and liabilities. As a

result, the short-term business performance and long-term business performance of the

organisation could be ascertained effectively (Fracassi 2016). For Harvey Norman

Limited, the operating efficiency ratios considered include inventory turnover,

receivables turnover, payables turnover and cash conversion cycle, which are

expressed only in terms of days The detailed calculations and analysis of these ratios

are represented below:

Operating Efficiency Ratios:-

Particulars Details 2017 (in $m) 2018 (in $m)

Revenue A 1,833,123 1,993,760

Cost of sales B 1,235,602 1,326,339

Opening inventories C 315,746 315,968

Closing inventories D 315,968 345,287

Average inventories E=(C+D)/2 315,857 330,628

6BUSINESS FINANCE

Opening receivables F 1,096,572 640,686

Closing receivables G 640,686 724,690

Average receivables H=(F+G)/2 868,629 682,688

Opening payables I 746,489 238,628

Closing payables J 238,628 289,986

Average payables K=(I+J)/2 492,559 264,307

Days inventory turnover L=365/(B/E) 93.30 90.99

Days receivables

turnover

M=365/(A/

H) 172.96 124.98

Days payables turnover N=365/(B/K) 70.49 79.80

Cash conversion cycle L+M-N 195.77 136.16

Table 2: Operating efficiency ratios of Harvey Norman Holdings Limited for the

years 2016-2018

(Source: Static1.squarespace.com 2019)

Days

inventory

turnover

Days

receivables

turnover

Days

payables

turnover

Cash

conversion

cycle

-

50.00

100.00

150.00

200.00

250.00

Operating Efficiency Ratios

2017

2018

Figure 2: Operating efficiency ratios of Harvey Norman Holdings Limited for the

years 2016-2018

(Source: Static1.squarespace.com 2019)

Inventory turnover signifies the ability of a firm to manage its inventory

appropriately (Vernimmen et al. 2014). In accordance with the above figure, inventory

turnover of Harvey Norman Holdings Limited is observed to have declined in 2018 from

Opening receivables F 1,096,572 640,686

Closing receivables G 640,686 724,690

Average receivables H=(F+G)/2 868,629 682,688

Opening payables I 746,489 238,628

Closing payables J 238,628 289,986

Average payables K=(I+J)/2 492,559 264,307

Days inventory turnover L=365/(B/E) 93.30 90.99

Days receivables

turnover

M=365/(A/

H) 172.96 124.98

Days payables turnover N=365/(B/K) 70.49 79.80

Cash conversion cycle L+M-N 195.77 136.16

Table 2: Operating efficiency ratios of Harvey Norman Holdings Limited for the

years 2016-2018

(Source: Static1.squarespace.com 2019)

Days

inventory

turnover

Days

receivables

turnover

Days

payables

turnover

Cash

conversion

cycle

-

50.00

100.00

150.00

200.00

250.00

Operating Efficiency Ratios

2017

2018

Figure 2: Operating efficiency ratios of Harvey Norman Holdings Limited for the

years 2016-2018

(Source: Static1.squarespace.com 2019)

Inventory turnover signifies the ability of a firm to manage its inventory

appropriately (Vernimmen et al. 2014). In accordance with the above figure, inventory

turnover of Harvey Norman Holdings Limited is observed to have declined in 2018 from

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7BUSINESS FINANCE

2017 denoting the increase in the ability of the organisation to release its inventory at a

rapid pace. Thus, inventory turnover expressed in terms of days is observed to be

favourable for Harvey Norman Holdings Limited.

Receivables turnover denotes the efficacy of the firms through which they are

collecting money for the products sold on credit to their customers (Ferran and Ho

2014). The above figure reveals the declining trend in the ratio of Harvey Norman

Holdings Limited from 2017 to 2018. Thus, Harvey Norman Holdings Limited has

adopted stringent debtor policy so that it could collect the outstanding amounts at an

earlier date for raising its cash balance and working capital. Overall, receivables

turnover expressed in days is considered to be suitable from the business perspective

of Harvey Norman Holdings Limited.

Payables turnover expressed in number of days reveals the capability of a

company in making payments to the suppliers and creditors in a timely manner (Gitman,

Juchau and Flanagan 2015). It could be witnessed that this ratio has increased for

Harvey Norman Holdings Limited in 2018, which implies that the creditors are allowing

more time to the organisation in settling its payments owing to the positive brand image

in the market.

Finally, cash conversion cycle is involved in gauging how capable a firm is to

transfer its resources into cash (Gullifer and Payne 2015). From the above table, it

could be seen that Harvey Norman Holdings Limited has managed to reduce its cash

conversion cycle in the year 2018, which is a healthy sign. The main reason behind

such reduction is quick collection from the customers, which has assisted in increasing

its availability of cash as well as working capital.

Therefore, by analysing the operating efficiency of Harvey Norman Holdings

Limited it could be perceived as beneficial from the perspective of both the company as

well as the investors.

2.3 Graphs and comparison of share price movements:

1/01/2017

1/03/2017

1/05/2017

1/07/2017

1/09/2017

1/11/2017

1/01/2018

1/03/2018

1/05/2018

1/07/2018

1/09/2018

1/11/2018

$-

$1,000.00

$2,000.00

$3,000.00

$4,000.00

$5,000.00

$6,000.00

$7,000.00

Share Price Movements

All Ordinaries Index

Harvey Norman

Figure 3: Share price movements of Harvey Norman Holdings Limited and All

Ordinaries Index from 2017-2018

(Source: Au.finance.yahoo.com 2019: Au.finance.yahoo.com)

2017 denoting the increase in the ability of the organisation to release its inventory at a

rapid pace. Thus, inventory turnover expressed in terms of days is observed to be

favourable for Harvey Norman Holdings Limited.

Receivables turnover denotes the efficacy of the firms through which they are

collecting money for the products sold on credit to their customers (Ferran and Ho

2014). The above figure reveals the declining trend in the ratio of Harvey Norman

Holdings Limited from 2017 to 2018. Thus, Harvey Norman Holdings Limited has

adopted stringent debtor policy so that it could collect the outstanding amounts at an

earlier date for raising its cash balance and working capital. Overall, receivables

turnover expressed in days is considered to be suitable from the business perspective

of Harvey Norman Holdings Limited.

Payables turnover expressed in number of days reveals the capability of a

company in making payments to the suppliers and creditors in a timely manner (Gitman,

Juchau and Flanagan 2015). It could be witnessed that this ratio has increased for

Harvey Norman Holdings Limited in 2018, which implies that the creditors are allowing

more time to the organisation in settling its payments owing to the positive brand image

in the market.

Finally, cash conversion cycle is involved in gauging how capable a firm is to

transfer its resources into cash (Gullifer and Payne 2015). From the above table, it

could be seen that Harvey Norman Holdings Limited has managed to reduce its cash

conversion cycle in the year 2018, which is a healthy sign. The main reason behind

such reduction is quick collection from the customers, which has assisted in increasing

its availability of cash as well as working capital.

Therefore, by analysing the operating efficiency of Harvey Norman Holdings

Limited it could be perceived as beneficial from the perspective of both the company as

well as the investors.

2.3 Graphs and comparison of share price movements:

1/01/2017

1/03/2017

1/05/2017

1/07/2017

1/09/2017

1/11/2017

1/01/2018

1/03/2018

1/05/2018

1/07/2018

1/09/2018

1/11/2018

$-

$1,000.00

$2,000.00

$3,000.00

$4,000.00

$5,000.00

$6,000.00

$7,000.00

Share Price Movements

All Ordinaries Index

Harvey Norman

Figure 3: Share price movements of Harvey Norman Holdings Limited and All

Ordinaries Index from 2017-2018

(Source: Au.finance.yahoo.com 2019: Au.finance.yahoo.com)

8BUSINESS FINANCE

The below-stated figure mainly assists in representing the monthly movements in

share prices compared to the share price movements in All Ordinaries Index for the

years 2017 and 2018. Based on the above figure, it could be witnessed that the monthly

share price of Harvey Norman Holdings Limited has been significantly lower compared

to the trend identified in All Ordinaries Index for the entire period. In all cases, the share

prices of Harvey Norman Holdings Limited are below than those of All Ordinaries Index,

as the former has failed to generate adequate returns when contrasted with those of All

Ordinaries Index. The trend is observed to be quite constant for Harvey Norman

Holdings Limited, while the trend is slightly fluctuating for All Ordinaries Index over the

period. Therefore, based on the above facts, it could be inferred that Harvey Norman

Limited has failed to match with the share price of the index and hence, lower returns

could be expected by investing in the shares of the organisation in future (Titman and

Martin 2014).

The major factors that have affected the share price of the organisation over the

past two years are elaborated as follows:

Sector performance:

The stock price of the companies in the similar sector would move in tandem with

each other. The reason is that the market conditions normally affect the organisations

operating in the same sector similarly (Hillier et al. 2014). However, the stock price of an

organisation might be impacted by any announcements of the competitors and the

situation is observed to be similar for Harvey Norman Holdings Limited as well.

Sentiment of the investors:

The investor sentiment or confidence could cause the market to move up or

down, which could result in increase or decline in share prices. Harvey Norman

Holdings Limited is observed to be operating in a market, in which the stock prices are

observed to decline coupled with declining investor confidence (Jordan 2014). This has

resulted in decline in share prices of Harvey Norman Holdings Limited.

2.4 Calculation of cost of equity:

According to the constant dividend growth model, the cost of equity is calculated

by dividing dividend paid by current share price, after which it is added with the growth

rate in dividend.

Particulars Details

Value

s

Dividend paid A $ 0.18

Current share

price B $ 3.37

Dividend growth

rate C 4%

Cost of equity

D=(A/B)

+C 9.34%

Table 3: Cost of equity of Harvey Norman Holdings Limited

(Source: As created by author)

2.5 Identification of the capital structure:

Particulars Details Values

The below-stated figure mainly assists in representing the monthly movements in

share prices compared to the share price movements in All Ordinaries Index for the

years 2017 and 2018. Based on the above figure, it could be witnessed that the monthly

share price of Harvey Norman Holdings Limited has been significantly lower compared

to the trend identified in All Ordinaries Index for the entire period. In all cases, the share

prices of Harvey Norman Holdings Limited are below than those of All Ordinaries Index,

as the former has failed to generate adequate returns when contrasted with those of All

Ordinaries Index. The trend is observed to be quite constant for Harvey Norman

Holdings Limited, while the trend is slightly fluctuating for All Ordinaries Index over the

period. Therefore, based on the above facts, it could be inferred that Harvey Norman

Limited has failed to match with the share price of the index and hence, lower returns

could be expected by investing in the shares of the organisation in future (Titman and

Martin 2014).

The major factors that have affected the share price of the organisation over the

past two years are elaborated as follows:

Sector performance:

The stock price of the companies in the similar sector would move in tandem with

each other. The reason is that the market conditions normally affect the organisations

operating in the same sector similarly (Hillier et al. 2014). However, the stock price of an

organisation might be impacted by any announcements of the competitors and the

situation is observed to be similar for Harvey Norman Holdings Limited as well.

Sentiment of the investors:

The investor sentiment or confidence could cause the market to move up or

down, which could result in increase or decline in share prices. Harvey Norman

Holdings Limited is observed to be operating in a market, in which the stock prices are

observed to decline coupled with declining investor confidence (Jordan 2014). This has

resulted in decline in share prices of Harvey Norman Holdings Limited.

2.4 Calculation of cost of equity:

According to the constant dividend growth model, the cost of equity is calculated

by dividing dividend paid by current share price, after which it is added with the growth

rate in dividend.

Particulars Details

Value

s

Dividend paid A $ 0.18

Current share

price B $ 3.37

Dividend growth

rate C 4%

Cost of equity

D=(A/B)

+C 9.34%

Table 3: Cost of equity of Harvey Norman Holdings Limited

(Source: As created by author)

2.5 Identification of the capital structure:

Particulars Details Values

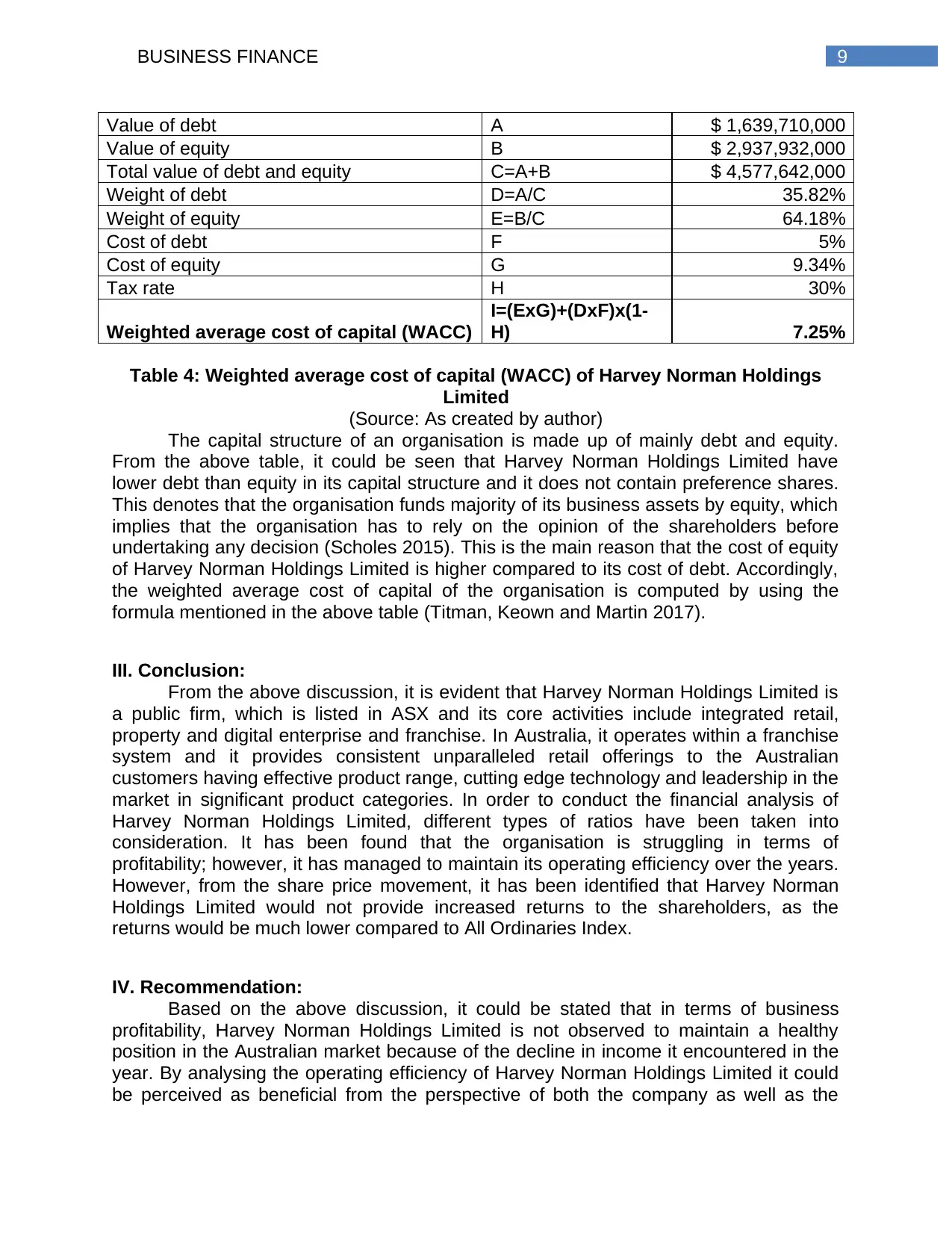

9BUSINESS FINANCE

Value of debt A $ 1,639,710,000

Value of equity B $ 2,937,932,000

Total value of debt and equity C=A+B $ 4,577,642,000

Weight of debt D=A/C 35.82%

Weight of equity E=B/C 64.18%

Cost of debt F 5%

Cost of equity G 9.34%

Tax rate H 30%

Weighted average cost of capital (WACC)

I=(ExG)+(DxF)x(1-

H) 7.25%

Table 4: Weighted average cost of capital (WACC) of Harvey Norman Holdings

Limited

(Source: As created by author)

The capital structure of an organisation is made up of mainly debt and equity.

From the above table, it could be seen that Harvey Norman Holdings Limited have

lower debt than equity in its capital structure and it does not contain preference shares.

This denotes that the organisation funds majority of its business assets by equity, which

implies that the organisation has to rely on the opinion of the shareholders before

undertaking any decision (Scholes 2015). This is the main reason that the cost of equity

of Harvey Norman Holdings Limited is higher compared to its cost of debt. Accordingly,

the weighted average cost of capital of the organisation is computed by using the

formula mentioned in the above table (Titman, Keown and Martin 2017).

III. Conclusion:

From the above discussion, it is evident that Harvey Norman Holdings Limited is

a public firm, which is listed in ASX and its core activities include integrated retail,

property and digital enterprise and franchise. In Australia, it operates within a franchise

system and it provides consistent unparalleled retail offerings to the Australian

customers having effective product range, cutting edge technology and leadership in the

market in significant product categories. In order to conduct the financial analysis of

Harvey Norman Holdings Limited, different types of ratios have been taken into

consideration. It has been found that the organisation is struggling in terms of

profitability; however, it has managed to maintain its operating efficiency over the years.

However, from the share price movement, it has been identified that Harvey Norman

Holdings Limited would not provide increased returns to the shareholders, as the

returns would be much lower compared to All Ordinaries Index.

IV. Recommendation:

Based on the above discussion, it could be stated that in terms of business

profitability, Harvey Norman Holdings Limited is not observed to maintain a healthy

position in the Australian market because of the decline in income it encountered in the

year. By analysing the operating efficiency of Harvey Norman Holdings Limited it could

be perceived as beneficial from the perspective of both the company as well as the

Value of debt A $ 1,639,710,000

Value of equity B $ 2,937,932,000

Total value of debt and equity C=A+B $ 4,577,642,000

Weight of debt D=A/C 35.82%

Weight of equity E=B/C 64.18%

Cost of debt F 5%

Cost of equity G 9.34%

Tax rate H 30%

Weighted average cost of capital (WACC)

I=(ExG)+(DxF)x(1-

H) 7.25%

Table 4: Weighted average cost of capital (WACC) of Harvey Norman Holdings

Limited

(Source: As created by author)

The capital structure of an organisation is made up of mainly debt and equity.

From the above table, it could be seen that Harvey Norman Holdings Limited have

lower debt than equity in its capital structure and it does not contain preference shares.

This denotes that the organisation funds majority of its business assets by equity, which

implies that the organisation has to rely on the opinion of the shareholders before

undertaking any decision (Scholes 2015). This is the main reason that the cost of equity

of Harvey Norman Holdings Limited is higher compared to its cost of debt. Accordingly,

the weighted average cost of capital of the organisation is computed by using the

formula mentioned in the above table (Titman, Keown and Martin 2017).

III. Conclusion:

From the above discussion, it is evident that Harvey Norman Holdings Limited is

a public firm, which is listed in ASX and its core activities include integrated retail,

property and digital enterprise and franchise. In Australia, it operates within a franchise

system and it provides consistent unparalleled retail offerings to the Australian

customers having effective product range, cutting edge technology and leadership in the

market in significant product categories. In order to conduct the financial analysis of

Harvey Norman Holdings Limited, different types of ratios have been taken into

consideration. It has been found that the organisation is struggling in terms of

profitability; however, it has managed to maintain its operating efficiency over the years.

However, from the share price movement, it has been identified that Harvey Norman

Holdings Limited would not provide increased returns to the shareholders, as the

returns would be much lower compared to All Ordinaries Index.

IV. Recommendation:

Based on the above discussion, it could be stated that in terms of business

profitability, Harvey Norman Holdings Limited is not observed to maintain a healthy

position in the Australian market because of the decline in income it encountered in the

year. By analysing the operating efficiency of Harvey Norman Holdings Limited it could

be perceived as beneficial from the perspective of both the company as well as the

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10BUSINESS FINANCE

investors. The stock price of the companies in the similar sector would move in tandem

with each other. The reason is that the market conditions normally affect the

organisations operating in the same sector similarly. However, the stock price of an

organisation might be impacted by any announcements of the competitors and the

situation is observed to be similar for Harvey Norman Holdings Limited as well. The

investor sentiment or confidence could cause the market to move up or down, which

could result in increase or decline in share prices. Harvey Norman Holdings Limited is

observed to be operating in a market, in which the stock prices are observed to decline

coupled with declining investor confidence. This has resulted in decline in share prices

of Harvey Norman Holdings Limited.

It could be seen that Harvey Norman Holdings Limited have lower debt than

equity in its capital structure and it does not contain preference shares. This denotes

that the organisation funds majority of its business assets by equity, which implies that

the organisation has to rely on the opinion of the shareholders before undertaking any

decision. This is the main reason that the cost of equity of Harvey Norman Holdings

Limited is higher compared to its cost of debt. Accordingly, the weighted average cost of

capital of the organisation is computed by using appropriate formula. Hence, the

investor is recommended not to invest in the shares of Harvey Norman Holdings

Limited, as the same would minimise the overall return on investment.

investors. The stock price of the companies in the similar sector would move in tandem

with each other. The reason is that the market conditions normally affect the

organisations operating in the same sector similarly. However, the stock price of an

organisation might be impacted by any announcements of the competitors and the

situation is observed to be similar for Harvey Norman Holdings Limited as well. The

investor sentiment or confidence could cause the market to move up or down, which

could result in increase or decline in share prices. Harvey Norman Holdings Limited is

observed to be operating in a market, in which the stock prices are observed to decline

coupled with declining investor confidence. This has resulted in decline in share prices

of Harvey Norman Holdings Limited.

It could be seen that Harvey Norman Holdings Limited have lower debt than

equity in its capital structure and it does not contain preference shares. This denotes

that the organisation funds majority of its business assets by equity, which implies that

the organisation has to rely on the opinion of the shareholders before undertaking any

decision. This is the main reason that the cost of equity of Harvey Norman Holdings

Limited is higher compared to its cost of debt. Accordingly, the weighted average cost of

capital of the organisation is computed by using appropriate formula. Hence, the

investor is recommended not to invest in the shares of Harvey Norman Holdings

Limited, as the same would minimise the overall return on investment.

11BUSINESS FINANCE

References:

Au.finance.yahoo.com., 2019. [online] Available at:

https://au.finance.yahoo.com/quote/%5EAORD/history?

period1=1483122600&period2=1548873000&interval=1mo&filter=history&frequency=1

mo [Accessed 31 May 2019].

Au.finance.yahoo.com., 2019. [online] Available at:

https://au.finance.yahoo.com/quote/HVN.AX/history?

period1=1481567400&period2=1548873000&interval=1mo&filter=history&frequency=1

mo [Accessed 31 May 2019].

Brooks, R., 2015. Financial management: core concepts. Pearson.

Dhaene, J., Hulle, C., Wuyts, G., Schoubben, F. and Schoutens, W., 2017. Is the capital

structure logic of corporate finance applicable to insurers? Review and analysis. Journal

of Economic Surveys, 31(1), pp.169-189.

Ehrhardt, M.C. and Brigham, E.F., 2016. Corporate finance: A focused approach.

Cengage learning.

Ferran, E. and Ho, L.C., 2014. Principles of corporate finance law. Oxford University

Press.

Foley, C.F. and Manova, K., 2015. International trade, multinational activity, and

corporate finance. economics, 7(1), pp.119-146.

Fracassi, C., 2016. Corporate finance policies and social networks. Management

Science, 63(8), pp.2420-2438.

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance.

Pearson Higher Education AU.

Gullifer, L. and Payne, J., 2015. Corporate finance law: principles and policy.

Bloomsbury Publishing.

Harvey Norman Holdings., 2019. Company Overview — Harvey Norman Holdings.

[online] Available at: http://www.harveynormanholdings.com.au/company [Accessed 31

May 2019].

Hillier, D., Clacher, I., Ross, S., Westerfield, R. and Jordan, B., 2014. Fundamentals of

corporate finance. McGraw Hill.

Jordan, B., 2014. Fundamentals of investments. McGraw-Hill Higher Education.

Scholes, M.S., 2015. Taxes and business strategy. Prentice Hall.

Static1.squarespace.com., 2019. [online] Available at:

https://static1.squarespace.com/static/54803162e4b08e1b8a472201/t/

5bad8412f4e1fcd2edb86026/1538098250289/2018-Annual-Report.pdf [Accessed 31

May 2019].

Titman, S. and Martin, J.D., 2014. Valuation. Pearson Higher Ed.

Titman, S., Keown, A.J. and Martin, J.D., 2017. Financial management: Principles and

applications. Pearson.

Vernimmen, P., Quiry, P., Dallocchio, M., Le Fur, Y. and Salvi, A., 2014. Corporate

finance: theory and practice. John Wiley & Sons.

References:

Au.finance.yahoo.com., 2019. [online] Available at:

https://au.finance.yahoo.com/quote/%5EAORD/history?

period1=1483122600&period2=1548873000&interval=1mo&filter=history&frequency=1

mo [Accessed 31 May 2019].

Au.finance.yahoo.com., 2019. [online] Available at:

https://au.finance.yahoo.com/quote/HVN.AX/history?

period1=1481567400&period2=1548873000&interval=1mo&filter=history&frequency=1

mo [Accessed 31 May 2019].

Brooks, R., 2015. Financial management: core concepts. Pearson.

Dhaene, J., Hulle, C., Wuyts, G., Schoubben, F. and Schoutens, W., 2017. Is the capital

structure logic of corporate finance applicable to insurers? Review and analysis. Journal

of Economic Surveys, 31(1), pp.169-189.

Ehrhardt, M.C. and Brigham, E.F., 2016. Corporate finance: A focused approach.

Cengage learning.

Ferran, E. and Ho, L.C., 2014. Principles of corporate finance law. Oxford University

Press.

Foley, C.F. and Manova, K., 2015. International trade, multinational activity, and

corporate finance. economics, 7(1), pp.119-146.

Fracassi, C., 2016. Corporate finance policies and social networks. Management

Science, 63(8), pp.2420-2438.

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance.

Pearson Higher Education AU.

Gullifer, L. and Payne, J., 2015. Corporate finance law: principles and policy.

Bloomsbury Publishing.

Harvey Norman Holdings., 2019. Company Overview — Harvey Norman Holdings.

[online] Available at: http://www.harveynormanholdings.com.au/company [Accessed 31

May 2019].

Hillier, D., Clacher, I., Ross, S., Westerfield, R. and Jordan, B., 2014. Fundamentals of

corporate finance. McGraw Hill.

Jordan, B., 2014. Fundamentals of investments. McGraw-Hill Higher Education.

Scholes, M.S., 2015. Taxes and business strategy. Prentice Hall.

Static1.squarespace.com., 2019. [online] Available at:

https://static1.squarespace.com/static/54803162e4b08e1b8a472201/t/

5bad8412f4e1fcd2edb86026/1538098250289/2018-Annual-Report.pdf [Accessed 31

May 2019].

Titman, S. and Martin, J.D., 2014. Valuation. Pearson Higher Ed.

Titman, S., Keown, A.J. and Martin, J.D., 2017. Financial management: Principles and

applications. Pearson.

Vernimmen, P., Quiry, P., Dallocchio, M., Le Fur, Y. and Salvi, A., 2014. Corporate

finance: theory and practice. John Wiley & Sons.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.