Analysis of Business Finance for International Investment Decisions

VerifiedAdded on 2023/01/11

Paraphrase This Document

INTRODUCTION.......................................................................................................................................3

MAIN BODY..............................................................................................................................................3

1. Capital investment appraisal:...........................................................................................................3

2. Source of finance:..........................................................................................................................14

3. Flexible budget:.............................................................................................................................17

4. Break Even Analysis......................................................................................................................20

CONCLUSION.........................................................................................................................................22

REFERENCES..........................................................................................................................................24

Corporate finance requires the assets and investments invested in the business. The

foundation of a company is finance. Acquisition of land, commodities, raw materials and the

other business activity flows are financial requirements (Ylhäinen, 2017). This is essential to

business entities to manage their financial resources in an effective manner so that total

utilization can become possible. The project report is based on an international company that

produces fashion cloths for different retailers of UK and USA. The project report consists

information about various tasks. Such as initial part of report is based on capital investment

appraisal under which different calculations are done as per methods. In the second task of report

different financial terms explained like bank overdraft, factoring, lease and many more. The third

part of report consists information about flexible budget and variance. While the end part of

report covers information about breakeven point and its calculations.

MAIN BODY

1. Capital investment appraisal:

Task 1 calculation:

Payback period

Country- Ethiopia

Investment= 500000

Year Cash flow

1 160000

2 160000

3 160000

4 160000

5 160000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

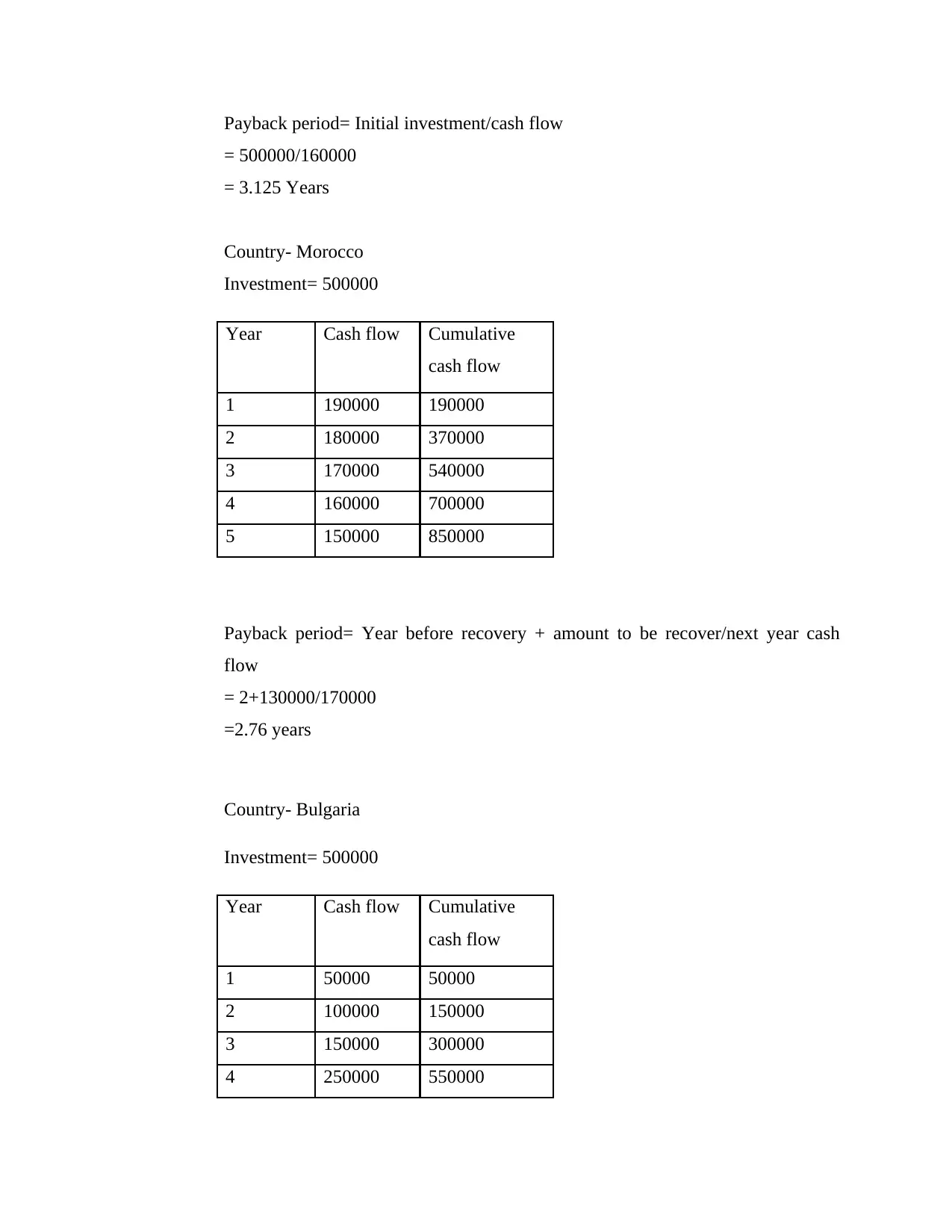

= 500000/160000

= 3.125 Years

Country- Morocco

Investment= 500000

Year Cash flow Cumulative

cash flow

1 190000 190000

2 180000 370000

3 170000 540000

4 160000 700000

5 150000 850000

Payback period= Year before recovery + amount to be recover/next year cash

flow

= 2+130000/170000

=2.76 years

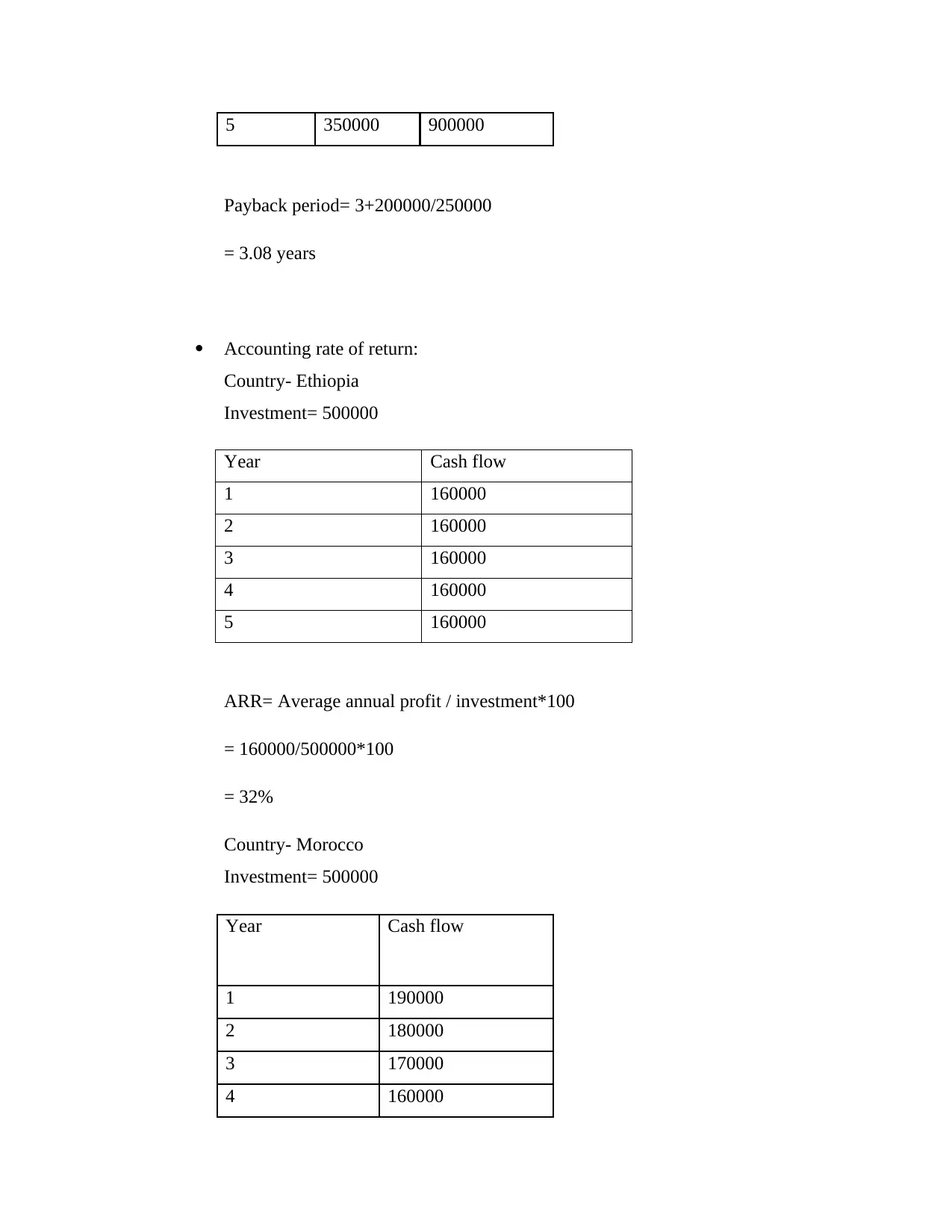

Country- Bulgaria

Investment= 500000

Year Cash flow Cumulative

cash flow

1 50000 50000

2 100000 150000

3 150000 300000

4 250000 550000

Paraphrase This Document

Payback period= 3+200000/250000

= 3.08 years

Accounting rate of return:

Country- Ethiopia

Investment= 500000

Year Cash flow

1 160000

2 160000

3 160000

4 160000

5 160000

ARR= Average annual profit / investment*100

= 160000/500000*100

= 32%

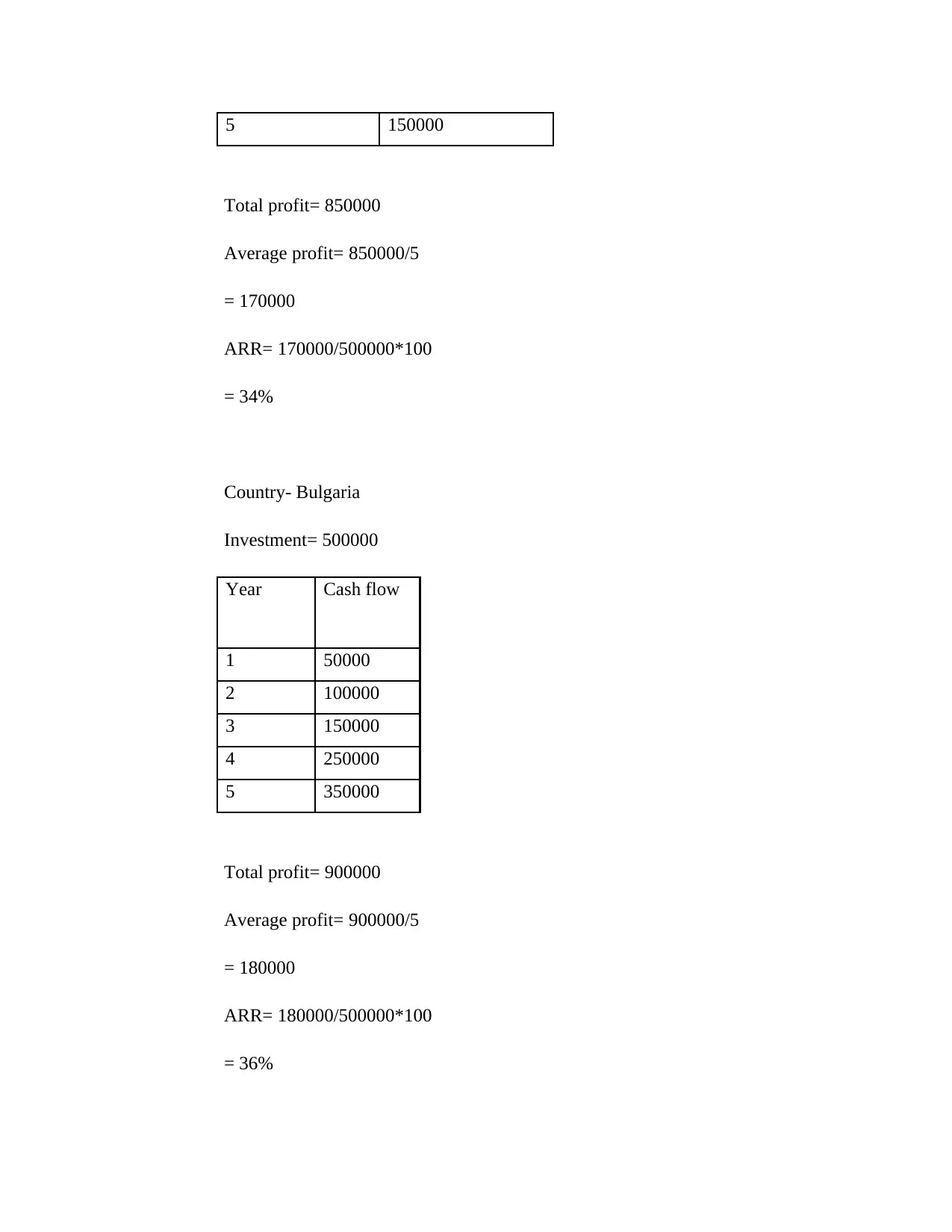

Country- Morocco

Investment= 500000

Year Cash flow

1 190000

2 180000

3 170000

4 160000

Total profit= 850000

Average profit= 850000/5

= 170000

ARR= 170000/500000*100

= 34%

Country- Bulgaria

Investment= 500000

Year Cash flow

1 50000

2 100000

3 150000

4 250000

5 350000

Total profit= 900000

Average profit= 900000/5

= 180000

ARR= 180000/500000*100

= 36%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

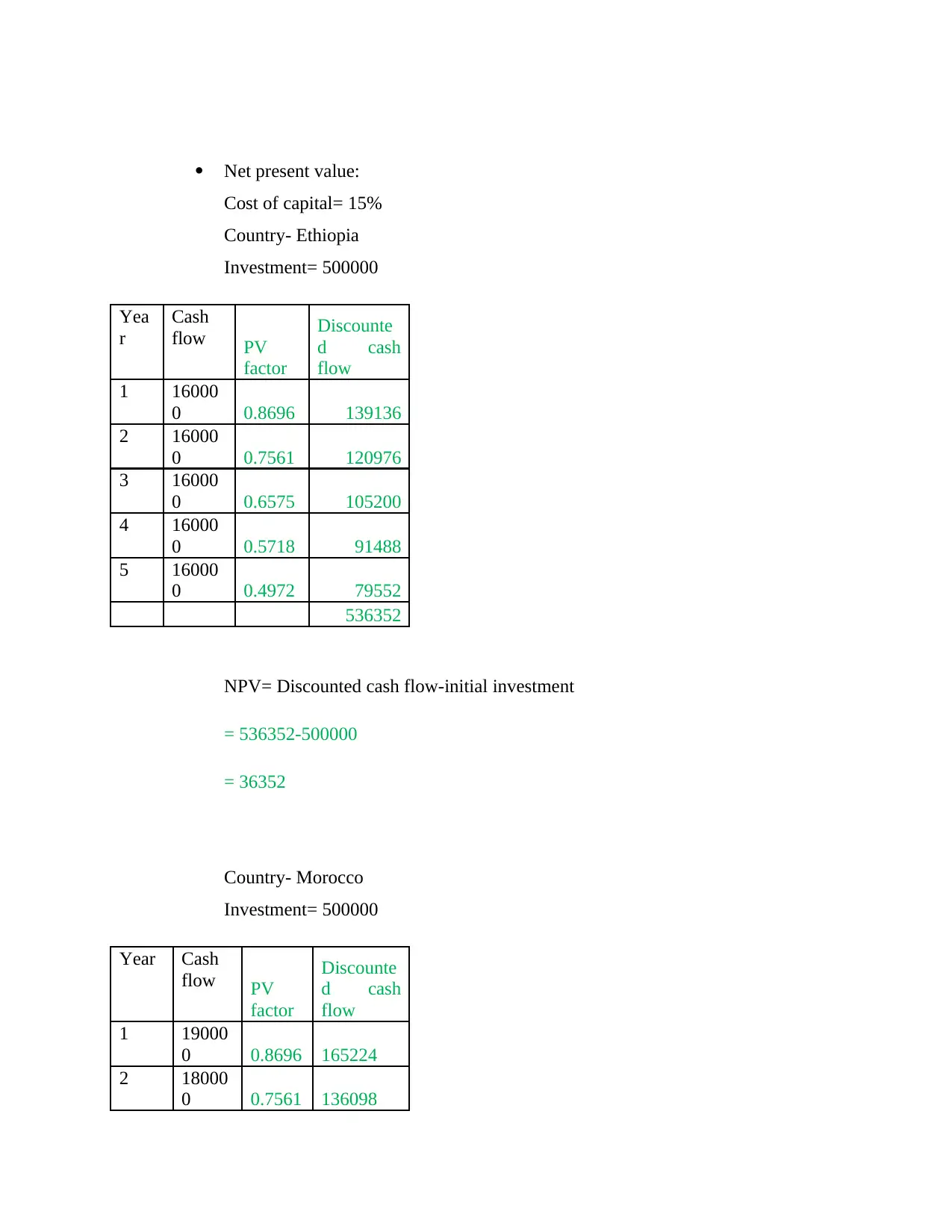

Cost of capital= 15%

Country- Ethiopia

Investment= 500000

Yea

r

Cash

flow PV

factor

Discounte

d cash

flow

1 16000

0 0.8696 139136

2 16000

0 0.7561 120976

3 16000

0 0.6575 105200

4 16000

0 0.5718 91488

5 16000

0 0.4972 79552

536352

NPV= Discounted cash flow-initial investment

= 536352-500000

= 36352

Country- Morocco

Investment= 500000

Year Cash

flow PV

factor

Discounte

d cash

flow

1 19000

0 0.8696 165224

2 18000

0 0.7561 136098

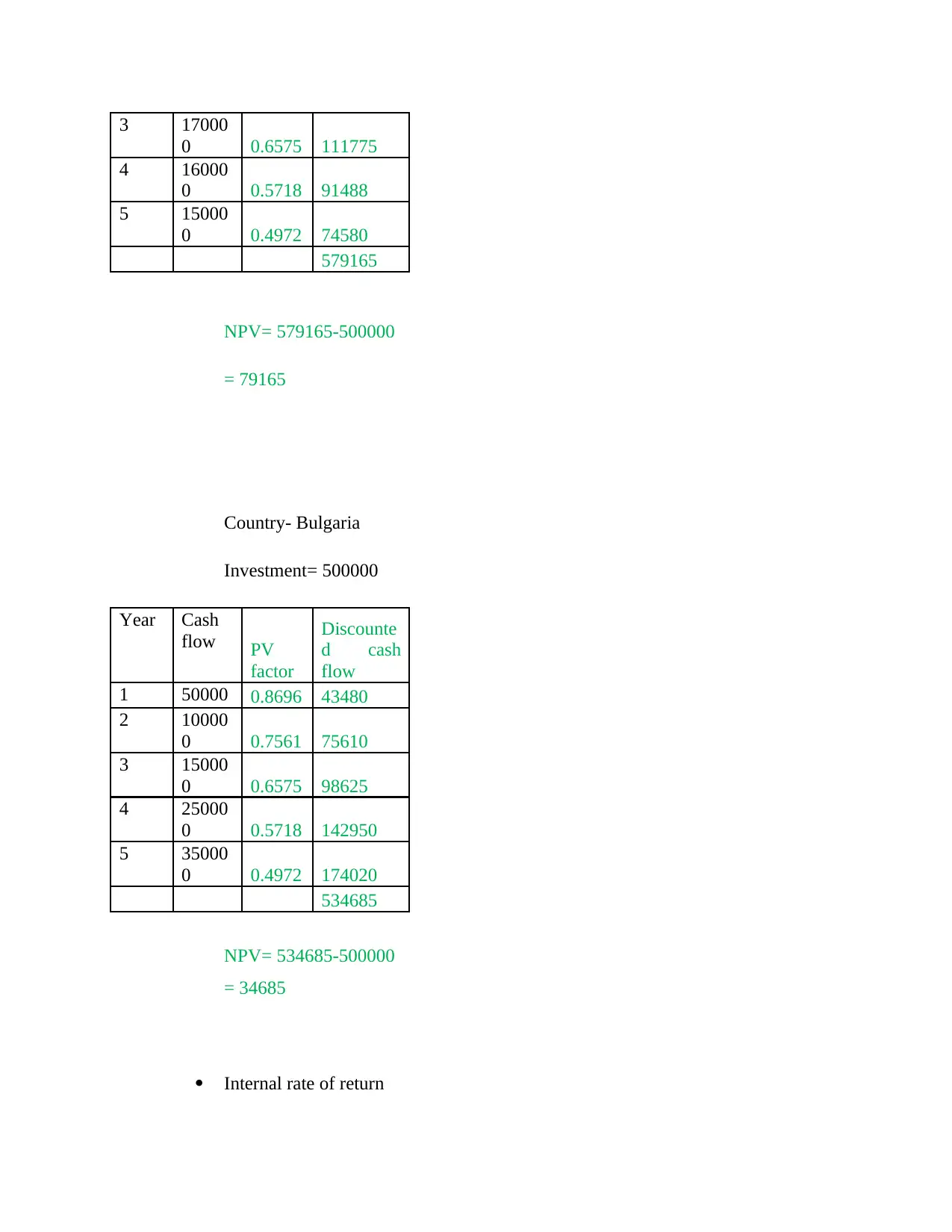

Paraphrase This Document

0 0.6575 111775

4 16000

0 0.5718 91488

5 15000

0 0.4972 74580

579165

NPV= 579165-500000

= 79165

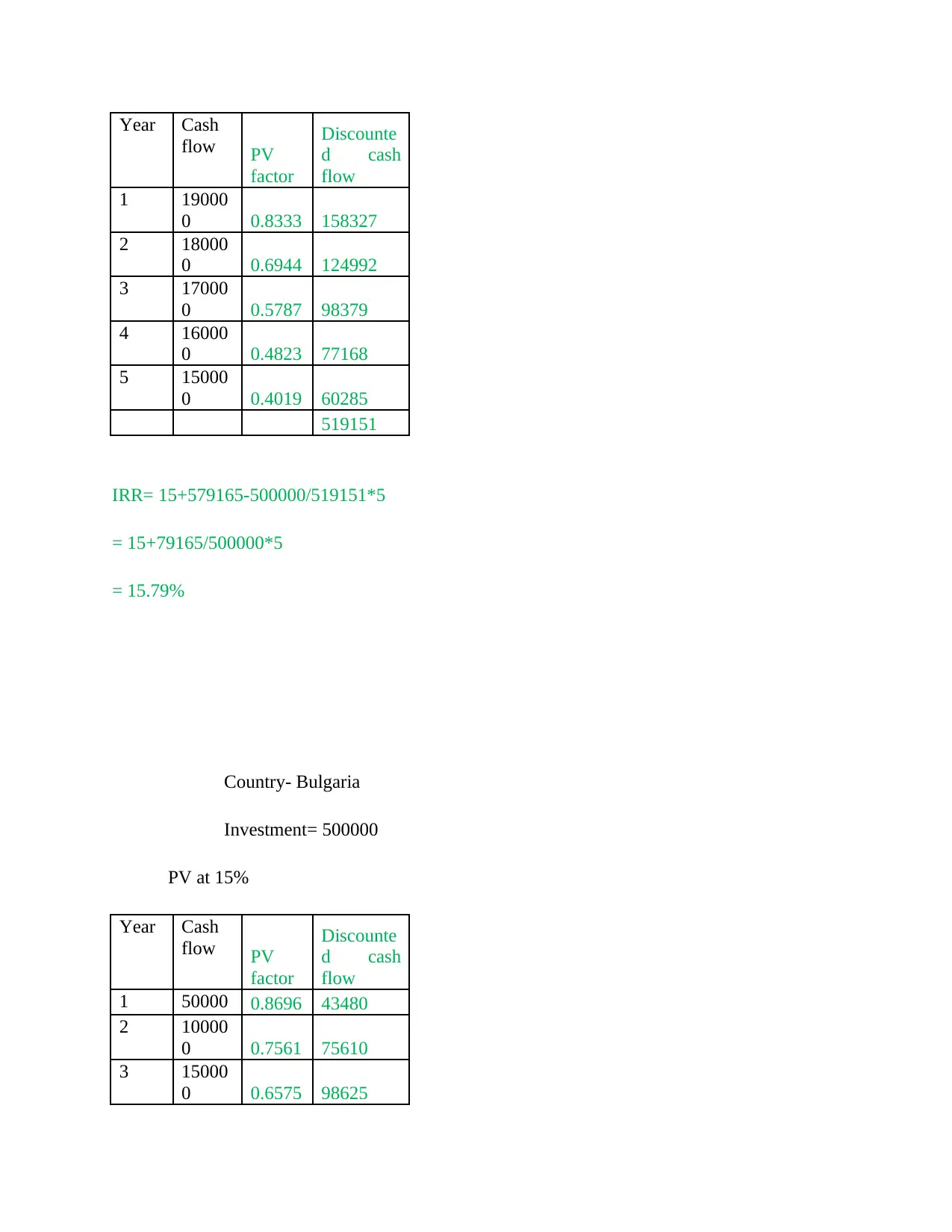

Country- Bulgaria

Investment= 500000

Year Cash

flow PV

factor

Discounte

d cash

flow

1 50000 0.8696 43480

2 10000

0 0.7561 75610

3 15000

0 0.6575 98625

4 25000

0 0.5718 142950

5 35000

0 0.4972 174020

534685

NPV= 534685-500000

= 34685

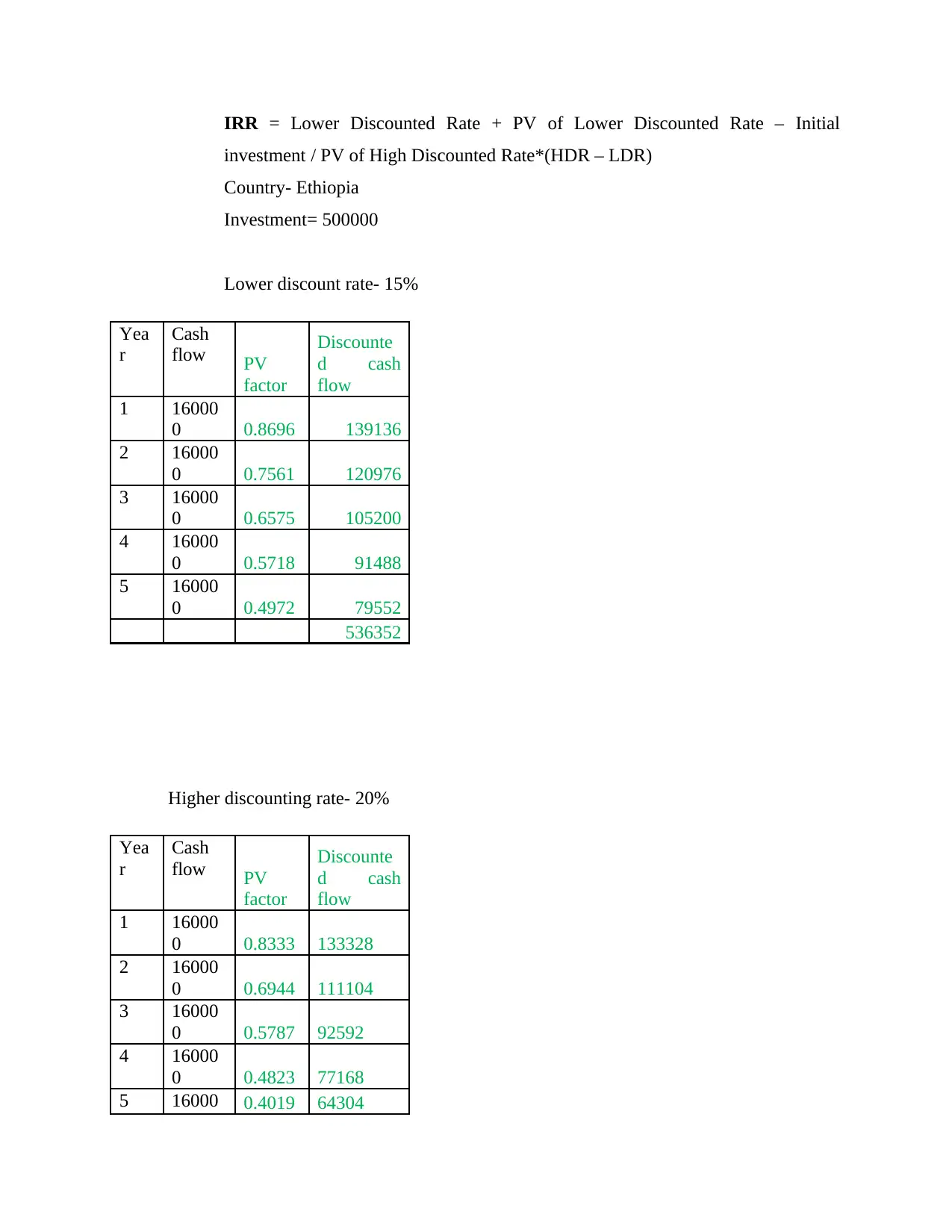

Internal rate of return

investment / PV of High Discounted Rate*(HDR – LDR)

Country- Ethiopia

Investment= 500000

Lower discount rate- 15%

Yea

r

Cash

flow PV

factor

Discounte

d cash

flow

1 16000

0 0.8696 139136

2 16000

0 0.7561 120976

3 16000

0 0.6575 105200

4 16000

0 0.5718 91488

5 16000

0 0.4972 79552

536352

Higher discounting rate- 20%

Yea

r

Cash

flow PV

factor

Discounte

d cash

flow

1 16000

0 0.8333 133328

2 16000

0 0.6944 111104

3 16000

0 0.5787 92592

4 16000

0 0.4823 77168

5 16000 0.4019 64304

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

478496

IRR= 15+536352-500000/478496*(20-15)

= 15+36352/478496*5

= 15+0.38

= 15.38

Country- Morocco

Investment= 500000

PV at 15%

Year Cash

flow PV

factor

Discounte

d cash

flow

1 19000

0 0.8696 165224

2 18000

0 0.7561 136098

3 17000

0 0.6575 111775

4 16000

0 0.5718 91488

5 15000

0 0.4972 74580

579165

PV at 20%

Paraphrase This Document

flow PV

factor

Discounte

d cash

flow

1 19000

0 0.8333 158327

2 18000

0 0.6944 124992

3 17000

0 0.5787 98379

4 16000

0 0.4823 77168

5 15000

0 0.4019 60285

519151

IRR= 15+579165-500000/519151*5

= 15+79165/500000*5

= 15.79%

Country- Bulgaria

Investment= 500000

PV at 15%

Year Cash

flow PV

factor

Discounte

d cash

flow

1 50000 0.8696 43480

2 10000

0 0.7561 75610

3 15000

0 0.6575 98625

0 0.5718 142950

5 35000

0 0.4972 174020

534685

PV at 20%

Year Cash

flow PV

factor

Discounte

d cash

flow

1 50000 0.8333 41665

2 10000

0 0.6944 69440

3 15000

0 0.5787 86805

4 25000

0 0.4823 120575

5 35000

0 0.4019 140665

459150

IRR= 15+534685-500000/459150*5

= 15+34685/459150*5

= 15.34%

Task 2 – Briefly explain the advantages and disadvantages of each method.

Payback period- It determines additional expenditures and allows the user to accept or

choose the right alternative. It is the approach of capital budgeting (Bendell and Doyle, 2017).

The payback term applies to the duration of the customer's checks. The business gains from a

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

maximized.

Advantage- The advantages of the payback period method are that it is especially beneficial for a

small company who does not have to carry out complex calculations, including selling expenses

and the revenue effect. Whether or not a project is selected is one of the most significant

strategies for the project calculating which is good for the consumer. This approach helps

managers to pick the right allocation of investments. This will entail a fast changeover, because

that would allow the business to bounce back from the initial investment sooner.

Disadvantage- The most important downside of the payback scheme is the absence of accounting

of interest on the duration. Cash flow is more critical than in later years in the first years of a

project. Two firms are bound by the same payback date. Yet one expenditure produces more

cash flow during the first few years

Net present value- NPV relates to the overall assessment actually being made of the plan,

one of the key tools employed by organizations for decision taking. This calls for a close analysis

of various intervals of cash inflow.

Advantages- The majority of companies use the NPV to determine commitment and assess

whether the company participates in this program. The positive value of the identified NPV and

its negative is rejected, because that is not a aid to the client (Adhikary and Kutsuna, 2016).

Disadvantages- Administrators may use this method for evaluating the feasibility of their firms

or to equate them to other deals, but just that the investment matches all cash flows.

Accounting rate of return- ARR assess in absolute terms the estimated cost of investment

gain or selling of the product. It is a strategic expenditure assessment and is one of the simplest

or quicker utilized by the client for project collection.

Paraphrase This Document

for the company. The management tests the ARR concept by choosing the correct layout before

settling on it.

Disadvantage- The value of resources in terms of time is not taken into account. The

methodology to capital expenditure assessment is also unscientific. For average returns, all

estimating losses and gross income do not compensate for cash flow of investments (Burns and

Dewhurst, 2016).

Internal rate of return- IRR is one of the main investment appraisal tools for most businesses

to determine if their recommendations are effective or not. Individual returns focused on a

shorter duration, calculating the real profit and evaluating the cash flow for the project involved.

Advantage- IRR is used only to define rates of return the team earns following the expenses and

then to take appropriate additional decisions.

Disadvantage- IRR recognizes economies of scale that adversely impact results. It is determined

by a control and impact process that does not yield accurate performance. The strategic decision-

making systems are also influenced.

Task 3 – Which country should the company invest in?

Payback period- On the basis of above calculated value of payback period, this can be

stated that company should go with Morocco country. This is so because under it, cost of

investment will be covered in less time in this country.

Accounting rate of return- On the basis of above calculated value of ARR, this can be

stated that company should go with Bulgaria country. This is so because under it, value of ARR

is higher that is of 36% and it is more than rest two countries.

Net present value- On the basis of above calculated value of NPV; this can be stated that

company should go with Morocco country. This is so because under it, value of NPV is higher

that is of 79165 and it is more than rest two countries.

that company should go with Morocco country. This is so because under it, value of IRR is

higher that is of 15.79 and it is more than rest two countries.

So, as per the above analysis this can be stated that company should go with Morocco because in

this country, company will sustain for long time period and will be able to generate higher

profit.

2. Source of finance:

Task 1 Difference between Ordinary Shares, Preference Share, Retained Profit and

Debentures.

Basis Ordinary Shares Preference Share Retained Profit Debentures

Meaning A common stock

is a part owner

where each

participant is a

partial owner and

sets out the

maximum

corporate liability

linked to a manage

earnings.

Preferred shares is

a form of shares

that may have a

mixture of

common equity

and debt

instrument

characteristics

which does not

include properties,

and is usually

considered a

hybrid component.

The corporation's

retained profits

are the

cumulative net

profit of the

business that is

maintained by

the corporation

for a certain date,

for example

towards the close

of the tax cycle.

A debenture is a

sort of collateral-

unsecured lending

tool. Since there is

no liquidity

protection for

debentures, the

debentures will be

backed by the

creditworthiness

and prestige of the

borrower. Both

corporations and

organizations often

issue debentures in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

or capital.

Voting

rights

Such types of

stockholders have

the right to vote in

any institution

(Klopotan, Zoroja

and Meško, 2018).

These shareholders

do not have any

voting rights.

There are not

external

stakeholders of

this profit as it is

generated inside

the firm.

The debenture

holders also do not

have voting rights.

Return Equity share

holders are being

paid dividend after

preference

shareholders.

They get a fixed

amount of

dividend before

ordinary share

holders.

It is a sort of

profit in which

no return is

provided to

anyone.

The debenture

holders also get a

common dividend.

From above all source of finance, company can raise funds of 500000 pounds from ordinary

shares. This is so because it is less risky and company does not require paying any fixed

amount of dividend to these shareholders.

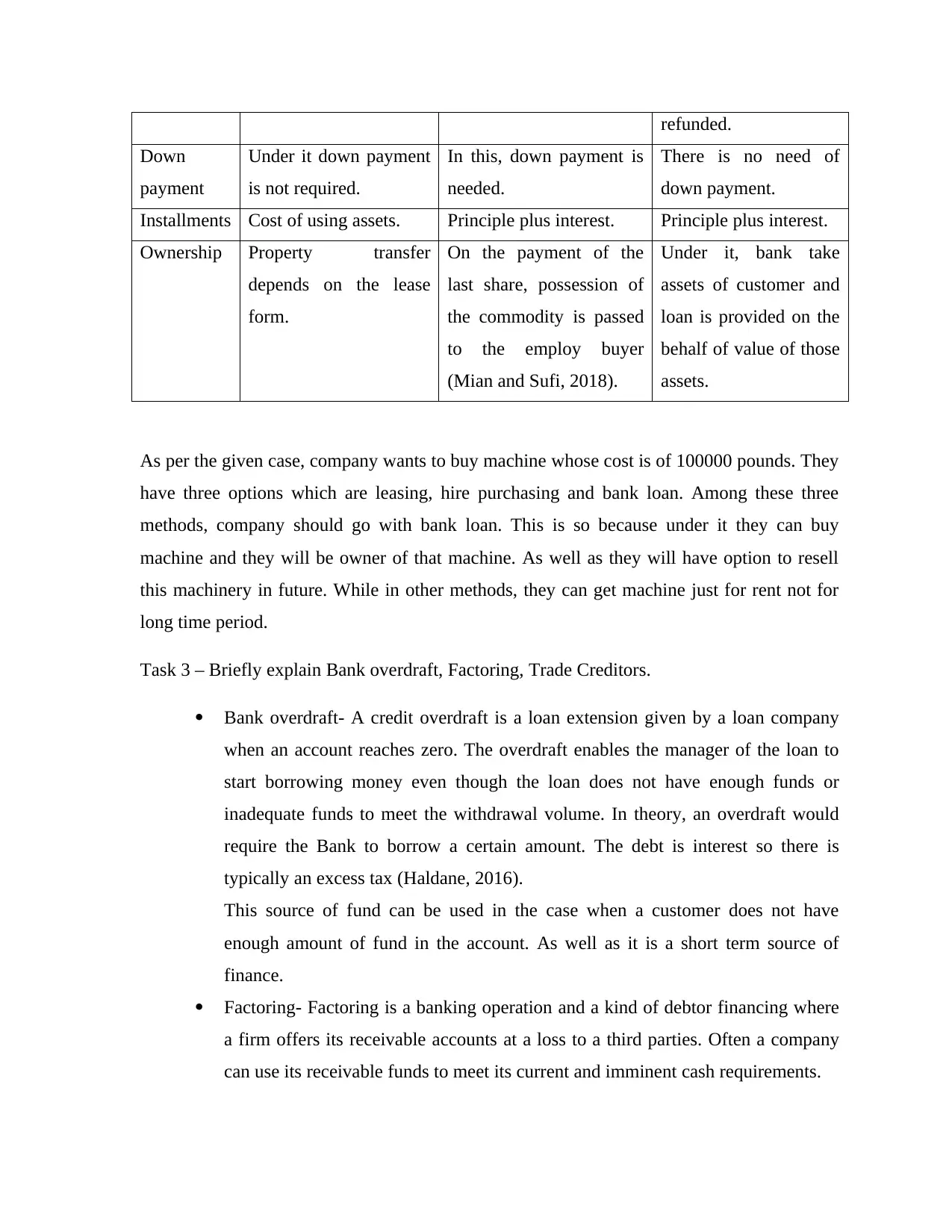

Task 2 Differences between Leasing, Hire Purchasing and Bank Loan:

Basis Leasing Hire Purchasing Bank Loan

Meaning Leasing is a contract

where one party buys

the goods and permits

the other party to use

them by paying for a

certain period is known

as leasing. Leasing is an

agreement.

Hire Purchasing is called

the contract in which one

group can use the other

group's assets for

equivalent monthly

installments.

In financial words, a

loan is the lending to

certain persons,

organizations or other

institutions with

capital. The borrower is

obligated to pay

interest on the loan, and

generally to repay the

principal sum lent

before the loan is

Paraphrase This Document

Down

payment

Under it down payment

is not required.

In this, down payment is

needed.

There is no need of

down payment.

Installments Cost of using assets. Principle plus interest. Principle plus interest.

Ownership Property transfer

depends on the lease

form.

On the payment of the

last share, possession of

the commodity is passed

to the employ buyer

(Mian and Sufi, 2018).

Under it, bank take

assets of customer and

loan is provided on the

behalf of value of those

assets.

As per the given case, company wants to buy machine whose cost is of 100000 pounds. They

have three options which are leasing, hire purchasing and bank loan. Among these three

methods, company should go with bank loan. This is so because under it they can buy

machine and they will be owner of that machine. As well as they will have option to resell

this machinery in future. While in other methods, they can get machine just for rent not for

long time period.

Task 3 – Briefly explain Bank overdraft, Factoring, Trade Creditors.

Bank overdraft- A credit overdraft is a loan extension given by a loan company

when an account reaches zero. The overdraft enables the manager of the loan to

start borrowing money even though the loan does not have enough funds or

inadequate funds to meet the withdrawal volume. In theory, an overdraft would

require the Bank to borrow a certain amount. The debt is interest so there is

typically an excess tax (Haldane, 2016).

This source of fund can be used in the case when a customer does not have

enough amount of fund in the account. As well as it is a short term source of

finance.

Factoring- Factoring is a banking operation and a kind of debtor financing where

a firm offers its receivable accounts at a loss to a third parties. Often a company

can use its receivable funds to meet its current and imminent cash requirements.

companies can sell their receivables to others.

Trade Creditors- Suppliers of which the supplier is obligated to pay for raw

materials or parts of a good. Deal partners and the sums to be due are classified as

obligations in corporate accounting procedures.

The source of finance is provided by suppliers to companies for short time period

when company does not have enough amounts of financial resources.

3. Flexible budget:

Task 1 Preparation of flexible budget-

Flexed budget operating statement for the year 31ST January 2019:

Particulars Budget Flex Actual Variance

Level of activity 50% 60% 60%

£ £

Costs:

Direct material 50000 60000 61000 1000 F

Direct labor 100000 120000 118000 2000 A

Variable overheads 10000 12000 14000 2000 F

Total variable cost 160000 192000 193000 1000 F

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Comment on findings- On the basis of above prepared flexible budget, this can be stated that all

the variances are showing adverse result. This is so because each aspect or expense is higher than

budgeted expense. Due to which result is negative. In this situation, it is essential for companies

to focus on minimizing their expenses and try to keep the value of cost lower then estimation.

Task 2 Behavioral issues in budgeting and its importance in budget setting.

There are behavior issues in budgets, such as manager's ineffective actions and budgetary

slackness. Such behavioral issues are made more apparent when analyzing their current results

and evaluating budget performance. Below some issues in budgeting are mentioned that are as

follows:

Dysfunctional Behavior- Budgets can bring positive behavior among people if

each manager’s objectives conform to the organization's goals (Heaton, Polson

and Witte, 2017). The perfect match (or close correspondence) between

organizational and management objectives is often referred to as the goal

congruence. Managers participating with the planning cycle should be happy to

deliver a realistic proposal for their organizational priorities and objectives.

Participative budgeting- Participatory budgeting is a budgeting mechanism that

includes citizens in the lower management ranks in the process of planning the

budget. In comparison to the budgeting mechanism implemented, participatory

budgeting is important for offering lower management a sense of control in the

company.

Budgetary slack- Budgetary slowness is often known as budget padding where a

planner intentionally underestimates revenue, overestimates expenses and needs

more capital than is necessary to sustain the budget amount of operations. The

discrepancy between a person's sales or expense projections versus a reasonable

expenditure or benefit projection is defined as fiscal slackness.

Paraphrase This Document

technical and official. In fact, though, budgeting is more frequently an informal

mechanism for discussions or where departmental managers fight for limited

resources in the company. According to Hopwood, this can dilute the initial aims,

as managers’ attempt (and struggle) to gain control and respect. Departmental

disputes or disagreements between the administrators are often related to the fact

that each organization struggles to reach its goals.

So these are the main behavioral issues in budgeting and these are important for budgeting

due to following reasons:

Budget is a critical tool for controlling. It can help to plan, implement, implement and

manage the company's strategic plan. There are behavior issues in budgets, such as manager's

ineffective actions and budgetary slackness (Cumming and Vismara, 2017). These behavioral

problems become more apparent in comparison and assessment of budget performance with

their actual performance. The outcome of the analysis and assessment may be directly linked

to the reward level. On the basis of it, manager of companies take suitable steps for next year

financial plan.

4. Break Even Analysis

Task 1 calculation:

C/S ratio= Contribution / sales *100

= 3/7*100

= 42.86%

Working Note:

Contribution= sales-variable expenses

= 7-4

Breakeven point (In units)= Fixed cost/contribution

= 50000/3

= 16666 units

Breakeven point (in sales)= Fixed cost/ PV ratio

= 50000/42.86%

= 116658 pounds

Number of units to make profit of 31000 pounds:

Units to be sold= Desired profit / Contribution per unit + Breakeven point in units

= 31000/3+16666

= 27000 units

Sales value to make profit of 31000 pounds:

Sales value to make profit= Desired profit / Contribution per unit + Breakeven

point in sales

= 31000/3+116658

= 126991 pounds

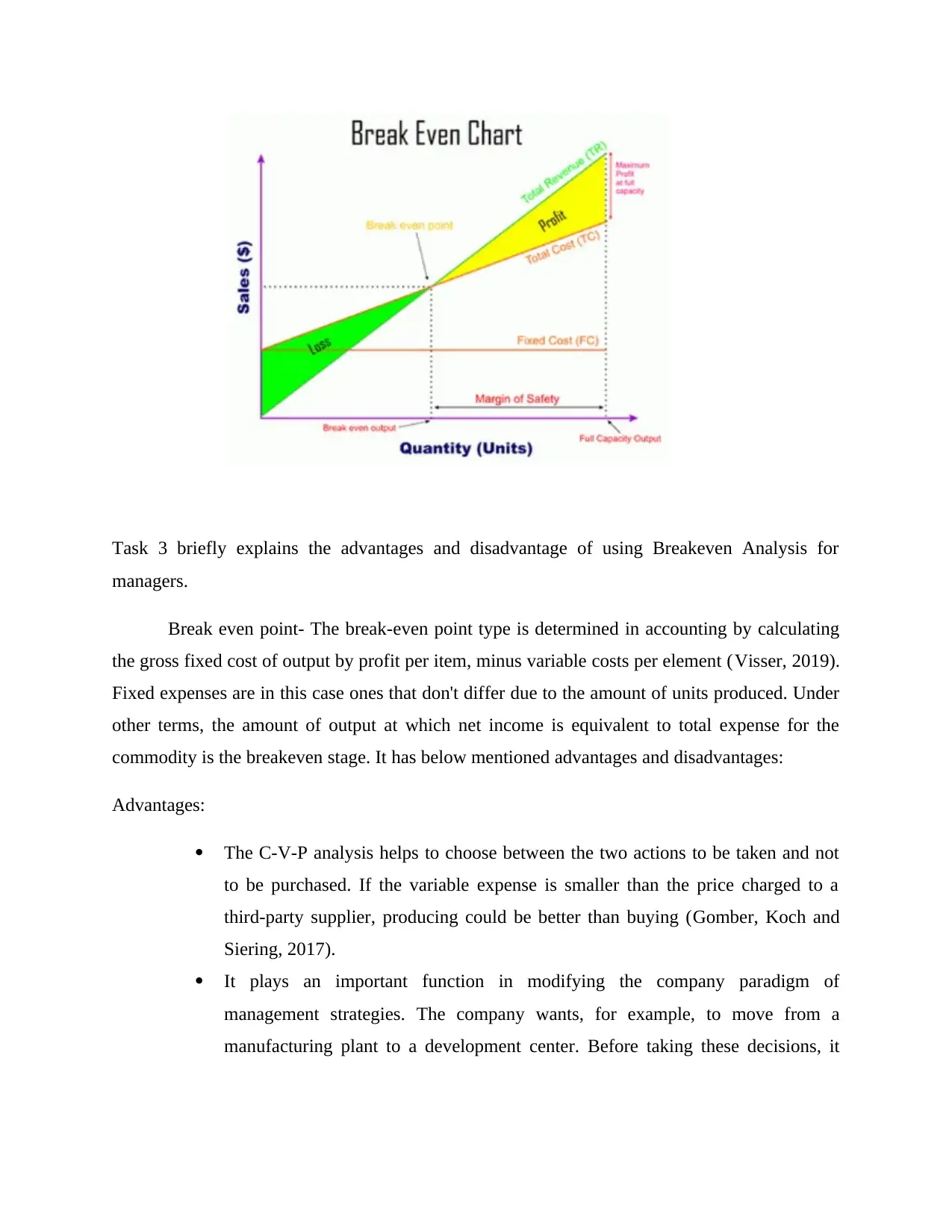

Task 2 Break even chart:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

managers.

Break even point- The break-even point type is determined in accounting by calculating

the gross fixed cost of output by profit per item, minus variable costs per element (Visser, 2019).

Fixed expenses are in this case ones that don't differ due to the amount of units produced. Under

other terms, the amount of output at which net income is equivalent to total expense for the

commodity is the breakeven stage. It has below mentioned advantages and disadvantages:

Advantages:

The C-V-P analysis helps to choose between the two actions to be taken and not

to be purchased. If the variable expense is smaller than the price charged to a

third-party supplier, producing could be better than buying (Gomber, Koch and

Siering, 2017).

It plays an important function in modifying the company paradigm of

management strategies. The company wants, for example, to move from a

manufacturing plant to a development center. Before taking these decisions, it

Paraphrase This Document

projected revenue and benefit.

Disadvantages:

The break-even diagram is based on assumptions. But the assumptions are not

right. In addition to the actual operating point, the fixed costs will differ.

Similarly, if the rule of the decrease or increase in return is valid in the company,

variable costs shall not differ in direct relation to degree of service.

The total cost line and the sales line appear straight in the break-even chart.

Because these definitions are not right, in reality these lines are not drawn

straight. It contributes to different break-even points at varying operation stages

(Cochrane, 2017).

CONCLUSION

On the basis of above project report this can be concluded that company should make

proper analysis of available funds. From the first part of report this can be concluded that

company should start their business in Morocco country because all methods are showing that

investing in this country will be beneficial for them. Under second part various kinds of source

of finance are mentioned and each of them has some features and drawbacks. The further part of

report concludes about flexible budget and variances as well as role of budgetary slack in budget

setting. The end part of report articulates about calculation of BEP and its advantages &

drawbacks.

Books and journal:

Ylhäinen, I., 2017. Life-cycle effects in small business finance. Journal of Banking &

Finance, 77, pp.176-196.

Bendell, J. and Doyle, I., 2017. Healing capitalism: five years in the life of business, finance and

corporate responsibility. Routledge.

Adhikary, B. and Kutsuna, K., 2016. Small Business Finance in Bangladesh:

Can'Crowdfunding'Be an Alternative?. Review of Integrative Business and Economics

Research, 4, pp.1-21.

Burns, P. and Dewhurst, J. eds., 2016. Small business and entrepreneurship. Macmillan

International Higher Education.

Klopotan, I., Zoroja, J. and Meško, M., 2018. Early warning system in business, finance, and

economics: Bibliometric and topic analysis. International Journal of Engineering

Business Management, 10, p.1847979018797013.

Mian, A. and Sufi, A., 2018. Finance and business cycles: the credit-driven household demand

channel. Journal of Economic Perspectives, 32(3), pp.31-58.

Haldane, A., 2016. Finance Version 2.0. Speech, Bank of England, 7.

Heaton, J.B., Polson, N.G. and Witte, J.H., 2017. Deep learning for finance: deep

portfolios. Applied Stochastic Models in Business and Industry, 33(1), pp.3-12.

Cumming, D.J. and Vismara, S., 2017. De-segmenting research in entrepreneurial

finance. Venture Capital, 19(1-2), pp.17-27.

Visser, H., 2019. Islamic finance: Principles and practice. Edward Elgar Publishing.

Gomber, P., Koch, J.A. and Siering, M., 2017. Digital Finance and FinTech: current research and

future research directions. Journal of Business Economics, 87(5), pp.537-580.

Cochrane, J.H., 2017. Macro-finance. Review of Finance, 21(3), pp.945-985.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.