Business Finance Analysis: Trend Ltd and Thorne Estates Limited

VerifiedAdded on 2022/12/17

|11

|3075

|28

Report

AI Summary

This report provides a comprehensive analysis of two companies' financial activities. It begins with an executive summary of Trend Ltd's finance in manufacturing fitness and footwear, exploring concepts such as profit, cash flow, working capital, receivables, inventories, and payables. The report examines the impact of operational management on financial results and recommends steps to improve cash flow through better working capital management. The second part of the report focuses on Thorne Estates Limited, presenting monthly cash budgets from January to April 2021 and offering recommendations to management based on the budget analysis. The report emphasizes the importance of cash flow management and financial planning for business stability and growth, including discussions on receivables, inventory, and payables and their impact on cash flow. The report provides a detailed overview of financial planning practices and offers recommendations to enhance cash governance.

Business finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Executive Summary.........................................................................................................................3

Task 1...............................................................................................................................................3

1. Explain.....................................................................................................................................3

2. Impact of company's operational management on financial results........................................5

3. Steps recommended to improve company's cash flow through better working capital

management.................................................................................................................................5

Executive Summary.........................................................................................................................7

Task 2...............................................................................................................................................7

1. Monthly cash budgets from 1st Jan to 30th April 2021...........................................................7

Monthly cash budgets..................................................................................................................7

2. Recommendations to the management of Thorne Estates Limited.........................................9

References......................................................................................................................................11

Executive Summary.........................................................................................................................3

Task 1...............................................................................................................................................3

1. Explain.....................................................................................................................................3

2. Impact of company's operational management on financial results........................................5

3. Steps recommended to improve company's cash flow through better working capital

management.................................................................................................................................5

Executive Summary.........................................................................................................................7

Task 2...............................................................................................................................................7

1. Monthly cash budgets from 1st Jan to 30th April 2021...........................................................7

Monthly cash budgets..................................................................................................................7

2. Recommendations to the management of Thorne Estates Limited.........................................9

References......................................................................................................................................11

Executive Summary

Financial management of company issues includes cash activities. It encompasses sales and cash

controls to ensure the company's financial stability. The focus of this research is to cover Trend

Ltd (TL corporate)'s finance activities in manufacturing of fitness and footwear. Trend Ltd

explores terms such as benefit, cash flow, operating expenses, receipts, inventory and payable

and evaluates their effect on the accounting records. Forms are also addressed to increase cash

flow through improved control of capital expenditures.

Task 1

1. Explain

A. Profit and cash flow

Profit - Profit is some over-cost sales. Income is the financial gain gained because the company's

net revenues outweigh the company's total expenditures. The corporation shall be either held for

future activities by a company or shall be divided to the owners (Klopotan, Zoroja and Meško,

2018). It is collected from a benefit and loss account sometimes called the revenue statement. A

business breaks into separate phases of its profit and loss account — firstly, processing profit

known as gross profit. Additionally, additional marketing and promotions costs are much lower

to the total revenue from gross profit. In addition, all non-operating expenditures and sales are

adjusted. Further, the final amount of net profit, also known as systemic profits, is calculated for

both non-operating costs and revenue. This surplus is then converted to the profit after tax by

income tax. It is said that the owners have this level of value accessible.

Cash flow - Cash balance applies to the net cash flow of a company over a certain time. Cash

refunds are considered inflow when outflow is cash transfers. If cash flow in a company beats

cash outflow, it is considered as a favourable situation for the firm and the shareholders will gain

more value (Mian and Sufi, 2018). For businesses to ensure smooth processes, cash flow control

is of extreme importance. Businesses also plan financial statement as operational requirements.

These plans are regularly, quarterly, half-yearly or annually tracked and revised to make

appropriate changes. An additional cash flow statement is designed for an aggregate cash inflow

outflow situation throughout the year or the time stated in the Company's balance sheet. The cash

flow is split into three sections – operational cash flow, investment cash flow and funding cash

flow. Operations require transactions, purchases, accounting operations, etc. Investment takes

Financial management of company issues includes cash activities. It encompasses sales and cash

controls to ensure the company's financial stability. The focus of this research is to cover Trend

Ltd (TL corporate)'s finance activities in manufacturing of fitness and footwear. Trend Ltd

explores terms such as benefit, cash flow, operating expenses, receipts, inventory and payable

and evaluates their effect on the accounting records. Forms are also addressed to increase cash

flow through improved control of capital expenditures.

Task 1

1. Explain

A. Profit and cash flow

Profit - Profit is some over-cost sales. Income is the financial gain gained because the company's

net revenues outweigh the company's total expenditures. The corporation shall be either held for

future activities by a company or shall be divided to the owners (Klopotan, Zoroja and Meško,

2018). It is collected from a benefit and loss account sometimes called the revenue statement. A

business breaks into separate phases of its profit and loss account — firstly, processing profit

known as gross profit. Additionally, additional marketing and promotions costs are much lower

to the total revenue from gross profit. In addition, all non-operating expenditures and sales are

adjusted. Further, the final amount of net profit, also known as systemic profits, is calculated for

both non-operating costs and revenue. This surplus is then converted to the profit after tax by

income tax. It is said that the owners have this level of value accessible.

Cash flow - Cash balance applies to the net cash flow of a company over a certain time. Cash

refunds are considered inflow when outflow is cash transfers. If cash flow in a company beats

cash outflow, it is considered as a favourable situation for the firm and the shareholders will gain

more value (Mian and Sufi, 2018). For businesses to ensure smooth processes, cash flow control

is of extreme importance. Businesses also plan financial statement as operational requirements.

These plans are regularly, quarterly, half-yearly or annually tracked and revised to make

appropriate changes. An additional cash flow statement is designed for an aggregate cash inflow

outflow situation throughout the year or the time stated in the Company's balance sheet. The cash

flow is split into three sections – operational cash flow, investment cash flow and funding cash

flow. Operations require transactions, purchases, accounting operations, etc. Investment takes

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

account of corporate investment input and outlet, circulated loans, interest received, selling of

capital assets — acquisition. Financing operations take account of financial structure changes,

loans used, interest payments, dividends.

Difference between two- The most important distinction between return on investments is that

profit is really just an accounting body that reports net profits generated in companies, whereas

cash flows reflect actual cash flows and outflows. In other terms, benefit is profitability of the

company and cash flow is stability of the company. Another distinction is that a corporation

benefits from the accounting standard while the cash balance of the company is measured from

the cash accounting information system.

B. Working Capital, receivables, inventories and payables

Working Capital - Two elements of working capital include accumulated assets, including such

currency, accounts receivables etc. and interest expense like payables, short-term lending, etc., as

a total balance of each (Young, 2018). When existing assets outweigh current liabilities, they are

known as the business's optimistic working capital

Receivables - Account receivables are those that owe money to businesses like commercial

debtors. This is the company's cash assets which represent those amounts that produce business

revenues in the coming years. In order to control the debtors payment period, the organisation

operates a special scheme to deal with industrial debtors.

Inventories - Stocks mean all the goods produced and traded by a corporation. It is kept between

productions or order by organisation before delivery is fulfilled. They can be either untreated,

medium or finished goods.

Payables - Account payables mean certain individuals, such as company creditors, who owe the

money to company. These are the firm's organizational obligations which represent those sums

to be charged in the immediate future by the company. Company operates a different payout time

bargaining scheme for business creditors.

C. Impact of change in working capital on cash flow

Working capital management and cash flow are important to the enterprise and communicate

with one another as the business analyses its profitability. Working capital is the disparity

between new and current obligations or, in many other terms, decides a corporation's free cash

for short-term liabilities (Tenca, Croce and Ughetto, 2018). Total assets contain currency and

capital assets — acquisition. Financing operations take account of financial structure changes,

loans used, interest payments, dividends.

Difference between two- The most important distinction between return on investments is that

profit is really just an accounting body that reports net profits generated in companies, whereas

cash flows reflect actual cash flows and outflows. In other terms, benefit is profitability of the

company and cash flow is stability of the company. Another distinction is that a corporation

benefits from the accounting standard while the cash balance of the company is measured from

the cash accounting information system.

B. Working Capital, receivables, inventories and payables

Working Capital - Two elements of working capital include accumulated assets, including such

currency, accounts receivables etc. and interest expense like payables, short-term lending, etc., as

a total balance of each (Young, 2018). When existing assets outweigh current liabilities, they are

known as the business's optimistic working capital

Receivables - Account receivables are those that owe money to businesses like commercial

debtors. This is the company's cash assets which represent those amounts that produce business

revenues in the coming years. In order to control the debtors payment period, the organisation

operates a special scheme to deal with industrial debtors.

Inventories - Stocks mean all the goods produced and traded by a corporation. It is kept between

productions or order by organisation before delivery is fulfilled. They can be either untreated,

medium or finished goods.

Payables - Account payables mean certain individuals, such as company creditors, who owe the

money to company. These are the firm's organizational obligations which represent those sums

to be charged in the immediate future by the company. Company operates a different payout time

bargaining scheme for business creditors.

C. Impact of change in working capital on cash flow

Working capital management and cash flow are important to the enterprise and communicate

with one another as the business analyses its profitability. Working capital is the disparity

between new and current obligations or, in many other terms, decides a corporation's free cash

for short-term liabilities (Tenca, Croce and Ughetto, 2018). Total assets contain currency and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

cash reserves that are a topic in the levels of cash flow. Positive working capital ensures that the

company has adequate resources to support its existing obligations which reflect its stable

financial status and good cash flow. On the other side, negative approach could not have given

enough resources to fund the existing liabilities. That may also lead to a corporation having

either paid enormous cash in the short term, or massive assets, which are not available in

companies, are needed in the near future. This protracted scenario is not a good one for the sector

and could cause liquidity problems for companies in the future.

2. Impact of company's operational management on financial results

Last year, the net profit of this business Trend Ltd. amounted to £60 million. This estimate is

acceptable and reflects the company's profitability. According to the given details, nevertheless,

the behavior of owner Arpha and the management of work capital were affected by productivity.

Debtor Tkechers owes £10 million, the creditor was in conflict for £12.5 million, and stock

piling supplies are available to avert work stoppage, meanwhile a disagreement with big

suppliers is settled. Moreover, Arpha is not able to press other consumers for reimbursement to

prevent further conflicts. Both this will have enormous adverse effects on working income and

financial performance. The value of debt has also risen from £60 million over the last year to £95

million in 2011. This indicates that the business has £35 million in extra capital, whilst the

investment in a corporation resulted in a loss of £20 million. This not only affected business

funding decisions, as well as the investment of cash flow choices.

3. Steps recommended to improve company's cash flow through better

working capital management

The study above suggests that the corporation improves the handling of their capital

expenditures:

• Company would attempt to retrieve the cash from all its debtors as quickly as possible in order

to prevent any decrease and the possibility of sub-liquidation. In addition, debtors with past or

record of default or missed payments shall be handled differently or not entirely.

• The Company is in litigation with Sadidas over £12.5 million that it refused reimbursement.

Manager Arpha claims that this conflict occurred because of a provider's poor quality provision

of materials and thus refused payment. It is now in danger of being tried by the retailer. The

company has adequate resources to support its existing obligations which reflect its stable

financial status and good cash flow. On the other side, negative approach could not have given

enough resources to fund the existing liabilities. That may also lead to a corporation having

either paid enormous cash in the short term, or massive assets, which are not available in

companies, are needed in the near future. This protracted scenario is not a good one for the sector

and could cause liquidity problems for companies in the future.

2. Impact of company's operational management on financial results

Last year, the net profit of this business Trend Ltd. amounted to £60 million. This estimate is

acceptable and reflects the company's profitability. According to the given details, nevertheless,

the behavior of owner Arpha and the management of work capital were affected by productivity.

Debtor Tkechers owes £10 million, the creditor was in conflict for £12.5 million, and stock

piling supplies are available to avert work stoppage, meanwhile a disagreement with big

suppliers is settled. Moreover, Arpha is not able to press other consumers for reimbursement to

prevent further conflicts. Both this will have enormous adverse effects on working income and

financial performance. The value of debt has also risen from £60 million over the last year to £95

million in 2011. This indicates that the business has £35 million in extra capital, whilst the

investment in a corporation resulted in a loss of £20 million. This not only affected business

funding decisions, as well as the investment of cash flow choices.

3. Steps recommended to improve company's cash flow through better

working capital management

The study above suggests that the corporation improves the handling of their capital

expenditures:

• Company would attempt to retrieve the cash from all its debtors as quickly as possible in order

to prevent any decrease and the possibility of sub-liquidation. In addition, debtors with past or

record of default or missed payments shall be handled differently or not entirely.

• The Company is in litigation with Sadidas over £12.5 million that it refused reimbursement.

Manager Arpha claims that this conflict occurred because of a provider's poor quality provision

of materials and thus refused payment. It is now in danger of being tried by the retailer. The

corporation is engaged in lawsuits that threaten the company's cash flow and operating resources

as well as its development and operations potential. It would then aim to resolve conflicts as

quickly as possible.

• In addition, in one of its warehouses Arpha has built up a quantity of inventories more than

needed to prevent interruptions in the time of dispute resolution. The company must stop over-

stocking because it would entail excessive inventory costs. This should instead provide for every

other provider to render emergency supplies of raw material.

as well as its development and operations potential. It would then aim to resolve conflicts as

quickly as possible.

• In addition, in one of its warehouses Arpha has built up a quantity of inventories more than

needed to prevent interruptions in the time of dispute resolution. The company must stop over-

stocking because it would entail excessive inventory costs. This should instead provide for every

other provider to render emergency supplies of raw material.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

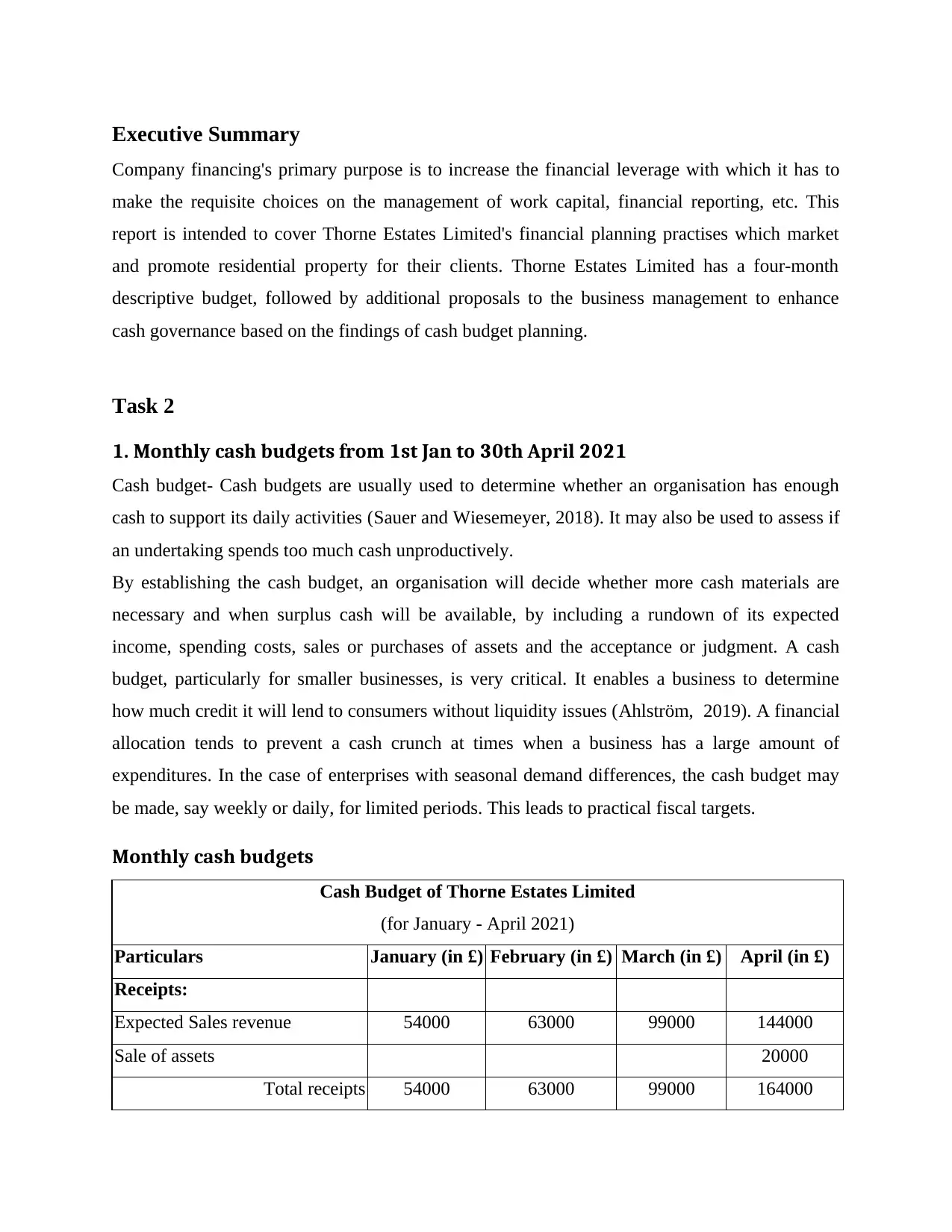

Executive Summary

Company financing's primary purpose is to increase the financial leverage with which it has to

make the requisite choices on the management of work capital, financial reporting, etc. This

report is intended to cover Thorne Estates Limited's financial planning practises which market

and promote residential property for their clients. Thorne Estates Limited has a four-month

descriptive budget, followed by additional proposals to the business management to enhance

cash governance based on the findings of cash budget planning.

Task 2

1. Monthly cash budgets from 1st Jan to 30th April 2021

Cash budget- Cash budgets are usually used to determine whether an organisation has enough

cash to support its daily activities (Sauer and Wiesemeyer, 2018). It may also be used to assess if

an undertaking spends too much cash unproductively.

By establishing the cash budget, an organisation will decide whether more cash materials are

necessary and when surplus cash will be available, by including a rundown of its expected

income, spending costs, sales or purchases of assets and the acceptance or judgment. A cash

budget, particularly for smaller businesses, is very critical. It enables a business to determine

how much credit it will lend to consumers without liquidity issues (Ahlström, 2019). A financial

allocation tends to prevent a cash crunch at times when a business has a large amount of

expenditures. In the case of enterprises with seasonal demand differences, the cash budget may

be made, say weekly or daily, for limited periods. This leads to practical fiscal targets.

Monthly cash budgets

Cash Budget of Thorne Estates Limited

(for January - April 2021)

Particulars January (in £) February (in £) March (in £) April (in £)

Receipts:

Expected Sales revenue 54000 63000 99000 144000

Sale of assets 20000

Total receipts 54000 63000 99000 164000

Company financing's primary purpose is to increase the financial leverage with which it has to

make the requisite choices on the management of work capital, financial reporting, etc. This

report is intended to cover Thorne Estates Limited's financial planning practises which market

and promote residential property for their clients. Thorne Estates Limited has a four-month

descriptive budget, followed by additional proposals to the business management to enhance

cash governance based on the findings of cash budget planning.

Task 2

1. Monthly cash budgets from 1st Jan to 30th April 2021

Cash budget- Cash budgets are usually used to determine whether an organisation has enough

cash to support its daily activities (Sauer and Wiesemeyer, 2018). It may also be used to assess if

an undertaking spends too much cash unproductively.

By establishing the cash budget, an organisation will decide whether more cash materials are

necessary and when surplus cash will be available, by including a rundown of its expected

income, spending costs, sales or purchases of assets and the acceptance or judgment. A cash

budget, particularly for smaller businesses, is very critical. It enables a business to determine

how much credit it will lend to consumers without liquidity issues (Ahlström, 2019). A financial

allocation tends to prevent a cash crunch at times when a business has a large amount of

expenditures. In the case of enterprises with seasonal demand differences, the cash budget may

be made, say weekly or daily, for limited periods. This leads to practical fiscal targets.

Monthly cash budgets

Cash Budget of Thorne Estates Limited

(for January - April 2021)

Particulars January (in £) February (in £) March (in £) April (in £)

Receipts:

Expected Sales revenue 54000 63000 99000 144000

Sale of assets 20000

Total receipts 54000 63000 99000 164000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

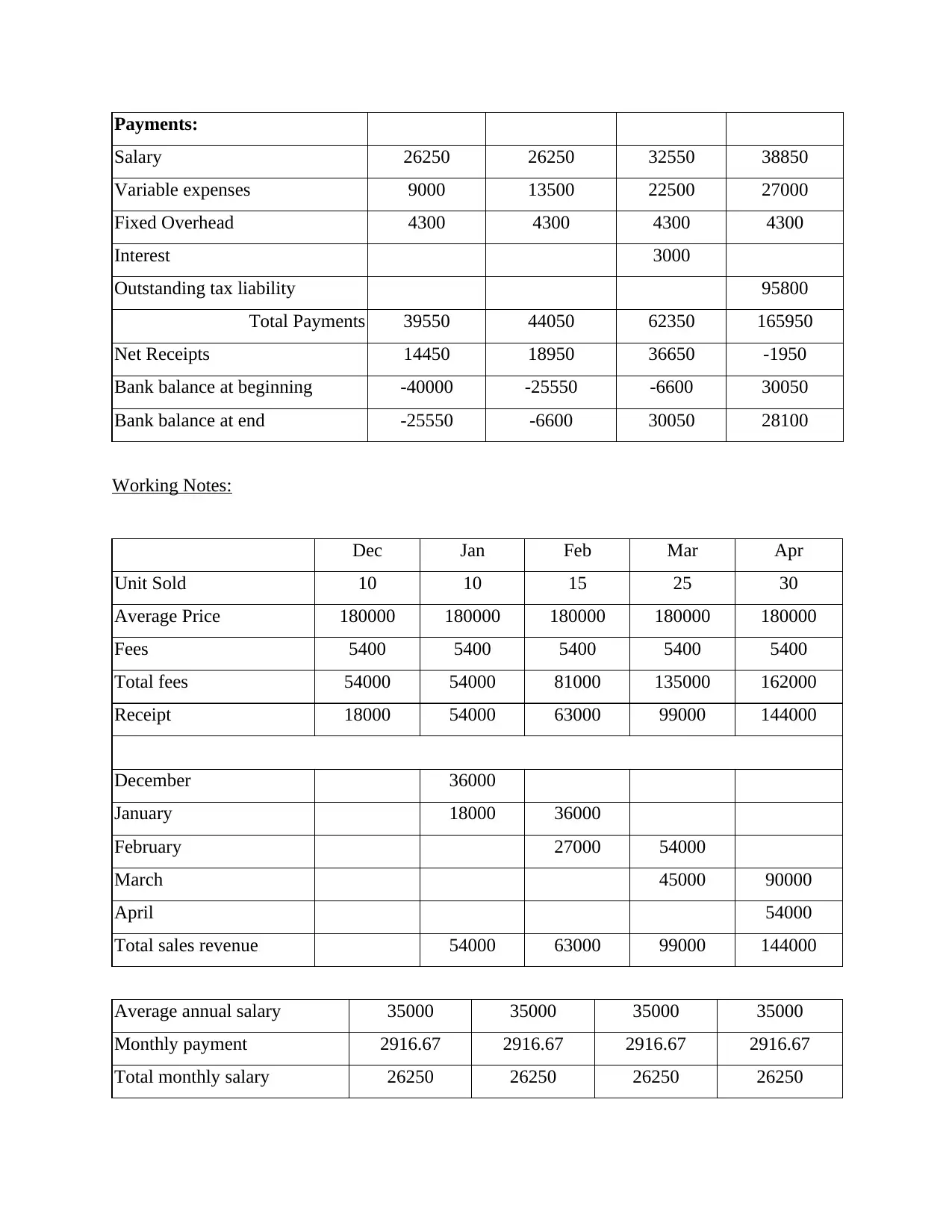

Payments:

Salary 26250 26250 32550 38850

Variable expenses 9000 13500 22500 27000

Fixed Overhead 4300 4300 4300 4300

Interest 3000

Outstanding tax liability 95800

Total Payments 39550 44050 62350 165950

Net Receipts 14450 18950 36650 -1950

Bank balance at beginning -40000 -25550 -6600 30050

Bank balance at end -25550 -6600 30050 28100

Working Notes:

Dec Jan Feb Mar Apr

Unit Sold 10 10 15 25 30

Average Price 180000 180000 180000 180000 180000

Fees 5400 5400 5400 5400 5400

Total fees 54000 54000 81000 135000 162000

Receipt 18000 54000 63000 99000 144000

December 36000

January 18000 36000

February 27000 54000

March 45000 90000

April 54000

Total sales revenue 54000 63000 99000 144000

Average annual salary 35000 35000 35000 35000

Monthly payment 2916.67 2916.67 2916.67 2916.67

Total monthly salary 26250 26250 26250 26250

Salary 26250 26250 32550 38850

Variable expenses 9000 13500 22500 27000

Fixed Overhead 4300 4300 4300 4300

Interest 3000

Outstanding tax liability 95800

Total Payments 39550 44050 62350 165950

Net Receipts 14450 18950 36650 -1950

Bank balance at beginning -40000 -25550 -6600 30050

Bank balance at end -25550 -6600 30050 28100

Working Notes:

Dec Jan Feb Mar Apr

Unit Sold 10 10 15 25 30

Average Price 180000 180000 180000 180000 180000

Fees 5400 5400 5400 5400 5400

Total fees 54000 54000 81000 135000 162000

Receipt 18000 54000 63000 99000 144000

December 36000

January 18000 36000

February 27000 54000

March 45000 90000

April 54000

Total sales revenue 54000 63000 99000 144000

Average annual salary 35000 35000 35000 35000

Monthly payment 2916.67 2916.67 2916.67 2916.67

Total monthly salary 26250 26250 26250 26250

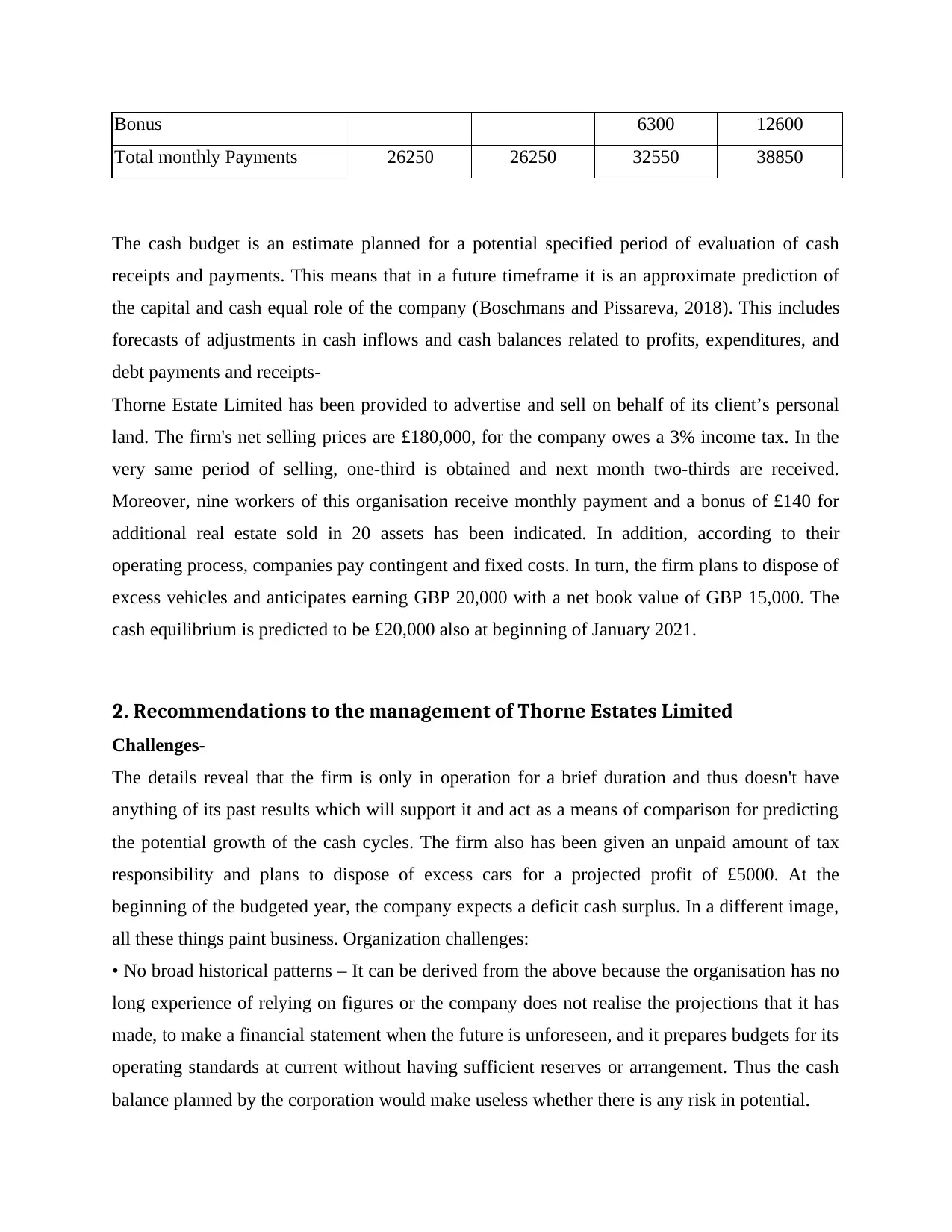

Bonus 6300 12600

Total monthly Payments 26250 26250 32550 38850

The cash budget is an estimate planned for a potential specified period of evaluation of cash

receipts and payments. This means that in a future timeframe it is an approximate prediction of

the capital and cash equal role of the company (Boschmans and Pissareva, 2018). This includes

forecasts of adjustments in cash inflows and cash balances related to profits, expenditures, and

debt payments and receipts-

Thorne Estate Limited has been provided to advertise and sell on behalf of its client’s personal

land. The firm's net selling prices are £180,000, for the company owes a 3% income tax. In the

very same period of selling, one-third is obtained and next month two-thirds are received.

Moreover, nine workers of this organisation receive monthly payment and a bonus of £140 for

additional real estate sold in 20 assets has been indicated. In addition, according to their

operating process, companies pay contingent and fixed costs. In turn, the firm plans to dispose of

excess vehicles and anticipates earning GBP 20,000 with a net book value of GBP 15,000. The

cash equilibrium is predicted to be £20,000 also at beginning of January 2021.

2. Recommendations to the management of Thorne Estates Limited

Challenges-

The details reveal that the firm is only in operation for a brief duration and thus doesn't have

anything of its past results which will support it and act as a means of comparison for predicting

the potential growth of the cash cycles. The firm also has been given an unpaid amount of tax

responsibility and plans to dispose of excess cars for a projected profit of £5000. At the

beginning of the budgeted year, the company expects a deficit cash surplus. In a different image,

all these things paint business. Organization challenges:

• No broad historical patterns – It can be derived from the above because the organisation has no

long experience of relying on figures or the company does not realise the projections that it has

made, to make a financial statement when the future is unforeseen, and it prepares budgets for its

operating standards at current without having sufficient reserves or arrangement. Thus the cash

balance planned by the corporation would make useless whether there is any risk in potential.

Total monthly Payments 26250 26250 32550 38850

The cash budget is an estimate planned for a potential specified period of evaluation of cash

receipts and payments. This means that in a future timeframe it is an approximate prediction of

the capital and cash equal role of the company (Boschmans and Pissareva, 2018). This includes

forecasts of adjustments in cash inflows and cash balances related to profits, expenditures, and

debt payments and receipts-

Thorne Estate Limited has been provided to advertise and sell on behalf of its client’s personal

land. The firm's net selling prices are £180,000, for the company owes a 3% income tax. In the

very same period of selling, one-third is obtained and next month two-thirds are received.

Moreover, nine workers of this organisation receive monthly payment and a bonus of £140 for

additional real estate sold in 20 assets has been indicated. In addition, according to their

operating process, companies pay contingent and fixed costs. In turn, the firm plans to dispose of

excess vehicles and anticipates earning GBP 20,000 with a net book value of GBP 15,000. The

cash equilibrium is predicted to be £20,000 also at beginning of January 2021.

2. Recommendations to the management of Thorne Estates Limited

Challenges-

The details reveal that the firm is only in operation for a brief duration and thus doesn't have

anything of its past results which will support it and act as a means of comparison for predicting

the potential growth of the cash cycles. The firm also has been given an unpaid amount of tax

responsibility and plans to dispose of excess cars for a projected profit of £5000. At the

beginning of the budgeted year, the company expects a deficit cash surplus. In a different image,

all these things paint business. Organization challenges:

• No broad historical patterns – It can be derived from the above because the organisation has no

long experience of relying on figures or the company does not realise the projections that it has

made, to make a financial statement when the future is unforeseen, and it prepares budgets for its

operating standards at current without having sufficient reserves or arrangement. Thus the cash

balance planned by the corporation would make useless whether there is any risk in potential.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

• Cash flow shortfall – The Corporation’s shortfall balance is projected to occur in January 2021

at the start. It has a 4-month budget and expects strong cash flows at the end of the 4-month

forecast cycle. Furthermore, if the organisation experiences volatile cash flows over the forecast

period, any strategy would be unsuccessful. Under-liquidation and over-liquidation also are

challenges with money management of a corporation to be under-liquidated, which can lead to

stoppage of activities.

Recommendations

In view of the terms set out above, the business is advised to ensure that the cash flow control is

smooth:

• To avoid a shortfall cash balance problem, companies must rethink negotiations with its

company partners such as suppliers, lenders, sellers, other borrowers, and so forth. The

business's partners must be made aware that their arrangements are checked to accommodate

their cash flow positions and a win-win outcome for both parties is established. A successful

business partner is often sponsored by employees and can also give better terms to the corporate.

In addition, business partners can aim to increase their profits and decrease costs apart from

signing agreements. It should aim to improve its business practises and then sell clients. It will

provide coupons and other consumer attraction rewards.

• The company's cash expenditure performance is focused on sales goals otherwise an

overarching budget goal is achieved and the company's cash preparation is interrupted (La Torre,

Chiappini and Rizzello, 2019). The corporation shall make a flexible budget and check them

annually to find differences before it becomes harmful, in order to prevent all other problems.

Variance research aims to plan disciplinary steps that track the company's cash management. In

addition, businesses should build a budget for a number of possible sales and spending situations,

to consider the manner in which such a situation should be tailored to occur. Even so, the

planning of budgets can be costly and businesses don't have to cost.

• The company's budget is very condensed and has not taken possible scenarios into account nor

space for other costs that might lead to issues with cash management. The Corporation would

also make a more comprehensive budget and therefore make extra funding available as

contingency and arrangements. The budget shall be split carefully into right headings so as to

define the proper costs and trend. This helps companies to optimise the composition of their sales

and costs.

at the start. It has a 4-month budget and expects strong cash flows at the end of the 4-month

forecast cycle. Furthermore, if the organisation experiences volatile cash flows over the forecast

period, any strategy would be unsuccessful. Under-liquidation and over-liquidation also are

challenges with money management of a corporation to be under-liquidated, which can lead to

stoppage of activities.

Recommendations

In view of the terms set out above, the business is advised to ensure that the cash flow control is

smooth:

• To avoid a shortfall cash balance problem, companies must rethink negotiations with its

company partners such as suppliers, lenders, sellers, other borrowers, and so forth. The

business's partners must be made aware that their arrangements are checked to accommodate

their cash flow positions and a win-win outcome for both parties is established. A successful

business partner is often sponsored by employees and can also give better terms to the corporate.

In addition, business partners can aim to increase their profits and decrease costs apart from

signing agreements. It should aim to improve its business practises and then sell clients. It will

provide coupons and other consumer attraction rewards.

• The company's cash expenditure performance is focused on sales goals otherwise an

overarching budget goal is achieved and the company's cash preparation is interrupted (La Torre,

Chiappini and Rizzello, 2019). The corporation shall make a flexible budget and check them

annually to find differences before it becomes harmful, in order to prevent all other problems.

Variance research aims to plan disciplinary steps that track the company's cash management. In

addition, businesses should build a budget for a number of possible sales and spending situations,

to consider the manner in which such a situation should be tailored to occur. Even so, the

planning of budgets can be costly and businesses don't have to cost.

• The company's budget is very condensed and has not taken possible scenarios into account nor

space for other costs that might lead to issues with cash management. The Corporation would

also make a more comprehensive budget and therefore make extra funding available as

contingency and arrangements. The budget shall be split carefully into right headings so as to

define the proper costs and trend. This helps companies to optimise the composition of their sales

and costs.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Klopotan, I., Zoroja, J. and Meško, M., 2018. Early warning system in business, finance, and

economics: Bibliometric and topic analysis. International Journal of Engineering

Business Management, 10, p.1847979018797013.

Mian, A. and Sufi, A., 2018. Finance and business cycles: the credit-driven household demand

channel. Journal of Economic Perspectives, 32(3), pp.31-58.

Young, C., 2018. Can women win on the obstacle course of business finance?.

Tenca, F., Croce, A. and Ughetto, E., 2018. Business angels research in entrepreneurial finance:

A literature review and a research agenda. Journal of Economic Surveys, 32(5), pp.1384-

1413.

Sauer, R.M. and Wiesemeyer, K.H., 2018. Entrepreneurship and gender: differential access to

finance and divergent business value. Oxford Review of Economic Policy, 34(4), pp.584-

596.

Ahlström, H., 2019. Policy Hotspots for Sustainability: Changes in the EU Regulation of

Sustainable Business and Finance. Sustainability, 11(2), p.499.

La Torre, M., Trotta, A., Chiappini, H. and Rizzello, A., 2019. Business models for sustainable

finance: The case study of social impact bonds. Sustainability, 11(7), p.1887.

Boschmans, K. and Pissareva, L., 2018. Fostering Markets for SME Finance: Matching Business

and Investor Needs.

Klopotan, I., Zoroja, J. and Meško, M., 2018. Early warning system in business, finance, and

economics: Bibliometric and topic analysis. International Journal of Engineering

Business Management, 10, p.1847979018797013.

Mian, A. and Sufi, A., 2018. Finance and business cycles: the credit-driven household demand

channel. Journal of Economic Perspectives, 32(3), pp.31-58.

Young, C., 2018. Can women win on the obstacle course of business finance?.

Tenca, F., Croce, A. and Ughetto, E., 2018. Business angels research in entrepreneurial finance:

A literature review and a research agenda. Journal of Economic Surveys, 32(5), pp.1384-

1413.

Sauer, R.M. and Wiesemeyer, K.H., 2018. Entrepreneurship and gender: differential access to

finance and divergent business value. Oxford Review of Economic Policy, 34(4), pp.584-

596.

Ahlström, H., 2019. Policy Hotspots for Sustainability: Changes in the EU Regulation of

Sustainable Business and Finance. Sustainability, 11(2), p.499.

La Torre, M., Trotta, A., Chiappini, H. and Rizzello, A., 2019. Business models for sustainable

finance: The case study of social impact bonds. Sustainability, 11(7), p.1887.

Boschmans, K. and Pissareva, L., 2018. Fostering Markets for SME Finance: Matching Business

and Investor Needs.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.