Business Finance 1: Project Evaluation, Stock Valuation, Portfolio

VerifiedAdded on 2023/06/03

|7

|989

|382

Homework Assignment

AI Summary

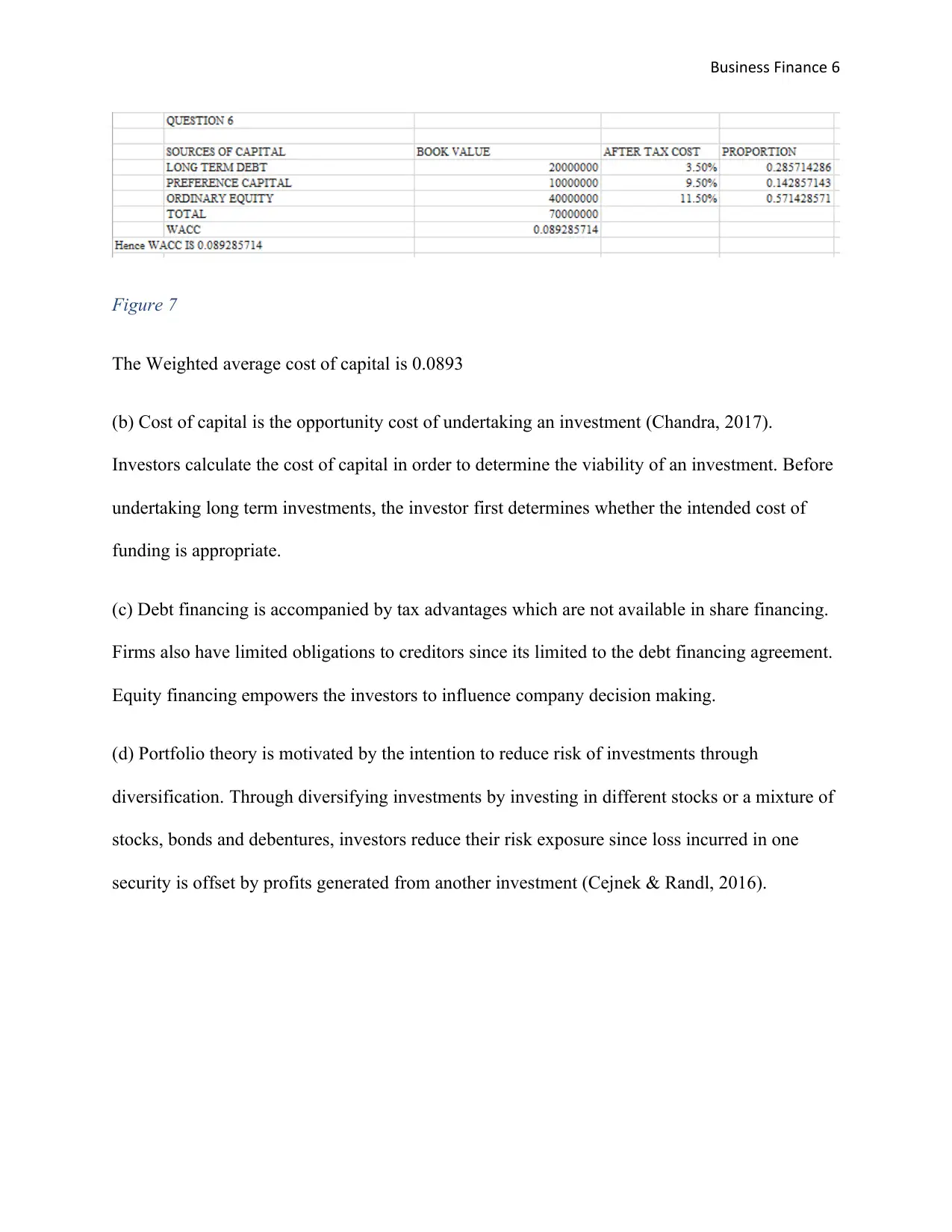

This assignment delves into various aspects of business finance, starting with a comparative analysis of project investment decisions using methods such as payback period, net present value (NPV), internal rate of return (IRR), and profitability index, ultimately favoring NPV for its comprehensive consideration of time value of money. It further explores stock valuation, demonstrating the inverse relationship between required return and share price, and discusses investor motivations for purchasing non-dividend paying stocks. The assignment also covers portfolio theory, emphasizing risk reduction through diversification, and calculates expected portfolio return and standard deviation. Finally, it addresses bond valuation, weighted average cost of capital (WACC), and the advantages and disadvantages of debt versus equity financing, highlighting the tax benefits of debt and the control implications of equity.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.