ACCT1001 - Financial Planning: Budgeting, Investment Decisions

VerifiedAdded on 2023/06/07

|9

|1949

|169

Homework Assignment

AI Summary

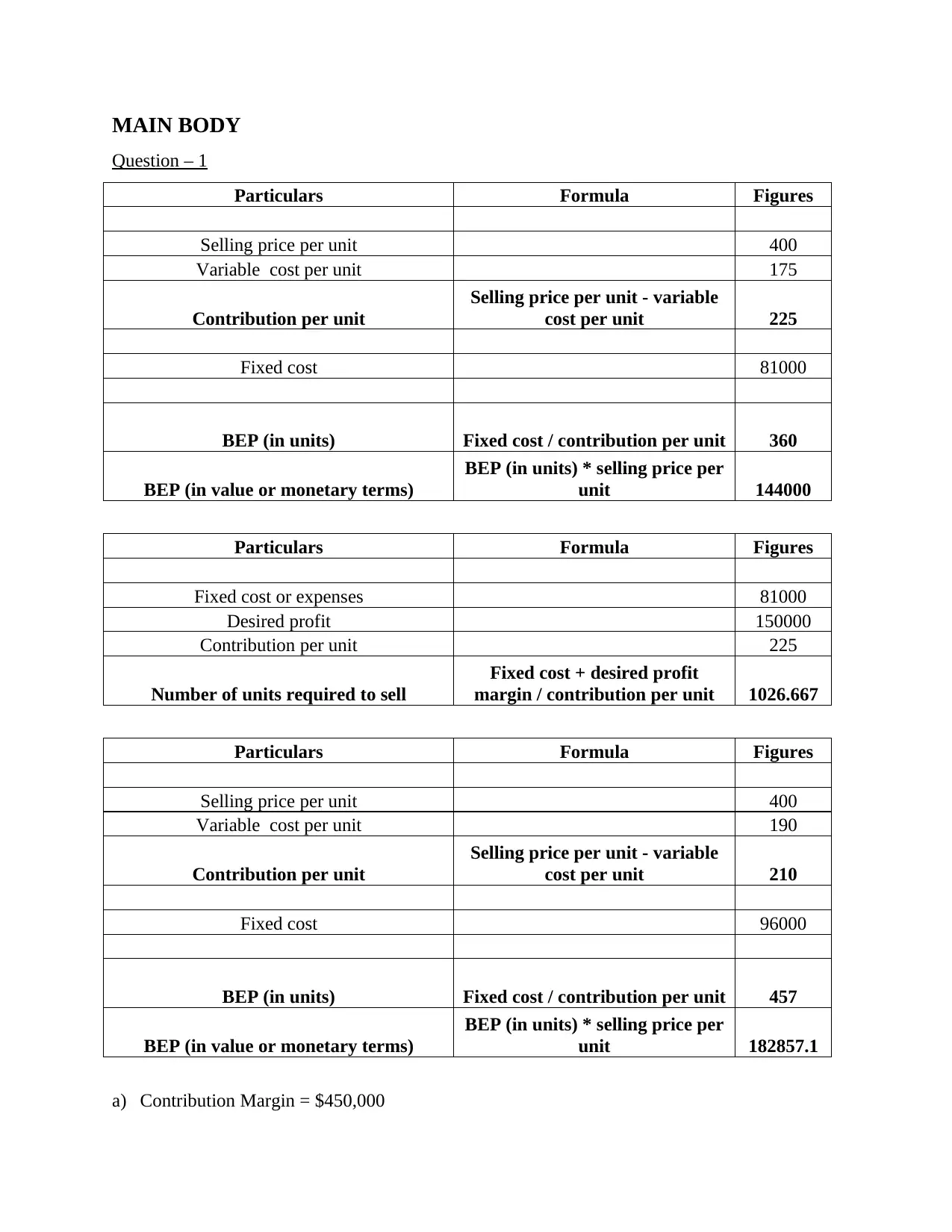

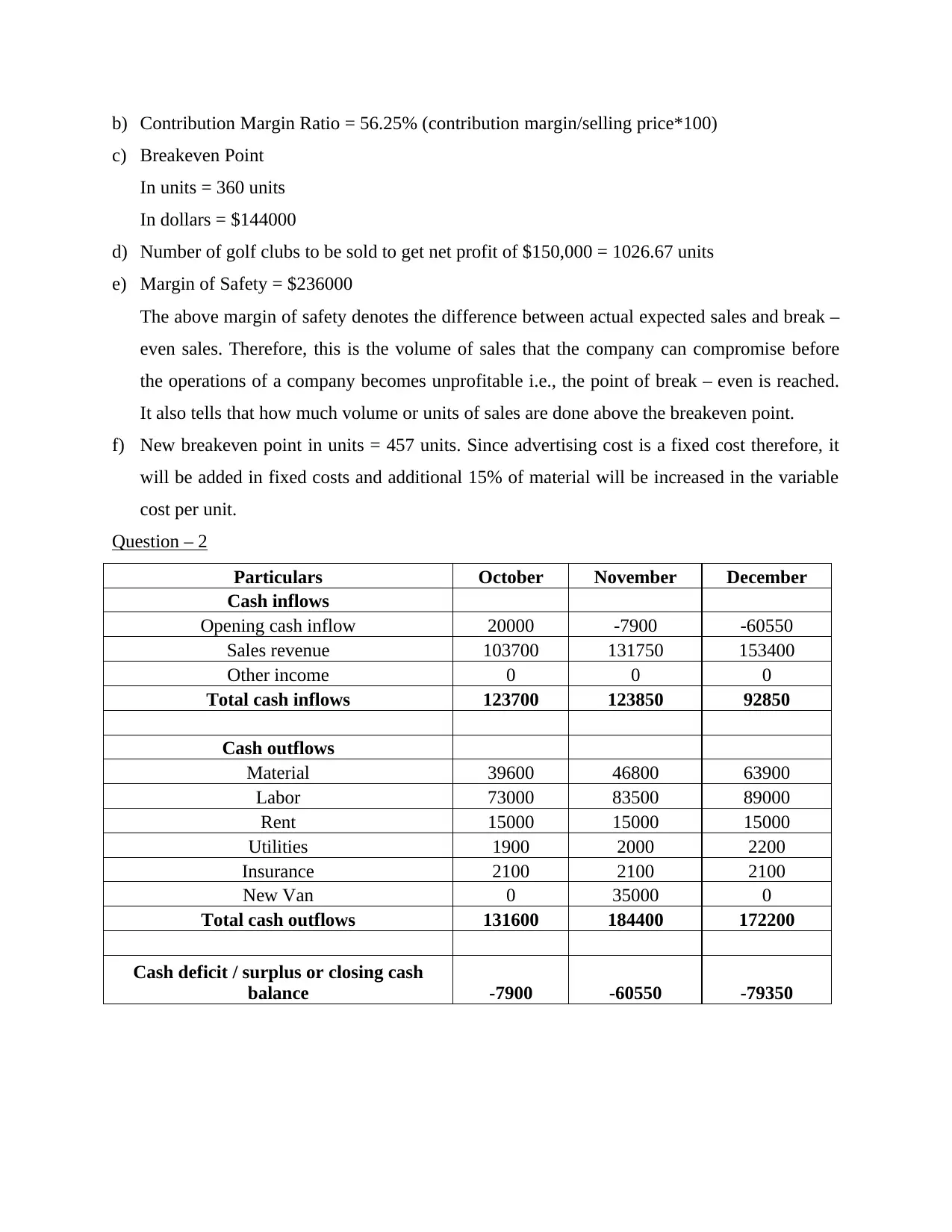

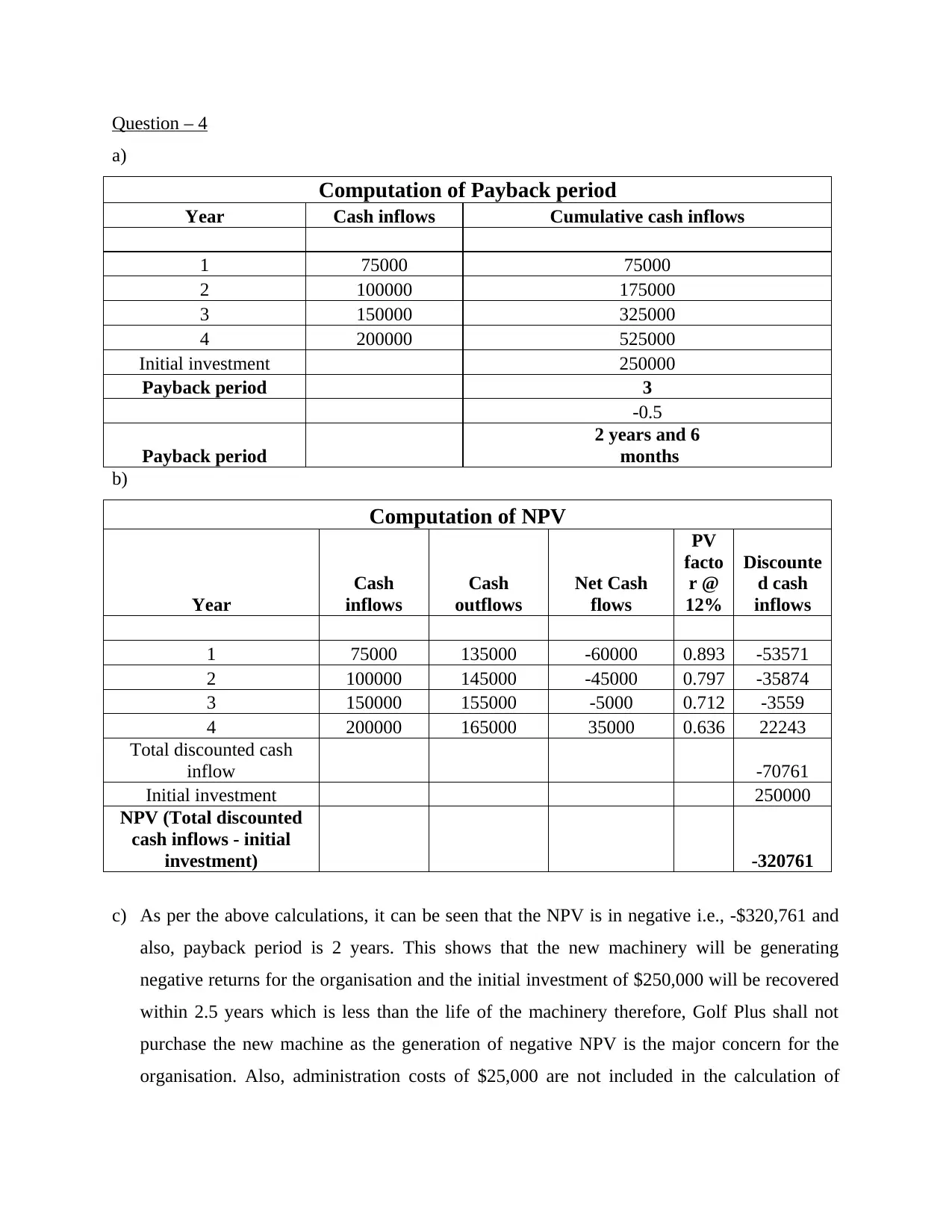

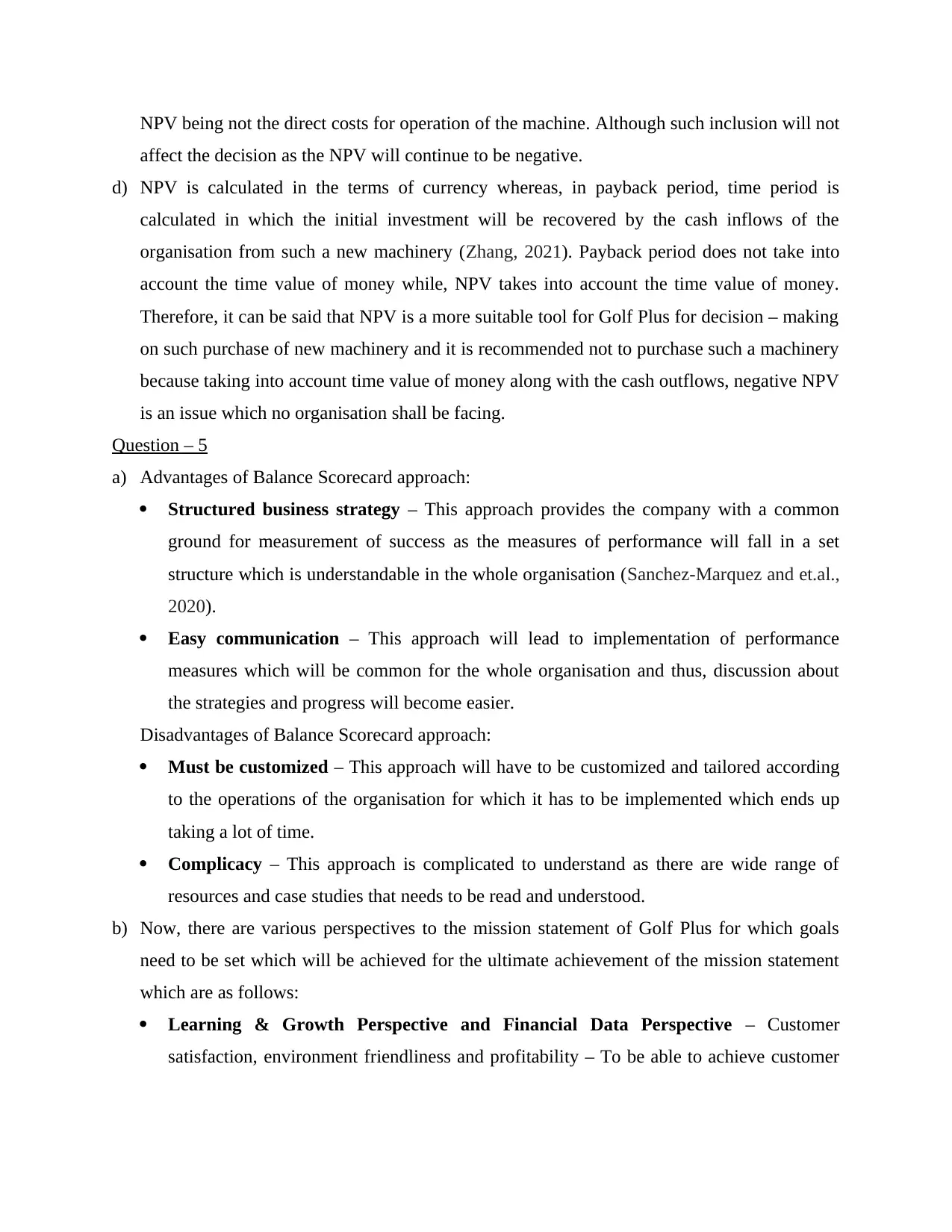

This assignment solution for ACCT1001 covers several key areas of business finance. It begins with break-even point (BEP) calculations, including determining BEP in units and monetary terms, and the number of units required to achieve a desired profit. The solution then presents a cash budget, analyzing cash inflows and outflows for October, November, and December, highlighting potential cash deficits and areas for improvement such as the proportion of cash versus credit sales and the efficiency of receivable recovery. The document also explores investment appraisal using payback period and Net Present Value (NPV) methods to evaluate the purchase of new machinery, concluding with a recommendation against the purchase based on the negative NPV. Finally, it discusses the advantages and disadvantages of the Balanced Scorecard approach, outlining perspectives, goals, and measures relevant to a company's mission statement. Desklib offers more solved assignments for students.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.