SSHA Project Investment Analysis - ACC211 Finance, Booli Electronics

VerifiedAdded on 2023/06/12

|11

|2298

|123

Report

AI Summary

This report provides a comprehensive financial analysis of Booli Electronics' proposed investment in a new 'smart speaker and home assistant' (SSHA) model. It includes calculations of the non-discounted payback period (2.14 years), profitability index (1.65), internal rate of return (19.77%), and net present value ($30,548,881.43). Sensitivity analyses are conducted to assess the impact of price and quantity changes on the NPV, revealing that NPV is highly sensitive to price changes and moderately sensitive to quantity changes. The report concludes that Booli Enterprise should accept the project due to the positive NPV, favorable profitability index and reasonable payback period and IRR. It recommends considering potential losses from other products when evaluating the investment to ensure the project's overall viability.

Running head: BUSINESS FINANCE

Business finance

Name of the student

Name of the university

Student ID

Author note

Business finance

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1BUSINESS FINANCE

Table of Contents

Introduction................................................................................................................................2

1. Non-discounted payback period.........................................................................................2

2. Profitability index...............................................................................................................3

3. Internal rate of return..........................................................................................................3

4. Net present value................................................................................................................3

5. Sensitivity analysis for price change..................................................................................4

6. Sensitivity analysis for price change..................................................................................6

7. Conclusion..........................................................................................................................8

8. Recommendation................................................................................................................8

Reference....................................................................................................................................9

Table of Contents

Introduction................................................................................................................................2

1. Non-discounted payback period.........................................................................................2

2. Profitability index...............................................................................................................3

3. Internal rate of return..........................................................................................................3

4. Net present value................................................................................................................3

5. Sensitivity analysis for price change..................................................................................4

6. Sensitivity analysis for price change..................................................................................6

7. Conclusion..........................................................................................................................8

8. Recommendation................................................................................................................8

Reference....................................................................................................................................9

2BUSINESS FINANCE

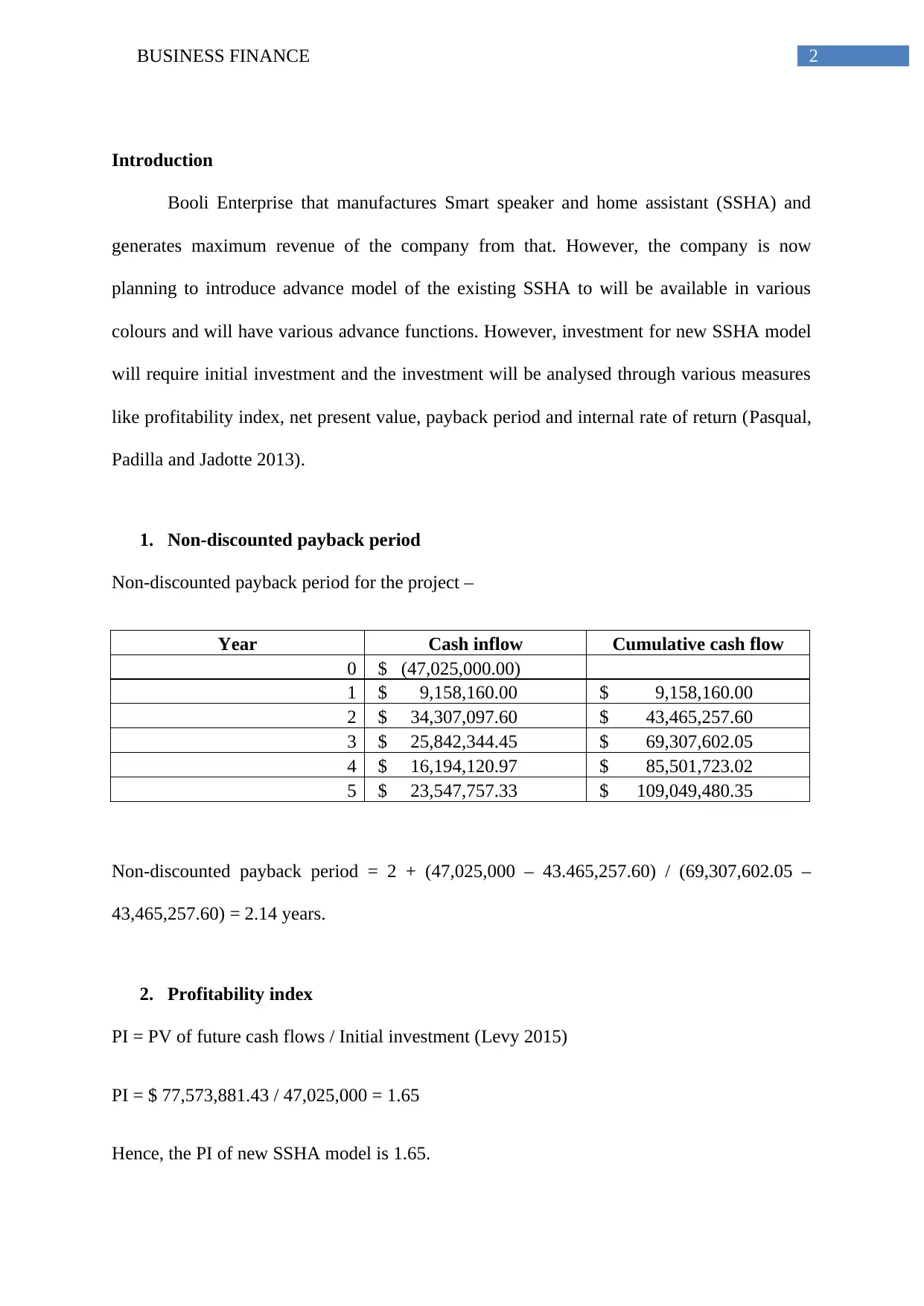

Introduction

Booli Enterprise that manufactures Smart speaker and home assistant (SSHA) and

generates maximum revenue of the company from that. However, the company is now

planning to introduce advance model of the existing SSHA to will be available in various

colours and will have various advance functions. However, investment for new SSHA model

will require initial investment and the investment will be analysed through various measures

like profitability index, net present value, payback period and internal rate of return (Pasqual,

Padilla and Jadotte 2013).

1. Non-discounted payback period

Non-discounted payback period for the project –

Year Cash inflow Cumulative cash flow

0 $ (47,025,000.00)

1 $ 9,158,160.00 $ 9,158,160.00

2 $ 34,307,097.60 $ 43,465,257.60

3 $ 25,842,344.45 $ 69,307,602.05

4 $ 16,194,120.97 $ 85,501,723.02

5 $ 23,547,757.33 $ 109,049,480.35

Non-discounted payback period = 2 + (47,025,000 – 43.465,257.60) / (69,307,602.05 –

43,465,257.60) = 2.14 years.

2. Profitability index

PI = PV of future cash flows / Initial investment (Levy 2015)

PI = $ 77,573,881.43 / 47,025,000 = 1.65

Hence, the PI of new SSHA model is 1.65.

Introduction

Booli Enterprise that manufactures Smart speaker and home assistant (SSHA) and

generates maximum revenue of the company from that. However, the company is now

planning to introduce advance model of the existing SSHA to will be available in various

colours and will have various advance functions. However, investment for new SSHA model

will require initial investment and the investment will be analysed through various measures

like profitability index, net present value, payback period and internal rate of return (Pasqual,

Padilla and Jadotte 2013).

1. Non-discounted payback period

Non-discounted payback period for the project –

Year Cash inflow Cumulative cash flow

0 $ (47,025,000.00)

1 $ 9,158,160.00 $ 9,158,160.00

2 $ 34,307,097.60 $ 43,465,257.60

3 $ 25,842,344.45 $ 69,307,602.05

4 $ 16,194,120.97 $ 85,501,723.02

5 $ 23,547,757.33 $ 109,049,480.35

Non-discounted payback period = 2 + (47,025,000 – 43.465,257.60) / (69,307,602.05 –

43,465,257.60) = 2.14 years.

2. Profitability index

PI = PV of future cash flows / Initial investment (Levy 2015)

PI = $ 77,573,881.43 / 47,025,000 = 1.65

Hence, the PI of new SSHA model is 1.65.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3BUSINESS FINANCE

3. Internal rate of return

Internal rate of return is the rate at which the present value of cash inflows will be

equal to cash outflows. The IRR of the project is 19.77% (Leyman and Vanhoucke 2016)

4. Net present value

Net present value is the difference between the present value of cash inflows and cash

outflows. The NPV of the project is $ 30,548,881.43 (Yuniningsih, Widodo and Wajdi 2017).

5. Sensitivity analysis for price change

Sensitivity analysis is conducted for the purpose of ascertaining the changes which

takes places on the dependent variable for significant changes in the independent variables

which are to be considered (Akbarzadehet al. 2016). The analysis is generally conducted

considering that the dependent variable is one and the independent variable is also one.

Sensitivity analysis is conducted so as to ensure that the business is able to understand how

much changes are brought forward when a small change in independent variables occur.

Certain examples of independent variables which can be given are sales prices, cost of capital

of the business (Nguyen and Reiter 2015). The dependent variables depend on the nature of

the business and the choice of the business as to what factor the business wants to consider

for the overall sensitivity analysis (Sanchezet al. 2013). The various steps which are required

to be carried out in case of sensitivity analysis is given below in details:

The first step in the sensitivity analysis is the identification of the inputs and outputs

which are related to the business. As per the question which is provided the input is

the selling price and the output is NPV which is calculated. The impact on the NPV

will be will be measured with the small changes in the price of the business. The other

3. Internal rate of return

Internal rate of return is the rate at which the present value of cash inflows will be

equal to cash outflows. The IRR of the project is 19.77% (Leyman and Vanhoucke 2016)

4. Net present value

Net present value is the difference between the present value of cash inflows and cash

outflows. The NPV of the project is $ 30,548,881.43 (Yuniningsih, Widodo and Wajdi 2017).

5. Sensitivity analysis for price change

Sensitivity analysis is conducted for the purpose of ascertaining the changes which

takes places on the dependent variable for significant changes in the independent variables

which are to be considered (Akbarzadehet al. 2016). The analysis is generally conducted

considering that the dependent variable is one and the independent variable is also one.

Sensitivity analysis is conducted so as to ensure that the business is able to understand how

much changes are brought forward when a small change in independent variables occur.

Certain examples of independent variables which can be given are sales prices, cost of capital

of the business (Nguyen and Reiter 2015). The dependent variables depend on the nature of

the business and the choice of the business as to what factor the business wants to consider

for the overall sensitivity analysis (Sanchezet al. 2013). The various steps which are required

to be carried out in case of sensitivity analysis is given below in details:

The first step in the sensitivity analysis is the identification of the inputs and outputs

which are related to the business. As per the question which is provided the input is

the selling price and the output is NPV which is calculated. The impact on the NPV

will be will be measured with the small changes in the price of the business. The other

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4BUSINESS FINANCE

factors which are involved with the investment are factors like selling quantity, initial

investments and discount rate are considered to be constant in such a case.

The second step will be to consider the percentage change in NPV which is caused

due to percentage change in the selling price (Baucells and Borgonovo 2013).

After the above two process, the sensitivity will be measured for the changes in the

NPV due to changes in the selling price of the product.

After the above steps, the management takes necessary decisions based on the

sensitivity data and graph as plotted using such a data.

Price NPV Changes (Price) Changes (NPV)

$ -

500 $ (15,635,004.70)

530 $ (8,225,825.11) 30 $ 7,409,179.59

560 $ (816,645.51) 30 $ 7,409,179.59

590 $ 6,592,534.08 30 $ 7,409,179.59

620 $ 14,001,713.67 30 $ 7,409,179.59

650 $ 21,410,893.27 30 $ 7,409,179.59

680 $ 28,820,072.86 30 $ 7,409,179.59

710 $ 36,229,252.46 30 $ 7,409,179.59

740 $ 43,638,432.05 30 $ 7,409,179.59

770 $ 51,047,611.64 30 $ 7,409,179.59

800 $ 58,456,791.24 30 $ 7,409,179.59

830 $ 65,865,970.83 30 $ 7,409,179.59

860 $ 73,275,150.43 30 $ 7,409,179.59

890 $ 80,684,330.02 30 $ 7,409,179.59

920 $ 88,093,509.61 30 $ 7,409,179.59

950 $ 95,502,689.21 30 $ 7,409,179.59

980 $ 102,911,868.80 30 $ 7,409,179.59

1010 $ 110,321,048.40 30 $ 7,409,179.59

1040 $ 117,730,227.99 30 $ 7,409,179.59

1070 $ 125,139,407.58 30 $ 7,409,179.59

1100 $ 132,548,587.18 30 $ 7,409,179.59

1130 $ 139,957,766.77 30 $ 7,409,179.59

1160 $ 147,366,946.37 30 $ 7,409,179.59

1190 $ 154,776,125.96 30 $ 7,409,179.59

1220 $ 162,185,305.55 30 $ 7,409,179.59

1250 $ 169,594,485.15 30 $ 7,409,179.59

1280 $ 177,003,664.74 30 $ 7,409,179.59

1310 $ 184,412,844.33 30 $ 7,409,179.59

factors which are involved with the investment are factors like selling quantity, initial

investments and discount rate are considered to be constant in such a case.

The second step will be to consider the percentage change in NPV which is caused

due to percentage change in the selling price (Baucells and Borgonovo 2013).

After the above two process, the sensitivity will be measured for the changes in the

NPV due to changes in the selling price of the product.

After the above steps, the management takes necessary decisions based on the

sensitivity data and graph as plotted using such a data.

Price NPV Changes (Price) Changes (NPV)

$ -

500 $ (15,635,004.70)

530 $ (8,225,825.11) 30 $ 7,409,179.59

560 $ (816,645.51) 30 $ 7,409,179.59

590 $ 6,592,534.08 30 $ 7,409,179.59

620 $ 14,001,713.67 30 $ 7,409,179.59

650 $ 21,410,893.27 30 $ 7,409,179.59

680 $ 28,820,072.86 30 $ 7,409,179.59

710 $ 36,229,252.46 30 $ 7,409,179.59

740 $ 43,638,432.05 30 $ 7,409,179.59

770 $ 51,047,611.64 30 $ 7,409,179.59

800 $ 58,456,791.24 30 $ 7,409,179.59

830 $ 65,865,970.83 30 $ 7,409,179.59

860 $ 73,275,150.43 30 $ 7,409,179.59

890 $ 80,684,330.02 30 $ 7,409,179.59

920 $ 88,093,509.61 30 $ 7,409,179.59

950 $ 95,502,689.21 30 $ 7,409,179.59

980 $ 102,911,868.80 30 $ 7,409,179.59

1010 $ 110,321,048.40 30 $ 7,409,179.59

1040 $ 117,730,227.99 30 $ 7,409,179.59

1070 $ 125,139,407.58 30 $ 7,409,179.59

1100 $ 132,548,587.18 30 $ 7,409,179.59

1130 $ 139,957,766.77 30 $ 7,409,179.59

1160 $ 147,366,946.37 30 $ 7,409,179.59

1190 $ 154,776,125.96 30 $ 7,409,179.59

1220 $ 162,185,305.55 30 $ 7,409,179.59

1250 $ 169,594,485.15 30 $ 7,409,179.59

1280 $ 177,003,664.74 30 $ 7,409,179.59

1310 $ 184,412,844.33 30 $ 7,409,179.59

5BUSINESS FINANCE

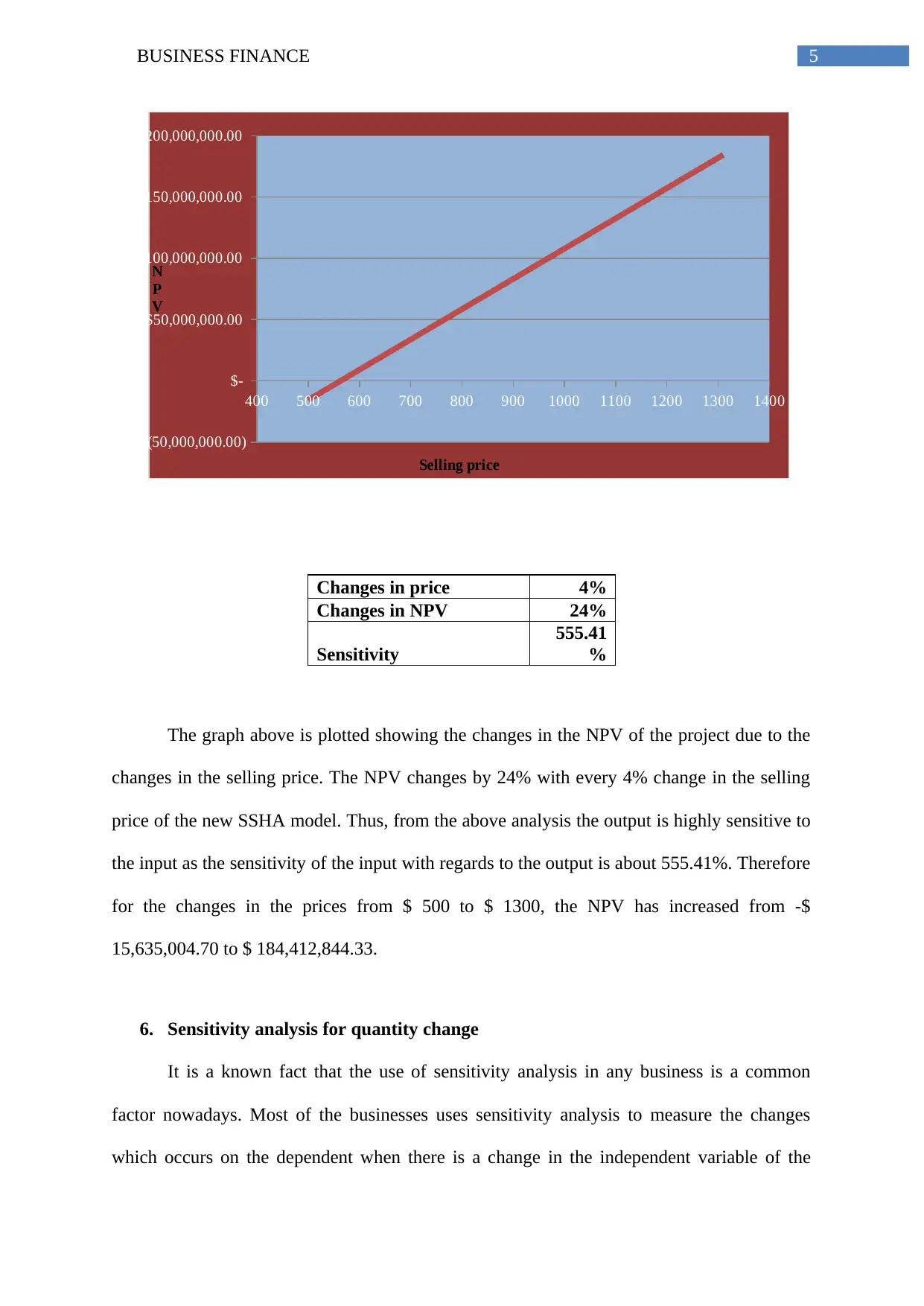

400 500 600 700 800 900 1000 1100 1200 1300 1400

$(50,000,000.00)

$-

$50,000,000.00

$100,000,000.00

$150,000,000.00

$200,000,000.00

Selling price

N

P

V

Changes in price 4%

Changes in NPV 24%

Sensitivity

555.41

%

The graph above is plotted showing the changes in the NPV of the project due to the

changes in the selling price. The NPV changes by 24% with every 4% change in the selling

price of the new SSHA model. Thus, from the above analysis the output is highly sensitive to

the input as the sensitivity of the input with regards to the output is about 555.41%. Therefore

for the changes in the prices from $ 500 to $ 1300, the NPV has increased from -$

15,635,004.70 to $ 184,412,844.33.

6. Sensitivity analysis for quantity change

It is a known fact that the use of sensitivity analysis in any business is a common

factor nowadays. Most of the businesses uses sensitivity analysis to measure the changes

which occurs on the dependent when there is a change in the independent variable of the

400 500 600 700 800 900 1000 1100 1200 1300 1400

$(50,000,000.00)

$-

$50,000,000.00

$100,000,000.00

$150,000,000.00

$200,000,000.00

Selling price

N

P

V

Changes in price 4%

Changes in NPV 24%

Sensitivity

555.41

%

The graph above is plotted showing the changes in the NPV of the project due to the

changes in the selling price. The NPV changes by 24% with every 4% change in the selling

price of the new SSHA model. Thus, from the above analysis the output is highly sensitive to

the input as the sensitivity of the input with regards to the output is about 555.41%. Therefore

for the changes in the prices from $ 500 to $ 1300, the NPV has increased from -$

15,635,004.70 to $ 184,412,844.33.

6. Sensitivity analysis for quantity change

It is a known fact that the use of sensitivity analysis in any business is a common

factor nowadays. Most of the businesses uses sensitivity analysis to measure the changes

which occurs on the dependent when there is a change in the independent variable of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6BUSINESS FINANCE

business (Tian 2013). The method is useful for establishing a relationship between the

independent and dependent variable which the business is considering. Such dependent and

independent variable can be anything such as NPV and selling price of the product. The

various steps which can be suggested for the purpose of conducting sensitivity analysis are

given below in point form:

In this case the input which is chosen by the business is the selling quantity and the

output that is to be considered is NPV. The changes in the NPV will be measured in

terms of the changes in the selling quantity of the product. The other factors which are

related to the project which can affect the analysis such as discount rate, initial

investments and selling price of the product are considered to be constant.

The percentage change in the NPV will be measured with respect to the percentage

change in the selling quantity of the product (Cucchiella, D’Adamo and Gastaldi

2015).

The NPV of the investment is to be then measured with the selling quantity and the

same is to be analyzed as well keeping in the that other factors remain constant

(Wang, Xia and Zhang 2014).

Then it is to be ascertained how the analysis of sensitivity of the project will be

affecting the business decision making process.

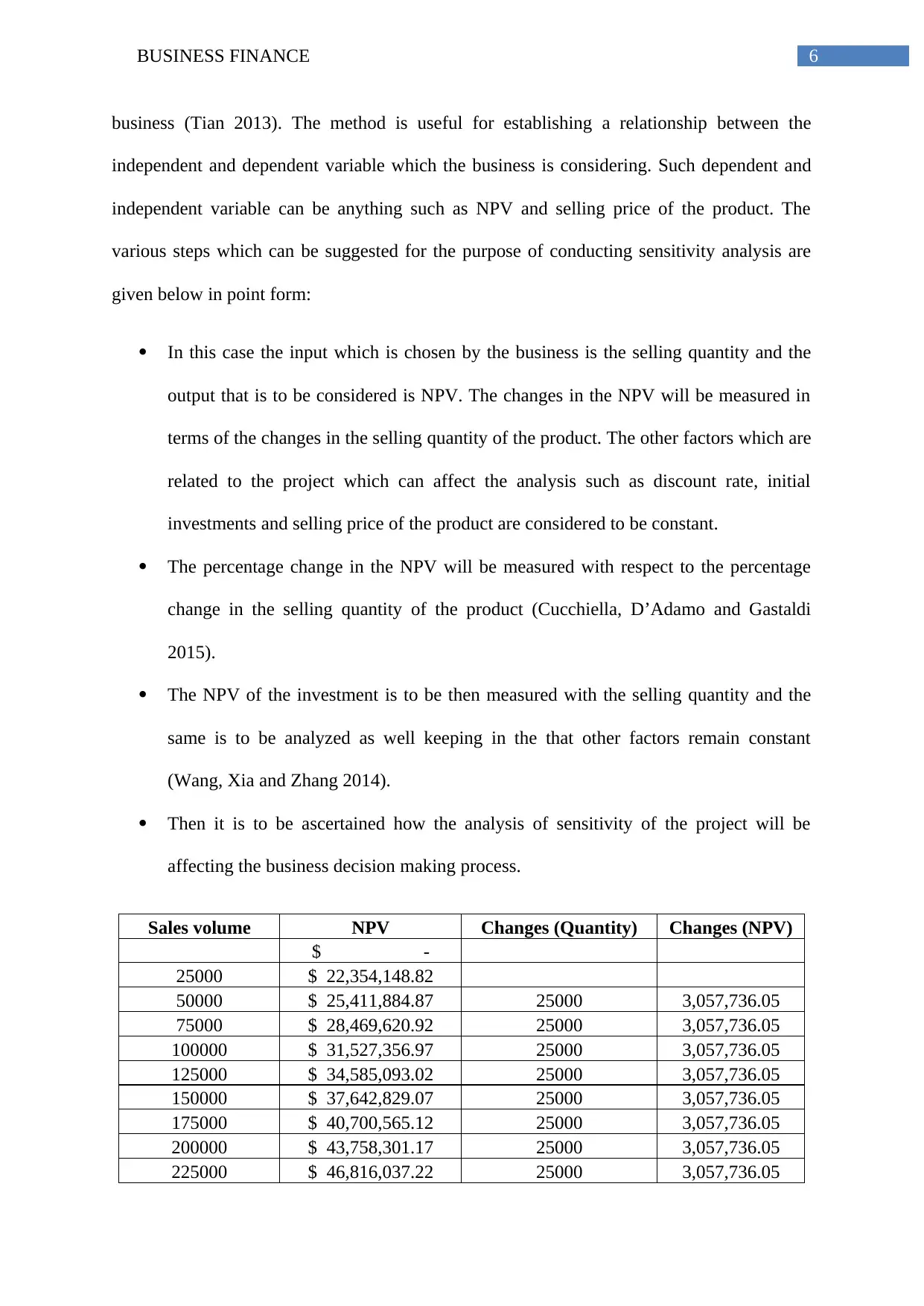

Sales volume NPV Changes (Quantity) Changes (NPV)

$ -

25000 $ 22,354,148.82

50000 $ 25,411,884.87 25000 3,057,736.05

75000 $ 28,469,620.92 25000 3,057,736.05

100000 $ 31,527,356.97 25000 3,057,736.05

125000 $ 34,585,093.02 25000 3,057,736.05

150000 $ 37,642,829.07 25000 3,057,736.05

175000 $ 40,700,565.12 25000 3,057,736.05

200000 $ 43,758,301.17 25000 3,057,736.05

225000 $ 46,816,037.22 25000 3,057,736.05

business (Tian 2013). The method is useful for establishing a relationship between the

independent and dependent variable which the business is considering. Such dependent and

independent variable can be anything such as NPV and selling price of the product. The

various steps which can be suggested for the purpose of conducting sensitivity analysis are

given below in point form:

In this case the input which is chosen by the business is the selling quantity and the

output that is to be considered is NPV. The changes in the NPV will be measured in

terms of the changes in the selling quantity of the product. The other factors which are

related to the project which can affect the analysis such as discount rate, initial

investments and selling price of the product are considered to be constant.

The percentage change in the NPV will be measured with respect to the percentage

change in the selling quantity of the product (Cucchiella, D’Adamo and Gastaldi

2015).

The NPV of the investment is to be then measured with the selling quantity and the

same is to be analyzed as well keeping in the that other factors remain constant

(Wang, Xia and Zhang 2014).

Then it is to be ascertained how the analysis of sensitivity of the project will be

affecting the business decision making process.

Sales volume NPV Changes (Quantity) Changes (NPV)

$ -

25000 $ 22,354,148.82

50000 $ 25,411,884.87 25000 3,057,736.05

75000 $ 28,469,620.92 25000 3,057,736.05

100000 $ 31,527,356.97 25000 3,057,736.05

125000 $ 34,585,093.02 25000 3,057,736.05

150000 $ 37,642,829.07 25000 3,057,736.05

175000 $ 40,700,565.12 25000 3,057,736.05

200000 $ 43,758,301.17 25000 3,057,736.05

225000 $ 46,816,037.22 25000 3,057,736.05

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7BUSINESS FINANCE

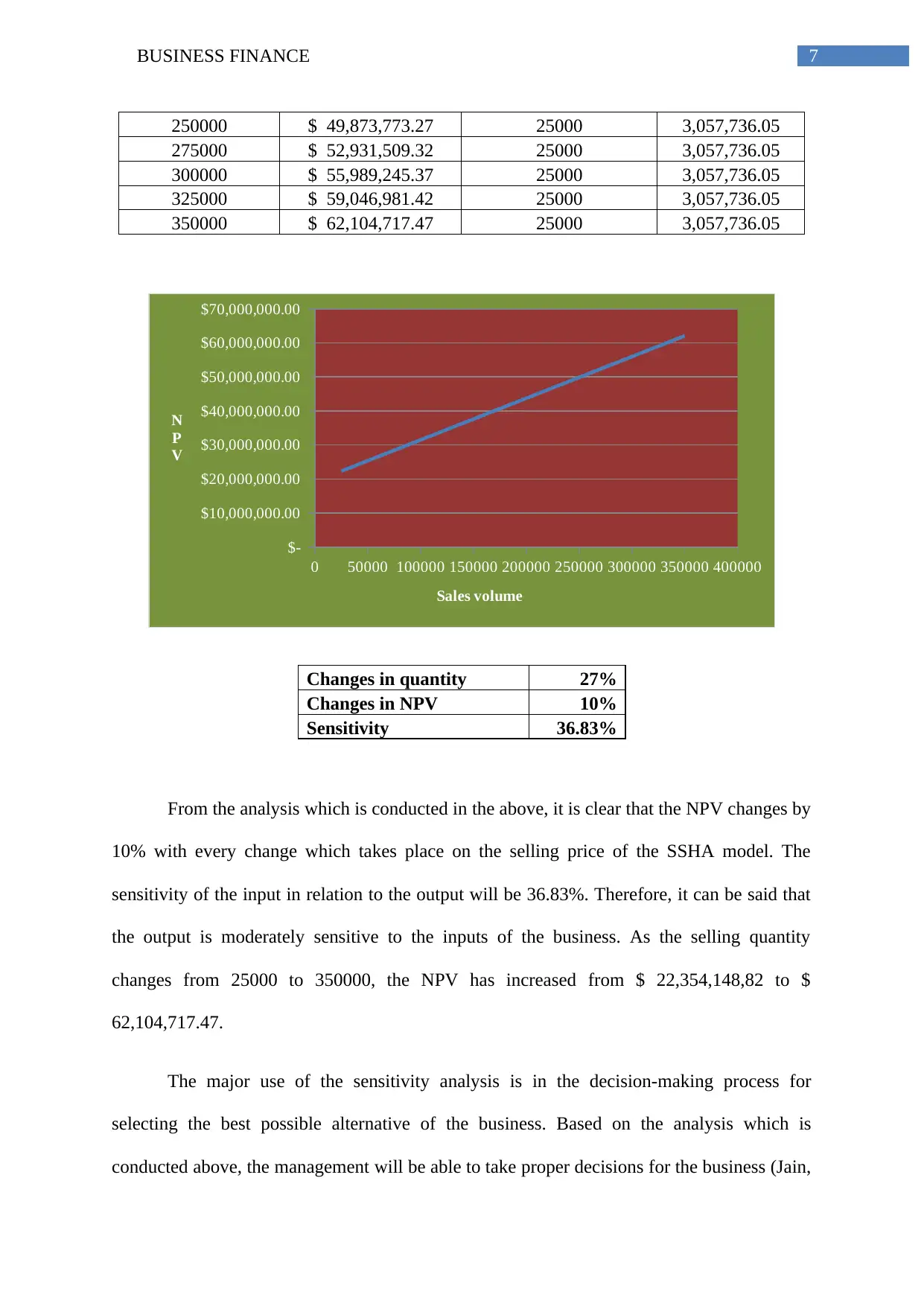

250000 $ 49,873,773.27 25000 3,057,736.05

275000 $ 52,931,509.32 25000 3,057,736.05

300000 $ 55,989,245.37 25000 3,057,736.05

325000 $ 59,046,981.42 25000 3,057,736.05

350000 $ 62,104,717.47 25000 3,057,736.05

0 50000 100000 150000 200000 250000 300000 350000 400000

$-

$10,000,000.00

$20,000,000.00

$30,000,000.00

$40,000,000.00

$50,000,000.00

$60,000,000.00

$70,000,000.00

Sales volume

N

P

V

Changes in quantity 27%

Changes in NPV 10%

Sensitivity 36.83%

From the analysis which is conducted in the above, it is clear that the NPV changes by

10% with every change which takes place on the selling price of the SSHA model. The

sensitivity of the input in relation to the output will be 36.83%. Therefore, it can be said that

the output is moderately sensitive to the inputs of the business. As the selling quantity

changes from 25000 to 350000, the NPV has increased from $ 22,354,148,82 to $

62,104,717.47.

The major use of the sensitivity analysis is in the decision-making process for

selecting the best possible alternative of the business. Based on the analysis which is

conducted above, the management will be able to take proper decisions for the business (Jain,

250000 $ 49,873,773.27 25000 3,057,736.05

275000 $ 52,931,509.32 25000 3,057,736.05

300000 $ 55,989,245.37 25000 3,057,736.05

325000 $ 59,046,981.42 25000 3,057,736.05

350000 $ 62,104,717.47 25000 3,057,736.05

0 50000 100000 150000 200000 250000 300000 350000 400000

$-

$10,000,000.00

$20,000,000.00

$30,000,000.00

$40,000,000.00

$50,000,000.00

$60,000,000.00

$70,000,000.00

Sales volume

N

P

V

Changes in quantity 27%

Changes in NPV 10%

Sensitivity 36.83%

From the analysis which is conducted in the above, it is clear that the NPV changes by

10% with every change which takes place on the selling price of the SSHA model. The

sensitivity of the input in relation to the output will be 36.83%. Therefore, it can be said that

the output is moderately sensitive to the inputs of the business. As the selling quantity

changes from 25000 to 350000, the NPV has increased from $ 22,354,148,82 to $

62,104,717.47.

The major use of the sensitivity analysis is in the decision-making process for

selecting the best possible alternative of the business. Based on the analysis which is

conducted above, the management will be able to take proper decisions for the business (Jain,

8BUSINESS FINANCE

Singh and Srivastava 2013). Sensitivity analysis considers all the factors to remain constant;

however in some cases this becomes irrelevant.

7. Conclusion

Thus, from the above analysis, it can be concluded that Booli Enterprise should invest

in the project or in other words should accept the project. Booli enterprise shall be

manufacturing new model for SSHA. The main reasons due to which the management

accepted the project are because the NPV for the project as calculated is positive, the

profitability index of the same is shown to be 1.65, payback period is calculated to 2.14

which is less than 5 years and hence favourable. The IRR of the project is shown to be 19.7%

that is appropriate.

8. Recommendation

As per the above analysis, it is suggested that the business shall accept the project. If

the manufacturing of the new product for existing SSHA as per the plan of the management

generates losses for any other product of the business then the same loss shall be included in

the amount of investment. If after inclusion of such loss from other product in the

investments results in negative NPV than the project should not be accepted. However, if the

result is shown to be positive then the project should be accepted.

Singh and Srivastava 2013). Sensitivity analysis considers all the factors to remain constant;

however in some cases this becomes irrelevant.

7. Conclusion

Thus, from the above analysis, it can be concluded that Booli Enterprise should invest

in the project or in other words should accept the project. Booli enterprise shall be

manufacturing new model for SSHA. The main reasons due to which the management

accepted the project are because the NPV for the project as calculated is positive, the

profitability index of the same is shown to be 1.65, payback period is calculated to 2.14

which is less than 5 years and hence favourable. The IRR of the project is shown to be 19.7%

that is appropriate.

8. Recommendation

As per the above analysis, it is suggested that the business shall accept the project. If

the manufacturing of the new product for existing SSHA as per the plan of the management

generates losses for any other product of the business then the same loss shall be included in

the amount of investment. If after inclusion of such loss from other product in the

investments results in negative NPV than the project should not be accepted. However, if the

result is shown to be positive then the project should be accepted.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9BUSINESS FINANCE

Reference

Akbarzadeh, M., Rashidi, S., Bovand, M. and Ellahi, R., 2016. A sensitivity analysis on

thermal and pumping power for the flow of nanofluid inside a wavy channel. Journal of

Molecular Liquids, 220, pp.1-13.

Baucells, M. and Borgonovo, E., 2013. Invariant probabilistic sensitivity

analysis. Management Science, 59(11), pp.2536-2549.

Cucchiella, F., D’Adamo, I. and Gastaldi, M., 2015. Financial analysis for investment and

policy decisions in the renewable energy sector. Clean Technologies and Environmental

Policy, 17(4), pp.887-904.

Jain, N., Singh, S.N. and Srivastava, S.C., 2013. A generalized approach for DG planning and

viability analysis under market scenario. IEEE Transactions on Industrial

Electronics, 60(11), pp.5075-5085.

Levy, H., 2015. Stochastic dominance: Investment decision making under uncertainty.

Springer.

Leyman, P. and Vanhoucke, M., 2016. Payment models and net present value optimization

for resource-constrained project scheduling. Computers & Industrial Engineering, 91,

pp.139-153.

Nguyen, A.T. and Reiter, S., 2015, December. A performance comparison of sensitivity

analysis methods for building energy models. In Building Simulation (Vol. 8, No. 6, pp. 651-

664). Tsinghua University Press.

Reference

Akbarzadeh, M., Rashidi, S., Bovand, M. and Ellahi, R., 2016. A sensitivity analysis on

thermal and pumping power for the flow of nanofluid inside a wavy channel. Journal of

Molecular Liquids, 220, pp.1-13.

Baucells, M. and Borgonovo, E., 2013. Invariant probabilistic sensitivity

analysis. Management Science, 59(11), pp.2536-2549.

Cucchiella, F., D’Adamo, I. and Gastaldi, M., 2015. Financial analysis for investment and

policy decisions in the renewable energy sector. Clean Technologies and Environmental

Policy, 17(4), pp.887-904.

Jain, N., Singh, S.N. and Srivastava, S.C., 2013. A generalized approach for DG planning and

viability analysis under market scenario. IEEE Transactions on Industrial

Electronics, 60(11), pp.5075-5085.

Levy, H., 2015. Stochastic dominance: Investment decision making under uncertainty.

Springer.

Leyman, P. and Vanhoucke, M., 2016. Payment models and net present value optimization

for resource-constrained project scheduling. Computers & Industrial Engineering, 91,

pp.139-153.

Nguyen, A.T. and Reiter, S., 2015, December. A performance comparison of sensitivity

analysis methods for building energy models. In Building Simulation (Vol. 8, No. 6, pp. 651-

664). Tsinghua University Press.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10BUSINESS FINANCE

Pasqual, J., Padilla, E. and Jadotte, E., 2013. Equivalence of different profitability criteria

with the net present value. International Journal of Production Economics, 142(1), pp.205-

210.

Sanchez, D.G., Lacarrière, B., Musy, M. and Bourges, B., 2014. Application of sensitivity

analysis in building energy simulations: Combining first-and second-order elementary effects

methods. Energy and Buildings, 68, pp.741-750.

Tian, W., 2013. A review of sensitivity analysis methods in building energy

analysis. Renewable and Sustainable Energy Reviews, 20, pp.411-419.

Wang, B., Xia, X. and Zhang, J., 2014. A multi-objective optimization model for the life-

cycle cost analysis and retrofitting planning of buildings. Energy and Buildings, 77, pp.227-

235.

Yuniningsih, Y., Widodo, S. and Wajdi, M.B.N., 2017. An analysis of Decision Making in

the Stock Investment. Economic: Journal of Economic and Islamic Law, 8(2), pp.122-128.

Pasqual, J., Padilla, E. and Jadotte, E., 2013. Equivalence of different profitability criteria

with the net present value. International Journal of Production Economics, 142(1), pp.205-

210.

Sanchez, D.G., Lacarrière, B., Musy, M. and Bourges, B., 2014. Application of sensitivity

analysis in building energy simulations: Combining first-and second-order elementary effects

methods. Energy and Buildings, 68, pp.741-750.

Tian, W., 2013. A review of sensitivity analysis methods in building energy

analysis. Renewable and Sustainable Energy Reviews, 20, pp.411-419.

Wang, B., Xia, X. and Zhang, J., 2014. A multi-objective optimization model for the life-

cycle cost analysis and retrofitting planning of buildings. Energy and Buildings, 77, pp.227-

235.

Yuniningsih, Y., Widodo, S. and Wajdi, M.B.N., 2017. An analysis of Decision Making in

the Stock Investment. Economic: Journal of Economic and Islamic Law, 8(2), pp.122-128.

1 out of 11