Business Finance: Analysis of Financial Viability and Ratios for Crusher PLC

VerifiedAdded on 2023/06/18

|15

|1257

|177

AI Summary

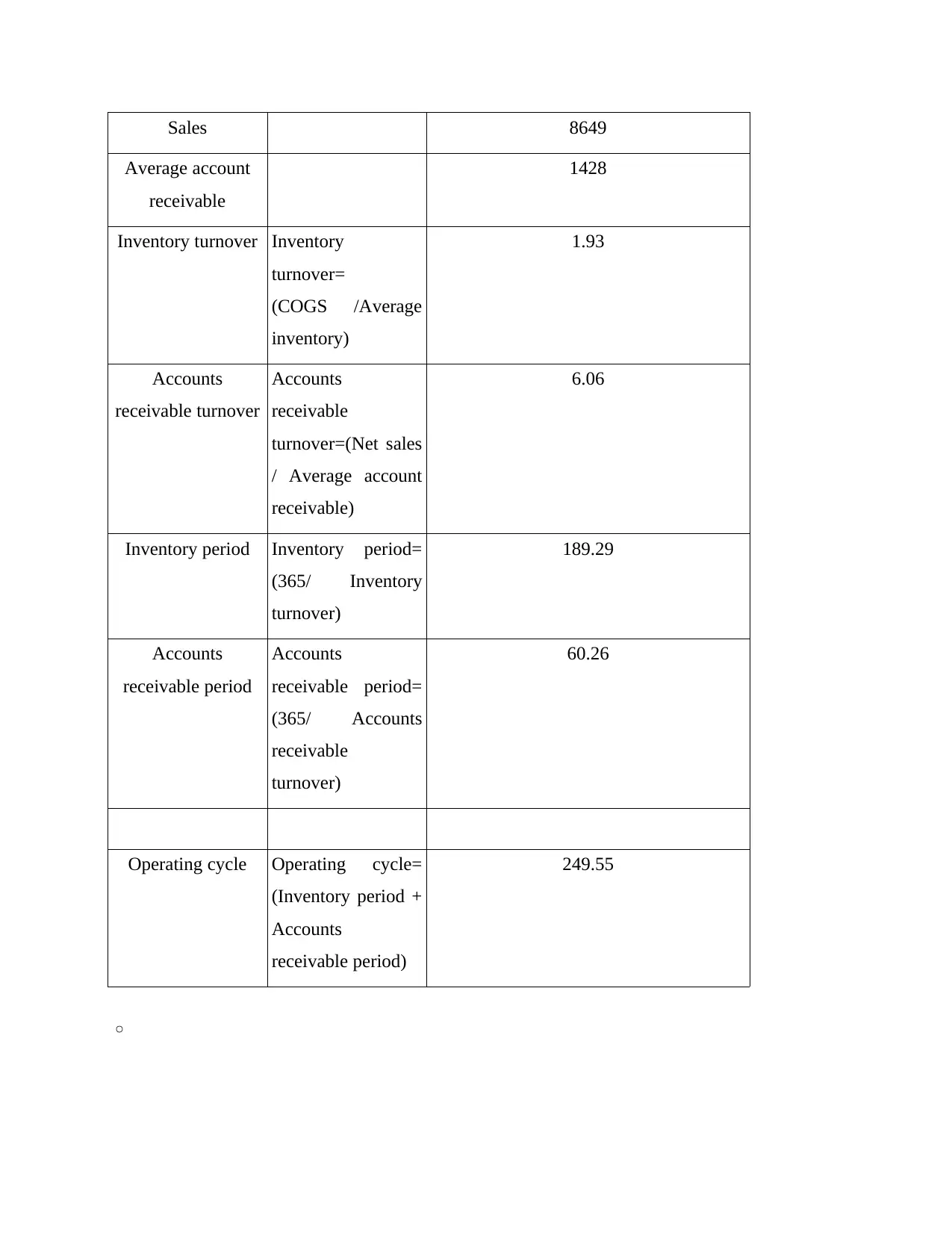

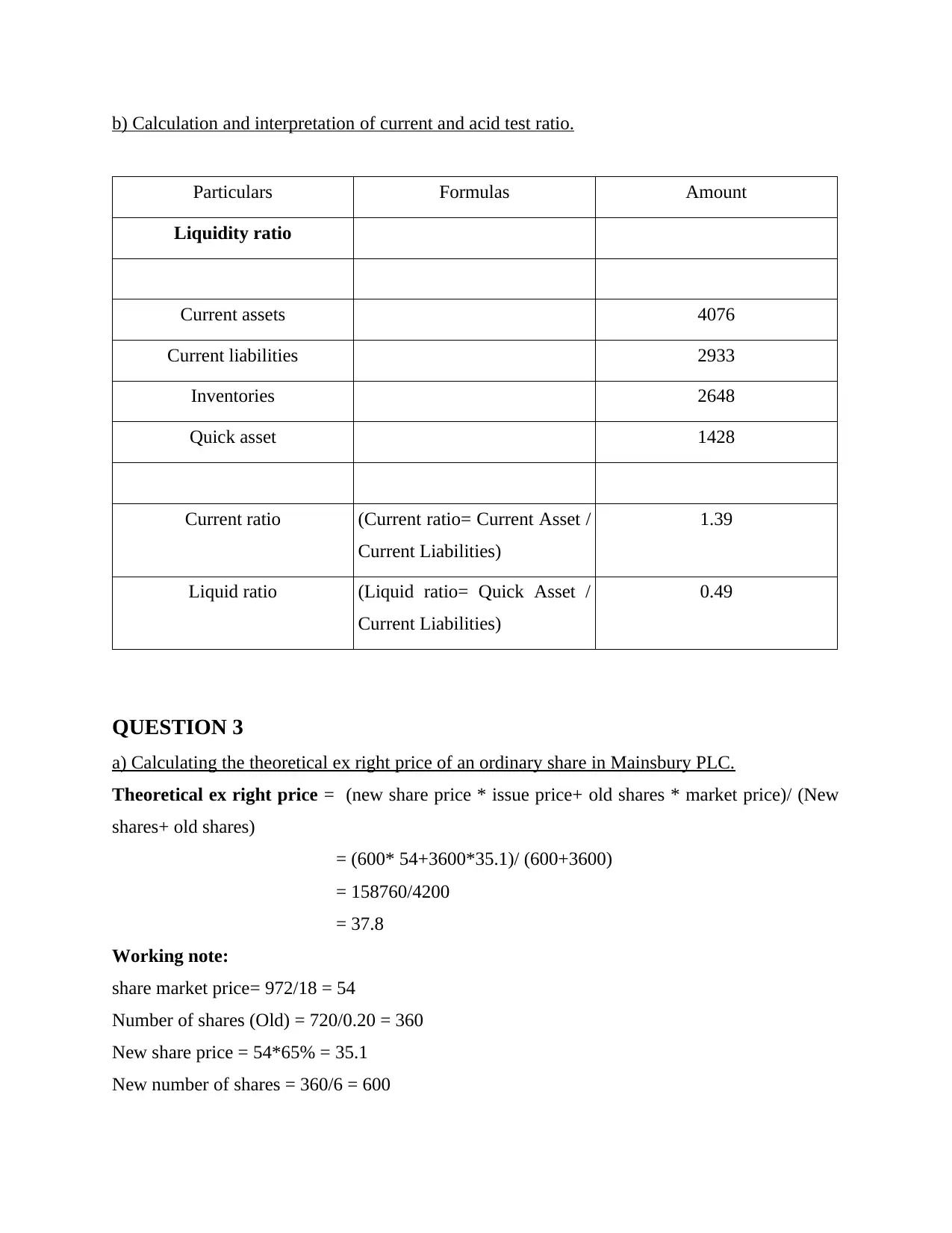

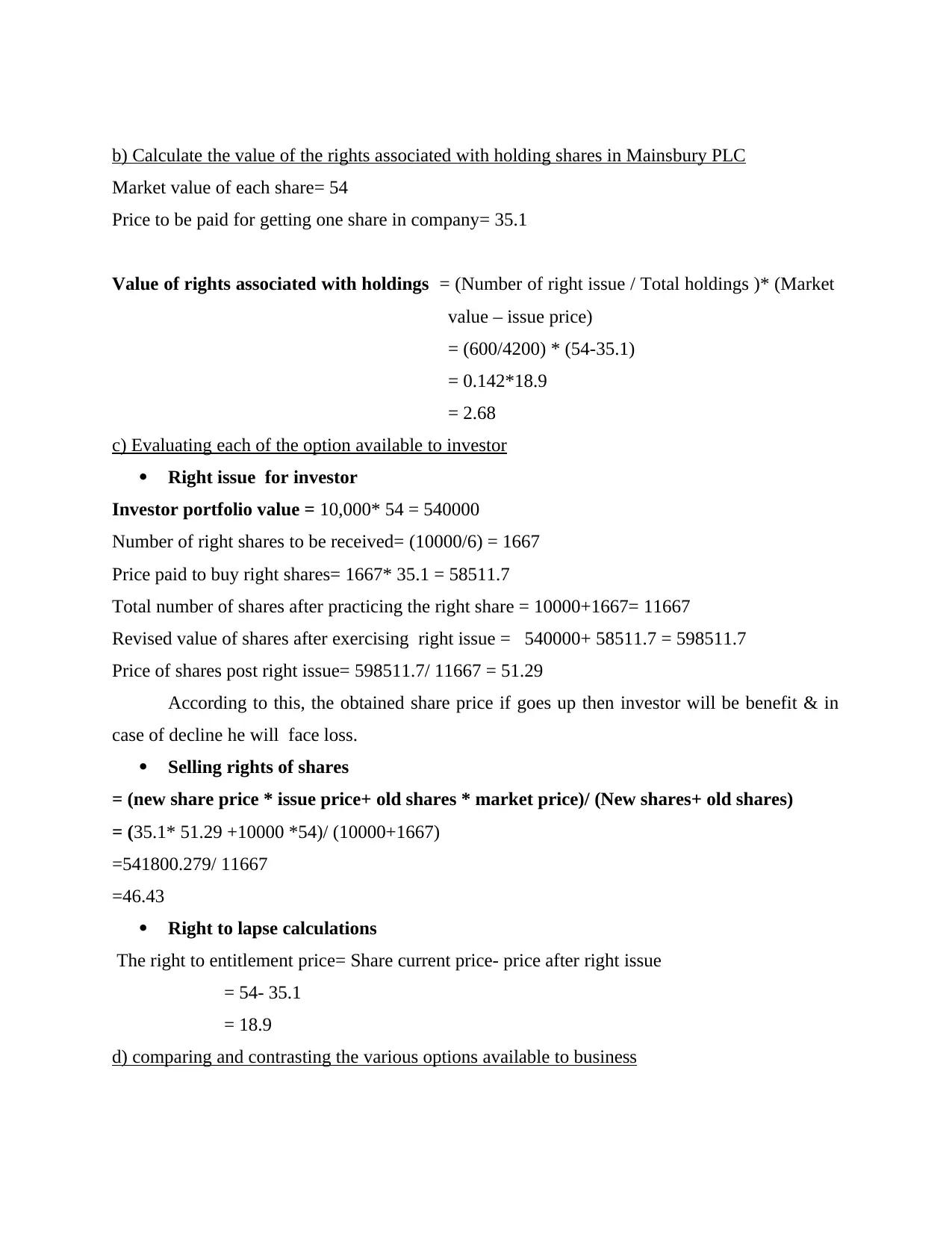

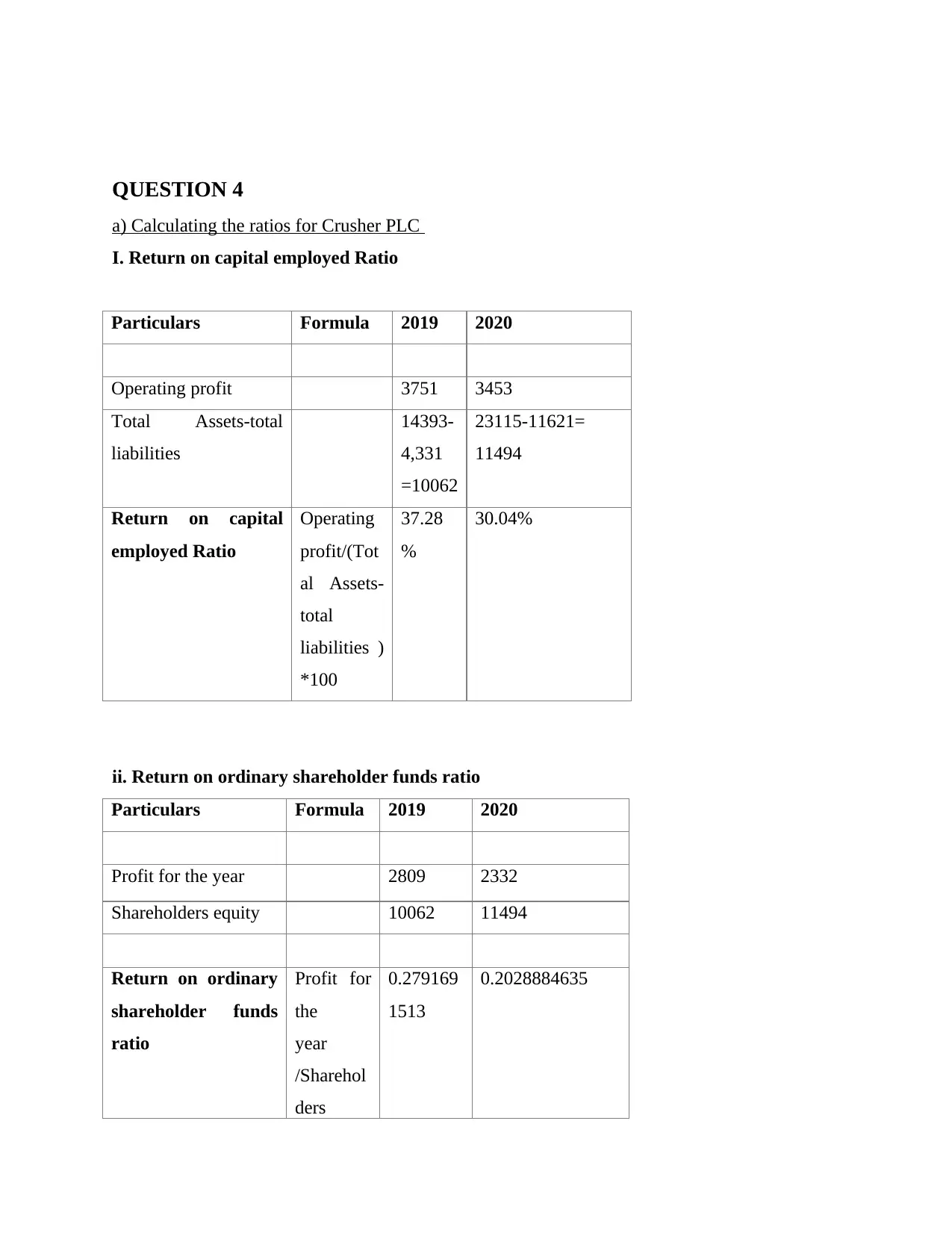

This article covers various topics related to business finance such as computation of net cash inflow, determination of internal rate of return, calculation of average operating cycle, current and acid test ratio, theoretical ex right price of an ordinary share in Mainsbury PLC, and financial ratios for Crusher PLC. The article provides a detailed analysis of the financial viability of investing in a project and compares different methods that can be used to account for risk while analyzing the viability of a project. It also includes calculations and interpretations of various financial ratios for Crusher PLC.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1 out of 15

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.