Business Finance Report: Time Value, Wealth, and Annuity Analysis

VerifiedAdded on 2021/02/18

|13

|3395

|70

Report

AI Summary

This report delves into key concepts within business finance, beginning with the time value of money and its significance in financial planning. It then examines the concept of maximizing shareholder wealth, emphasizing the importance of efficient management and positive net present value. The report differentiates between effective and nominal interest rates, illustrating their application in evaluating investment opportunities. Furthermore, it provides a detailed explanation of calculating present and future values, including the nuances of ordinary and annuity due structures. The report also includes practical examples, such as evaluating investment suitability based on present value and net present value calculations, and analyzing different annuity scenarios to determine the best investment options. The overall aim is to provide a comprehensive overview of financial principles essential for sound business decision-making.

Business finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

Concept of time value of money and its use and importance in the finance...............................1

Concept of maximising the wealth of the shareholders and significance of maximising the

wealth for management...............................................................................................................2

Difference between effective rate of return and nominal rate. Situations when these are used

to evaluate different investment opportunities............................................................................3

Method of calculating present value and future value of an annuity. Difference between

ordinary annuity and annuity due................................................................................................3

PART 2............................................................................................................................................4

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

Concept of time value of money and its use and importance in the finance...............................1

Concept of maximising the wealth of the shareholders and significance of maximising the

wealth for management...............................................................................................................2

Difference between effective rate of return and nominal rate. Situations when these are used

to evaluate different investment opportunities............................................................................3

Method of calculating present value and future value of an annuity. Difference between

ordinary annuity and annuity due................................................................................................3

PART 2............................................................................................................................................4

REFERENCES..............................................................................................................................10

INTRODUCTION

Business finance is an economic activity that helps commercial entities and non- profits

organizations for short- term operating needs or long term investment. It is the term that

encompasses a wide range of activities and disciplines rotating around the management of

money and other valuable assets. It is a financial plan for a business that helps the managers in

achieving the goals with efficiency. The report describes about the time value of money and its

significance in the finance. Further it reflects the importance of maximising the shareholders'

wealth and the difference between effective and nominal rate. Evaluation present value and

future value and the difference between ordinary and due annuity is also mentioned in the report.

PART 1

Concept of time value of money and its use and importance in the finance.

Time value of money is one of the most important concepts in finance. It is the money

that the firm has in its possession today is more valuable than future payments because the

money received now can be invested to earn the positive returns in the future (Muda and

Hasibuan, A.N., 2018). For example- A dollar on hand today is worth more than a dollar to be

received in the future because the dollar on hand today can be invested to earn interest to yield

more than a dollar in the probable future.

This depends upon the rate of return or interest rate which can be earner on the investment. The

time value of money compares the future value with the present value of an amount of money

(Gudkov, Ignatieva, and Ziveyi, 2019). Future value is the amount to which an amount of

money will grow in a defined period at a specified investment rate.

Uses Importance

Time value techniques are widely used in

personal financial planning.

It is used to evaluate the future value of an

investment made today.

For computing the present value of cash to be

received at some future date time value of

money is considered.

This tool helps in calculating the return on

The major importance of time value of money

is required in the finance for accounting

accuracy of certain transactions such as loan

amortization, lease payments, and bond

interest.

In order to design systems that optimize the

firm's cash-flow, time value of money plays an

essential role.

1

Business finance is an economic activity that helps commercial entities and non- profits

organizations for short- term operating needs or long term investment. It is the term that

encompasses a wide range of activities and disciplines rotating around the management of

money and other valuable assets. It is a financial plan for a business that helps the managers in

achieving the goals with efficiency. The report describes about the time value of money and its

significance in the finance. Further it reflects the importance of maximising the shareholders'

wealth and the difference between effective and nominal rate. Evaluation present value and

future value and the difference between ordinary and due annuity is also mentioned in the report.

PART 1

Concept of time value of money and its use and importance in the finance.

Time value of money is one of the most important concepts in finance. It is the money

that the firm has in its possession today is more valuable than future payments because the

money received now can be invested to earn the positive returns in the future (Muda and

Hasibuan, A.N., 2018). For example- A dollar on hand today is worth more than a dollar to be

received in the future because the dollar on hand today can be invested to earn interest to yield

more than a dollar in the probable future.

This depends upon the rate of return or interest rate which can be earner on the investment. The

time value of money compares the future value with the present value of an amount of money

(Gudkov, Ignatieva, and Ziveyi, 2019). Future value is the amount to which an amount of

money will grow in a defined period at a specified investment rate.

Uses Importance

Time value techniques are widely used in

personal financial planning.

It is used to evaluate the future value of an

investment made today.

For computing the present value of cash to be

received at some future date time value of

money is considered.

This tool helps in calculating the return on

The major importance of time value of money

is required in the finance for accounting

accuracy of certain transactions such as loan

amortization, lease payments, and bond

interest.

In order to design systems that optimize the

firm's cash-flow, time value of money plays an

essential role.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

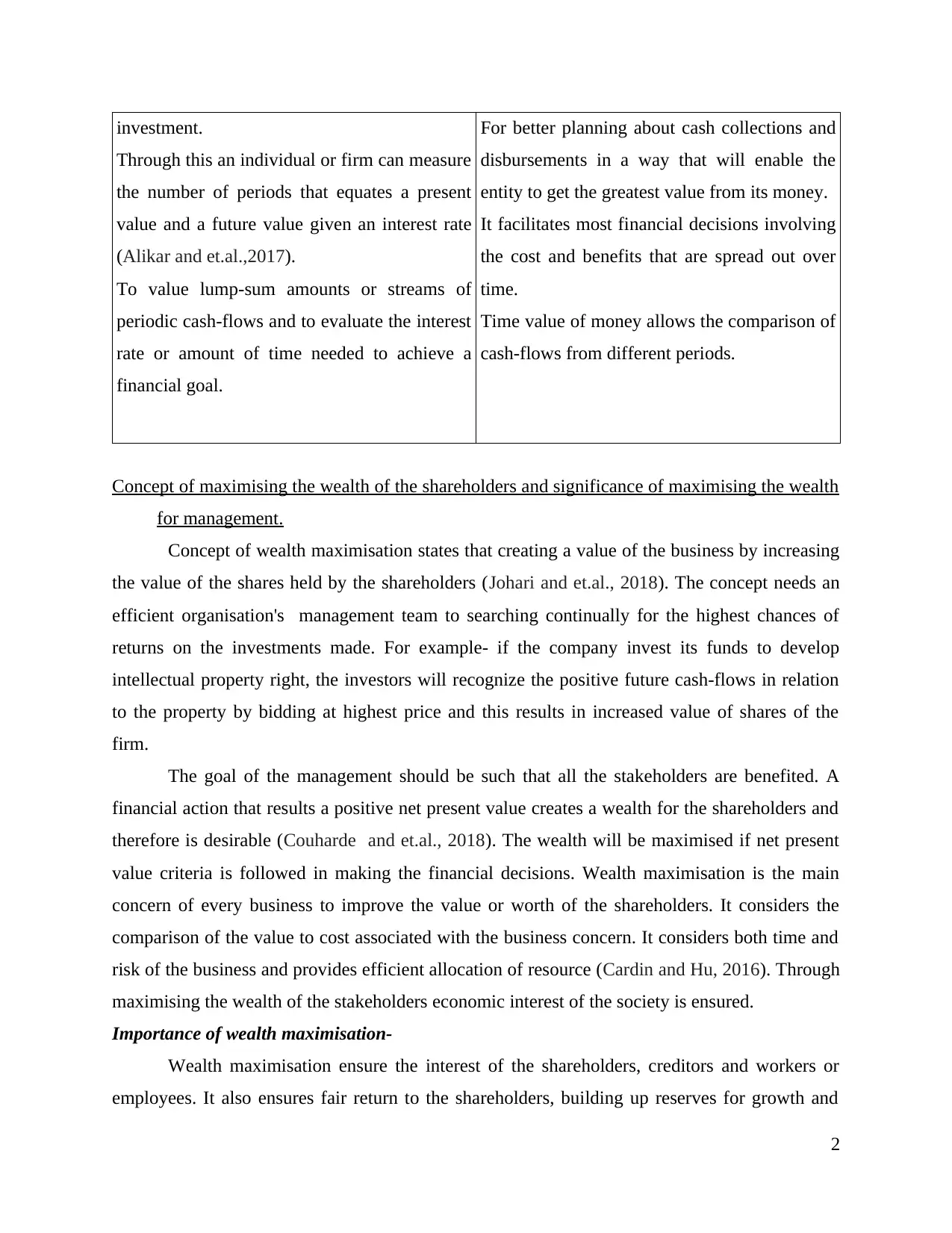

investment.

Through this an individual or firm can measure

the number of periods that equates a present

value and a future value given an interest rate

(Alikar and et.al.,2017).

To value lump-sum amounts or streams of

periodic cash-flows and to evaluate the interest

rate or amount of time needed to achieve a

financial goal.

For better planning about cash collections and

disbursements in a way that will enable the

entity to get the greatest value from its money.

It facilitates most financial decisions involving

the cost and benefits that are spread out over

time.

Time value of money allows the comparison of

cash-flows from different periods.

Concept of maximising the wealth of the shareholders and significance of maximising the wealth

for management.

Concept of wealth maximisation states that creating a value of the business by increasing

the value of the shares held by the shareholders (Johari and et.al., 2018). The concept needs an

efficient organisation's management team to searching continually for the highest chances of

returns on the investments made. For example- if the company invest its funds to develop

intellectual property right, the investors will recognize the positive future cash-flows in relation

to the property by bidding at highest price and this results in increased value of shares of the

firm.

The goal of the management should be such that all the stakeholders are benefited. A

financial action that results a positive net present value creates a wealth for the shareholders and

therefore is desirable (Couharde and et.al., 2018). The wealth will be maximised if net present

value criteria is followed in making the financial decisions. Wealth maximisation is the main

concern of every business to improve the value or worth of the shareholders. It considers the

comparison of the value to cost associated with the business concern. It considers both time and

risk of the business and provides efficient allocation of resource (Cardin and Hu, 2016). Through

maximising the wealth of the stakeholders economic interest of the society is ensured.

Importance of wealth maximisation-

Wealth maximisation ensure the interest of the shareholders, creditors and workers or

employees. It also ensures fair return to the shareholders, building up reserves for growth and

2

Through this an individual or firm can measure

the number of periods that equates a present

value and a future value given an interest rate

(Alikar and et.al.,2017).

To value lump-sum amounts or streams of

periodic cash-flows and to evaluate the interest

rate or amount of time needed to achieve a

financial goal.

For better planning about cash collections and

disbursements in a way that will enable the

entity to get the greatest value from its money.

It facilitates most financial decisions involving

the cost and benefits that are spread out over

time.

Time value of money allows the comparison of

cash-flows from different periods.

Concept of maximising the wealth of the shareholders and significance of maximising the wealth

for management.

Concept of wealth maximisation states that creating a value of the business by increasing

the value of the shares held by the shareholders (Johari and et.al., 2018). The concept needs an

efficient organisation's management team to searching continually for the highest chances of

returns on the investments made. For example- if the company invest its funds to develop

intellectual property right, the investors will recognize the positive future cash-flows in relation

to the property by bidding at highest price and this results in increased value of shares of the

firm.

The goal of the management should be such that all the stakeholders are benefited. A

financial action that results a positive net present value creates a wealth for the shareholders and

therefore is desirable (Couharde and et.al., 2018). The wealth will be maximised if net present

value criteria is followed in making the financial decisions. Wealth maximisation is the main

concern of every business to improve the value or worth of the shareholders. It considers the

comparison of the value to cost associated with the business concern. It considers both time and

risk of the business and provides efficient allocation of resource (Cardin and Hu, 2016). Through

maximising the wealth of the stakeholders economic interest of the society is ensured.

Importance of wealth maximisation-

Wealth maximisation ensure the interest of the shareholders, creditors and workers or

employees. It also ensures fair return to the shareholders, building up reserves for growth and

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

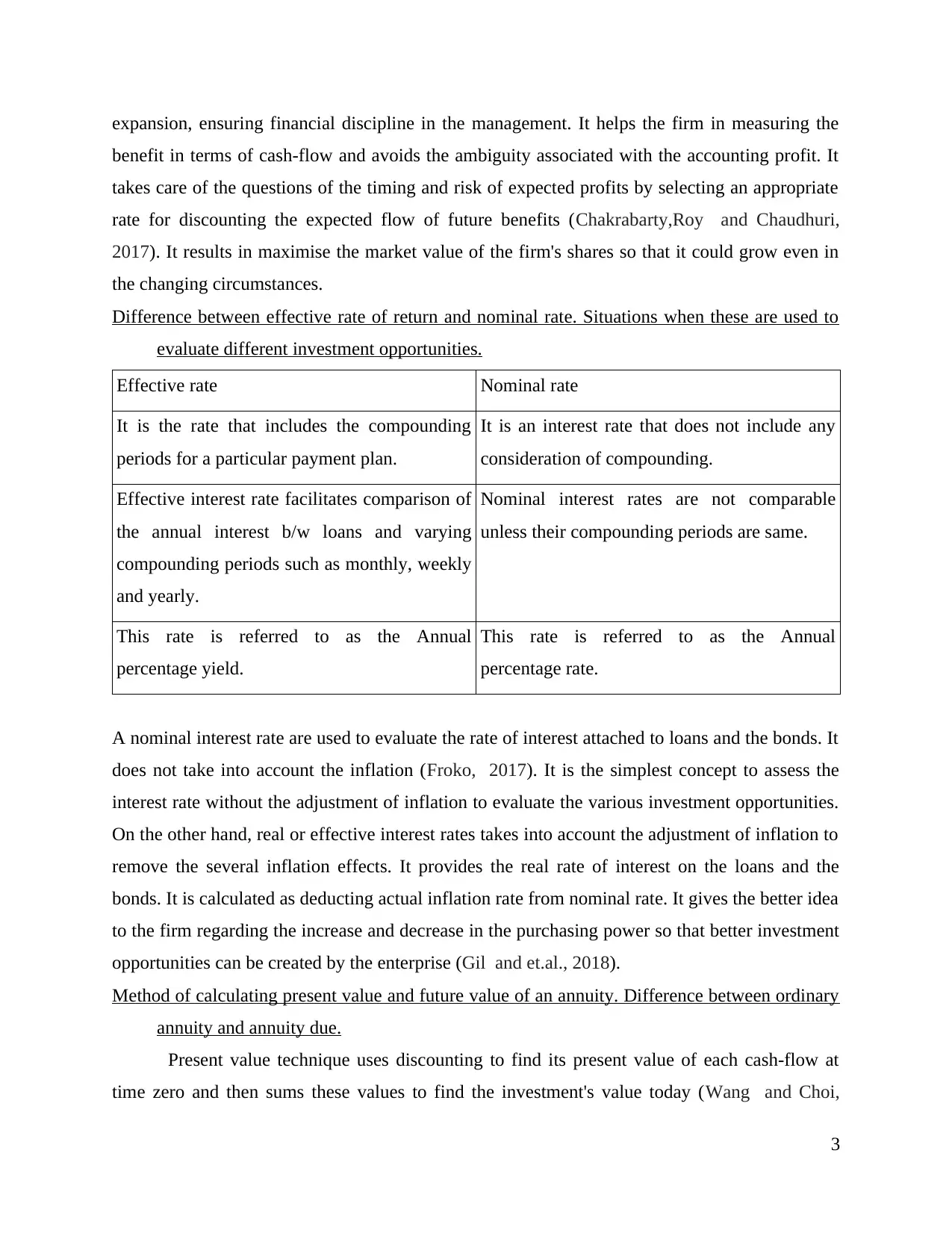

expansion, ensuring financial discipline in the management. It helps the firm in measuring the

benefit in terms of cash-flow and avoids the ambiguity associated with the accounting profit. It

takes care of the questions of the timing and risk of expected profits by selecting an appropriate

rate for discounting the expected flow of future benefits (Chakrabarty,Roy and Chaudhuri,

2017). It results in maximise the market value of the firm's shares so that it could grow even in

the changing circumstances.

Difference between effective rate of return and nominal rate. Situations when these are used to

evaluate different investment opportunities.

Effective rate Nominal rate

It is the rate that includes the compounding

periods for a particular payment plan.

It is an interest rate that does not include any

consideration of compounding.

Effective interest rate facilitates comparison of

the annual interest b/w loans and varying

compounding periods such as monthly, weekly

and yearly.

Nominal interest rates are not comparable

unless their compounding periods are same.

This rate is referred to as the Annual

percentage yield.

This rate is referred to as the Annual

percentage rate.

A nominal interest rate are used to evaluate the rate of interest attached to loans and the bonds. It

does not take into account the inflation (Froko, 2017). It is the simplest concept to assess the

interest rate without the adjustment of inflation to evaluate the various investment opportunities.

On the other hand, real or effective interest rates takes into account the adjustment of inflation to

remove the several inflation effects. It provides the real rate of interest on the loans and the

bonds. It is calculated as deducting actual inflation rate from nominal rate. It gives the better idea

to the firm regarding the increase and decrease in the purchasing power so that better investment

opportunities can be created by the enterprise (Gil and et.al., 2018).

Method of calculating present value and future value of an annuity. Difference between ordinary

annuity and annuity due.

Present value technique uses discounting to find its present value of each cash-flow at

time zero and then sums these values to find the investment's value today (Wang and Choi,

3

benefit in terms of cash-flow and avoids the ambiguity associated with the accounting profit. It

takes care of the questions of the timing and risk of expected profits by selecting an appropriate

rate for discounting the expected flow of future benefits (Chakrabarty,Roy and Chaudhuri,

2017). It results in maximise the market value of the firm's shares so that it could grow even in

the changing circumstances.

Difference between effective rate of return and nominal rate. Situations when these are used to

evaluate different investment opportunities.

Effective rate Nominal rate

It is the rate that includes the compounding

periods for a particular payment plan.

It is an interest rate that does not include any

consideration of compounding.

Effective interest rate facilitates comparison of

the annual interest b/w loans and varying

compounding periods such as monthly, weekly

and yearly.

Nominal interest rates are not comparable

unless their compounding periods are same.

This rate is referred to as the Annual

percentage yield.

This rate is referred to as the Annual

percentage rate.

A nominal interest rate are used to evaluate the rate of interest attached to loans and the bonds. It

does not take into account the inflation (Froko, 2017). It is the simplest concept to assess the

interest rate without the adjustment of inflation to evaluate the various investment opportunities.

On the other hand, real or effective interest rates takes into account the adjustment of inflation to

remove the several inflation effects. It provides the real rate of interest on the loans and the

bonds. It is calculated as deducting actual inflation rate from nominal rate. It gives the better idea

to the firm regarding the increase and decrease in the purchasing power so that better investment

opportunities can be created by the enterprise (Gil and et.al., 2018).

Method of calculating present value and future value of an annuity. Difference between ordinary

annuity and annuity due.

Present value technique uses discounting to find its present value of each cash-flow at

time zero and then sums these values to find the investment's value today (Wang and Choi,

3

2015). On the other side, future value technique uses compounding to find future value of each

cash-flow at the end of the investment's and then sums these values to find the future value of the

investment made.

Difference-

Ordinary annuity Annuity due

An annuity for which payments are made at the

end of each interest period.

An annuity for which payments are required at

the beginning of each period.

For example- Bonds, housing loan, mortgage

payment etc.

For example- Rent, premium of insurance etc.

Equal periodic cash-flows that begin at the end

of each time interval.

Equal periodic cash-flows that begin right

away or at the beginning of each time interval.

It is appropriate at the time of making

payments.

It is appropriate at the time of receiving the

amount due.

The payment under this method belongs to the

period preceding its date.

The payment under this method belongs to the

period following its date.

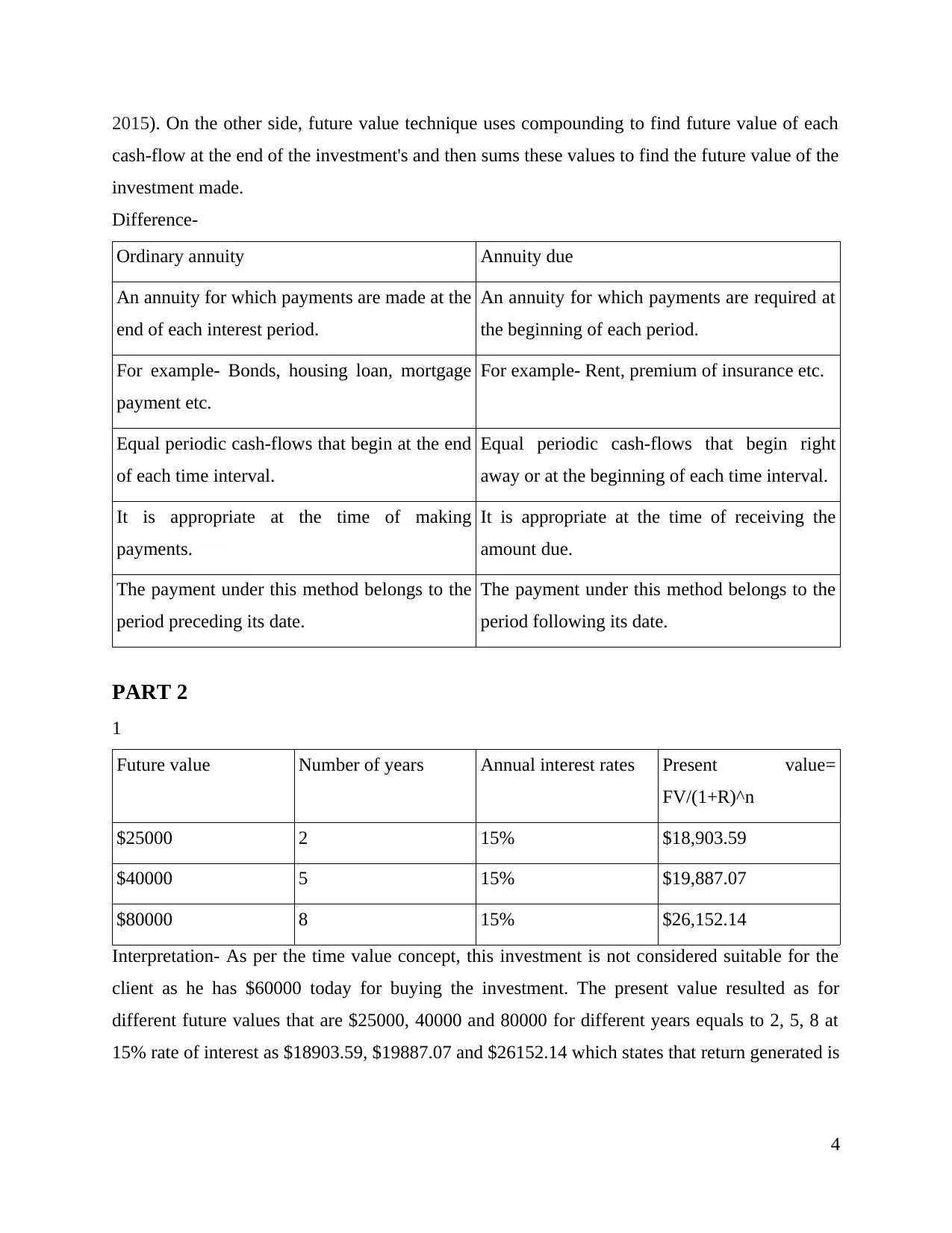

PART 2

1

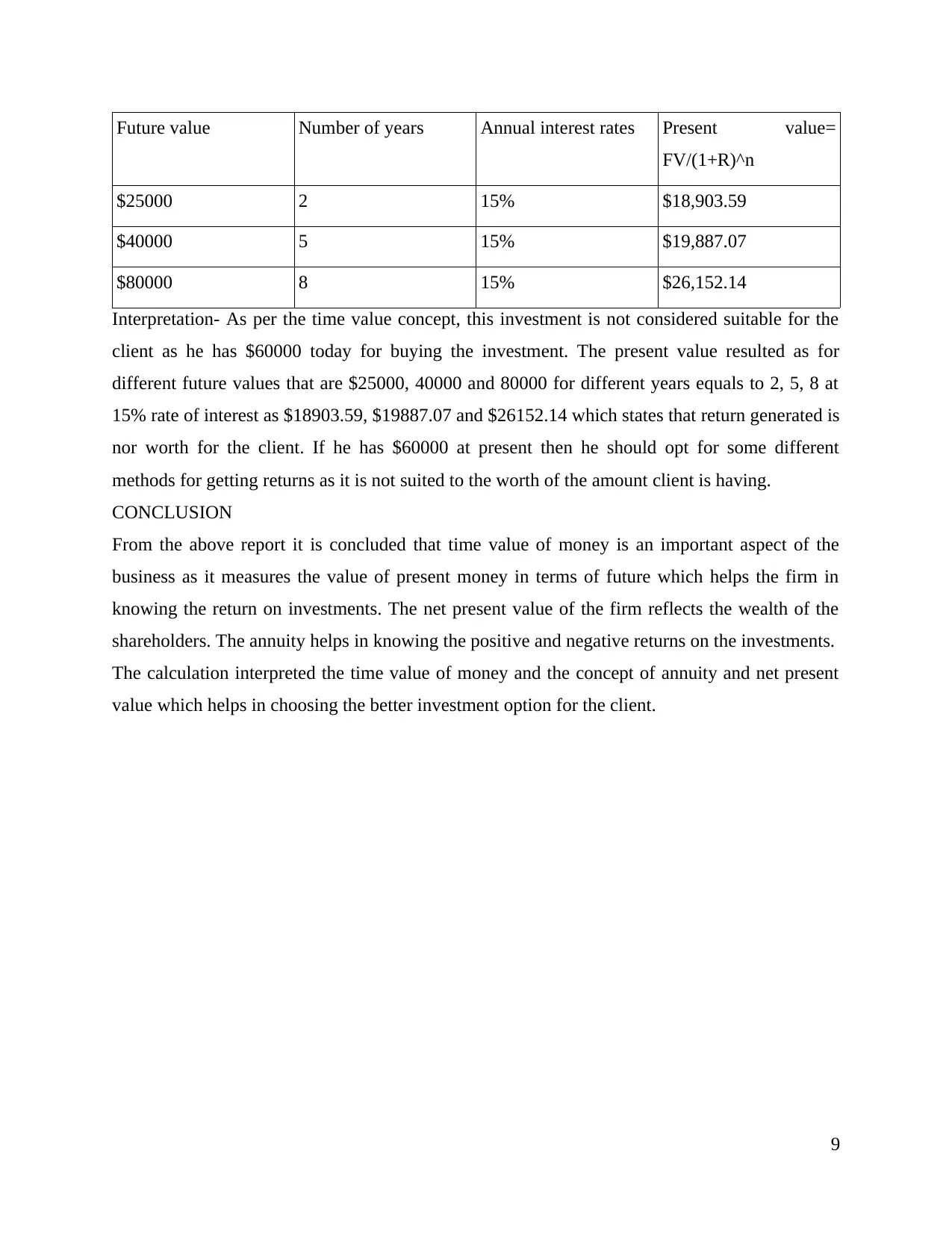

Future value Number of years Annual interest rates Present value=

FV/(1+R)^n

$25000 2 15% $18,903.59

$40000 5 15% $19,887.07

$80000 8 15% $26,152.14

Interpretation- As per the time value concept, this investment is not considered suitable for the

client as he has $60000 today for buying the investment. The present value resulted as for

different future values that are $25000, 40000 and 80000 for different years equals to 2, 5, 8 at

15% rate of interest as $18903.59, $19887.07 and $26152.14 which states that return generated is

4

cash-flow at the end of the investment's and then sums these values to find the future value of the

investment made.

Difference-

Ordinary annuity Annuity due

An annuity for which payments are made at the

end of each interest period.

An annuity for which payments are required at

the beginning of each period.

For example- Bonds, housing loan, mortgage

payment etc.

For example- Rent, premium of insurance etc.

Equal periodic cash-flows that begin at the end

of each time interval.

Equal periodic cash-flows that begin right

away or at the beginning of each time interval.

It is appropriate at the time of making

payments.

It is appropriate at the time of receiving the

amount due.

The payment under this method belongs to the

period preceding its date.

The payment under this method belongs to the

period following its date.

PART 2

1

Future value Number of years Annual interest rates Present value=

FV/(1+R)^n

$25000 2 15% $18,903.59

$40000 5 15% $19,887.07

$80000 8 15% $26,152.14

Interpretation- As per the time value concept, this investment is not considered suitable for the

client as he has $60000 today for buying the investment. The present value resulted as for

different future values that are $25000, 40000 and 80000 for different years equals to 2, 5, 8 at

15% rate of interest as $18903.59, $19887.07 and $26152.14 which states that return generated is

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

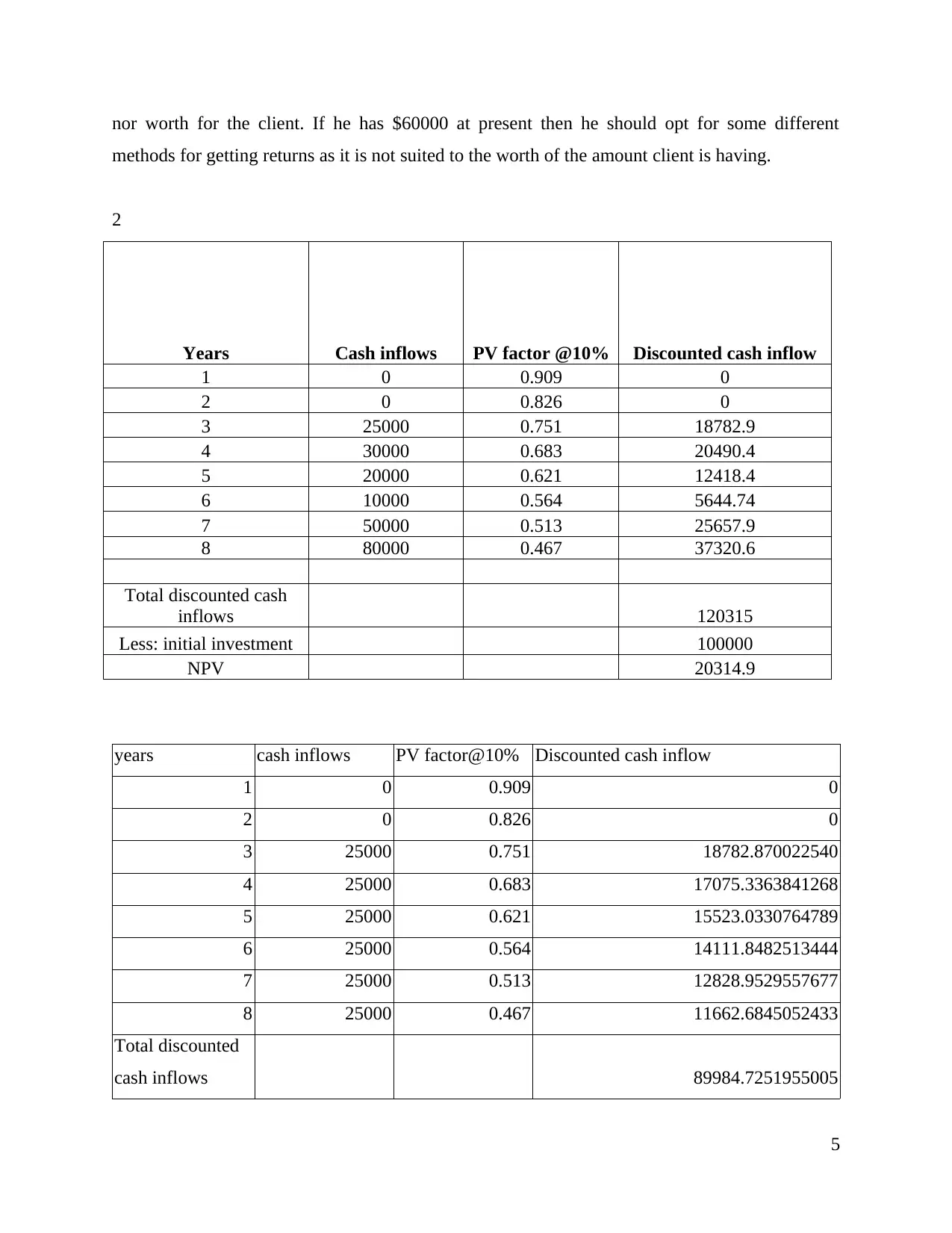

nor worth for the client. If he has $60000 at present then he should opt for some different

methods for getting returns as it is not suited to the worth of the amount client is having.

2

Years Cash inflows PV factor @10% Discounted cash inflow

1 0 0.909 0

2 0 0.826 0

3 25000 0.751 18782.9

4 30000 0.683 20490.4

5 20000 0.621 12418.4

6 10000 0.564 5644.74

7 50000 0.513 25657.9

8 80000 0.467 37320.6

Total discounted cash

inflows 120315

Less: initial investment 100000

NPV 20314.9

years cash inflows PV factor@10% Discounted cash inflow

1 0 0.909 0

2 0 0.826 0

3 25000 0.751 18782.870022540

4 25000 0.683 17075.3363841268

5 25000 0.621 15523.0330764789

6 25000 0.564 14111.8482513444

7 25000 0.513 12828.9529557677

8 25000 0.467 11662.6845052433

Total discounted

cash inflows 89984.7251955005

5

methods for getting returns as it is not suited to the worth of the amount client is having.

2

Years Cash inflows PV factor @10% Discounted cash inflow

1 0 0.909 0

2 0 0.826 0

3 25000 0.751 18782.9

4 30000 0.683 20490.4

5 20000 0.621 12418.4

6 10000 0.564 5644.74

7 50000 0.513 25657.9

8 80000 0.467 37320.6

Total discounted cash

inflows 120315

Less: initial investment 100000

NPV 20314.9

years cash inflows PV factor@10% Discounted cash inflow

1 0 0.909 0

2 0 0.826 0

3 25000 0.751 18782.870022540

4 25000 0.683 17075.3363841268

5 25000 0.621 15523.0330764789

6 25000 0.564 14111.8482513444

7 25000 0.513 12828.9529557677

8 25000 0.467 11662.6845052433

Total discounted

cash inflows 89984.7251955005

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

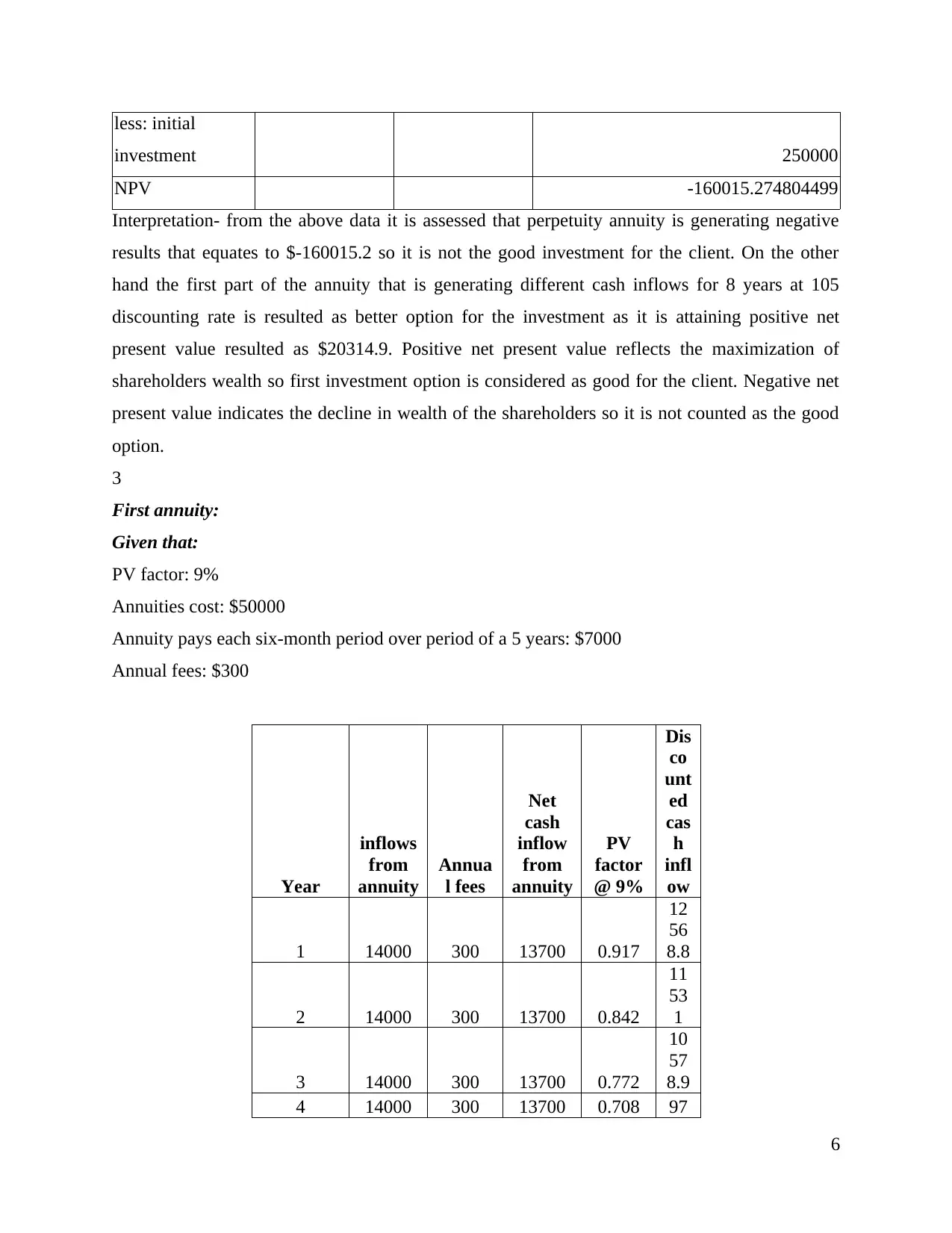

less: initial

investment 250000

NPV -160015.274804499

Interpretation- from the above data it is assessed that perpetuity annuity is generating negative

results that equates to $-160015.2 so it is not the good investment for the client. On the other

hand the first part of the annuity that is generating different cash inflows for 8 years at 105

discounting rate is resulted as better option for the investment as it is attaining positive net

present value resulted as $20314.9. Positive net present value reflects the maximization of

shareholders wealth so first investment option is considered as good for the client. Negative net

present value indicates the decline in wealth of the shareholders so it is not counted as the good

option.

3

First annuity:

Given that:

PV factor: 9%

Annuities cost: $50000

Annuity pays each six-month period over period of a 5 years: $7000

Annual fees: $300

Year

inflows

from

annuity

Annua

l fees

Net

cash

inflow

from

annuity

PV

factor

@ 9%

Dis

co

unt

ed

cas

h

infl

ow

1 14000 300 13700 0.917

12

56

8.8

2 14000 300 13700 0.842

11

53

1

3 14000 300 13700 0.772

10

57

8.9

4 14000 300 13700 0.708 97

6

investment 250000

NPV -160015.274804499

Interpretation- from the above data it is assessed that perpetuity annuity is generating negative

results that equates to $-160015.2 so it is not the good investment for the client. On the other

hand the first part of the annuity that is generating different cash inflows for 8 years at 105

discounting rate is resulted as better option for the investment as it is attaining positive net

present value resulted as $20314.9. Positive net present value reflects the maximization of

shareholders wealth so first investment option is considered as good for the client. Negative net

present value indicates the decline in wealth of the shareholders so it is not counted as the good

option.

3

First annuity:

Given that:

PV factor: 9%

Annuities cost: $50000

Annuity pays each six-month period over period of a 5 years: $7000

Annual fees: $300

Year

inflows

from

annuity

Annua

l fees

Net

cash

inflow

from

annuity

PV

factor

@ 9%

Dis

co

unt

ed

cas

h

infl

ow

1 14000 300 13700 0.917

12

56

8.8

2 14000 300 13700 0.842

11

53

1

3 14000 300 13700 0.772

10

57

8.9

4 14000 300 13700 0.708 97

6

05.

43

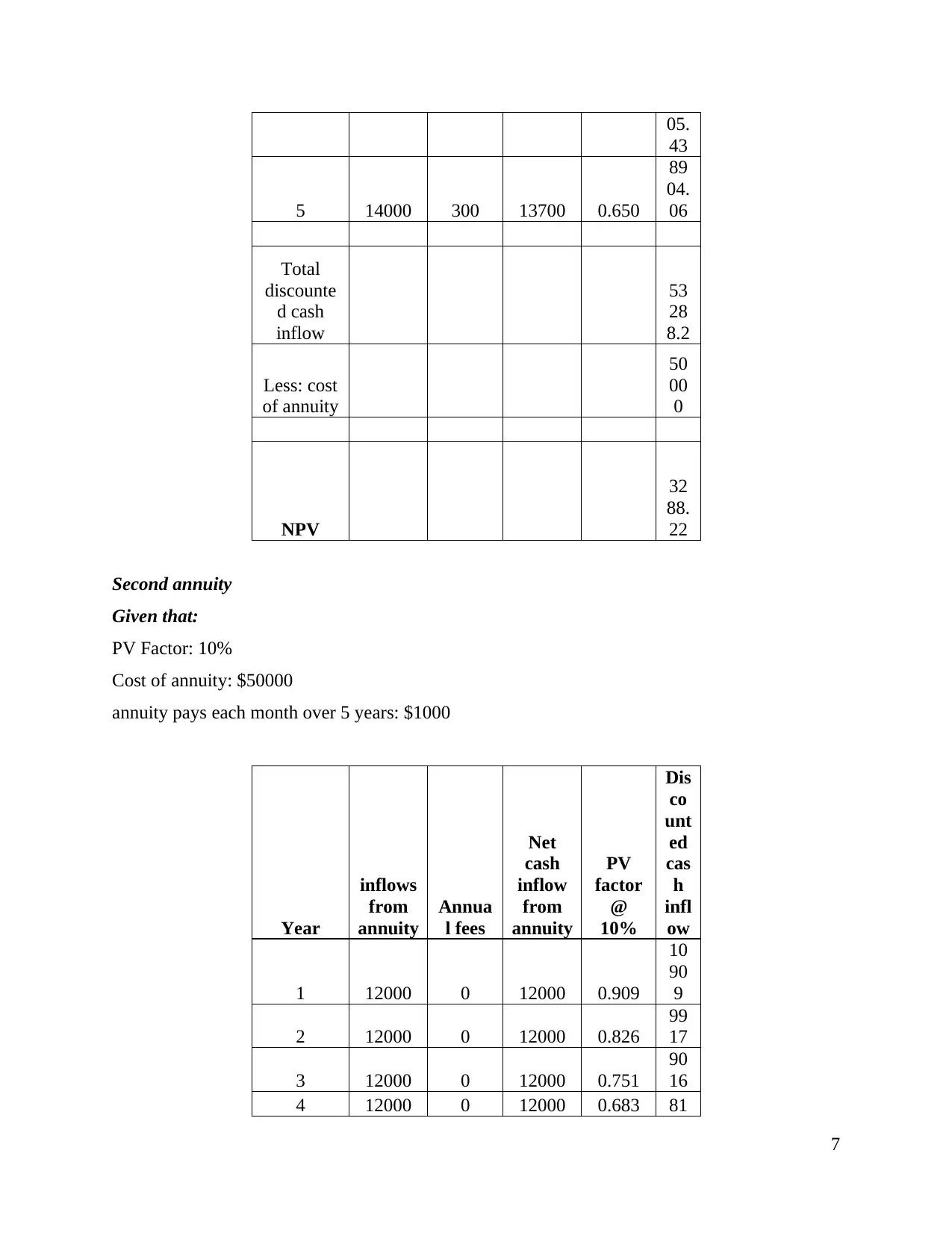

5 14000 300 13700 0.650

89

04.

06

Total

discounte

d cash

inflow

53

28

8.2

Less: cost

of annuity

50

00

0

NPV

32

88.

22

Second annuity

Given that:

PV Factor: 10%

Cost of annuity: $50000

annuity pays each month over 5 years: $1000

Year

inflows

from

annuity

Annua

l fees

Net

cash

inflow

from

annuity

PV

factor

@

10%

Dis

co

unt

ed

cas

h

infl

ow

1 12000 0 12000 0.909

10

90

9

2 12000 0 12000 0.826

99

17

3 12000 0 12000 0.751

90

16

4 12000 0 12000 0.683 81

7

43

5 14000 300 13700 0.650

89

04.

06

Total

discounte

d cash

inflow

53

28

8.2

Less: cost

of annuity

50

00

0

NPV

32

88.

22

Second annuity

Given that:

PV Factor: 10%

Cost of annuity: $50000

annuity pays each month over 5 years: $1000

Year

inflows

from

annuity

Annua

l fees

Net

cash

inflow

from

annuity

PV

factor

@

10%

Dis

co

unt

ed

cas

h

infl

ow

1 12000 0 12000 0.909

10

90

9

2 12000 0 12000 0.826

99

17

3 12000 0 12000 0.751

90

16

4 12000 0 12000 0.683 81

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

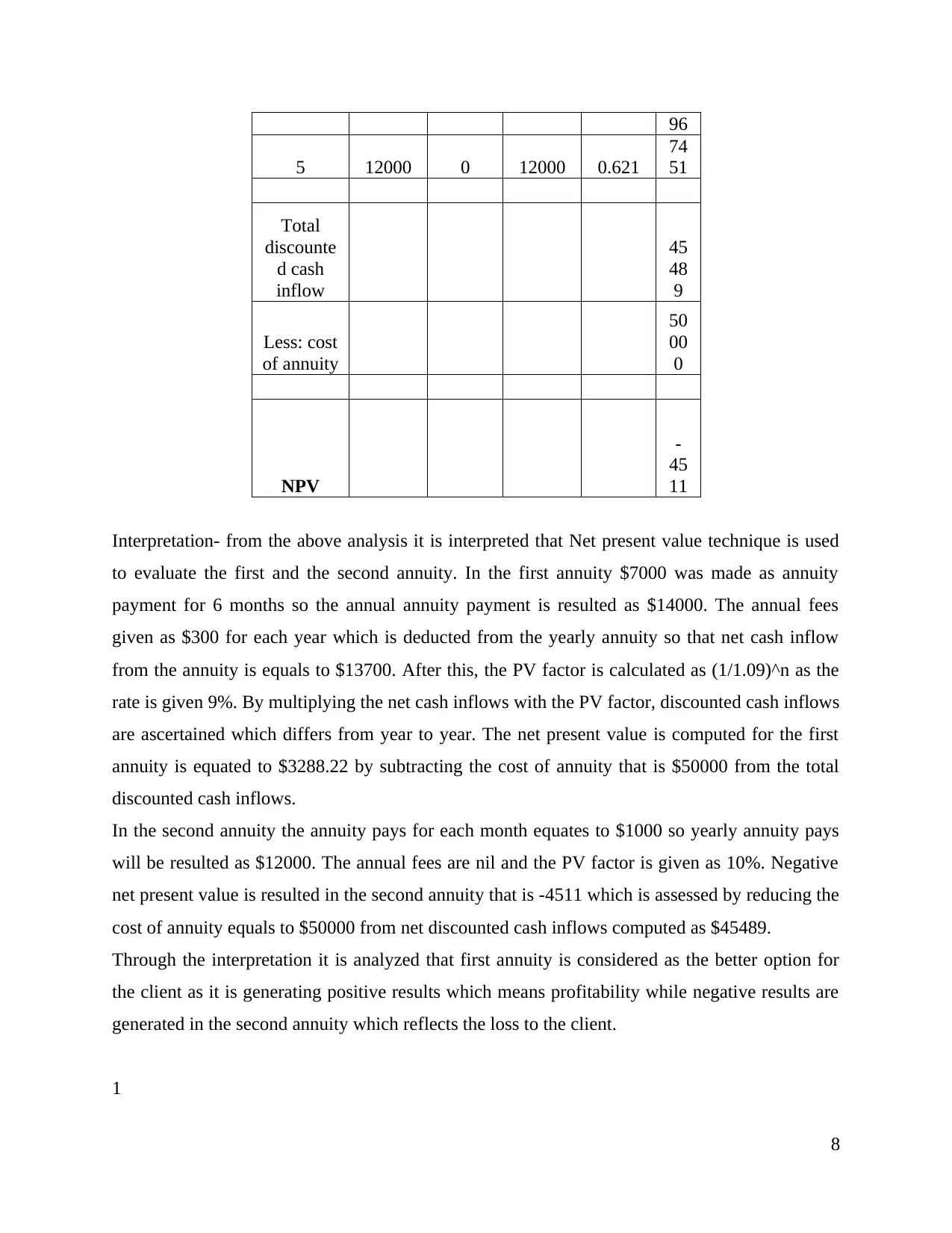

96

5 12000 0 12000 0.621

74

51

Total

discounte

d cash

inflow

45

48

9

Less: cost

of annuity

50

00

0

NPV

-

45

11

Interpretation- from the above analysis it is interpreted that Net present value technique is used

to evaluate the first and the second annuity. In the first annuity $7000 was made as annuity

payment for 6 months so the annual annuity payment is resulted as $14000. The annual fees

given as $300 for each year which is deducted from the yearly annuity so that net cash inflow

from the annuity is equals to $13700. After this, the PV factor is calculated as (1/1.09)^n as the

rate is given 9%. By multiplying the net cash inflows with the PV factor, discounted cash inflows

are ascertained which differs from year to year. The net present value is computed for the first

annuity is equated to $3288.22 by subtracting the cost of annuity that is $50000 from the total

discounted cash inflows.

In the second annuity the annuity pays for each month equates to $1000 so yearly annuity pays

will be resulted as $12000. The annual fees are nil and the PV factor is given as 10%. Negative

net present value is resulted in the second annuity that is -4511 which is assessed by reducing the

cost of annuity equals to $50000 from net discounted cash inflows computed as $45489.

Through the interpretation it is analyzed that first annuity is considered as the better option for

the client as it is generating positive results which means profitability while negative results are

generated in the second annuity which reflects the loss to the client.

1

8

5 12000 0 12000 0.621

74

51

Total

discounte

d cash

inflow

45

48

9

Less: cost

of annuity

50

00

0

NPV

-

45

11

Interpretation- from the above analysis it is interpreted that Net present value technique is used

to evaluate the first and the second annuity. In the first annuity $7000 was made as annuity

payment for 6 months so the annual annuity payment is resulted as $14000. The annual fees

given as $300 for each year which is deducted from the yearly annuity so that net cash inflow

from the annuity is equals to $13700. After this, the PV factor is calculated as (1/1.09)^n as the

rate is given 9%. By multiplying the net cash inflows with the PV factor, discounted cash inflows

are ascertained which differs from year to year. The net present value is computed for the first

annuity is equated to $3288.22 by subtracting the cost of annuity that is $50000 from the total

discounted cash inflows.

In the second annuity the annuity pays for each month equates to $1000 so yearly annuity pays

will be resulted as $12000. The annual fees are nil and the PV factor is given as 10%. Negative

net present value is resulted in the second annuity that is -4511 which is assessed by reducing the

cost of annuity equals to $50000 from net discounted cash inflows computed as $45489.

Through the interpretation it is analyzed that first annuity is considered as the better option for

the client as it is generating positive results which means profitability while negative results are

generated in the second annuity which reflects the loss to the client.

1

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Future value Number of years Annual interest rates Present value=

FV/(1+R)^n

$25000 2 15% $18,903.59

$40000 5 15% $19,887.07

$80000 8 15% $26,152.14

Interpretation- As per the time value concept, this investment is not considered suitable for the

client as he has $60000 today for buying the investment. The present value resulted as for

different future values that are $25000, 40000 and 80000 for different years equals to 2, 5, 8 at

15% rate of interest as $18903.59, $19887.07 and $26152.14 which states that return generated is

nor worth for the client. If he has $60000 at present then he should opt for some different

methods for getting returns as it is not suited to the worth of the amount client is having.

CONCLUSION

From the above report it is concluded that time value of money is an important aspect of the

business as it measures the value of present money in terms of future which helps the firm in

knowing the return on investments. The net present value of the firm reflects the wealth of the

shareholders. The annuity helps in knowing the positive and negative returns on the investments.

The calculation interpreted the time value of money and the concept of annuity and net present

value which helps in choosing the better investment option for the client.

9

FV/(1+R)^n

$25000 2 15% $18,903.59

$40000 5 15% $19,887.07

$80000 8 15% $26,152.14

Interpretation- As per the time value concept, this investment is not considered suitable for the

client as he has $60000 today for buying the investment. The present value resulted as for

different future values that are $25000, 40000 and 80000 for different years equals to 2, 5, 8 at

15% rate of interest as $18903.59, $19887.07 and $26152.14 which states that return generated is

nor worth for the client. If he has $60000 at present then he should opt for some different

methods for getting returns as it is not suited to the worth of the amount client is having.

CONCLUSION

From the above report it is concluded that time value of money is an important aspect of the

business as it measures the value of present money in terms of future which helps the firm in

knowing the return on investments. The net present value of the firm reflects the wealth of the

shareholders. The annuity helps in knowing the positive and negative returns on the investments.

The calculation interpreted the time value of money and the concept of annuity and net present

value which helps in choosing the better investment option for the client.

9

REFERENCES

Books and journals

Alikar, N. and et.al.,2017. A bi-objective multi-period series-parallel inventory-redundancy

allocation problem with time value of money and inflation considerations. Computers &

Industrial Engineering. 104. pp.51-67.

Cardin, M. A. and Hu, J., 2016. Analyzing the tradeoffs between economies of scale, time-value

of money, and flexibility in design under uncertainty: Study of centralized versus

decentralized waste-to-energy systems. Journal of Mechanical Design. 138(1). p.011401.

Chakrabarty, R., Roy, T. and Chaudhuri, K. S., 2017. A production: inventory model for

defective items with shortages incorporating inflation and time value of

money. International Journal of Applied and Computational Mathematics. 3(1). pp.195-

212.

Couharde, C. and et.al., 2018. EQCHANGE: A world database on actual and equilibrium

effective exchange rates. International economics. 156. pp.206-230.

Froko, N. A., 2017. Short Term Financial Leverage and Shareholders’ Wealth Maximisation of

Ghanaian Banks: New Theoretical Evidence. Structure. 8(13).

Gil, A. and et.al., 2018. Experimental analysis of the effective thermal conductivity enhancement

of PCM using finned tubes in high temperature bulk tanks. Applied Thermal

Engineering. 142. pp.736-744.

Gudkov, N., Ignatieva, K. and Ziveyi, J., 2019. Pricing of guaranteed minimum withdrawal

benefits in variable annuities under stochastic volatility, stochastic interest rates and

stochastic mortality via the componentwise splitting method. Quantitative Finance. 19(3).

pp.501-518.

Johari, M. and et.al., 2018. Bi-level credit period coordination for periodic review inventory

system with price-credit dependent demand under time value of money. Transportation

Research Part E: Logistics and Transportation Review. 114. pp.270-291.

Muda, I. and Hasibuan, A. N., 2018. Public Discovery of the Concept of Time Value of Money

with Economic Value of Time. In Proceedings of MICoMS 2017 (pp. 251-257). Emerald

Publishing Limited.

10

Books and journals

Alikar, N. and et.al.,2017. A bi-objective multi-period series-parallel inventory-redundancy

allocation problem with time value of money and inflation considerations. Computers &

Industrial Engineering. 104. pp.51-67.

Cardin, M. A. and Hu, J., 2016. Analyzing the tradeoffs between economies of scale, time-value

of money, and flexibility in design under uncertainty: Study of centralized versus

decentralized waste-to-energy systems. Journal of Mechanical Design. 138(1). p.011401.

Chakrabarty, R., Roy, T. and Chaudhuri, K. S., 2017. A production: inventory model for

defective items with shortages incorporating inflation and time value of

money. International Journal of Applied and Computational Mathematics. 3(1). pp.195-

212.

Couharde, C. and et.al., 2018. EQCHANGE: A world database on actual and equilibrium

effective exchange rates. International economics. 156. pp.206-230.

Froko, N. A., 2017. Short Term Financial Leverage and Shareholders’ Wealth Maximisation of

Ghanaian Banks: New Theoretical Evidence. Structure. 8(13).

Gil, A. and et.al., 2018. Experimental analysis of the effective thermal conductivity enhancement

of PCM using finned tubes in high temperature bulk tanks. Applied Thermal

Engineering. 142. pp.736-744.

Gudkov, N., Ignatieva, K. and Ziveyi, J., 2019. Pricing of guaranteed minimum withdrawal

benefits in variable annuities under stochastic volatility, stochastic interest rates and

stochastic mortality via the componentwise splitting method. Quantitative Finance. 19(3).

pp.501-518.

Johari, M. and et.al., 2018. Bi-level credit period coordination for periodic review inventory

system with price-credit dependent demand under time value of money. Transportation

Research Part E: Logistics and Transportation Review. 114. pp.270-291.

Muda, I. and Hasibuan, A. N., 2018. Public Discovery of the Concept of Time Value of Money

with Economic Value of Time. In Proceedings of MICoMS 2017 (pp. 251-257). Emerald

Publishing Limited.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.