Business Finance (LSME505) Assignment 2: Case Study Analysis

VerifiedAdded on 2022/11/29

|10

|2556

|350

Case Study

AI Summary

This document presents a comprehensive case study analysis in business finance, addressing key concepts and calculations. It begins by calculating the payback periods and net present values (NPV) for two projects, considering a 12% cost of capital, and discusses the suitability of each project bas...

Business finance

(Assignment 2: A Case Study)

(Assignment 2: A Case Study)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Question 1........................................................................................................................................3

Question 2........................................................................................................................................5

REFERENCES..............................................................................................................................10

Question 1........................................................................................................................................3

Question 2........................................................................................................................................5

REFERENCES..............................................................................................................................10

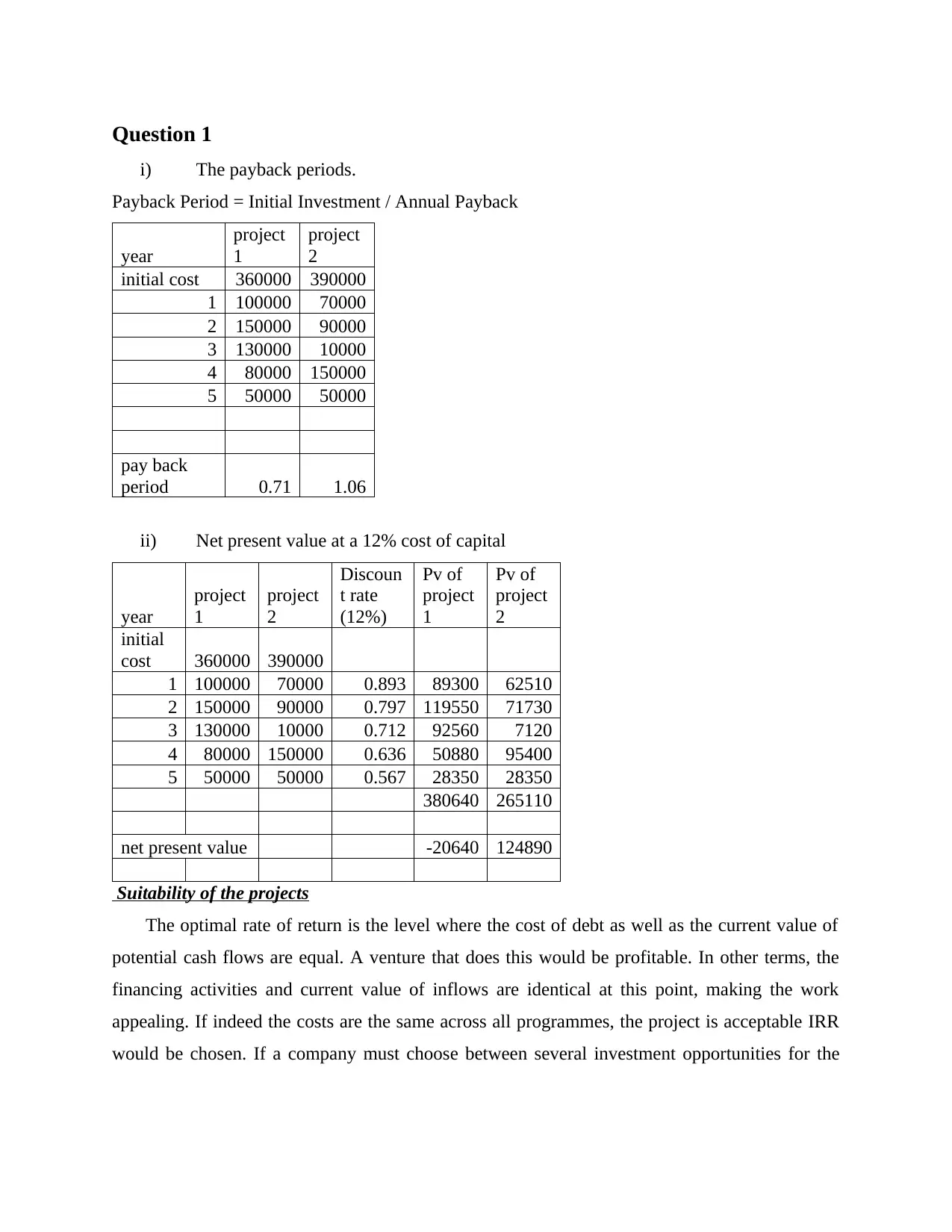

Question 1

i) The payback periods.

Payback Period = Initial Investment / Annual Payback

year

project

1

project

2

initial cost 360000 390000

1 100000 70000

2 150000 90000

3 130000 10000

4 80000 150000

5 50000 50000

pay back

period 0.71 1.06

ii) Net present value at a 12% cost of capital

year

project

1

project

2

Discoun

t rate

(12%)

Pv of

project

1

Pv of

project

2

initial

cost 360000 390000

1 100000 70000 0.893 89300 62510

2 150000 90000 0.797 119550 71730

3 130000 10000 0.712 92560 7120

4 80000 150000 0.636 50880 95400

5 50000 50000 0.567 28350 28350

380640 265110

net present value -20640 124890

Suitability of the projects

The optimal rate of return is the level where the cost of debt as well as the current value of

potential cash flows are equal. A venture that does this would be profitable. In other terms, the

financing activities and current value of inflows are identical at this point, making the work

appealing. If indeed the costs are the same across all programmes, the project is acceptable IRR

would be chosen. If a company must choose between several investment opportunities for the

i) The payback periods.

Payback Period = Initial Investment / Annual Payback

year

project

1

project

2

initial cost 360000 390000

1 100000 70000

2 150000 90000

3 130000 10000

4 80000 150000

5 50000 50000

pay back

period 0.71 1.06

ii) Net present value at a 12% cost of capital

year

project

1

project

2

Discoun

t rate

(12%)

Pv of

project

1

Pv of

project

2

initial

cost 360000 390000

1 100000 70000 0.893 89300 62510

2 150000 90000 0.797 119550 71730

3 130000 10000 0.712 92560 7120

4 80000 150000 0.636 50880 95400

5 50000 50000 0.567 28350 28350

380640 265110

net present value -20640 124890

Suitability of the projects

The optimal rate of return is the level where the cost of debt as well as the current value of

potential cash flows are equal. A venture that does this would be profitable. In other terms, the

financing activities and current value of inflows are identical at this point, making the work

appealing. If indeed the costs are the same across all programmes, the project is acceptable IRR

would be chosen. If a company must choose between several investment opportunities for the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

same cost of capital, the IRR would be used to rate the ventures to include the most successful

project. The IRR should ideally be greater than the cost of money.

In real-world settings, because any project would need a huge increase and it would have a

result and discussion, a company will use a mix of capital budgeting strategies such as NPV,

IRR, as well as payback time to choose the right project. The length of the project is not taken

into account by the IRR. For example, if an organisation would choose among two projects,

Project A with an IRR to 12% and a period of one year, and Project B with just an IRR of 12%

as well as a period of five years, and then a cost of money of 10%, both initiatives are profitable.

If the corporation chooses Project B but it does have a higher IRR, it is wrong since Project B

does have a longer length (Massa, Tucci and Afuah, 2017). The IRR is typically used to

determine the feasibility of financial products or ventures. The greater the IRR, it’s most

lucrative a financial system or enterprise is to participate throughout. Assuming that all financial

goods need the same initial investment, the item with both the acute Stress will be the better. Of

necessity, until investing, one must be aware of the risks involved. The net present value (NPV),

that is calculated by taking the present value (PV) of a project's cumulative costs and profits and

downplaying it to match potential working capital, is a critical element in determining the

crossover rate. Often businesses use present value models or diagrams to aid in decision-making.

One of two future projects is more lucrative is determined by the crossover rate. The estimation,

in particular, provides insight into another success of various programmes and balances their

future profits against risks.

The IRR is calculated using the same equation as the NPV. The NPV, on the other hand, is

replaced with zero, as well as the IRR is used in place of either the discount factor. In addition,

however unlike NPV, the IRR assumes that all cash inflows from a project is invested back in the

IRR instead of price of funds. Positive cash balances are assumed to be allocated to the IRR

throughout the formula. The IRR may recover the program's return on equity if the NPV is

exactly zero. Or, unless the return on capital is 8.5 percent as well as the NPV of the a company

is zero, their IRR for such a project would be 8.5 percent. As a result, the current value of all

currency inflows would only be enough to cover the cost of money. A negative net present value

(NPV) or an IRR well below return on capital equals zero value for the owners (Merton, 2016).

Another drawback of that same IRR would be that it takes into account the time worth of

currency and the national economy including its cash flow. IRR, on the other hand, cannot be

project. The IRR should ideally be greater than the cost of money.

In real-world settings, because any project would need a huge increase and it would have a

result and discussion, a company will use a mix of capital budgeting strategies such as NPV,

IRR, as well as payback time to choose the right project. The length of the project is not taken

into account by the IRR. For example, if an organisation would choose among two projects,

Project A with an IRR to 12% and a period of one year, and Project B with just an IRR of 12%

as well as a period of five years, and then a cost of money of 10%, both initiatives are profitable.

If the corporation chooses Project B but it does have a higher IRR, it is wrong since Project B

does have a longer length (Massa, Tucci and Afuah, 2017). The IRR is typically used to

determine the feasibility of financial products or ventures. The greater the IRR, it’s most

lucrative a financial system or enterprise is to participate throughout. Assuming that all financial

goods need the same initial investment, the item with both the acute Stress will be the better. Of

necessity, until investing, one must be aware of the risks involved. The net present value (NPV),

that is calculated by taking the present value (PV) of a project's cumulative costs and profits and

downplaying it to match potential working capital, is a critical element in determining the

crossover rate. Often businesses use present value models or diagrams to aid in decision-making.

One of two future projects is more lucrative is determined by the crossover rate. The estimation,

in particular, provides insight into another success of various programmes and balances their

future profits against risks.

The IRR is calculated using the same equation as the NPV. The NPV, on the other hand, is

replaced with zero, as well as the IRR is used in place of either the discount factor. In addition,

however unlike NPV, the IRR assumes that all cash inflows from a project is invested back in the

IRR instead of price of funds. Positive cash balances are assumed to be allocated to the IRR

throughout the formula. The IRR may recover the program's return on equity if the NPV is

exactly zero. Or, unless the return on capital is 8.5 percent as well as the NPV of the a company

is zero, their IRR for such a project would be 8.5 percent. As a result, the current value of all

currency inflows would only be enough to cover the cost of money. A negative net present value

(NPV) or an IRR well below return on capital equals zero value for the owners (Merton, 2016).

Another drawback of that same IRR would be that it takes into account the time worth of

currency and the national economy including its cash flow. IRR, on the other hand, cannot be

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

scaled or added to the valuation of owners. So, if three schemes have IRRs of 10%, 13%, and

22%, the overall IRR is indeed not exactly 45 percent. Alternatively, most of the projects' cash

flows can be averaged to calculate the right IRR, which, such as the NPV, gives no indication of

the scale of the initial investment (Nair and Reddy, 2017).

Question 2

Ratio analysis

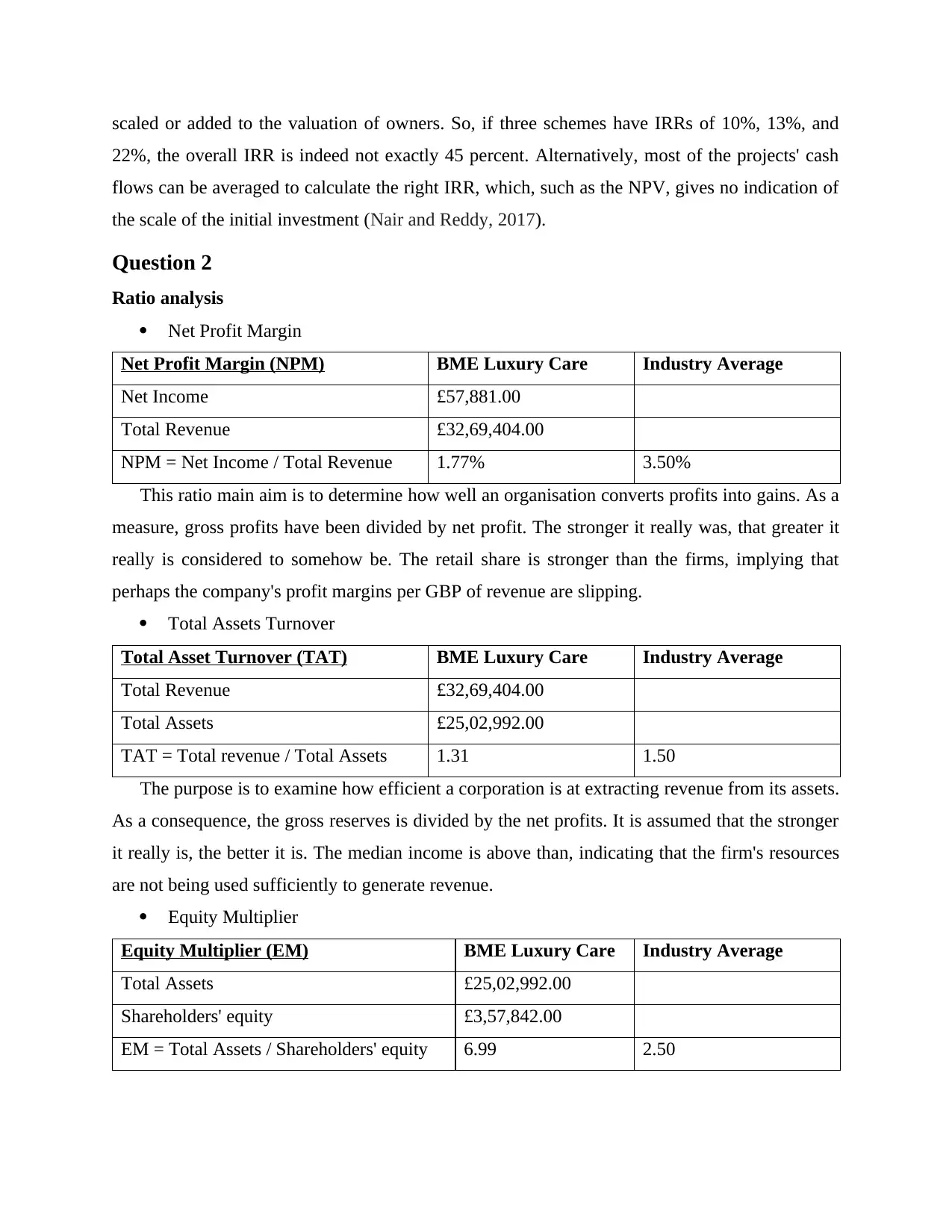

Net Profit Margin

Net Profit Margin (NPM) BME Luxury Care Industry Average

Net Income £57,881.00

Total Revenue £32,69,404.00

NPM = Net Income / Total Revenue 1.77% 3.50%

This ratio main aim is to determine how well an organisation converts profits into gains. As a

measure, gross profits have been divided by net profit. The stronger it really was, that greater it

really is considered to somehow be. The retail share is stronger than the firms, implying that

perhaps the company's profit margins per GBP of revenue are slipping.

Total Assets Turnover

Total Asset Turnover (TAT) BME Luxury Care Industry Average

Total Revenue £32,69,404.00

Total Assets £25,02,992.00

TAT = Total revenue / Total Assets 1.31 1.50

The purpose is to examine how efficient a corporation is at extracting revenue from its assets.

As a consequence, the gross reserves is divided by the net profits. It is assumed that the stronger

it really is, the better it is. The median income is above than, indicating that the firm's resources

are not being used sufficiently to generate revenue.

Equity Multiplier

Equity Multiplier (EM) BME Luxury Care Industry Average

Total Assets £25,02,992.00

Shareholders' equity £3,57,842.00

EM = Total Assets / Shareholders' equity 6.99 2.50

22%, the overall IRR is indeed not exactly 45 percent. Alternatively, most of the projects' cash

flows can be averaged to calculate the right IRR, which, such as the NPV, gives no indication of

the scale of the initial investment (Nair and Reddy, 2017).

Question 2

Ratio analysis

Net Profit Margin

Net Profit Margin (NPM) BME Luxury Care Industry Average

Net Income £57,881.00

Total Revenue £32,69,404.00

NPM = Net Income / Total Revenue 1.77% 3.50%

This ratio main aim is to determine how well an organisation converts profits into gains. As a

measure, gross profits have been divided by net profit. The stronger it really was, that greater it

really is considered to somehow be. The retail share is stronger than the firms, implying that

perhaps the company's profit margins per GBP of revenue are slipping.

Total Assets Turnover

Total Asset Turnover (TAT) BME Luxury Care Industry Average

Total Revenue £32,69,404.00

Total Assets £25,02,992.00

TAT = Total revenue / Total Assets 1.31 1.50

The purpose is to examine how efficient a corporation is at extracting revenue from its assets.

As a consequence, the gross reserves is divided by the net profits. It is assumed that the stronger

it really is, the better it is. The median income is above than, indicating that the firm's resources

are not being used sufficiently to generate revenue.

Equity Multiplier

Equity Multiplier (EM) BME Luxury Care Industry Average

Total Assets £25,02,992.00

Shareholders' equity £3,57,842.00

EM = Total Assets / Shareholders' equity 6.99 2.50

It must have been a contributing factor for determining how much of a company's assets is

funded by capital. As a result, equity and net reserves have been divided. A greater spending

ratio indicates that the investments were repaid with a substantial amount of debt. The sector

average is lower than that of the industry median, indicates that a company relies more on debt,

which really is expensive but also can contribute to bankruptcy (Naumovski, Taneski and

Dojcinovski, 2018).

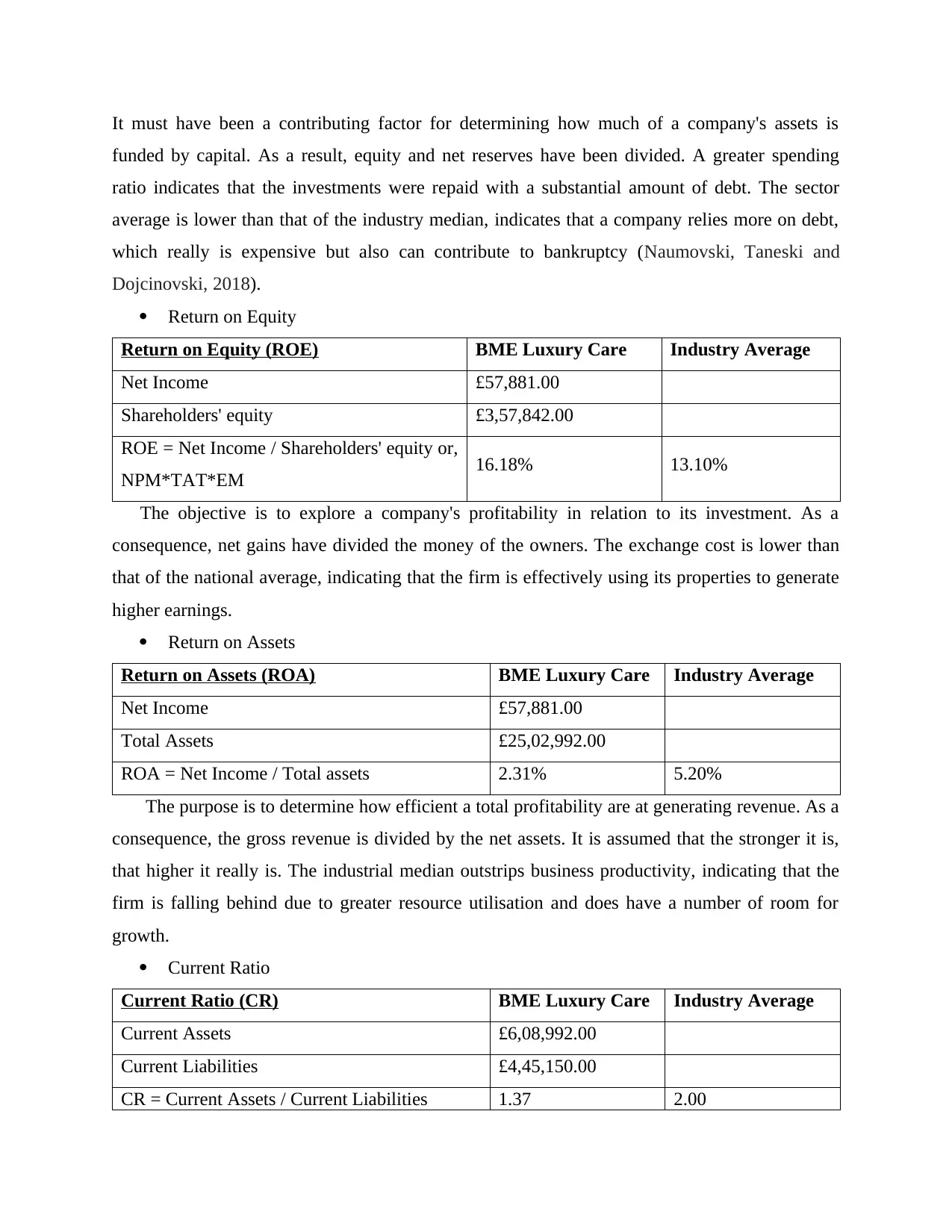

Return on Equity

Return on Equity (ROE) BME Luxury Care Industry Average

Net Income £57,881.00

Shareholders' equity £3,57,842.00

ROE = Net Income / Shareholders' equity or,

NPM*TAT*EM 16.18% 13.10%

The objective is to explore a company's profitability in relation to its investment. As a

consequence, net gains have divided the money of the owners. The exchange cost is lower than

that of the national average, indicating that the firm is effectively using its properties to generate

higher earnings.

Return on Assets

Return on Assets (ROA) BME Luxury Care Industry Average

Net Income £57,881.00

Total Assets £25,02,992.00

ROA = Net Income / Total assets 2.31% 5.20%

The purpose is to determine how efficient a total profitability are at generating revenue. As a

consequence, the gross revenue is divided by the net assets. It is assumed that the stronger it is,

that higher it really is. The industrial median outstrips business productivity, indicating that the

firm is falling behind due to greater resource utilisation and does have a number of room for

growth.

Current Ratio

Current Ratio (CR) BME Luxury Care Industry Average

Current Assets £6,08,992.00

Current Liabilities £4,45,150.00

CR = Current Assets / Current Liabilities 1.37 2.00

funded by capital. As a result, equity and net reserves have been divided. A greater spending

ratio indicates that the investments were repaid with a substantial amount of debt. The sector

average is lower than that of the industry median, indicates that a company relies more on debt,

which really is expensive but also can contribute to bankruptcy (Naumovski, Taneski and

Dojcinovski, 2018).

Return on Equity

Return on Equity (ROE) BME Luxury Care Industry Average

Net Income £57,881.00

Shareholders' equity £3,57,842.00

ROE = Net Income / Shareholders' equity or,

NPM*TAT*EM 16.18% 13.10%

The objective is to explore a company's profitability in relation to its investment. As a

consequence, net gains have divided the money of the owners. The exchange cost is lower than

that of the national average, indicating that the firm is effectively using its properties to generate

higher earnings.

Return on Assets

Return on Assets (ROA) BME Luxury Care Industry Average

Net Income £57,881.00

Total Assets £25,02,992.00

ROA = Net Income / Total assets 2.31% 5.20%

The purpose is to determine how efficient a total profitability are at generating revenue. As a

consequence, the gross revenue is divided by the net assets. It is assumed that the stronger it is,

that higher it really is. The industrial median outstrips business productivity, indicating that the

firm is falling behind due to greater resource utilisation and does have a number of room for

growth.

Current Ratio

Current Ratio (CR) BME Luxury Care Industry Average

Current Assets £6,08,992.00

Current Liabilities £4,45,150.00

CR = Current Assets / Current Liabilities 1.37 2.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

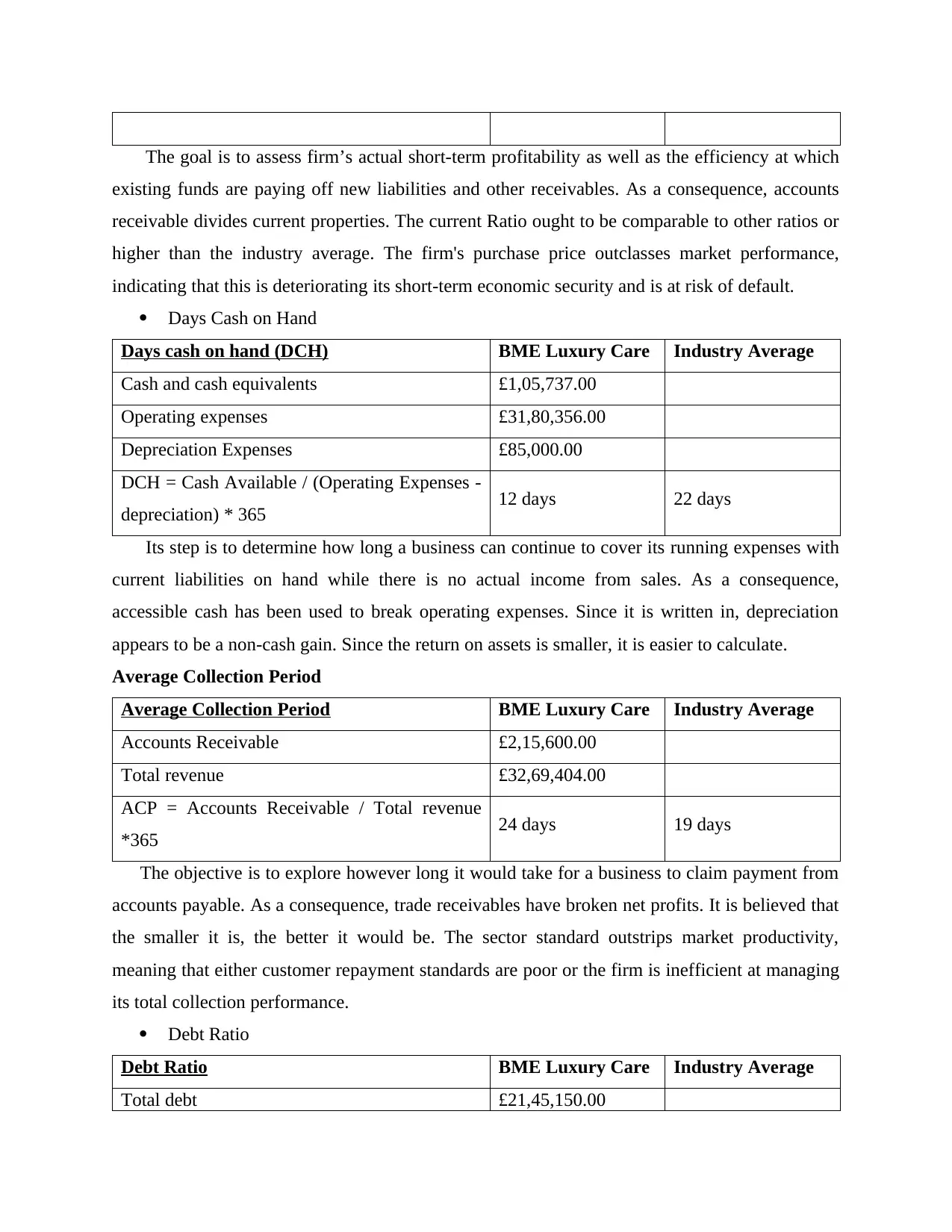

The goal is to assess firm’s actual short-term profitability as well as the efficiency at which

existing funds are paying off new liabilities and other receivables. As a consequence, accounts

receivable divides current properties. The current Ratio ought to be comparable to other ratios or

higher than the industry average. The firm's purchase price outclasses market performance,

indicating that this is deteriorating its short-term economic security and is at risk of default.

Days Cash on Hand

Days cash on hand (DCH) BME Luxury Care Industry Average

Cash and cash equivalents £1,05,737.00

Operating expenses £31,80,356.00

Depreciation Expenses £85,000.00

DCH = Cash Available / (Operating Expenses -

depreciation) * 365 12 days 22 days

Its step is to determine how long a business can continue to cover its running expenses with

current liabilities on hand while there is no actual income from sales. As a consequence,

accessible cash has been used to break operating expenses. Since it is written in, depreciation

appears to be a non-cash gain. Since the return on assets is smaller, it is easier to calculate.

Average Collection Period

Average Collection Period BME Luxury Care Industry Average

Accounts Receivable £2,15,600.00

Total revenue £32,69,404.00

ACP = Accounts Receivable / Total revenue

*365 24 days 19 days

The objective is to explore however long it would take for a business to claim payment from

accounts payable. As a consequence, trade receivables have broken net profits. It is believed that

the smaller it is, the better it would be. The sector standard outstrips market productivity,

meaning that either customer repayment standards are poor or the firm is inefficient at managing

its total collection performance.

Debt Ratio

Debt Ratio BME Luxury Care Industry Average

Total debt £21,45,150.00

existing funds are paying off new liabilities and other receivables. As a consequence, accounts

receivable divides current properties. The current Ratio ought to be comparable to other ratios or

higher than the industry average. The firm's purchase price outclasses market performance,

indicating that this is deteriorating its short-term economic security and is at risk of default.

Days Cash on Hand

Days cash on hand (DCH) BME Luxury Care Industry Average

Cash and cash equivalents £1,05,737.00

Operating expenses £31,80,356.00

Depreciation Expenses £85,000.00

DCH = Cash Available / (Operating Expenses -

depreciation) * 365 12 days 22 days

Its step is to determine how long a business can continue to cover its running expenses with

current liabilities on hand while there is no actual income from sales. As a consequence,

accessible cash has been used to break operating expenses. Since it is written in, depreciation

appears to be a non-cash gain. Since the return on assets is smaller, it is easier to calculate.

Average Collection Period

Average Collection Period BME Luxury Care Industry Average

Accounts Receivable £2,15,600.00

Total revenue £32,69,404.00

ACP = Accounts Receivable / Total revenue

*365 24 days 19 days

The objective is to explore however long it would take for a business to claim payment from

accounts payable. As a consequence, trade receivables have broken net profits. It is believed that

the smaller it is, the better it would be. The sector standard outstrips market productivity,

meaning that either customer repayment standards are poor or the firm is inefficient at managing

its total collection performance.

Debt Ratio

Debt Ratio BME Luxury Care Industry Average

Total debt £21,45,150.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

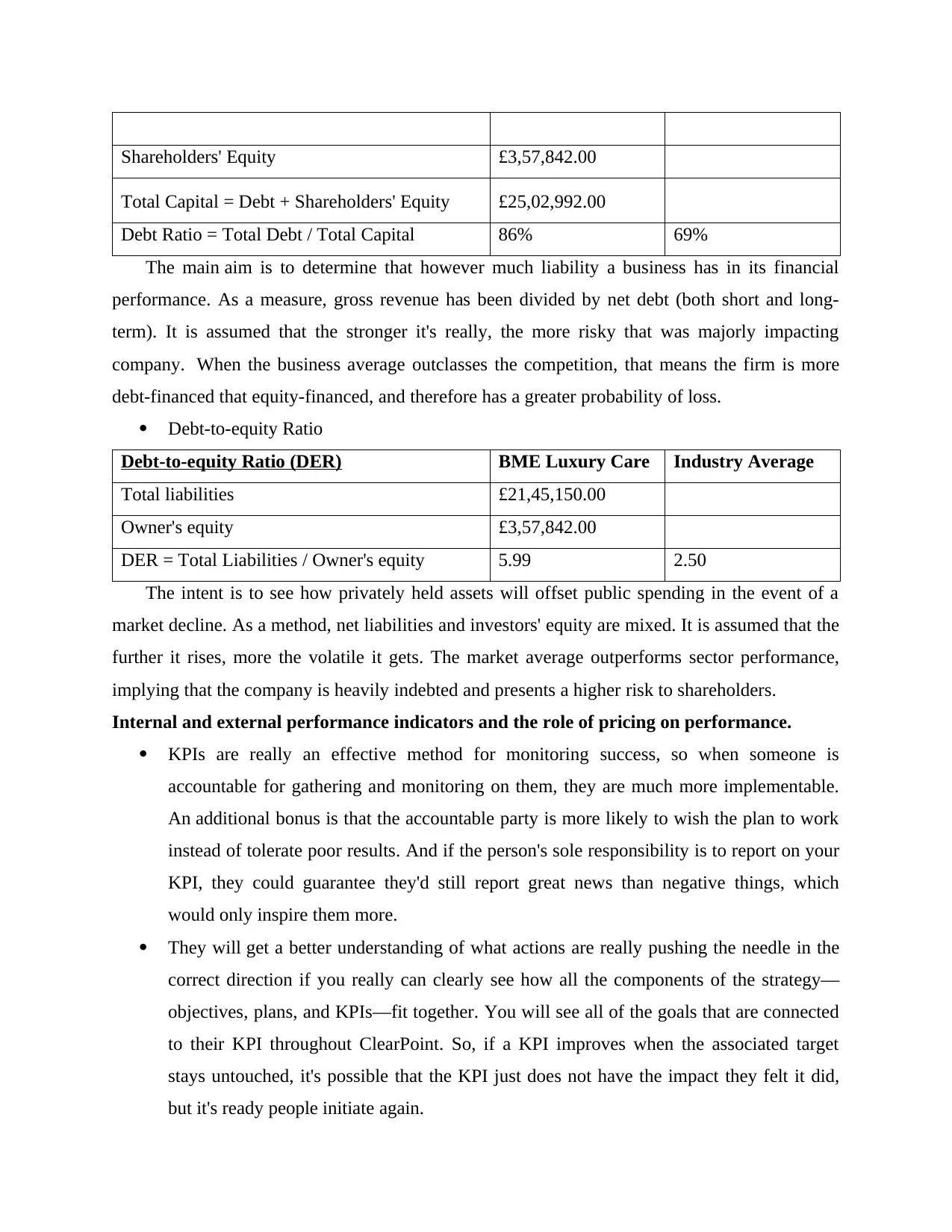

Shareholders' Equity £3,57,842.00

Total Capital = Debt + Shareholders' Equity £25,02,992.00

Debt Ratio = Total Debt / Total Capital 86% 69%

The main aim is to determine that however much liability a business has in its financial

performance. As a measure, gross revenue has been divided by net debt (both short and long-

term). It is assumed that the stronger it's really, the more risky that was majorly impacting

company. When the business average outclasses the competition, that means the firm is more

debt-financed that equity-financed, and therefore has a greater probability of loss.

Debt-to-equity Ratio

Debt-to-equity Ratio (DER) BME Luxury Care Industry Average

Total liabilities £21,45,150.00

Owner's equity £3,57,842.00

DER = Total Liabilities / Owner's equity 5.99 2.50

The intent is to see how privately held assets will offset public spending in the event of a

market decline. As a method, net liabilities and investors' equity are mixed. It is assumed that the

further it rises, more the volatile it gets. The market average outperforms sector performance,

implying that the company is heavily indebted and presents a higher risk to shareholders.

Internal and external performance indicators and the role of pricing on performance.

KPIs are really an effective method for monitoring success, so when someone is

accountable for gathering and monitoring on them, they are much more implementable.

An additional bonus is that the accountable party is more likely to wish the plan to work

instead of tolerate poor results. And if the person's sole responsibility is to report on your

KPI, they could guarantee they'd still report great news than negative things, which

would only inspire them more.

They will get a better understanding of what actions are really pushing the needle in the

correct direction if you really can clearly see how all the components of the strategy—

objectives, plans, and KPIs—fit together. You will see all of the goals that are connected

to their KPI throughout ClearPoint. So, if a KPI improves when the associated target

stays untouched, it's possible that the KPI just does not have the impact they felt it did,

but it's ready people initiate again.

Total Capital = Debt + Shareholders' Equity £25,02,992.00

Debt Ratio = Total Debt / Total Capital 86% 69%

The main aim is to determine that however much liability a business has in its financial

performance. As a measure, gross revenue has been divided by net debt (both short and long-

term). It is assumed that the stronger it's really, the more risky that was majorly impacting

company. When the business average outclasses the competition, that means the firm is more

debt-financed that equity-financed, and therefore has a greater probability of loss.

Debt-to-equity Ratio

Debt-to-equity Ratio (DER) BME Luxury Care Industry Average

Total liabilities £21,45,150.00

Owner's equity £3,57,842.00

DER = Total Liabilities / Owner's equity 5.99 2.50

The intent is to see how privately held assets will offset public spending in the event of a

market decline. As a method, net liabilities and investors' equity are mixed. It is assumed that the

further it rises, more the volatile it gets. The market average outperforms sector performance,

implying that the company is heavily indebted and presents a higher risk to shareholders.

Internal and external performance indicators and the role of pricing on performance.

KPIs are really an effective method for monitoring success, so when someone is

accountable for gathering and monitoring on them, they are much more implementable.

An additional bonus is that the accountable party is more likely to wish the plan to work

instead of tolerate poor results. And if the person's sole responsibility is to report on your

KPI, they could guarantee they'd still report great news than negative things, which

would only inspire them more.

They will get a better understanding of what actions are really pushing the needle in the

correct direction if you really can clearly see how all the components of the strategy—

objectives, plans, and KPIs—fit together. You will see all of the goals that are connected

to their KPI throughout ClearPoint. So, if a KPI improves when the associated target

stays untouched, it's possible that the KPI just does not have the impact they felt it did,

but it's ready people initiate again.

they will get a better understanding of what actions are really pushing the needle in the

correct direction if you really can clearly see how all the components of the strategic

plan, plans, and KPIs—fit together. They will see all of the goals that are connected to

their KPI throughout ClearPoint. So, if a KPI improves when the associated target stays

untouched, it's possible that the KPI just does not have the impact they felt it did, but its

ready people initiate again.

correct direction if you really can clearly see how all the components of the strategic

plan, plans, and KPIs—fit together. They will see all of the goals that are connected to

their KPI throughout ClearPoint. So, if a KPI improves when the associated target stays

untouched, it's possible that the KPI just does not have the impact they felt it did, but its

ready people initiate again.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Massa, L., Tucci, C. L. and Afuah, A., 2017. A critical assessment of business model research.

Academy of Management Annals. 11(1). pp.73-104.

Merton, R., 2016. Manifest and latent functions. Social theory re-wired: new connections to

classical and contemporary perspectives (2nd edition). New York: Routledge. pp.68-84.

Nair, J. and Reddy, D. B. S., 2017. Leveraging Enterprise Resource Planning Systems to Digitize

Business Functions. In Enterprise Information Systems and the Digitalization of

Business Functions (pp. 20-46). IGI Global.

Naumovski, T., Taneski, N. and Dojcinovski, M., 2018. Supporting Critical Business Functions

by using Public Key Infrastructure (PKI).

Schade, M. and et.al., 2016. The impact of attitude functions on luxury brand consumption: An

age-based group comparison. Journal of business research. 69(1). pp.314-322.

Steinbart, P. J. and et.al., 2018. The influence of a good relationship between the internal audit

and information security functions on information security outcomes. Accounting,

Organizations and Society. 71. pp.15-29.

Wollschlaeger, M., Sauter, T. and Jasperneite, J., 2017. The future of industrial communication:

Automation networks in the era of the internet of things and industry 4.0. IEEE

industrial electronics magazine. 11(1). pp.17-27.

Yeoh, W. and Popovič, A., 2016. Extending the understanding of critical success factors for

implementing business intelligence systems. Journal of the Association for Information

Science and Technology. 67(1). pp.134-147.

Books and Journals

Massa, L., Tucci, C. L. and Afuah, A., 2017. A critical assessment of business model research.

Academy of Management Annals. 11(1). pp.73-104.

Merton, R., 2016. Manifest and latent functions. Social theory re-wired: new connections to

classical and contemporary perspectives (2nd edition). New York: Routledge. pp.68-84.

Nair, J. and Reddy, D. B. S., 2017. Leveraging Enterprise Resource Planning Systems to Digitize

Business Functions. In Enterprise Information Systems and the Digitalization of

Business Functions (pp. 20-46). IGI Global.

Naumovski, T., Taneski, N. and Dojcinovski, M., 2018. Supporting Critical Business Functions

by using Public Key Infrastructure (PKI).

Schade, M. and et.al., 2016. The impact of attitude functions on luxury brand consumption: An

age-based group comparison. Journal of business research. 69(1). pp.314-322.

Steinbart, P. J. and et.al., 2018. The influence of a good relationship between the internal audit

and information security functions on information security outcomes. Accounting,

Organizations and Society. 71. pp.15-29.

Wollschlaeger, M., Sauter, T. and Jasperneite, J., 2017. The future of industrial communication:

Automation networks in the era of the internet of things and industry 4.0. IEEE

industrial electronics magazine. 11(1). pp.17-27.

Yeoh, W. and Popovič, A., 2016. Extending the understanding of critical success factors for

implementing business intelligence systems. Journal of the Association for Information

Science and Technology. 67(1). pp.134-147.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.