Business Finance: Cash Conversion Cycle, NPV, IRR, Rights Issue

Added on 2023-01-05

15 Pages2880 Words44 Views

Business

Finance

Finance

Table of Contents

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

A. The length of cash conversion cycle and its significance to the company:............................1

B. should it accept the offer:........................................................................................................2

QUESTION 2...................................................................................................................................2

A. Net present value:....................................................................................................................2

B. Internal rate of return:.............................................................................................................3

C. Increase in cost of capital in year 5:........................................................................................4

QUESTION 3 ..................................................................................................................................5

A. The theoretical ex- rights price per share:...............................................................................5

B. The net cash raised:.................................................................................................................6

C. The value of the rights:............................................................................................................6

D. Advantage and disadvantage of right issue:............................................................................7

QUESTION 4...................................................................................................................................7

A. The company's weighted average cost of capital using market weightings:..........................7

B. Discussion of integration a sensible level of gearing into their capital structure, can

minimise their weighted average cost of capital:.........................................................................8

CONCLUSION................................................................................................................................8

REFRENCES.................................................................................................................................10

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

A. The length of cash conversion cycle and its significance to the company:............................1

B. should it accept the offer:........................................................................................................2

QUESTION 2...................................................................................................................................2

A. Net present value:....................................................................................................................2

B. Internal rate of return:.............................................................................................................3

C. Increase in cost of capital in year 5:........................................................................................4

QUESTION 3 ..................................................................................................................................5

A. The theoretical ex- rights price per share:...............................................................................5

B. The net cash raised:.................................................................................................................6

C. The value of the rights:............................................................................................................6

D. Advantage and disadvantage of right issue:............................................................................7

QUESTION 4...................................................................................................................................7

A. The company's weighted average cost of capital using market weightings:..........................7

B. Discussion of integration a sensible level of gearing into their capital structure, can

minimise their weighted average cost of capital:.........................................................................8

CONCLUSION................................................................................................................................8

REFRENCES.................................................................................................................................10

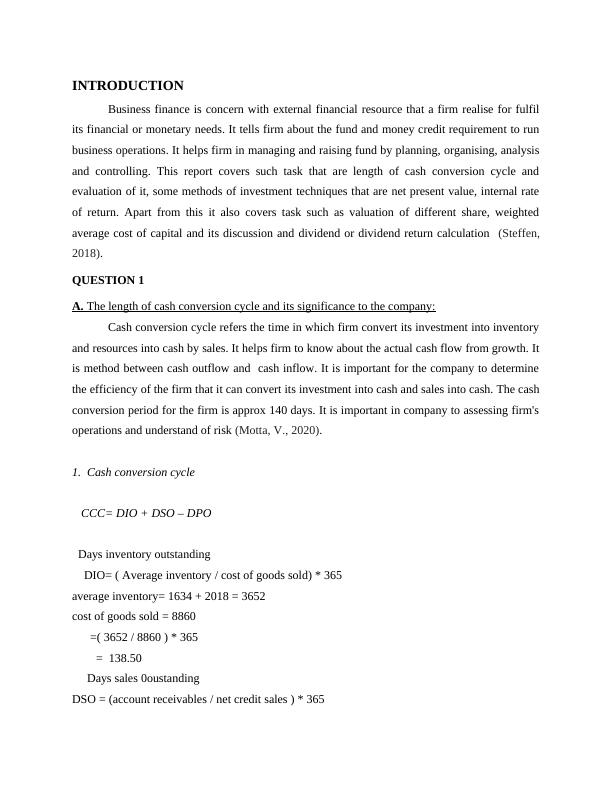

INTRODUCTION

Business finance is concern with external financial resource that a firm realise for fulfil

its financial or monetary needs. It tells firm about the fund and money credit requirement to run

business operations. It helps firm in managing and raising fund by planning, organising, analysis

and controlling. This report covers such task that are length of cash conversion cycle and

evaluation of it, some methods of investment techniques that are net present value, internal rate

of return. Apart from this it also covers task such as valuation of different share, weighted

average cost of capital and its discussion and dividend or dividend return calculation (Steffen,

2018).

QUESTION 1

A. The length of cash conversion cycle and its significance to the company:

Cash conversion cycle refers the time in which firm convert its investment into inventory

and resources into cash by sales. It helps firm to know about the actual cash flow from growth. It

is method between cash outflow and cash inflow. It is important for the company to determine

the efficiency of the firm that it can convert its investment into cash and sales into cash. The cash

conversion period for the firm is approx 140 days. It is important in company to assessing firm's

operations and understand of risk (Motta, V., 2020).

1. Cash conversion cycle

CCC= DIO + DSO – DPO

Days inventory outstanding

DIO= ( Average inventory / cost of goods sold) * 365

average inventory= 1634 + 2018 = 3652

cost of goods sold = 8860

=( 3652 / 8860 ) * 365

= 138.50

Days sales 0oustanding

DSO = (account receivables / net credit sales ) * 365

Business finance is concern with external financial resource that a firm realise for fulfil

its financial or monetary needs. It tells firm about the fund and money credit requirement to run

business operations. It helps firm in managing and raising fund by planning, organising, analysis

and controlling. This report covers such task that are length of cash conversion cycle and

evaluation of it, some methods of investment techniques that are net present value, internal rate

of return. Apart from this it also covers task such as valuation of different share, weighted

average cost of capital and its discussion and dividend or dividend return calculation (Steffen,

2018).

QUESTION 1

A. The length of cash conversion cycle and its significance to the company:

Cash conversion cycle refers the time in which firm convert its investment into inventory

and resources into cash by sales. It helps firm to know about the actual cash flow from growth. It

is method between cash outflow and cash inflow. It is important for the company to determine

the efficiency of the firm that it can convert its investment into cash and sales into cash. The cash

conversion period for the firm is approx 140 days. It is important in company to assessing firm's

operations and understand of risk (Motta, V., 2020).

1. Cash conversion cycle

CCC= DIO + DSO – DPO

Days inventory outstanding

DIO= ( Average inventory / cost of goods sold) * 365

average inventory= 1634 + 2018 = 3652

cost of goods sold = 8860

=( 3652 / 8860 ) * 365

= 138.50

Days sales 0oustanding

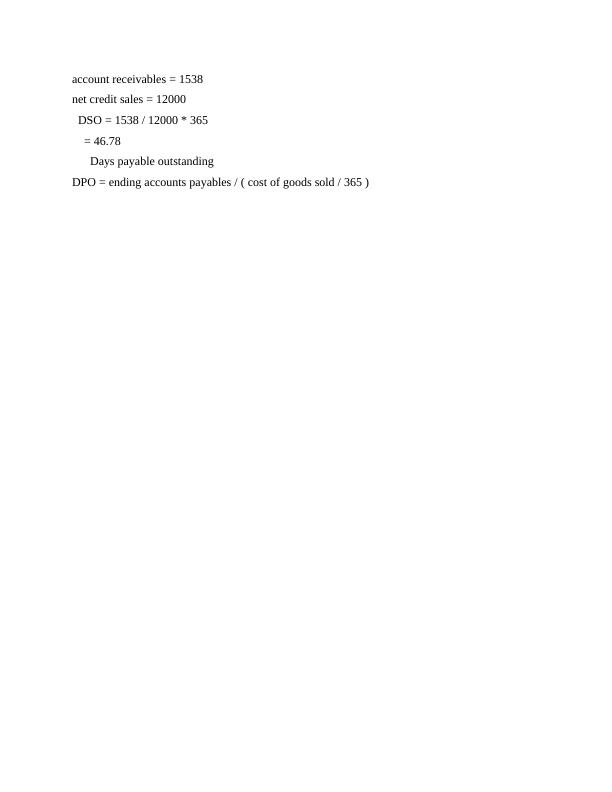

DSO = (account receivables / net credit sales ) * 365

account receivables = 1538

net credit sales = 12000

DSO = 1538 / 12000 * 365

= 46.78

Days payable outstanding

DPO = ending accounts payables / ( cost of goods sold / 365 )

net credit sales = 12000

DSO = 1538 / 12000 * 365

= 46.78

Days payable outstanding

DPO = ending accounts payables / ( cost of goods sold / 365 )

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Business Financelg...

|20

|3128

|106

Analysis of Working capital managementlg...

|9

|2114

|307

Cash Conversion Cycle Case Study 2022lg...

|7

|1230

|25

A case study on the financial management of an organisationlg...

|11

|2799

|237

(solved) Assignment on Corporate Financelg...

|7

|1179

|295

Financial and Non-Financial Analysis of JB Hi Filg...

|4

|1137

|375