Business Finance: Calculation of Break-Even Point, Margins, and Profit

Added on 2023-06-10

12 Pages2690 Words257 Views

Business Finance

Table of Contents

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

Calculation of contribution per unit, break-even point in units and monetary terms, margin of

safety in percentage......................................................................................................................3

Calculating number of units to be sold for gaining desired profit...............................................4

Preparing memo for the Financial Manager................................................................................4

Using Marginal and absorption costing for profit calculation.....................................................5

PART B............................................................................................................................................6

Demonstrating the understanding of standard costing system and variance analysis.................6

Calculating variances...................................................................................................................7

Preparing budget for 10000 units.................................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

Calculation of contribution per unit, break-even point in units and monetary terms, margin of

safety in percentage......................................................................................................................3

Calculating number of units to be sold for gaining desired profit...............................................4

Preparing memo for the Financial Manager................................................................................4

Using Marginal and absorption costing for profit calculation.....................................................5

PART B............................................................................................................................................6

Demonstrating the understanding of standard costing system and variance analysis.................6

Calculating variances...................................................................................................................7

Preparing budget for 10000 units.................................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES................................................................................................................................1

INTRODUCTION

Business Finance refers to the process by which companies raise and manages the funds

for the business enterprise operations. The report will calculate the contribution per unit for

Lobelia Ltd. Break even point both in units and sales will be calculated in the report for the firm.

Further the report will calculate the margin of safety in percentage to budgeted sales of the

enterprise. The firm desires to earn a profit of £700,000, the will do the required calculation to

find out the number of units the firm need to sale for attaining desired profit. In addition, the

report will prepare a memo for the financial manager of Lobelia Ltd. The report will highlight

the profit calculation based on marginal and absorption costing methodologies. Through the

report significance of standard costing system and variance analysis will be outlined.

PART A

Calculation of contribution per unit, break-even point in units and monetary terms, margin of

safety in percentage

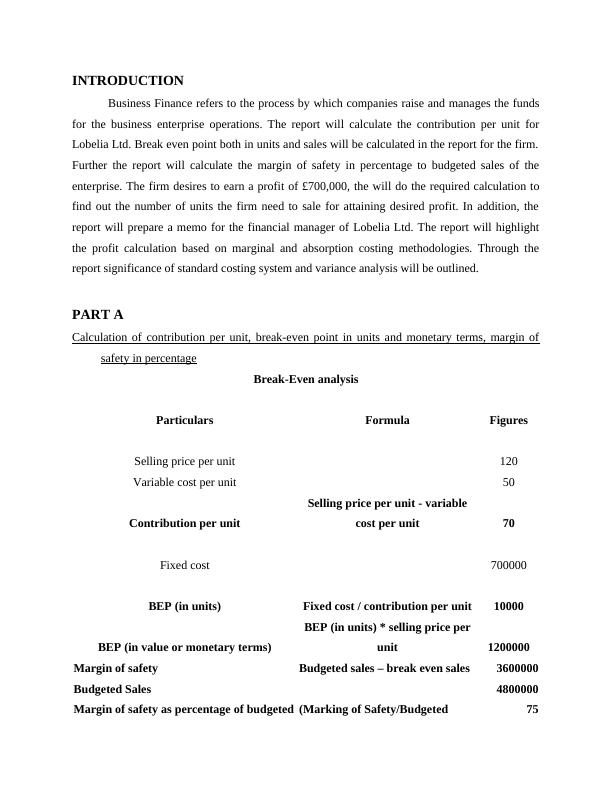

Break-Even analysis

Particulars Formula Figures

Selling price per unit 120

Variable cost per unit 50

Contribution per unit

Selling price per unit - variable

cost per unit 70

Fixed cost 700000

BEP (in units) Fixed cost / contribution per unit 10000

BEP (in value or monetary terms)

BEP (in units) * selling price per

unit 1200000

Margin of safety Budgeted sales – break even sales 3600000

Budgeted Sales 4800000

Margin of safety as percentage of budgeted (Marking of Safety/Budgeted 75

Business Finance refers to the process by which companies raise and manages the funds

for the business enterprise operations. The report will calculate the contribution per unit for

Lobelia Ltd. Break even point both in units and sales will be calculated in the report for the firm.

Further the report will calculate the margin of safety in percentage to budgeted sales of the

enterprise. The firm desires to earn a profit of £700,000, the will do the required calculation to

find out the number of units the firm need to sale for attaining desired profit. In addition, the

report will prepare a memo for the financial manager of Lobelia Ltd. The report will highlight

the profit calculation based on marginal and absorption costing methodologies. Through the

report significance of standard costing system and variance analysis will be outlined.

PART A

Calculation of contribution per unit, break-even point in units and monetary terms, margin of

safety in percentage

Break-Even analysis

Particulars Formula Figures

Selling price per unit 120

Variable cost per unit 50

Contribution per unit

Selling price per unit - variable

cost per unit 70

Fixed cost 700000

BEP (in units) Fixed cost / contribution per unit 10000

BEP (in value or monetary terms)

BEP (in units) * selling price per

unit 1200000

Margin of safety Budgeted sales – break even sales 3600000

Budgeted Sales 4800000

Margin of safety as percentage of budgeted (Marking of Safety/Budgeted 75

sales Sales)*100

Breakeven Analysis is used for calculating the number of unit a firm must sell in order to

recover all the costs it has incurred on production process. It is a situation of no profit and no

loss. After attaining the breakeven point the firm starts earning profits. Breakeven point can be

calculated in number of units and in monetary terms. Monetary terms gives the amount for sales.

From the above calculation it is interpreted that Lobelia Ltd's breakeven point in units is 10000.

It means that the firm has to sell 10000 units for reaching the position of no profit and no profit

loss (Haloho, 2021). The firm on selling 10000 units will earn £1200000 as its sales revenue.

After selling the breakeven units the firm will start earning the profits as all its fixed and variable

costs will be covered. Margin of safety is calculated by subtracting the break even sales from the

budgeted sales. The margin of safety for Lobelia ltd is 3600000. The margin of safety as the

percentage of budgeted sales is 75%. Margin of safety in percentage is calculated by dividing the

margin of safety value with budget sales of Lobelia Ltd. multiplied by 100.

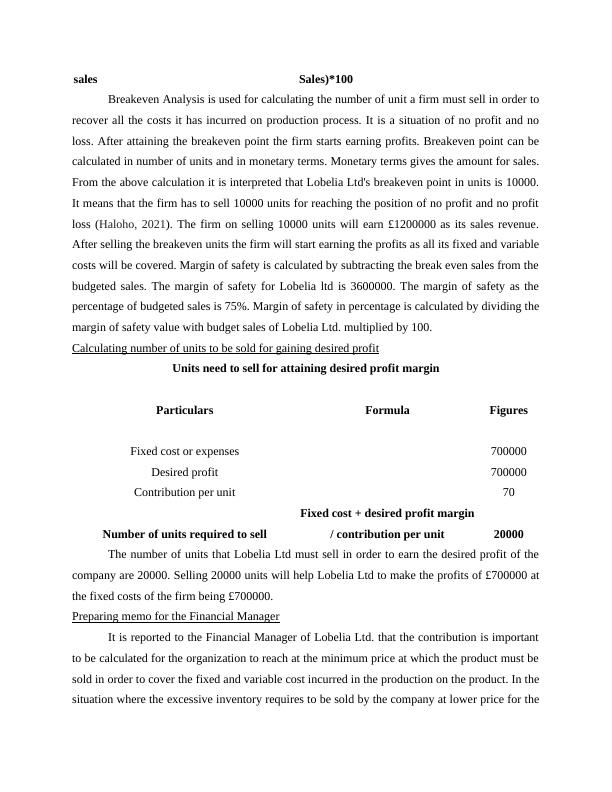

Calculating number of units to be sold for gaining desired profit

Units need to sell for attaining desired profit margin

Particulars Formula Figures

Fixed cost or expenses 700000

Desired profit 700000

Contribution per unit 70

Number of units required to sell

Fixed cost + desired profit margin

/ contribution per unit 20000

The number of units that Lobelia Ltd must sell in order to earn the desired profit of the

company are 20000. Selling 20000 units will help Lobelia Ltd to make the profits of £700000 at

the fixed costs of the firm being £700000.

Preparing memo for the Financial Manager

It is reported to the Financial Manager of Lobelia Ltd. that the contribution is important

to be calculated for the organization to reach at the minimum price at which the product must be

sold in order to cover the fixed and variable cost incurred in the production on the product. In the

situation where the excessive inventory requires to be sold by the company at lower price for the

Breakeven Analysis is used for calculating the number of unit a firm must sell in order to

recover all the costs it has incurred on production process. It is a situation of no profit and no

loss. After attaining the breakeven point the firm starts earning profits. Breakeven point can be

calculated in number of units and in monetary terms. Monetary terms gives the amount for sales.

From the above calculation it is interpreted that Lobelia Ltd's breakeven point in units is 10000.

It means that the firm has to sell 10000 units for reaching the position of no profit and no profit

loss (Haloho, 2021). The firm on selling 10000 units will earn £1200000 as its sales revenue.

After selling the breakeven units the firm will start earning the profits as all its fixed and variable

costs will be covered. Margin of safety is calculated by subtracting the break even sales from the

budgeted sales. The margin of safety for Lobelia ltd is 3600000. The margin of safety as the

percentage of budgeted sales is 75%. Margin of safety in percentage is calculated by dividing the

margin of safety value with budget sales of Lobelia Ltd. multiplied by 100.

Calculating number of units to be sold for gaining desired profit

Units need to sell for attaining desired profit margin

Particulars Formula Figures

Fixed cost or expenses 700000

Desired profit 700000

Contribution per unit 70

Number of units required to sell

Fixed cost + desired profit margin

/ contribution per unit 20000

The number of units that Lobelia Ltd must sell in order to earn the desired profit of the

company are 20000. Selling 20000 units will help Lobelia Ltd to make the profits of £700000 at

the fixed costs of the firm being £700000.

Preparing memo for the Financial Manager

It is reported to the Financial Manager of Lobelia Ltd. that the contribution is important

to be calculated for the organization to reach at the minimum price at which the product must be

sold in order to cover the fixed and variable cost incurred in the production on the product. In the

situation where the excessive inventory requires to be sold by the company at lower price for the

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Business Finance Case Study 1: Contribution, Break Even, Margin of Safety, Profit, Costing Methods, Variance Analysis, Budgetinglg...

|12

|2611

|161

Business Finance: Breakeven Analysis, Costing Systems, and Budgeting Practiceslg...

|13

|2656

|252

Business Finance: Cost Estimation and Investment Assessment Approacheslg...

|12

|2814

|301

Corporate Finance: Cost Estimating and Investment Assessment Methodologieslg...

|11

|2681

|456

Business Financelg...

|23

|5468

|265

Managing Finance and Cost in Business: A Case Studylg...

|10

|2148

|33