Business Finance: Profit, Cash Flow, Working Capital, and Cash Budget

VerifiedAdded on 2022/12/26

|12

|3098

|42

AI Summary

This document provides an overview of business finance, focusing on profit, cash flow, working capital, and cash budget. It explains the differences between profit and cash flow, and the impact of changes in working capital on a business organization. It also offers recommendations for effective working capital management. Additionally, it includes a case study on Thorne Estates and the preparation of a monthly cash budget.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Business Finance

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

EXECUTIVE SUMMARY.............................................................................................................1

TASK 1............................................................................................................................................1

1) A) Meaning of profit and cash flow and description of their difference................................1

B) Explanation of working capital, receivables, payables and inventory...................................2

C) Explanation of changes in working capital effect cash flow..................................................3

2) Impact of changes in working capital on business organization............................................3

3) Recommendation related to effective working capital management......................................4

TASK 2............................................................................................................................................5

EXECUTIVE SUMMARY.............................................................................................................5

1. Prepare a monthly cash budget...............................................................................................5

2. Observation and recommendations make to management of Thorne Estates.........................6

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................8

APPENDIX......................................................................................................................................9

EXECUTIVE SUMMARY.............................................................................................................1

TASK 1............................................................................................................................................1

1) A) Meaning of profit and cash flow and description of their difference................................1

B) Explanation of working capital, receivables, payables and inventory...................................2

C) Explanation of changes in working capital effect cash flow..................................................3

2) Impact of changes in working capital on business organization............................................3

3) Recommendation related to effective working capital management......................................4

TASK 2............................................................................................................................................5

EXECUTIVE SUMMARY.............................................................................................................5

1. Prepare a monthly cash budget...............................................................................................5

2. Observation and recommendations make to management of Thorne Estates.........................6

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................8

APPENDIX......................................................................................................................................9

EXECUTIVE SUMMARY

Financing is a procedure of providing funds for various operational activities, making

purchase or investing. Business finance is a term in which raising and arranging of funds by

business entity. For this require to proper planning, analysis and control operations that mainly

related to top of the organizational structure of an entity (Paolone, 2020). It is known as an

approach that is based on the funding and credit which are utilised in an entity. To better

understand the concept of Business finance selected Trends Ltd which is a manufacturing firm

and selling out clothes and accessories for gym. In this report covers various topics like profit,

cash flow, working capital, receivables and payables. Along with provide appropriate

recommendations in the context of proper management of working capital.

TASK 1

1) A) Meaning of profit and cash flow and description of their difference

Profit: This term is defined as financial benefit realized if revenues generated from a

business operation exceeds the expenditure, costs and taxes consist in sustaining the activity in

question. It is essential part of any business that use to present financial performance of

company. On the basis of profitability an organisation can take investment decisions and attract

investors for the investment. It shows growth and strong performance status of running business

entity whether it is financial or non-financial.

Cash flow: It defines the net amount of cash that an organisation receives and pay out a

period of time. An effective stage of cash flow must be managed for an organisation to remain in

entity on the other side positive cash flows are required to generate value for investors.

Whenever time period is over so cash flow is tracked by the mainly a standard reporting period

like monthly, quarter or year basis. It has been categorised into three parts such as, operational,

financing and investing activities (Mian and Sufi, 2018).

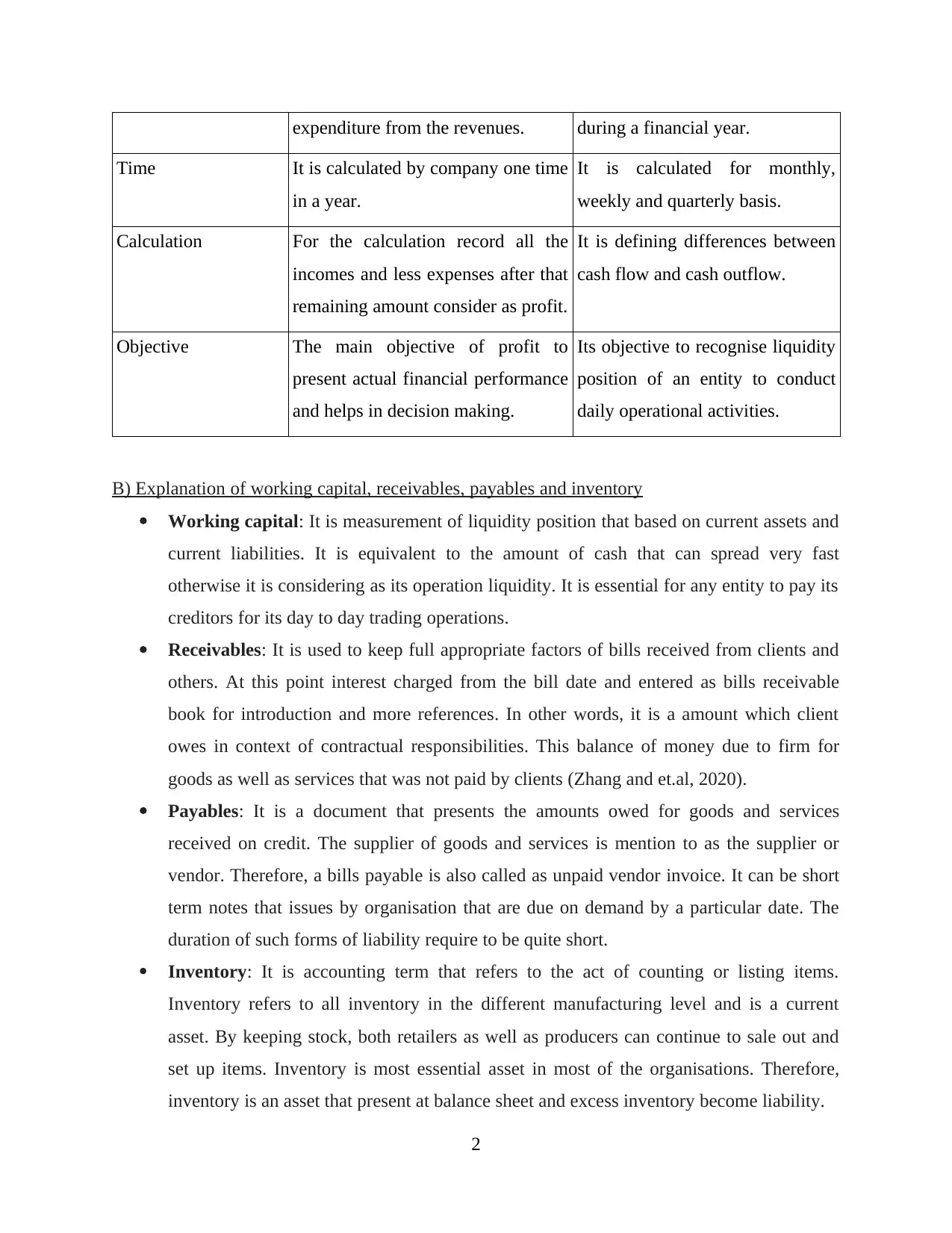

Difference between profit and cash flow

Particular Profit Cash flow

Meaning It is a net amount that generate by

the company after deduction all the

It is related with amount that

flows into as well as out of entity

1

Financing is a procedure of providing funds for various operational activities, making

purchase or investing. Business finance is a term in which raising and arranging of funds by

business entity. For this require to proper planning, analysis and control operations that mainly

related to top of the organizational structure of an entity (Paolone, 2020). It is known as an

approach that is based on the funding and credit which are utilised in an entity. To better

understand the concept of Business finance selected Trends Ltd which is a manufacturing firm

and selling out clothes and accessories for gym. In this report covers various topics like profit,

cash flow, working capital, receivables and payables. Along with provide appropriate

recommendations in the context of proper management of working capital.

TASK 1

1) A) Meaning of profit and cash flow and description of their difference

Profit: This term is defined as financial benefit realized if revenues generated from a

business operation exceeds the expenditure, costs and taxes consist in sustaining the activity in

question. It is essential part of any business that use to present financial performance of

company. On the basis of profitability an organisation can take investment decisions and attract

investors for the investment. It shows growth and strong performance status of running business

entity whether it is financial or non-financial.

Cash flow: It defines the net amount of cash that an organisation receives and pay out a

period of time. An effective stage of cash flow must be managed for an organisation to remain in

entity on the other side positive cash flows are required to generate value for investors.

Whenever time period is over so cash flow is tracked by the mainly a standard reporting period

like monthly, quarter or year basis. It has been categorised into three parts such as, operational,

financing and investing activities (Mian and Sufi, 2018).

Difference between profit and cash flow

Particular Profit Cash flow

Meaning It is a net amount that generate by

the company after deduction all the

It is related with amount that

flows into as well as out of entity

1

expenditure from the revenues. during a financial year.

Time It is calculated by company one time

in a year.

It is calculated for monthly,

weekly and quarterly basis.

Calculation For the calculation record all the

incomes and less expenses after that

remaining amount consider as profit.

It is defining differences between

cash flow and cash outflow.

Objective The main objective of profit to

present actual financial performance

and helps in decision making.

Its objective to recognise liquidity

position of an entity to conduct

daily operational activities.

B) Explanation of working capital, receivables, payables and inventory

Working capital: It is measurement of liquidity position that based on current assets and

current liabilities. It is equivalent to the amount of cash that can spread very fast

otherwise it is considering as its operation liquidity. It is essential for any entity to pay its

creditors for its day to day trading operations.

Receivables: It is used to keep full appropriate factors of bills received from clients and

others. At this point interest charged from the bill date and entered as bills receivable

book for introduction and more references. In other words, it is a amount which client

owes in context of contractual responsibilities. This balance of money due to firm for

goods as well as services that was not paid by clients (Zhang and et.al, 2020).

Payables: It is a document that presents the amounts owed for goods and services

received on credit. The supplier of goods and services is mention to as the supplier or

vendor. Therefore, a bills payable is also called as unpaid vendor invoice. It can be short

term notes that issues by organisation that are due on demand by a particular date. The

duration of such forms of liability require to be quite short.

Inventory: It is accounting term that refers to the act of counting or listing items.

Inventory refers to all inventory in the different manufacturing level and is a current

asset. By keeping stock, both retailers as well as producers can continue to sale out and

set up items. Inventory is most essential asset in most of the organisations. Therefore,

inventory is an asset that present at balance sheet and excess inventory become liability.

2

Time It is calculated by company one time

in a year.

It is calculated for monthly,

weekly and quarterly basis.

Calculation For the calculation record all the

incomes and less expenses after that

remaining amount consider as profit.

It is defining differences between

cash flow and cash outflow.

Objective The main objective of profit to

present actual financial performance

and helps in decision making.

Its objective to recognise liquidity

position of an entity to conduct

daily operational activities.

B) Explanation of working capital, receivables, payables and inventory

Working capital: It is measurement of liquidity position that based on current assets and

current liabilities. It is equivalent to the amount of cash that can spread very fast

otherwise it is considering as its operation liquidity. It is essential for any entity to pay its

creditors for its day to day trading operations.

Receivables: It is used to keep full appropriate factors of bills received from clients and

others. At this point interest charged from the bill date and entered as bills receivable

book for introduction and more references. In other words, it is a amount which client

owes in context of contractual responsibilities. This balance of money due to firm for

goods as well as services that was not paid by clients (Zhang and et.al, 2020).

Payables: It is a document that presents the amounts owed for goods and services

received on credit. The supplier of goods and services is mention to as the supplier or

vendor. Therefore, a bills payable is also called as unpaid vendor invoice. It can be short

term notes that issues by organisation that are due on demand by a particular date. The

duration of such forms of liability require to be quite short.

Inventory: It is accounting term that refers to the act of counting or listing items.

Inventory refers to all inventory in the different manufacturing level and is a current

asset. By keeping stock, both retailers as well as producers can continue to sale out and

set up items. Inventory is most essential asset in most of the organisations. Therefore,

inventory is an asset that present at balance sheet and excess inventory become liability.

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

C) Explanation of changes in working capital effect cash flow

Working capital is defined the differences between current assets and current liabilities

that will know as net working capital of an entity. This term is mainly affected to cash flow

whenever transactions in current assets and current liabilities by same amount then there will be

no charges is working capital. When an entity collected cash in brief time period so that has to be

paid in 60 days than there is increasing the statement of cash flow. On the other side, when entity

busy any machinery so deduct cash so working capital presents in decreasing manner. Thus,

changes in cash activities impact on the working capital because it is based on daily operational

activities and both are considering under current assets (Lau, Simonetti, Trinugroho and Tan,

2020).

2) Impact of changes in working capital on business organization

Trends Ltd is a production organisation that manufacturer gym cloths and footwear that

supplies by companies to different firm and also design according to their requirement under

their own brands. An entity has been accomplished turnover in excess of 300 Pounds dollar.

There are carrying out different financial results that can be managed by company:

Profit: Trend limited has generated profit of 60 million Pound in last year that can present

their effective financial situation to handle different business activities. To know accurate

amount of profit less amount of tax liability and interest that will help to determine actual

position and take investment decision in regard of future.

Cash flow: For better cash flow management Trend limited can use effective policies and

strategies like offering discounts on products to clear out its debts and manage

statements. Through cash flow know cash position and manage liquidity effectively.

Payable: An organisation requires enhancing the amount of current assets because it also

increase amount of current liabilities as they required enough amount of money to pay of

the liability. Such as, trend Ltd has enhanced to 95 million pounds from 60 million pound

year before so it presents that organisation is accountable to pay its debt more than

before. Therefore, the manager of an entity has looking for investors in regard of

investment that might deduct the debt in an entity.

Working capital: It is presenting daily operations so liquidity of business based on this

term that conduct profitability of an entity. Ratio in working capital deduct because of

3

Working capital is defined the differences between current assets and current liabilities

that will know as net working capital of an entity. This term is mainly affected to cash flow

whenever transactions in current assets and current liabilities by same amount then there will be

no charges is working capital. When an entity collected cash in brief time period so that has to be

paid in 60 days than there is increasing the statement of cash flow. On the other side, when entity

busy any machinery so deduct cash so working capital presents in decreasing manner. Thus,

changes in cash activities impact on the working capital because it is based on daily operational

activities and both are considering under current assets (Lau, Simonetti, Trinugroho and Tan,

2020).

2) Impact of changes in working capital on business organization

Trends Ltd is a production organisation that manufacturer gym cloths and footwear that

supplies by companies to different firm and also design according to their requirement under

their own brands. An entity has been accomplished turnover in excess of 300 Pounds dollar.

There are carrying out different financial results that can be managed by company:

Profit: Trend limited has generated profit of 60 million Pound in last year that can present

their effective financial situation to handle different business activities. To know accurate

amount of profit less amount of tax liability and interest that will help to determine actual

position and take investment decision in regard of future.

Cash flow: For better cash flow management Trend limited can use effective policies and

strategies like offering discounts on products to clear out its debts and manage

statements. Through cash flow know cash position and manage liquidity effectively.

Payable: An organisation requires enhancing the amount of current assets because it also

increase amount of current liabilities as they required enough amount of money to pay of

the liability. Such as, trend Ltd has enhanced to 95 million pounds from 60 million pound

year before so it presents that organisation is accountable to pay its debt more than

before. Therefore, the manager of an entity has looking for investors in regard of

investment that might deduct the debt in an entity.

Working capital: It is presenting daily operations so liquidity of business based on this

term that conduct profitability of an entity. Ratio in working capital deduct because of

3

loosing future clients and low supply in the raw material to its suppliers. In the Trend

limited the amount of working capital can be operated by effective delivery of supply and

on time payment from supplier to assure for the effective balance in working capital. To

enhance the current asset in entity require keeping the balance of cash.

Receivable: Tketchers Ltd and Sadidas Ltd are two main clients that are controlled by

Arpha who has 30% of total shares as well as 70% has to family members.

3) Recommendation related to effective working capital management

Working capital management is essential tool the supports to an organisation to make

efficient use of current assets that supports business to manage cash flow activities. Working

capital financing is required to reinforce cash flow by increasing the way to manage working

capital. It is important to produce cash flow in the management of an entity. Trend Ltd can use

particular way to maintain cash flow is:

Develop cash budget: It is a good method to manage cash flow in proper manner because

in this budget record all the transactions that conduct in cash. It will interpret effective

position of cash outflow as well as inflow that supports entity to take right decisions in

regard future and take measurable action. It is utilised by cash manager in order to help

them to make strategies and policies.

Review of supply and inventory: The cash flow activities based on the working capital

that could be use by an entity to enhance its cash flow through effective supply of stock.

Along with it will increase the effectiveness in an entity and assure the worthiness of an

entity and will deduct the chances of dispute with the loyal provider as it occurs with

Trend Ltd. Along with they will ensure that an entity is effectively supplying its stock on

particular time to enhance the cash flow of firm.

Predication of cash flow: By effective cash flow like receivables as well as payables in an

entity will assist in effective manner in the context of investment and other required

operations.

4

limited the amount of working capital can be operated by effective delivery of supply and

on time payment from supplier to assure for the effective balance in working capital. To

enhance the current asset in entity require keeping the balance of cash.

Receivable: Tketchers Ltd and Sadidas Ltd are two main clients that are controlled by

Arpha who has 30% of total shares as well as 70% has to family members.

3) Recommendation related to effective working capital management

Working capital management is essential tool the supports to an organisation to make

efficient use of current assets that supports business to manage cash flow activities. Working

capital financing is required to reinforce cash flow by increasing the way to manage working

capital. It is important to produce cash flow in the management of an entity. Trend Ltd can use

particular way to maintain cash flow is:

Develop cash budget: It is a good method to manage cash flow in proper manner because

in this budget record all the transactions that conduct in cash. It will interpret effective

position of cash outflow as well as inflow that supports entity to take right decisions in

regard future and take measurable action. It is utilised by cash manager in order to help

them to make strategies and policies.

Review of supply and inventory: The cash flow activities based on the working capital

that could be use by an entity to enhance its cash flow through effective supply of stock.

Along with it will increase the effectiveness in an entity and assure the worthiness of an

entity and will deduct the chances of dispute with the loyal provider as it occurs with

Trend Ltd. Along with they will ensure that an entity is effectively supplying its stock on

particular time to enhance the cash flow of firm.

Predication of cash flow: By effective cash flow like receivables as well as payables in an

entity will assist in effective manner in the context of investment and other required

operations.

4

TASK 2

EXECUTIVE SUMMARY

Budget is a written document that is produced by managers to recognise potential

financial gain generated by business entity in next year. According to budget business planning

their strategy and take appropriate steps. Along with it is utilised to apply strategies in regard

decision making procedure. The finance manager uses this budget for the performance

measurement and analysis of strategic analysis. This report based on Thorne Estate limited that

will advertise and sells residential property. In this report prepare cash budget to analysis actual

cash position of business and provide suggestions (Klopotan, Zoroja and Meško, 2018).

1. Prepare a monthly cash budget

A cash budget represents the anticipated potential cash flow of an entity over a defined

period of time. For the preparation of budget record all the cash receipts that occur in future over

the budget period and the expenditure to be consisted of cash and eventually cash balance with

an entity at the end of the period. Therefore, cash position can be ascertained more rarely and

keep a check on the entity's performance in context of budget.

In case of business an organisation is facing various ups and downs so cash budget is

prepared by an entity for small durations like weekly and monthly. It will support to accomplish

actual goals of budget. An organisation can go for longer period budget and cash flow related to

stable with little changes. This budget provides wide sense of an entity cash requirements in the

near future. One essential thing to be considered into accounts that in cash budget consist of

those transactions that actual cash will come in or go out. It provides a shape after the

formulation of other budgets such as, sales, purchases many others.

It can be seen from the above calculations that the units sold minimum in the month of

December and January. On the other side in the month of April pattern of sales can be analysed

from that only. Besides from this total receipt of an entity involves cash fees, credit fees that is 2

percent of sales of assets. Thorne Ltd receive 1% cash sales in same month after remaining 2%

next after 2 months. As per the month of January to April total receipt were 54000, 63000, 99000

and 164000 respectively (Hanley, 2020). From the total receipt of the company less amount of

payment in which consist of bonus, salary, taxation, interest and fixed overhead. The average

salary per employee is 35000 per year so accordingly divide by 12 months and multiply by 9

5

EXECUTIVE SUMMARY

Budget is a written document that is produced by managers to recognise potential

financial gain generated by business entity in next year. According to budget business planning

their strategy and take appropriate steps. Along with it is utilised to apply strategies in regard

decision making procedure. The finance manager uses this budget for the performance

measurement and analysis of strategic analysis. This report based on Thorne Estate limited that

will advertise and sells residential property. In this report prepare cash budget to analysis actual

cash position of business and provide suggestions (Klopotan, Zoroja and Meško, 2018).

1. Prepare a monthly cash budget

A cash budget represents the anticipated potential cash flow of an entity over a defined

period of time. For the preparation of budget record all the cash receipts that occur in future over

the budget period and the expenditure to be consisted of cash and eventually cash balance with

an entity at the end of the period. Therefore, cash position can be ascertained more rarely and

keep a check on the entity's performance in context of budget.

In case of business an organisation is facing various ups and downs so cash budget is

prepared by an entity for small durations like weekly and monthly. It will support to accomplish

actual goals of budget. An organisation can go for longer period budget and cash flow related to

stable with little changes. This budget provides wide sense of an entity cash requirements in the

near future. One essential thing to be considered into accounts that in cash budget consist of

those transactions that actual cash will come in or go out. It provides a shape after the

formulation of other budgets such as, sales, purchases many others.

It can be seen from the above calculations that the units sold minimum in the month of

December and January. On the other side in the month of April pattern of sales can be analysed

from that only. Besides from this total receipt of an entity involves cash fees, credit fees that is 2

percent of sales of assets. Thorne Ltd receive 1% cash sales in same month after remaining 2%

next after 2 months. As per the month of January to April total receipt were 54000, 63000, 99000

and 164000 respectively (Hanley, 2020). From the total receipt of the company less amount of

payment in which consist of bonus, salary, taxation, interest and fixed overhead. The average

salary per employee is 35000 per year so accordingly divide by 12 months and multiply by 9

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

employees. The variable expenditure rate 0.5% apply on each property that sale out by company.

The closing balance in January (-25550) because of company liquidity position is not good and

do not able to conduct business activities in proper manner. Same procedure follows in other

months and get negative closing balance in February due to less liquidity position but in March

company get positive balance because of able to maintain cash as per the requirement (Hsuan-

Chi, 2019).

2. Observation and recommendations make to management of Thorne Estates

As per the calculation of Thorne Ltd has a fixed volume of revenues in specified period

of time. As per the selling of company it is determined that in summer maximum items are

selling out in compare of winters. Thus, it is defined that business is profitable in summer season

because most of the people prefer to swimming so for this require costumes and different

equipment’s. Therefore, firm must try to sell more items that can be organisation run on

profitable manner in winters so it is essential for firm.

It is recommended that to manage effective cash position in the company production

increase in summer and contact with different organisations to increase their sales. There are

applying all relevant theories and concepts at the time preparation of budget it helps to record all

the transactions in proper manner. Sales are the main source of funds so design effective

strategies to improve sales and attract more customers. Moreover, there are required to applied

different operational activities for collect fund for an entity. The effective payment by supplier is

high so for this require to conduct proper planning after that predict future cash expenses. It is

advised to Thorne Estates limited that when the duration of credit is permitted by borrowers in

one month so amount will be paid in month of Feb for various payment activities that has done in

January.

CONCLUSION

As per the above report it has been concluded that to operate different business operations

require to finance that helps to achieve short term as well as long term goals and objectives.

There are analysing different concepts that defined about the business in depth manner like

profit, inventory, working capital. The effective cash flow presents the actual position of

business. Along with there are preparing cash budget that present actual position of business.

There are providing appropriate recommendations for effective cash budget.

6

The closing balance in January (-25550) because of company liquidity position is not good and

do not able to conduct business activities in proper manner. Same procedure follows in other

months and get negative closing balance in February due to less liquidity position but in March

company get positive balance because of able to maintain cash as per the requirement (Hsuan-

Chi, 2019).

2. Observation and recommendations make to management of Thorne Estates

As per the calculation of Thorne Ltd has a fixed volume of revenues in specified period

of time. As per the selling of company it is determined that in summer maximum items are

selling out in compare of winters. Thus, it is defined that business is profitable in summer season

because most of the people prefer to swimming so for this require costumes and different

equipment’s. Therefore, firm must try to sell more items that can be organisation run on

profitable manner in winters so it is essential for firm.

It is recommended that to manage effective cash position in the company production

increase in summer and contact with different organisations to increase their sales. There are

applying all relevant theories and concepts at the time preparation of budget it helps to record all

the transactions in proper manner. Sales are the main source of funds so design effective

strategies to improve sales and attract more customers. Moreover, there are required to applied

different operational activities for collect fund for an entity. The effective payment by supplier is

high so for this require to conduct proper planning after that predict future cash expenses. It is

advised to Thorne Estates limited that when the duration of credit is permitted by borrowers in

one month so amount will be paid in month of Feb for various payment activities that has done in

January.

CONCLUSION

As per the above report it has been concluded that to operate different business operations

require to finance that helps to achieve short term as well as long term goals and objectives.

There are analysing different concepts that defined about the business in depth manner like

profit, inventory, working capital. The effective cash flow presents the actual position of

business. Along with there are preparing cash budget that present actual position of business.

There are providing appropriate recommendations for effective cash budget.

6

7

REFERENCES

Books and Journals

Paolone, F., 2020. The Historical Background of Cash Flow Statement: First Evidences and

Contributions. In Accounting, Cash Flow and Value Relevance (pp. 23-35). Springer, Cham.

Available through: https://anglia.primo.exlibrisgroup.com/permalink/44APU_INST/16n1f1b/

cdi_askewsholts_vlebooks_9783030506889)

Mian, A. and Sufi, A., 2018. Finance and business cycles: the credit-driven household demand

channel. Journal of Economic Perspectives. 32(3). pp.31-58.

Available through: https://anglia.primo.exlibrisgroup.com/permalink/44APU_INST/16n1f1b/

cdi_proquest_journals_2080766511

Zhang, Y. F. and et.al, 2020. Finance business partnering and manufacturing firms’ performance:

a mediating role of non-financial performance. Journal of Business Economics and

Management. 21(2). pp.473-496.

Available through: https://anglia.primo.exlibrisgroup.com/permalink/44APU_INST/16n1f1b/

cdi_doaj_primary_oai_doaj_org_article_bba29b8c72fc43d9b92457f63cb71363)

Lau, E., Simonetti, B., Trinugroho, I. and Tan, L. M., 2020. Economics and Finance Readings.

Springer.

Available through: https://anglia.primo.exlibrisgroup.com/permalink/44APU_INST/16n1f1b/

cdi_askewsholts_vlebooks_9789811529061)

Klopotan, I., Zoroja, J. and Meško, M., 2018. Early warning system in business, finance, and

economics: Bibliometric and topic analysis. International Journal of Engineering

Business Management. 10. p.1847979018797013.

Available through: https://anglia.primo.exlibrisgroup.com/permalink/44APU_INST/16n1f1b/

cdi_crossref_primary_10_1177_1847979018797013)

Hsuan-Chi, C., 2019. Introduction to the special issue of “Business Finance and Enterprise

Management”. Asia Pacific Management Review. 24(1). p.60.

Available through: < https://anglia.primo.exlibrisgroup.com/permalink/44APU_INST/16n1f1b/

cdi_proquest_journals_2198019061>

8

Books and Journals

Paolone, F., 2020. The Historical Background of Cash Flow Statement: First Evidences and

Contributions. In Accounting, Cash Flow and Value Relevance (pp. 23-35). Springer, Cham.

Available through: https://anglia.primo.exlibrisgroup.com/permalink/44APU_INST/16n1f1b/

cdi_askewsholts_vlebooks_9783030506889)

Mian, A. and Sufi, A., 2018. Finance and business cycles: the credit-driven household demand

channel. Journal of Economic Perspectives. 32(3). pp.31-58.

Available through: https://anglia.primo.exlibrisgroup.com/permalink/44APU_INST/16n1f1b/

cdi_proquest_journals_2080766511

Zhang, Y. F. and et.al, 2020. Finance business partnering and manufacturing firms’ performance:

a mediating role of non-financial performance. Journal of Business Economics and

Management. 21(2). pp.473-496.

Available through: https://anglia.primo.exlibrisgroup.com/permalink/44APU_INST/16n1f1b/

cdi_doaj_primary_oai_doaj_org_article_bba29b8c72fc43d9b92457f63cb71363)

Lau, E., Simonetti, B., Trinugroho, I. and Tan, L. M., 2020. Economics and Finance Readings.

Springer.

Available through: https://anglia.primo.exlibrisgroup.com/permalink/44APU_INST/16n1f1b/

cdi_askewsholts_vlebooks_9789811529061)

Klopotan, I., Zoroja, J. and Meško, M., 2018. Early warning system in business, finance, and

economics: Bibliometric and topic analysis. International Journal of Engineering

Business Management. 10. p.1847979018797013.

Available through: https://anglia.primo.exlibrisgroup.com/permalink/44APU_INST/16n1f1b/

cdi_crossref_primary_10_1177_1847979018797013)

Hsuan-Chi, C., 2019. Introduction to the special issue of “Business Finance and Enterprise

Management”. Asia Pacific Management Review. 24(1). p.60.

Available through: < https://anglia.primo.exlibrisgroup.com/permalink/44APU_INST/16n1f1b/

cdi_proquest_journals_2198019061>

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

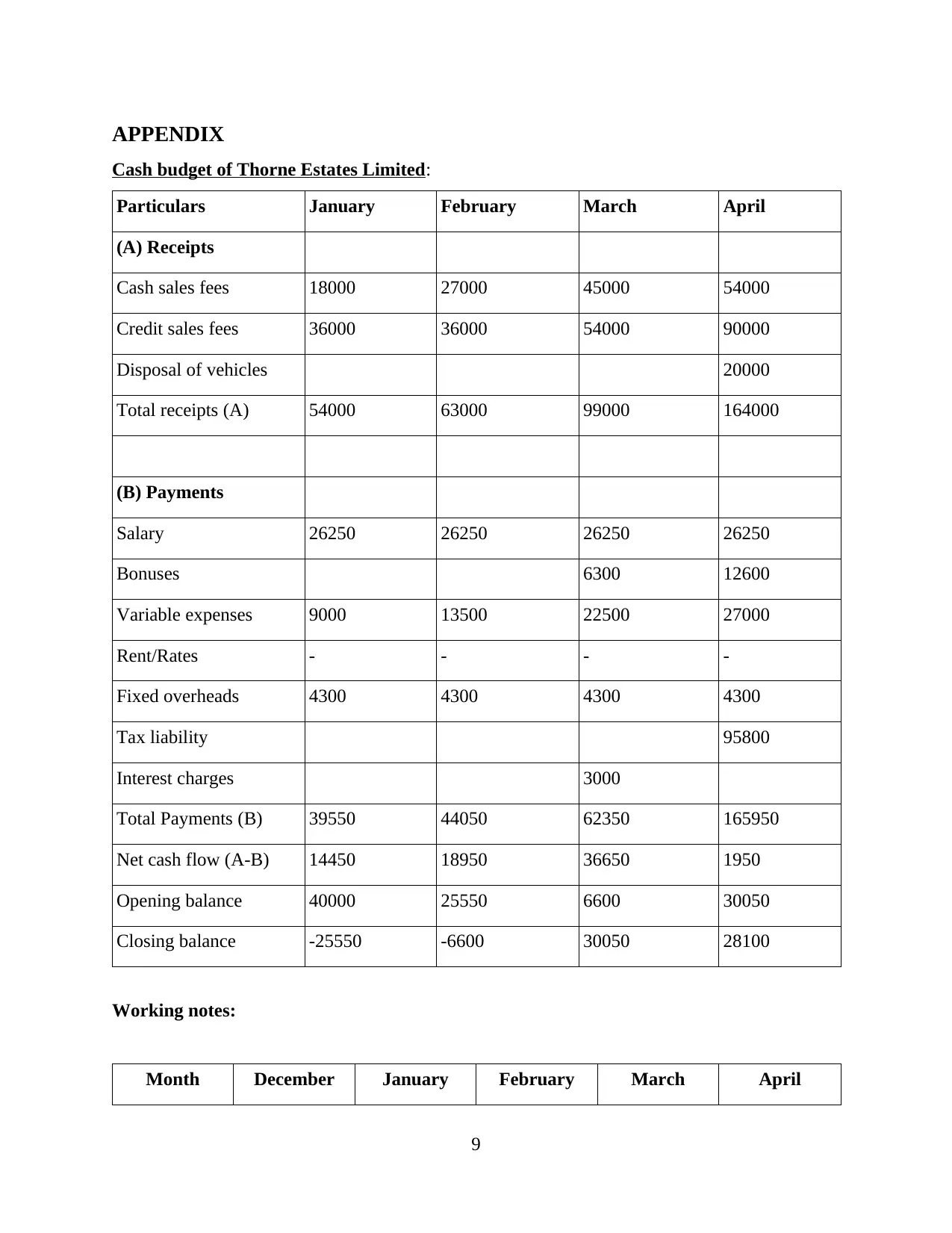

APPENDIX

Cash budget of Thorne Estates Limited:

Particulars January February March April

(A) Receipts

Cash sales fees 18000 27000 45000 54000

Credit sales fees 36000 36000 54000 90000

Disposal of vehicles 20000

Total receipts (A) 54000 63000 99000 164000

(B) Payments

Salary 26250 26250 26250 26250

Bonuses 6300 12600

Variable expenses 9000 13500 22500 27000

Rent/Rates - - - -

Fixed overheads 4300 4300 4300 4300

Tax liability 95800

Interest charges 3000

Total Payments (B) 39550 44050 62350 165950

Net cash flow (A-B) 14450 18950 36650 1950

Opening balance 40000 25550 6600 30050

Closing balance -25550 -6600 30050 28100

Working notes:

Month December January February March April

9

Cash budget of Thorne Estates Limited:

Particulars January February March April

(A) Receipts

Cash sales fees 18000 27000 45000 54000

Credit sales fees 36000 36000 54000 90000

Disposal of vehicles 20000

Total receipts (A) 54000 63000 99000 164000

(B) Payments

Salary 26250 26250 26250 26250

Bonuses 6300 12600

Variable expenses 9000 13500 22500 27000

Rent/Rates - - - -

Fixed overheads 4300 4300 4300 4300

Tax liability 95800

Interest charges 3000

Total Payments (B) 39550 44050 62350 165950

Net cash flow (A-B) 14450 18950 36650 1950

Opening balance 40000 25550 6600 30050

Closing balance -25550 -6600 30050 28100

Working notes:

Month December January February March April

9

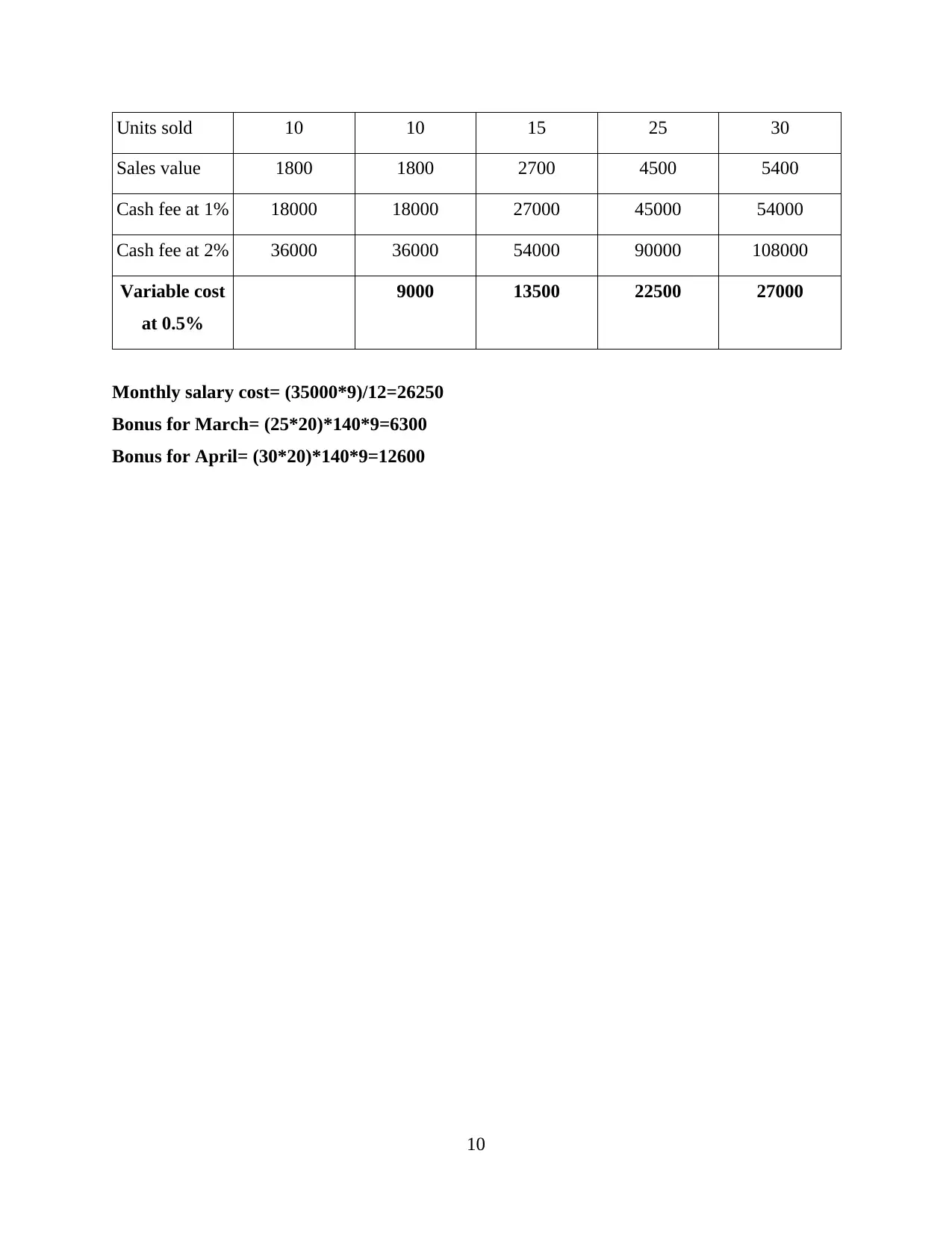

Units sold 10 10 15 25 30

Sales value 1800 1800 2700 4500 5400

Cash fee at 1% 18000 18000 27000 45000 54000

Cash fee at 2% 36000 36000 54000 90000 108000

Variable cost

at 0.5%

9000 13500 22500 27000

Monthly salary cost= (35000*9)/12=26250

Bonus for March= (25*20)*140*9=6300

Bonus for April= (30*20)*140*9=12600

10

Sales value 1800 1800 2700 4500 5400

Cash fee at 1% 18000 18000 27000 45000 54000

Cash fee at 2% 36000 36000 54000 90000 108000

Variable cost

at 0.5%

9000 13500 22500 27000

Monthly salary cost= (35000*9)/12=26250

Bonus for March= (25*20)*140*9=6300

Bonus for April= (30*20)*140*9=12600

10

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.