Cost Analysis, Reduction Strategies, and Cash Flow Forecast in Finance

VerifiedAdded on 2023/06/10

|17

|4453

|391

Report

AI Summary

This report provides a comprehensive analysis of cost information for Dysonica, identifying variable, fixed, and semi-variable costs. It explores methods for cost reduction, including activity-based costing, absorption costing, and marginal costing, highlighting their advantages and disadvantages. A 12-month cash flow forecast is prepared to facilitate better spending, cost management, and financial planning. The report evaluates the company's performance based on the budget forecast, considering financial and non-financial implications, as well as external factors impacting the cost base, and concludes with recommendations for the company to improve its financial strategies. Desklib provides similar solved assignments.

Time constrained project

Business Finance

Business Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENT

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Methods of attributing indirect costs...........................................................................................4

TASK 2............................................................................................................................................9

Methods to reduce costs...............................................................................................................9

TASK 3..........................................................................................................................................11

Preparing the Cash Flow Forecast of 12 months.......................................................................11

TASK 4..........................................................................................................................................14

Evaluating performance of company based on information of budget......................................14

Considering the financial and non-financial implications with external factors affecting cost

base............................................................................................................................................15

Recommendations to the company............................................................................................16

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................18

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Methods of attributing indirect costs...........................................................................................4

TASK 2............................................................................................................................................9

Methods to reduce costs...............................................................................................................9

TASK 3..........................................................................................................................................11

Preparing the Cash Flow Forecast of 12 months.......................................................................11

TASK 4..........................................................................................................................................14

Evaluating performance of company based on information of budget......................................14

Considering the financial and non-financial implications with external factors affecting cost

base............................................................................................................................................15

Recommendations to the company............................................................................................16

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................18

INTRODUCTION

Business finance is defined as the process of raising and managing the funds of the

company. By planning, analysing and controlling the operations are the main functions of the

financial manager that they must perform to attain goals. The current assignment is based on the

Dysonica which is the successful international company used to do innovations. This report will

outline the examination of cost information in order to identify variable costs, fixed cost or semi-

variable costs. Further this current report will outline the methods in order to reduce the cost in

the organization. Moreover, this report will also include the cash flow forecast that is based on

12 months’ budget to have proper spending, cost reduction and finance management. At the end

this report will outline the performance of the organization by budget forecasted. It will also

consider financial and non- financial implications with external factors that impact the cost.

TASK 1

Expense Type Reason

Raw Materials Variable Cost Raw materials are the variable

cost as the amount of raw

materials used varies with the

level of production by the

company.

Machinery Fixed Cost Machinery expense is a fixed

cost because the cost incurred

does not change with the level

of production.

Factory and Storage Rent Fixed Cost Factory and storage has to be

paid even if the production

units are zero. Hence it is

Business finance is defined as the process of raising and managing the funds of the

company. By planning, analysing and controlling the operations are the main functions of the

financial manager that they must perform to attain goals. The current assignment is based on the

Dysonica which is the successful international company used to do innovations. This report will

outline the examination of cost information in order to identify variable costs, fixed cost or semi-

variable costs. Further this current report will outline the methods in order to reduce the cost in

the organization. Moreover, this report will also include the cash flow forecast that is based on

12 months’ budget to have proper spending, cost reduction and finance management. At the end

this report will outline the performance of the organization by budget forecasted. It will also

consider financial and non- financial implications with external factors that impact the cost.

TASK 1

Expense Type Reason

Raw Materials Variable Cost Raw materials are the variable

cost as the amount of raw

materials used varies with the

level of production by the

company.

Machinery Fixed Cost Machinery expense is a fixed

cost because the cost incurred

does not change with the level

of production.

Factory and Storage Rent Fixed Cost Factory and storage has to be

paid even if the production

units are zero. Hence it is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

categorised as fixed cost.

Direct labour Variable Cost Direct labour is a type of

variable cost. Because as the

number of units produced

increases the labour cost also

increases.

Utilities Semi Variable Cost Utilities includes electricity,

water, etc. expenses. It is

categorised under semi

variable cost because a certain

amount is fixed as required to

be paid even at zero level of

production and rest amount is

incurred in accordance with

the level of production.

Office and Sales Staff Fixed Cost Office and sales staff have to

be paid at all levels of

production at same rate.

Hence it is fixed cost.

Insurance Fixed Cost Insurance cost is constant at

all levels of production as it is

a fixed cost.

Logistics Variable Cost Transportation cost are

covered in logistics. Hence it

is a variable cost dependent of

the production units.

Methods of attributing indirect costs

Absorption costing: The absorption costing is also known as full costing which is the

best managerial accounting method in order to capture the costs that is associated with the

manufacturing of the product (Nan, 2019). This cost used to allocate the fixed overheads to the

units that is produced over the period. This cost helps the company to allocate the fixed

Direct labour Variable Cost Direct labour is a type of

variable cost. Because as the

number of units produced

increases the labour cost also

increases.

Utilities Semi Variable Cost Utilities includes electricity,

water, etc. expenses. It is

categorised under semi

variable cost because a certain

amount is fixed as required to

be paid even at zero level of

production and rest amount is

incurred in accordance with

the level of production.

Office and Sales Staff Fixed Cost Office and sales staff have to

be paid at all levels of

production at same rate.

Hence it is fixed cost.

Insurance Fixed Cost Insurance cost is constant at

all levels of production as it is

a fixed cost.

Logistics Variable Cost Transportation cost are

covered in logistics. Hence it

is a variable cost dependent of

the production units.

Methods of attributing indirect costs

Absorption costing: The absorption costing is also known as full costing which is the

best managerial accounting method in order to capture the costs that is associated with the

manufacturing of the product (Nan, 2019). This cost used to allocate the fixed overheads to the

units that is produced over the period. This cost helps the company to allocate the fixed

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

overheads costs whether the products are sold or not. In this type of costing the more cost is

added at the ending of inventory which is carried out by the company in the balance sheet of next

year.

Assumption: It is assumed that the firm produces and sells 10,000 units yearly.

Absorption Costing

Attributing indirect costs

Indirect Cost Attribution Per Unit Cost

Machinery Cost (fixed

manufacturing overhead)

(£1500 x 12) / 10000 Units 18

Factory And Storage Rent

(fixed manufacturing

overhead)

(£18000 x 12) / 10000 Units 21.6

Office and Sales Staff (fixed

manufacturing overhead)

(£9000 x 12) / 10000 Units 10.8

Insurance (fixed

manufacturing overhead)

(£500 x 12) / 10000 Units 0.6

Total Fixed Manufacturing

Overheads

51

Utilities (Variable

manufacturing overhead)

(£500 x 12) / 10000 Units 0.6

Logistics (Variable

manufacturing overhead)

(£3000 x 12) / 10000 Units 3.6

Total Variable

Manufacturing Overhead

4.2

Calculating Per Unit Cost

Particulars Formula Value

Direct Material Cost per Unit £15000 * 12 / 10000 units 18

Direct Labour Cost per Unit £17500 * 12 / 10000 units 21

Variable Overhead per Unit 4.2

Fixed Overhead per Unit 51

added at the ending of inventory which is carried out by the company in the balance sheet of next

year.

Assumption: It is assumed that the firm produces and sells 10,000 units yearly.

Absorption Costing

Attributing indirect costs

Indirect Cost Attribution Per Unit Cost

Machinery Cost (fixed

manufacturing overhead)

(£1500 x 12) / 10000 Units 18

Factory And Storage Rent

(fixed manufacturing

overhead)

(£18000 x 12) / 10000 Units 21.6

Office and Sales Staff (fixed

manufacturing overhead)

(£9000 x 12) / 10000 Units 10.8

Insurance (fixed

manufacturing overhead)

(£500 x 12) / 10000 Units 0.6

Total Fixed Manufacturing

Overheads

51

Utilities (Variable

manufacturing overhead)

(£500 x 12) / 10000 Units 0.6

Logistics (Variable

manufacturing overhead)

(£3000 x 12) / 10000 Units 3.6

Total Variable

Manufacturing Overhead

4.2

Calculating Per Unit Cost

Particulars Formula Value

Direct Material Cost per Unit £15000 * 12 / 10000 units 18

Direct Labour Cost per Unit £17500 * 12 / 10000 units 21

Variable Overhead per Unit 4.2

Fixed Overhead per Unit 51

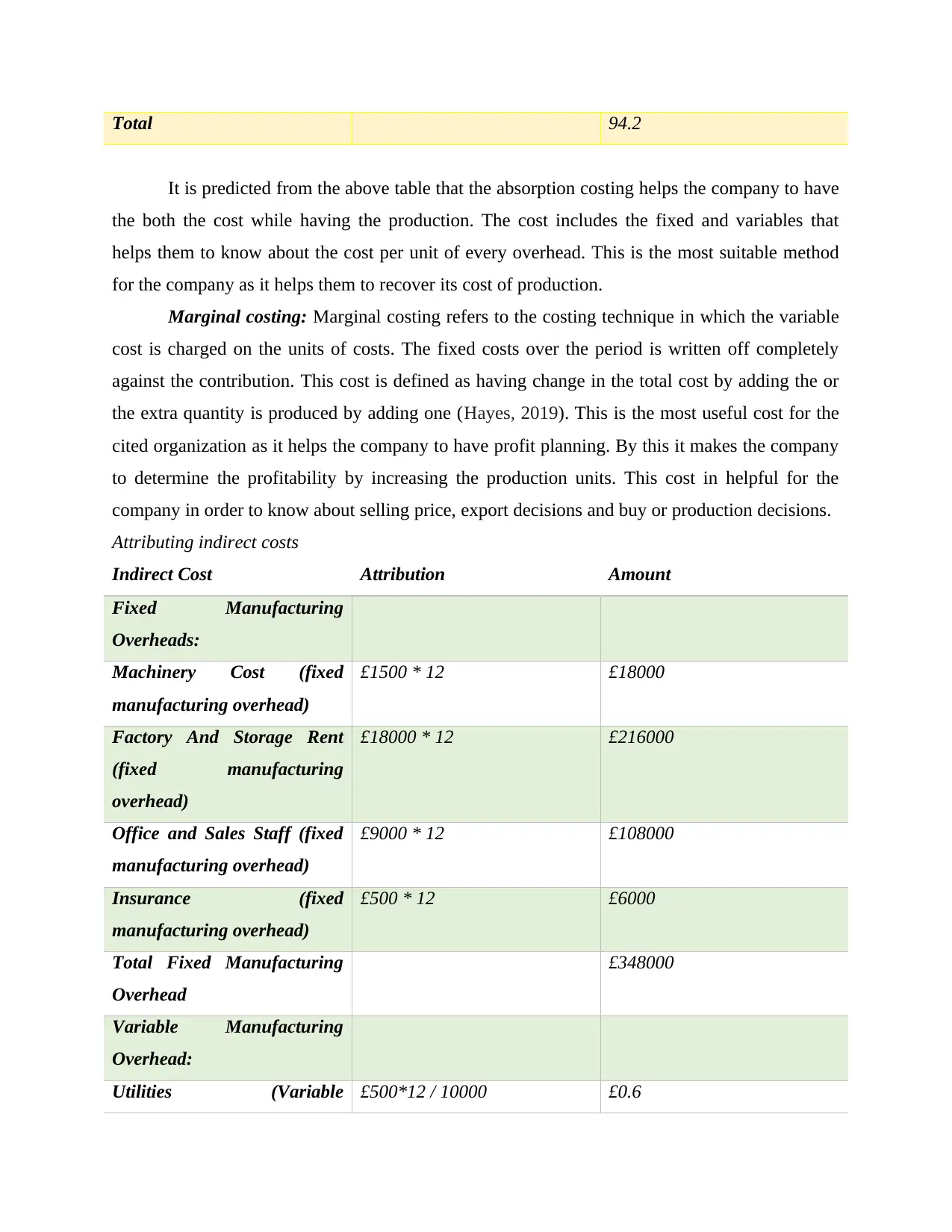

Total 94.2

It is predicted from the above table that the absorption costing helps the company to have

the both the cost while having the production. The cost includes the fixed and variables that

helps them to know about the cost per unit of every overhead. This is the most suitable method

for the company as it helps them to recover its cost of production.

Marginal costing: Marginal costing refers to the costing technique in which the variable

cost is charged on the units of costs. The fixed costs over the period is written off completely

against the contribution. This cost is defined as having change in the total cost by adding the or

the extra quantity is produced by adding one (Hayes, 2019). This is the most useful cost for the

cited organization as it helps the company to have profit planning. By this it makes the company

to determine the profitability by increasing the production units. This cost in helpful for the

company in order to know about selling price, export decisions and buy or production decisions.

Attributing indirect costs

Indirect Cost Attribution Amount

Fixed Manufacturing

Overheads:

Machinery Cost (fixed

manufacturing overhead)

£1500 * 12 £18000

Factory And Storage Rent

(fixed manufacturing

overhead)

£18000 * 12 £216000

Office and Sales Staff (fixed

manufacturing overhead)

£9000 * 12 £108000

Insurance (fixed

manufacturing overhead)

£500 * 12 £6000

Total Fixed Manufacturing

Overhead

£348000

Variable Manufacturing

Overhead:

Utilities (Variable £500*12 / 10000 £0.6

It is predicted from the above table that the absorption costing helps the company to have

the both the cost while having the production. The cost includes the fixed and variables that

helps them to know about the cost per unit of every overhead. This is the most suitable method

for the company as it helps them to recover its cost of production.

Marginal costing: Marginal costing refers to the costing technique in which the variable

cost is charged on the units of costs. The fixed costs over the period is written off completely

against the contribution. This cost is defined as having change in the total cost by adding the or

the extra quantity is produced by adding one (Hayes, 2019). This is the most useful cost for the

cited organization as it helps the company to have profit planning. By this it makes the company

to determine the profitability by increasing the production units. This cost in helpful for the

company in order to know about selling price, export decisions and buy or production decisions.

Attributing indirect costs

Indirect Cost Attribution Amount

Fixed Manufacturing

Overheads:

Machinery Cost (fixed

manufacturing overhead)

£1500 * 12 £18000

Factory And Storage Rent

(fixed manufacturing

overhead)

£18000 * 12 £216000

Office and Sales Staff (fixed

manufacturing overhead)

£9000 * 12 £108000

Insurance (fixed

manufacturing overhead)

£500 * 12 £6000

Total Fixed Manufacturing

Overhead

£348000

Variable Manufacturing

Overhead:

Utilities (Variable £500*12 / 10000 £0.6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

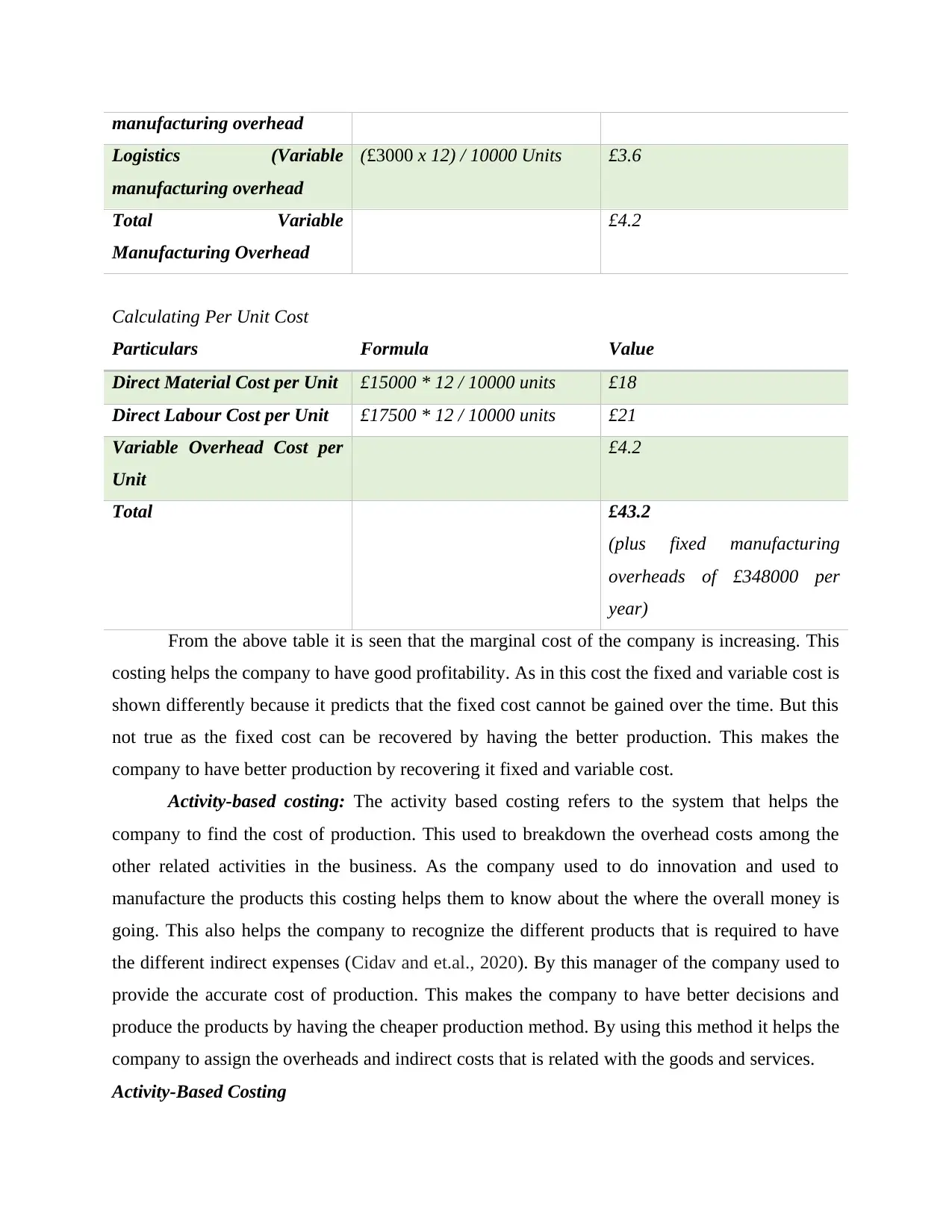

manufacturing overhead

Logistics (Variable

manufacturing overhead

(£3000 x 12) / 10000 Units £3.6

Total Variable

Manufacturing Overhead

£4.2

Calculating Per Unit Cost

Particulars Formula Value

Direct Material Cost per Unit £15000 * 12 / 10000 units £18

Direct Labour Cost per Unit £17500 * 12 / 10000 units £21

Variable Overhead Cost per

Unit

£4.2

Total £43.2

(plus fixed manufacturing

overheads of £348000 per

year)

From the above table it is seen that the marginal cost of the company is increasing. This

costing helps the company to have good profitability. As in this cost the fixed and variable cost is

shown differently because it predicts that the fixed cost cannot be gained over the time. But this

not true as the fixed cost can be recovered by having the better production. This makes the

company to have better production by recovering it fixed and variable cost.

Activity-based costing: The activity based costing refers to the system that helps the

company to find the cost of production. This used to breakdown the overhead costs among the

other related activities in the business. As the company used to do innovation and used to

manufacture the products this costing helps them to know about the where the overall money is

going. This also helps the company to recognize the different products that is required to have

the different indirect expenses (Cidav and et.al., 2020). By this manager of the company used to

provide the accurate cost of production. This makes the company to have better decisions and

produce the products by having the cheaper production method. By using this method it helps the

company to assign the overheads and indirect costs that is related with the goods and services.

Activity-Based Costing

Logistics (Variable

manufacturing overhead

(£3000 x 12) / 10000 Units £3.6

Total Variable

Manufacturing Overhead

£4.2

Calculating Per Unit Cost

Particulars Formula Value

Direct Material Cost per Unit £15000 * 12 / 10000 units £18

Direct Labour Cost per Unit £17500 * 12 / 10000 units £21

Variable Overhead Cost per

Unit

£4.2

Total £43.2

(plus fixed manufacturing

overheads of £348000 per

year)

From the above table it is seen that the marginal cost of the company is increasing. This

costing helps the company to have good profitability. As in this cost the fixed and variable cost is

shown differently because it predicts that the fixed cost cannot be gained over the time. But this

not true as the fixed cost can be recovered by having the better production. This makes the

company to have better production by recovering it fixed and variable cost.

Activity-based costing: The activity based costing refers to the system that helps the

company to find the cost of production. This used to breakdown the overhead costs among the

other related activities in the business. As the company used to do innovation and used to

manufacture the products this costing helps them to know about the where the overall money is

going. This also helps the company to recognize the different products that is required to have

the different indirect expenses (Cidav and et.al., 2020). By this manager of the company used to

provide the accurate cost of production. This makes the company to have better decisions and

produce the products by having the cheaper production method. By using this method it helps the

company to assign the overheads and indirect costs that is related with the goods and services.

Activity-Based Costing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

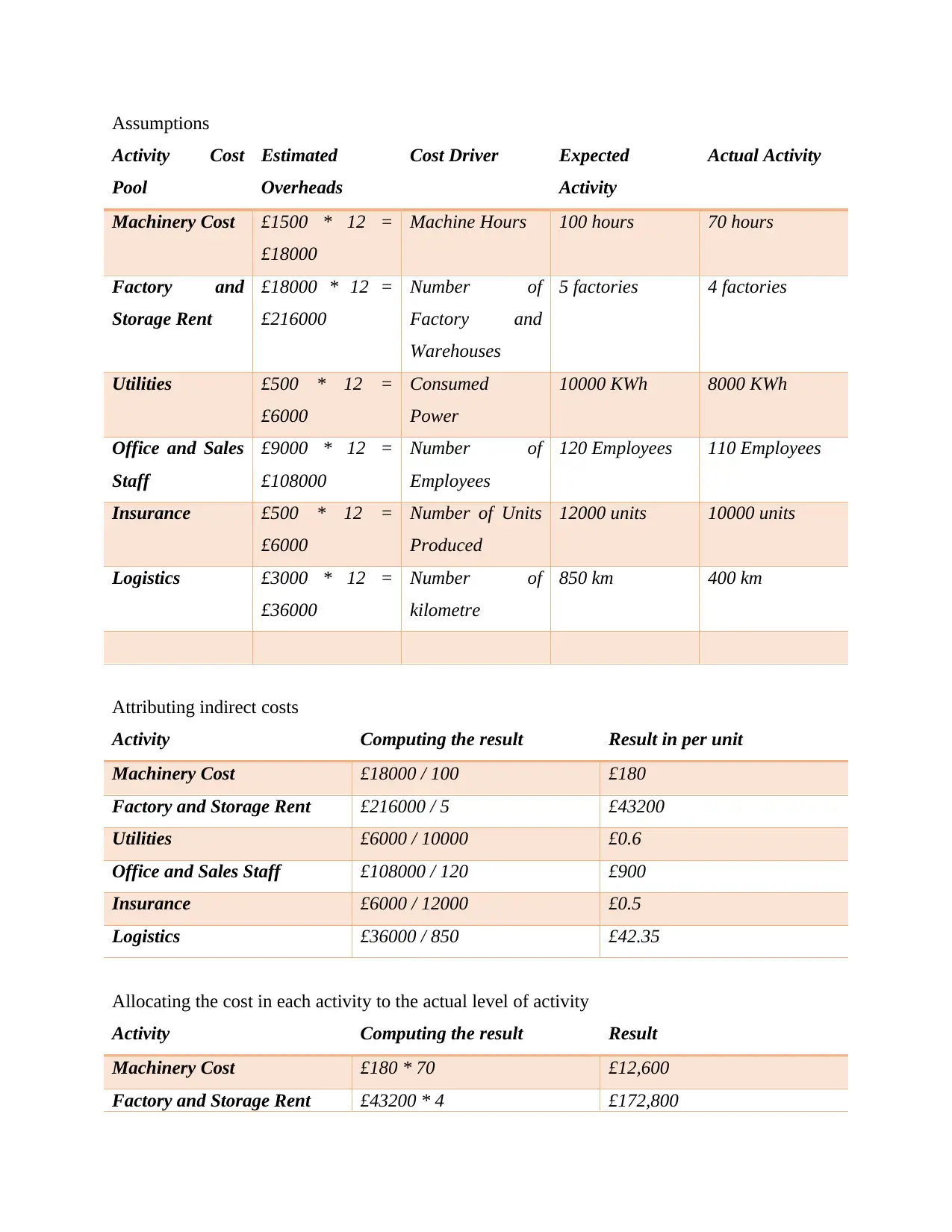

Assumptions

Activity Cost

Pool

Estimated

Overheads

Cost Driver Expected

Activity

Actual Activity

Machinery Cost £1500 * 12 =

£18000

Machine Hours 100 hours 70 hours

Factory and

Storage Rent

£18000 * 12 =

£216000

Number of

Factory and

Warehouses

5 factories 4 factories

Utilities £500 * 12 =

£6000

Consumed

Power

10000 KWh 8000 KWh

Office and Sales

Staff

£9000 * 12 =

£108000

Number of

Employees

120 Employees 110 Employees

Insurance £500 * 12 =

£6000

Number of Units

Produced

12000 units 10000 units

Logistics £3000 * 12 =

£36000

Number of

kilometre

850 km 400 km

Attributing indirect costs

Activity Computing the result Result in per unit

Machinery Cost £18000 / 100 £180

Factory and Storage Rent £216000 / 5 £43200

Utilities £6000 / 10000 £0.6

Office and Sales Staff £108000 / 120 £900

Insurance £6000 / 12000 £0.5

Logistics £36000 / 850 £42.35

Allocating the cost in each activity to the actual level of activity

Activity Computing the result Result

Machinery Cost £180 * 70 £12,600

Factory and Storage Rent £43200 * 4 £172,800

Activity Cost

Pool

Estimated

Overheads

Cost Driver Expected

Activity

Actual Activity

Machinery Cost £1500 * 12 =

£18000

Machine Hours 100 hours 70 hours

Factory and

Storage Rent

£18000 * 12 =

£216000

Number of

Factory and

Warehouses

5 factories 4 factories

Utilities £500 * 12 =

£6000

Consumed

Power

10000 KWh 8000 KWh

Office and Sales

Staff

£9000 * 12 =

£108000

Number of

Employees

120 Employees 110 Employees

Insurance £500 * 12 =

£6000

Number of Units

Produced

12000 units 10000 units

Logistics £3000 * 12 =

£36000

Number of

kilometre

850 km 400 km

Attributing indirect costs

Activity Computing the result Result in per unit

Machinery Cost £18000 / 100 £180

Factory and Storage Rent £216000 / 5 £43200

Utilities £6000 / 10000 £0.6

Office and Sales Staff £108000 / 120 £900

Insurance £6000 / 12000 £0.5

Logistics £36000 / 850 £42.35

Allocating the cost in each activity to the actual level of activity

Activity Computing the result Result

Machinery Cost £180 * 70 £12,600

Factory and Storage Rent £43200 * 4 £172,800

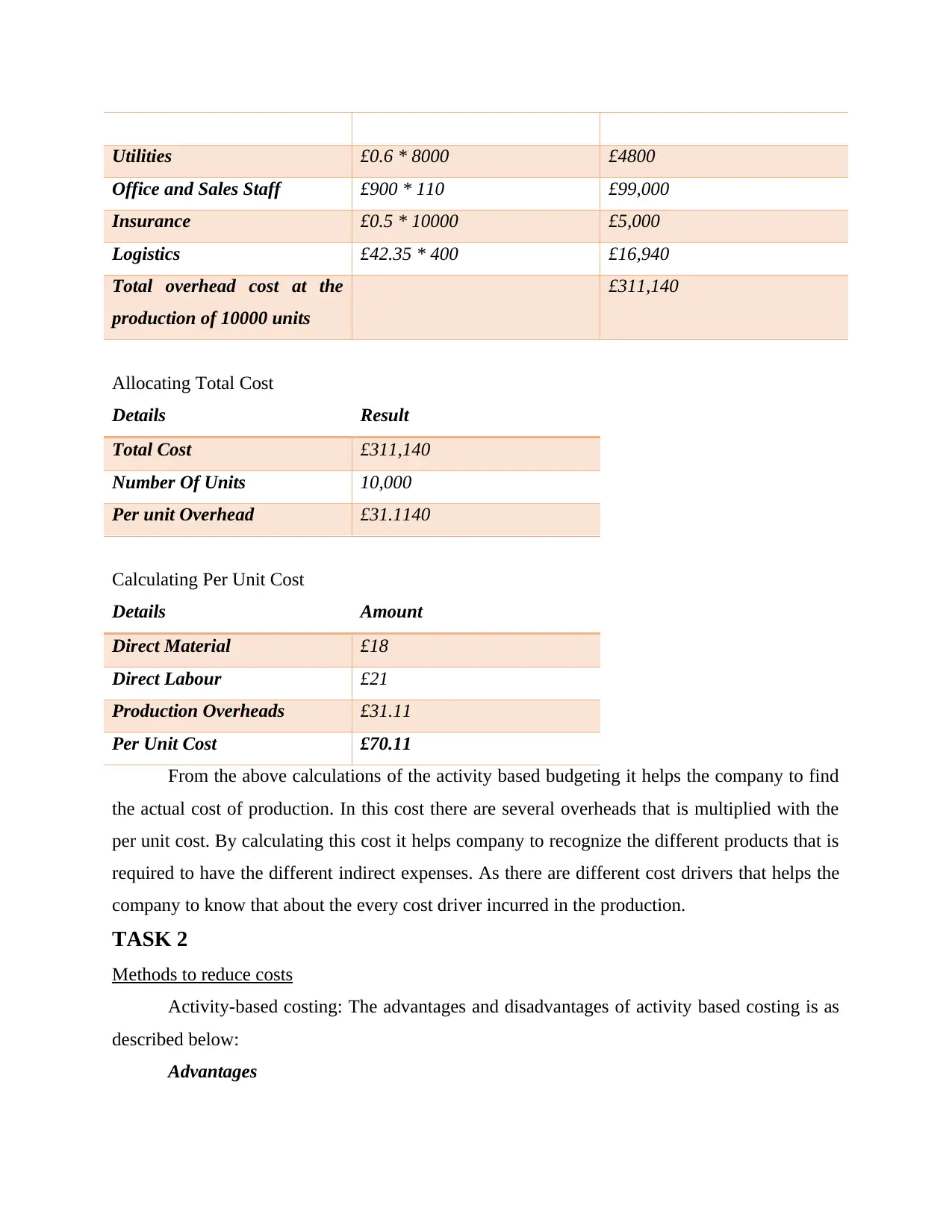

Utilities £0.6 * 8000 £4800

Office and Sales Staff £900 * 110 £99,000

Insurance £0.5 * 10000 £5,000

Logistics £42.35 * 400 £16,940

Total overhead cost at the

production of 10000 units

£311,140

Allocating Total Cost

Details Result

Total Cost £311,140

Number Of Units 10,000

Per unit Overhead £31.1140

Calculating Per Unit Cost

Details Amount

Direct Material £18

Direct Labour £21

Production Overheads £31.11

Per Unit Cost £70.11

From the above calculations of the activity based budgeting it helps the company to find

the actual cost of production. In this cost there are several overheads that is multiplied with the

per unit cost. By calculating this cost it helps company to recognize the different products that is

required to have the different indirect expenses. As there are different cost drivers that helps the

company to know that about the every cost driver incurred in the production.

TASK 2

Methods to reduce costs

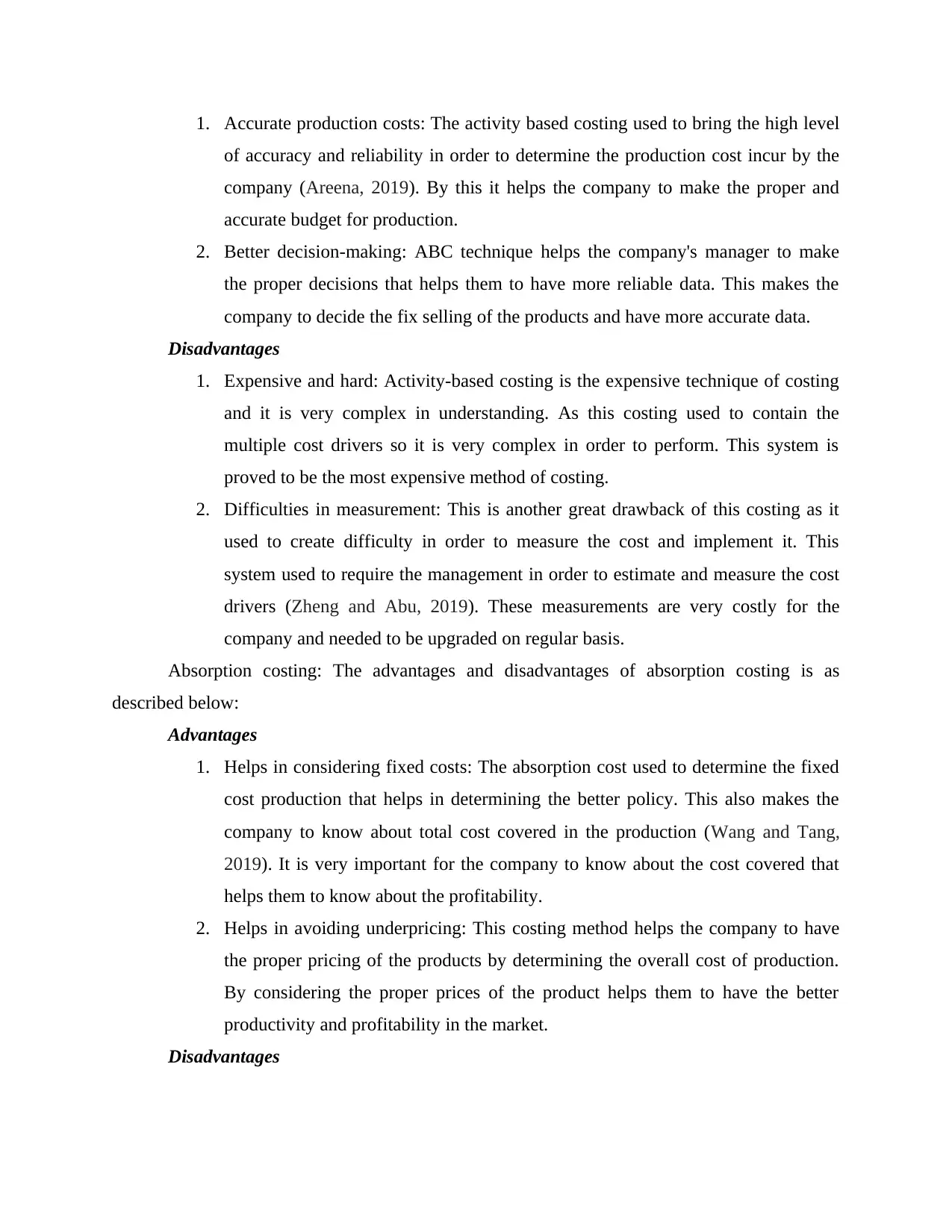

Activity-based costing: The advantages and disadvantages of activity based costing is as

described below:

Advantages

Office and Sales Staff £900 * 110 £99,000

Insurance £0.5 * 10000 £5,000

Logistics £42.35 * 400 £16,940

Total overhead cost at the

production of 10000 units

£311,140

Allocating Total Cost

Details Result

Total Cost £311,140

Number Of Units 10,000

Per unit Overhead £31.1140

Calculating Per Unit Cost

Details Amount

Direct Material £18

Direct Labour £21

Production Overheads £31.11

Per Unit Cost £70.11

From the above calculations of the activity based budgeting it helps the company to find

the actual cost of production. In this cost there are several overheads that is multiplied with the

per unit cost. By calculating this cost it helps company to recognize the different products that is

required to have the different indirect expenses. As there are different cost drivers that helps the

company to know that about the every cost driver incurred in the production.

TASK 2

Methods to reduce costs

Activity-based costing: The advantages and disadvantages of activity based costing is as

described below:

Advantages

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1. Accurate production costs: The activity based costing used to bring the high level

of accuracy and reliability in order to determine the production cost incur by the

company (Areena, 2019). By this it helps the company to make the proper and

accurate budget for production.

2. Better decision-making: ABC technique helps the company's manager to make

the proper decisions that helps them to have more reliable data. This makes the

company to decide the fix selling of the products and have more accurate data.

Disadvantages

1. Expensive and hard: Activity-based costing is the expensive technique of costing

and it is very complex in understanding. As this costing used to contain the

multiple cost drivers so it is very complex in order to perform. This system is

proved to be the most expensive method of costing.

2. Difficulties in measurement: This is another great drawback of this costing as it

used to create difficulty in order to measure the cost and implement it. This

system used to require the management in order to estimate and measure the cost

drivers (Zheng and Abu, 2019). These measurements are very costly for the

company and needed to be upgraded on regular basis.

Absorption costing: The advantages and disadvantages of absorption costing is as

described below:

Advantages

1. Helps in considering fixed costs: The absorption cost used to determine the fixed

cost production that helps in determining the better policy. This also makes the

company to know about total cost covered in the production (Wang and Tang,

2019). It is very important for the company to know about the cost covered that

helps them to know about the profitability.

2. Helps in avoiding underpricing: This costing method helps the company to have

the proper pricing of the products by determining the overall cost of production.

By considering the proper prices of the product helps them to have the better

productivity and profitability in the market.

Disadvantages

of accuracy and reliability in order to determine the production cost incur by the

company (Areena, 2019). By this it helps the company to make the proper and

accurate budget for production.

2. Better decision-making: ABC technique helps the company's manager to make

the proper decisions that helps them to have more reliable data. This makes the

company to decide the fix selling of the products and have more accurate data.

Disadvantages

1. Expensive and hard: Activity-based costing is the expensive technique of costing

and it is very complex in understanding. As this costing used to contain the

multiple cost drivers so it is very complex in order to perform. This system is

proved to be the most expensive method of costing.

2. Difficulties in measurement: This is another great drawback of this costing as it

used to create difficulty in order to measure the cost and implement it. This

system used to require the management in order to estimate and measure the cost

drivers (Zheng and Abu, 2019). These measurements are very costly for the

company and needed to be upgraded on regular basis.

Absorption costing: The advantages and disadvantages of absorption costing is as

described below:

Advantages

1. Helps in considering fixed costs: The absorption cost used to determine the fixed

cost production that helps in determining the better policy. This also makes the

company to know about total cost covered in the production (Wang and Tang,

2019). It is very important for the company to know about the cost covered that

helps them to know about the profitability.

2. Helps in avoiding underpricing: This costing method helps the company to have

the proper pricing of the products by determining the overall cost of production.

By considering the proper prices of the product helps them to have the better

productivity and profitability in the market.

Disadvantages

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1. Inaccurate distribution of fixed costs: The inaccurate distribution of the fixed

overheads provides the difficulty for the company. This makes the company to be

in difficulty in order to have the proper apportionment of the fixed cost.

2. Difficulty in decision-making: This costing method is not suitable as it provide

the difficulty in order to have the proper management decisions (Moisello and

Mella, 2020). The decision-making is basically related to the product mix, buying

decisions and others. This method is not helpful for the business as this only

includes the fixed costs.

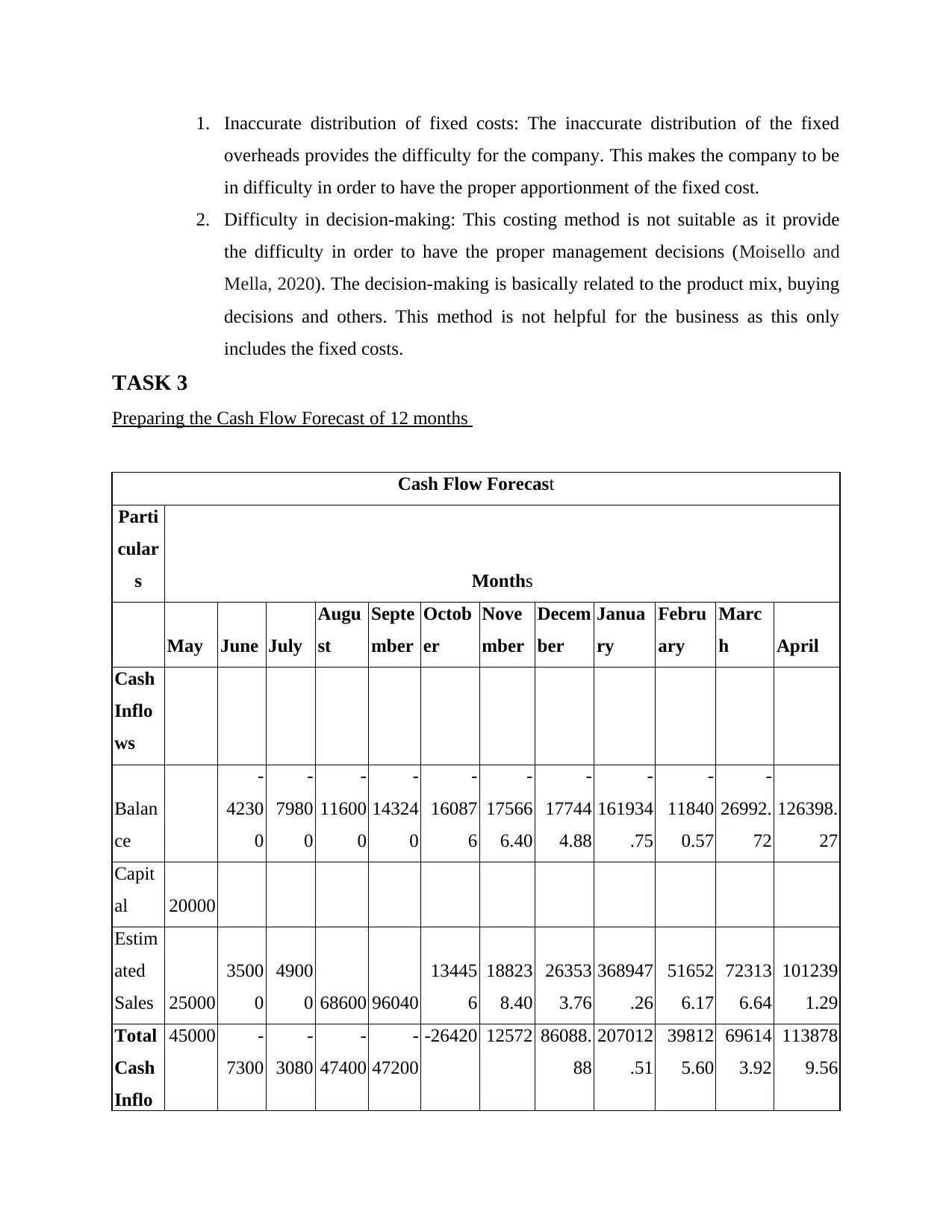

TASK 3

Preparing the Cash Flow Forecast of 12 months

Cash Flow Forecast

Parti

cular

s Months

May June July

Augu

st

Septe

mber

Octob

er

Nove

mber

Decem

ber

Janua

ry

Febru

ary

Marc

h April

Cash

Inflo

ws

Balan

ce

-

4230

0

-

7980

0

-

11600

0

-

14324

0

-

16087

6

-

17566

6.40

-

17744

4.88

-

161934

.75

-

11840

0.57

-

26992.

72

126398.

27

Capit

al 20000

Estim

ated

Sales 25000

3500

0

4900

0 68600 96040

13445

6

18823

8.40

26353

3.76

368947

.26

51652

6.17

72313

6.64

101239

1.29

Total

Cash

Inflo

45000 -

7300

-

3080

-

47400

-

47200

-26420 12572 86088.

88

207012

.51

39812

5.60

69614

3.92

113878

9.56

overheads provides the difficulty for the company. This makes the company to be

in difficulty in order to have the proper apportionment of the fixed cost.

2. Difficulty in decision-making: This costing method is not suitable as it provide

the difficulty in order to have the proper management decisions (Moisello and

Mella, 2020). The decision-making is basically related to the product mix, buying

decisions and others. This method is not helpful for the business as this only

includes the fixed costs.

TASK 3

Preparing the Cash Flow Forecast of 12 months

Cash Flow Forecast

Parti

cular

s Months

May June July

Augu

st

Septe

mber

Octob

er

Nove

mber

Decem

ber

Janua

ry

Febru

ary

Marc

h April

Cash

Inflo

ws

Balan

ce

-

4230

0

-

7980

0

-

11600

0

-

14324

0

-

16087

6

-

17566

6.40

-

17744

4.88

-

161934

.75

-

11840

0.57

-

26992.

72

126398.

27

Capit

al 20000

Estim

ated

Sales 25000

3500

0

4900

0 68600 96040

13445

6

18823

8.40

26353

3.76

368947

.26

51652

6.17

72313

6.64

101239

1.29

Total

Cash

Inflo

45000 -

7300

-

3080

-

47400

-

47200

-26420 12572 86088.

88

207012

.51

39812

5.60

69614

3.92

113878

9.56

ws 0

Cash

Outfl

ows:

Raw

Mater

ials 15000

2100

0

2940

0 41160 57624

80673.

60

11294

3.04

15812

0.26

221368

.36

30991

5.70

43388

1.98

607434.

78

Rent 18000

1800

0

1800

0 18000 18000 25000 25000 25000 25000 25000 25000 25000

Utiliti

es 2500 2500 2500 2500

Telep

hones 1000 1000 1000 1000

Water 100 100 100 100

Misce

llaneo

us 50 50 50 50 50 50 50 50 50 50 50 50

Acco

untant

's Fee 1500

Insura

nce 500 500 500 500 500 500 500 500 500 500 500 500

Salari

es 26500

2650

0

2650

0 26500 26500 26500 26500 31800 31800 31800 31800 31800

Vehic

les:

New

Van 5000

New

Car 15000 200 200 200 200 200 200 200 200 200 200 200

Mark 1250 1750 2450 3430 4802 6722.8 18823 26353. 36894. 51652. 72313. 101239.

Cash

Outfl

ows:

Raw

Mater

ials 15000

2100

0

2940

0 41160 57624

80673.

60

11294

3.04

15812

0.26

221368

.36

30991

5.70

43388

1.98

607434.

78

Rent 18000

1800

0

1800

0 18000 18000 25000 25000 25000 25000 25000 25000 25000

Utiliti

es 2500 2500 2500 2500

Telep

hones 1000 1000 1000 1000

Water 100 100 100 100

Misce

llaneo

us 50 50 50 50 50 50 50 50 50 50 50 50

Acco

untant

's Fee 1500

Insura

nce 500 500 500 500 500 500 500 500 500 500 500 500

Salari

es 26500

2650

0

2650

0 26500 26500 26500 26500 31800 31800 31800 31800 31800

Vehic

les:

New

Van 5000

New

Car 15000 200 200 200 200 200 200 200 200 200 200 200

Mark 1250 1750 2450 3430 4802 6722.8 18823 26353. 36894. 51652. 72313. 101239.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.