Business Finance - Assignment

VerifiedAdded on 2021/06/18

|14

|2826

|47

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

RUNNING HEAD: BUSINESS FINANCE

Finance

Finance

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Business finance 1

Contents

Introduction...........................................................................................................................................2

Question 1.............................................................................................................................................2

Question 2.............................................................................................................................................3

Question 3.............................................................................................................................................3

Question 4.............................................................................................................................................4

Question 5.............................................................................................................................................5

Question 6.............................................................................................................................................7

Question 7.............................................................................................................................................7

Question 8.............................................................................................................................................8

Conclusion.............................................................................................................................................8

References...........................................................................................................................................10

Appendix.............................................................................................................................................12

Contents

Introduction...........................................................................................................................................2

Question 1.............................................................................................................................................2

Question 2.............................................................................................................................................3

Question 3.............................................................................................................................................3

Question 4.............................................................................................................................................4

Question 5.............................................................................................................................................5

Question 6.............................................................................................................................................7

Question 7.............................................................................................................................................7

Question 8.............................................................................................................................................8

Conclusion.............................................................................................................................................8

References...........................................................................................................................................10

Appendix.............................................................................................................................................12

Business finance 2

Introduction

Capital budgeting techniques are basically different methods used for evaluating a project.

These techniques helps in knowing the viability and feasibility of an investment project and

assist in taking decisions related to them (Baker, Jabbouri & Dyaz, 2017). The report contains

an analysis of the project undertaken by Booli Electronics. Booli is planning to expand its

operations and for this it wanted to know about the profitability and sustainability of the

project. In order to carry out the analysis, capital budgeting techniques such as Net present

value, pay-back period, profitability index and internal rate of return are been used in the

report. On the basis of this the decisions and recommendations are provided in the later part.

The report also include a sensitivity analysis of NPV with a change in the price and quantity.

Impact of the same is been discussed in the further part of the report. In the last, a conclusion

is been given covering the findings of the analysis.

Question 1

Payback period is describes as amount of time required by a project to recoup the initial

investment.in other words, it is simply the break-even point of a series of cash flows. A non-

discounted payback period is the one which does not takes into account the time value of

money. This is the only drawback of the method. However, it is the simplest technique used

for evaluation and is very important for the investors or the organizations to determine the

payback period for taking related decisions (Chaysin, Daengdej & Tangjitprom, 2016).

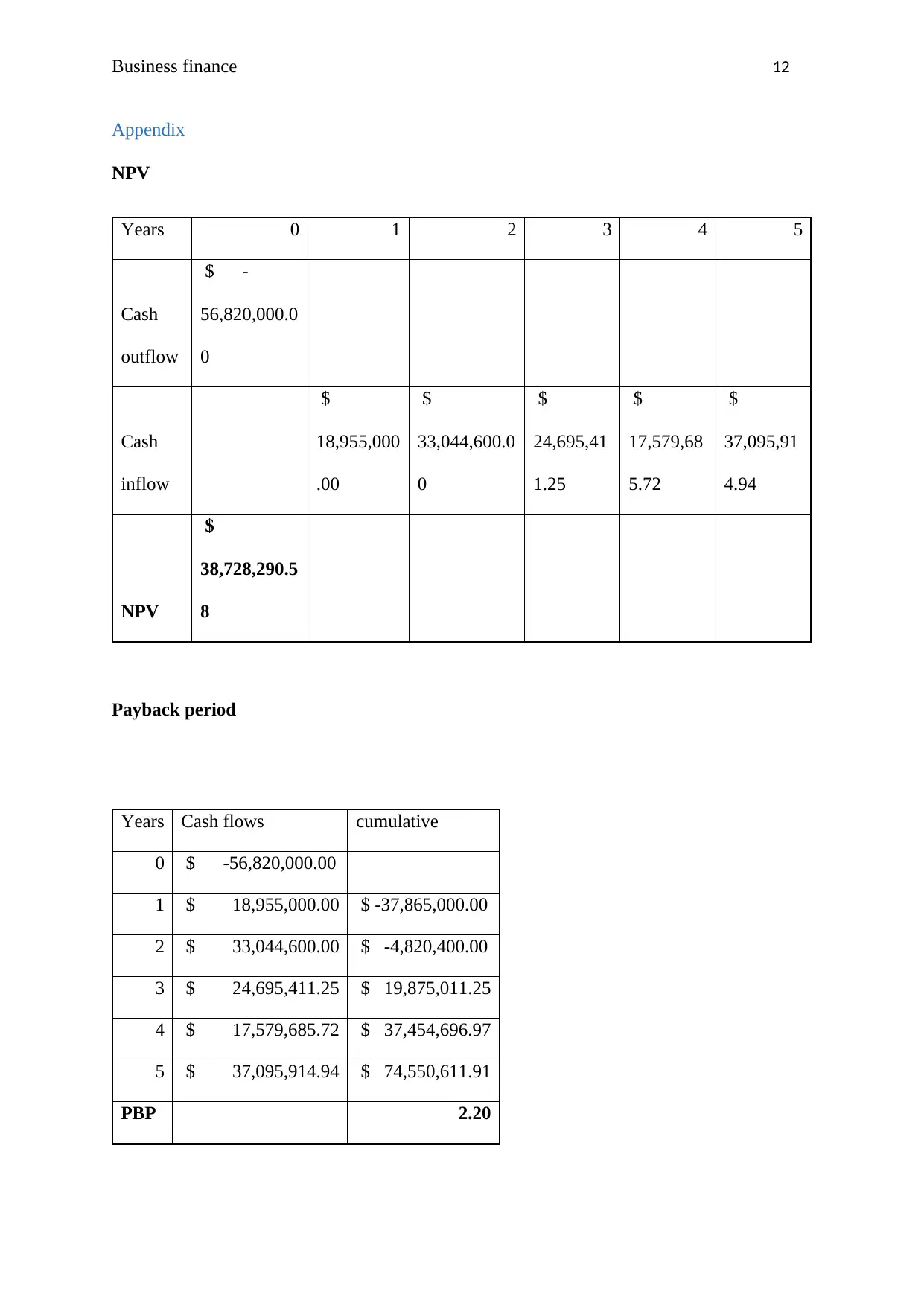

In case of Booli Electronics, the PBP of their project is 2.20 years which means that the

project will cover the initial outlay in less than three years of its life. After that the cash flow

generated will be the profits for the company (Refer Appendix 1).

Introduction

Capital budgeting techniques are basically different methods used for evaluating a project.

These techniques helps in knowing the viability and feasibility of an investment project and

assist in taking decisions related to them (Baker, Jabbouri & Dyaz, 2017). The report contains

an analysis of the project undertaken by Booli Electronics. Booli is planning to expand its

operations and for this it wanted to know about the profitability and sustainability of the

project. In order to carry out the analysis, capital budgeting techniques such as Net present

value, pay-back period, profitability index and internal rate of return are been used in the

report. On the basis of this the decisions and recommendations are provided in the later part.

The report also include a sensitivity analysis of NPV with a change in the price and quantity.

Impact of the same is been discussed in the further part of the report. In the last, a conclusion

is been given covering the findings of the analysis.

Question 1

Payback period is describes as amount of time required by a project to recoup the initial

investment.in other words, it is simply the break-even point of a series of cash flows. A non-

discounted payback period is the one which does not takes into account the time value of

money. This is the only drawback of the method. However, it is the simplest technique used

for evaluation and is very important for the investors or the organizations to determine the

payback period for taking related decisions (Chaysin, Daengdej & Tangjitprom, 2016).

In case of Booli Electronics, the PBP of their project is 2.20 years which means that the

project will cover the initial outlay in less than three years of its life. After that the cash flow

generated will be the profits for the company (Refer Appendix 1).

Business finance 3

Question 2

The profitability index is that capital budgeting tool which reflects profitability of the project.

The fundamental rule of PI is that the project is accepted when PI is greater than one and is

rejected when it is less than one. It can be calculate by adding NPV to the initial investment

and dividing their sum with initial outlay or investment. Generally, proposals having high PI

are more desirable (Moyer, McGuigan, Rao & Kretlow, 2011).

PI = (NPV+ initial investment)/Initial investment

Primary advantage of this method is that it allows quantifying the amount of value created at

per unit of investment. It gives the values in absolute measure. The drawback of this method

is that it may not be suitable for deciding about the mutually exclusive projects (Shapiro,

2008).

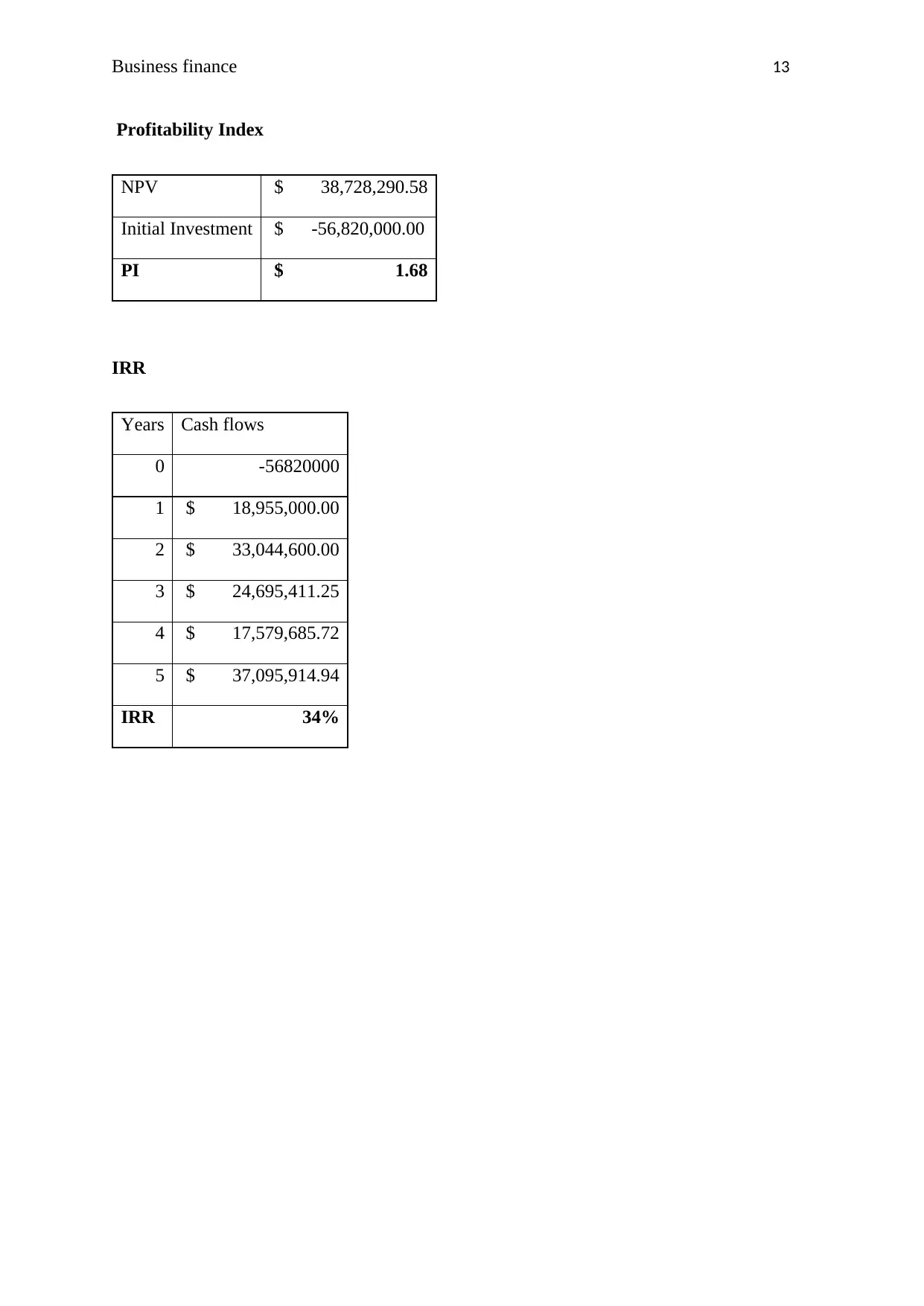

Booli electronics has a PI of $1.68, which is greater than 1 and implies that company will

earn profits in its manufacturing business of new SSHA. Project’s PI also satisfies the rule of

profitability index and hence is regarded as profitable. Looking at the PI and PBP, company

should go for investing in this project. However, the PI ranking can be conflicting in case of

mutually exclusive projects as the size of the investment differs (Refer Appendix 1).

Question 3

Internal rate of return is that when the present value of cash outflow is equal to the present

value of cash inflow. In other words, the point where NPV of a project is zero. The decision

rule for IRR is that accept those projects which have IRR more than the discounting rate and

reject the one having IRR less than the discounting rate (Venkatesh & Gugloth, 2017). When

the internal rate of return is more than the cost of capital, it means the project is profitable

and the company can pursue it. One benefit of using IRR is that it does not require calculation

Question 2

The profitability index is that capital budgeting tool which reflects profitability of the project.

The fundamental rule of PI is that the project is accepted when PI is greater than one and is

rejected when it is less than one. It can be calculate by adding NPV to the initial investment

and dividing their sum with initial outlay or investment. Generally, proposals having high PI

are more desirable (Moyer, McGuigan, Rao & Kretlow, 2011).

PI = (NPV+ initial investment)/Initial investment

Primary advantage of this method is that it allows quantifying the amount of value created at

per unit of investment. It gives the values in absolute measure. The drawback of this method

is that it may not be suitable for deciding about the mutually exclusive projects (Shapiro,

2008).

Booli electronics has a PI of $1.68, which is greater than 1 and implies that company will

earn profits in its manufacturing business of new SSHA. Project’s PI also satisfies the rule of

profitability index and hence is regarded as profitable. Looking at the PI and PBP, company

should go for investing in this project. However, the PI ranking can be conflicting in case of

mutually exclusive projects as the size of the investment differs (Refer Appendix 1).

Question 3

Internal rate of return is that when the present value of cash outflow is equal to the present

value of cash inflow. In other words, the point where NPV of a project is zero. The decision

rule for IRR is that accept those projects which have IRR more than the discounting rate and

reject the one having IRR less than the discounting rate (Venkatesh & Gugloth, 2017). When

the internal rate of return is more than the cost of capital, it means the project is profitable

and the company can pursue it. One benefit of using IRR is that it does not require calculation

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Business finance 4

of hurdle rate or required rate of return. One pitfall is that it ignores the economies of scale

(Gotze, Northcott & Schuster, 2016).

The discounting rate decided by Booli Electronics is 11% and the project has an IRR of 34%.

This means that manufacturing a new SSHA will give more profits to the company, as it has

high IRR and is desirable to go with according to the decision rule of the method (Refer

Appendix 1).

Question 4

Net Present Value is also one of the capital budgeting technique used for evaluating a project

in which investment is required to be made. This method is considered to the most popular

and accurate for making decisions regarding the investments. It measures the profitability of a

project and rank them according to their viability (Bierman & Smidt, 2014). NPV method is

superior to all the other techniques because it has no serious flaws. The primary advantage of

this technique is that it considers the time value of money and can rank the mutually

exclusive projects of different sizes and horizon. The only limitation to this concept is that it

uses discounting rate and relies on future cash flows which are estimated and are uncertain

but the same issue is with other methods also (Daunfeldt & Hartwig, 2014).

Net present value is calculated as follows:

NPV = PV of cash inflow – PV of cash outflow

A project having high and positive NPV is considered to more suitable and acceptable than

the one which has a negative NPV. The decision taken on the basis of this method follow

some criteria, which is as follows:

NPV > 0 = Accept

NPV < 0 = Reject

of hurdle rate or required rate of return. One pitfall is that it ignores the economies of scale

(Gotze, Northcott & Schuster, 2016).

The discounting rate decided by Booli Electronics is 11% and the project has an IRR of 34%.

This means that manufacturing a new SSHA will give more profits to the company, as it has

high IRR and is desirable to go with according to the decision rule of the method (Refer

Appendix 1).

Question 4

Net Present Value is also one of the capital budgeting technique used for evaluating a project

in which investment is required to be made. This method is considered to the most popular

and accurate for making decisions regarding the investments. It measures the profitability of a

project and rank them according to their viability (Bierman & Smidt, 2014). NPV method is

superior to all the other techniques because it has no serious flaws. The primary advantage of

this technique is that it considers the time value of money and can rank the mutually

exclusive projects of different sizes and horizon. The only limitation to this concept is that it

uses discounting rate and relies on future cash flows which are estimated and are uncertain

but the same issue is with other methods also (Daunfeldt & Hartwig, 2014).

Net present value is calculated as follows:

NPV = PV of cash inflow – PV of cash outflow

A project having high and positive NPV is considered to more suitable and acceptable than

the one which has a negative NPV. The decision taken on the basis of this method follow

some criteria, which is as follows:

NPV > 0 = Accept

NPV < 0 = Reject

Business finance 5

NPV = 0 = Accept or reject

The above criteria helps the investors to decide and evaluate the feasibility of a proposal

(Leung, Springborn, Turner & Brockerhoff, 2014).

Looking at the case of Booli Electronics, the NPV of the project is $38,728,290.58 which is

positive and reasonably higher. According to the above criteria, the company must accept the

project as it will generate positive cash flows in future and will be profitable for the

organization. It also implies that the total shareholder wealth of the firm will increased by that

amount (Refer Appendix 1).

Question 5

Sensitivity analysis is the technique used to measure the changes in the dependent variable

when the values of an independent variable is changes under some set of assumptions. In

other words, it is also known as What-if analysis that it is a way to predict the outcome of the

changes made (Borgonovo, 2017).

As per the calculations done it can be said that NPV is highly sensitive to the changes in the

price of new SSHA. The below table shows the variations in NPV of the project as and when

the prices are increased or decreased.

Base case (prices) Best case (prices) Worst case (prices)

$ 685.00 $ 700.00 $ 570.00

$ 702.13 $ 720.00 $ 585.00

$ 719.68 $ 740.00 $ 595.00

$ 737.67 $ 780.00 $ 610.00

$ 756.11 $ 800.00 $ 625.00

NPV $ 38,728,290.58 $ 44,463,757.08 $ 10,012,019.71

NPV = 0 = Accept or reject

The above criteria helps the investors to decide and evaluate the feasibility of a proposal

(Leung, Springborn, Turner & Brockerhoff, 2014).

Looking at the case of Booli Electronics, the NPV of the project is $38,728,290.58 which is

positive and reasonably higher. According to the above criteria, the company must accept the

project as it will generate positive cash flows in future and will be profitable for the

organization. It also implies that the total shareholder wealth of the firm will increased by that

amount (Refer Appendix 1).

Question 5

Sensitivity analysis is the technique used to measure the changes in the dependent variable

when the values of an independent variable is changes under some set of assumptions. In

other words, it is also known as What-if analysis that it is a way to predict the outcome of the

changes made (Borgonovo, 2017).

As per the calculations done it can be said that NPV is highly sensitive to the changes in the

price of new SSHA. The below table shows the variations in NPV of the project as and when

the prices are increased or decreased.

Base case (prices) Best case (prices) Worst case (prices)

$ 685.00 $ 700.00 $ 570.00

$ 702.13 $ 720.00 $ 585.00

$ 719.68 $ 740.00 $ 595.00

$ 737.67 $ 780.00 $ 610.00

$ 756.11 $ 800.00 $ 625.00

NPV $ 38,728,290.58 $ 44,463,757.08 $ 10,012,019.71

Business finance 6

The above table shows three scenarios that are normal case, best case and worst case

scenarios. All the cases are properly analysed and then the decision is been take.

Normal case: Under this scenario, the selling price of new SSHA are taken as it was

decided by the company. No changes are been made and the NPV is calculated as per

them. The NPV under this situation is $38,728,290 which shows that the project is

profitable and can be accepted.

Best case: This is that case where the amount of NPV is highest with less variations

in the selling price of SSHA. Under this situation, the sale price of the project has

been increased through some extent because of some market factors that influence

prices to a great extent. Due to such upsurge the value of NPV also rises to

$44,463,757.08, making the project more profitable than earlier. This is called best

case scenario because here the NPV is highest which implies that the manufacturing

of new SSHA will generate more profits if sold at increased prices.

Worst case: The circumstances where the net present value of a project is low or

negative and the selling price is also reduced is known as worst case scenario. From

the table it can be said that, in this case the price are been reduced to some extent as

compare to the base case prices and as a result of which, the NPV of the project also

falls to $10,012,019.71 making it less profitable.

So as per the sensitivity analysis, it can be said that the change in the price do have a

significant effect on NPV. From the above three scenarios, the best one is that where the

prices are increased and highest NPV is recorded.

The above table shows three scenarios that are normal case, best case and worst case

scenarios. All the cases are properly analysed and then the decision is been take.

Normal case: Under this scenario, the selling price of new SSHA are taken as it was

decided by the company. No changes are been made and the NPV is calculated as per

them. The NPV under this situation is $38,728,290 which shows that the project is

profitable and can be accepted.

Best case: This is that case where the amount of NPV is highest with less variations

in the selling price of SSHA. Under this situation, the sale price of the project has

been increased through some extent because of some market factors that influence

prices to a great extent. Due to such upsurge the value of NPV also rises to

$44,463,757.08, making the project more profitable than earlier. This is called best

case scenario because here the NPV is highest which implies that the manufacturing

of new SSHA will generate more profits if sold at increased prices.

Worst case: The circumstances where the net present value of a project is low or

negative and the selling price is also reduced is known as worst case scenario. From

the table it can be said that, in this case the price are been reduced to some extent as

compare to the base case prices and as a result of which, the NPV of the project also

falls to $10,012,019.71 making it less profitable.

So as per the sensitivity analysis, it can be said that the change in the price do have a

significant effect on NPV. From the above three scenarios, the best one is that where the

prices are increased and highest NPV is recorded.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business finance 7

Question 6

Fluctuations in selling price affected the NPV to a great extent and so does the changes in

quantity sold. The modification in number of quantity sold of SSHA also impacted its NPV.

The below table show the clear impact of quantity variations.

Base case (Quantity) Changes in quantity

85000 85000

136000 87125

102000 89303

74000 91536

63000 93824

NPV $ 38,728,290.58 $ 34,122,641.37

It can be observed from the table that at the decided quantity of SSHA, the NPV is

$38,728,290.58 keeping the project profitable. However, as and when the quantity sold

changes the NPV also changes. A constant increase can be observed in the changed quantity.

As a result of which, the NPV falls to $34,122,641.37 a compare to the earlier one. Hence, it

can be interpreted that with an increase in the quantity the NPV reduces showing an inverse

effect. While the same in not with the prices. When the prices increase, NPV also rises and

vice versa. Overall, it can be said that changes in both the prices and quantity affect the NPV

negatively and positively.

Question 7

From the capital budgeting analysis following factors are been identified:

Pay-back period is shorter with 2.2 years.

Profitability index is 1.68 which is greater than 1.

Question 6

Fluctuations in selling price affected the NPV to a great extent and so does the changes in

quantity sold. The modification in number of quantity sold of SSHA also impacted its NPV.

The below table show the clear impact of quantity variations.

Base case (Quantity) Changes in quantity

85000 85000

136000 87125

102000 89303

74000 91536

63000 93824

NPV $ 38,728,290.58 $ 34,122,641.37

It can be observed from the table that at the decided quantity of SSHA, the NPV is

$38,728,290.58 keeping the project profitable. However, as and when the quantity sold

changes the NPV also changes. A constant increase can be observed in the changed quantity.

As a result of which, the NPV falls to $34,122,641.37 a compare to the earlier one. Hence, it

can be interpreted that with an increase in the quantity the NPV reduces showing an inverse

effect. While the same in not with the prices. When the prices increase, NPV also rises and

vice versa. Overall, it can be said that changes in both the prices and quantity affect the NPV

negatively and positively.

Question 7

From the capital budgeting analysis following factors are been identified:

Pay-back period is shorter with 2.2 years.

Profitability index is 1.68 which is greater than 1.

Business finance 8

Internal rate of return is 34% which is more than the required rate of return of 11%/

Net present value is positive and high at $38,728,290.58 (Refer Appendix 1).

By considering the above points, Booli Electronics must manufacture the new SSHA as it

will be the most profitable project of the company. It will generate high cash flows as high

IRR, NPV, PI and shorter payback period. Apart from this, the product will made increased

sales during its life (Nichol & Dowling, 2014).

After taking into account the financial factors company also look as the non-financial aspects

of the project. Such as the new SSHA will have several new and unique features like Wi-Fi

tethering and access to a large number of music streaming services including Amazon,

Spotify etc. on the basis of this, Booli should accept this project.

Question 8

The overall sales of Booli can be reduced if the company only focus on the production of new

SSHA. Trying of another model can impact the sales of others. However, as SSHA being the

unique in nature and its production offering more profits to the company, then Booli should

produce this new product. As the introduction of SSHA shows the increasing trend in the

sales of Booli Electronics, the same is reduced later on due to the reduction in quantity. The

way reduction in sales impact the analysis is that it can reduce the profitability of the project

by reducing the value of cash inflows. Then the project will be no longer profitable and may

have low NPV and IRR. So, it can be said that the reduction is sale of other models will leave

a significant impact on the overall analysis for the company (McCombie & Thirlwall, 2016).

Conclusion

From the above report, it can be concluded that capital budgeting techniques are very

important while analysing a particular investment project. The first part of the report

concludes that various methods of investment appraisal are used to evaluate the usefulness of

Internal rate of return is 34% which is more than the required rate of return of 11%/

Net present value is positive and high at $38,728,290.58 (Refer Appendix 1).

By considering the above points, Booli Electronics must manufacture the new SSHA as it

will be the most profitable project of the company. It will generate high cash flows as high

IRR, NPV, PI and shorter payback period. Apart from this, the product will made increased

sales during its life (Nichol & Dowling, 2014).

After taking into account the financial factors company also look as the non-financial aspects

of the project. Such as the new SSHA will have several new and unique features like Wi-Fi

tethering and access to a large number of music streaming services including Amazon,

Spotify etc. on the basis of this, Booli should accept this project.

Question 8

The overall sales of Booli can be reduced if the company only focus on the production of new

SSHA. Trying of another model can impact the sales of others. However, as SSHA being the

unique in nature and its production offering more profits to the company, then Booli should

produce this new product. As the introduction of SSHA shows the increasing trend in the

sales of Booli Electronics, the same is reduced later on due to the reduction in quantity. The

way reduction in sales impact the analysis is that it can reduce the profitability of the project

by reducing the value of cash inflows. Then the project will be no longer profitable and may

have low NPV and IRR. So, it can be said that the reduction is sale of other models will leave

a significant impact on the overall analysis for the company (McCombie & Thirlwall, 2016).

Conclusion

From the above report, it can be concluded that capital budgeting techniques are very

important while analysing a particular investment project. The first part of the report

concludes that various methods of investment appraisal are used to evaluate the usefulness of

Business finance 9

manufacturing new SSHA. It is recommend that the company must go for the production of

the new SSHA as it is economically and financially feasible and also has some unique

features.

The second part of the report deals with the sensitivity analysis of NPV. The outcome of the

analysis is that when the prices rises, the NPV also increases and vice versa. While in case of

quantity change, an inverse effect is there. Increase in quantity reduces the NPV of the

project. Overall, it can be concluded that Booli Electronics Limited must accept this new

production of SSHA.

manufacturing new SSHA. It is recommend that the company must go for the production of

the new SSHA as it is economically and financially feasible and also has some unique

features.

The second part of the report deals with the sensitivity analysis of NPV. The outcome of the

analysis is that when the prices rises, the NPV also increases and vice versa. While in case of

quantity change, an inverse effect is there. Increase in quantity reduces the NPV of the

project. Overall, it can be concluded that Booli Electronics Limited must accept this new

production of SSHA.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Business finance 10

References

Baker, H.K., Jabbouri, I. & Dyaz, C. (2017). Corporate finance practices in

Morocco. Managerial Finance, 43(8), 865-880.

Bierman Jr, H. & Smidt, S. (2014). Advanced capital budgeting: Refinements in the

economic analysis of investment projects. Oxon: Routledge.

Borgonovo, E. (2017). Sensitivity Analysis: An Introduction for the Management

Scientist (Vol. 251). Switzerland: Springer.

Chaysin, P., Daengdej, J. & Tangjitprom, N., (2016). Survey on Available Methods to

Evaluate IT Investment. Electronic Journal Information Systems Evaluation

Volume, 19(1).

Daunfeldt, S.O. & Hartwig, F. (2014). What determines the use of capital budgeting

methods?: Evidence from Swedish listed companies. Journal of Finance and

Economics, 2(4),101-112.

Gotze, U., Northcott, D., & Schuster, P. (2016). INVESTMENT APPRAISAL. (2nd ed.). New

York: Springer.

Leung, B., Springborn, M.R., Turner, J.A. & Brockerhoff, E.G. (2014). Pathway‐level risk

analysis: the net present value of an invasive species policy in the US. Frontiers in

Ecology and the Environment, 12(5), 273-279.

McCombie, J. & Thirlwall, A.P (2016). Economic growth and the balance-of-payments

constraint. New York: Springer.

References

Baker, H.K., Jabbouri, I. & Dyaz, C. (2017). Corporate finance practices in

Morocco. Managerial Finance, 43(8), 865-880.

Bierman Jr, H. & Smidt, S. (2014). Advanced capital budgeting: Refinements in the

economic analysis of investment projects. Oxon: Routledge.

Borgonovo, E. (2017). Sensitivity Analysis: An Introduction for the Management

Scientist (Vol. 251). Switzerland: Springer.

Chaysin, P., Daengdej, J. & Tangjitprom, N., (2016). Survey on Available Methods to

Evaluate IT Investment. Electronic Journal Information Systems Evaluation

Volume, 19(1).

Daunfeldt, S.O. & Hartwig, F. (2014). What determines the use of capital budgeting

methods?: Evidence from Swedish listed companies. Journal of Finance and

Economics, 2(4),101-112.

Gotze, U., Northcott, D., & Schuster, P. (2016). INVESTMENT APPRAISAL. (2nd ed.). New

York: Springer.

Leung, B., Springborn, M.R., Turner, J.A. & Brockerhoff, E.G. (2014). Pathway‐level risk

analysis: the net present value of an invasive species policy in the US. Frontiers in

Ecology and the Environment, 12(5), 273-279.

McCombie, J. & Thirlwall, A.P (2016). Economic growth and the balance-of-payments

constraint. New York: Springer.

Business finance 11

Moyer, R. C., McGuigan, J., Rao, R., & Kretlow, W. (2011). Contemporary financial

management. (13th ed.). USA: Cengage Learning.

Nichol, E. & Dowling, M. (2014). Profitability and investment factors for UK asset pricing

models. Economics Letters, 125(3), 364-366.

Shapiro, A. C. (2008). Capital budgeting and investment analysis. India: Pearson Education.

Venkatesh, M., & Gugloth, D. (2017). A Review of Capital Budgeting Techniques.

International Journal of Economics and Management Studies (Retrieved from

http://www.internationaljournalssrg.org/IJEMS/2017/Special-Issues/ICEEMST/

IJEMS-ICEEMST-P102.pdf

Moyer, R. C., McGuigan, J., Rao, R., & Kretlow, W. (2011). Contemporary financial

management. (13th ed.). USA: Cengage Learning.

Nichol, E. & Dowling, M. (2014). Profitability and investment factors for UK asset pricing

models. Economics Letters, 125(3), 364-366.

Shapiro, A. C. (2008). Capital budgeting and investment analysis. India: Pearson Education.

Venkatesh, M., & Gugloth, D. (2017). A Review of Capital Budgeting Techniques.

International Journal of Economics and Management Studies (Retrieved from

http://www.internationaljournalssrg.org/IJEMS/2017/Special-Issues/ICEEMST/

IJEMS-ICEEMST-P102.pdf

Business finance 12

Appendix

NPV

Years 0 1 2 3 4 5

Cash

outflow

$ -

56,820,000.0

0

Cash

inflow

$

18,955,000

.00

$

33,044,600.0

0

$

24,695,41

1.25

$

17,579,68

5.72

$

37,095,91

4.94

NPV

$

38,728,290.5

8

Payback period

Years Cash flows cumulative

0 $ -56,820,000.00

1 $ 18,955,000.00 $ -37,865,000.00

2 $ 33,044,600.00 $ -4,820,400.00

3 $ 24,695,411.25 $ 19,875,011.25

4 $ 17,579,685.72 $ 37,454,696.97

5 $ 37,095,914.94 $ 74,550,611.91

PBP 2.20

Appendix

NPV

Years 0 1 2 3 4 5

Cash

outflow

$ -

56,820,000.0

0

Cash

inflow

$

18,955,000

.00

$

33,044,600.0

0

$

24,695,41

1.25

$

17,579,68

5.72

$

37,095,91

4.94

NPV

$

38,728,290.5

8

Payback period

Years Cash flows cumulative

0 $ -56,820,000.00

1 $ 18,955,000.00 $ -37,865,000.00

2 $ 33,044,600.00 $ -4,820,400.00

3 $ 24,695,411.25 $ 19,875,011.25

4 $ 17,579,685.72 $ 37,454,696.97

5 $ 37,095,914.94 $ 74,550,611.91

PBP 2.20

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business finance 13

Profitability Index

NPV $ 38,728,290.58

Initial Investment $ -56,820,000.00

PI $ 1.68

IRR

Years Cash flows

0 -56820000

1 $ 18,955,000.00

2 $ 33,044,600.00

3 $ 24,695,411.25

4 $ 17,579,685.72

5 $ 37,095,914.94

IRR 34%

Profitability Index

NPV $ 38,728,290.58

Initial Investment $ -56,820,000.00

PI $ 1.68

IRR

Years Cash flows

0 -56820000

1 $ 18,955,000.00

2 $ 33,044,600.00

3 $ 24,695,411.25

4 $ 17,579,685.72

5 $ 37,095,914.94

IRR 34%

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.