BAC221 Business Finance Assignment: WACC and NPV Analysis

VerifiedAdded on 2022/10/02

|8

|1375

|97

Homework Assignment

AI Summary

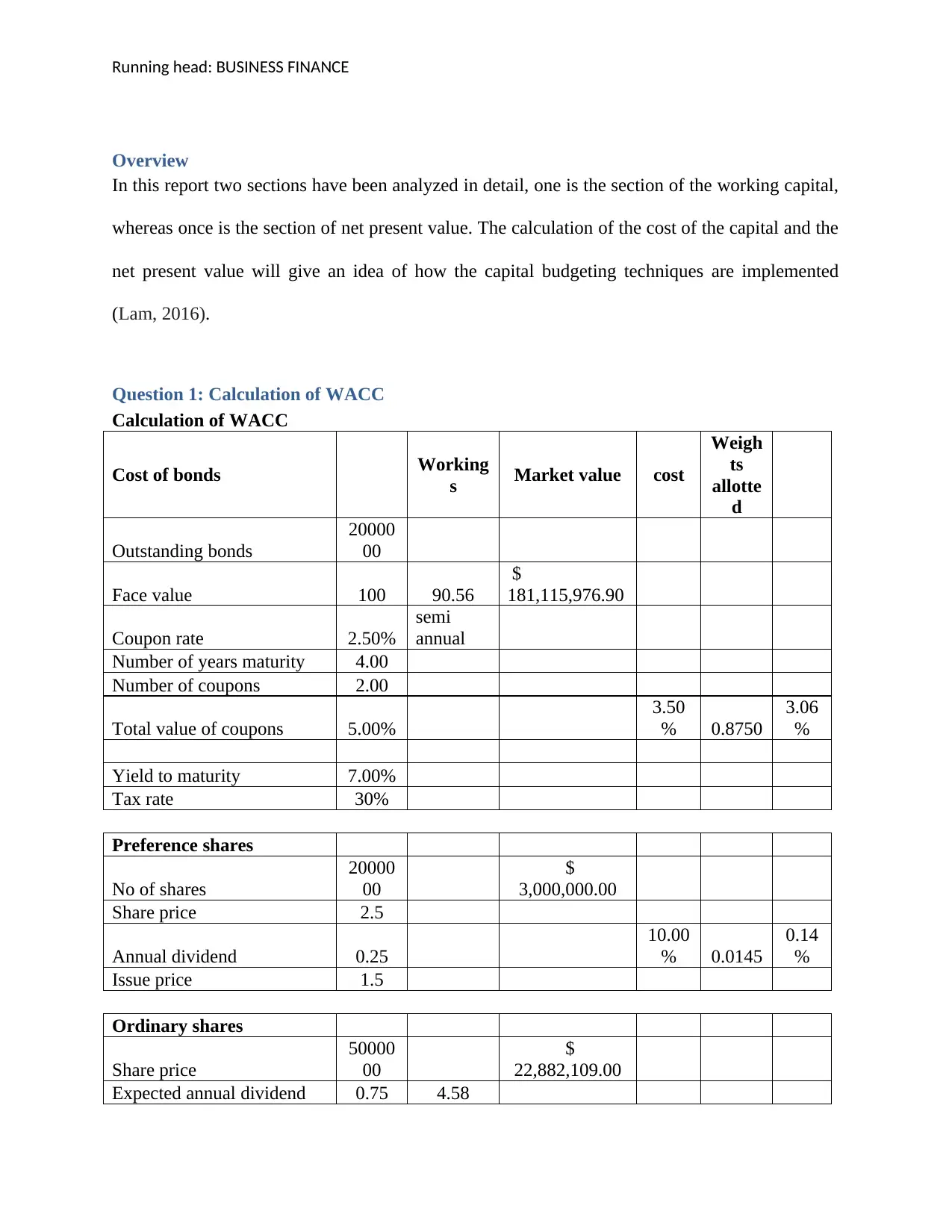

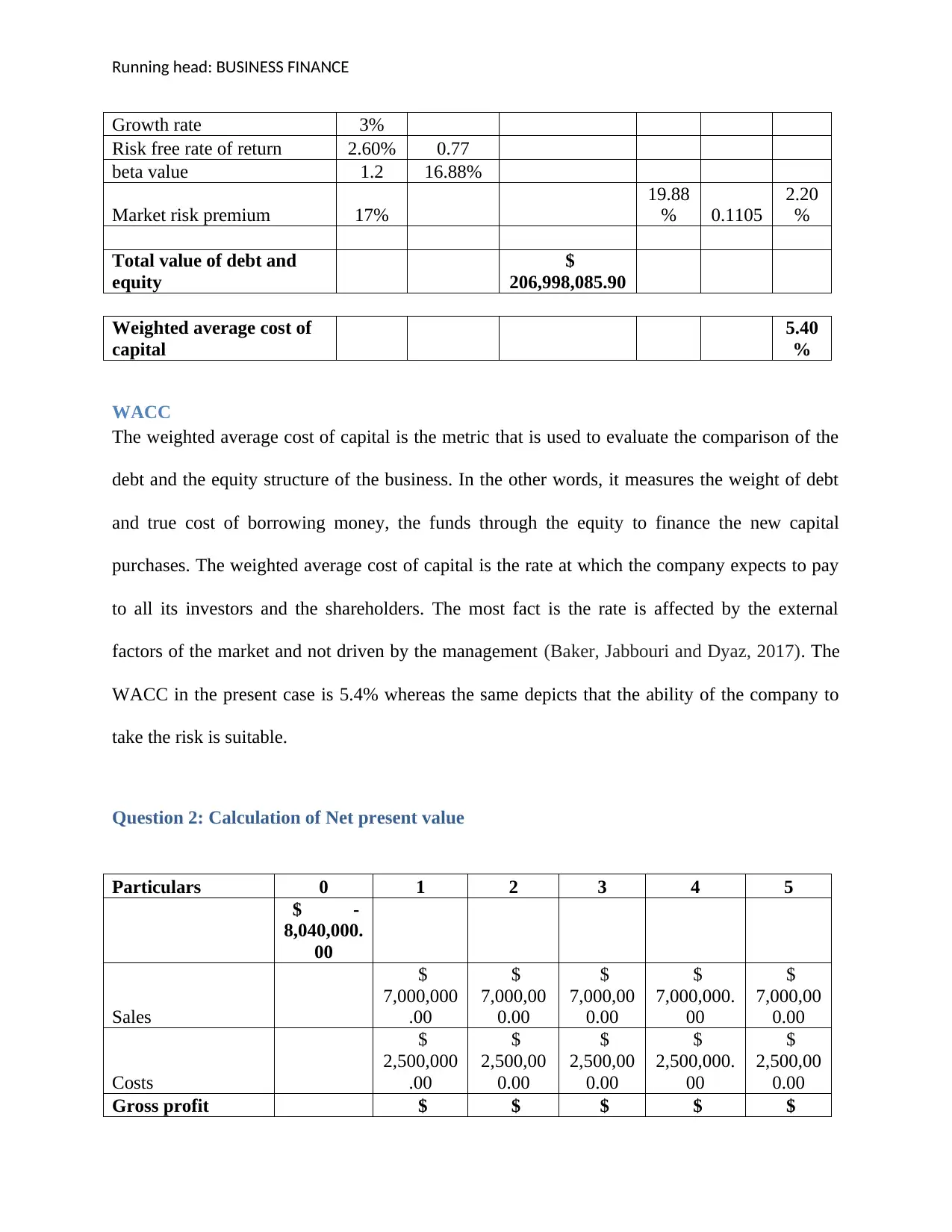

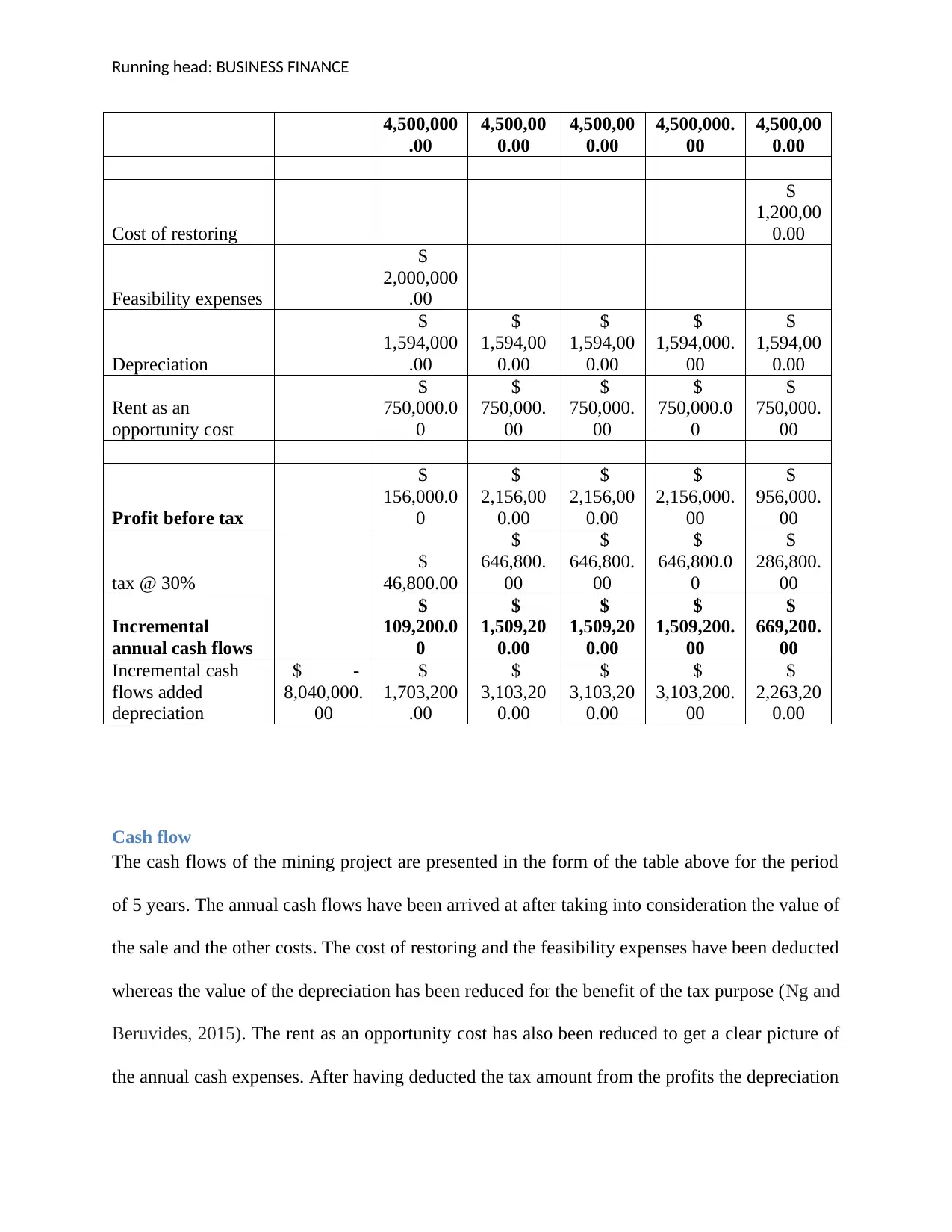

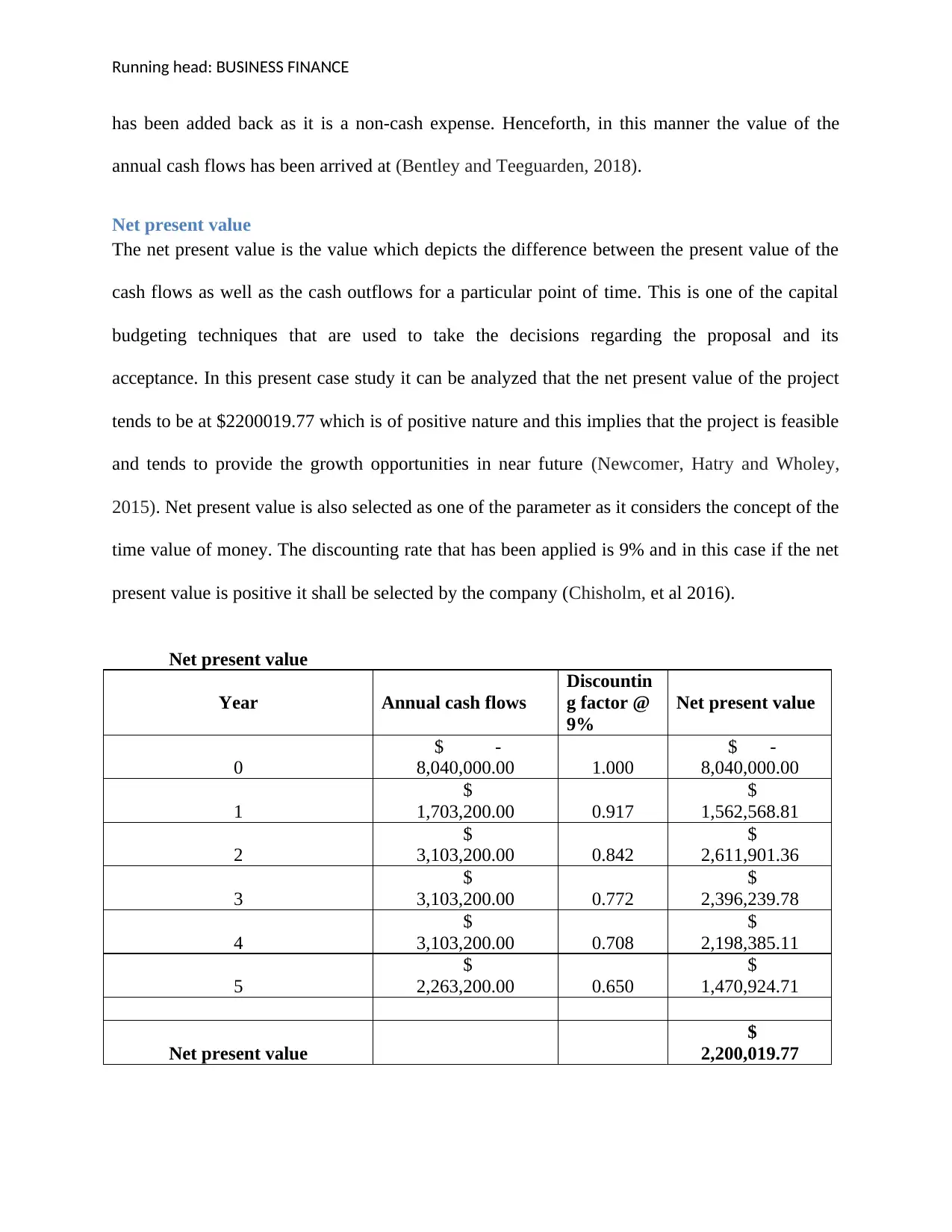

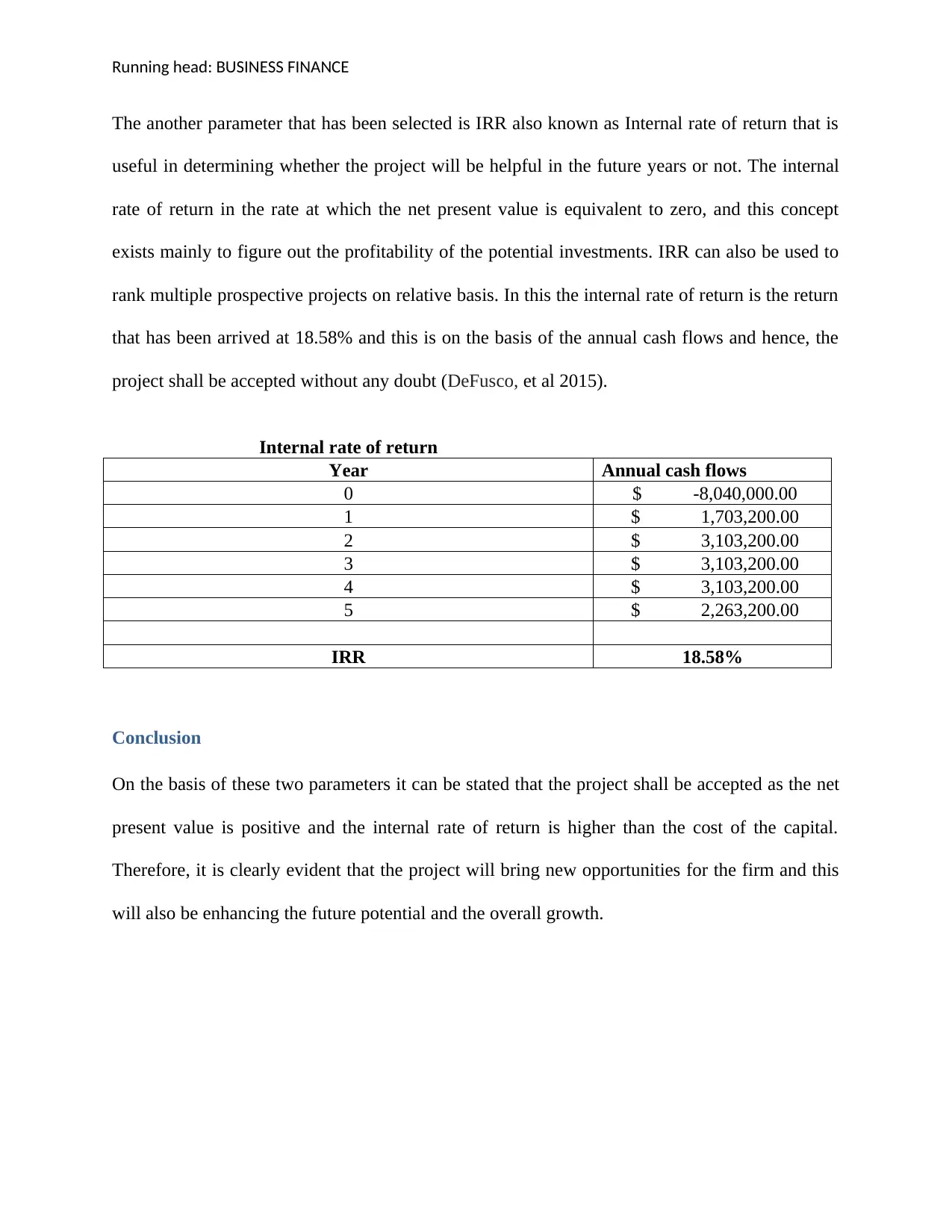

This report presents a detailed analysis of a business finance assignment, focusing on the calculation of the Weighted Average Cost of Capital (WACC) and Net Present Value (NPV). The assignment utilizes data related to Quick Investments Ltd., including bond information, preference shares, and ordinary shares, to determine the WACC. The report then calculates the NPV of a mining project over a five-year period, considering sales, costs, depreciation, and tax implications. Furthermore, the Internal Rate of Return (IRR) is calculated to evaluate the project's profitability. The analysis concludes that the project is financially viable, offering growth opportunities, as the NPV is positive and the IRR exceeds the cost of capital. The report highlights the application of capital budgeting techniques and provides a comprehensive understanding of financial decision-making.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.