Finance Report: Evaluating Costing, Analyzing Variance & Budgeting

VerifiedAdded on 2023/06/10

|11

|1999

|343

Report

AI Summary

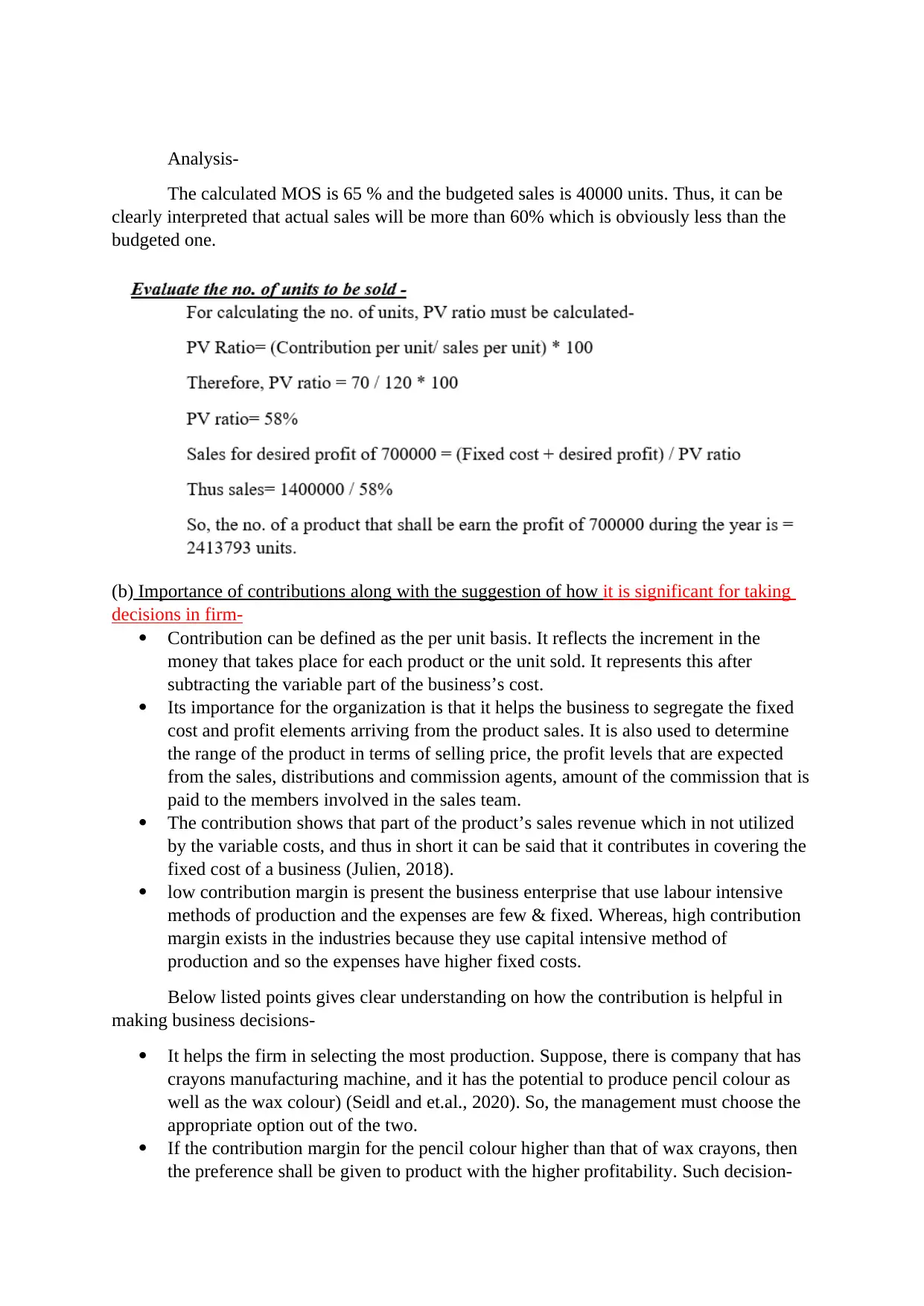

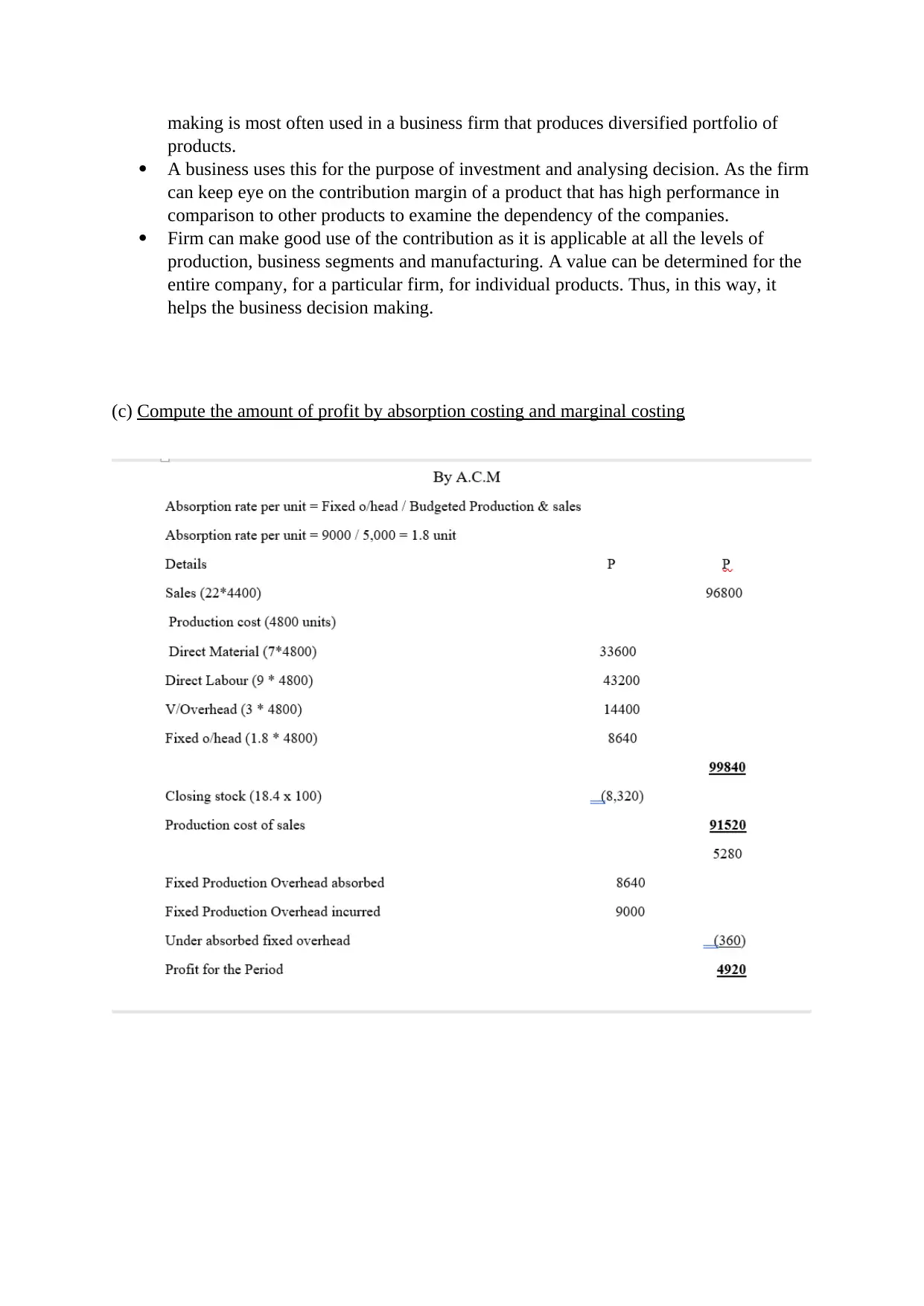

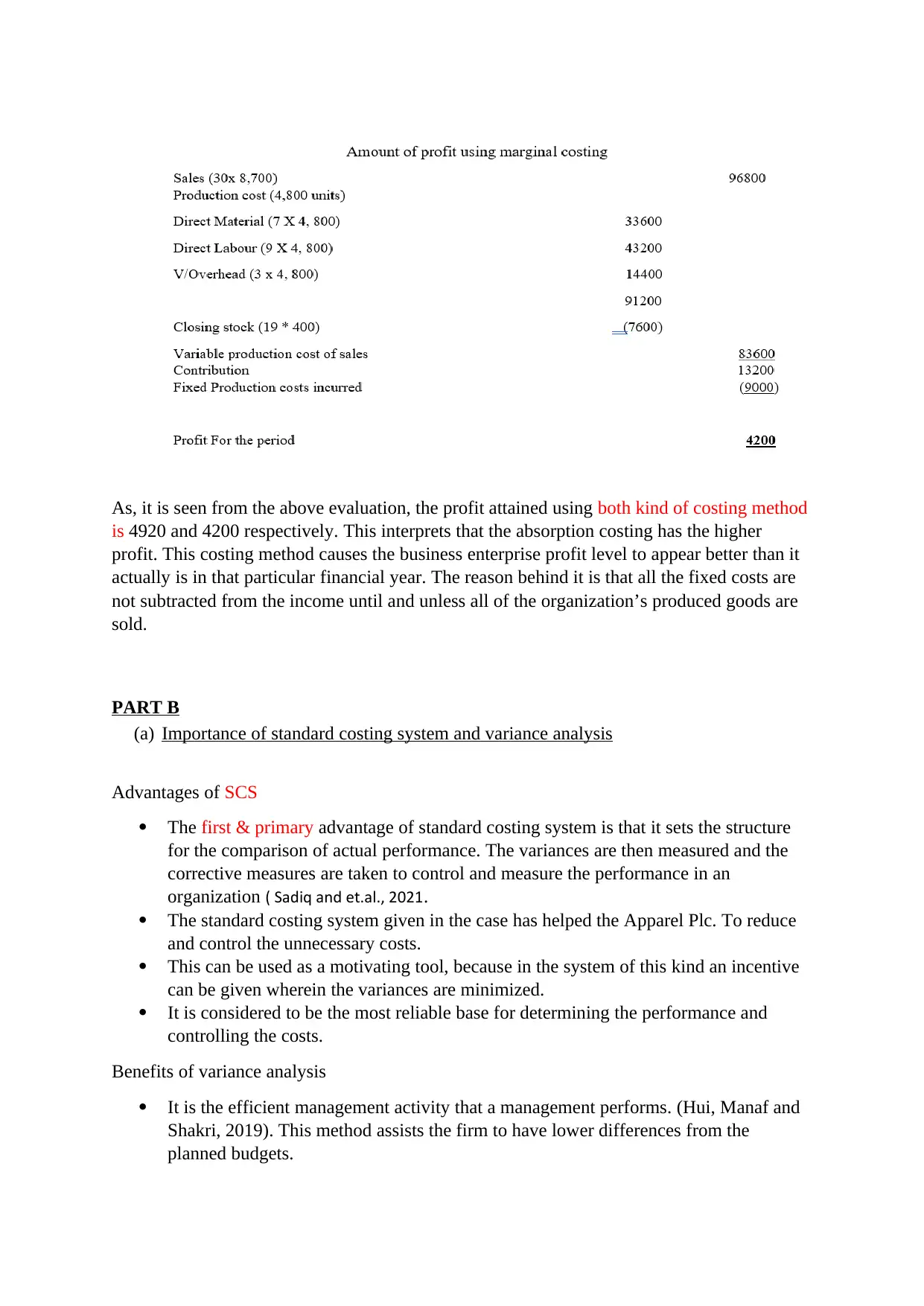

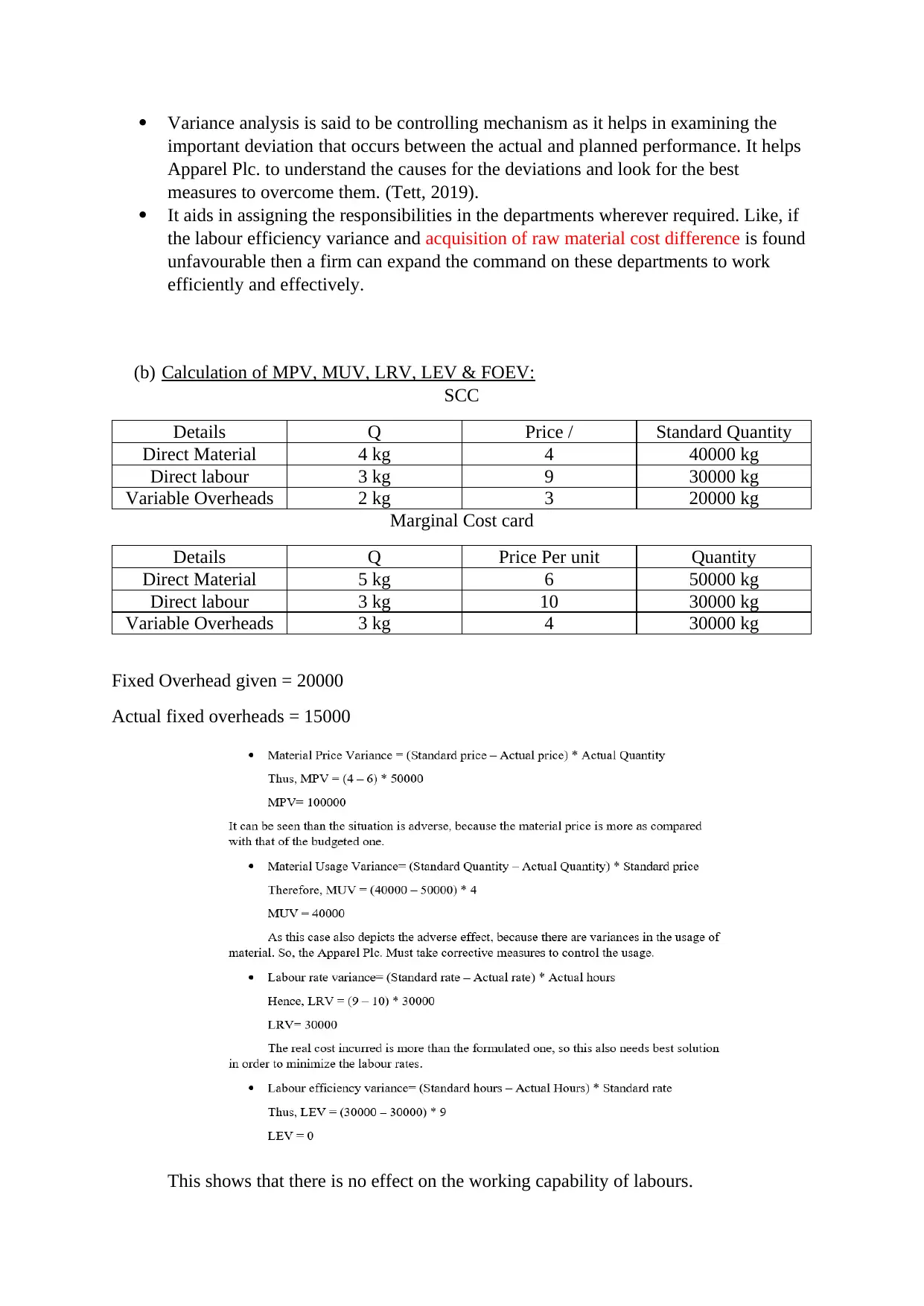

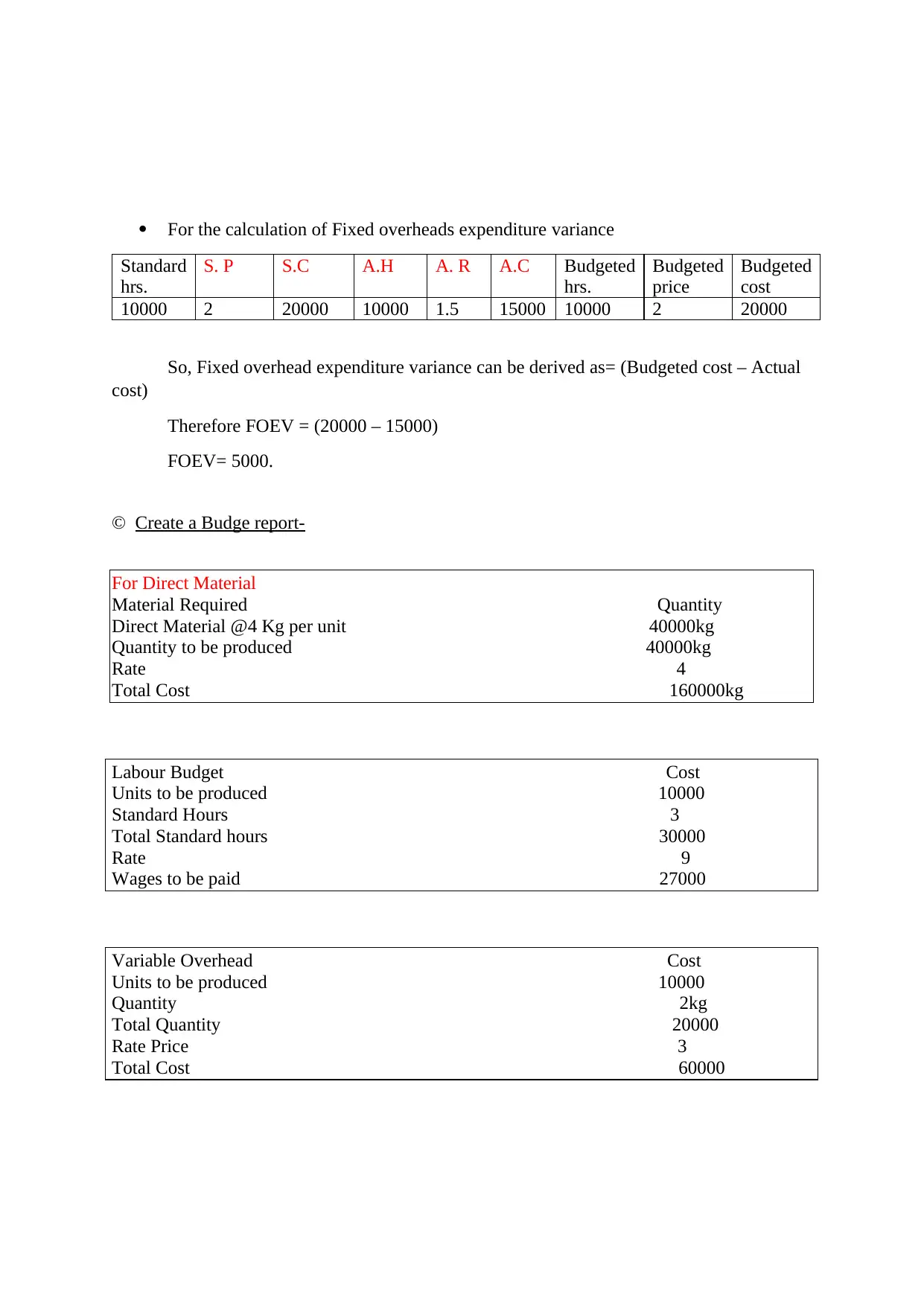

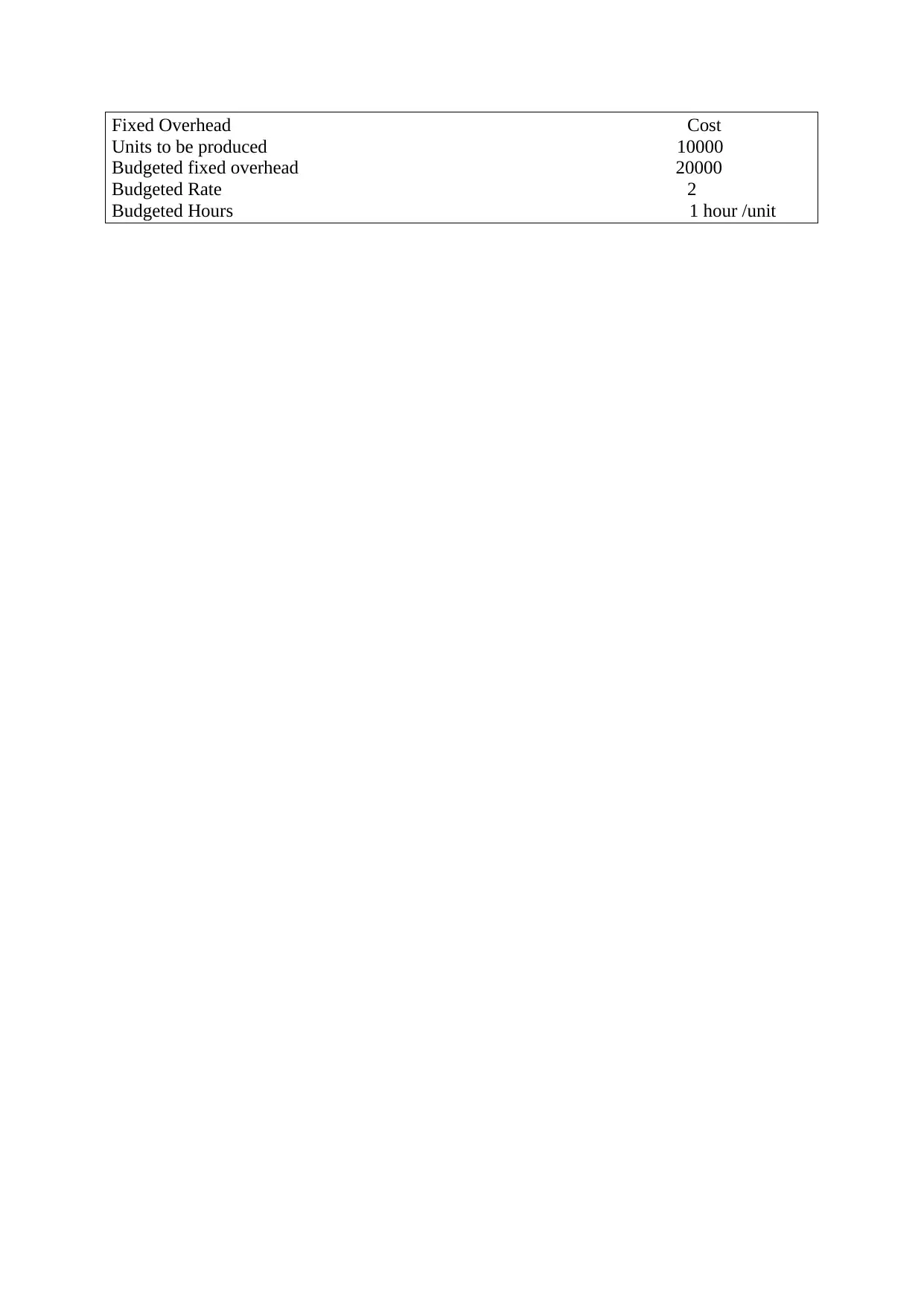

This report provides a detailed analysis of business finance concepts, focusing on costing methods (absorption and marginal costing), variance analysis, and budgeting. It evaluates the contribution per unit, break-even point (BEP), and margin of safety (MOS), highlighting the importance of contribution in business decision-making. The report computes profit using both absorption and marginal costing methods and discusses the advantages of standard costing systems and variance analysis. Furthermore, it includes calculations for material price variance (MPV), material usage variance (MUV), labor rate variance (LRV), labor efficiency variance (LEV), and fixed overhead expenditure variance (FOEV). The report concludes with the preparation of a budget for Apparel Plc, based on the standard cost card, emphasizing the role of these financial tools in identifying deviations and implementing corrective measures to achieve fiscal goals.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.