ACC211: Booli Enterprise Manufacturing of Electronic Goods PDF 2023

VerifiedAdded on 2021/06/18

|17

|3051

|64

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Business Finance

1

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

INTRODUCTION.................................................................................................................................3

FINANCIAL VIABILITY OF THE PROJECT....................................................................................4

Non-Discounted Pay-Back Period.....................................................................................................4

Profitability Index..............................................................................................................................4

Internal Rate of Return......................................................................................................................4

Net Present Value..............................................................................................................................4

SENSITIVITY ANALYSIS..................................................................................................................5

Change in sales price.........................................................................................................................5

Change in sales quantity....................................................................................................................5

EFFECT OF LOSS OF SALE OF OTHER MODELS DUE TO NEW PROJECT...............................7

CONCLUSION AND RECOMMENDATION.....................................................................................8

Bibliography..........................................................................................................................................9

Appendix.............................................................................................................................................10

2

INTRODUCTION.................................................................................................................................3

FINANCIAL VIABILITY OF THE PROJECT....................................................................................4

Non-Discounted Pay-Back Period.....................................................................................................4

Profitability Index..............................................................................................................................4

Internal Rate of Return......................................................................................................................4

Net Present Value..............................................................................................................................4

SENSITIVITY ANALYSIS..................................................................................................................5

Change in sales price.........................................................................................................................5

Change in sales quantity....................................................................................................................5

EFFECT OF LOSS OF SALE OF OTHER MODELS DUE TO NEW PROJECT...............................7

CONCLUSION AND RECOMMENDATION.....................................................................................8

Bibliography..........................................................................................................................................9

Appendix.............................................................................................................................................10

2

INTRODUCTION

In the given scenario we see that the company Booli Ltd which has been involved in the

production of electronic items wants to introduce in the market a new product. Introduction

of a new project required detailed analysis and research on the same. (Seal, 2012)We have

implemented a few capital budgeting techniques for the said proposal in order to evaluate the

profitability of the same. Capital budgeting tool is a financial tool which helps us evaluate the

viability of an investment option. (Adelaja, 2015)This is based on lot of assumptions and

rules. It is important that all these rules are kept in mind while implanting this technique.

3

In the given scenario we see that the company Booli Ltd which has been involved in the

production of electronic items wants to introduce in the market a new product. Introduction

of a new project required detailed analysis and research on the same. (Seal, 2012)We have

implemented a few capital budgeting techniques for the said proposal in order to evaluate the

profitability of the same. Capital budgeting tool is a financial tool which helps us evaluate the

viability of an investment option. (Adelaja, 2015)This is based on lot of assumptions and

rules. It is important that all these rules are kept in mind while implanting this technique.

3

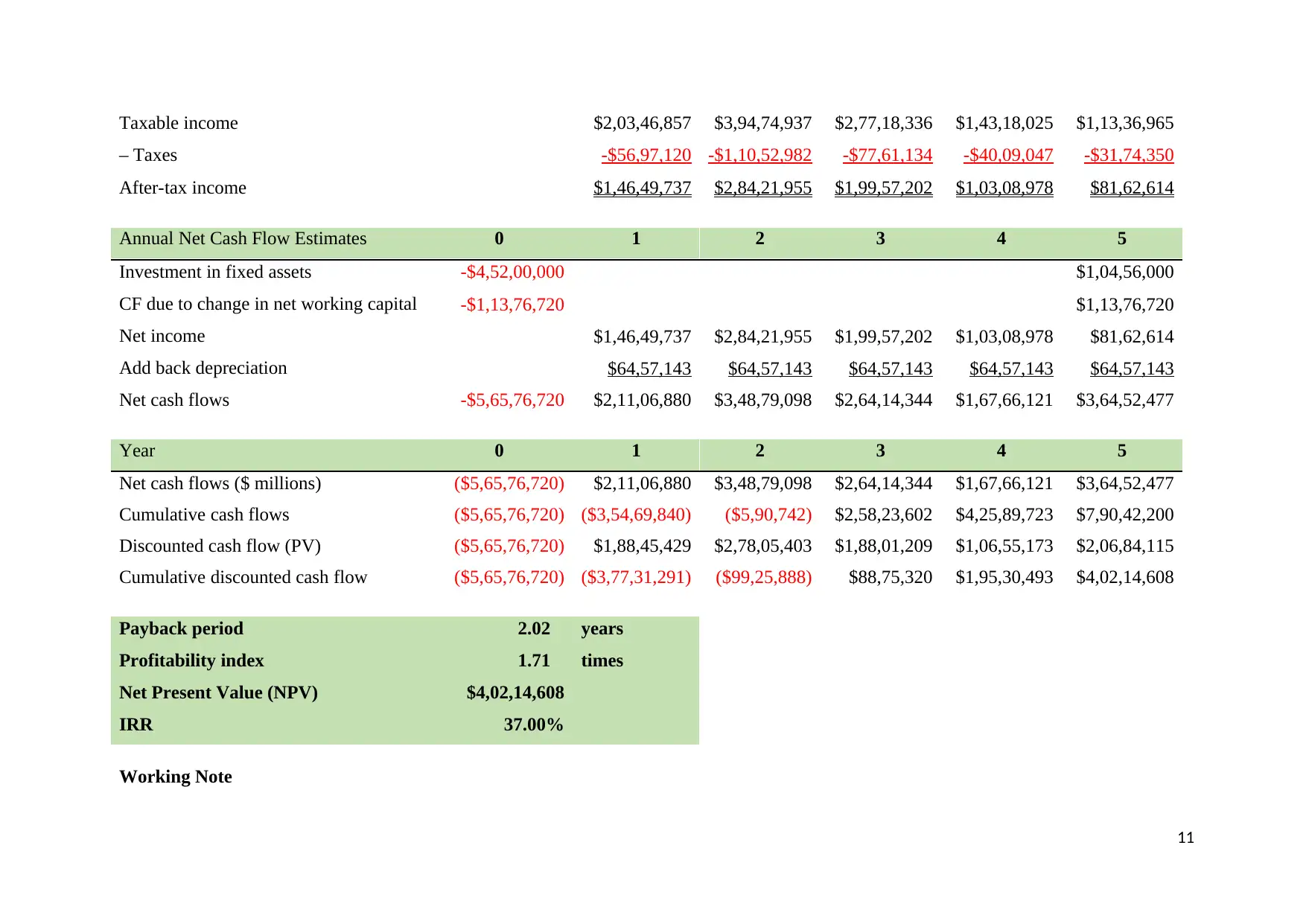

FINANCIAL VIABILITY OF THE PROJECT

Non-Discounted Pay-Back Period

Pay-back period is the capital budgeting tool that helps the investor estimate the time period

in which he would recover the invested amount in a project (Atkinson, 2012). The cash flows

generated from a project after the pay-back period contribute towards the profit of the

investor.

For the given case the pay-back period of the project is 2.02 years, with the project life of 5

years. This means that the project will recover the initial investment amount within 2.02 years

and any earning beyond this will be profit for the company.

Profitability Index

Profitability index is the return ratio which provides the investor with an estimated amount of

return per unit of investment made by the investor. (Berry, 2009)The project of Booli ltd has

a Profitability index of 1.71 times. This indicates that the project will earn 1.71 for every

dollar invested. Since the amount earned is more than invested the project seems viable.

Internal Rate of Return

Internal rate of return calculate the actual return earned on project based on the estimated

cash flows. (Bierman & Smidt, 2010) The internal rate of return of the for the project

amounts to 37% percent, when the required rate of return for the project is 12%. Since the

project is earning more than the expected rate the project seems financially viable.

Net Present Value

Net present value is the sum total of present values of cash inflows and outflows.

(Dayananda, Irons, Harrison, Herbohn, & Rowland, 2008) Positive NPV indicates creation of

value and negation indicates loss. For the given project for Booli ltd the Net present value

amount to $40.2 million. Since the project is expected to create value for the firm, it should

be accepted.

4

Non-Discounted Pay-Back Period

Pay-back period is the capital budgeting tool that helps the investor estimate the time period

in which he would recover the invested amount in a project (Atkinson, 2012). The cash flows

generated from a project after the pay-back period contribute towards the profit of the

investor.

For the given case the pay-back period of the project is 2.02 years, with the project life of 5

years. This means that the project will recover the initial investment amount within 2.02 years

and any earning beyond this will be profit for the company.

Profitability Index

Profitability index is the return ratio which provides the investor with an estimated amount of

return per unit of investment made by the investor. (Berry, 2009)The project of Booli ltd has

a Profitability index of 1.71 times. This indicates that the project will earn 1.71 for every

dollar invested. Since the amount earned is more than invested the project seems viable.

Internal Rate of Return

Internal rate of return calculate the actual return earned on project based on the estimated

cash flows. (Bierman & Smidt, 2010) The internal rate of return of the for the project

amounts to 37% percent, when the required rate of return for the project is 12%. Since the

project is earning more than the expected rate the project seems financially viable.

Net Present Value

Net present value is the sum total of present values of cash inflows and outflows.

(Dayananda, Irons, Harrison, Herbohn, & Rowland, 2008) Positive NPV indicates creation of

value and negation indicates loss. For the given project for Booli ltd the Net present value

amount to $40.2 million. Since the project is expected to create value for the firm, it should

be accepted.

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

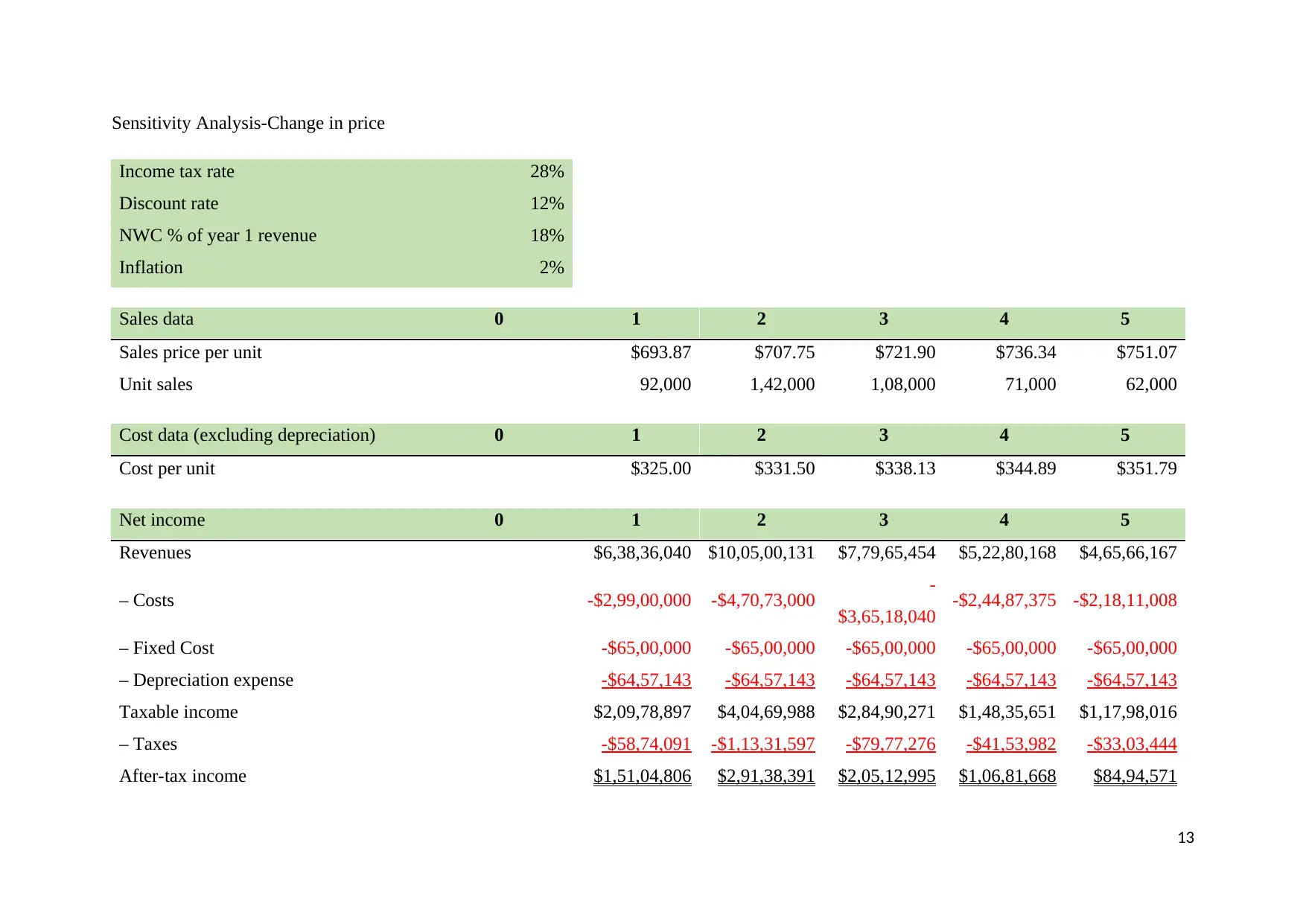

SENSITIVITY ANALYSIS

The process of sensitivity analysis helps the investor evaluate the effect of change in

independent variable on the dependent variables (Menifield, 2014). This process helps us

calculate the variance in the expected result of the investment if any changes in the

assumption for the investment are made. In our discussion following, we have discussed

about the sensitivity of the project output with respect to change in the sales price and the

units sold.

Change in sales price

In our discussion below we have calculated the effect of change in price of the product on

other outputs which have been discussed above.

We have increased the sale price of the product by 1% in order to evaluate the effect of

change. Increase in sale price leads to increase in cash flows, which in turn increases the net

present value. The net present value increased by 4.35%. The net present value earlier was $

40.2 million; effect of increase in sale price increased the NPV to $ 41.9 million. Also,

increase in sales price has the following effects:

- Effect on IRR- the IRR increased from 37% to 38%. Increase of 1% in price results an

increase of 2.67% in IRR

- Effect on Pay-back period- the pay-back period decreases from 2.02 years to 1.99 years.

Increase in 1% in price results a decrease of 1.75% in pay-back period.

- Effect on profitability index- the profitability index increases from 1.71 to 1.74 times. An

increase of 1% in sales price increases the profitability index by 1.77%

The variable which was most affected by change in sales price is the net present value. Even

a small change in the price of the product is likely to have a huge impact on the net present

value of the proposed project.

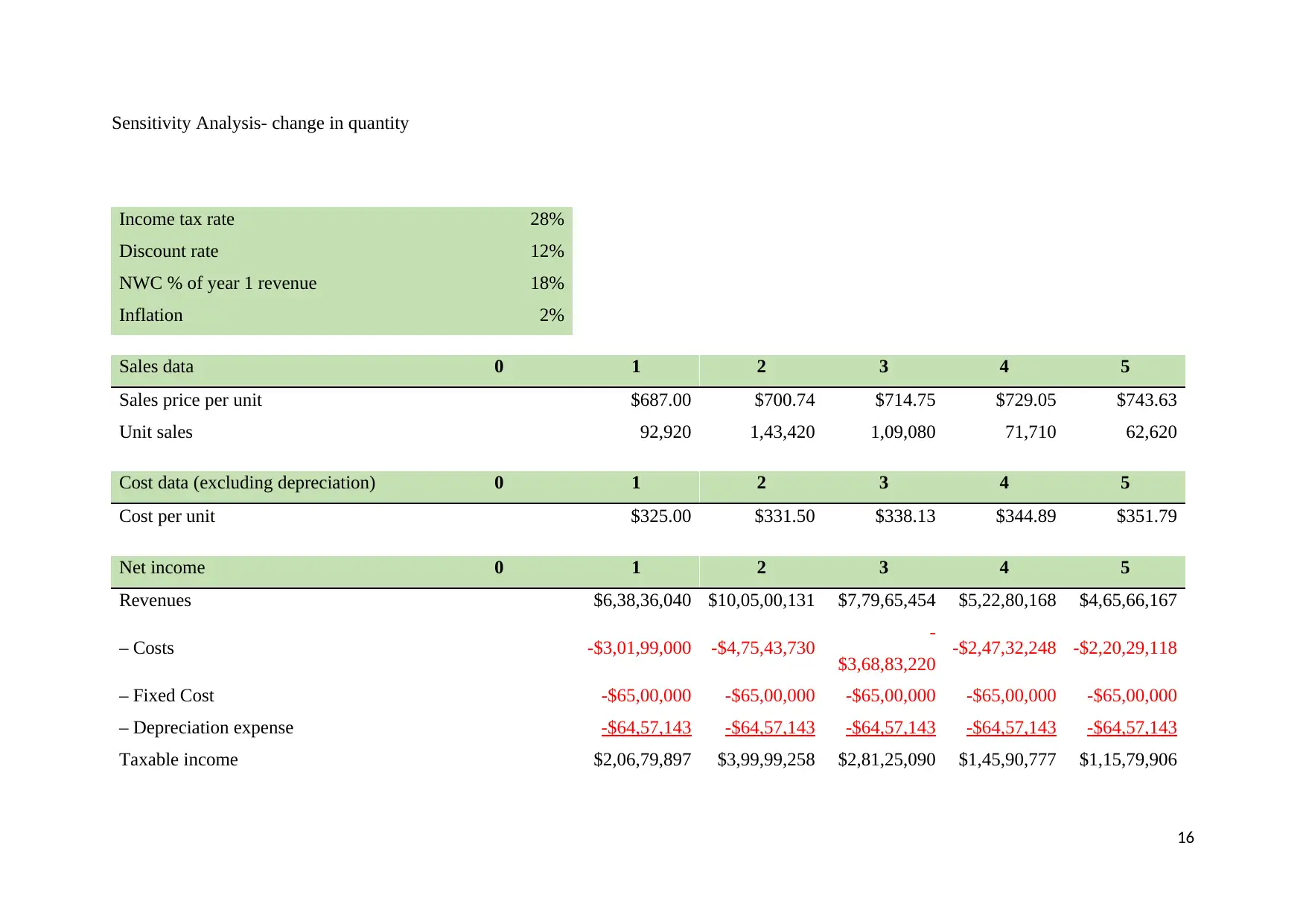

Change in sales quantity

In our discussion below we have calculated the effect of change in sales quantity of the

product on other outputs which have been discussed above.

We have increased the sale quantity of the product by 1% in order to evaluate the effect of

change. Increase in sale quantity leads to increase in cash flows, which in turn increases the

5

The process of sensitivity analysis helps the investor evaluate the effect of change in

independent variable on the dependent variables (Menifield, 2014). This process helps us

calculate the variance in the expected result of the investment if any changes in the

assumption for the investment are made. In our discussion following, we have discussed

about the sensitivity of the project output with respect to change in the sales price and the

units sold.

Change in sales price

In our discussion below we have calculated the effect of change in price of the product on

other outputs which have been discussed above.

We have increased the sale price of the product by 1% in order to evaluate the effect of

change. Increase in sale price leads to increase in cash flows, which in turn increases the net

present value. The net present value increased by 4.35%. The net present value earlier was $

40.2 million; effect of increase in sale price increased the NPV to $ 41.9 million. Also,

increase in sales price has the following effects:

- Effect on IRR- the IRR increased from 37% to 38%. Increase of 1% in price results an

increase of 2.67% in IRR

- Effect on Pay-back period- the pay-back period decreases from 2.02 years to 1.99 years.

Increase in 1% in price results a decrease of 1.75% in pay-back period.

- Effect on profitability index- the profitability index increases from 1.71 to 1.74 times. An

increase of 1% in sales price increases the profitability index by 1.77%

The variable which was most affected by change in sales price is the net present value. Even

a small change in the price of the product is likely to have a huge impact on the net present

value of the proposed project.

Change in sales quantity

In our discussion below we have calculated the effect of change in sales quantity of the

product on other outputs which have been discussed above.

We have increased the sale quantity of the product by 1% in order to evaluate the effect of

change. Increase in sale quantity leads to increase in cash flows, which in turn increases the

5

net present value. The net present value increased by 2.23%. The net present value earlier

was $ 40.2 million; effect of increase in sale quantity increased the NPV to $ 41.1 million.

Also, increase in sales quantity has the following effects:

- Effect on IRR- the IRR increased from 37% to 37.47%. Increase of 1% in price results an

increase of 1.30% in IRR

- Effect on Pay-back period- the pay-back period decreases from 2.02 years to 2 years.

Increase in 1% in price results a decrease of 0.94% in pay-back period.

- Effect on profitability index- the profitability index increases from 1.71 to 1.73 times. An

increase of 1% in sales price increases the profitability index by 0.89%

The variable which was most affected by change in sales quantity is the net present value.

Even a small change in the quantity of the product is likely to have a huge impact on the net

present value of the proposed project.

The figures used in capital budgeting decision are all based on detailed market research. The

inputs and the outputs are pre determined based on assumptions and research. This not the

actual data and in no way does this implicate that the result that will be achieved will be

same as expected. (Noreen, 2015) This execution of capital budgeting technique is a risky

work. Change in the inputs has a huge impact on the result of the investment. There is always

an uncertainty risk involved in this execution. (Rivenbark, Vogt, & Marlowe, 2009) The

project when analysed should be taken care of the uncertainties that are involved. The market

is dynamic and the results may not turn out as expected. Therefore sensitivity analysis helps

us have an idea of how these variables can affect the output.

6

was $ 40.2 million; effect of increase in sale quantity increased the NPV to $ 41.1 million.

Also, increase in sales quantity has the following effects:

- Effect on IRR- the IRR increased from 37% to 37.47%. Increase of 1% in price results an

increase of 1.30% in IRR

- Effect on Pay-back period- the pay-back period decreases from 2.02 years to 2 years.

Increase in 1% in price results a decrease of 0.94% in pay-back period.

- Effect on profitability index- the profitability index increases from 1.71 to 1.73 times. An

increase of 1% in sales price increases the profitability index by 0.89%

The variable which was most affected by change in sales quantity is the net present value.

Even a small change in the quantity of the product is likely to have a huge impact on the net

present value of the proposed project.

The figures used in capital budgeting decision are all based on detailed market research. The

inputs and the outputs are pre determined based on assumptions and research. This not the

actual data and in no way does this implicate that the result that will be achieved will be

same as expected. (Noreen, 2015) This execution of capital budgeting technique is a risky

work. Change in the inputs has a huge impact on the result of the investment. There is always

an uncertainty risk involved in this execution. (Rivenbark, Vogt, & Marlowe, 2009) The

project when analysed should be taken care of the uncertainties that are involved. The market

is dynamic and the results may not turn out as expected. Therefore sensitivity analysis helps

us have an idea of how these variables can affect the output.

6

EFFECT OF LOSS OF SALE OF OTHER MODELS DUE TO NEW PROJECT

There are certain costs which affect our decision of acceptance or rejection of investment

proposal. The expenses which have already been occurred do not form part of capital

budgeting decision as acceptance or rejection of the project will not affect the validity of the

expenses already incurred (Peterson & Fabozzi, 2012). In case the investor has to let go any

of his existing incomes due to acceptance of the project, then loss of such income should be

included in the analysis.

In the given case Booli ltd might loose sales of existing product due to introduction of new

product. This cost of this should be included in the analysis. This might reduce the returns

from the new investment opportunity.

7

There are certain costs which affect our decision of acceptance or rejection of investment

proposal. The expenses which have already been occurred do not form part of capital

budgeting decision as acceptance or rejection of the project will not affect the validity of the

expenses already incurred (Peterson & Fabozzi, 2012). In case the investor has to let go any

of his existing incomes due to acceptance of the project, then loss of such income should be

included in the analysis.

In the given case Booli ltd might loose sales of existing product due to introduction of new

product. This cost of this should be included in the analysis. This might reduce the returns

from the new investment opportunity.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONCLUSION AND RECOMMENDATION

The calculations made above conclude that the project is likely to create positive wealth for

Booli ltd. The project has a high net present value, with a good internal rate of return and low

pay back period. The project seems viable form the financial perspective. The returns on the

project are expected to be higher than the cost of the project.

Therefore, the project seems to create value for the company, and seems viable. Hence the

project should be accepted.

8

The calculations made above conclude that the project is likely to create positive wealth for

Booli ltd. The project has a high net present value, with a good internal rate of return and low

pay back period. The project seems viable form the financial perspective. The returns on the

project are expected to be higher than the cost of the project.

Therefore, the project seems to create value for the company, and seems viable. Hence the

project should be accepted.

8

Bibliography

Adelaja, T. (2015). Capital Budgeting: Investment Appraisal Techniques Under Certainty.

Chicago: CreateSpace Independent Publishing Platform .

Atkinson, A. A. (2012). Management accounting. Upper Saddle River, N.J.: Paerson.

Berry, L. E. (2009). Management accounting demystified. New York: McGraw-Hill.

Bierman, H., & Smidt, S. (2010). The Capital Budgeting Decision. Boston: Routledge.

Dayananda, D., Irons, R., Harrison, S., Herbohn, J., & Rowland, P. (2008). Capital

Budgeting: Financial Appraisal of Investment Projects. Cambridge: Cambridge University

Press.

Menifield, C. E. (2014). The Basics of Public Budgeting and Financial Management: A

Handbook for Academics and Practitioners. Lanham, Md.: University Press of America.

Noreen, E. (2015). The theory of constraints and its implications for management accounting.

Great Barrington, MA: North River Press.

Peterson, P. P., & Fabozzi, F. J. (2012). Capital Budgeting. New York, NY: Wiley.

Rivenbark, W. C., Vogt, J., & Marlowe, J. (2009). Capital Budgeting and Finance: A Guide

for Local Governments. Washington, D.C.: ICMA Press.

Seal, W. (2012). Management accounting. Maidenhead: McGraw-Hill Higher Education.

9

Adelaja, T. (2015). Capital Budgeting: Investment Appraisal Techniques Under Certainty.

Chicago: CreateSpace Independent Publishing Platform .

Atkinson, A. A. (2012). Management accounting. Upper Saddle River, N.J.: Paerson.

Berry, L. E. (2009). Management accounting demystified. New York: McGraw-Hill.

Bierman, H., & Smidt, S. (2010). The Capital Budgeting Decision. Boston: Routledge.

Dayananda, D., Irons, R., Harrison, S., Herbohn, J., & Rowland, P. (2008). Capital

Budgeting: Financial Appraisal of Investment Projects. Cambridge: Cambridge University

Press.

Menifield, C. E. (2014). The Basics of Public Budgeting and Financial Management: A

Handbook for Academics and Practitioners. Lanham, Md.: University Press of America.

Noreen, E. (2015). The theory of constraints and its implications for management accounting.

Great Barrington, MA: North River Press.

Peterson, P. P., & Fabozzi, F. J. (2012). Capital Budgeting. New York, NY: Wiley.

Rivenbark, W. C., Vogt, J., & Marlowe, J. (2009). Capital Budgeting and Finance: A Guide

for Local Governments. Washington, D.C.: ICMA Press.

Seal, W. (2012). Management accounting. Maidenhead: McGraw-Hill Higher Education.

9

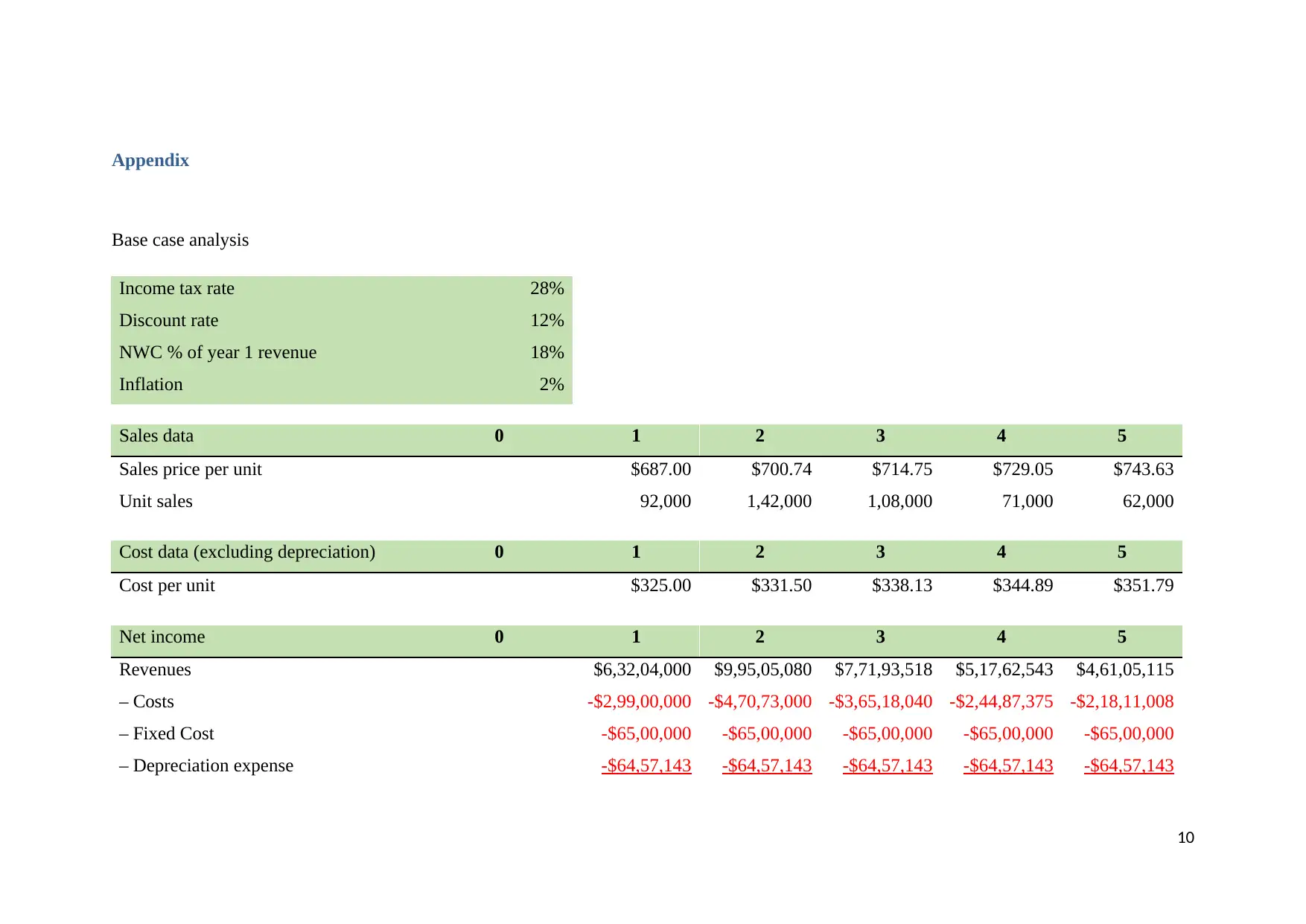

Appendix

Base case analysis

Income tax rate 28%

Discount rate 12%

NWC % of year 1 revenue 18%

Inflation 2%

Sales data 0 1 2 3 4 5

Sales price per unit $687.00 $700.74 $714.75 $729.05 $743.63

Unit sales 92,000 1,42,000 1,08,000 71,000 62,000

Cost data (excluding depreciation) 0 1 2 3 4 5

Cost per unit $325.00 $331.50 $338.13 $344.89 $351.79

Net income 0 1 2 3 4 5

Revenues $6,32,04,000 $9,95,05,080 $7,71,93,518 $5,17,62,543 $4,61,05,115

– Costs -$2,99,00,000 -$4,70,73,000 -$3,65,18,040 -$2,44,87,375 -$2,18,11,008

– Fixed Cost -$65,00,000 -$65,00,000 -$65,00,000 -$65,00,000 -$65,00,000

– Depreciation expense -$64,57,143 -$64,57,143 -$64,57,143 -$64,57,143 -$64,57,143

10

Base case analysis

Income tax rate 28%

Discount rate 12%

NWC % of year 1 revenue 18%

Inflation 2%

Sales data 0 1 2 3 4 5

Sales price per unit $687.00 $700.74 $714.75 $729.05 $743.63

Unit sales 92,000 1,42,000 1,08,000 71,000 62,000

Cost data (excluding depreciation) 0 1 2 3 4 5

Cost per unit $325.00 $331.50 $338.13 $344.89 $351.79

Net income 0 1 2 3 4 5

Revenues $6,32,04,000 $9,95,05,080 $7,71,93,518 $5,17,62,543 $4,61,05,115

– Costs -$2,99,00,000 -$4,70,73,000 -$3,65,18,040 -$2,44,87,375 -$2,18,11,008

– Fixed Cost -$65,00,000 -$65,00,000 -$65,00,000 -$65,00,000 -$65,00,000

– Depreciation expense -$64,57,143 -$64,57,143 -$64,57,143 -$64,57,143 -$64,57,143

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Taxable income $2,03,46,857 $3,94,74,937 $2,77,18,336 $1,43,18,025 $1,13,36,965

– Taxes -$56,97,120 -$1,10,52,982 -$77,61,134 -$40,09,047 -$31,74,350

After-tax income $1,46,49,737 $2,84,21,955 $1,99,57,202 $1,03,08,978 $81,62,614

Annual Net Cash Flow Estimates 0 1 2 3 4 5

Investment in fixed assets -$4,52,00,000 $1,04,56,000

CF due to change in net working capital -$1,13,76,720 $1,13,76,720

Net income $1,46,49,737 $2,84,21,955 $1,99,57,202 $1,03,08,978 $81,62,614

Add back depreciation $64,57,143 $64,57,143 $64,57,143 $64,57,143 $64,57,143

Net cash flows -$5,65,76,720 $2,11,06,880 $3,48,79,098 $2,64,14,344 $1,67,66,121 $3,64,52,477

Year 0 1 2 3 4 5

Net cash flows ($ millions) ($5,65,76,720) $2,11,06,880 $3,48,79,098 $2,64,14,344 $1,67,66,121 $3,64,52,477

Cumulative cash flows ($5,65,76,720) ($3,54,69,840) ($5,90,742) $2,58,23,602 $4,25,89,723 $7,90,42,200

Discounted cash flow (PV) ($5,65,76,720) $1,88,45,429 $2,78,05,403 $1,88,01,209 $1,06,55,173 $2,06,84,115

Cumulative discounted cash flow ($5,65,76,720) ($3,77,31,291) ($99,25,888) $88,75,320 $1,95,30,493 $4,02,14,608

Payback period 2.02 years

Profitability index 1.71 times

Net Present Value (NPV) $4,02,14,608

IRR 37.00%

Working Note

11

– Taxes -$56,97,120 -$1,10,52,982 -$77,61,134 -$40,09,047 -$31,74,350

After-tax income $1,46,49,737 $2,84,21,955 $1,99,57,202 $1,03,08,978 $81,62,614

Annual Net Cash Flow Estimates 0 1 2 3 4 5

Investment in fixed assets -$4,52,00,000 $1,04,56,000

CF due to change in net working capital -$1,13,76,720 $1,13,76,720

Net income $1,46,49,737 $2,84,21,955 $1,99,57,202 $1,03,08,978 $81,62,614

Add back depreciation $64,57,143 $64,57,143 $64,57,143 $64,57,143 $64,57,143

Net cash flows -$5,65,76,720 $2,11,06,880 $3,48,79,098 $2,64,14,344 $1,67,66,121 $3,64,52,477

Year 0 1 2 3 4 5

Net cash flows ($ millions) ($5,65,76,720) $2,11,06,880 $3,48,79,098 $2,64,14,344 $1,67,66,121 $3,64,52,477

Cumulative cash flows ($5,65,76,720) ($3,54,69,840) ($5,90,742) $2,58,23,602 $4,25,89,723 $7,90,42,200

Discounted cash flow (PV) ($5,65,76,720) $1,88,45,429 $2,78,05,403 $1,88,01,209 $1,06,55,173 $2,06,84,115

Cumulative discounted cash flow ($5,65,76,720) ($3,77,31,291) ($99,25,888) $88,75,320 $1,95,30,493 $4,02,14,608

Payback period 2.02 years

Profitability index 1.71 times

Net Present Value (NPV) $4,02,14,608

IRR 37.00%

Working Note

11

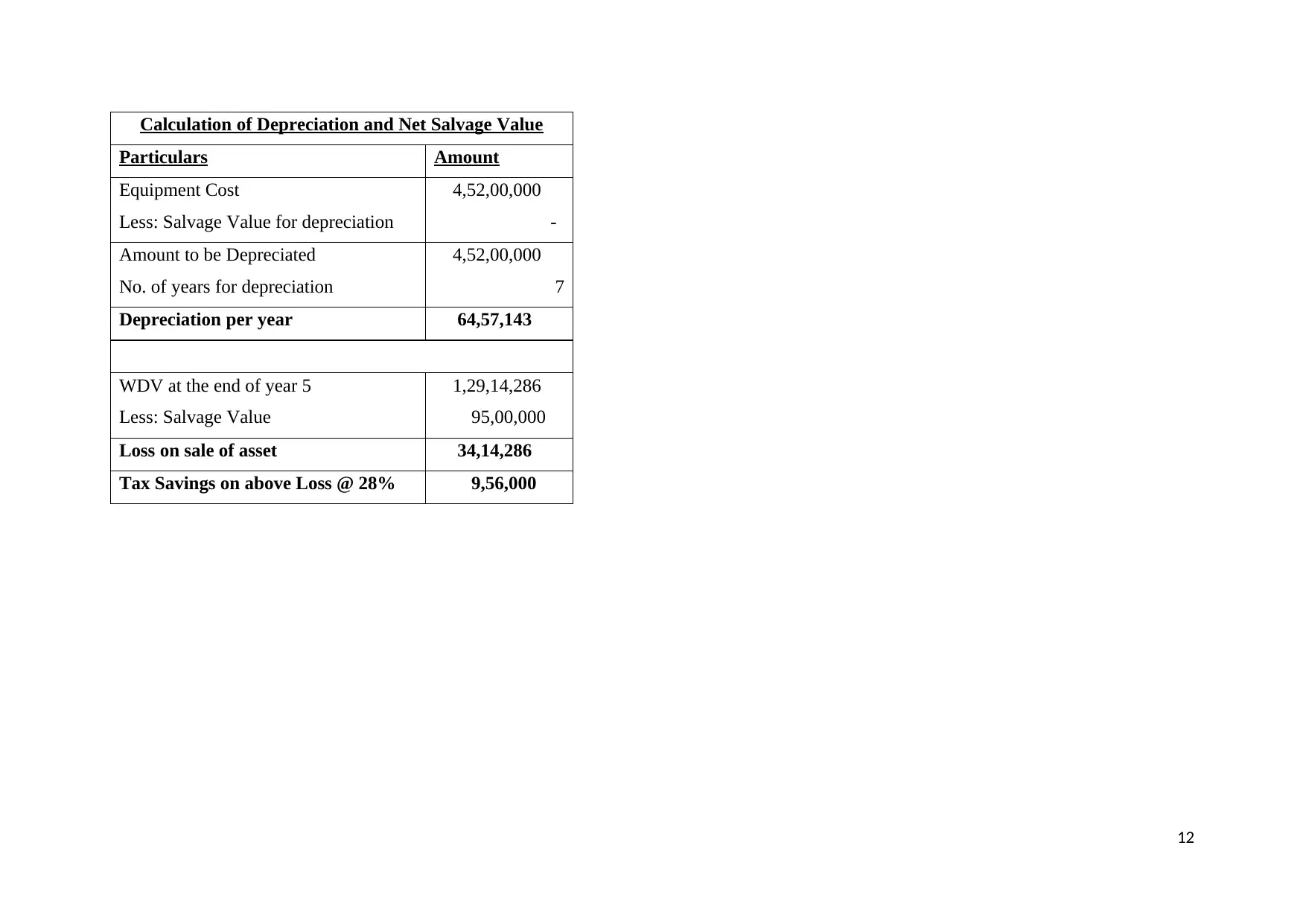

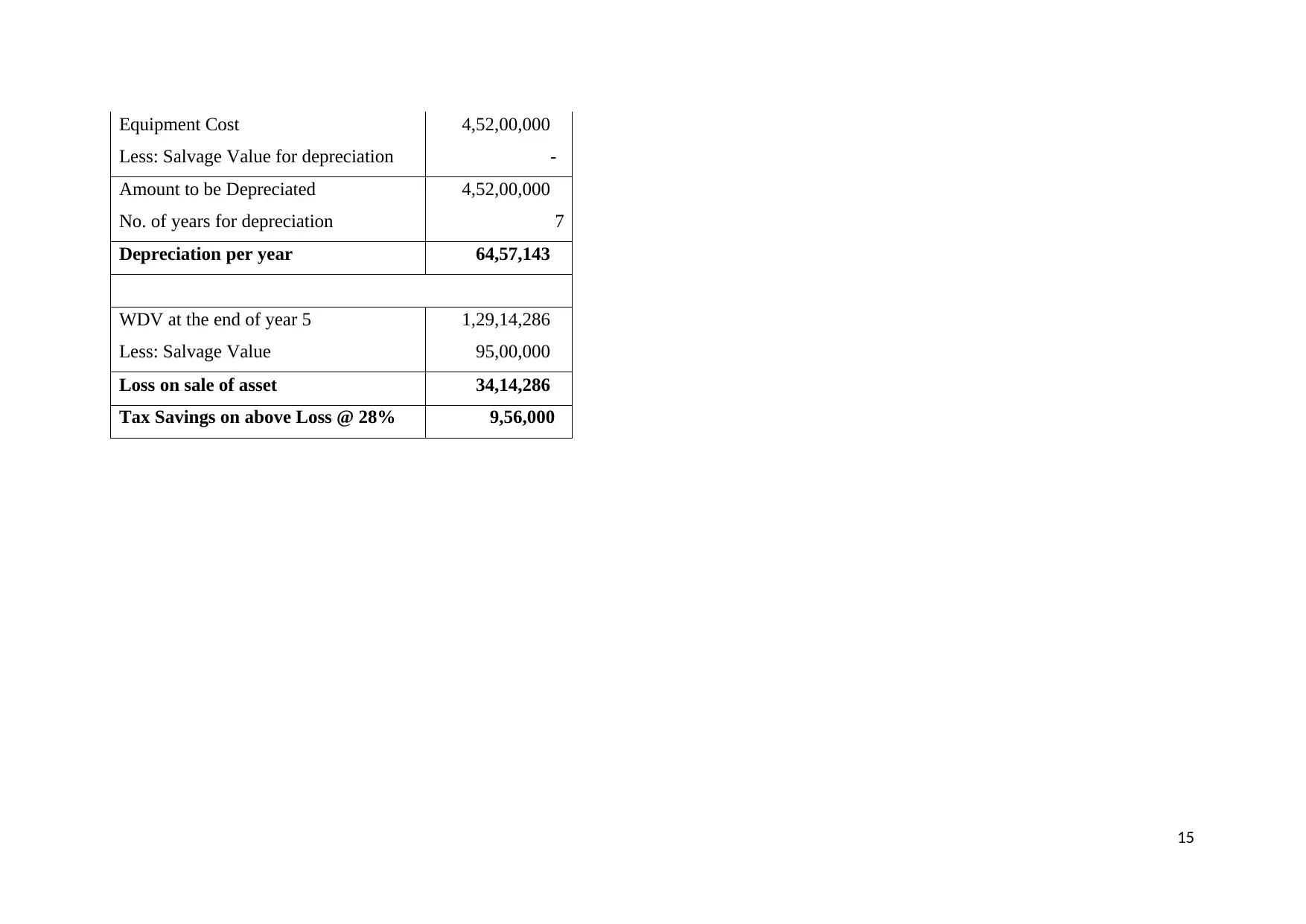

Calculation of Depreciation and Net Salvage Value

Particulars Amount

Equipment Cost 4,52,00,000

Less: Salvage Value for depreciation -

Amount to be Depreciated 4,52,00,000

No. of years for depreciation 7

Depreciation per year 64,57,143

WDV at the end of year 5 1,29,14,286

Less: Salvage Value 95,00,000

Loss on sale of asset 34,14,286

Tax Savings on above Loss @ 28% 9,56,000

12

Particulars Amount

Equipment Cost 4,52,00,000

Less: Salvage Value for depreciation -

Amount to be Depreciated 4,52,00,000

No. of years for depreciation 7

Depreciation per year 64,57,143

WDV at the end of year 5 1,29,14,286

Less: Salvage Value 95,00,000

Loss on sale of asset 34,14,286

Tax Savings on above Loss @ 28% 9,56,000

12

Sensitivity Analysis-Change in price

Income tax rate 28%

Discount rate 12%

NWC % of year 1 revenue 18%

Inflation 2%

Sales data 0 1 2 3 4 5

Sales price per unit $693.87 $707.75 $721.90 $736.34 $751.07

Unit sales 92,000 1,42,000 1,08,000 71,000 62,000

Cost data (excluding depreciation) 0 1 2 3 4 5

Cost per unit $325.00 $331.50 $338.13 $344.89 $351.79

Net income 0 1 2 3 4 5

Revenues $6,38,36,040 $10,05,00,131 $7,79,65,454 $5,22,80,168 $4,65,66,167

– Costs -$2,99,00,000 -$4,70,73,000 -

$3,65,18,040 -$2,44,87,375 -$2,18,11,008

– Fixed Cost -$65,00,000 -$65,00,000 -$65,00,000 -$65,00,000 -$65,00,000

– Depreciation expense -$64,57,143 -$64,57,143 -$64,57,143 -$64,57,143 -$64,57,143

Taxable income $2,09,78,897 $4,04,69,988 $2,84,90,271 $1,48,35,651 $1,17,98,016

– Taxes -$58,74,091 -$1,13,31,597 -$79,77,276 -$41,53,982 -$33,03,444

After-tax income $1,51,04,806 $2,91,38,391 $2,05,12,995 $1,06,81,668 $84,94,571

13

Income tax rate 28%

Discount rate 12%

NWC % of year 1 revenue 18%

Inflation 2%

Sales data 0 1 2 3 4 5

Sales price per unit $693.87 $707.75 $721.90 $736.34 $751.07

Unit sales 92,000 1,42,000 1,08,000 71,000 62,000

Cost data (excluding depreciation) 0 1 2 3 4 5

Cost per unit $325.00 $331.50 $338.13 $344.89 $351.79

Net income 0 1 2 3 4 5

Revenues $6,38,36,040 $10,05,00,131 $7,79,65,454 $5,22,80,168 $4,65,66,167

– Costs -$2,99,00,000 -$4,70,73,000 -

$3,65,18,040 -$2,44,87,375 -$2,18,11,008

– Fixed Cost -$65,00,000 -$65,00,000 -$65,00,000 -$65,00,000 -$65,00,000

– Depreciation expense -$64,57,143 -$64,57,143 -$64,57,143 -$64,57,143 -$64,57,143

Taxable income $2,09,78,897 $4,04,69,988 $2,84,90,271 $1,48,35,651 $1,17,98,016

– Taxes -$58,74,091 -$1,13,31,597 -$79,77,276 -$41,53,982 -$33,03,444

After-tax income $1,51,04,806 $2,91,38,391 $2,05,12,995 $1,06,81,668 $84,94,571

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

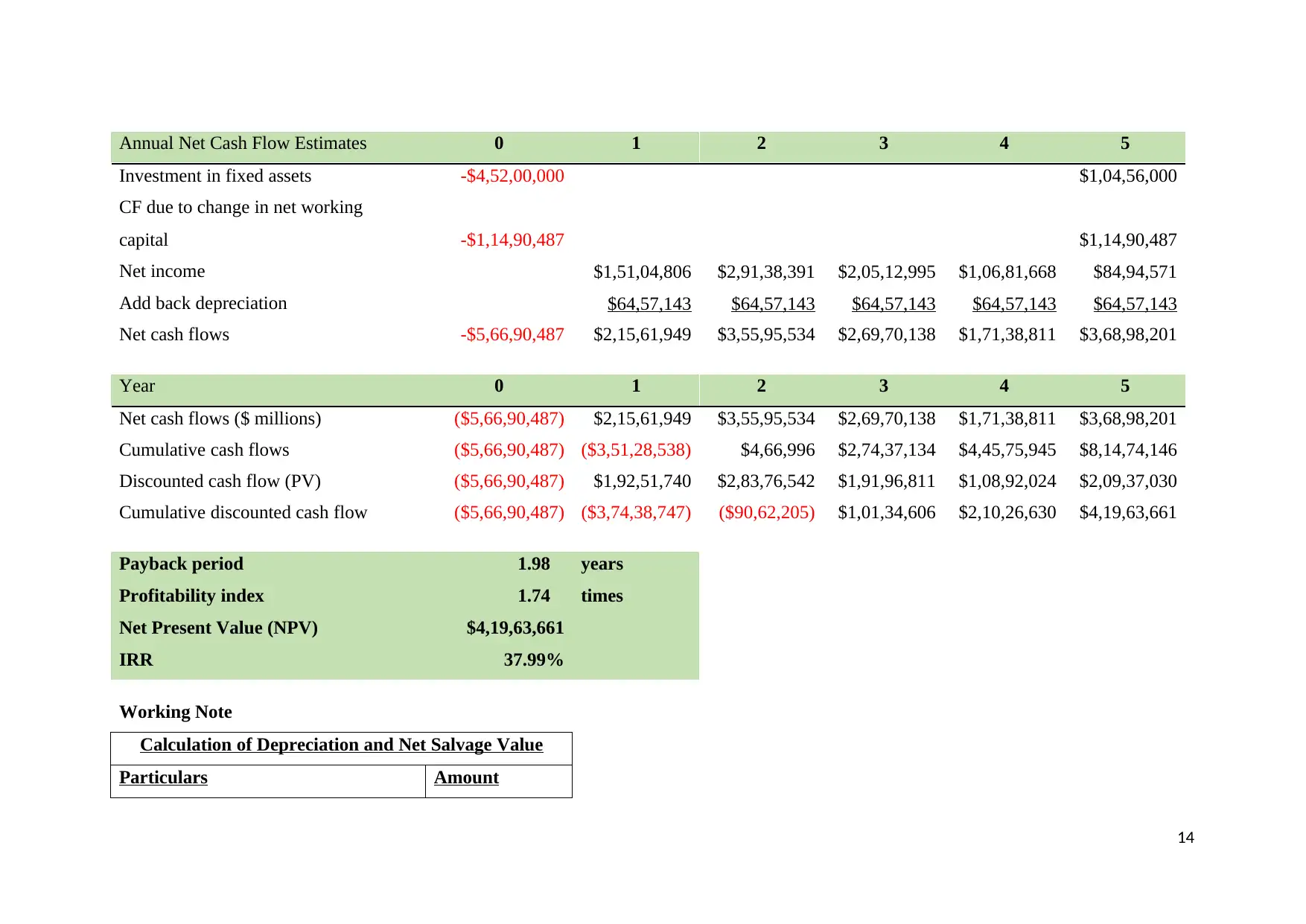

Annual Net Cash Flow Estimates 0 1 2 3 4 5

Investment in fixed assets -$4,52,00,000 $1,04,56,000

CF due to change in net working

capital -$1,14,90,487 $1,14,90,487

Net income $1,51,04,806 $2,91,38,391 $2,05,12,995 $1,06,81,668 $84,94,571

Add back depreciation $64,57,143 $64,57,143 $64,57,143 $64,57,143 $64,57,143

Net cash flows -$5,66,90,487 $2,15,61,949 $3,55,95,534 $2,69,70,138 $1,71,38,811 $3,68,98,201

Year 0 1 2 3 4 5

Net cash flows ($ millions) ($5,66,90,487) $2,15,61,949 $3,55,95,534 $2,69,70,138 $1,71,38,811 $3,68,98,201

Cumulative cash flows ($5,66,90,487) ($3,51,28,538) $4,66,996 $2,74,37,134 $4,45,75,945 $8,14,74,146

Discounted cash flow (PV) ($5,66,90,487) $1,92,51,740 $2,83,76,542 $1,91,96,811 $1,08,92,024 $2,09,37,030

Cumulative discounted cash flow ($5,66,90,487) ($3,74,38,747) ($90,62,205) $1,01,34,606 $2,10,26,630 $4,19,63,661

Payback period 1.98 years

Profitability index 1.74 times

Net Present Value (NPV) $4,19,63,661

IRR 37.99%

Working Note

Calculation of Depreciation and Net Salvage Value

Particulars Amount

14

Investment in fixed assets -$4,52,00,000 $1,04,56,000

CF due to change in net working

capital -$1,14,90,487 $1,14,90,487

Net income $1,51,04,806 $2,91,38,391 $2,05,12,995 $1,06,81,668 $84,94,571

Add back depreciation $64,57,143 $64,57,143 $64,57,143 $64,57,143 $64,57,143

Net cash flows -$5,66,90,487 $2,15,61,949 $3,55,95,534 $2,69,70,138 $1,71,38,811 $3,68,98,201

Year 0 1 2 3 4 5

Net cash flows ($ millions) ($5,66,90,487) $2,15,61,949 $3,55,95,534 $2,69,70,138 $1,71,38,811 $3,68,98,201

Cumulative cash flows ($5,66,90,487) ($3,51,28,538) $4,66,996 $2,74,37,134 $4,45,75,945 $8,14,74,146

Discounted cash flow (PV) ($5,66,90,487) $1,92,51,740 $2,83,76,542 $1,91,96,811 $1,08,92,024 $2,09,37,030

Cumulative discounted cash flow ($5,66,90,487) ($3,74,38,747) ($90,62,205) $1,01,34,606 $2,10,26,630 $4,19,63,661

Payback period 1.98 years

Profitability index 1.74 times

Net Present Value (NPV) $4,19,63,661

IRR 37.99%

Working Note

Calculation of Depreciation and Net Salvage Value

Particulars Amount

14

Equipment Cost 4,52,00,000

Less: Salvage Value for depreciation -

Amount to be Depreciated 4,52,00,000

No. of years for depreciation 7

Depreciation per year 64,57,143

WDV at the end of year 5 1,29,14,286

Less: Salvage Value 95,00,000

Loss on sale of asset 34,14,286

Tax Savings on above Loss @ 28% 9,56,000

15

Less: Salvage Value for depreciation -

Amount to be Depreciated 4,52,00,000

No. of years for depreciation 7

Depreciation per year 64,57,143

WDV at the end of year 5 1,29,14,286

Less: Salvage Value 95,00,000

Loss on sale of asset 34,14,286

Tax Savings on above Loss @ 28% 9,56,000

15

Sensitivity Analysis- change in quantity

Income tax rate 28%

Discount rate 12%

NWC % of year 1 revenue 18%

Inflation 2%

Sales data 0 1 2 3 4 5

Sales price per unit $687.00 $700.74 $714.75 $729.05 $743.63

Unit sales 92,920 1,43,420 1,09,080 71,710 62,620

Cost data (excluding depreciation) 0 1 2 3 4 5

Cost per unit $325.00 $331.50 $338.13 $344.89 $351.79

Net income 0 1 2 3 4 5

Revenues $6,38,36,040 $10,05,00,131 $7,79,65,454 $5,22,80,168 $4,65,66,167

– Costs -$3,01,99,000 -$4,75,43,730 -

$3,68,83,220 -$2,47,32,248 -$2,20,29,118

– Fixed Cost -$65,00,000 -$65,00,000 -$65,00,000 -$65,00,000 -$65,00,000

– Depreciation expense -$64,57,143 -$64,57,143 -$64,57,143 -$64,57,143 -$64,57,143

Taxable income $2,06,79,897 $3,99,99,258 $2,81,25,090 $1,45,90,777 $1,15,79,906

16

Income tax rate 28%

Discount rate 12%

NWC % of year 1 revenue 18%

Inflation 2%

Sales data 0 1 2 3 4 5

Sales price per unit $687.00 $700.74 $714.75 $729.05 $743.63

Unit sales 92,920 1,43,420 1,09,080 71,710 62,620

Cost data (excluding depreciation) 0 1 2 3 4 5

Cost per unit $325.00 $331.50 $338.13 $344.89 $351.79

Net income 0 1 2 3 4 5

Revenues $6,38,36,040 $10,05,00,131 $7,79,65,454 $5,22,80,168 $4,65,66,167

– Costs -$3,01,99,000 -$4,75,43,730 -

$3,68,83,220 -$2,47,32,248 -$2,20,29,118

– Fixed Cost -$65,00,000 -$65,00,000 -$65,00,000 -$65,00,000 -$65,00,000

– Depreciation expense -$64,57,143 -$64,57,143 -$64,57,143 -$64,57,143 -$64,57,143

Taxable income $2,06,79,897 $3,99,99,258 $2,81,25,090 $1,45,90,777 $1,15,79,906

16

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

– Taxes -$57,90,371 -$1,11,99,792 -$78,75,025 -$40,85,418 -$32,42,374

After-tax income $1,48,89,526 $2,87,99,466 $2,02,50,065 $1,05,05,359 $83,37,532

Annual Net Cash Flow Estimates 0 1 2 3 4 5

Investment in fixed assets -$4,52,00,000 $1,04,56,000

CF due to change in net working

capital -$1,14,90,487 $1,14,90,487

Net income $1,48,89,526 $2,87,99,466 $2,02,50,065 $1,05,05,359 $83,37,532

Add back depreciation $64,57,143 $64,57,143 $64,57,143 $64,57,143 $64,57,143

Net cash flows -$5,66,90,487 $2,13,46,669 $3,52,56,609 $2,67,07,208 $1,69,62,502 $3,67,41,162

Year 0 1 2 3 4 5

Net cash flows ($ millions) ($5,66,90,487) $2,13,46,669 $3,52,56,609 $2,67,07,208 $1,69,62,502 $3,67,41,162

Cumulative cash flows ($5,66,90,487) ($3,53,43,818) ($87,210) $2,66,19,998 $4,35,82,500 $8,03,23,662

Discounted cash flow (PV) ($5,66,90,487) $1,90,59,526 $2,81,06,353 $1,90,09,663 $1,07,79,977 $2,08,47,922

Cumulative discounted cash flow ($5,66,90,487) ($3,76,30,961) ($95,24,609) $94,85,054 $2,02,65,031 $4,11,12,953

Payback period 2.00 years

Profitability index 1.73 times

Net Present Value (NPV) $4,11,12,953

IRR 37.48%

Working Note

17

After-tax income $1,48,89,526 $2,87,99,466 $2,02,50,065 $1,05,05,359 $83,37,532

Annual Net Cash Flow Estimates 0 1 2 3 4 5

Investment in fixed assets -$4,52,00,000 $1,04,56,000

CF due to change in net working

capital -$1,14,90,487 $1,14,90,487

Net income $1,48,89,526 $2,87,99,466 $2,02,50,065 $1,05,05,359 $83,37,532

Add back depreciation $64,57,143 $64,57,143 $64,57,143 $64,57,143 $64,57,143

Net cash flows -$5,66,90,487 $2,13,46,669 $3,52,56,609 $2,67,07,208 $1,69,62,502 $3,67,41,162

Year 0 1 2 3 4 5

Net cash flows ($ millions) ($5,66,90,487) $2,13,46,669 $3,52,56,609 $2,67,07,208 $1,69,62,502 $3,67,41,162

Cumulative cash flows ($5,66,90,487) ($3,53,43,818) ($87,210) $2,66,19,998 $4,35,82,500 $8,03,23,662

Discounted cash flow (PV) ($5,66,90,487) $1,90,59,526 $2,81,06,353 $1,90,09,663 $1,07,79,977 $2,08,47,922

Cumulative discounted cash flow ($5,66,90,487) ($3,76,30,961) ($95,24,609) $94,85,054 $2,02,65,031 $4,11,12,953

Payback period 2.00 years

Profitability index 1.73 times

Net Present Value (NPV) $4,11,12,953

IRR 37.48%

Working Note

17

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.