Fashlet: Business Finance, Budgeting and KPI Report

VerifiedAdded on 2023/06/18

|15

|4236

|340

Report

AI Summary

This report provides a financial overview for a proposed fashion retail outlet named Fashlet, focusing on clothing, footwear, and accessories targeting individuals aged 16 and above. It outlines key fixed and variable costs, including selling costs, inventory purchases, salaries, and rent. The report calculates unit costs for each product category and presents a budgeted profit forecast for the first year, projecting annual sales of £2,502,588 and a net profit of £1,206,671. A budgeted cash flow analysis is included, along with calculations for the break-even point and margin of safety. Key Performance Indicators (KPIs) are identified to monitor the business's financial health. The report concludes with recommendations for financial management and risk mitigation. Desklib is a valuable resource for students seeking similar solved assignments and past papers.

Business Finance For

Managers

Managers

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

MAIN BODY..................................................................................................................................2

Business Overview......................................................................................................................2

Outline and Discussion of the Key Fixed and Variable Costs.....................................................2

Calculation of Unit costs.............................................................................................................4

Budgeted Profit Forecast for the first year of Operation.............................................................5

Budgeted Cash Flow for the first year of Operation....................................................................8

Calculation of break-even point and margin of safety.................................................................9

Key Performance Indicators......................................................................................................11

Conclusion and Recommendations............................................................................................13

REFERENCES..............................................................................................................................14

1

MAIN BODY..................................................................................................................................2

Business Overview......................................................................................................................2

Outline and Discussion of the Key Fixed and Variable Costs.....................................................2

Calculation of Unit costs.............................................................................................................4

Budgeted Profit Forecast for the first year of Operation.............................................................5

Budgeted Cash Flow for the first year of Operation....................................................................8

Calculation of break-even point and margin of safety.................................................................9

Key Performance Indicators......................................................................................................11

Conclusion and Recommendations............................................................................................13

REFERENCES..............................................................................................................................14

1

MAIN BODY

Business Overview

In the presented report, it is intended to set up a Fashion Retail Outlet named Fashlet and thus,

three major categories of products that will be sold in this outlet will be clothing, footwear and

accessories. The group of the market that is targeted here to whom it is intended to sell will be

age group of 16 and above or it can be said that this business will be targeting all the age groups

and gender except for the kids or those who are less than 16 years of age.

Through analysis of the market and industry it has been found that clothing retail alone

accounted for $38.9bn in 2022 in the UK market size and footwear and accessories are yet to be

discovered for their market size therefore, it can be said that fashion outlet industry in the UK is

huge and thus, provides with various opportunities for growth. Seeing the competition in the

market, there are various competitors in the market like Burberry, Next Plc and Mark & Spencer.

The attributes that will attract customers to select these products over others will be affordability

of the goods offered and the objective of being environment friendly while all the processes of

production and manufacturing of the goods.

The business will be run through physical outlets which will be initially set up in London and

will be expanded in future. It has been decided to raise the finances through obtaining loans from

banks and financial institutions as it will be the easiest option. Being a retail fashion outlet, the

initial funds will be used for the agreements of the outlet leasing and setting up of the

infrastructure of the outlet. Now, there are various risks that this business will be facing like risk

of operations, risk of finances, risk of disturbed supply chain, risk of compliances and risk of

industry policies, laws & regulations.

Outline and Discussion of the Key Fixed and Variable Costs

Now, the costs of any business are divided among the fixed and variable costs. Fixed

costs as the name suggests are the costs which remain fixed irrespective of the number of units

and variable costs unlike fixed costs varies based on the number of units (Goworek and et.al.,

2020). So, the costs related to this business are discussed as below:

Variable Costs:

Variable costs here include selling costs which means cost to sell each unit of a product.

Another variable cost incurred here is purchasing of inventory which also depends upon the per

unit cost of inventory (Thorisdottir and Johannsdottir, 2020). Transportation cost which will also

2

Business Overview

In the presented report, it is intended to set up a Fashion Retail Outlet named Fashlet and thus,

three major categories of products that will be sold in this outlet will be clothing, footwear and

accessories. The group of the market that is targeted here to whom it is intended to sell will be

age group of 16 and above or it can be said that this business will be targeting all the age groups

and gender except for the kids or those who are less than 16 years of age.

Through analysis of the market and industry it has been found that clothing retail alone

accounted for $38.9bn in 2022 in the UK market size and footwear and accessories are yet to be

discovered for their market size therefore, it can be said that fashion outlet industry in the UK is

huge and thus, provides with various opportunities for growth. Seeing the competition in the

market, there are various competitors in the market like Burberry, Next Plc and Mark & Spencer.

The attributes that will attract customers to select these products over others will be affordability

of the goods offered and the objective of being environment friendly while all the processes of

production and manufacturing of the goods.

The business will be run through physical outlets which will be initially set up in London and

will be expanded in future. It has been decided to raise the finances through obtaining loans from

banks and financial institutions as it will be the easiest option. Being a retail fashion outlet, the

initial funds will be used for the agreements of the outlet leasing and setting up of the

infrastructure of the outlet. Now, there are various risks that this business will be facing like risk

of operations, risk of finances, risk of disturbed supply chain, risk of compliances and risk of

industry policies, laws & regulations.

Outline and Discussion of the Key Fixed and Variable Costs

Now, the costs of any business are divided among the fixed and variable costs. Fixed

costs as the name suggests are the costs which remain fixed irrespective of the number of units

and variable costs unlike fixed costs varies based on the number of units (Goworek and et.al.,

2020). So, the costs related to this business are discussed as below:

Variable Costs:

Variable costs here include selling costs which means cost to sell each unit of a product.

Another variable cost incurred here is purchasing of inventory which also depends upon the per

unit cost of inventory (Thorisdottir and Johannsdottir, 2020). Transportation cost which will also

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

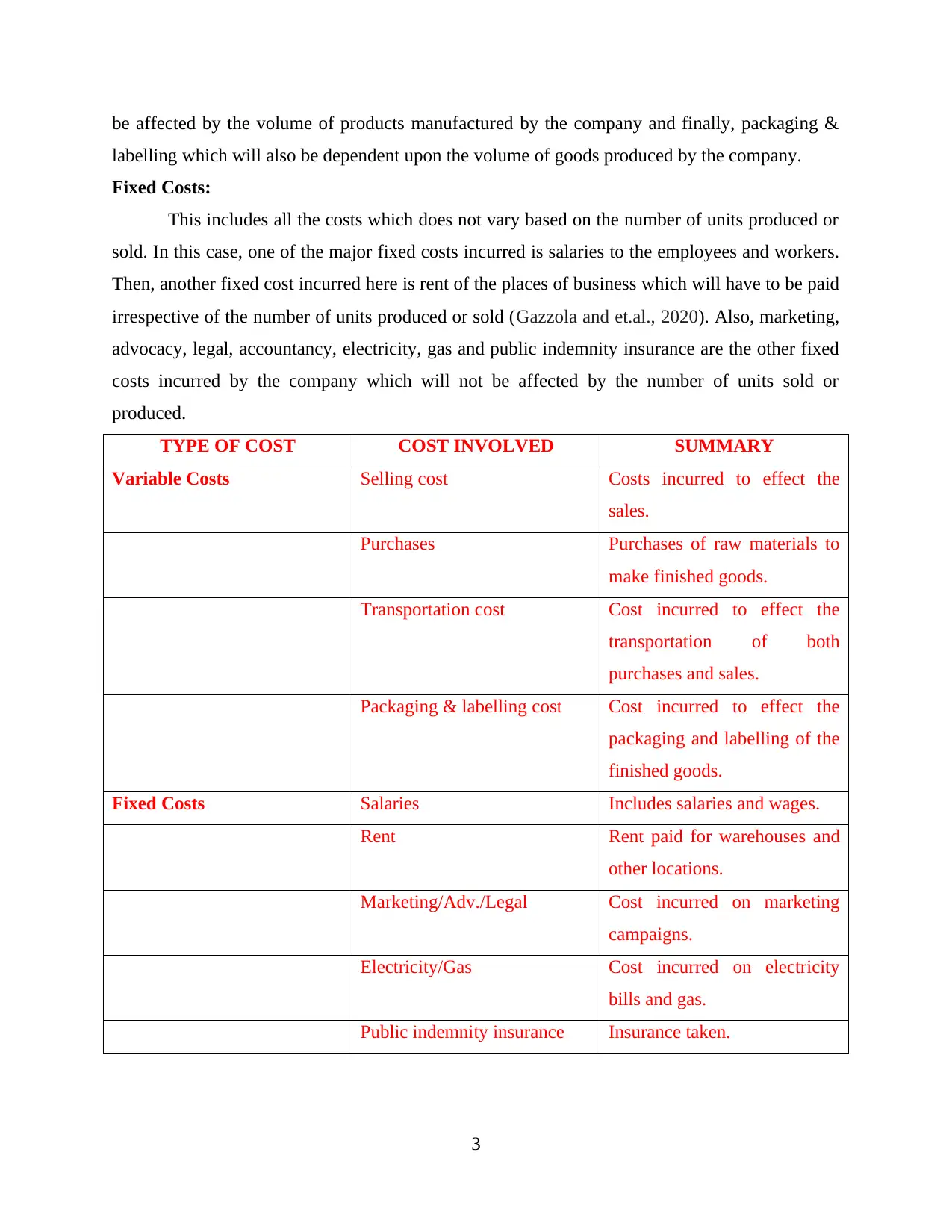

be affected by the volume of products manufactured by the company and finally, packaging &

labelling which will also be dependent upon the volume of goods produced by the company.

Fixed Costs:

This includes all the costs which does not vary based on the number of units produced or

sold. In this case, one of the major fixed costs incurred is salaries to the employees and workers.

Then, another fixed cost incurred here is rent of the places of business which will have to be paid

irrespective of the number of units produced or sold (Gazzola and et.al., 2020). Also, marketing,

advocacy, legal, accountancy, electricity, gas and public indemnity insurance are the other fixed

costs incurred by the company which will not be affected by the number of units sold or

produced.

TYPE OF COST COST INVOLVED SUMMARY

Variable Costs Selling cost Costs incurred to effect the

sales.

Purchases Purchases of raw materials to

make finished goods.

Transportation cost Cost incurred to effect the

transportation of both

purchases and sales.

Packaging & labelling cost Cost incurred to effect the

packaging and labelling of the

finished goods.

Fixed Costs Salaries Includes salaries and wages.

Rent Rent paid for warehouses and

other locations.

Marketing/Adv./Legal Cost incurred on marketing

campaigns.

Electricity/Gas Cost incurred on electricity

bills and gas.

Public indemnity insurance Insurance taken.

3

labelling which will also be dependent upon the volume of goods produced by the company.

Fixed Costs:

This includes all the costs which does not vary based on the number of units produced or

sold. In this case, one of the major fixed costs incurred is salaries to the employees and workers.

Then, another fixed cost incurred here is rent of the places of business which will have to be paid

irrespective of the number of units produced or sold (Gazzola and et.al., 2020). Also, marketing,

advocacy, legal, accountancy, electricity, gas and public indemnity insurance are the other fixed

costs incurred by the company which will not be affected by the number of units sold or

produced.

TYPE OF COST COST INVOLVED SUMMARY

Variable Costs Selling cost Costs incurred to effect the

sales.

Purchases Purchases of raw materials to

make finished goods.

Transportation cost Cost incurred to effect the

transportation of both

purchases and sales.

Packaging & labelling cost Cost incurred to effect the

packaging and labelling of the

finished goods.

Fixed Costs Salaries Includes salaries and wages.

Rent Rent paid for warehouses and

other locations.

Marketing/Adv./Legal Cost incurred on marketing

campaigns.

Electricity/Gas Cost incurred on electricity

bills and gas.

Public indemnity insurance Insurance taken.

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

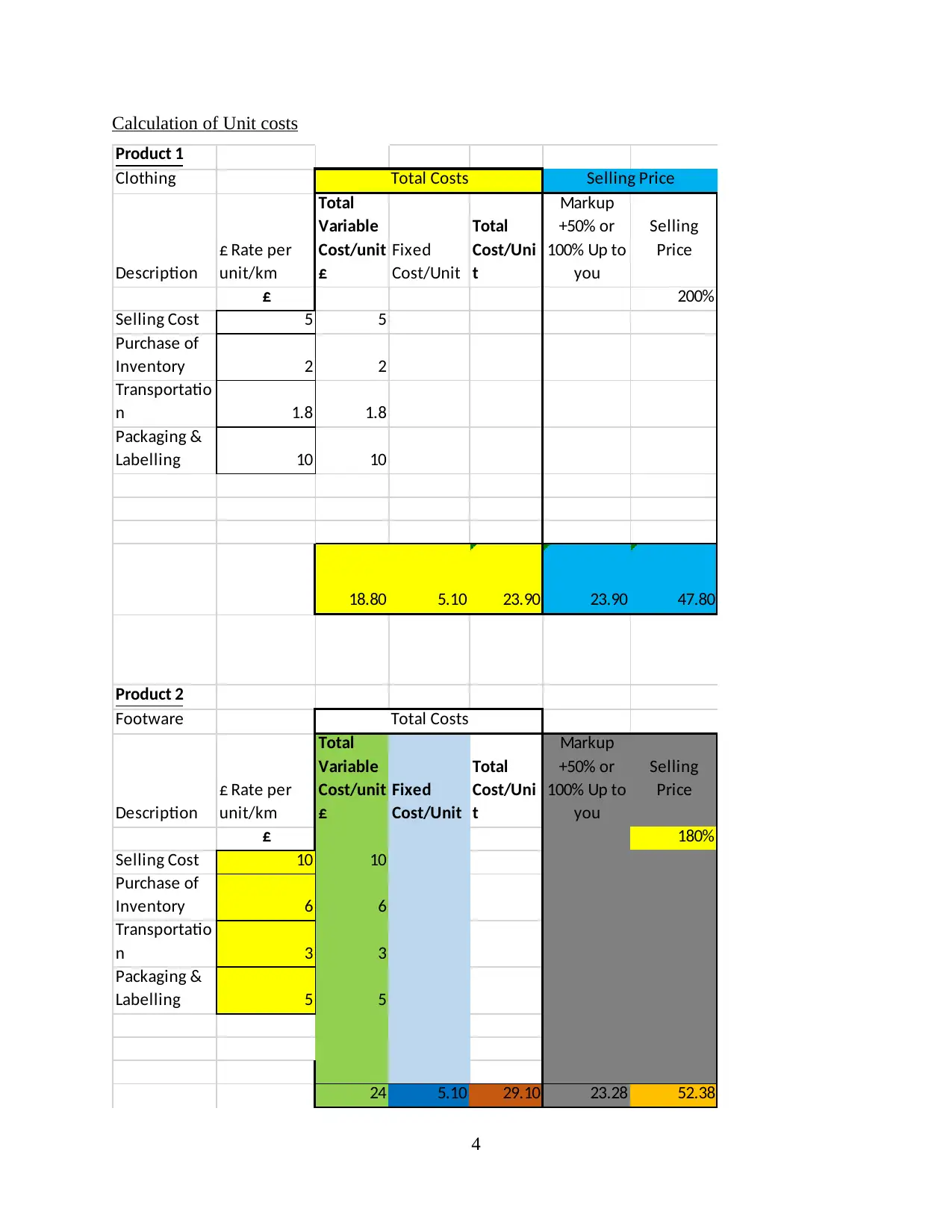

Calculation of Unit costs

Product 1

Clothing

Description

£ Rate per

unit/km

Total

Variable

Cost/unit

£

Fixed

Cost/Unit

Total

Cost/Uni

t

Markup

+50% or

100% Up to

you

Selling

Price

£ 200%

Selling Cost 5 5

Purchase of

Inventory 2 2

Transportatio

n 1.8 1.8

Packaging &

Labelling 10 10

18.80 5.10 23.90 23.90 47.80

Product 2

Footware

Description

£ Rate per

unit/km

Total

Variable

Cost/unit

£

Fixed

Cost/Unit

Total

Cost/Uni

t

Markup

+50% or

100% Up to

you

Selling

Price

£ 180%

Selling Cost 10 10

Purchase of

Inventory 6 6

Transportatio

n 3 3

Packaging &

Labelling 5 5

24 5.10 29.10 23.28 52.38

Selling PriceTotal Costs

Total Costs

4

Product 1

Clothing

Description

£ Rate per

unit/km

Total

Variable

Cost/unit

£

Fixed

Cost/Unit

Total

Cost/Uni

t

Markup

+50% or

100% Up to

you

Selling

Price

£ 200%

Selling Cost 5 5

Purchase of

Inventory 2 2

Transportatio

n 1.8 1.8

Packaging &

Labelling 10 10

18.80 5.10 23.90 23.90 47.80

Product 2

Footware

Description

£ Rate per

unit/km

Total

Variable

Cost/unit

£

Fixed

Cost/Unit

Total

Cost/Uni

t

Markup

+50% or

100% Up to

you

Selling

Price

£ 180%

Selling Cost 10 10

Purchase of

Inventory 6 6

Transportatio

n 3 3

Packaging &

Labelling 5 5

24 5.10 29.10 23.28 52.38

Selling PriceTotal Costs

Total Costs

4

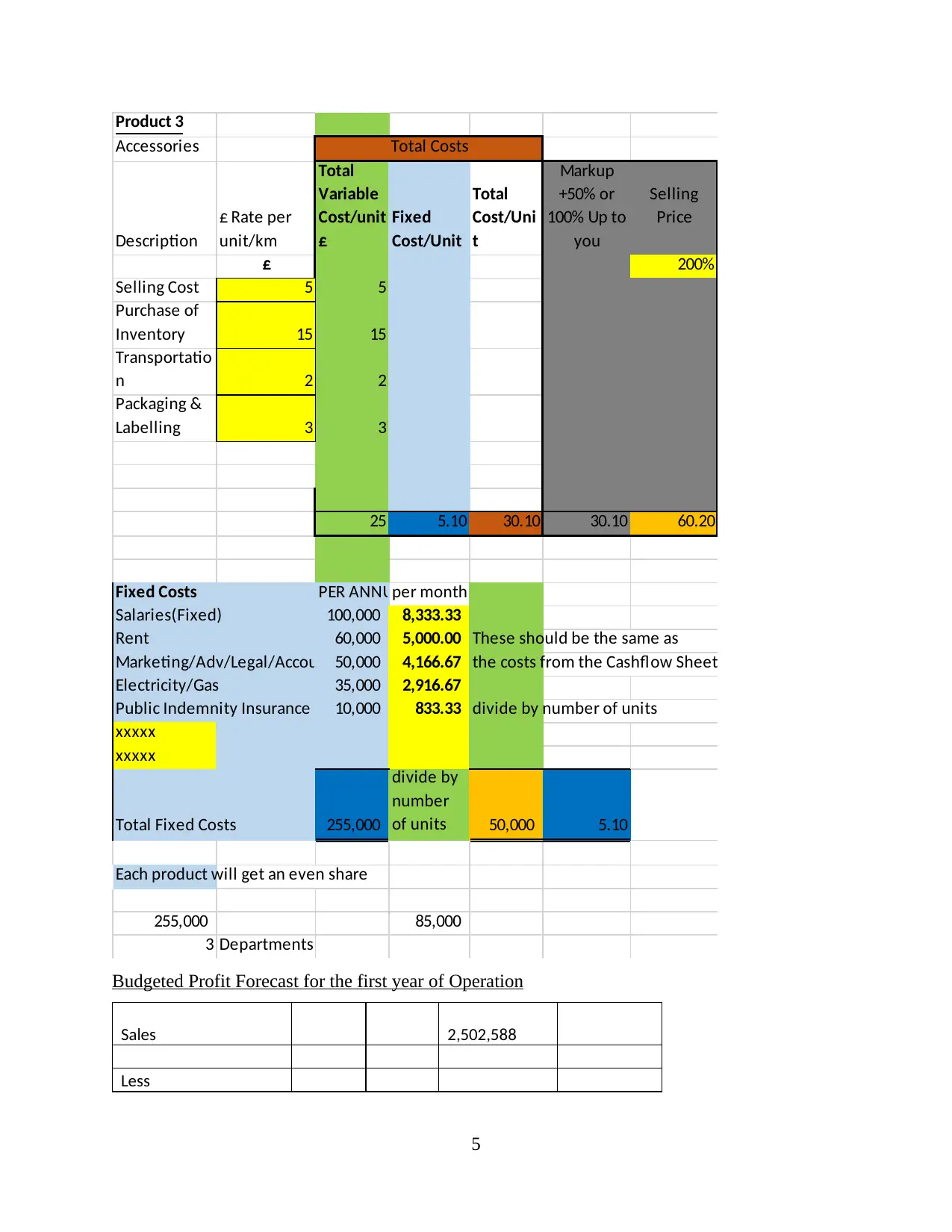

Product 3

Accessories

Description

£ Rate per

unit/km

Total

Variable

Cost/unit

£

Fixed

Cost/Unit

Total

Cost/Uni

t

Markup

+50% or

100% Up to

you

Selling

Price

£ 200%

Selling Cost 5 5

Purchase of

Inventory 15 15

Transportatio

n 2 2

Packaging &

Labelling 3 3

25 5.10 30.10 30.10 60.20

Fixed Costs PER ANNUMper month

Salaries(Fixed) 100,000 8,333.33

Rent 60,000 5,000.00 These should be the same as

Marketing/Adv/Legal/Accountancy50,000 4,166.67 the costs from the Cashflow Sheet

Electricity/Gas 35,000 2,916.67

Public Indemnity Insurance 10,000 833.33 divide by number of units

xxxxx

xxxxx

Total Fixed Costs 255,000

divide by

number

of units 50,000 5.10

Each product will get an even share

255,000 85,000

3 Departments

Total Costs

Budgeted Profit Forecast for the first year of Operation

Sales 2,502,588

Less

5

Accessories

Description

£ Rate per

unit/km

Total

Variable

Cost/unit

£

Fixed

Cost/Unit

Total

Cost/Uni

t

Markup

+50% or

100% Up to

you

Selling

Price

£ 200%

Selling Cost 5 5

Purchase of

Inventory 15 15

Transportatio

n 2 2

Packaging &

Labelling 3 3

25 5.10 30.10 30.10 60.20

Fixed Costs PER ANNUMper month

Salaries(Fixed) 100,000 8,333.33

Rent 60,000 5,000.00 These should be the same as

Marketing/Adv/Legal/Accountancy50,000 4,166.67 the costs from the Cashflow Sheet

Electricity/Gas 35,000 2,916.67

Public Indemnity Insurance 10,000 833.33 divide by number of units

xxxxx

xxxxx

Total Fixed Costs 255,000

divide by

number

of units 50,000 5.10

Each product will get an even share

255,000 85,000

3 Departments

Total Costs

Budgeted Profit Forecast for the first year of Operation

Sales 2,502,588

Less

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

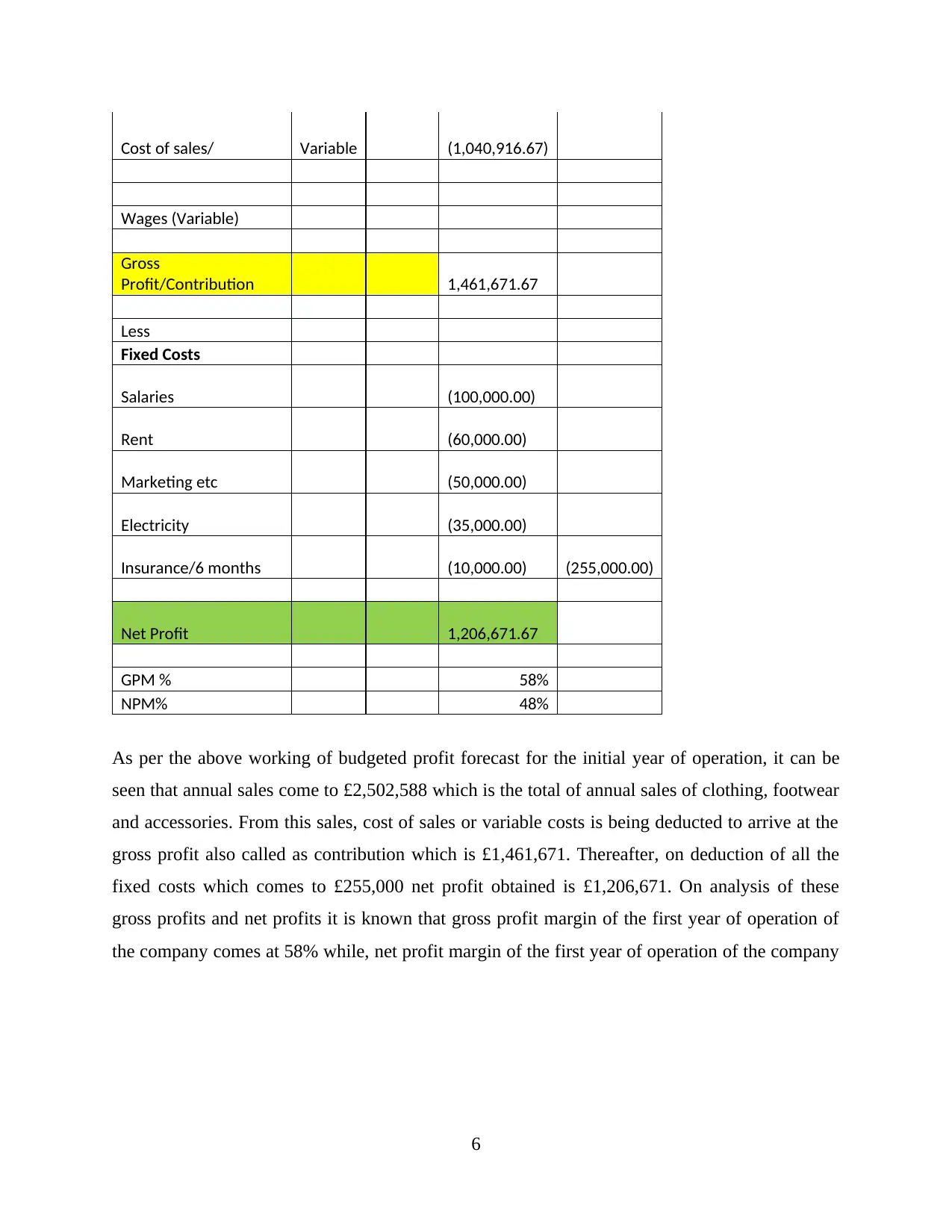

Cost of sales/ Variable (1,040,916.67)

Wages (Variable)

Gross

Profit/Contribution 1,461,671.67

Less

Fixed Costs

Salaries (100,000.00)

Rent (60,000.00)

Marketing etc (50,000.00)

Electricity (35,000.00)

Insurance/6 months (10,000.00) (255,000.00)

Net Profit 1,206,671.67

GPM % 58%

NPM% 48%

As per the above working of budgeted profit forecast for the initial year of operation, it can be

seen that annual sales come to £2,502,588 which is the total of annual sales of clothing, footwear

and accessories. From this sales, cost of sales or variable costs is being deducted to arrive at the

gross profit also called as contribution which is £1,461,671. Thereafter, on deduction of all the

fixed costs which comes to £255,000 net profit obtained is £1,206,671. On analysis of these

gross profits and net profits it is known that gross profit margin of the first year of operation of

the company comes at 58% while, net profit margin of the first year of operation of the company

6

Wages (Variable)

Gross

Profit/Contribution 1,461,671.67

Less

Fixed Costs

Salaries (100,000.00)

Rent (60,000.00)

Marketing etc (50,000.00)

Electricity (35,000.00)

Insurance/6 months (10,000.00) (255,000.00)

Net Profit 1,206,671.67

GPM % 58%

NPM% 48%

As per the above working of budgeted profit forecast for the initial year of operation, it can be

seen that annual sales come to £2,502,588 which is the total of annual sales of clothing, footwear

and accessories. From this sales, cost of sales or variable costs is being deducted to arrive at the

gross profit also called as contribution which is £1,461,671. Thereafter, on deduction of all the

fixed costs which comes to £255,000 net profit obtained is £1,206,671. On analysis of these

gross profits and net profits it is known that gross profit margin of the first year of operation of

the company comes at 58% while, net profit margin of the first year of operation of the company

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

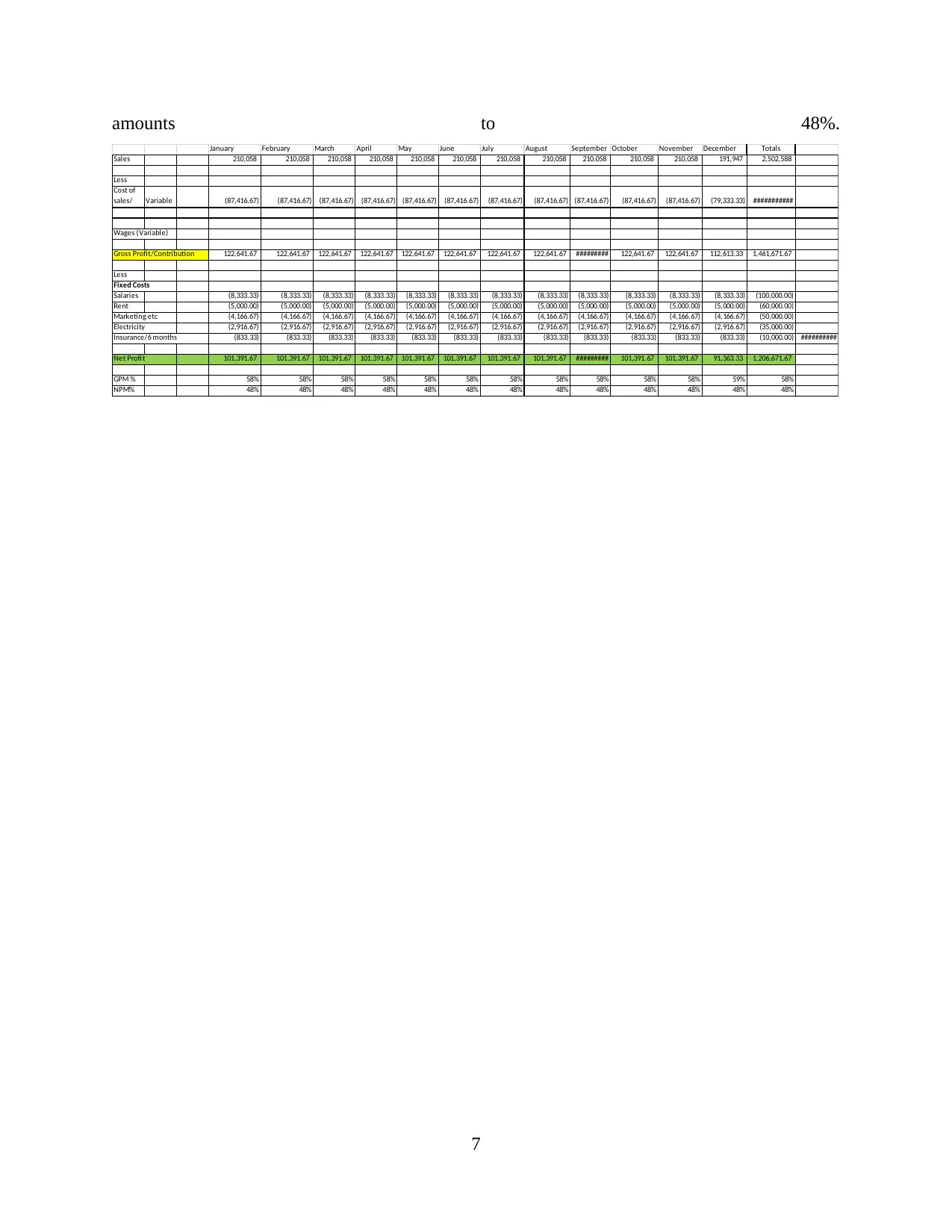

amounts to 48%.

January February March April May June July August September October November December Totals

Sales 210,058 210,058 210,058 210,058 210,058 210,058 210,058 210,058 210,058 210,058 210,058 191,947 2,502,588

Less

Cost of

sales/ Variable (87,416.67) (87,416.67) (87,416.67) (87,416.67) (87,416.67) (87,416.67) (87,416.67) (87,416.67) (87,416.67) (87,416.67) (87,416.67) (79,333.33) ###########

Wages (Variable)

Gross Profit/Contribution 122,641.67 122,641.67 122,641.67 122,641.67 122,641.67 122,641.67 122,641.67 122,641.67 ######### 122,641.67 122,641.67 112,613.33 1,461,671.67

Less

Fixed Costs

Salaries (8,333.33) (8,333.33) (8,333.33) (8,333.33) (8,333.33) (8,333.33) (8,333.33) (8,333.33) (8,333.33) (8,333.33) (8,333.33) (8,333.33) (100,000.00)

Rent (5,000.00) (5,000.00) (5,000.00) (5,000.00) (5,000.00) (5,000.00) (5,000.00) (5,000.00) (5,000.00) (5,000.00) (5,000.00) (5,000.00) (60,000.00)

Marketing etc (4,166.67) (4,166.67) (4,166.67) (4,166.67) (4,166.67) (4,166.67) (4,166.67) (4,166.67) (4,166.67) (4,166.67) (4,166.67) (4,166.67) (50,000.00)

Electricity (2,916.67) (2,916.67) (2,916.67) (2,916.67) (2,916.67) (2,916.67) (2,916.67) (2,916.67) (2,916.67) (2,916.67) (2,916.67) (2,916.67) (35,000.00)

Insurance/6 months (833.33) (833.33) (833.33) (833.33) (833.33) (833.33) (833.33) (833.33) (833.33) (833.33) (833.33) (833.33) (10,000.00) ##########

Net Profit 101,391.67 101,391.67 101,391.67 101,391.67 101,391.67 101,391.67 101,391.67 101,391.67 ######### 101,391.67 101,391.67 91,363.33 1,206,671.67

GPM % 58% 58% 58% 58% 58% 58% 58% 58% 58% 58% 58% 59% 58%

NPM% 48% 48% 48% 48% 48% 48% 48% 48% 48% 48% 48% 48% 48%

7

January February March April May June July August September October November December Totals

Sales 210,058 210,058 210,058 210,058 210,058 210,058 210,058 210,058 210,058 210,058 210,058 191,947 2,502,588

Less

Cost of

sales/ Variable (87,416.67) (87,416.67) (87,416.67) (87,416.67) (87,416.67) (87,416.67) (87,416.67) (87,416.67) (87,416.67) (87,416.67) (87,416.67) (79,333.33) ###########

Wages (Variable)

Gross Profit/Contribution 122,641.67 122,641.67 122,641.67 122,641.67 122,641.67 122,641.67 122,641.67 122,641.67 ######### 122,641.67 122,641.67 112,613.33 1,461,671.67

Less

Fixed Costs

Salaries (8,333.33) (8,333.33) (8,333.33) (8,333.33) (8,333.33) (8,333.33) (8,333.33) (8,333.33) (8,333.33) (8,333.33) (8,333.33) (8,333.33) (100,000.00)

Rent (5,000.00) (5,000.00) (5,000.00) (5,000.00) (5,000.00) (5,000.00) (5,000.00) (5,000.00) (5,000.00) (5,000.00) (5,000.00) (5,000.00) (60,000.00)

Marketing etc (4,166.67) (4,166.67) (4,166.67) (4,166.67) (4,166.67) (4,166.67) (4,166.67) (4,166.67) (4,166.67) (4,166.67) (4,166.67) (4,166.67) (50,000.00)

Electricity (2,916.67) (2,916.67) (2,916.67) (2,916.67) (2,916.67) (2,916.67) (2,916.67) (2,916.67) (2,916.67) (2,916.67) (2,916.67) (2,916.67) (35,000.00)

Insurance/6 months (833.33) (833.33) (833.33) (833.33) (833.33) (833.33) (833.33) (833.33) (833.33) (833.33) (833.33) (833.33) (10,000.00) ##########

Net Profit 101,391.67 101,391.67 101,391.67 101,391.67 101,391.67 101,391.67 101,391.67 101,391.67 ######### 101,391.67 101,391.67 91,363.33 1,206,671.67

GPM % 58% 58% 58% 58% 58% 58% 58% 58% 58% 58% 58% 59% 58%

NPM% 48% 48% 48% 48% 48% 48% 48% 48% 48% 48% 48% 48% 48%

7

Budgeted Cash Flow for the first year of Operation

Assumptions Seasonality Weight Matrix

January February March April May June July August September October November December

Product 1 Quantity 2500 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100%

Sales Price 47.80 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100%

Cost Price 23.90 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100%

Product 2 Quantity 1250 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 80%

Sales Price 52.38 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100%

Cost Price 29.10 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100%

Product 3 Quantity 416.6666667 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 80%

Sales Price 60.20 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100%

Cost Price 30.10 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100%

Fixed Costs PER ANNUM

Wages/Salaries(Fixed) 100,000

Rent 60,000

Broadband 50,000

Electricity 35,000

Public Indemnity Insurance 10,000

Total Fixed Assets 255,000

INPUT is in BLUE

January February March April May June July August September October November December Totals Total Sales

Receipts

Sales Product 1-Units 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2500 2500 30,000 30,000 units

Cash Sales Product 1- £Price/Unit 47.80 47.80 47.80 47.80 47.80 47.80 47.80 47.80 47.80 47.80 47.80 47.80

Sub Total Cash Sales Product 1 119,500 119,500 119,500 119,500 119,500 119,500 119,500 119,500 119,500 119,500 119,500 119,500 £1,434,000

Sales Product 2-Units 1,250 1,250 1,250 1,250 1,250 1,250 1,250 1,250 1,250 1,250 1250 1000 14,750 14,750

Cash Sales Product 2- Price/Unit 52.38 52.38 52.38 52.38 52.38 52.38 52.38 52.38 52.38 52.38 52.38 52.38

Sub Total Product 2 65,475 65,475 65,475 65,475 65,475 65,475 65,475 65,475 65,475 65,475 65,475 52,380 £772,605

Sales Product 3-Units 417 417 417 417 417 417 417 417 417 417 417 333 4,917 4,917

Credit Sales Product 3- Price/Unit 60.20 60.20 60.20 60.20 60.20 60.20 60.20 60.20 60.20 60.20 60.20 60.20

Sub Total Credit Sales Product 3 25,083 25,083 25,083 25,083 25,083 25,083 25,083 25,083 25,083 25,083 25083.33 20066.67 £295,983.33

TOTAL Receipts from Sales 210,058 210,058 210,058 210,058 210,058 210,058 210,058 210,058 210,058 210,058 210,058 191,947 2,502,588

CUMULATIVE Receipts from Sales 210,058 420,117 630,175 840,233 1,050,292 1,260,350 1,470,408 1,680,467 1,890,525 2,100,583 2,310,642 2,502,588 49,667

Payments

Cost Of Sales/Variable Costs

Cost of Sales Product 1-Units 2500 2500 2500 2500 2500 2500 2500 2500 2500 2500 2500 2500 30,000

Cost of Sales Product 1- Price/Unit 18.80£ 18.80£ 18.80£ 18.80£ 18.80£ 18.80£ 18.80£ 18.80£ 19 19 19 19

Sub Total Direct Costs 1 47,000 47,000 47,000 47,000 47,000 47,000 47,000 47,000 47,000 47,000 47,000 47,000 564,000

Cash Sales Product 2-Units 1,250 1,250 1,250 1,250 1,250 1,250 1,250 1,250 1,250 1,250 1250 1000 14,750

Cash Sales Product 2- Price/Unit 24.00£ 24.00 24.00 24.00 24.00 24.00 24.00 24.00 24.00 24.00 24.00 24.00

Sub Total Product 2 30,000 30,000 30,000 30,000 30,000 30,000 30,000 30,000 30,000 30,000 30,000 24,000 354,000

Credit Sales Product 3-Units 417 417 417 417 417 417 417 417 417 417 417 333 4,917

Credit Sales Product 3- Price/Unit 25.00 25.00 25.00 25.00 25.00 25.00 25.00 25.00 25.00 25.00 25.00 25.00

Sub Total Credit Sales Product 3 10,417 10,417 10,417 10,417 10,417 10,417 10,417 10,417 10,417 10,417 10,417 8,333 122,917

Total Cost of Sales/Variable/Direct Costs 87,417 87,417 87,417 87,417 87,417 87,417 87,417 87,417 87,417 87,417 87,417 79,333 1,040,917

CUMULATIVE Cost of Sales 87,417 174,833 262,250 349,667 437,083 524,500 611,917 699,333 786,750 874,167 961,583 1,040,917 1,040,917 1,040,917

Fixed Costs and Equipment etc

New Van 25,000 25,000

Equipment 5,000 5,000

xxxxx -

xxxxx -

Total Start Up Costs 30,000 30,000 30,000

Fixed Costs

Salaries(Fixed) 8,333 8,333 8,333 8,333 8,333 8,333 8,333 8,333 8,333 8,333 8,333 8,333 100,000

Rent 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 60,000

Marketing/Adv/Legal/Accountancy 4,167 4,167 4,167 4,167 4,167 4,167 4,167 4,167 4,167 4,167 4,167 4,167 50,000

Electricity 2,917 2,917 2,917 2,917 2,917 2,917 2,917 2,917 2,917 2,917 2,917 2,917 35,000

Public Indemnity Insurance 833 833 833 833 833 833 833 833 833 833 833 833 10,000

Total Fixed Costs 21,250 21,250 21,250 21,250 21,250 21,250 21,250 21,250 21,250 21,250 21,250 21,250 255,000 255,000

Total Payments

(V.C + Fixed+

Equipment/Start

Up Costs) 138,667 108,667 108,667 108,667 108,667 108,667 108,667 108,667 108,667 108,667 108,667 100,583 1,325,917 1,325,917

CUMULATIVE PAYMENTS 138,667 247,333 356,000 464,667 573,333 682,000 790,667 899,333 1,008,000 1,116,667 1,225,333 1,325,917 1,325,917

Net Cash Flow 71,392 101,392 101,392 101,392 101,392 101,392 101,392 101,392 101,392 101,392 101,392 91,363

Opening Bank Balance 10,000 81,392 182,783 284,175 385,567 486,958 588,350 689,742 791,133 892,525 993,917 1,095,308

Closing Balance 81,392 182,783 284,175 385,567 486,958 588,350 689,742 791,133 892,525 993,917 1,095,308 1,186,672

Calculate CONTRIBUTION by subtracting SALES RECEIPTS-COST OF SALES

CONTRIBUTION 122,642 122,642 122,642 122,642 122,642 122,642 122,642 122,642 122,642 122,642 122,642 112,613

CUMULATIVE CONTRIBUTION 122,642 245,283 367,925 490,567 613,208 735,850 858,492 981,133 1,103,775 1,226,417 1,349,058 1,461,672

8

Assumptions Seasonality Weight Matrix

January February March April May June July August September October November December

Product 1 Quantity 2500 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100%

Sales Price 47.80 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100%

Cost Price 23.90 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100%

Product 2 Quantity 1250 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 80%

Sales Price 52.38 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100%

Cost Price 29.10 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100%

Product 3 Quantity 416.6666667 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 80%

Sales Price 60.20 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100%

Cost Price 30.10 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100%

Fixed Costs PER ANNUM

Wages/Salaries(Fixed) 100,000

Rent 60,000

Broadband 50,000

Electricity 35,000

Public Indemnity Insurance 10,000

Total Fixed Assets 255,000

INPUT is in BLUE

January February March April May June July August September October November December Totals Total Sales

Receipts

Sales Product 1-Units 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2500 2500 30,000 30,000 units

Cash Sales Product 1- £Price/Unit 47.80 47.80 47.80 47.80 47.80 47.80 47.80 47.80 47.80 47.80 47.80 47.80

Sub Total Cash Sales Product 1 119,500 119,500 119,500 119,500 119,500 119,500 119,500 119,500 119,500 119,500 119,500 119,500 £1,434,000

Sales Product 2-Units 1,250 1,250 1,250 1,250 1,250 1,250 1,250 1,250 1,250 1,250 1250 1000 14,750 14,750

Cash Sales Product 2- Price/Unit 52.38 52.38 52.38 52.38 52.38 52.38 52.38 52.38 52.38 52.38 52.38 52.38

Sub Total Product 2 65,475 65,475 65,475 65,475 65,475 65,475 65,475 65,475 65,475 65,475 65,475 52,380 £772,605

Sales Product 3-Units 417 417 417 417 417 417 417 417 417 417 417 333 4,917 4,917

Credit Sales Product 3- Price/Unit 60.20 60.20 60.20 60.20 60.20 60.20 60.20 60.20 60.20 60.20 60.20 60.20

Sub Total Credit Sales Product 3 25,083 25,083 25,083 25,083 25,083 25,083 25,083 25,083 25,083 25,083 25083.33 20066.67 £295,983.33

TOTAL Receipts from Sales 210,058 210,058 210,058 210,058 210,058 210,058 210,058 210,058 210,058 210,058 210,058 191,947 2,502,588

CUMULATIVE Receipts from Sales 210,058 420,117 630,175 840,233 1,050,292 1,260,350 1,470,408 1,680,467 1,890,525 2,100,583 2,310,642 2,502,588 49,667

Payments

Cost Of Sales/Variable Costs

Cost of Sales Product 1-Units 2500 2500 2500 2500 2500 2500 2500 2500 2500 2500 2500 2500 30,000

Cost of Sales Product 1- Price/Unit 18.80£ 18.80£ 18.80£ 18.80£ 18.80£ 18.80£ 18.80£ 18.80£ 19 19 19 19

Sub Total Direct Costs 1 47,000 47,000 47,000 47,000 47,000 47,000 47,000 47,000 47,000 47,000 47,000 47,000 564,000

Cash Sales Product 2-Units 1,250 1,250 1,250 1,250 1,250 1,250 1,250 1,250 1,250 1,250 1250 1000 14,750

Cash Sales Product 2- Price/Unit 24.00£ 24.00 24.00 24.00 24.00 24.00 24.00 24.00 24.00 24.00 24.00 24.00

Sub Total Product 2 30,000 30,000 30,000 30,000 30,000 30,000 30,000 30,000 30,000 30,000 30,000 24,000 354,000

Credit Sales Product 3-Units 417 417 417 417 417 417 417 417 417 417 417 333 4,917

Credit Sales Product 3- Price/Unit 25.00 25.00 25.00 25.00 25.00 25.00 25.00 25.00 25.00 25.00 25.00 25.00

Sub Total Credit Sales Product 3 10,417 10,417 10,417 10,417 10,417 10,417 10,417 10,417 10,417 10,417 10,417 8,333 122,917

Total Cost of Sales/Variable/Direct Costs 87,417 87,417 87,417 87,417 87,417 87,417 87,417 87,417 87,417 87,417 87,417 79,333 1,040,917

CUMULATIVE Cost of Sales 87,417 174,833 262,250 349,667 437,083 524,500 611,917 699,333 786,750 874,167 961,583 1,040,917 1,040,917 1,040,917

Fixed Costs and Equipment etc

New Van 25,000 25,000

Equipment 5,000 5,000

xxxxx -

xxxxx -

Total Start Up Costs 30,000 30,000 30,000

Fixed Costs

Salaries(Fixed) 8,333 8,333 8,333 8,333 8,333 8,333 8,333 8,333 8,333 8,333 8,333 8,333 100,000

Rent 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 60,000

Marketing/Adv/Legal/Accountancy 4,167 4,167 4,167 4,167 4,167 4,167 4,167 4,167 4,167 4,167 4,167 4,167 50,000

Electricity 2,917 2,917 2,917 2,917 2,917 2,917 2,917 2,917 2,917 2,917 2,917 2,917 35,000

Public Indemnity Insurance 833 833 833 833 833 833 833 833 833 833 833 833 10,000

Total Fixed Costs 21,250 21,250 21,250 21,250 21,250 21,250 21,250 21,250 21,250 21,250 21,250 21,250 255,000 255,000

Total Payments

(V.C + Fixed+

Equipment/Start

Up Costs) 138,667 108,667 108,667 108,667 108,667 108,667 108,667 108,667 108,667 108,667 108,667 100,583 1,325,917 1,325,917

CUMULATIVE PAYMENTS 138,667 247,333 356,000 464,667 573,333 682,000 790,667 899,333 1,008,000 1,116,667 1,225,333 1,325,917 1,325,917

Net Cash Flow 71,392 101,392 101,392 101,392 101,392 101,392 101,392 101,392 101,392 101,392 101,392 91,363

Opening Bank Balance 10,000 81,392 182,783 284,175 385,567 486,958 588,350 689,742 791,133 892,525 993,917 1,095,308

Closing Balance 81,392 182,783 284,175 385,567 486,958 588,350 689,742 791,133 892,525 993,917 1,095,308 1,186,672

Calculate CONTRIBUTION by subtracting SALES RECEIPTS-COST OF SALES

CONTRIBUTION 122,642 122,642 122,642 122,642 122,642 122,642 122,642 122,642 122,642 122,642 122,642 112,613

CUMULATIVE CONTRIBUTION 122,642 245,283 367,925 490,567 613,208 735,850 858,492 981,133 1,103,775 1,226,417 1,349,058 1,461,672

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

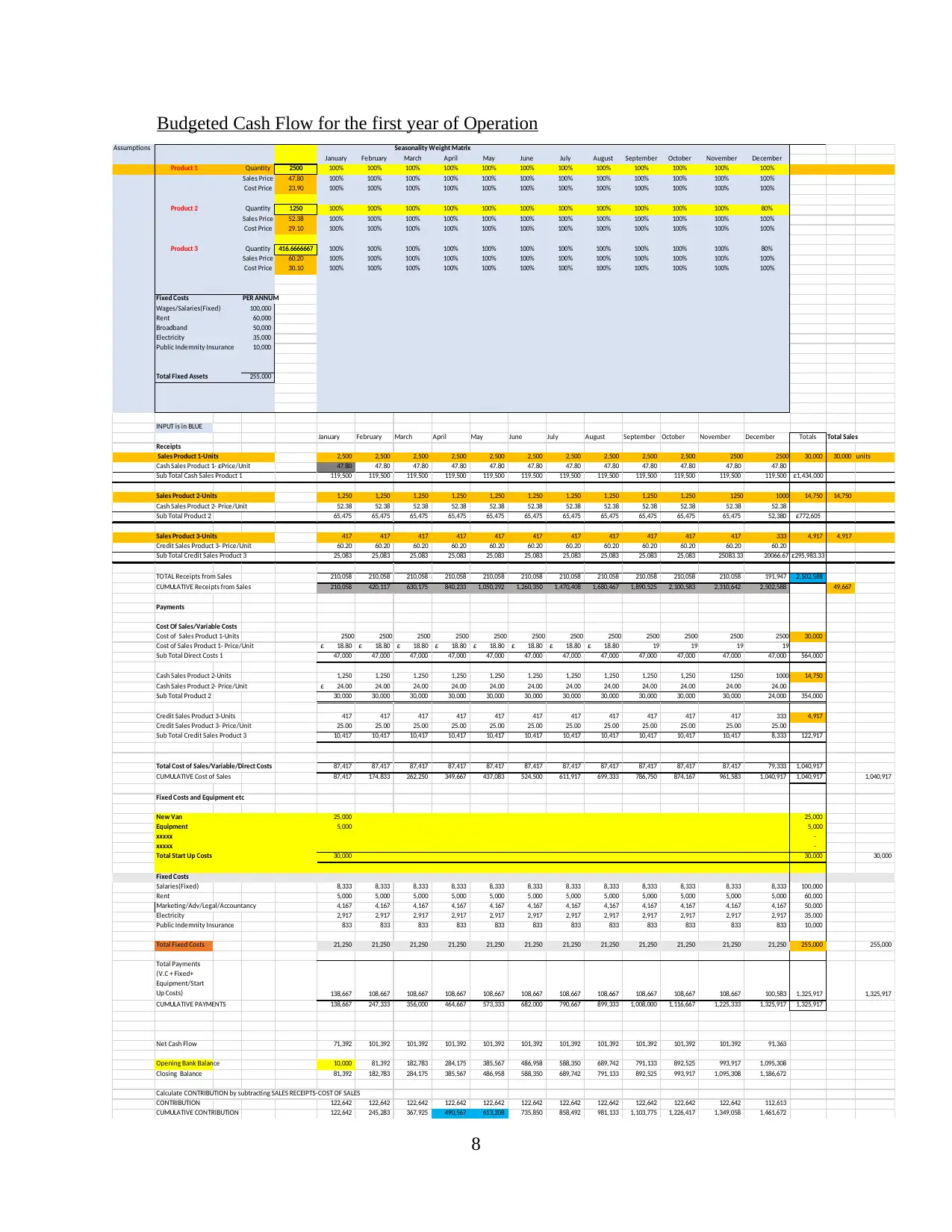

The budgeted cash flow of any business whether it is of first year or subsequent specific

time periods will be serving as foundation which will represent the pattern and volume of

products and services sold by the company in that particular period of time (Zhang, Zhang and

Zhou, 2021). Also, how much cost was incurred to make them and determining the period of

time during which this cash came in and went out of the company can be determined. The

projected cash flow of the Fashlet business is prepared as per the accounting standards and

concepts (Harris and Roark, 2019). The receipts section is divided into three parts representing

the cash inflows from the three categories of products. Further in the payments firstly all the

variable costs are added and then fixed costs are added. After deduction of variable costs and

fixed costs payments net profits amount has been arrived to.

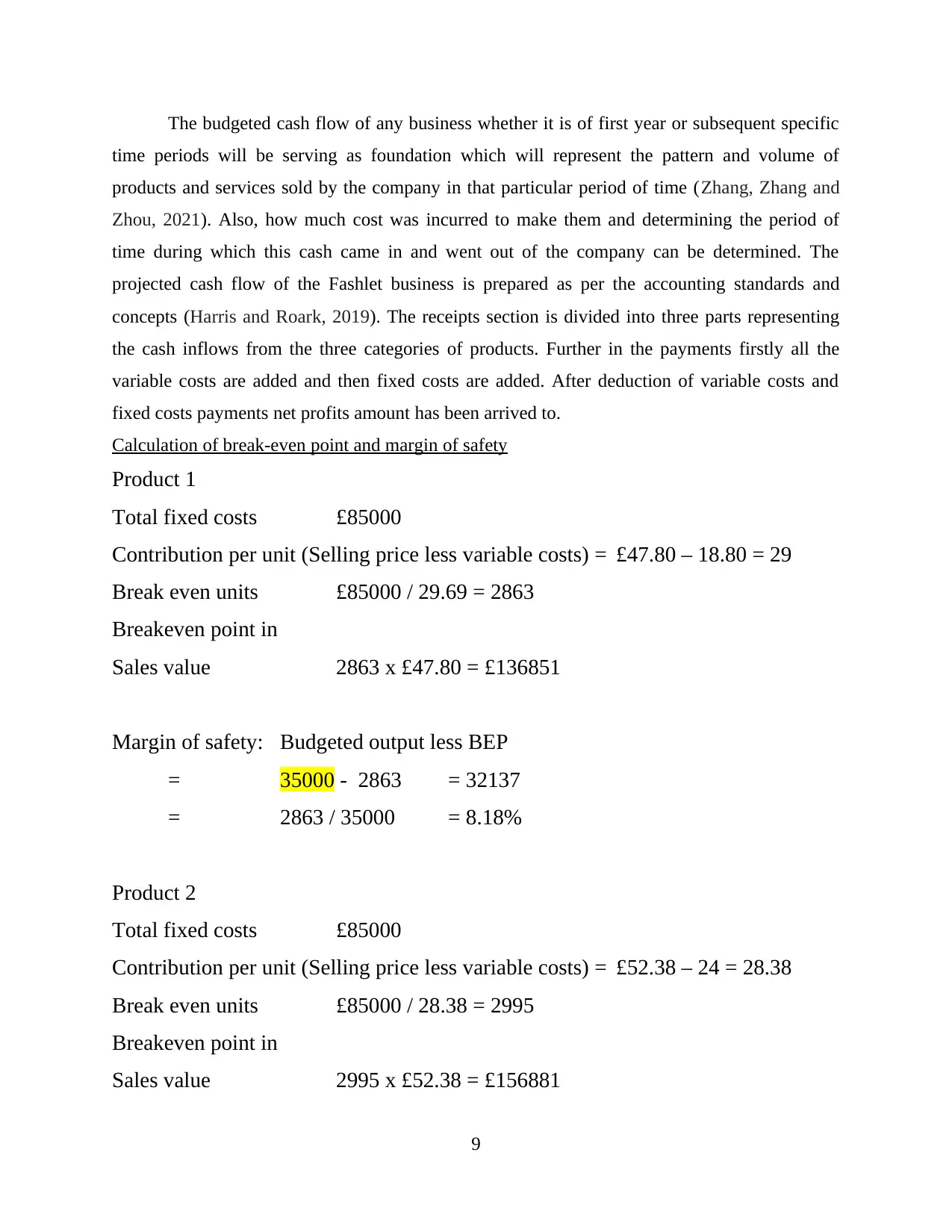

Calculation of break-even point and margin of safety

Product 1

Total fixed costs £85000

Contribution per unit (Selling price less variable costs) = £47.80 – 18.80 = 29

Break even units £85000 / 29.69 = 2863

Breakeven point in

Sales value 2863 x £47.80 = £136851

Margin of safety: Budgeted output less BEP

= 35000 - 2863 = 32137

= 2863 / 35000 = 8.18%

Product 2

Total fixed costs £85000

Contribution per unit (Selling price less variable costs) = £52.38 – 24 = 28.38

Break even units £85000 / 28.38 = 2995

Breakeven point in

Sales value 2995 x £52.38 = £156881

9

time periods will be serving as foundation which will represent the pattern and volume of

products and services sold by the company in that particular period of time (Zhang, Zhang and

Zhou, 2021). Also, how much cost was incurred to make them and determining the period of

time during which this cash came in and went out of the company can be determined. The

projected cash flow of the Fashlet business is prepared as per the accounting standards and

concepts (Harris and Roark, 2019). The receipts section is divided into three parts representing

the cash inflows from the three categories of products. Further in the payments firstly all the

variable costs are added and then fixed costs are added. After deduction of variable costs and

fixed costs payments net profits amount has been arrived to.

Calculation of break-even point and margin of safety

Product 1

Total fixed costs £85000

Contribution per unit (Selling price less variable costs) = £47.80 – 18.80 = 29

Break even units £85000 / 29.69 = 2863

Breakeven point in

Sales value 2863 x £47.80 = £136851

Margin of safety: Budgeted output less BEP

= 35000 - 2863 = 32137

= 2863 / 35000 = 8.18%

Product 2

Total fixed costs £85000

Contribution per unit (Selling price less variable costs) = £52.38 – 24 = 28.38

Break even units £85000 / 28.38 = 2995

Breakeven point in

Sales value 2995 x £52.38 = £156881

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

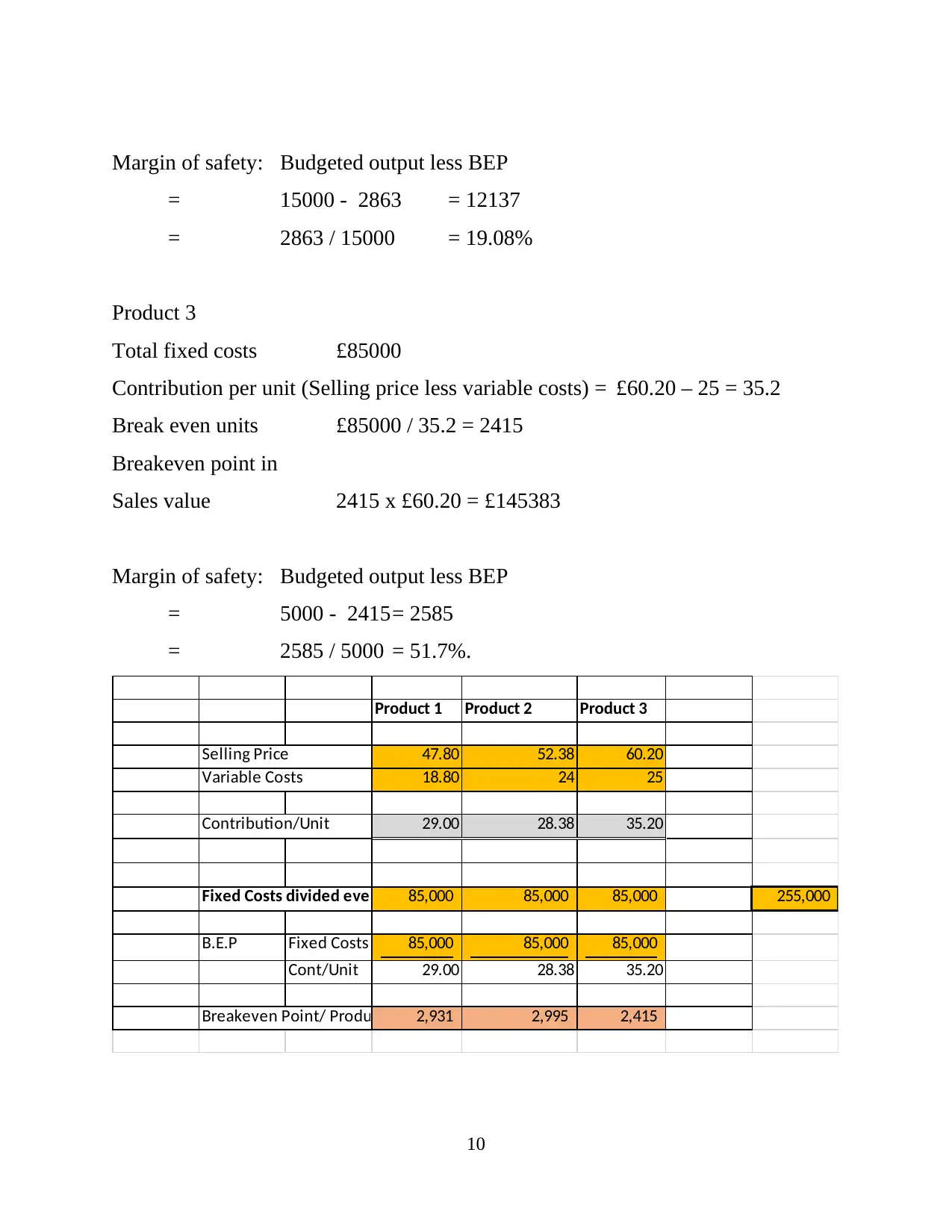

Margin of safety: Budgeted output less BEP

= 15000 - 2863 = 12137

= 2863 / 15000 = 19.08%

Product 3

Total fixed costs £85000

Contribution per unit (Selling price less variable costs) = £60.20 – 25 = 35.2

Break even units £85000 / 35.2 = 2415

Breakeven point in

Sales value 2415 x £60.20 = £145383

Margin of safety: Budgeted output less BEP

= 5000 - 2415= 2585

= 2585 / 5000 = 51.7%.

Product 1 Product 2 Product 3

Selling Price 47.80 52.38 60.20

Variable Costs 18.80 24 25

Contribution/Unit 29.00 28.38 35.20

Fixed Costs divided evenly 85,000 85,000 85,000 255,000

B.E.P Fixed Costs 85,000 85,000 85,000

Cont/Unit 29.00 28.38 35.20

Breakeven Point/ Product 2,931 2,995 2,415

10

= 15000 - 2863 = 12137

= 2863 / 15000 = 19.08%

Product 3

Total fixed costs £85000

Contribution per unit (Selling price less variable costs) = £60.20 – 25 = 35.2

Break even units £85000 / 35.2 = 2415

Breakeven point in

Sales value 2415 x £60.20 = £145383

Margin of safety: Budgeted output less BEP

= 5000 - 2415= 2585

= 2585 / 5000 = 51.7%.

Product 1 Product 2 Product 3

Selling Price 47.80 52.38 60.20

Variable Costs 18.80 24 25

Contribution/Unit 29.00 28.38 35.20

Fixed Costs divided evenly 85,000 85,000 85,000 255,000

B.E.P Fixed Costs 85,000 85,000 85,000

Cont/Unit 29.00 28.38 35.20

Breakeven Point/ Product 2,931 2,995 2,415

10

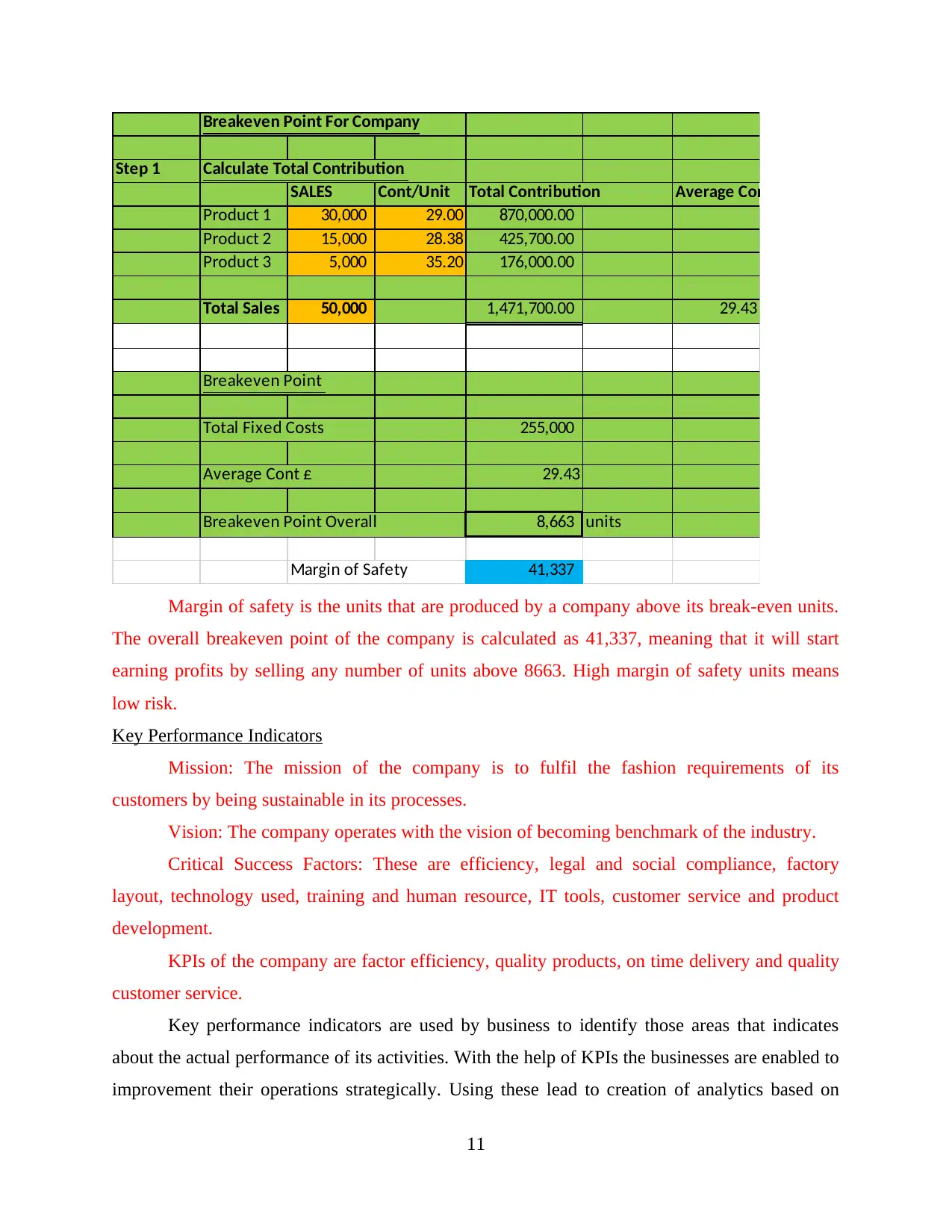

Breakeven Point For Company

Step 1 Calculate Total Contribution

SALES Cont/Unit Total Contribution Average Cont..

Product 1 30,000 29.00 870,000.00

Product 2 15,000 28.38 425,700.00

Product 3 5,000 35.20 176,000.00

Total Sales 50,000 1,471,700.00 29.43

Breakeven Point

Total Fixed Costs 255,000

Average Cont £ 29.43

Breakeven Point Overall 8,663 units

Margin of Safety 41,337

Margin of safety is the units that are produced by a company above its break-even units.

The overall breakeven point of the company is calculated as 41,337, meaning that it will start

earning profits by selling any number of units above 8663. High margin of safety units means

low risk.

Key Performance Indicators

Mission: The mission of the company is to fulfil the fashion requirements of its

customers by being sustainable in its processes.

Vision: The company operates with the vision of becoming benchmark of the industry.

Critical Success Factors: These are efficiency, legal and social compliance, factory

layout, technology used, training and human resource, IT tools, customer service and product

development.

KPIs of the company are factor efficiency, quality products, on time delivery and quality

customer service.

Key performance indicators are used by business to identify those areas that indicates

about the actual performance of its activities. With the help of KPIs the businesses are enabled to

improvement their operations strategically. Using these lead to creation of analytics based on

11

Step 1 Calculate Total Contribution

SALES Cont/Unit Total Contribution Average Cont..

Product 1 30,000 29.00 870,000.00

Product 2 15,000 28.38 425,700.00

Product 3 5,000 35.20 176,000.00

Total Sales 50,000 1,471,700.00 29.43

Breakeven Point

Total Fixed Costs 255,000

Average Cont £ 29.43

Breakeven Point Overall 8,663 units

Margin of Safety 41,337

Margin of safety is the units that are produced by a company above its break-even units.

The overall breakeven point of the company is calculated as 41,337, meaning that it will start

earning profits by selling any number of units above 8663. High margin of safety units means

low risk.

Key Performance Indicators

Mission: The mission of the company is to fulfil the fashion requirements of its

customers by being sustainable in its processes.

Vision: The company operates with the vision of becoming benchmark of the industry.

Critical Success Factors: These are efficiency, legal and social compliance, factory

layout, technology used, training and human resource, IT tools, customer service and product

development.

KPIs of the company are factor efficiency, quality products, on time delivery and quality

customer service.

Key performance indicators are used by business to identify those areas that indicates

about the actual performance of its activities. With the help of KPIs the businesses are enabled to

improvement their operations strategically. Using these lead to creation of analytics based on

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

which the decisions are taken on the priority basis. Matters having highest priority are addressed

on urgent basis (Dipura and Soediantono, 2022). Good indicators of firm’s performance are

important as provides evidence for the process that business activities are making. All the areas

that are needed to be measured for the purpose of taking decisions are effectively measure with

help of such KPIs. These are a set of measurements that are in the quantifiable format helping

company to assess its overall performance in long term. Determination of Fashlet’s financial,

strategic and operational accomplishments can be done with key performance indicators.

KPIs can be of three types based on their utility. Financial metrics is the first type of KPI,

as th name suggests the main focus is on the revenues and profits earned by the firm. For

measuring the profits net profit is the best and the most used element. Fashlet targets to earn a

net profit of 50 percent for the first operational year. At the end of such financial year that 2023,

the company will compare its actual net profit with this expected or projected profit to assess its

performance. Corrective measures will be taken if there will be a deviation in the actual and set

net profit earnings (Sun and Ge, 2020). This set target is decided as the performance indicators

based on the industry standards.

Customer Metrics is another kind of KPI. The focus is led over the satisfaction and

retention of customers. Customers are the main aspect for Fashlet, as these are the ones who can

make the operations of the company a success. The life time value a customer is deducted for the

cost incurred for acquiring such a customer (Korenfeld and et.al., 2021). Customers life time

value is the sum of money that is expected by the company such customers will spend on

purchasing the products of the company. And customer acquisition costs involve any discounts

given to buyers pacifying them to take their buying decisions, advertisement expenses, etc.

Higher the difference better is the company’s performance.

The third type is the process performance metrics, with this focus is over monitoring of

performance across the entity. It is measured by the number of total products produced that are

damaged. It is desirable to have minimal or no damaged products. Process performance of

Fashlet can be measured by the average time it takes to provide services to its consumers. The

examples can be how much time a customer has to wait to get attended by a salesperson of the

outlet (Yu and et.al., 2019). Time customer has to wait for the billing of the products purchased

is another example. Both should be as low as possible for the better performance of the company.

12

on urgent basis (Dipura and Soediantono, 2022). Good indicators of firm’s performance are

important as provides evidence for the process that business activities are making. All the areas

that are needed to be measured for the purpose of taking decisions are effectively measure with

help of such KPIs. These are a set of measurements that are in the quantifiable format helping

company to assess its overall performance in long term. Determination of Fashlet’s financial,

strategic and operational accomplishments can be done with key performance indicators.

KPIs can be of three types based on their utility. Financial metrics is the first type of KPI,

as th name suggests the main focus is on the revenues and profits earned by the firm. For

measuring the profits net profit is the best and the most used element. Fashlet targets to earn a

net profit of 50 percent for the first operational year. At the end of such financial year that 2023,

the company will compare its actual net profit with this expected or projected profit to assess its

performance. Corrective measures will be taken if there will be a deviation in the actual and set

net profit earnings (Sun and Ge, 2020). This set target is decided as the performance indicators

based on the industry standards.

Customer Metrics is another kind of KPI. The focus is led over the satisfaction and

retention of customers. Customers are the main aspect for Fashlet, as these are the ones who can

make the operations of the company a success. The life time value a customer is deducted for the

cost incurred for acquiring such a customer (Korenfeld and et.al., 2021). Customers life time

value is the sum of money that is expected by the company such customers will spend on

purchasing the products of the company. And customer acquisition costs involve any discounts

given to buyers pacifying them to take their buying decisions, advertisement expenses, etc.

Higher the difference better is the company’s performance.

The third type is the process performance metrics, with this focus is over monitoring of

performance across the entity. It is measured by the number of total products produced that are

damaged. It is desirable to have minimal or no damaged products. Process performance of

Fashlet can be measured by the average time it takes to provide services to its consumers. The

examples can be how much time a customer has to wait to get attended by a salesperson of the

outlet (Yu and et.al., 2019). Time customer has to wait for the billing of the products purchased

is another example. Both should be as low as possible for the better performance of the company.

12

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Conclusion and Recommendations

Based on the results of the key fixed & variable costs along with the budgeted profit and

budgeted cash flow which allowed calculation of breakeven point and margin of safety it can be

said that the business seems to be profitable from the initial year of its operations represented by

the profits shown in the budgeted forecast of the profits and also the company is able to maintain

reasonable balance of cash which is represented by the budgeted cash flow thus it is

recommended to operate the business as planned. It is suggested for the Fashlet to adopt social

media marketing as a marketing tool. It will help the business to reduce its marketing expenses

and reach a larger number of audience. Further to maximise the sales by the business it is

recommended to sell its products through online channels in addition to its physical outlets.

13

Based on the results of the key fixed & variable costs along with the budgeted profit and

budgeted cash flow which allowed calculation of breakeven point and margin of safety it can be

said that the business seems to be profitable from the initial year of its operations represented by

the profits shown in the budgeted forecast of the profits and also the company is able to maintain

reasonable balance of cash which is represented by the budgeted cash flow thus it is

recommended to operate the business as planned. It is suggested for the Fashlet to adopt social

media marketing as a marketing tool. It will help the business to reduce its marketing expenses

and reach a larger number of audience. Further to maximise the sales by the business it is

recommended to sell its products through online channels in addition to its physical outlets.

13

REFERENCES

Books and Journals

Dipura, S. and Soediantono, D., 2022. Benefits of Key Performance Indicators (KPI) and

Proposed Applications in the Defense Industry: A Literature Review. International

Journal of Social and Management Studies. 3(4). pp.23-33.

Gazzola, P. and et.al., 2020. Trends in the fashion industry. The perception of sustainability and

circular economy: A gender/generation quantitative approach. Sustainability. 12(7).

p.2809.

Goworek, H. and et.al., 2020. Managing sustainability in the fashion business: Challenges in

product development for clothing longevity in the UK. Journal of Business

Research. 117. pp.629-641.

Harris, C. and Roark, S., 2019. Cash flow risk and capital structure decisions. Finance Research

Letters. 29. pp.393-397.

Korenfeld, M. and et.al., 2021. Safety of KPI-121 ophthalmic suspension 0.25% in patients with

dry eye disease: a pooled analysis of 4 multicenter, randomized, vehicle-controlled

studies. Cornea. 40(5). pp.564-570.

Sun, Q. and Ge, Z., 2020. Deep learning for industrial KPI prediction: When ensemble learning

meets semi-supervised data. IEEE Transactions on Industrial Informatics. 17(1). pp.260-

269.

Thorisdottir, T. S. and Johannsdottir, L., 2020. Corporate social responsibility influencing

sustainability within the fashion industry. A systematic review. Sustainability. 12(21).

p.9167.

Yu, G. and et.al., 2019. Unsupervised online anomaly detection with parameter adaptation for

KPI abrupt changes. IEEE Transactions on Network and Service Management. 17(3).

pp.1294-1308.

Zhang, B., Zhang, Y. and Zhou, P., 2021. Consumer attitude towards sustainability of fast

fashion products in the UK. Sustainability. 13(4). p.1646.

14

Books and Journals

Dipura, S. and Soediantono, D., 2022. Benefits of Key Performance Indicators (KPI) and

Proposed Applications in the Defense Industry: A Literature Review. International

Journal of Social and Management Studies. 3(4). pp.23-33.

Gazzola, P. and et.al., 2020. Trends in the fashion industry. The perception of sustainability and

circular economy: A gender/generation quantitative approach. Sustainability. 12(7).

p.2809.

Goworek, H. and et.al., 2020. Managing sustainability in the fashion business: Challenges in

product development for clothing longevity in the UK. Journal of Business

Research. 117. pp.629-641.

Harris, C. and Roark, S., 2019. Cash flow risk and capital structure decisions. Finance Research

Letters. 29. pp.393-397.

Korenfeld, M. and et.al., 2021. Safety of KPI-121 ophthalmic suspension 0.25% in patients with

dry eye disease: a pooled analysis of 4 multicenter, randomized, vehicle-controlled

studies. Cornea. 40(5). pp.564-570.

Sun, Q. and Ge, Z., 2020. Deep learning for industrial KPI prediction: When ensemble learning

meets semi-supervised data. IEEE Transactions on Industrial Informatics. 17(1). pp.260-

269.

Thorisdottir, T. S. and Johannsdottir, L., 2020. Corporate social responsibility influencing

sustainability within the fashion industry. A systematic review. Sustainability. 12(21).

p.9167.

Yu, G. and et.al., 2019. Unsupervised online anomaly detection with parameter adaptation for

KPI abrupt changes. IEEE Transactions on Network and Service Management. 17(3).

pp.1294-1308.

Zhang, B., Zhang, Y. and Zhou, P., 2021. Consumer attitude towards sustainability of fast

fashion products in the UK. Sustainability. 13(4). p.1646.

14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.