Business Finance Report: Uber Tools Ltd Financial Performance Analysis

VerifiedAdded on 2020/10/23

|11

|3312

|175

Report

AI Summary

This report provides a comprehensive analysis of business finance, focusing on the concepts of profit, cash flow, and working capital, and their application to a case study of Uber Tools Ltd. The report begins by differentiating between profit and cash flow, explaining the significance of working capital, and exploring how changes in working capital impact cash flow. It then applies these concepts to Uber Tools Ltd, examining its financial performance through the lens of financial ratios, including sales growth, gross profit, operating profit, gearing ratio, interest coverage, liquidity ratio, return on equity, and return on capital employed. The analysis includes a cash flow statement for Uber Tools Ltd, identifying sources and uses of cash. The report also provides recommendations for improving the company's cash flow through better working capital management, including resolving disputes with customers, managing inventory levels, and addressing debt obligations. Finally, it assesses the financial performance of the business based on the calculated ratios and offers insights into the company's financial health and areas for improvement.

BUSINESS FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

1. a) Profit and cash Flow and their Difference .........................................................................1

b) Working capital and the meaning of receivables, inventory and payables.............................2

c) Changes in working capital affect cash flow .........................................................................2

2) Application of concepts to Uber Tools Ltd ...........................................................................3

3) Steps that should be taken to improve company's cash flow through better working capital

management................................................................................................................................4

PART 2............................................................................................................................................4

1. a) Elements of financial performance.....................................................................................4

b) Calculation of Ratios..............................................................................................................5

c) Application of result based on result ......................................................................................6

2) Analyse and recommendation for assessing the financial performance of business .............7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

1. a) Profit and cash Flow and their Difference .........................................................................1

b) Working capital and the meaning of receivables, inventory and payables.............................2

c) Changes in working capital affect cash flow .........................................................................2

2) Application of concepts to Uber Tools Ltd ...........................................................................3

3) Steps that should be taken to improve company's cash flow through better working capital

management................................................................................................................................4

PART 2............................................................................................................................................4

1. a) Elements of financial performance.....................................................................................4

b) Calculation of Ratios..............................................................................................................5

c) Application of result based on result ......................................................................................6

2) Analyse and recommendation for assessing the financial performance of business .............7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................9

INTRODUCTION

Business finance refers to the way the business can acquire funds for its operations. It

involved the money and credit involved in the business. It is required to make provision of funds

so that it can be used whenever the funds are required in business. This assignment will include

the Uber tools Ltd that owns and operated a factory in Newmarket producing powers tools. The

company’s last year turnover was £400 Million. Further, this assignment will provide

understanding about profit and cash flow and how these two are different. Also, it will explain

information about changes in working capital and its effect on cash flow along with financial

performance of the company on the basis of financial ratios.

PART 1

1. a) Profit and cash Flow and their Difference

Profit of the company provide understanding about the revenue earned by the company

during a financial year. Profitability of the company is determined on the basis of preparing the

income statement which provides understanding about the profits earned by company through its

business activities (Burns and Dewhurst, 2016). The company’s profit is the net income earned

by firm by deducting the operating and trading expenses from the sales. Without adequate profit,

a firm cannot survive in the long run (What's more important, cash flow or profits, 2018). Cash

flow refers to the cash inflow and outflow through the operating, financing and investing

activities performed by company.

Difference between profit and cash flow

Profit Cash Flow

It is the money left over the sales by

subtracting the cost.

It represents the money from different

activities which consist of operating,

financing and investing.

Timing in acquiring cash is different

because sometimes the cash is not

received by customers due to delay

payments (Jordà, Schularick and

Taylor, 2016).

It is calculated before the money is

received.

1

Business finance refers to the way the business can acquire funds for its operations. It

involved the money and credit involved in the business. It is required to make provision of funds

so that it can be used whenever the funds are required in business. This assignment will include

the Uber tools Ltd that owns and operated a factory in Newmarket producing powers tools. The

company’s last year turnover was £400 Million. Further, this assignment will provide

understanding about profit and cash flow and how these two are different. Also, it will explain

information about changes in working capital and its effect on cash flow along with financial

performance of the company on the basis of financial ratios.

PART 1

1. a) Profit and cash Flow and their Difference

Profit of the company provide understanding about the revenue earned by the company

during a financial year. Profitability of the company is determined on the basis of preparing the

income statement which provides understanding about the profits earned by company through its

business activities (Burns and Dewhurst, 2016). The company’s profit is the net income earned

by firm by deducting the operating and trading expenses from the sales. Without adequate profit,

a firm cannot survive in the long run (What's more important, cash flow or profits, 2018). Cash

flow refers to the cash inflow and outflow through the operating, financing and investing

activities performed by company.

Difference between profit and cash flow

Profit Cash Flow

It is the money left over the sales by

subtracting the cost.

It represents the money from different

activities which consist of operating,

financing and investing.

Timing in acquiring cash is different

because sometimes the cash is not

received by customers due to delay

payments (Jordà, Schularick and

Taylor, 2016).

It is calculated before the money is

received.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It is based on cash basis of accounting It is an accrual concept (Finance,

2015).

b) Working capital and the meaning of receivables, inventory and payables

Working capital is the money which is available within the firm from performing its day-

to – day operations. It is used to calculate the liquidity of the firm on the basis of its working

capital requirement. It is calculated by subtracting the current liabilities from the current assets. It

includes the account receivables, payables and inventory (Bendell and Doyle, 2017). Balance

sheet is used to identify the amount of working capital. Balance sheet is prepared to measure the

position and liquidity of the company by comparing assets and liabilities of the firm.

Account receivables: It is shown in the current assets of the balance sheet. This account

shows the amount which is due from the customers that purchased the goods on credit.

Account payables: It is an account which is shown on the liabilities side and provides

information about the amount which is unpaid to the suppliers or vendors of company for

purchasing the goods and services on credit (Canales, 2016).

Inventory: It is the amount of goods which is present with the company for selling and it

includes three stages which consist of raw material, work in progress and finished goods

(Inventory, 2018). It is recorded in current asset section as it is held with the company for less

than one year.

c) Changes in working capital affect cash flow

Working capital of the company have their impact on the cash flow because if there are

any changes in the working capital it will be reflected through the cash flow. Changes in working

capital affect the cash flow from operations.

The following are the changes which will affect the cash flow:

Increase in assets: If there is any increase in the assets, the cash flow from operations

will decrease.

Decrease in assets: If the assets side of the balance sheet is decreasing, then the cash

flow from operations will increase.

Increase in the balance of liability: There is a direct relation between the cash flow and

liabilities which means increase in liabilities will result in increase of cash flow from

operations (Kraemer-Eis and et.al., 2018).

2

2015).

b) Working capital and the meaning of receivables, inventory and payables

Working capital is the money which is available within the firm from performing its day-

to – day operations. It is used to calculate the liquidity of the firm on the basis of its working

capital requirement. It is calculated by subtracting the current liabilities from the current assets. It

includes the account receivables, payables and inventory (Bendell and Doyle, 2017). Balance

sheet is used to identify the amount of working capital. Balance sheet is prepared to measure the

position and liquidity of the company by comparing assets and liabilities of the firm.

Account receivables: It is shown in the current assets of the balance sheet. This account

shows the amount which is due from the customers that purchased the goods on credit.

Account payables: It is an account which is shown on the liabilities side and provides

information about the amount which is unpaid to the suppliers or vendors of company for

purchasing the goods and services on credit (Canales, 2016).

Inventory: It is the amount of goods which is present with the company for selling and it

includes three stages which consist of raw material, work in progress and finished goods

(Inventory, 2018). It is recorded in current asset section as it is held with the company for less

than one year.

c) Changes in working capital affect cash flow

Working capital of the company have their impact on the cash flow because if there are

any changes in the working capital it will be reflected through the cash flow. Changes in working

capital affect the cash flow from operations.

The following are the changes which will affect the cash flow:

Increase in assets: If there is any increase in the assets, the cash flow from operations

will decrease.

Decrease in assets: If the assets side of the balance sheet is decreasing, then the cash

flow from operations will increase.

Increase in the balance of liability: There is a direct relation between the cash flow and

liabilities which means increase in liabilities will result in increase of cash flow from

operations (Kraemer-Eis and et.al., 2018).

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

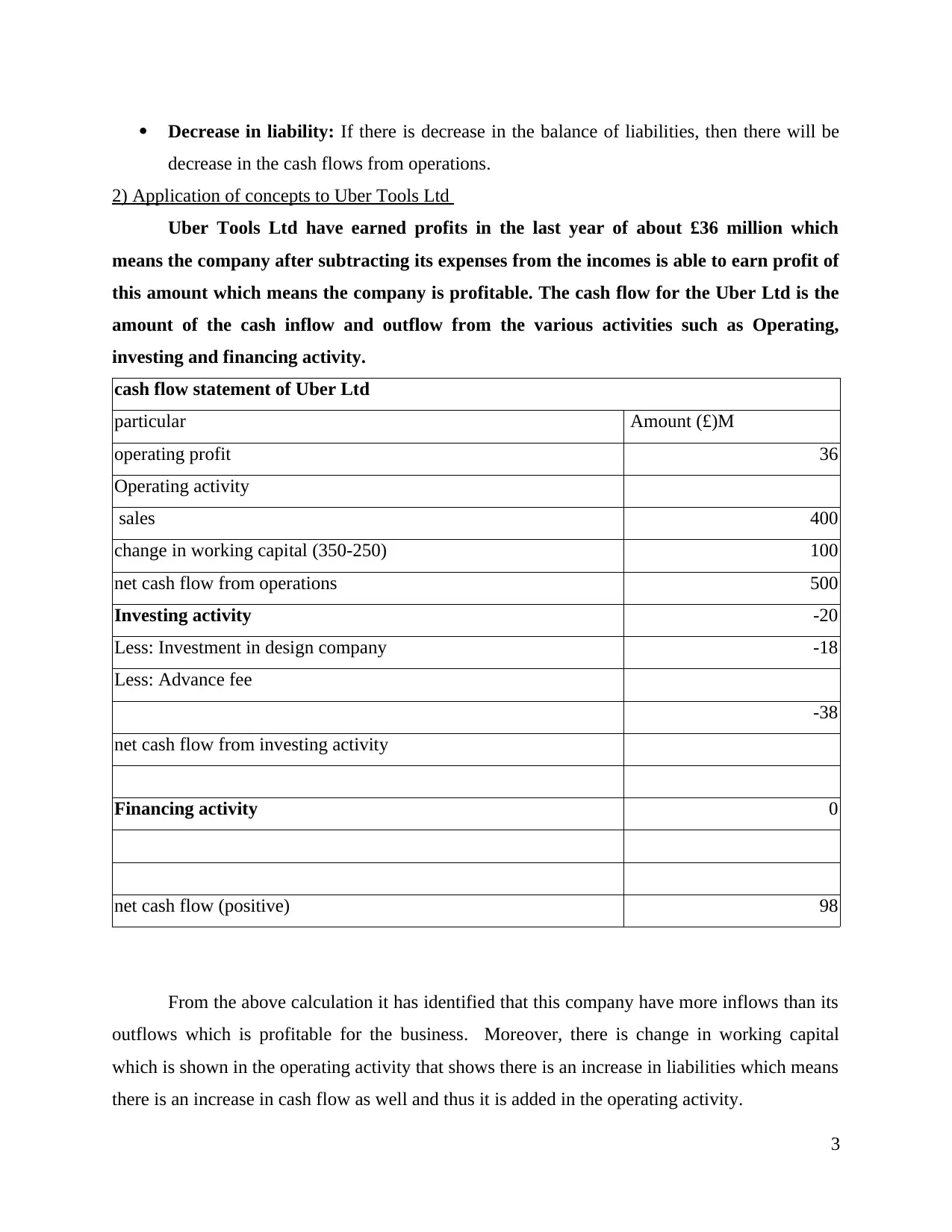

Decrease in liability: If there is decrease in the balance of liabilities, then there will be

decrease in the cash flows from operations.

2) Application of concepts to Uber Tools Ltd

Uber Tools Ltd have earned profits in the last year of about £36 million which

means the company after subtracting its expenses from the incomes is able to earn profit of

this amount which means the company is profitable. The cash flow for the Uber Ltd is the

amount of the cash inflow and outflow from the various activities such as Operating,

investing and financing activity.

cash flow statement of Uber Ltd

particular Amount (£)M

operating profit 36

Operating activity

sales 400

change in working capital (350-250) 100

net cash flow from operations 500

Investing activity -20

Less: Investment in design company -18

Less: Advance fee

-38

net cash flow from investing activity

Financing activity 0

net cash flow (positive) 98

From the above calculation it has identified that this company have more inflows than its

outflows which is profitable for the business. Moreover, there is change in working capital

which is shown in the operating activity that shows there is an increase in liabilities which means

there is an increase in cash flow as well and thus it is added in the operating activity.

3

decrease in the cash flows from operations.

2) Application of concepts to Uber Tools Ltd

Uber Tools Ltd have earned profits in the last year of about £36 million which

means the company after subtracting its expenses from the incomes is able to earn profit of

this amount which means the company is profitable. The cash flow for the Uber Ltd is the

amount of the cash inflow and outflow from the various activities such as Operating,

investing and financing activity.

cash flow statement of Uber Ltd

particular Amount (£)M

operating profit 36

Operating activity

sales 400

change in working capital (350-250) 100

net cash flow from operations 500

Investing activity -20

Less: Investment in design company -18

Less: Advance fee

-38

net cash flow from investing activity

Financing activity 0

net cash flow (positive) 98

From the above calculation it has identified that this company have more inflows than its

outflows which is profitable for the business. Moreover, there is change in working capital

which is shown in the operating activity that shows there is an increase in liabilities which means

there is an increase in cash flow as well and thus it is added in the operating activity.

3

The account receivables are the customers of this company which are D & R DIY Ltd

and BricoFrance SA, these are accounts which are shown on the assets side of balance sheet.

Also, the liabilities of the company are amounting of £350 million which has been increased

from £250 million and will be reflected in the cash flows.

There is a dispute between the BricoFrance SA and the company and it is required that

the company must maintain the inventory level of about £35 million after the dispute is sorted.

Also, the company paid advance fee to a designing company and invested a sum of £20 million

which is investment for the company and thus it is shown as an investment activity. The

company’s management might affect its financial results as there is no dispute with the main

customer due to which the company’s sales may get affected due to which the profitability of the

firm will also get affected.

3) Steps that should be taken to improve company's cash flow through better working capital

management

Working capital of Uber Tools Ltd = current assets – current liabilities

account receivable - debts

= 12- 350 = -338

Uber tools Ltd., in order to improve its cash flow must resolve the dispute with its

customer that is BricoFrance SA which will assist them in increasing the good relations with the

customers to pay the amount in order to maintain its positive working capital. It is required that

the company should managed its inventory level in order to increase its current assets to have

positive working capital which will in turn will assist in managing the working capital

requirement of firm. Also, the debts of the company are increased from £250 million to £350

million which means the liabilities of the company has been increased which will reduce the

working capital. Thus, it is required that the firm must meet its debt obligation to improve its

cash flow. It is required that the shareholders must invest more money in the company in order to

meet the debt's obligation of company (Scholes, 2015). It can be analysed that the working

capital of the company is negative and in order to manage that, it is required to improve the cash

flow of company. It is also needed to increase the cash inflow for the firm through increasing its

current assets.

PART 2

4

and BricoFrance SA, these are accounts which are shown on the assets side of balance sheet.

Also, the liabilities of the company are amounting of £350 million which has been increased

from £250 million and will be reflected in the cash flows.

There is a dispute between the BricoFrance SA and the company and it is required that

the company must maintain the inventory level of about £35 million after the dispute is sorted.

Also, the company paid advance fee to a designing company and invested a sum of £20 million

which is investment for the company and thus it is shown as an investment activity. The

company’s management might affect its financial results as there is no dispute with the main

customer due to which the company’s sales may get affected due to which the profitability of the

firm will also get affected.

3) Steps that should be taken to improve company's cash flow through better working capital

management

Working capital of Uber Tools Ltd = current assets – current liabilities

account receivable - debts

= 12- 350 = -338

Uber tools Ltd., in order to improve its cash flow must resolve the dispute with its

customer that is BricoFrance SA which will assist them in increasing the good relations with the

customers to pay the amount in order to maintain its positive working capital. It is required that

the company should managed its inventory level in order to increase its current assets to have

positive working capital which will in turn will assist in managing the working capital

requirement of firm. Also, the debts of the company are increased from £250 million to £350

million which means the liabilities of the company has been increased which will reduce the

working capital. Thus, it is required that the firm must meet its debt obligation to improve its

cash flow. It is required that the shareholders must invest more money in the company in order to

meet the debt's obligation of company (Scholes, 2015). It can be analysed that the working

capital of the company is negative and in order to manage that, it is required to improve the cash

flow of company. It is also needed to increase the cash inflow for the firm through increasing its

current assets.

PART 2

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

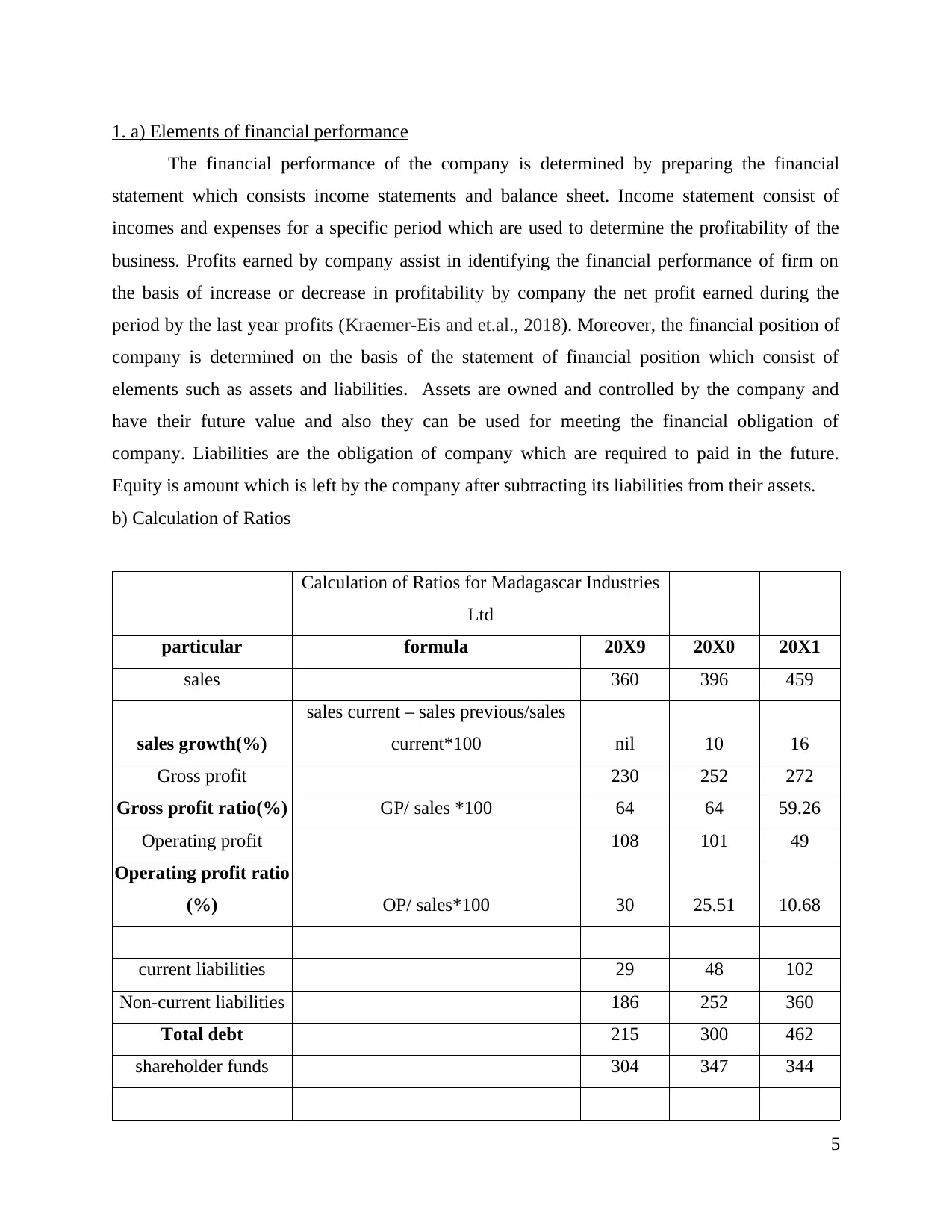

1. a) Elements of financial performance

The financial performance of the company is determined by preparing the financial

statement which consists income statements and balance sheet. Income statement consist of

incomes and expenses for a specific period which are used to determine the profitability of the

business. Profits earned by company assist in identifying the financial performance of firm on

the basis of increase or decrease in profitability by company the net profit earned during the

period by the last year profits (Kraemer-Eis and et.al., 2018). Moreover, the financial position of

company is determined on the basis of the statement of financial position which consist of

elements such as assets and liabilities. Assets are owned and controlled by the company and

have their future value and also they can be used for meeting the financial obligation of

company. Liabilities are the obligation of company which are required to paid in the future.

Equity is amount which is left by the company after subtracting its liabilities from their assets.

b) Calculation of Ratios

Calculation of Ratios for Madagascar Industries

Ltd

particular formula 20X9 20X0 20X1

sales 360 396 459

sales growth(%)

sales current – sales previous/sales

current*100 nil 10 16

Gross profit 230 252 272

Gross profit ratio(%) GP/ sales *100 64 64 59.26

Operating profit 108 101 49

Operating profit ratio

(%) OP/ sales*100 30 25.51 10.68

current liabilities 29 48 102

Non-current liabilities 186 252 360

Total debt 215 300 462

shareholder funds 304 347 344

5

The financial performance of the company is determined by preparing the financial

statement which consists income statements and balance sheet. Income statement consist of

incomes and expenses for a specific period which are used to determine the profitability of the

business. Profits earned by company assist in identifying the financial performance of firm on

the basis of increase or decrease in profitability by company the net profit earned during the

period by the last year profits (Kraemer-Eis and et.al., 2018). Moreover, the financial position of

company is determined on the basis of the statement of financial position which consist of

elements such as assets and liabilities. Assets are owned and controlled by the company and

have their future value and also they can be used for meeting the financial obligation of

company. Liabilities are the obligation of company which are required to paid in the future.

Equity is amount which is left by the company after subtracting its liabilities from their assets.

b) Calculation of Ratios

Calculation of Ratios for Madagascar Industries

Ltd

particular formula 20X9 20X0 20X1

sales 360 396 459

sales growth(%)

sales current – sales previous/sales

current*100 nil 10 16

Gross profit 230 252 272

Gross profit ratio(%) GP/ sales *100 64 64 59.26

Operating profit 108 101 49

Operating profit ratio

(%) OP/ sales*100 30 25.51 10.68

current liabilities 29 48 102

Non-current liabilities 186 252 360

Total debt 215 300 462

shareholder funds 304 347 344

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

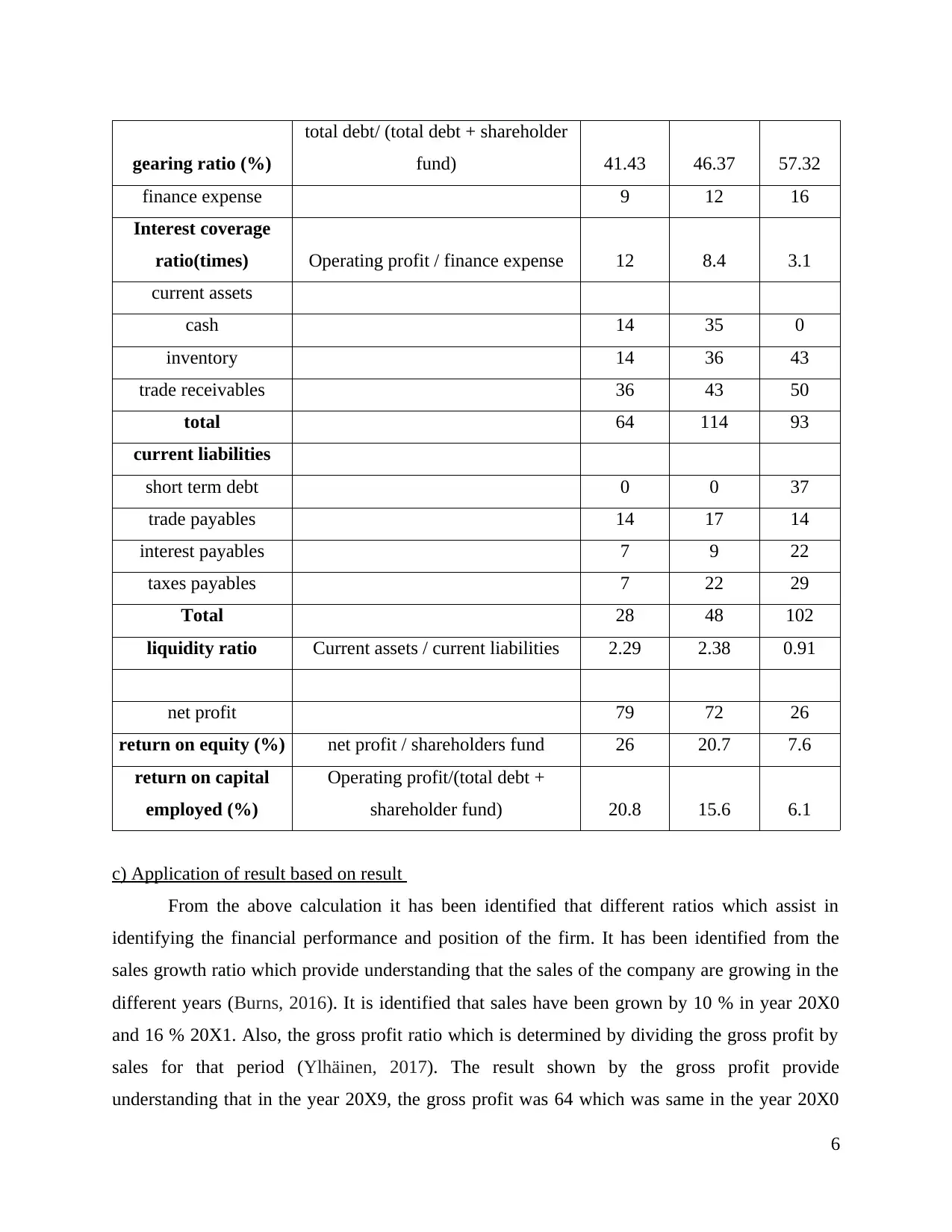

gearing ratio (%)

total debt/ (total debt + shareholder

fund) 41.43 46.37 57.32

finance expense 9 12 16

Interest coverage

ratio(times) Operating profit / finance expense 12 8.4 3.1

current assets

cash 14 35 0

inventory 14 36 43

trade receivables 36 43 50

total 64 114 93

current liabilities

short term debt 0 0 37

trade payables 14 17 14

interest payables 7 9 22

taxes payables 7 22 29

Total 28 48 102

liquidity ratio Current assets / current liabilities 2.29 2.38 0.91

net profit 79 72 26

return on equity (%) net profit / shareholders fund 26 20.7 7.6

return on capital

employed (%)

Operating profit/(total debt +

shareholder fund) 20.8 15.6 6.1

c) Application of result based on result

From the above calculation it has been identified that different ratios which assist in

identifying the financial performance and position of the firm. It has been identified from the

sales growth ratio which provide understanding that the sales of the company are growing in the

different years (Burns, 2016). It is identified that sales have been grown by 10 % in year 20X0

and 16 % 20X1. Also, the gross profit ratio which is determined by dividing the gross profit by

sales for that period (Ylhäinen, 2017). The result shown by the gross profit provide

understanding that in the year 20X9, the gross profit was 64 which was same in the year 20X0

6

total debt/ (total debt + shareholder

fund) 41.43 46.37 57.32

finance expense 9 12 16

Interest coverage

ratio(times) Operating profit / finance expense 12 8.4 3.1

current assets

cash 14 35 0

inventory 14 36 43

trade receivables 36 43 50

total 64 114 93

current liabilities

short term debt 0 0 37

trade payables 14 17 14

interest payables 7 9 22

taxes payables 7 22 29

Total 28 48 102

liquidity ratio Current assets / current liabilities 2.29 2.38 0.91

net profit 79 72 26

return on equity (%) net profit / shareholders fund 26 20.7 7.6

return on capital

employed (%)

Operating profit/(total debt +

shareholder fund) 20.8 15.6 6.1

c) Application of result based on result

From the above calculation it has been identified that different ratios which assist in

identifying the financial performance and position of the firm. It has been identified from the

sales growth ratio which provide understanding that the sales of the company are growing in the

different years (Burns, 2016). It is identified that sales have been grown by 10 % in year 20X0

and 16 % 20X1. Also, the gross profit ratio which is determined by dividing the gross profit by

sales for that period (Ylhäinen, 2017). The result shown by the gross profit provide

understanding that in the year 20X9, the gross profit was 64 which was same in the year 20X0

6

and after in the year 20X1 the gross profit reduced which shows the gross profitability is

reduced.

From the operating profit ratio which is identified by dividing the operating profit by

sales of that year. It is identified that the operating profit of the company is reduced over the

years which is not beneficial for the firms as it will lead to reduction the performance of

company. Furthermore, from the calculation it is identified about the gearing ratio which shows

relation between the debts and equity to identify the liquidity position of firm. Another ratio

which is related to interest coverage ratio shows the ability of the operating profit to cover the

interest expense of firm. It is shown that in the year 20X9, the operating profit can be used 12

times for covering the interest expense. Whereas in the year 20X0, the operating profit can be

used 8.4 times for covering interest expense and in the year 20X1 it can cover the interest

expense by 3.1 times.

From this, it can be interpreted that the interest coverage ratio is decreasing over the year

which is not beneficial for the company. From the calculation of Liquidity ratio which shows the

relation between the current assets and current liabilities and the ability of the current assets to

meet the current obligation of firm. The liquidity ratio in the year 20X9 was 2.29 which

increased to 2.38 in year 20X0 which shows the current assets are capable to meet the current

obligation of companies in these period. But in the year of 20X1 the liquidity ratio come to 0.91

which is less than the ideal ratio of 1:1 Which means the current assets of company cannot meet

the current obligation which is not good for the company.

Another ratio which is calculated is return on equity which shows the amount of return on

the capital invested in the firm which is reducing over the years and thus the returns for the

company on their equity are reducing. The return on capital employed ratio is calculated to

determine the amount of return on the capital employed in business which is also reducing over

the period. The change in the ratio is due to increase or decrease in the elements present in the

income or balance sheet statement which shows that the company is performing bad over the

years as per shown through the ratios.

2) Analyse and recommendation for assessing the financial performance of business

The financial performance of the company can be assessed through the use of ratios

which are identified through the information used from the income statement and balance sheet.

It is analysed that the company is increasing its sales over the period which is beneficial for the

7

reduced.

From the operating profit ratio which is identified by dividing the operating profit by

sales of that year. It is identified that the operating profit of the company is reduced over the

years which is not beneficial for the firms as it will lead to reduction the performance of

company. Furthermore, from the calculation it is identified about the gearing ratio which shows

relation between the debts and equity to identify the liquidity position of firm. Another ratio

which is related to interest coverage ratio shows the ability of the operating profit to cover the

interest expense of firm. It is shown that in the year 20X9, the operating profit can be used 12

times for covering the interest expense. Whereas in the year 20X0, the operating profit can be

used 8.4 times for covering interest expense and in the year 20X1 it can cover the interest

expense by 3.1 times.

From this, it can be interpreted that the interest coverage ratio is decreasing over the year

which is not beneficial for the company. From the calculation of Liquidity ratio which shows the

relation between the current assets and current liabilities and the ability of the current assets to

meet the current obligation of firm. The liquidity ratio in the year 20X9 was 2.29 which

increased to 2.38 in year 20X0 which shows the current assets are capable to meet the current

obligation of companies in these period. But in the year of 20X1 the liquidity ratio come to 0.91

which is less than the ideal ratio of 1:1 Which means the current assets of company cannot meet

the current obligation which is not good for the company.

Another ratio which is calculated is return on equity which shows the amount of return on

the capital invested in the firm which is reducing over the years and thus the returns for the

company on their equity are reducing. The return on capital employed ratio is calculated to

determine the amount of return on the capital employed in business which is also reducing over

the period. The change in the ratio is due to increase or decrease in the elements present in the

income or balance sheet statement which shows that the company is performing bad over the

years as per shown through the ratios.

2) Analyse and recommendation for assessing the financial performance of business

The financial performance of the company can be assessed through the use of ratios

which are identified through the information used from the income statement and balance sheet.

It is analysed that the company is increasing its sales over the period which is beneficial for the

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

firm but due to increase in expenses over the period as resulted into the decrease in profitability

of firms. So, it is recommended to company to reduce its expenses and cost to increase the

profitability of business which will help the firm in improving their financial performance.

It is analysed that the company’s current liabilities are more that its current assets due to

which the liquidity position of the company is not good which is reflected through the liquidity

ratio which shows that the company ability to meet the current obligation is reducing over the

years. The company’s financial performance is not good as per the ratios calculated as it shows

that the expenses for the company are increasing over the years which results into reducing in

their profitability. Also, the return on the equity is reducing over the years which shows the poor

financial performance of company. So, it is recommenced to board that the company must

reduce its expenses and should monitor the company's financial performances on the basis of

ratios to identify the changes which are required in the company to improve the financial

performance of firm.

CONCLUSION

From this assignment, it has concluded that business finance is required to perform the

various operations of organisation. It has provided information about the profit and cash flow

and the difference between them which shows that the profit is related to the revenue generated

by the business whereas cash flow involved the cash inflow and outflow for the period.

Moreover, the study has shown understanding about working capital and the effect on cash flow

due to changes in working capital that shows if the relation of assets and liabilities with cash

flow. This assignment has shown calculation of ratios on the basis of information provide in the

income statement and balance sheet.

8

of firms. So, it is recommended to company to reduce its expenses and cost to increase the

profitability of business which will help the firm in improving their financial performance.

It is analysed that the company’s current liabilities are more that its current assets due to

which the liquidity position of the company is not good which is reflected through the liquidity

ratio which shows that the company ability to meet the current obligation is reducing over the

years. The company’s financial performance is not good as per the ratios calculated as it shows

that the expenses for the company are increasing over the years which results into reducing in

their profitability. Also, the return on the equity is reducing over the years which shows the poor

financial performance of company. So, it is recommenced to board that the company must

reduce its expenses and should monitor the company's financial performances on the basis of

ratios to identify the changes which are required in the company to improve the financial

performance of firm.

CONCLUSION

From this assignment, it has concluded that business finance is required to perform the

various operations of organisation. It has provided information about the profit and cash flow

and the difference between them which shows that the profit is related to the revenue generated

by the business whereas cash flow involved the cash inflow and outflow for the period.

Moreover, the study has shown understanding about working capital and the effect on cash flow

due to changes in working capital that shows if the relation of assets and liabilities with cash

flow. This assignment has shown calculation of ratios on the basis of information provide in the

income statement and balance sheet.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and journals

Bendell, J. and Doyle, I., 2017. Healing capitalism: five years in the life of business, finance and

corporate responsibility. Routledge.

Burns, P. and Dewhurst, J. eds., 2016. Small business and entrepreneurship. Macmillan

International Higher Education.

Burns, P., 2016. Entrepreneurship and small business. Palgrave Macmillan Limited.

Canales, R., 2016. From ideals to institutions: Institutional entrepreneurship and the growth of

Mexican small business finance. Organization Science. 27(6). pp.1548-1573.

Finance, B., 2015. Business Finance.

Jordà, Ò., Schularick, M. and Taylor, A. M., 2016. The great mortgaging: housing finance,

crises and business cycles. Economic Policy. 31(85). pp.107-152.

Kraemer-Eis, H. and et.al., 2018. European Small Business Finance Outlook: December 2018.

(No. 2018/53). EIF Working Paper.

Scholes, M. S., 2015. Taxes and business strategy. Prentice Hall.

Ylhäinen, I., 2017. Life-cycle effects in small business finance. Journal of Banking &

Finance. 77. pp.176-196.

Online

Inventory. 2018. [Online]. Available through:

<https://www.accountingtools.com/articles/2017/5/13/inventory>

What's more important, cash flow or profits. 2018. [Online]. Available through:

<https://www.investopedia.com/ask/answers/111714/whats-more-important-cash-flow-

or-profits.asp>

9

Books and journals

Bendell, J. and Doyle, I., 2017. Healing capitalism: five years in the life of business, finance and

corporate responsibility. Routledge.

Burns, P. and Dewhurst, J. eds., 2016. Small business and entrepreneurship. Macmillan

International Higher Education.

Burns, P., 2016. Entrepreneurship and small business. Palgrave Macmillan Limited.

Canales, R., 2016. From ideals to institutions: Institutional entrepreneurship and the growth of

Mexican small business finance. Organization Science. 27(6). pp.1548-1573.

Finance, B., 2015. Business Finance.

Jordà, Ò., Schularick, M. and Taylor, A. M., 2016. The great mortgaging: housing finance,

crises and business cycles. Economic Policy. 31(85). pp.107-152.

Kraemer-Eis, H. and et.al., 2018. European Small Business Finance Outlook: December 2018.

(No. 2018/53). EIF Working Paper.

Scholes, M. S., 2015. Taxes and business strategy. Prentice Hall.

Ylhäinen, I., 2017. Life-cycle effects in small business finance. Journal of Banking &

Finance. 77. pp.176-196.

Online

Inventory. 2018. [Online]. Available through:

<https://www.accountingtools.com/articles/2017/5/13/inventory>

What's more important, cash flow or profits. 2018. [Online]. Available through:

<https://www.investopedia.com/ask/answers/111714/whats-more-important-cash-flow-

or-profits.asp>

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.