Business Finance: Investment Analysis, NPV, and Value Management

VerifiedAdded on 2023/01/19

|8

|1541

|48

Homework Assignment

AI Summary

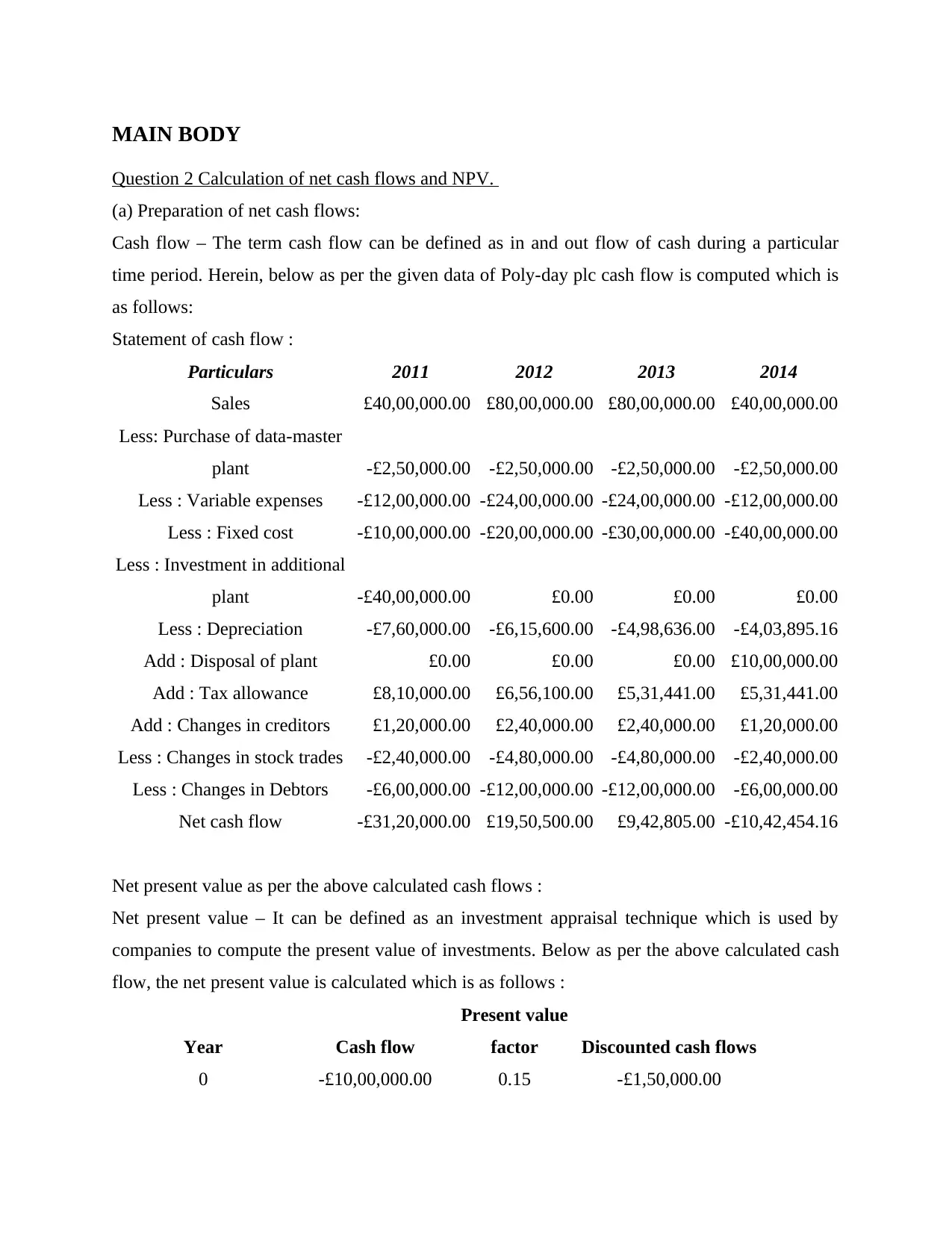

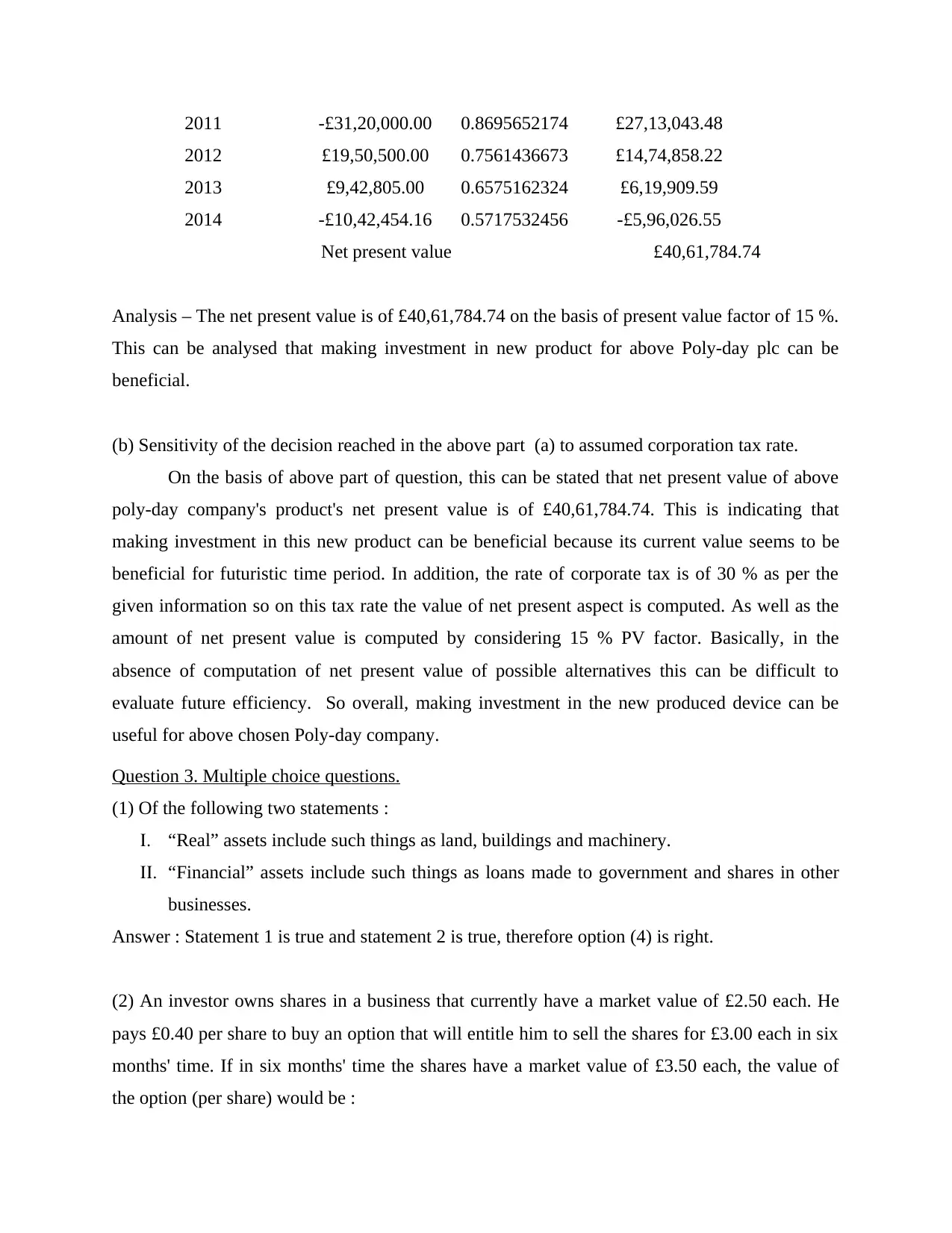

This homework assignment addresses key concepts in business finance, including the calculation of net cash flows and net present value (NPV) for an investment project. The student prepares a cash flow statement, calculates NPV using a 15% discount rate, and analyzes the sensitivity of the decision to the corporation tax rate. The assignment also includes multiple-choice questions covering topics like real and financial assets, option valuation, relevant data, agency costs, the separation theorem, P/E ratio, internal rate of return (IRR), and the IRR approach. Finally, the assignment explains the principles of value-based management in relation to shareholder value analysis (SVA) and economic value added (EVA), defining VBM and outlining its core principles: creating value, managing for value, and measuring value. References to relevant books and journals are also provided.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.