Business Finance - Sample Assignment PDF

VerifiedAdded on 2021/06/17

|11

|2267

|89

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: BUSINESS FINANCE

Business finance

Name of the student

Name of the university

Student ID

Author note

Business finance

Name of the student

Name of the university

Student ID

Author note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1BUSINESS FINANCE

Table of Contents

Introduction................................................................................................................................2

Answer 1 – Non-discounted payback period.............................................................................2

Answer 2 – profitability index...................................................................................................3

Answer 3 – internal rate of return..............................................................................................3

Answer 4 – net present value.....................................................................................................3

Answer 5 – Sensitivity analysis for price change......................................................................4

Answer 6 - Sensitivity analysis for price change.......................................................................6

Answer 7 – Conclusion..............................................................................................................8

Answer 8 – Recommendation....................................................................................................8

Reference....................................................................................................................................9

Table of Contents

Introduction................................................................................................................................2

Answer 1 – Non-discounted payback period.............................................................................2

Answer 2 – profitability index...................................................................................................3

Answer 3 – internal rate of return..............................................................................................3

Answer 4 – net present value.....................................................................................................3

Answer 5 – Sensitivity analysis for price change......................................................................4

Answer 6 - Sensitivity analysis for price change.......................................................................6

Answer 7 – Conclusion..............................................................................................................8

Answer 8 – Recommendation....................................................................................................8

Reference....................................................................................................................................9

2BUSINESS FINANCE

Introduction

Booli Enterprise is an Australian based company located in Victoria and the company

is engaged in the manufacturing of electronic goods. Major revenue generating product of the

company is SSHA (smart speaker and home assistant). At present the company is selling one

model for SSHA and the sales from the model are excellent. However, technological changes

and limited features of the existing model the company is planning to launch new SSHA with

advanced features. The main objective of this report is to analyse the investment and

profitability for the new SSHA model. Techniques that will be used for analysing the project

are net present value, profitability index, discounted payback period and internal rate of

return. The report will also perform the analysis the sensitivity of selling price and selling

quantity on NPV of the project (Brooks 2015).

Answer 1 – Non-discounted payback period

Payback period measures the time required for covering up the amount of initial

investment for any project and the point after which the project will start earning profit.

However, the payback period is just concerned about the time required for covering up the

initial investment amount and does not give any importance on the project’s capability to earn

profit beyond the payback period (Pasqual, Padilla and Jadotte 2013).

Non-discounted payback period for the project –

Year Cash inflow Cumulative cash flow

0 $ (47,025,000.00)

1 $ 9,158,160.00 $ 9,158,160.00

2 $ 34,307,097.60 $ 43,465,257.60

3 $ 25,842,344.45 $ 69,307,602.05

4 $ 16,194,120.97 $ 85,501,723.02

5 $ 23,547,757.33 $ 109,049,480.35

Introduction

Booli Enterprise is an Australian based company located in Victoria and the company

is engaged in the manufacturing of electronic goods. Major revenue generating product of the

company is SSHA (smart speaker and home assistant). At present the company is selling one

model for SSHA and the sales from the model are excellent. However, technological changes

and limited features of the existing model the company is planning to launch new SSHA with

advanced features. The main objective of this report is to analyse the investment and

profitability for the new SSHA model. Techniques that will be used for analysing the project

are net present value, profitability index, discounted payback period and internal rate of

return. The report will also perform the analysis the sensitivity of selling price and selling

quantity on NPV of the project (Brooks 2015).

Answer 1 – Non-discounted payback period

Payback period measures the time required for covering up the amount of initial

investment for any project and the point after which the project will start earning profit.

However, the payback period is just concerned about the time required for covering up the

initial investment amount and does not give any importance on the project’s capability to earn

profit beyond the payback period (Pasqual, Padilla and Jadotte 2013).

Non-discounted payback period for the project –

Year Cash inflow Cumulative cash flow

0 $ (47,025,000.00)

1 $ 9,158,160.00 $ 9,158,160.00

2 $ 34,307,097.60 $ 43,465,257.60

3 $ 25,842,344.45 $ 69,307,602.05

4 $ 16,194,120.97 $ 85,501,723.02

5 $ 23,547,757.33 $ 109,049,480.35

3BUSINESS FINANCE

Non-discounted payback period = 2 + (47,025,000 – 43.465,257.60) / (69,307,602.05 –

43,465,257.60) = 2.14 years.

Answer 2 – profitability index

PI is the investment analysis tool that states whether the project shall be rejected or

accepted. It takes into consideration the time value of money (Leung et al. 2014). The

formula used for computing the PI is as follows –

PI = PV of future cash flows / Initial investment

PI = $ 77,573,881.43 / 47,025,000 = 1.65

Therefore the profitability index of the project is 1.65.

Answer 3 – internal rate of return

IRR is used under capital budgeting for projecting the expected profitability of any

project (Gallo 2014). It is a discount rate at which the net present value of the future cash

flows is equal to zero. IRR of the project for producing new SSHA model is 19.77%.

Answer 4 – net present value

NPV is the expected changes in the wealth of the investor taking into consideration

the time value factor of money. It is the difference between the net cash inflows from the

project and the initial investment required for the project. This method of analysing the

project is considered as most appropriate as it considers the time value of money through

using the discount rate. The NPV of the project for producing New SSHA model is $

30,548,881.43 (Leyman and Vanhoucke 2016).

Non-discounted payback period = 2 + (47,025,000 – 43.465,257.60) / (69,307,602.05 –

43,465,257.60) = 2.14 years.

Answer 2 – profitability index

PI is the investment analysis tool that states whether the project shall be rejected or

accepted. It takes into consideration the time value of money (Leung et al. 2014). The

formula used for computing the PI is as follows –

PI = PV of future cash flows / Initial investment

PI = $ 77,573,881.43 / 47,025,000 = 1.65

Therefore the profitability index of the project is 1.65.

Answer 3 – internal rate of return

IRR is used under capital budgeting for projecting the expected profitability of any

project (Gallo 2014). It is a discount rate at which the net present value of the future cash

flows is equal to zero. IRR of the project for producing new SSHA model is 19.77%.

Answer 4 – net present value

NPV is the expected changes in the wealth of the investor taking into consideration

the time value factor of money. It is the difference between the net cash inflows from the

project and the initial investment required for the project. This method of analysing the

project is considered as most appropriate as it considers the time value of money through

using the discount rate. The NPV of the project for producing New SSHA model is $

30,548,881.43 (Leyman and Vanhoucke 2016).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4BUSINESS FINANCE

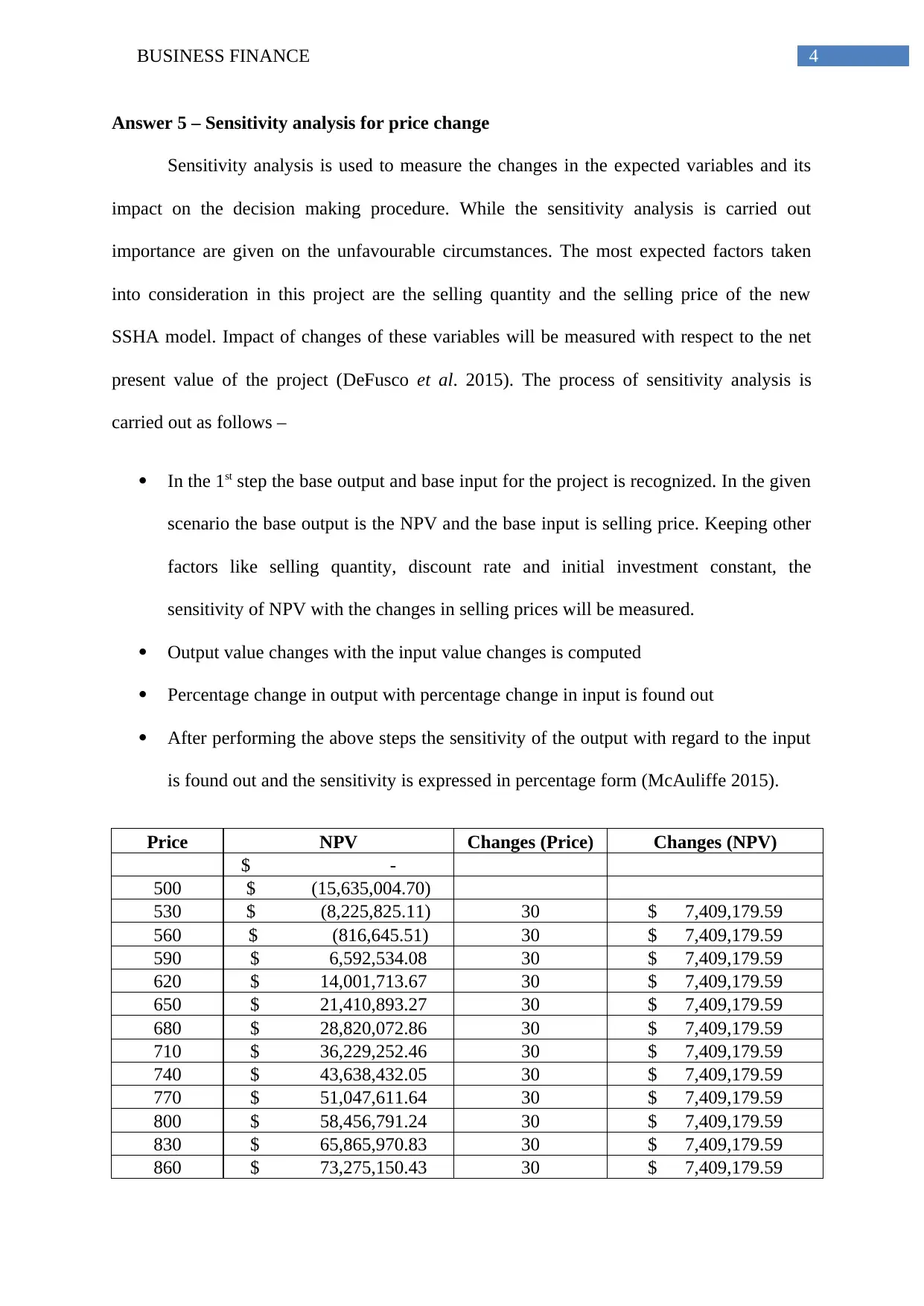

Answer 5 – Sensitivity analysis for price change

Sensitivity analysis is used to measure the changes in the expected variables and its

impact on the decision making procedure. While the sensitivity analysis is carried out

importance are given on the unfavourable circumstances. The most expected factors taken

into consideration in this project are the selling quantity and the selling price of the new

SSHA model. Impact of changes of these variables will be measured with respect to the net

present value of the project (DeFusco et al. 2015). The process of sensitivity analysis is

carried out as follows –

In the 1st step the base output and base input for the project is recognized. In the given

scenario the base output is the NPV and the base input is selling price. Keeping other

factors like selling quantity, discount rate and initial investment constant, the

sensitivity of NPV with the changes in selling prices will be measured.

Output value changes with the input value changes is computed

Percentage change in output with percentage change in input is found out

After performing the above steps the sensitivity of the output with regard to the input

is found out and the sensitivity is expressed in percentage form (McAuliffe 2015).

Price NPV Changes (Price) Changes (NPV)

$ -

500 $ (15,635,004.70)

530 $ (8,225,825.11) 30 $ 7,409,179.59

560 $ (816,645.51) 30 $ 7,409,179.59

590 $ 6,592,534.08 30 $ 7,409,179.59

620 $ 14,001,713.67 30 $ 7,409,179.59

650 $ 21,410,893.27 30 $ 7,409,179.59

680 $ 28,820,072.86 30 $ 7,409,179.59

710 $ 36,229,252.46 30 $ 7,409,179.59

740 $ 43,638,432.05 30 $ 7,409,179.59

770 $ 51,047,611.64 30 $ 7,409,179.59

800 $ 58,456,791.24 30 $ 7,409,179.59

830 $ 65,865,970.83 30 $ 7,409,179.59

860 $ 73,275,150.43 30 $ 7,409,179.59

Answer 5 – Sensitivity analysis for price change

Sensitivity analysis is used to measure the changes in the expected variables and its

impact on the decision making procedure. While the sensitivity analysis is carried out

importance are given on the unfavourable circumstances. The most expected factors taken

into consideration in this project are the selling quantity and the selling price of the new

SSHA model. Impact of changes of these variables will be measured with respect to the net

present value of the project (DeFusco et al. 2015). The process of sensitivity analysis is

carried out as follows –

In the 1st step the base output and base input for the project is recognized. In the given

scenario the base output is the NPV and the base input is selling price. Keeping other

factors like selling quantity, discount rate and initial investment constant, the

sensitivity of NPV with the changes in selling prices will be measured.

Output value changes with the input value changes is computed

Percentage change in output with percentage change in input is found out

After performing the above steps the sensitivity of the output with regard to the input

is found out and the sensitivity is expressed in percentage form (McAuliffe 2015).

Price NPV Changes (Price) Changes (NPV)

$ -

500 $ (15,635,004.70)

530 $ (8,225,825.11) 30 $ 7,409,179.59

560 $ (816,645.51) 30 $ 7,409,179.59

590 $ 6,592,534.08 30 $ 7,409,179.59

620 $ 14,001,713.67 30 $ 7,409,179.59

650 $ 21,410,893.27 30 $ 7,409,179.59

680 $ 28,820,072.86 30 $ 7,409,179.59

710 $ 36,229,252.46 30 $ 7,409,179.59

740 $ 43,638,432.05 30 $ 7,409,179.59

770 $ 51,047,611.64 30 $ 7,409,179.59

800 $ 58,456,791.24 30 $ 7,409,179.59

830 $ 65,865,970.83 30 $ 7,409,179.59

860 $ 73,275,150.43 30 $ 7,409,179.59

5BUSINESS FINANCE

890 $ 80,684,330.02 30 $ 7,409,179.59

920 $ 88,093,509.61 30 $ 7,409,179.59

950 $ 95,502,689.21 30 $ 7,409,179.59

980 $ 102,911,868.80 30 $ 7,409,179.59

1010 $ 110,321,048.40 30 $ 7,409,179.59

1040 $ 117,730,227.99 30 $ 7,409,179.59

1070 $ 125,139,407.58 30 $ 7,409,179.59

1100 $ 132,548,587.18 30 $ 7,409,179.59

1130 $ 139,957,766.77 30 $ 7,409,179.59

1160 $ 147,366,946.37 30 $ 7,409,179.59

1190 $ 154,776,125.96 30 $ 7,409,179.59

1220 $ 162,185,305.55 30 $ 7,409,179.59

1250 $ 169,594,485.15 30 $ 7,409,179.59

1280 $ 177,003,664.74 30 $ 7,409,179.59

1310 $ 184,412,844.33 30 $ 7,409,179.59

400 500 600 700 800 900 1000 1100 1200 1300 1400

$(50,000,000.00)

$-

$50,000,000.00

$100,000,000.00

$150,000,000.00

$200,000,000.00

Selling price

N

P

V

Changes in price 4%

Changes in NPV 24%

Sensitivity

555.41

%

It is observed from the above presented table and graph that the output that is the NPV

changes positively with the changes in the input that is the selling prices. For the changes in

price ranged from $ 500 to $ 1310 the NPV ranged from -$15,635,004.70 to $

184,412,844.33. For every $ 30 increase in the input there is a change of $ 7,409,179.59 in

890 $ 80,684,330.02 30 $ 7,409,179.59

920 $ 88,093,509.61 30 $ 7,409,179.59

950 $ 95,502,689.21 30 $ 7,409,179.59

980 $ 102,911,868.80 30 $ 7,409,179.59

1010 $ 110,321,048.40 30 $ 7,409,179.59

1040 $ 117,730,227.99 30 $ 7,409,179.59

1070 $ 125,139,407.58 30 $ 7,409,179.59

1100 $ 132,548,587.18 30 $ 7,409,179.59

1130 $ 139,957,766.77 30 $ 7,409,179.59

1160 $ 147,366,946.37 30 $ 7,409,179.59

1190 $ 154,776,125.96 30 $ 7,409,179.59

1220 $ 162,185,305.55 30 $ 7,409,179.59

1250 $ 169,594,485.15 30 $ 7,409,179.59

1280 $ 177,003,664.74 30 $ 7,409,179.59

1310 $ 184,412,844.33 30 $ 7,409,179.59

400 500 600 700 800 900 1000 1100 1200 1300 1400

$(50,000,000.00)

$-

$50,000,000.00

$100,000,000.00

$150,000,000.00

$200,000,000.00

Selling price

N

P

V

Changes in price 4%

Changes in NPV 24%

Sensitivity

555.41

%

It is observed from the above presented table and graph that the output that is the NPV

changes positively with the changes in the input that is the selling prices. For the changes in

price ranged from $ 500 to $ 1310 the NPV ranged from -$15,635,004.70 to $

184,412,844.33. For every $ 30 increase in the input there is a change of $ 7,409,179.59 in

6BUSINESS FINANCE

the output. In other words, for every 4% changes in the selling price there is a 24% changes

in the NPV. The sensitivity is thus comes as 555.41%. Therefore, the NPV is highly sensitive

to the changes in the NPV (Baucells and Borgonovo 2013).

Answer 6 - Sensitivity analysis for price change

Various factors that lead to performing the sensitivity analysis are as follows –

Most likely variables that have maximum impact on the decision making procedures

can be recognized through the sensitivity analysis

It assists in taking the corrective actions or appropriate decisions after recognising the

impact of changes in the variables

While the sensitivity analysis is carried out with regard to the changes in the selling

quantity of the product and its impact on the project’s NPV, the output here is the NPV and

the input here is the selling quantity (Iooss and Lemaître 2015). In this part, the sensitivity

analysis will be carried out for changes in the selling quantity while keeping the other factors

like selling price, discount rate and initial investment constant.

Sales volume NPV Changes (Quantity) Changes (NPV)

$ -

25000 $ 22,354,148.82

50000 $ 25,411,884.87 25000 3,057,736.05

75000 $ 28,469,620.92 25000 3,057,736.05

100000 $ 31,527,356.97 25000 3,057,736.05

125000 $ 34,585,093.02 25000 3,057,736.05

150000 $ 37,642,829.07 25000 3,057,736.05

175000 $ 40,700,565.12 25000 3,057,736.05

200000 $ 43,758,301.17 25000 3,057,736.05

225000 $ 46,816,037.22 25000 3,057,736.05

250000 $ 49,873,773.27 25000 3,057,736.05

275000 $ 52,931,509.32 25000 3,057,736.05

300000 $ 55,989,245.37 25000 3,057,736.05

325000 $ 59,046,981.42 25000 3,057,736.05

350000 $ 62,104,717.47 25000 3,057,736.05

the output. In other words, for every 4% changes in the selling price there is a 24% changes

in the NPV. The sensitivity is thus comes as 555.41%. Therefore, the NPV is highly sensitive

to the changes in the NPV (Baucells and Borgonovo 2013).

Answer 6 - Sensitivity analysis for price change

Various factors that lead to performing the sensitivity analysis are as follows –

Most likely variables that have maximum impact on the decision making procedures

can be recognized through the sensitivity analysis

It assists in taking the corrective actions or appropriate decisions after recognising the

impact of changes in the variables

While the sensitivity analysis is carried out with regard to the changes in the selling

quantity of the product and its impact on the project’s NPV, the output here is the NPV and

the input here is the selling quantity (Iooss and Lemaître 2015). In this part, the sensitivity

analysis will be carried out for changes in the selling quantity while keeping the other factors

like selling price, discount rate and initial investment constant.

Sales volume NPV Changes (Quantity) Changes (NPV)

$ -

25000 $ 22,354,148.82

50000 $ 25,411,884.87 25000 3,057,736.05

75000 $ 28,469,620.92 25000 3,057,736.05

100000 $ 31,527,356.97 25000 3,057,736.05

125000 $ 34,585,093.02 25000 3,057,736.05

150000 $ 37,642,829.07 25000 3,057,736.05

175000 $ 40,700,565.12 25000 3,057,736.05

200000 $ 43,758,301.17 25000 3,057,736.05

225000 $ 46,816,037.22 25000 3,057,736.05

250000 $ 49,873,773.27 25000 3,057,736.05

275000 $ 52,931,509.32 25000 3,057,736.05

300000 $ 55,989,245.37 25000 3,057,736.05

325000 $ 59,046,981.42 25000 3,057,736.05

350000 $ 62,104,717.47 25000 3,057,736.05

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7BUSINESS FINANCE

0 50000 100000 150000 200000 250000 300000 350000 400000

$-

$10,000,000.00

$20,000,000.00

$30,000,000.00

$40,000,000.00

$50,000,000.00

$60,000,000.00

$70,000,000.00

Sales volume

N

P

V

Changes in quantity 27%

Changes in NPV 10%

Sensitivity 36.83%

It is observed from the above presented table and graph that the output that is the

NPV changes positively with the changes in the input that is the selling quantity. For the

changes in selling quantity ranged from 25000 to 350,000 the NPV ranged from

$22,354,148,82 to $ 62,104,717.47. For every 25000 increase in the input there is a change of

$ 30,57,736.05 in the output. In other words, for every 27% changes in the selling price there

is a 10% changes in the NPV. The sensitivity is thus comes as 36.83%. Therefore, the NPV is

moderately sensitive to the changes in the NPV (Butler et al. 2014).

Sensitivity analysis helps in taking appropriate decisions regarding the input and

output variables as it gives the insights regarding how the changes in input has it impact on

the output. Based on the result the analysts and the management can take appropriate

decisions (Baucells and Borgonovo 2013). However, sometimes the sensitivity analysis

seems ambiguous as the pessimistic level and optimistic level is depended on the user’s own

0 50000 100000 150000 200000 250000 300000 350000 400000

$-

$10,000,000.00

$20,000,000.00

$30,000,000.00

$40,000,000.00

$50,000,000.00

$60,000,000.00

$70,000,000.00

Sales volume

N

P

V

Changes in quantity 27%

Changes in NPV 10%

Sensitivity 36.83%

It is observed from the above presented table and graph that the output that is the

NPV changes positively with the changes in the input that is the selling quantity. For the

changes in selling quantity ranged from 25000 to 350,000 the NPV ranged from

$22,354,148,82 to $ 62,104,717.47. For every 25000 increase in the input there is a change of

$ 30,57,736.05 in the output. In other words, for every 27% changes in the selling price there

is a 10% changes in the NPV. The sensitivity is thus comes as 36.83%. Therefore, the NPV is

moderately sensitive to the changes in the NPV (Butler et al. 2014).

Sensitivity analysis helps in taking appropriate decisions regarding the input and

output variables as it gives the insights regarding how the changes in input has it impact on

the output. Based on the result the analysts and the management can take appropriate

decisions (Baucells and Borgonovo 2013). However, sometimes the sensitivity analysis

seems ambiguous as the pessimistic level and optimistic level is depended on the user’s own

8BUSINESS FINANCE

approach. Further, it changes only one variable at a time keeping other variables constant.

However, in practical situation it may not be possible always (Levy 2015).

Answer 7 – Conclusion

It can be concluded from the above analysis that the New SSHA model shall be

produced by Booli Enterprise. The reason behind the acceptability of the project is that the

NPV of the project is $ 30,548,881.41, payback period is less than the projects useful life that

is 2.14 years, IRR of the project is higher than the required rate of return that is 19.77%.

Answer 8 – Recommendation

If it is found that producing of New model for SSHA will be made in exchange of loss

from other products, while calculating the NPV for new SSHA the amount of loss shall be

included in the initial investment. If after including the loss the new SSHA project’s NPV

comes positive then the project shall be accepted.

approach. Further, it changes only one variable at a time keeping other variables constant.

However, in practical situation it may not be possible always (Levy 2015).

Answer 7 – Conclusion

It can be concluded from the above analysis that the New SSHA model shall be

produced by Booli Enterprise. The reason behind the acceptability of the project is that the

NPV of the project is $ 30,548,881.41, payback period is less than the projects useful life that

is 2.14 years, IRR of the project is higher than the required rate of return that is 19.77%.

Answer 8 – Recommendation

If it is found that producing of New model for SSHA will be made in exchange of loss

from other products, while calculating the NPV for new SSHA the amount of loss shall be

included in the initial investment. If after including the loss the new SSHA project’s NPV

comes positive then the project shall be accepted.

9BUSINESS FINANCE

Reference

Baucells, M. and Borgonovo, E., 2013. Invariant probabilistic sensitivity

analysis. Management Science, 59(11), pp.2536-2549.

Brooks, R., 2015. Financial management: core concepts. Pearson.

Butler, M.P., Reed, P.M., Fisher-Vanden, K., Keller, K. and Wagener, T., 2014. Identifying

parametric controls and dependencies in integrated assessment models using global

sensitivity analysis. Environmental modelling & software, 59, pp.10-29.

DeFusco, R.A., McLeavey, D.W., Pinto, J.E., Anson, M.J. and Runkle, D.E.,

2015. Quantitative investment analysis. John Wiley & Sons.

Gorshkov, A.S., Rymkevich, P.P., Nemova, D.V. and Vatin, N.I., 2014. Method of

calculating the payback period of investment for renovation of building facades. Stroitel'stvo

Unikal'nyh Zdanij i Sooruzenij, (2), p.82.

Harrison, F. and Lock, D., 2017. Advanced project management: a structured approach.

Routledge.

Iooss, B. and Lemaître, P., 2015. A review on global sensitivity analysis methods.

In Uncertainty management in simulation-optimization of complex systems (pp. 101-122).

Springer, Boston, MA.

Leung, B., Springborn, M.R., Turner, J.A. and Brockerhoff, E.G., 2014. Pathway‐level risk

analysis: the net present value of an invasive species policy in the US. Frontiers in Ecology

and the Environment, 12(5), pp.273-279.

Reference

Baucells, M. and Borgonovo, E., 2013. Invariant probabilistic sensitivity

analysis. Management Science, 59(11), pp.2536-2549.

Brooks, R., 2015. Financial management: core concepts. Pearson.

Butler, M.P., Reed, P.M., Fisher-Vanden, K., Keller, K. and Wagener, T., 2014. Identifying

parametric controls and dependencies in integrated assessment models using global

sensitivity analysis. Environmental modelling & software, 59, pp.10-29.

DeFusco, R.A., McLeavey, D.W., Pinto, J.E., Anson, M.J. and Runkle, D.E.,

2015. Quantitative investment analysis. John Wiley & Sons.

Gorshkov, A.S., Rymkevich, P.P., Nemova, D.V. and Vatin, N.I., 2014. Method of

calculating the payback period of investment for renovation of building facades. Stroitel'stvo

Unikal'nyh Zdanij i Sooruzenij, (2), p.82.

Harrison, F. and Lock, D., 2017. Advanced project management: a structured approach.

Routledge.

Iooss, B. and Lemaître, P., 2015. A review on global sensitivity analysis methods.

In Uncertainty management in simulation-optimization of complex systems (pp. 101-122).

Springer, Boston, MA.

Leung, B., Springborn, M.R., Turner, J.A. and Brockerhoff, E.G., 2014. Pathway‐level risk

analysis: the net present value of an invasive species policy in the US. Frontiers in Ecology

and the Environment, 12(5), pp.273-279.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10BUSINESS FINANCE

Leyman, P. and Vanhoucke, M., 2016. Payment models and net present value optimization

for resource-constrained project scheduling. Computers & Industrial Engineering, 91,

pp.139-153.

Pasqual, J., Padilla, E. and Jadotte, E., 2013. Equivalence of different profitability criteria

with the net present value. International Journal of Production Economics, 142(1), pp.205-

210.

Ross, S.A., Bianchi, R., Christensen, M., Drew, M., Westerfield, R. and Jordan, B.D.,

2014. Fundamentals of Corporate Finance: Introduction to corporate finance Chapter: 2

Financial statements, taxes and cash flow PART 2 Chapter: 3 Working with financial

statements Chapter: 4 Long-term financial planning and corporate growth PART 3 Chapter: 5

First principles of valuation: TVM Chapter: 6 Valuing shares and bonds PART 4 Chapter: 7

Net present value and other investment criteria Chapter: 8 Making capital investment

decisions Chapter: 9 Project analysis and evaluation PART 5 Chapter: 10 Lessons ....

McGraw-Hill Education (Australia).

Song, Z., Li, Z., Wei, M., Lai, F. and Bai, B., 2014. Sensitivity analysis of water-alternating-

CO2 flooding for enhanced oil recovery in high water cut oil reservoirs. Computers &

Fluids, 99, pp.93-103.

Leyman, P. and Vanhoucke, M., 2016. Payment models and net present value optimization

for resource-constrained project scheduling. Computers & Industrial Engineering, 91,

pp.139-153.

Pasqual, J., Padilla, E. and Jadotte, E., 2013. Equivalence of different profitability criteria

with the net present value. International Journal of Production Economics, 142(1), pp.205-

210.

Ross, S.A., Bianchi, R., Christensen, M., Drew, M., Westerfield, R. and Jordan, B.D.,

2014. Fundamentals of Corporate Finance: Introduction to corporate finance Chapter: 2

Financial statements, taxes and cash flow PART 2 Chapter: 3 Working with financial

statements Chapter: 4 Long-term financial planning and corporate growth PART 3 Chapter: 5

First principles of valuation: TVM Chapter: 6 Valuing shares and bonds PART 4 Chapter: 7

Net present value and other investment criteria Chapter: 8 Making capital investment

decisions Chapter: 9 Project analysis and evaluation PART 5 Chapter: 10 Lessons ....

McGraw-Hill Education (Australia).

Song, Z., Li, Z., Wei, M., Lai, F. and Bai, B., 2014. Sensitivity analysis of water-alternating-

CO2 flooding for enhanced oil recovery in high water cut oil reservoirs. Computers &

Fluids, 99, pp.93-103.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.