Business Finance Project: Analyzing Financial Information and Ratios

VerifiedAdded on 2021/02/20

|10

|2231

|37

Report

AI Summary

This report provides an in-depth analysis of financial information, focusing on key financial ratios such as liquidity, profitability, and turnover ratios. It explores the legal requirements for financial information from various business organizations in the UK, including sole traders, partnerships, and ...

Business Finance project 4

Understanding Financial

Information

Understanding Financial

Information

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION................................................................................................................................3

LO 1......................................................................................................................................................3

1.1 Key Financial Ratios..................................................................................................................3

LO 2......................................................................................................................................................6

2.1 Financial Information legally required from major types of Business Organisation in the UK

are.....................................................................................................................................................6

LO 3......................................................................................................................................................6

3.1 Management needs for Financial Information...............................................................................6

LO 4......................................................................................................................................................7

4.1 Other users of Financial Information.........................................................................................7

LO 5......................................................................................................................................................8

5.1 Purpose of main Financial Statements in Business...................................................................8

CONCLUSION....................................................................................................................................8

REFERENCES.....................................................................................................................................9

INTRODUCTION................................................................................................................................3

LO 1......................................................................................................................................................3

1.1 Key Financial Ratios..................................................................................................................3

LO 2......................................................................................................................................................6

2.1 Financial Information legally required from major types of Business Organisation in the UK

are.....................................................................................................................................................6

LO 3......................................................................................................................................................6

3.1 Management needs for Financial Information...............................................................................6

LO 4......................................................................................................................................................7

4.1 Other users of Financial Information.........................................................................................7

LO 5......................................................................................................................................................8

5.1 Purpose of main Financial Statements in Business...................................................................8

CONCLUSION....................................................................................................................................8

REFERENCES.....................................................................................................................................9

INTRODUCTION

Business Finance refers to the financing in the company either by investing retained

earnings or borrowing debt from outside in order to finance the company. It includes the various

key financial ratios which depicts the financial position of the company. It also includes the main

purpose of the financial information and how the other uses this financial information in taking

decisions for the organisation. It includes the various types of business forms and what are the legal

requirements to be completed to run those business. It also covers that how management uses this

financial information in taking the major decisions.

LO 1

1.1 Key Financial Ratios

Financial Ratios refers to the analysis and interpretation of the financial statements using various

ratios. The main purposes of ratio analysis are-

The main purpose of financial ratios is to check the performance of the company based

on the performance of the previous year.

To identify the performance of the company over the years and based on those results

company can take certain decisions.

The other purpose of financial ratios is to understand the liquidity position, profitability

position of the company.

Limitations of financial ratios are-

The main limitation of the financial statements is that assets of the company are recorded at

historical values. They do not reflect at current information of the company.

Every business follows different accounting standards in their company. This makes the two

company incomparable.

Fixed assets in the balance sheet are shown at cost only and there are no changes in the price

level which makes comparison difficult.

Liquidity Ratios

Particulars 20xx

Current Assets 525

Current Liabilities 255

Business Finance refers to the financing in the company either by investing retained

earnings or borrowing debt from outside in order to finance the company. It includes the various

key financial ratios which depicts the financial position of the company. It also includes the main

purpose of the financial information and how the other uses this financial information in taking

decisions for the organisation. It includes the various types of business forms and what are the legal

requirements to be completed to run those business. It also covers that how management uses this

financial information in taking the major decisions.

LO 1

1.1 Key Financial Ratios

Financial Ratios refers to the analysis and interpretation of the financial statements using various

ratios. The main purposes of ratio analysis are-

The main purpose of financial ratios is to check the performance of the company based

on the performance of the previous year.

To identify the performance of the company over the years and based on those results

company can take certain decisions.

The other purpose of financial ratios is to understand the liquidity position, profitability

position of the company.

Limitations of financial ratios are-

The main limitation of the financial statements is that assets of the company are recorded at

historical values. They do not reflect at current information of the company.

Every business follows different accounting standards in their company. This makes the two

company incomparable.

Fixed assets in the balance sheet are shown at cost only and there are no changes in the price

level which makes comparison difficult.

Liquidity Ratios

Particulars 20xx

Current Assets 525

Current Liabilities 255

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

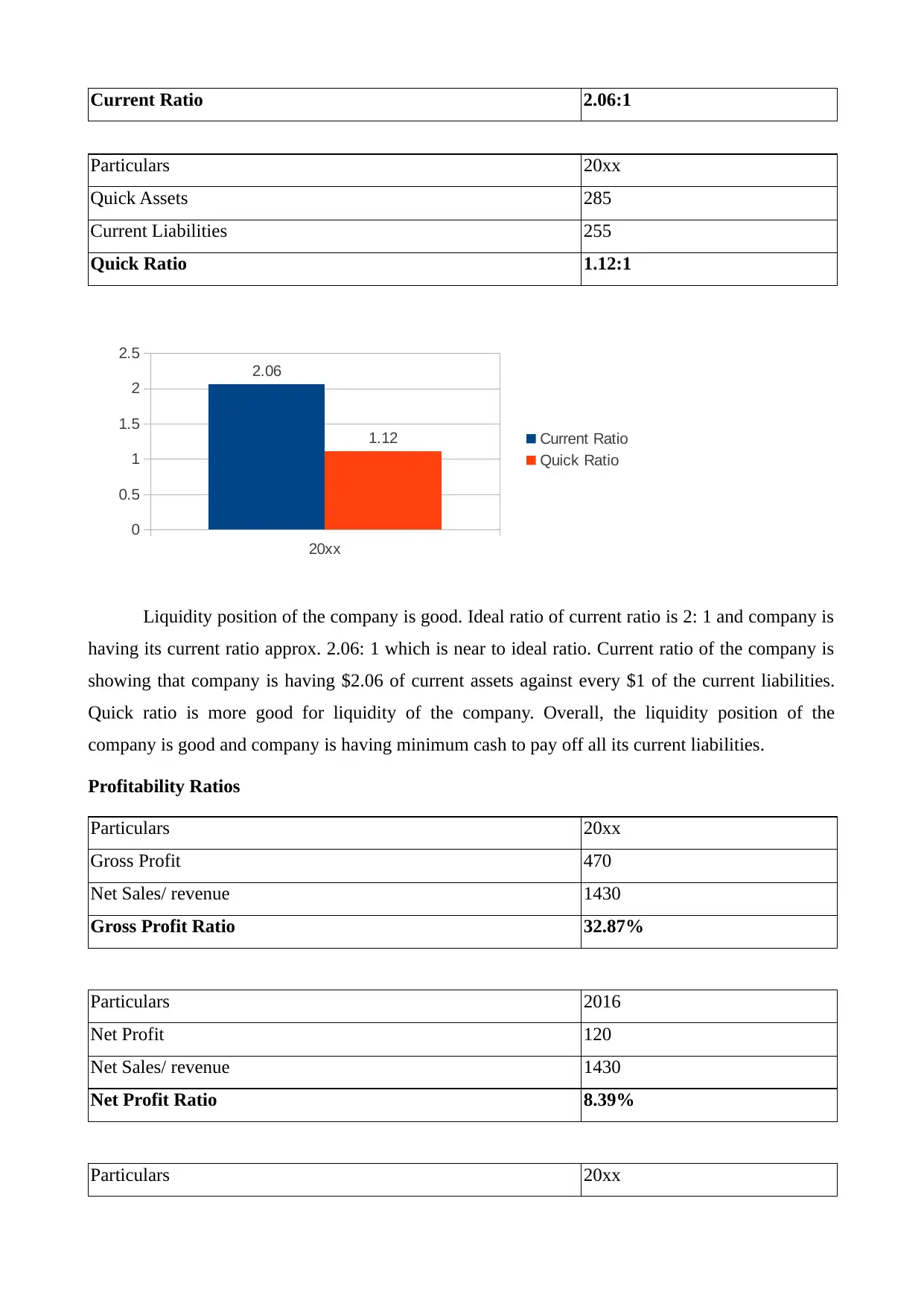

Current Ratio 2.06:1

Particulars 20xx

Quick Assets 285

Current Liabilities 255

Quick Ratio 1.12:1

20xx

0

0.5

1

1.5

2

2.5

2.06

1.12 Current Ratio

Quick Ratio

Liquidity position of the company is good. Ideal ratio of current ratio is 2: 1 and company is

having its current ratio approx. 2.06: 1 which is near to ideal ratio. Current ratio of the company is

showing that company is having $2.06 of current assets against every $1 of the current liabilities.

Quick ratio is more good for liquidity of the company. Overall, the liquidity position of the

company is good and company is having minimum cash to pay off all its current liabilities.

Profitability Ratios

Particulars 20xx

Gross Profit 470

Net Sales/ revenue 1430

Gross Profit Ratio 32.87%

Particulars 2016

Net Profit 120

Net Sales/ revenue 1430

Net Profit Ratio 8.39%

Particulars 20xx

Particulars 20xx

Quick Assets 285

Current Liabilities 255

Quick Ratio 1.12:1

20xx

0

0.5

1

1.5

2

2.5

2.06

1.12 Current Ratio

Quick Ratio

Liquidity position of the company is good. Ideal ratio of current ratio is 2: 1 and company is

having its current ratio approx. 2.06: 1 which is near to ideal ratio. Current ratio of the company is

showing that company is having $2.06 of current assets against every $1 of the current liabilities.

Quick ratio is more good for liquidity of the company. Overall, the liquidity position of the

company is good and company is having minimum cash to pay off all its current liabilities.

Profitability Ratios

Particulars 20xx

Gross Profit 470

Net Sales/ revenue 1430

Gross Profit Ratio 32.87%

Particulars 2016

Net Profit 120

Net Sales/ revenue 1430

Net Profit Ratio 8.39%

Particulars 20xx

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Net Profit 120

Total Assets 1805

Return on Assets 6.65%

Particulars 20xx

Net Profit 120

Total Equity 1300

Return on Equity 9.23%

Particulars 2016

Net Profit 120

Capital Employed 1550

Return on Capital Employed 7.74%

20xx

0

0.05

0.1

0.15

0.2

0.25

0.3

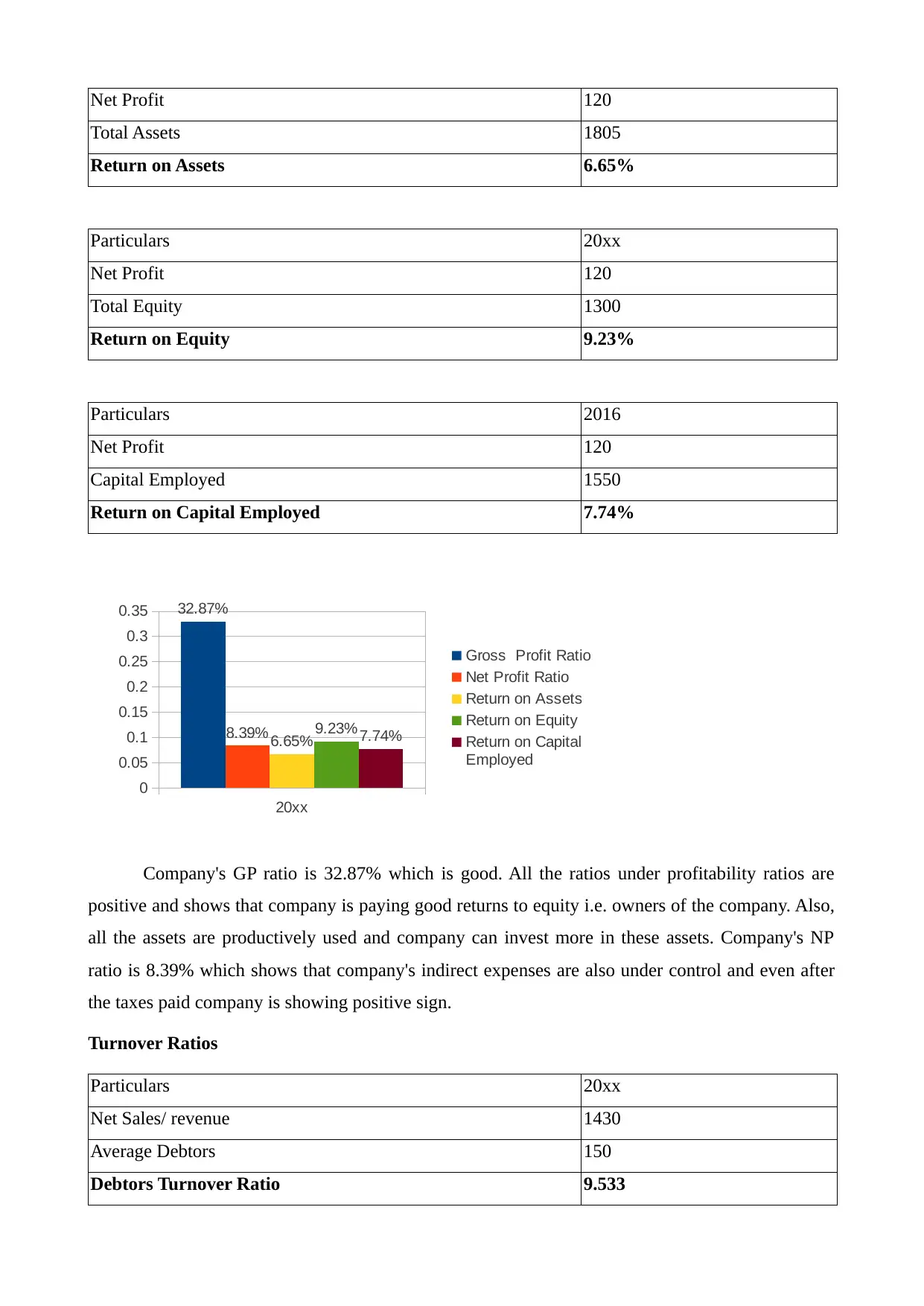

0.35 32.87%

8.39% 6.65% 9.23% 7.74%

Gross Profit Ratio

Net Profit Ratio

Return on Assets

Return on Equity

Return on Capital

Employed

Company's GP ratio is 32.87% which is good. All the ratios under profitability ratios are

positive and shows that company is paying good returns to equity i.e. owners of the company. Also,

all the assets are productively used and company can invest more in these assets. Company's NP

ratio is 8.39% which shows that company's indirect expenses are also under control and even after

the taxes paid company is showing positive sign.

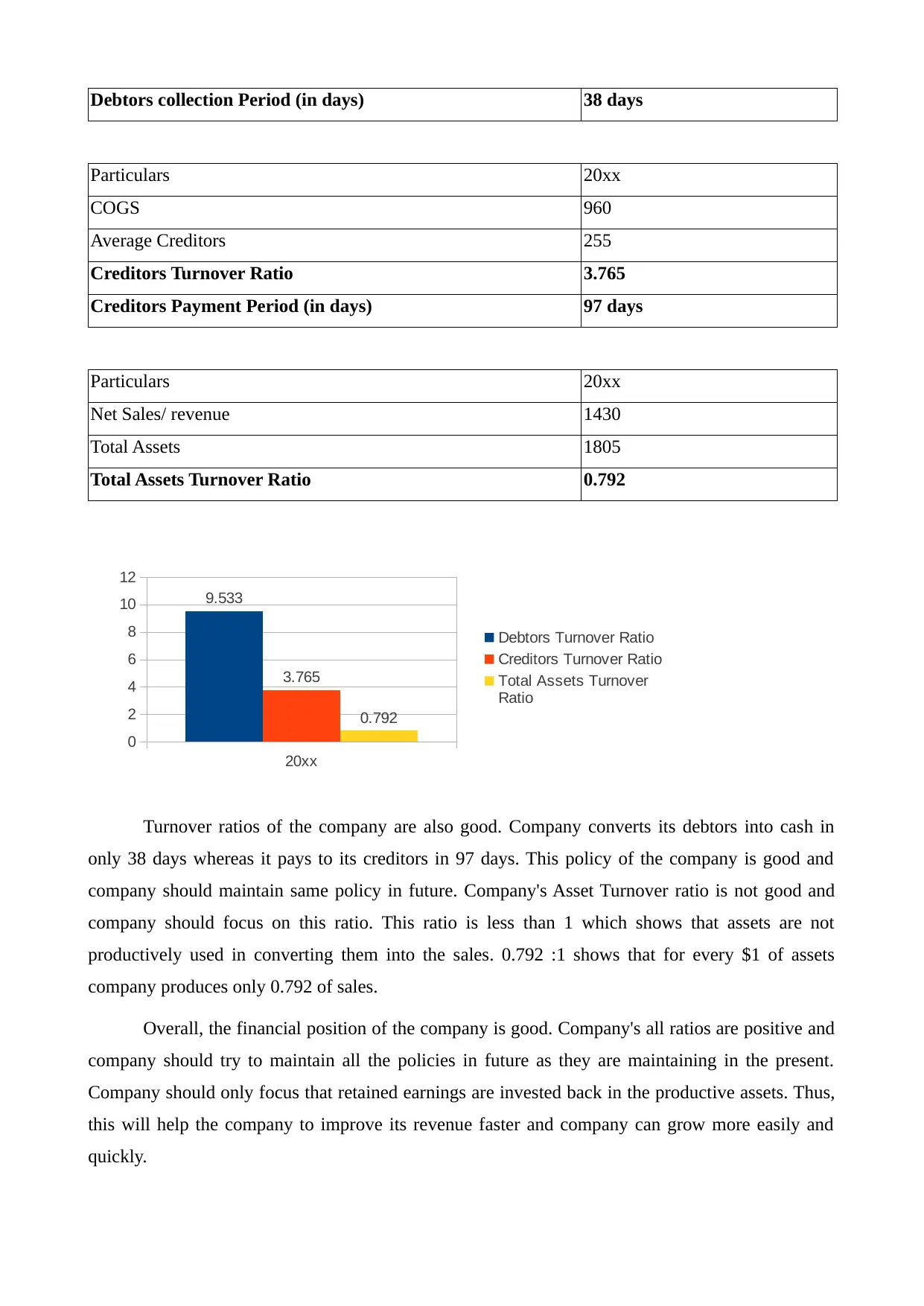

Turnover Ratios

Particulars 20xx

Net Sales/ revenue 1430

Average Debtors 150

Debtors Turnover Ratio 9.533

Total Assets 1805

Return on Assets 6.65%

Particulars 20xx

Net Profit 120

Total Equity 1300

Return on Equity 9.23%

Particulars 2016

Net Profit 120

Capital Employed 1550

Return on Capital Employed 7.74%

20xx

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35 32.87%

8.39% 6.65% 9.23% 7.74%

Gross Profit Ratio

Net Profit Ratio

Return on Assets

Return on Equity

Return on Capital

Employed

Company's GP ratio is 32.87% which is good. All the ratios under profitability ratios are

positive and shows that company is paying good returns to equity i.e. owners of the company. Also,

all the assets are productively used and company can invest more in these assets. Company's NP

ratio is 8.39% which shows that company's indirect expenses are also under control and even after

the taxes paid company is showing positive sign.

Turnover Ratios

Particulars 20xx

Net Sales/ revenue 1430

Average Debtors 150

Debtors Turnover Ratio 9.533

Debtors collection Period (in days) 38 days

Particulars 20xx

COGS 960

Average Creditors 255

Creditors Turnover Ratio 3.765

Creditors Payment Period (in days) 97 days

Particulars 20xx

Net Sales/ revenue 1430

Total Assets 1805

Total Assets Turnover Ratio 0.792

20xx

0

2

4

6

8

10

12

9.533

3.765

0.792

Debtors Turnover Ratio

Creditors Turnover Ratio

Total Assets Turnover

Ratio

Turnover ratios of the company are also good. Company converts its debtors into cash in

only 38 days whereas it pays to its creditors in 97 days. This policy of the company is good and

company should maintain same policy in future. Company's Asset Turnover ratio is not good and

company should focus on this ratio. This ratio is less than 1 which shows that assets are not

productively used in converting them into the sales. 0.792 :1 shows that for every $1 of assets

company produces only 0.792 of sales.

Overall, the financial position of the company is good. Company's all ratios are positive and

company should try to maintain all the policies in future as they are maintaining in the present.

Company should only focus that retained earnings are invested back in the productive assets. Thus,

this will help the company to improve its revenue faster and company can grow more easily and

quickly.

Particulars 20xx

COGS 960

Average Creditors 255

Creditors Turnover Ratio 3.765

Creditors Payment Period (in days) 97 days

Particulars 20xx

Net Sales/ revenue 1430

Total Assets 1805

Total Assets Turnover Ratio 0.792

20xx

0

2

4

6

8

10

12

9.533

3.765

0.792

Debtors Turnover Ratio

Creditors Turnover Ratio

Total Assets Turnover

Ratio

Turnover ratios of the company are also good. Company converts its debtors into cash in

only 38 days whereas it pays to its creditors in 97 days. This policy of the company is good and

company should maintain same policy in future. Company's Asset Turnover ratio is not good and

company should focus on this ratio. This ratio is less than 1 which shows that assets are not

productively used in converting them into the sales. 0.792 :1 shows that for every $1 of assets

company produces only 0.792 of sales.

Overall, the financial position of the company is good. Company's all ratios are positive and

company should try to maintain all the policies in future as they are maintaining in the present.

Company should only focus that retained earnings are invested back in the productive assets. Thus,

this will help the company to improve its revenue faster and company can grow more easily and

quickly.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

LO 2

2.1 Financial Information legally required from major types of Business Organisation in the UK are

There are various types of Business Organisation in the UK are -

Sole Traders-

In this type of business only an individual requires to run the business. Sole trader prepares

the balance sheet at a specific point of time. The statement of financial performance also known as

income statement or trading account are also prepared in order to know the profitability position of

the business. To determine the link between the balance sheet and income statement the statement

of changes in Owner's equity is also prepared. This statement shows the increase or decrease of

owner's equity in the business.

Partnership-

In this there is minimum requirement of 2 persons to start the business. There can unlimited

number of partners in the business (Mason 2015). Partnership firms are required to prepare the

statement of partner's equity in order to know the increase or decrease of equity by the partners.

Firm has to also prepare the income statements, balance sheet and cash flow statement.

Private and Public Companies-

In this type of business, the company is owned by shareholders who appoint one director to

give direction to the business. Company needs to maintain the statement of income, Statement of

comprehensive income, balance sheet, statement of cash flows, statement of stockholders' equity

etc. These five statements are to accompanied with notes to the financial statements.

Franchising-

It is business in which a company gives license to other individuals or companies to use

their name for top use their ideas. Franchisor has to maintain the legal documents related to their

franchise business and they are working according to the rules and regulations of the company. The

legal documents of the Franchise business. (Mason 2015).

2.1 Financial Information legally required from major types of Business Organisation in the UK are

There are various types of Business Organisation in the UK are -

Sole Traders-

In this type of business only an individual requires to run the business. Sole trader prepares

the balance sheet at a specific point of time. The statement of financial performance also known as

income statement or trading account are also prepared in order to know the profitability position of

the business. To determine the link between the balance sheet and income statement the statement

of changes in Owner's equity is also prepared. This statement shows the increase or decrease of

owner's equity in the business.

Partnership-

In this there is minimum requirement of 2 persons to start the business. There can unlimited

number of partners in the business (Mason 2015). Partnership firms are required to prepare the

statement of partner's equity in order to know the increase or decrease of equity by the partners.

Firm has to also prepare the income statements, balance sheet and cash flow statement.

Private and Public Companies-

In this type of business, the company is owned by shareholders who appoint one director to

give direction to the business. Company needs to maintain the statement of income, Statement of

comprehensive income, balance sheet, statement of cash flows, statement of stockholders' equity

etc. These five statements are to accompanied with notes to the financial statements.

Franchising-

It is business in which a company gives license to other individuals or companies to use

their name for top use their ideas. Franchisor has to maintain the legal documents related to their

franchise business and they are working according to the rules and regulations of the company. The

legal documents of the Franchise business. (Mason 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

LO 3

3.1 Management needs Financial Information

Company's needs financial information to know the profitability position, liquidity position

and efficiency position of the company.

Company also needs Financial Information in order to take major decisions related to cost

allocation and how to maximize the profits of the company.

It also needs to analyse the company's financial statements with the competitive' s financial

statements to make competitive analysis (Zietlow and et.al., 2018).

It is also used to know whether company is achieving its objectives or not. Whether its

targets are achieved or not.

Management wants to know whether there is proper allocation of profits or not. The retained

earnings are properly invested in productive assets or not.

Planning and Budgeting are also made on the basis of the Financial Information of the

business. Also, financial projections are made on the basis of the financial statements

(McKinney 2015).

LO 4

4.1 Other users of Financial Information

There are various types of other users of financial information such as-

Owners and Investors-

These are highly interested in knowing the financial statements of the company because they

have invested in the company and wants to make certain decisions whether to purchase or sell the

company's shares. They also want to know the growth prospects of the company. In this way, small

business owners need financial information to determine that the company will be profitable,

improve, continue or drop it.

Lenders, Trade Creditors or Suppliers-

Lenders are interested that the company to whom they are want to provide the loan or not.

They want to know that whether the company will repay their loans or not. They are interested in

3.1 Management needs Financial Information

Company's needs financial information to know the profitability position, liquidity position

and efficiency position of the company.

Company also needs Financial Information in order to take major decisions related to cost

allocation and how to maximize the profits of the company.

It also needs to analyse the company's financial statements with the competitive' s financial

statements to make competitive analysis (Zietlow and et.al., 2018).

It is also used to know whether company is achieving its objectives or not. Whether its

targets are achieved or not.

Management wants to know whether there is proper allocation of profits or not. The retained

earnings are properly invested in productive assets or not.

Planning and Budgeting are also made on the basis of the Financial Information of the

business. Also, financial projections are made on the basis of the financial statements

(McKinney 2015).

LO 4

4.1 Other users of Financial Information

There are various types of other users of financial information such as-

Owners and Investors-

These are highly interested in knowing the financial statements of the company because they

have invested in the company and wants to make certain decisions whether to purchase or sell the

company's shares. They also want to know the growth prospects of the company. In this way, small

business owners need financial information to determine that the company will be profitable,

improve, continue or drop it.

Lenders, Trade Creditors or Suppliers-

Lenders are interested that the company to whom they are want to provide the loan or not.

They want to know that whether the company will repay their loans or not. They are interested in

the financial statements of the company in order to know that company is working the profitability

or not (Minnis 2017).

Government-

Government wants to know that company is paying taxes on the profits shown in the

financial statements. They are interested in an entity's financial information for taxation and

regulatory purposes. In general, they want to know how much the taxpayer makes determine the tax

due thereon.

Management-

Management wants to know the financial information in order to make operational and

financial decisions. They want to take certain decisions such as how much supplies will they

purchase? Do we have enough cash? etc. Thus, in order to take such decisions, management want to

know the financial position of the company.

LO 5

5.1 Purpose of main Financial Statements in Business

Income Statement

The main purpose of income statement is to show the profitability position of the company

i.e. showing the net profits after paying all expenses such as taxes, interests, operating expenses of

the company. This contains the several items which helps in determining how a profit or loss are

generated. Income Statement gives different information to different users such as lenders use the

income statement to know whether he should lend loan to the company or not. An investor use same

income statement to know what is profitability position of the company.

Balance Sheet

The main purpose of balance sheet is to reveal the financial status of the company as of a

specific point of time. The statement shows the total value of the company in terms of the assets and

the value of the financing done to invest in those assets. The statement also shows the subsets of the

various heads and these are compared with each other. Current assets are compared with current

liabilities to see whether the equal amount of current assets are there to pay against current

liabilities. Non current liabilities are compared with Fixed Assets to know Fixed assets are there to

pay off the long term debts.

Cash Flow Statement

or not (Minnis 2017).

Government-

Government wants to know that company is paying taxes on the profits shown in the

financial statements. They are interested in an entity's financial information for taxation and

regulatory purposes. In general, they want to know how much the taxpayer makes determine the tax

due thereon.

Management-

Management wants to know the financial information in order to make operational and

financial decisions. They want to take certain decisions such as how much supplies will they

purchase? Do we have enough cash? etc. Thus, in order to take such decisions, management want to

know the financial position of the company.

LO 5

5.1 Purpose of main Financial Statements in Business

Income Statement

The main purpose of income statement is to show the profitability position of the company

i.e. showing the net profits after paying all expenses such as taxes, interests, operating expenses of

the company. This contains the several items which helps in determining how a profit or loss are

generated. Income Statement gives different information to different users such as lenders use the

income statement to know whether he should lend loan to the company or not. An investor use same

income statement to know what is profitability position of the company.

Balance Sheet

The main purpose of balance sheet is to reveal the financial status of the company as of a

specific point of time. The statement shows the total value of the company in terms of the assets and

the value of the financing done to invest in those assets. The statement also shows the subsets of the

various heads and these are compared with each other. Current assets are compared with current

liabilities to see whether the equal amount of current assets are there to pay against current

liabilities. Non current liabilities are compared with Fixed Assets to know Fixed assets are there to

pay off the long term debts.

Cash Flow Statement

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The main purpose of the cash flow statement is to check the liquidity position of the

company. To see that cash inflows are more than cash outflows. The primary purpose of the cash

flow statement is to know the cash flows from operating income, investing income and financing

income (Jansen 2017).

CONCLUSION

This report shows the financial position of the company is good and company should

maintain its policies for future on which company is working presently. Company's financial ratios

shows that company is having good financial position. Also, by using this information managers,

other users can take best decisions. The company can also use this information to maximize the

profits and know where the extra cost has been allocated. Thus, company should try to maintain the

same policies in order to maintain same financial position.

company. To see that cash inflows are more than cash outflows. The primary purpose of the cash

flow statement is to know the cash flows from operating income, investing income and financing

income (Jansen 2017).

CONCLUSION

This report shows the financial position of the company is good and company should

maintain its policies for future on which company is working presently. Company's financial ratios

shows that company is having good financial position. Also, by using this information managers,

other users can take best decisions. The company can also use this information to maximize the

profits and know where the extra cost has been allocated. Thus, company should try to maintain the

same policies in order to maintain same financial position.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.