MNT Finance Memo: Evaluating Options for Driverless Sports Cars

VerifiedAdded on 2023/01/19

|5

|945

|87

Report

AI Summary

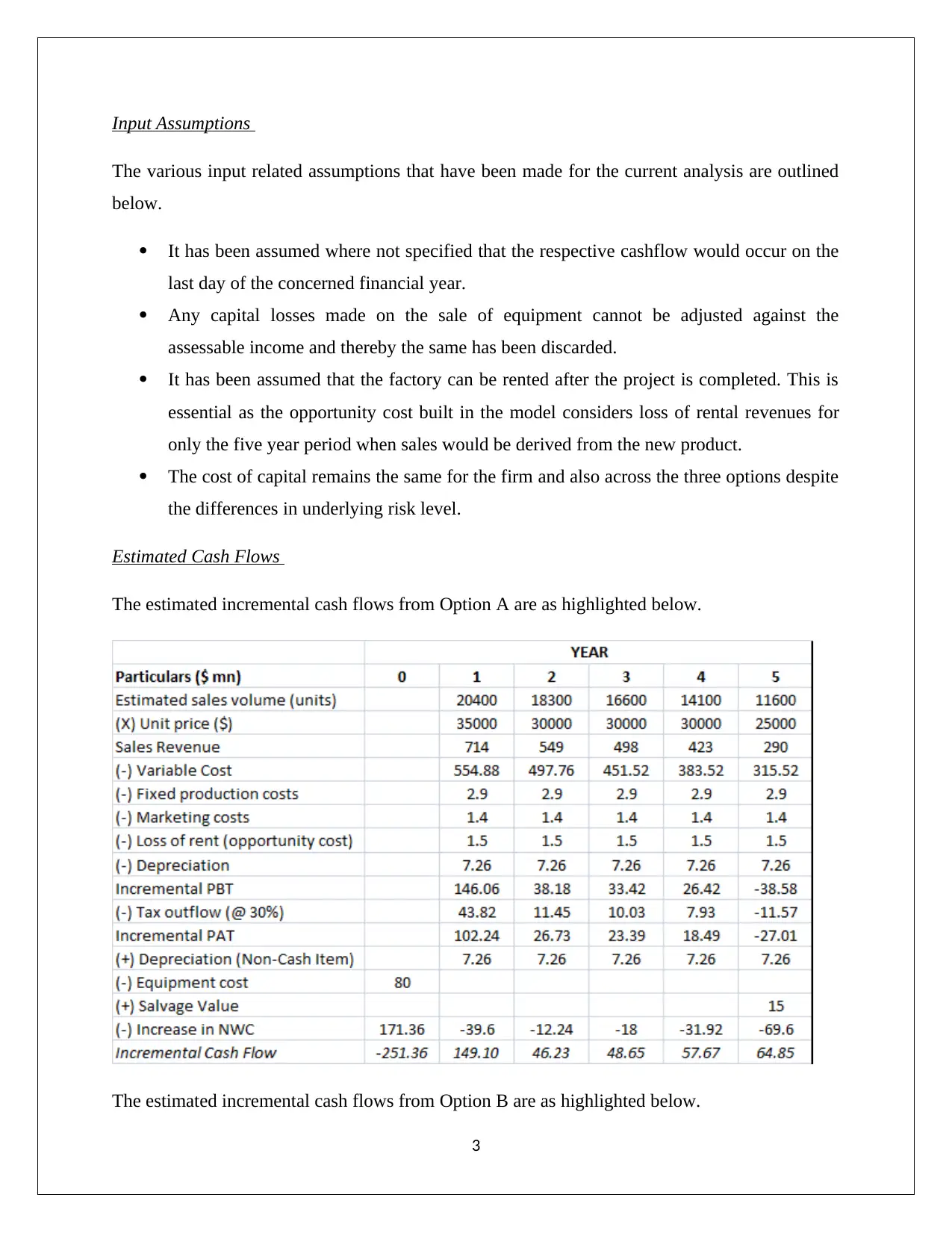

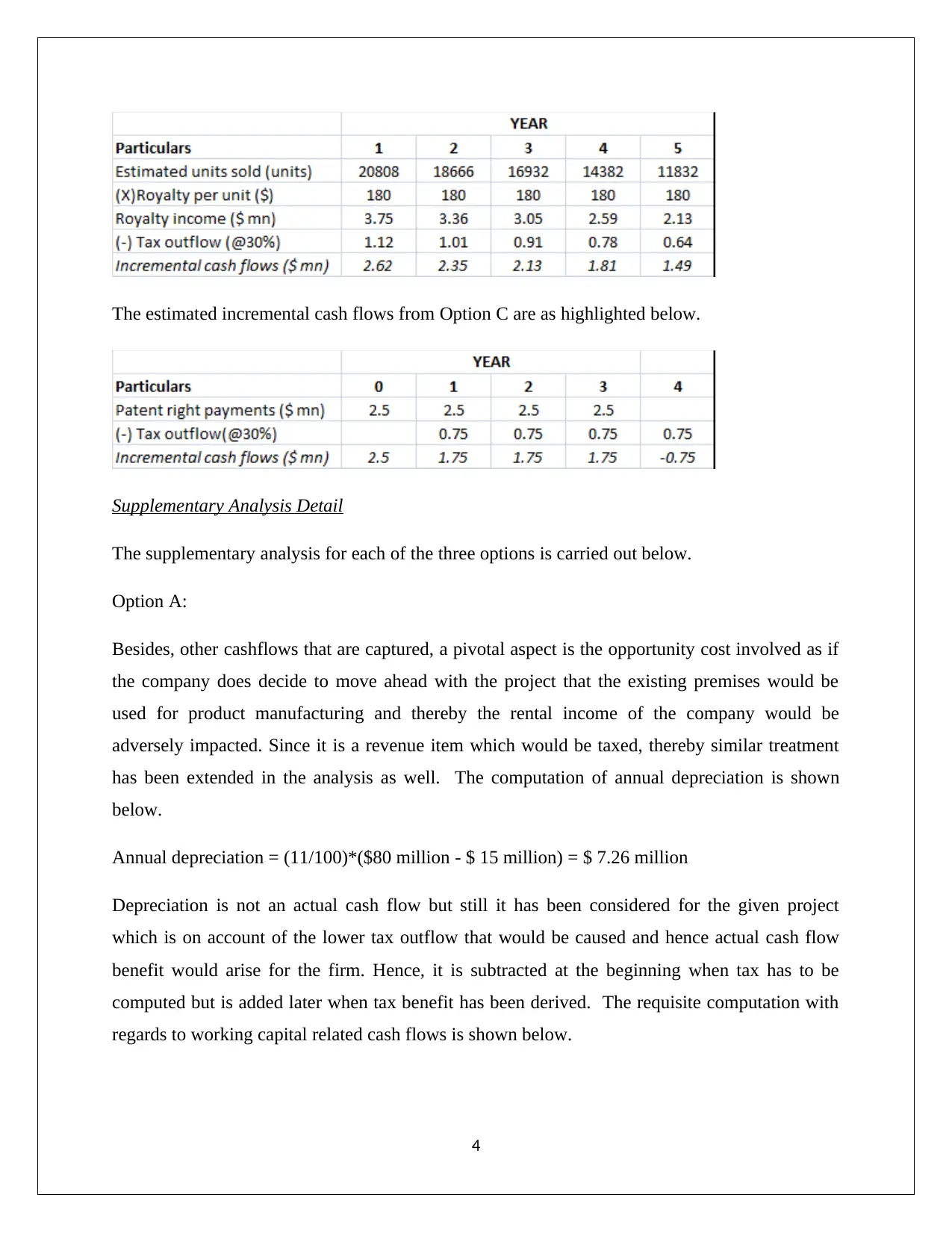

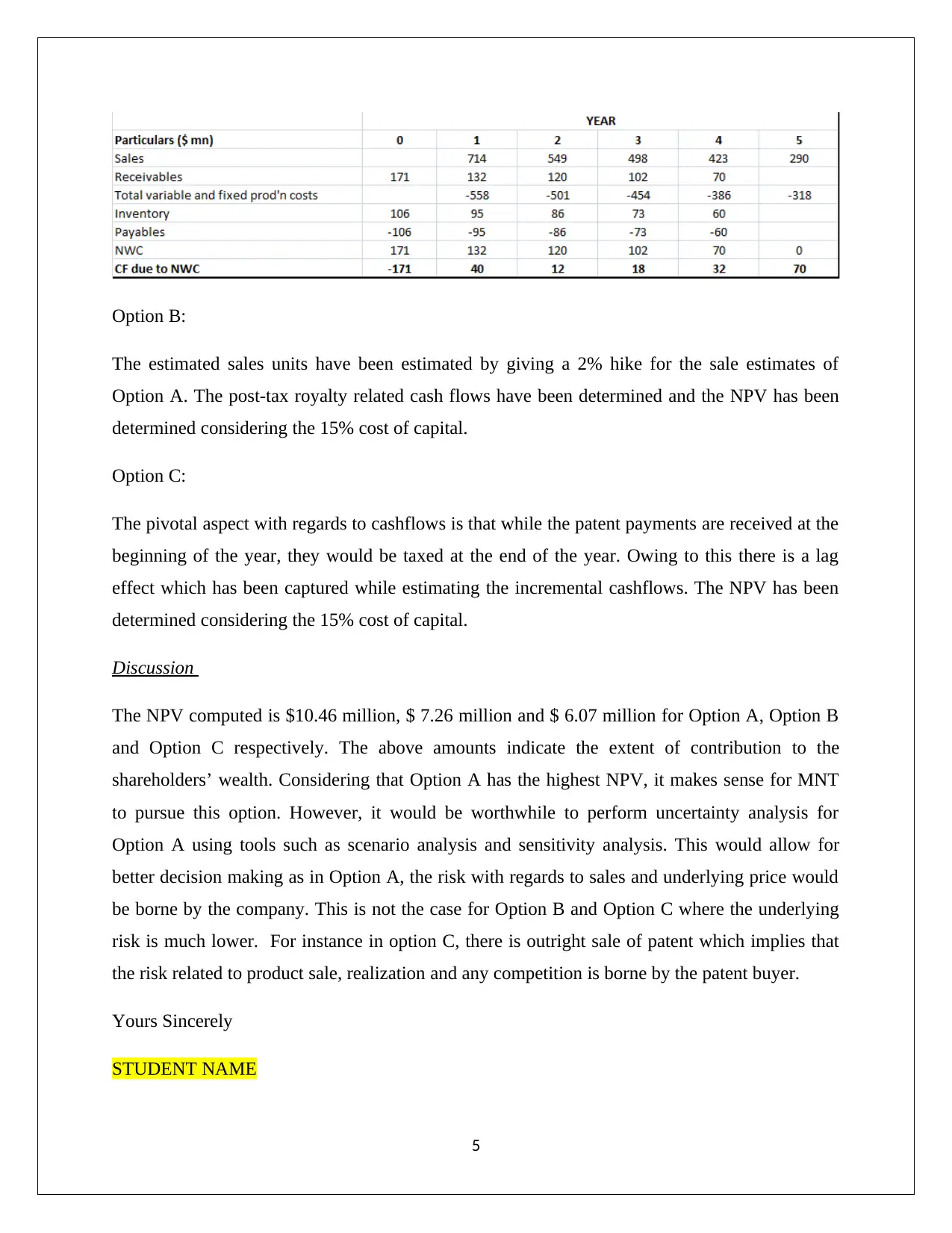

This finance memo, prepared by a student, evaluates three mutually exclusive options for MicroNet Technologies (MNT) regarding the commercialization of driverless sports car technology. The analysis employs Net Present Value (NPV) as the primary decision rule to determine the most financially viable option. Option A, involving in-house manufacturing and direct sales, is found to be the most superior, with the highest NPV. The memo details the methodology, key findings, and recommendations, while also outlining various input assumptions such as cash flow timings, depreciation calculations, and working capital considerations. Supplementary analyses for each option are included, along with a discussion of the risks and benefits associated with each approach, emphasizing the importance of uncertainty analysis, such as scenario and sensitivity analyses, for a more informed decision-making process. The memo concludes by advising the board to consider qualitative aspects alongside the financial analysis before making a final decision.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.