Business Finance Assignment - Project Evaluation and Analysis

VerifiedAdded on 2023/06/10

|20

|3128

|106

Homework Assignment

AI Summary

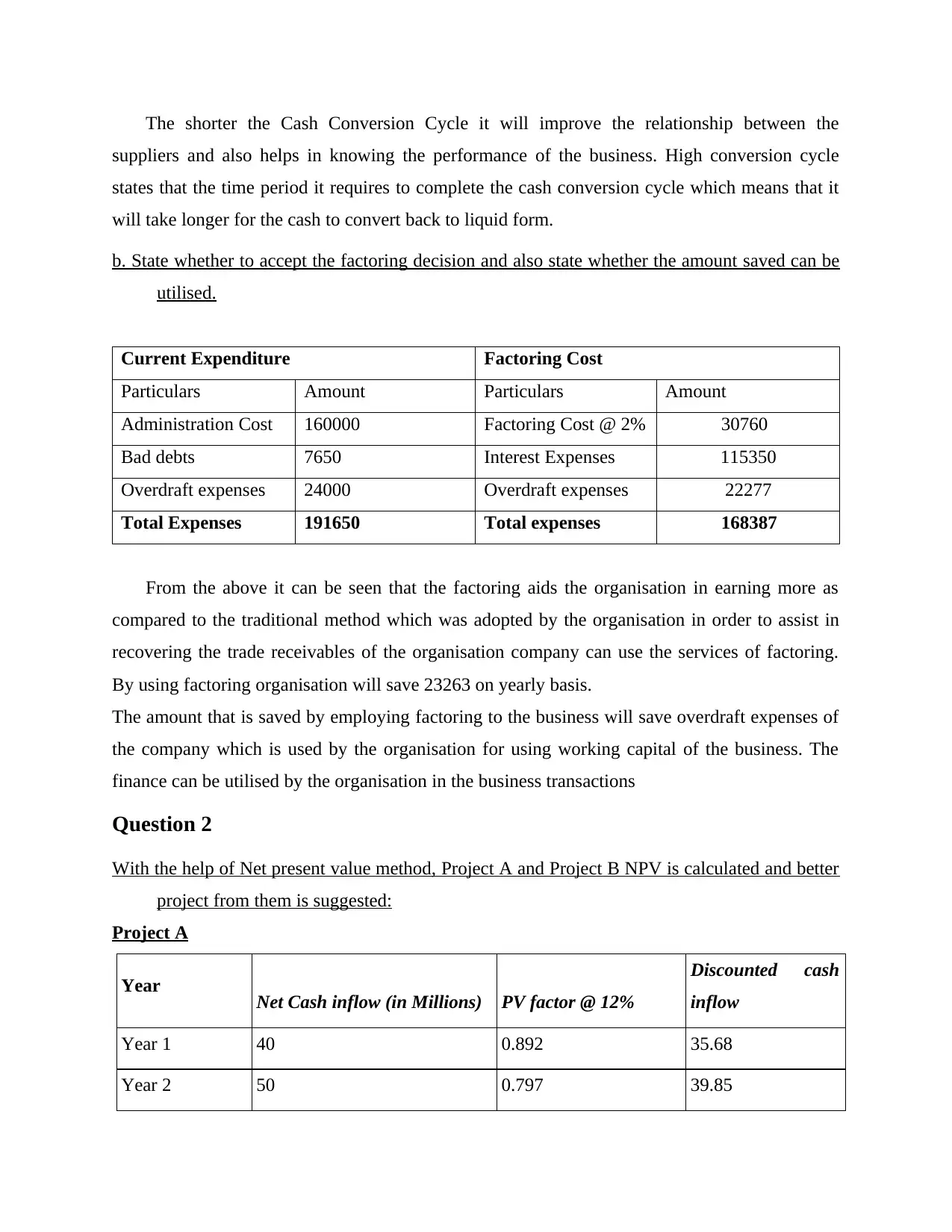

This assignment provides a comprehensive analysis of various business finance concepts. It begins by calculating the cash conversion cycle, which is crucial for understanding a company's liquidity. The assignment then delves into project evaluation, using the Net Present Value (NPV) and Internal Rate of Return (IRR) methods to compare and recommend the best investment project. Furthermore, it addresses the impact of changes in the cost of capital. The assignment also covers the calculation of the Weighted Average Cost of Capital (WACC), including market weightings, and discusses strategies for reducing WACC. Finally, it explores dividend policies, including the determination of annual dividend payments, practical considerations for setting dividend sizes, and the impact of different dividend options on shareholder wealth.

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.