Business Finance Project 4: Understanding and Analyzing Financial Data

VerifiedAdded on 2021/02/19

|10

|2314

|38

Report

AI Summary

This report provides a comprehensive analysis of financial information, focusing on its importance for business decision-making. It begins by explaining the legal requirements for different business structures, including sole traders, partnerships, private limited companies, and public limited companie...

Business Finance project 4

Understanding Financial

Information

Understanding Financial

Information

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

CONCLUSION................................................................................................................................1

REFERENCES................................................................................................................................2

INTRODUCTION...........................................................................................................................1

CONCLUSION................................................................................................................................1

REFERENCES................................................................................................................................2

INTRODUCTION

Financial information keeps proper records of the various financial transactions which

helps management of the organization in giving relevant information for crucial decision

making. This report will include key financial ratios by applying it with business performance.

This study will also evaluate the management need of financial data. This study also helps in

understanding the users of financial information. Furthermore, this study highlights the purpose

of various financial statements.

2. 1 Legal requirements for different business organization.

Sole trader: It is an effective of business structure which is very easy and inexpensive to

set up. Sole trader is a business which is completely owned by an individual and does not have

any share in the profit. The management of the company should up to date its profitability

information and also calculate tax for smooth functioning of the business.

Partnership: This firm is a business in whicvh group of people or partners come together

to carry out the business (Qrunig and Qrunig, 2016). Partners of this company share profits and

losses with each partners within specific ratio or share of them in business. There are various

legal requirement in UK within which it must comply with for smooth functioning of the

business. The partners individually assess tax returns in accordance with their share of profits to

the HMRC. It must also pay NIC (National Insurance Contribution). The partnership firm must

also sign a deed and compalt with various legal requrements such as disclosure of annual returns.

Private limited company: This business entity is a private ownership of the business.

This company is established for the purpose of making profits which leads to graeter market

share (Thompson, 2017). The company should comply with various legal requirement of UK

such as proper records and mainenance of MOA, AOA, copmpany records, corporation tax and

proper disclosure of annual reports finacially.

Public limited company: This is an organization whose securities are listed on the

recognized stock exchange to buy and sell shares. This company is completely regulated by

various authorities. The company should publish all the financial statemnts aby showing true

financial position opf the company (Martínez‐Ferrero, Garcia‐Sanchez and Cuadrado‐

Ballesteros, 2015). It is there legal requirement to pay tax and disclosr=e true statemnts to

shareholders.

1

Financial information keeps proper records of the various financial transactions which

helps management of the organization in giving relevant information for crucial decision

making. This report will include key financial ratios by applying it with business performance.

This study will also evaluate the management need of financial data. This study also helps in

understanding the users of financial information. Furthermore, this study highlights the purpose

of various financial statements.

2. 1 Legal requirements for different business organization.

Sole trader: It is an effective of business structure which is very easy and inexpensive to

set up. Sole trader is a business which is completely owned by an individual and does not have

any share in the profit. The management of the company should up to date its profitability

information and also calculate tax for smooth functioning of the business.

Partnership: This firm is a business in whicvh group of people or partners come together

to carry out the business (Qrunig and Qrunig, 2016). Partners of this company share profits and

losses with each partners within specific ratio or share of them in business. There are various

legal requirement in UK within which it must comply with for smooth functioning of the

business. The partners individually assess tax returns in accordance with their share of profits to

the HMRC. It must also pay NIC (National Insurance Contribution). The partnership firm must

also sign a deed and compalt with various legal requrements such as disclosure of annual returns.

Private limited company: This business entity is a private ownership of the business.

This company is established for the purpose of making profits which leads to graeter market

share (Thompson, 2017). The company should comply with various legal requirement of UK

such as proper records and mainenance of MOA, AOA, copmpany records, corporation tax and

proper disclosure of annual reports finacially.

Public limited company: This is an organization whose securities are listed on the

recognized stock exchange to buy and sell shares. This company is completely regulated by

various authorities. The company should publish all the financial statemnts aby showing true

financial position opf the company (Martínez‐Ferrero, Garcia‐Sanchez and Cuadrado‐

Ballesteros, 2015). It is there legal requirement to pay tax and disclosr=e true statemnts to

shareholders.

1

You're viewing a preview

Unlock full access by subscribing today!

3.1 Need of financial information for management.

Financial information is a formal representation and recording of financial transactions

for the particular period (Fields, 2016). Financial information takes into consideration financial

data which results in higher operational efficiency and standards. Management of the

organization generates various financial statements which includes balance sheet, income

statement, Cash flow statement and Statement of change in Equity. These statements give

detailed analysis of the various financial transactions and give clear picture about the operations

of the business.

Managers of the organization can use these financial information in order to take long

term growth and operational efficiency of the business (Martínez‐Ferrero, Garcia‐Sanchez and

Cuadrado‐Ballesteros, 2015). These financial information helps in taking strategic decision to

perform various financial analysis and make investment decisions. Financial information of the

company helps in estimating the financial position of the company by critically evaluating the

company's liquidity, financial leverage, profitability and operational efficiency. Managers of the

company use financial information to analyse and compare the actual performance of the

company with its competitors in order to develop strategic plan and set benchmark to attain

higher competitive position (Why Do Managers Analyze Financial Statements?, 2017).

Financial information is necessary because it helps in managing the credit risk which helps in

managing the funds and attain effective liquidity position in the company to carry out various

function smoothly. Managers of the company use financial information to mitigate target by

setting standard and benchmark. This helps in achieving greater heights with greater accuracy

and efficiency (Christensen, Nikolaev and Wittenberg‐Moerman, 2016). Financial information

is crucial for the future prediction of the business. Financial information helps management in

optimum utilization of the resources and make funds available for higher operational

productivity and timely attainment of goals and objectives.

3. Explaining various stakeholders and their interest in the financial information.

There are various other stakeholders that has the interest in the financial statements of the

organization. Specifically the stakeholders are classified into two parts that include internal and

the external stakeholders (Lakis and Masiulevičius, 2017). Internal stakeholders refers to the

parties that are present within the organization like managers, employees etc. while the external

2

Financial information is a formal representation and recording of financial transactions

for the particular period (Fields, 2016). Financial information takes into consideration financial

data which results in higher operational efficiency and standards. Management of the

organization generates various financial statements which includes balance sheet, income

statement, Cash flow statement and Statement of change in Equity. These statements give

detailed analysis of the various financial transactions and give clear picture about the operations

of the business.

Managers of the organization can use these financial information in order to take long

term growth and operational efficiency of the business (Martínez‐Ferrero, Garcia‐Sanchez and

Cuadrado‐Ballesteros, 2015). These financial information helps in taking strategic decision to

perform various financial analysis and make investment decisions. Financial information of the

company helps in estimating the financial position of the company by critically evaluating the

company's liquidity, financial leverage, profitability and operational efficiency. Managers of the

company use financial information to analyse and compare the actual performance of the

company with its competitors in order to develop strategic plan and set benchmark to attain

higher competitive position (Why Do Managers Analyze Financial Statements?, 2017).

Financial information is necessary because it helps in managing the credit risk which helps in

managing the funds and attain effective liquidity position in the company to carry out various

function smoothly. Managers of the company use financial information to mitigate target by

setting standard and benchmark. This helps in achieving greater heights with greater accuracy

and efficiency (Christensen, Nikolaev and Wittenberg‐Moerman, 2016). Financial information

is crucial for the future prediction of the business. Financial information helps management in

optimum utilization of the resources and make funds available for higher operational

productivity and timely attainment of goals and objectives.

3. Explaining various stakeholders and their interest in the financial information.

There are various other stakeholders that has the interest in the financial statements of the

organization. Specifically the stakeholders are classified into two parts that include internal and

the external stakeholders (Lakis and Masiulevičius, 2017). Internal stakeholders refers to the

parties that are present within the organization like managers, employees etc. while the external

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

stakeholders' means the parties that are outside to the company such as customers, government,

investors and competitors.

Managers- The management team has to understand the liquidity, cash flow and the

profitability of an enterprise for each month in order to make the financing and the operational

decisions of the business.

Competitors- Companies competing against each other assess the financial statements for

evaluating the financial condition of the business and in gaining the competitive strategies.

Customers- For selecting the supplier for the major contract, customer review the

financial statements for judging the financial ability of the supplier for remaining in the business

for a longer period in providing goods and the services provisioned in the contract (Asztalos,

Hennig and Warburton, 2016).

Employees- They use the financial information for evaluating the performance of the

company and for increasing the involvement of the employee and in understanding the business

appropriately.

Investors- Such stakeholders require financial information in order to analyse the

company performance in which they had made the investment and in making the decision for

making further investment or to withdraw the investment if the company is not performing well.

4. Explaining the purpose of the income statement and the balance sheet.

Profit and loss statement referred as the financial statement which summarizes revenues,

expenses and the cost that are incurred during the specified period. This statement facilitates the

information regarding the ability of the company in generating the profit by the way of

increasing revenue and the reducing the cost (Huseynov and Yıldırım, 2016). The major purpose

of income statement is to provide accurate view of the financial performance of the company.

The basic purpose of the statement is to provide the information relating to the profitability of the

organization and the other important details that include sales, turnover, operational

expenditures, cost of sales and the financial expenditure. It also provides data for planning and

the controlling process in order to compare the budgeted and the actual results called as the

variance analysis.

Balance sheet is the financial statement that is prepared for reporting the assets, liabilities

and the shareholders' equity of the company at particular time period and facilitates the base for

3

investors and competitors.

Managers- The management team has to understand the liquidity, cash flow and the

profitability of an enterprise for each month in order to make the financing and the operational

decisions of the business.

Competitors- Companies competing against each other assess the financial statements for

evaluating the financial condition of the business and in gaining the competitive strategies.

Customers- For selecting the supplier for the major contract, customer review the

financial statements for judging the financial ability of the supplier for remaining in the business

for a longer period in providing goods and the services provisioned in the contract (Asztalos,

Hennig and Warburton, 2016).

Employees- They use the financial information for evaluating the performance of the

company and for increasing the involvement of the employee and in understanding the business

appropriately.

Investors- Such stakeholders require financial information in order to analyse the

company performance in which they had made the investment and in making the decision for

making further investment or to withdraw the investment if the company is not performing well.

4. Explaining the purpose of the income statement and the balance sheet.

Profit and loss statement referred as the financial statement which summarizes revenues,

expenses and the cost that are incurred during the specified period. This statement facilitates the

information regarding the ability of the company in generating the profit by the way of

increasing revenue and the reducing the cost (Huseynov and Yıldırım, 2016). The major purpose

of income statement is to provide accurate view of the financial performance of the company.

The basic purpose of the statement is to provide the information relating to the profitability of the

organization and the other important details that include sales, turnover, operational

expenditures, cost of sales and the financial expenditure. It also provides data for planning and

the controlling process in order to compare the budgeted and the actual results called as the

variance analysis.

Balance sheet is the financial statement that is prepared for reporting the assets, liabilities

and the shareholders' equity of the company at particular time period and facilitates the base for

3

calculating the return rate and in evaluating the capital structure (Sutton, Cordery and van Zijl,

2015). The main purpose of the balance sheet is to communicate the financial status of the

organization at specific period. It provides all the details regarding the funds of the enterprise and

in making the assessment relating to the ability of the company in meeting its current obligations.

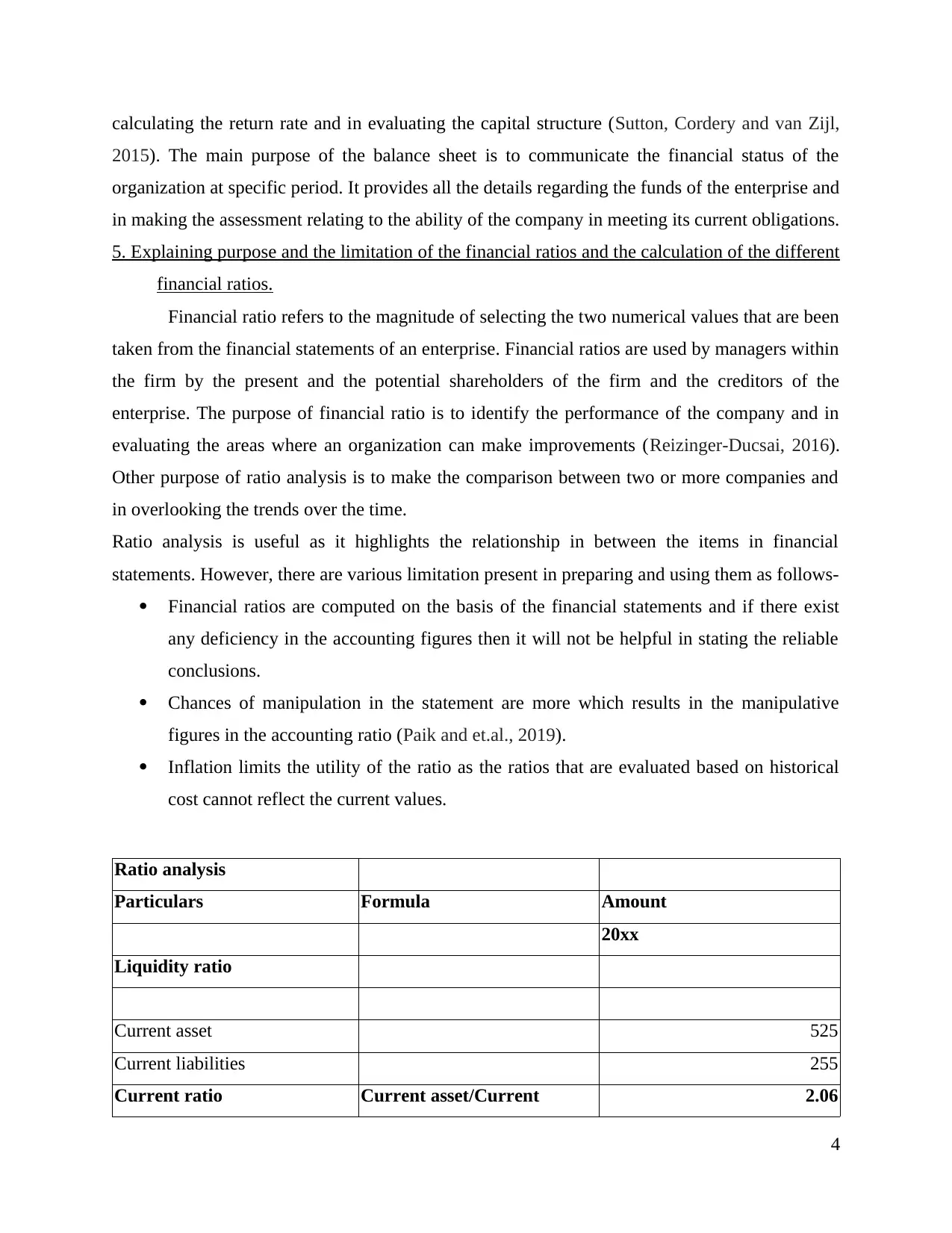

5. Explaining purpose and the limitation of the financial ratios and the calculation of the different

financial ratios.

Financial ratio refers to the magnitude of selecting the two numerical values that are been

taken from the financial statements of an enterprise. Financial ratios are used by managers within

the firm by the present and the potential shareholders of the firm and the creditors of the

enterprise. The purpose of financial ratio is to identify the performance of the company and in

evaluating the areas where an organization can make improvements (Reizinger-Ducsai, 2016).

Other purpose of ratio analysis is to make the comparison between two or more companies and

in overlooking the trends over the time.

Ratio analysis is useful as it highlights the relationship in between the items in financial

statements. However, there are various limitation present in preparing and using them as follows-

Financial ratios are computed on the basis of the financial statements and if there exist

any deficiency in the accounting figures then it will not be helpful in stating the reliable

conclusions.

Chances of manipulation in the statement are more which results in the manipulative

figures in the accounting ratio (Paik and et.al., 2019).

Inflation limits the utility of the ratio as the ratios that are evaluated based on historical

cost cannot reflect the current values.

Ratio analysis

Particulars Formula Amount

20xx

Liquidity ratio

Current asset 525

Current liabilities 255

Current ratio Current asset/Current 2.06

4

2015). The main purpose of the balance sheet is to communicate the financial status of the

organization at specific period. It provides all the details regarding the funds of the enterprise and

in making the assessment relating to the ability of the company in meeting its current obligations.

5. Explaining purpose and the limitation of the financial ratios and the calculation of the different

financial ratios.

Financial ratio refers to the magnitude of selecting the two numerical values that are been

taken from the financial statements of an enterprise. Financial ratios are used by managers within

the firm by the present and the potential shareholders of the firm and the creditors of the

enterprise. The purpose of financial ratio is to identify the performance of the company and in

evaluating the areas where an organization can make improvements (Reizinger-Ducsai, 2016).

Other purpose of ratio analysis is to make the comparison between two or more companies and

in overlooking the trends over the time.

Ratio analysis is useful as it highlights the relationship in between the items in financial

statements. However, there are various limitation present in preparing and using them as follows-

Financial ratios are computed on the basis of the financial statements and if there exist

any deficiency in the accounting figures then it will not be helpful in stating the reliable

conclusions.

Chances of manipulation in the statement are more which results in the manipulative

figures in the accounting ratio (Paik and et.al., 2019).

Inflation limits the utility of the ratio as the ratios that are evaluated based on historical

cost cannot reflect the current values.

Ratio analysis

Particulars Formula Amount

20xx

Liquidity ratio

Current asset 525

Current liabilities 255

Current ratio Current asset/Current 2.06

4

You're viewing a preview

Unlock full access by subscribing today!

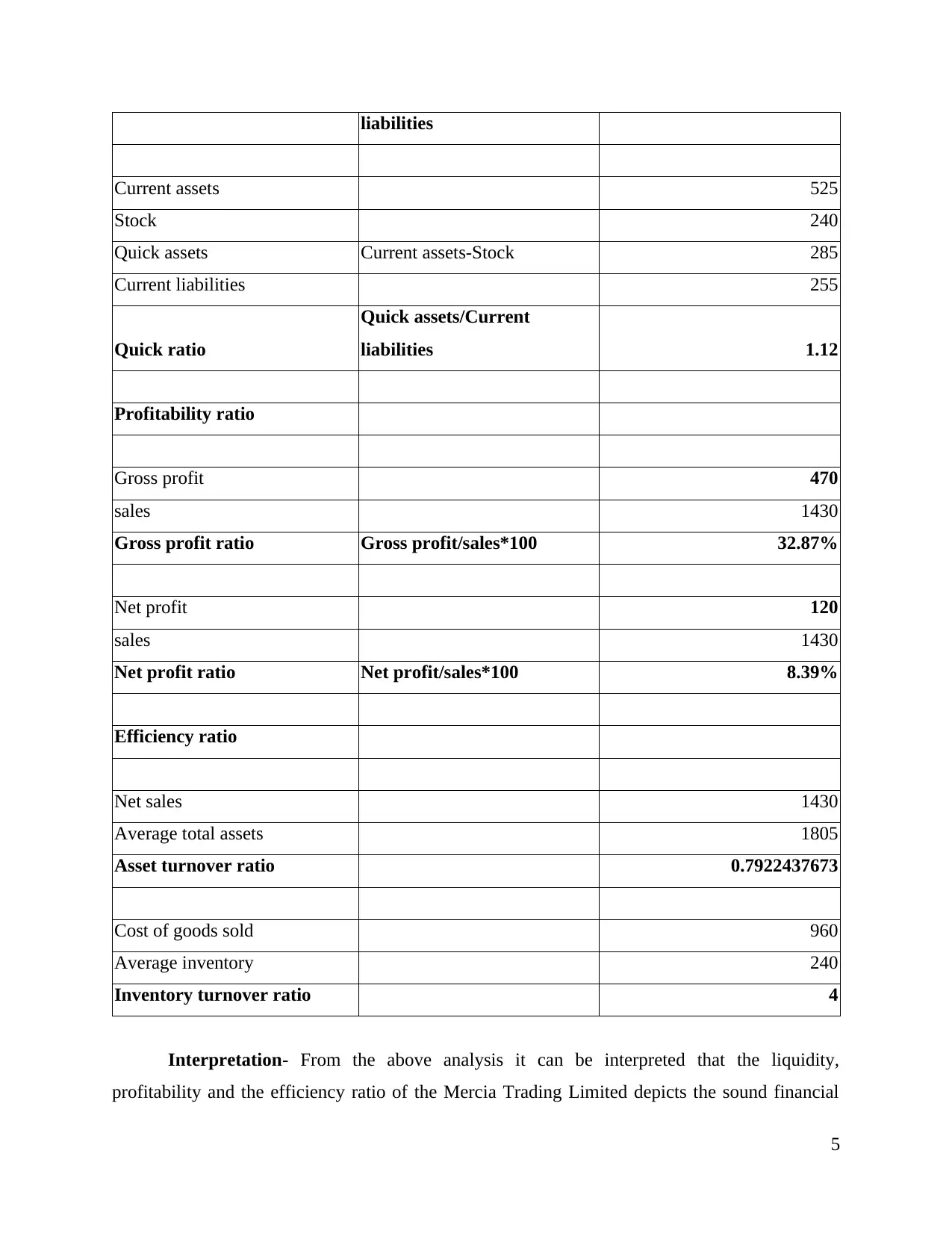

liabilities

Current assets 525

Stock 240

Quick assets Current assets-Stock 285

Current liabilities 255

Quick ratio

Quick assets/Current

liabilities 1.12

Profitability ratio

Gross profit 470

sales 1430

Gross profit ratio Gross profit/sales*100 32.87%

Net profit 120

sales 1430

Net profit ratio Net profit/sales*100 8.39%

Efficiency ratio

Net sales 1430

Average total assets 1805

Asset turnover ratio 0.7922437673

Cost of goods sold 960

Average inventory 240

Inventory turnover ratio 4

Interpretation- From the above analysis it can be interpreted that the liquidity,

profitability and the efficiency ratio of the Mercia Trading Limited depicts the sound financial

5

Current assets 525

Stock 240

Quick assets Current assets-Stock 285

Current liabilities 255

Quick ratio

Quick assets/Current

liabilities 1.12

Profitability ratio

Gross profit 470

sales 1430

Gross profit ratio Gross profit/sales*100 32.87%

Net profit 120

sales 1430

Net profit ratio Net profit/sales*100 8.39%

Efficiency ratio

Net sales 1430

Average total assets 1805

Asset turnover ratio 0.7922437673

Cost of goods sold 960

Average inventory 240

Inventory turnover ratio 4

Interpretation- From the above analysis it can be interpreted that the liquidity,

profitability and the efficiency ratio of the Mercia Trading Limited depicts the sound financial

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

position of the company as the liquidity ratio is close to the ideal ratio that is 2:1 which means

the company has efficiently managed it current assets resulted as 2.06 as current ratio and 1.12 as

quick ratio. The profitability of company si also good as the gross and net profit ratio equated to

32.87% and 8.39%. The assets turnover and the inventory turnover resulted as 0.79 and 4 times

which is also a good ratio.

CONCLUSION

From the above study it has been concluded that, financial information is crucial for the

managers as it will evaluate and examine the financial position of the company. It also helps in

comparing the performance with the competitors to attain higher competitive position and attain

targets. It has been summarized that, there are various business structure which must comply

with legal requremnts of UK. This study also highlights, in- depth understanding on various

finacial staremnts and financial ratios.

6

the company has efficiently managed it current assets resulted as 2.06 as current ratio and 1.12 as

quick ratio. The profitability of company si also good as the gross and net profit ratio equated to

32.87% and 8.39%. The assets turnover and the inventory turnover resulted as 0.79 and 4 times

which is also a good ratio.

CONCLUSION

From the above study it has been concluded that, financial information is crucial for the

managers as it will evaluate and examine the financial position of the company. It also helps in

comparing the performance with the competitors to attain higher competitive position and attain

targets. It has been summarized that, there are various business structure which must comply

with legal requremnts of UK. This study also highlights, in- depth understanding on various

finacial staremnts and financial ratios.

6

REFERENCES

Books and Journals

Asztalos, S. J., Hennig, W. and Warburton, W. K., 2016. General purpose pulse shape analysis

for fast scintillators implemented in digital readout electronics. Nuclear Instruments and

Methods in Physics Research Section A: Accelerators, Spectrometers, Detectors and

Associated Equipment. 806. pp.132-138.

Christensen, H.B., Nikolaev, V.V. and Wittenberg‐Moerman, R., 2016. Accounting information

in financial contracting: The incomplete contract theory perspective. Journal of accounting

research.54(2). pp.397-435.

Fields, E., 2016. The essentials of finance and accounting for nonfinancial managers. Amacom.

Huseynov, F. and Yıldırım, S. Ö., 2016. Internet users’ attitudes toward business-to-consumer

online shopping: A survey. Information Development. 32(3). pp.452-465.

Lakis, V. and Masiulevičius, A., 2017. ACCEPTABLE AUDIT MATERIALITY FOR USERS

OF FINANCIAL STATEMENTS. Journal of Management. 2(31).

Martínez‐Ferrero, J., Garcia‐Sanchez, I.M. and Cuadrado‐Ballesteros, B., 2015. Effect of

financial reporting quality on sustainability information disclosure. Corporate Social

Responsibility and Environmental Management. 22(1). pp.45-64.

Paik, D.G. and et.al., 2019. Loan purpose and accounting based debt covenants. Review of

Accounting and Finance. 18(2). pp.321-343.

Qrunig, J.E. and Qrunig, L.A., 2016. Toward a theory of the public relations behavior of

organizations: Review of a program of research. In Public relations research annual (pp.

37-74). Routledge.

Reizinger-Ducsai, A., 2016. Bankruptcy prediction and financial statements. The reliability of a

financial statement for the purpose of modelling. Prace Naukowe Uniwersytetu

Ekonomicznego we Wrocławiu. (441). pp.202-213.

Sutton, D. B., Cordery, C. J. and van Zijl, T., 2015. The purpose of financial reporting: The case

for coherence in the conceptual framework and standards. Abacus. 51(1). pp.116-141.

7

Books and Journals

Asztalos, S. J., Hennig, W. and Warburton, W. K., 2016. General purpose pulse shape analysis

for fast scintillators implemented in digital readout electronics. Nuclear Instruments and

Methods in Physics Research Section A: Accelerators, Spectrometers, Detectors and

Associated Equipment. 806. pp.132-138.

Christensen, H.B., Nikolaev, V.V. and Wittenberg‐Moerman, R., 2016. Accounting information

in financial contracting: The incomplete contract theory perspective. Journal of accounting

research.54(2). pp.397-435.

Fields, E., 2016. The essentials of finance and accounting for nonfinancial managers. Amacom.

Huseynov, F. and Yıldırım, S. Ö., 2016. Internet users’ attitudes toward business-to-consumer

online shopping: A survey. Information Development. 32(3). pp.452-465.

Lakis, V. and Masiulevičius, A., 2017. ACCEPTABLE AUDIT MATERIALITY FOR USERS

OF FINANCIAL STATEMENTS. Journal of Management. 2(31).

Martínez‐Ferrero, J., Garcia‐Sanchez, I.M. and Cuadrado‐Ballesteros, B., 2015. Effect of

financial reporting quality on sustainability information disclosure. Corporate Social

Responsibility and Environmental Management. 22(1). pp.45-64.

Paik, D.G. and et.al., 2019. Loan purpose and accounting based debt covenants. Review of

Accounting and Finance. 18(2). pp.321-343.

Qrunig, J.E. and Qrunig, L.A., 2016. Toward a theory of the public relations behavior of

organizations: Review of a program of research. In Public relations research annual (pp.

37-74). Routledge.

Reizinger-Ducsai, A., 2016. Bankruptcy prediction and financial statements. The reliability of a

financial statement for the purpose of modelling. Prace Naukowe Uniwersytetu

Ekonomicznego we Wrocławiu. (441). pp.202-213.

Sutton, D. B., Cordery, C. J. and van Zijl, T., 2015. The purpose of financial reporting: The case

for coherence in the conceptual framework and standards. Abacus. 51(1). pp.116-141.

7

You're viewing a preview

Unlock full access by subscribing today!

Thompson, J.D., 2017. Organizations in action: Social science bases of administrative theory.

Routledge.

Online

Why Do Managers Analyze Financial Statements?. 2017. [ONLINE]. Available

through:<https://bizfluent.com/info-8507676-do-managers-analyze-financial-statements.html>

8

Routledge.

Online

Why Do Managers Analyze Financial Statements?. 2017. [ONLINE]. Available

through:<https://bizfluent.com/info-8507676-do-managers-analyze-financial-statements.html>

8

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.