Business Finance Project: Evaluating Investment Strategies and Risks

VerifiedAdded on 2023/01/05

|14

|3400

|40

Project

AI Summary

This project provides a comprehensive analysis of business finance, focusing on investment instruments and strategies. It begins with an executive summary and introduction, followed by a detailed discussion on the differences between debt and equity securities, yield changes, and various types of ris...

Business Finance project

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

EXECUTIVE SUMMARY.............................................................................................................3

INTRODUCTION...........................................................................................................................4

ANALYSIS AND DISCUSSION...................................................................................................4

Difference between return on debt securities and equity securities............................................4

Yield change through time but the coupon rate remains same....................................................5

Types of risk and how it is affected by increase in the number of shares in the portfolio..........5

Capital Asset Pricing Model (CAPM) to price risky securities...................................................6

Clients Investments......................................................................................................................7

Investment decision.....................................................................................................................8

Determining the internal rate of return........................................................................................9

Investing into bonds...................................................................................................................11

CONCLUSION AND RECOMMENDATION............................................................................12

REFERENCES..............................................................................................................................14

EXECUTIVE SUMMARY.............................................................................................................3

INTRODUCTION...........................................................................................................................4

ANALYSIS AND DISCUSSION...................................................................................................4

Difference between return on debt securities and equity securities............................................4

Yield change through time but the coupon rate remains same....................................................5

Types of risk and how it is affected by increase in the number of shares in the portfolio..........5

Capital Asset Pricing Model (CAPM) to price risky securities...................................................6

Clients Investments......................................................................................................................7

Investment decision.....................................................................................................................8

Determining the internal rate of return........................................................................................9

Investing into bonds...................................................................................................................11

CONCLUSION AND RECOMMENDATION............................................................................12

REFERENCES..............................................................................................................................14

EXECUTIVE SUMMARY

This report provides an insight on the various types of instruments and securities which are

being available for the investment purpose. This involves identifying the risk associated with

different instruments, methods for valuation of eth same, impact of fluctuation in the market over

the value of investment. It includes the mathematical calculation pertaining security valuation.

This report provides an insight on the various types of instruments and securities which are

being available for the investment purpose. This involves identifying the risk associated with

different instruments, methods for valuation of eth same, impact of fluctuation in the market over

the value of investment. It includes the mathematical calculation pertaining security valuation.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

This report is based on providing information along with certain calculations in in respect

to the various forms of investment option available for the purpose of financing business. There

are certain limitation pertaining to the report which are:

The financial position of client is not available.

The client is having only intermediate level of financial knowledge.

No information in respect to how many of these investments the client can purchase or

invest into.

This report provides a clear insight into the various aspects of the investment in both

theoretical and the mathematical calculations.

ANALYSIS AND DISCUSSION

Difference between return on debt securities and equity securities

Both the forms of investment provide a good return but the they are different from each

other in terms of return. In case of debt securities which involves bonds, mortgages and so forth,

includes the return in terms of fixed percentage or the fixed amount in relation to interest. While

the equity investment which involves stocks comes along with a claim on the income of the

company. The debt instrument is less risky in comparison with the equity instrument but it offers

lower return and is consistent in nature (Cheung and et.al.,2017). It is less volatile as compared

to the equity securities. with less highs and lows than the securities exchange. The security and

loan market generally encounter less value changes, regardless, than stocks. Likewise, at the time

of liquidation the bondholders or the debt holders are paid first. Mortgage ventures, as other

obligation instruments, accompanied with the interest costs and are backed up by real estate

security.

On the other hand, in the equity investment, fortune can be made or lost. Any financial

exchange can be unstable, with the fast changing value of the stocks. Regularly, these wide value

swings are not founded on the strength of the association backing them up however is because of

political, social or legislative issues in the nation of origin of the organization. Equity securities

are an exemplary case of taking on higher danger of misfortune as a byproduct of possibly higher

This report is based on providing information along with certain calculations in in respect

to the various forms of investment option available for the purpose of financing business. There

are certain limitation pertaining to the report which are:

The financial position of client is not available.

The client is having only intermediate level of financial knowledge.

No information in respect to how many of these investments the client can purchase or

invest into.

This report provides a clear insight into the various aspects of the investment in both

theoretical and the mathematical calculations.

ANALYSIS AND DISCUSSION

Difference between return on debt securities and equity securities

Both the forms of investment provide a good return but the they are different from each

other in terms of return. In case of debt securities which involves bonds, mortgages and so forth,

includes the return in terms of fixed percentage or the fixed amount in relation to interest. While

the equity investment which involves stocks comes along with a claim on the income of the

company. The debt instrument is less risky in comparison with the equity instrument but it offers

lower return and is consistent in nature (Cheung and et.al.,2017). It is less volatile as compared

to the equity securities. with less highs and lows than the securities exchange. The security and

loan market generally encounter less value changes, regardless, than stocks. Likewise, at the time

of liquidation the bondholders or the debt holders are paid first. Mortgage ventures, as other

obligation instruments, accompanied with the interest costs and are backed up by real estate

security.

On the other hand, in the equity investment, fortune can be made or lost. Any financial

exchange can be unstable, with the fast changing value of the stocks. Regularly, these wide value

swings are not founded on the strength of the association backing them up however is because of

political, social or legislative issues in the nation of origin of the organization. Equity securities

are an exemplary case of taking on higher danger of misfortune as a byproduct of possibly higher

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

prize. In the event of closure of business or winding up, the equity holders are paid after meeting

up with all the obligations of the business including payment to debt holders.

The debt funds are invested into the fixed income bearing securities while the equity funds

are invested in the share market. Each of these funds are having different characteristics which

determines how they behave (Grundy and Verwijmeren, 2020). It is dependent upon the need of

the investor before making an investment. For instance, some investors are interested in gaining

higher return in order to accomplish their goals which also includes undertaking higher risk. On

the other hand, some investors are least interested in taking risk for which they use debt

securities and it is also used for meeting the short term to medium term goals. Equity investment

can possibly offer better yields, yet with risk, while debt securities offer generally stable however

moderate to low returns.

Yield change through time but the coupon rate remains same

The investor is required to look into two important aspect before buying the bond which

are- yield to maturity and the coupon rate. Yield to maturity (YTM) refers to the rate of return on

the bond on the assumption that investor will hold the bond till its maturity. It is the whole of the

entirety of its residual coupon payment. A bonds YTM rises or falls relying upon its fairly

estimated worth and the number of installments left to be made. The coupon rate is the yearly

measure of interest amount that the owner of the security will get (BARKLEY, 2019). To

confuse things the coupon rate may likewise be called as the yield from the bond. The coupon

rate of eth bond security is fixed even if there is any change in the par or the face value of bond.

For example, the bond of $1000 face value (FV) issued at the semiannual payment of $10 each.

In order to determine the coupon rate, the yearly interest amount will be divided by the FV,

which is $10*2=$20, so the coupon rate is $20/$1000 = 2%. No matter what is the price of the

bond trades, but the interest amount will remain the same $20 and of the interest rate goes up the

value of bond will reduce to $980 but the 2% coupon rate will remain as is it is. This is the

reason why the yield changes with change in time but the coupon rate remains constant.

Types of risk and how it is affected by increase in the number of shares in the portfolio

There are majorly two types of risk, one is systematic risk and other is unsystematic risk.

The former is associated with the market return. It is considered as an inherent risk associated

with the stock market and is applicable all the sectors and industry and over which less or no

up with all the obligations of the business including payment to debt holders.

The debt funds are invested into the fixed income bearing securities while the equity funds

are invested in the share market. Each of these funds are having different characteristics which

determines how they behave (Grundy and Verwijmeren, 2020). It is dependent upon the need of

the investor before making an investment. For instance, some investors are interested in gaining

higher return in order to accomplish their goals which also includes undertaking higher risk. On

the other hand, some investors are least interested in taking risk for which they use debt

securities and it is also used for meeting the short term to medium term goals. Equity investment

can possibly offer better yields, yet with risk, while debt securities offer generally stable however

moderate to low returns.

Yield change through time but the coupon rate remains same

The investor is required to look into two important aspect before buying the bond which

are- yield to maturity and the coupon rate. Yield to maturity (YTM) refers to the rate of return on

the bond on the assumption that investor will hold the bond till its maturity. It is the whole of the

entirety of its residual coupon payment. A bonds YTM rises or falls relying upon its fairly

estimated worth and the number of installments left to be made. The coupon rate is the yearly

measure of interest amount that the owner of the security will get (BARKLEY, 2019). To

confuse things the coupon rate may likewise be called as the yield from the bond. The coupon

rate of eth bond security is fixed even if there is any change in the par or the face value of bond.

For example, the bond of $1000 face value (FV) issued at the semiannual payment of $10 each.

In order to determine the coupon rate, the yearly interest amount will be divided by the FV,

which is $10*2=$20, so the coupon rate is $20/$1000 = 2%. No matter what is the price of the

bond trades, but the interest amount will remain the same $20 and of the interest rate goes up the

value of bond will reduce to $980 but the 2% coupon rate will remain as is it is. This is the

reason why the yield changes with change in time but the coupon rate remains constant.

Types of risk and how it is affected by increase in the number of shares in the portfolio

There are majorly two types of risk, one is systematic risk and other is unsystematic risk.

The former is associated with the market return. It is considered as an inherent risk associated

with the stock market and is applicable all the sectors and industry and over which less or no

control can be exercised. The main source of such risk could be macroeconomic factors, for

example, inflation, changes in loan costs, variances in monetary standards, downturns, wars, and

so on Large scale factors which impact the direction and unpredictability of the whole market

would be systematic risk (Hassas and Sattari, 2017). An individual organization can't control the

risk. For example, if eth govt bonds is providing 5% yield as compared to share market which is

offering minimum 10% of return. Then all of a sudden, govt. announces additional tax of 1 per

cent on the stock market transaction. This is a systematic risk having an influence over all the

stocks consequently making the government bonds look more attractive. Thus, increasing the

number of shares leads to increase in risk.

Unsystematic risk is firm specific. These are the risk which are already existing but is very

much unpanned and can occur at any pint of time leading to disruption widely (GHALIBAF and

Salmalian, 2019). For instance, an investor purchases the shares of $10000 of 10 companies and

if any uncertain event occurs, leading to setback and few companies faces the reduction in the

share price, the investor will experience the loss. But on the other side, an investor, buys

$100000 worth of stock of just one company, would will experience 10 times loss because of the

occurrence of these events. It will result into increase in loss or gain which is uncertain.

applying the

Capital Asset Pricing Model (CAPM) to price risky securities

This model is based upon the principle that the only reason an investor would earn higher

on an average by making an investment into 1 stock instead of another. It offers the investors the

way of measuring the return that they deserve on an investment in return of putting their money

on risk. This model presents a relationship between the required rate of return and the systematic

risk associated with it, by using the formula Eri =Rf+βi * (ERm−Rf). The risk-free rate takes into

consideration the time value of money while the other factor accounts for the additional risk. The

beta in CAPM measures the level of risk in the investment (Rossi, 2016). If the stock is riskier

than the market then the beta will be more than 1 and on the other hand, if the beta is lower than

one, it means that the investment will minimize the risk of the portfolio. This help the investor in

evaluating whether the stock is overvalued or undervalued which is because of the volatility

existing n the market. Thus, investor makes use of CAPM model while evaluating the risky

securities.

example, inflation, changes in loan costs, variances in monetary standards, downturns, wars, and

so on Large scale factors which impact the direction and unpredictability of the whole market

would be systematic risk (Hassas and Sattari, 2017). An individual organization can't control the

risk. For example, if eth govt bonds is providing 5% yield as compared to share market which is

offering minimum 10% of return. Then all of a sudden, govt. announces additional tax of 1 per

cent on the stock market transaction. This is a systematic risk having an influence over all the

stocks consequently making the government bonds look more attractive. Thus, increasing the

number of shares leads to increase in risk.

Unsystematic risk is firm specific. These are the risk which are already existing but is very

much unpanned and can occur at any pint of time leading to disruption widely (GHALIBAF and

Salmalian, 2019). For instance, an investor purchases the shares of $10000 of 10 companies and

if any uncertain event occurs, leading to setback and few companies faces the reduction in the

share price, the investor will experience the loss. But on the other side, an investor, buys

$100000 worth of stock of just one company, would will experience 10 times loss because of the

occurrence of these events. It will result into increase in loss or gain which is uncertain.

applying the

Capital Asset Pricing Model (CAPM) to price risky securities

This model is based upon the principle that the only reason an investor would earn higher

on an average by making an investment into 1 stock instead of another. It offers the investors the

way of measuring the return that they deserve on an investment in return of putting their money

on risk. This model presents a relationship between the required rate of return and the systematic

risk associated with it, by using the formula Eri =Rf+βi * (ERm−Rf). The risk-free rate takes into

consideration the time value of money while the other factor accounts for the additional risk. The

beta in CAPM measures the level of risk in the investment (Rossi, 2016). If the stock is riskier

than the market then the beta will be more than 1 and on the other hand, if the beta is lower than

one, it means that the investment will minimize the risk of the portfolio. This help the investor in

evaluating whether the stock is overvalued or undervalued which is because of the volatility

existing n the market. Thus, investor makes use of CAPM model while evaluating the risky

securities.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

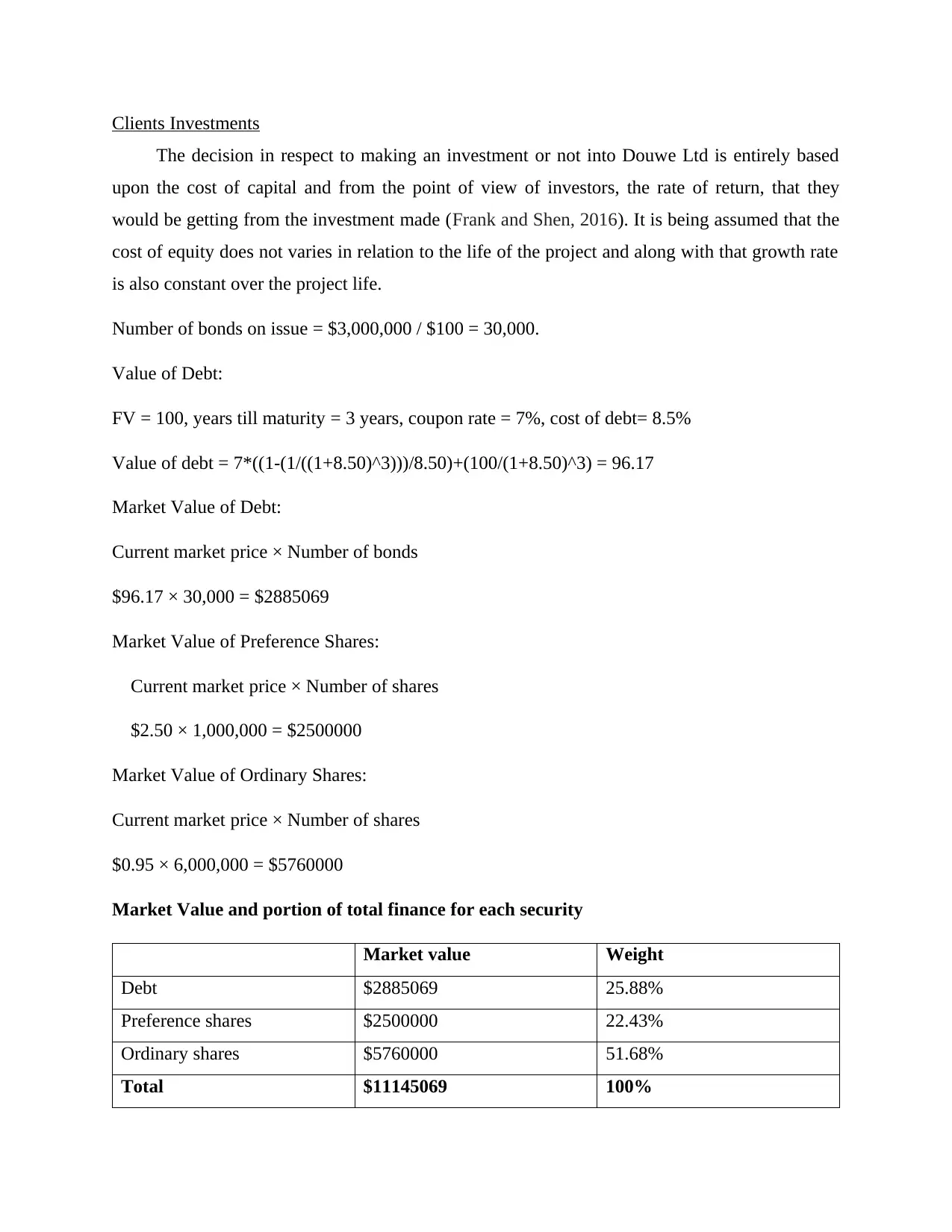

Clients Investments

The decision in respect to making an investment or not into Douwe Ltd is entirely based

upon the cost of capital and from the point of view of investors, the rate of return, that they

would be getting from the investment made (Frank and Shen, 2016). It is being assumed that the

cost of equity does not varies in relation to the life of the project and along with that growth rate

is also constant over the project life.

Number of bonds on issue = $3,000,000 / $100 = 30,000.

Value of Debt:

FV = 100, years till maturity = 3 years, coupon rate = 7%, cost of debt= 8.5%

Value of debt = 7*((1-(1/((1+8.50)^3)))/8.50)+(100/(1+8.50)^3) = 96.17

Market Value of Debt:

Current market price × Number of bonds

$96.17 × 30,000 = $2885069

Market Value of Preference Shares:

Current market price × Number of shares

$2.50 × 1,000,000 = $2500000

Market Value of Ordinary Shares:

Current market price × Number of shares

$0.95 × 6,000,000 = $5760000

Market Value and portion of total finance for each security

Market value Weight

Debt $2885069 25.88%

Preference shares $2500000 22.43%

Ordinary shares $5760000 51.68%

Total $11145069 100%

The decision in respect to making an investment or not into Douwe Ltd is entirely based

upon the cost of capital and from the point of view of investors, the rate of return, that they

would be getting from the investment made (Frank and Shen, 2016). It is being assumed that the

cost of equity does not varies in relation to the life of the project and along with that growth rate

is also constant over the project life.

Number of bonds on issue = $3,000,000 / $100 = 30,000.

Value of Debt:

FV = 100, years till maturity = 3 years, coupon rate = 7%, cost of debt= 8.5%

Value of debt = 7*((1-(1/((1+8.50)^3)))/8.50)+(100/(1+8.50)^3) = 96.17

Market Value of Debt:

Current market price × Number of bonds

$96.17 × 30,000 = $2885069

Market Value of Preference Shares:

Current market price × Number of shares

$2.50 × 1,000,000 = $2500000

Market Value of Ordinary Shares:

Current market price × Number of shares

$0.95 × 6,000,000 = $5760000

Market Value and portion of total finance for each security

Market value Weight

Debt $2885069 25.88%

Preference shares $2500000 22.43%

Ordinary shares $5760000 51.68%

Total $11145069 100%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

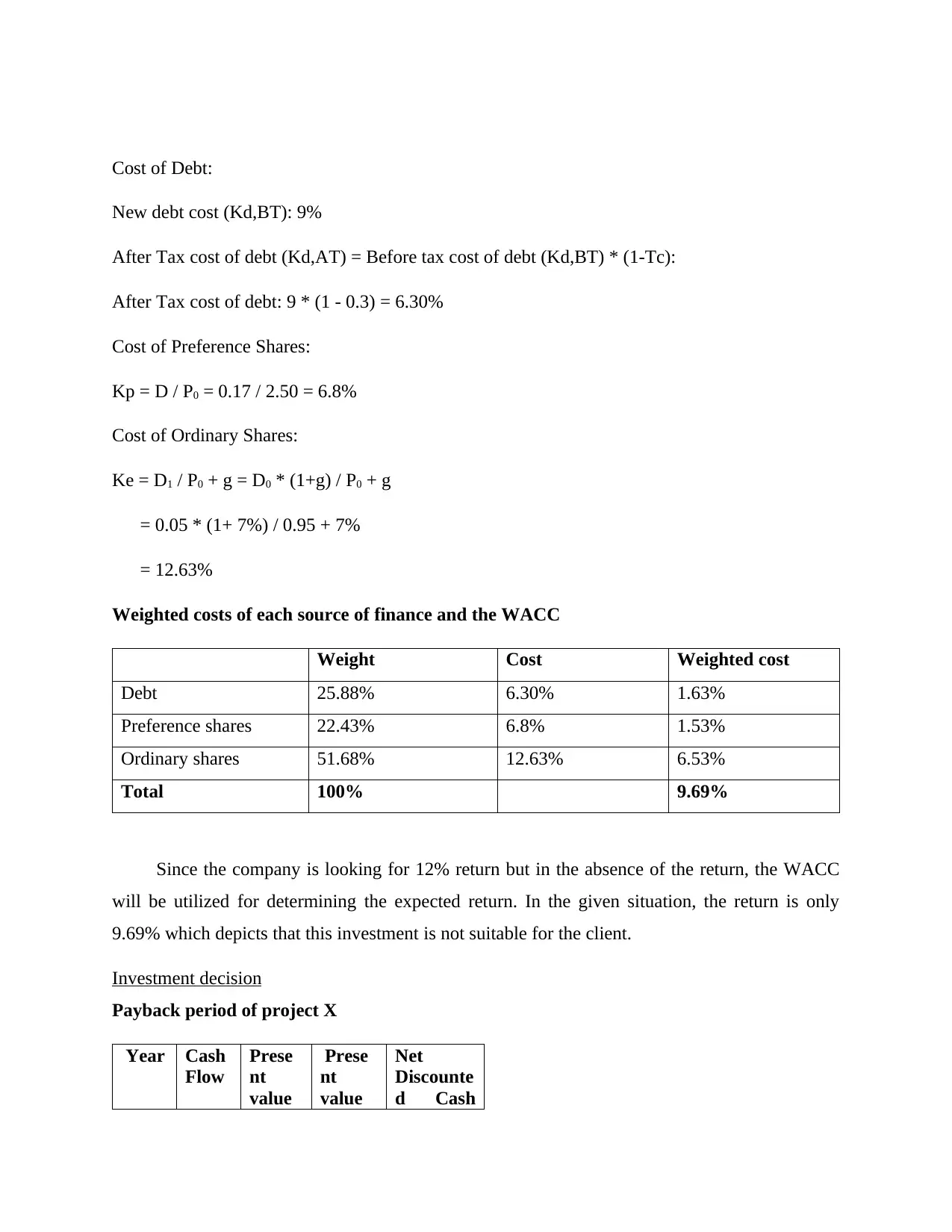

Cost of Debt:

New debt cost (Kd,BT): 9%

After Tax cost of debt (Kd,AT) = Before tax cost of debt (Kd,BT) * (1-Tc):

After Tax cost of debt: 9 * (1 - 0.3) = 6.30%

Cost of Preference Shares:

Kp = D / P0 = 0.17 / 2.50 = 6.8%

Cost of Ordinary Shares:

Ke = D1 / P0 + g = D0 * (1+g) / P0 + g

= 0.05 * (1+ 7%) / 0.95 + 7%

= 12.63%

Weighted costs of each source of finance and the WACC

Weight Cost Weighted cost

Debt 25.88% 6.30% 1.63%

Preference shares 22.43% 6.8% 1.53%

Ordinary shares 51.68% 12.63% 6.53%

Total 100% 9.69%

Since the company is looking for 12% return but in the absence of the return, the WACC

will be utilized for determining the expected return. In the given situation, the return is only

9.69% which depicts that this investment is not suitable for the client.

Investment decision

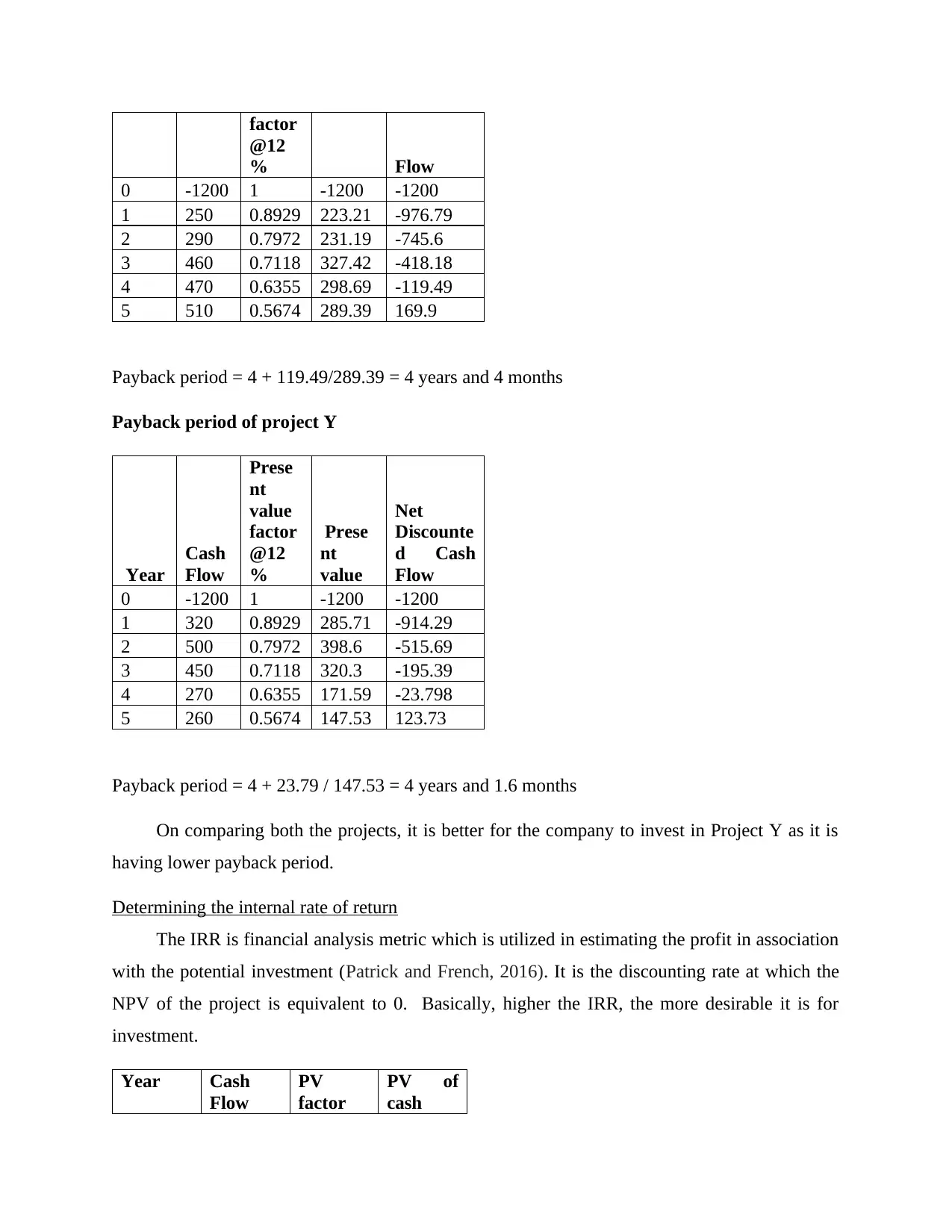

Payback period of project X

Year Cash

Flow

Prese

nt

value

Prese

nt

value

Net

Discounte

d Cash

New debt cost (Kd,BT): 9%

After Tax cost of debt (Kd,AT) = Before tax cost of debt (Kd,BT) * (1-Tc):

After Tax cost of debt: 9 * (1 - 0.3) = 6.30%

Cost of Preference Shares:

Kp = D / P0 = 0.17 / 2.50 = 6.8%

Cost of Ordinary Shares:

Ke = D1 / P0 + g = D0 * (1+g) / P0 + g

= 0.05 * (1+ 7%) / 0.95 + 7%

= 12.63%

Weighted costs of each source of finance and the WACC

Weight Cost Weighted cost

Debt 25.88% 6.30% 1.63%

Preference shares 22.43% 6.8% 1.53%

Ordinary shares 51.68% 12.63% 6.53%

Total 100% 9.69%

Since the company is looking for 12% return but in the absence of the return, the WACC

will be utilized for determining the expected return. In the given situation, the return is only

9.69% which depicts that this investment is not suitable for the client.

Investment decision

Payback period of project X

Year Cash

Flow

Prese

nt

value

Prese

nt

value

Net

Discounte

d Cash

factor

@12

% Flow

0 -1200 1 -1200 -1200

1 250 0.8929 223.21 -976.79

2 290 0.7972 231.19 -745.6

3 460 0.7118 327.42 -418.18

4 470 0.6355 298.69 -119.49

5 510 0.5674 289.39 169.9

Payback period = 4 + 119.49/289.39 = 4 years and 4 months

Payback period of project Y

Year

Cash

Flow

Prese

nt

value

factor

@12

%

Prese

nt

value

Net

Discounte

d Cash

Flow

0 -1200 1 -1200 -1200

1 320 0.8929 285.71 -914.29

2 500 0.7972 398.6 -515.69

3 450 0.7118 320.3 -195.39

4 270 0.6355 171.59 -23.798

5 260 0.5674 147.53 123.73

Payback period = 4 + 23.79 / 147.53 = 4 years and 1.6 months

On comparing both the projects, it is better for the company to invest in Project Y as it is

having lower payback period.

Determining the internal rate of return

The IRR is financial analysis metric which is utilized in estimating the profit in association

with the potential investment (Patrick and French, 2016). It is the discounting rate at which the

NPV of the project is equivalent to 0. Basically, higher the IRR, the more desirable it is for

investment.

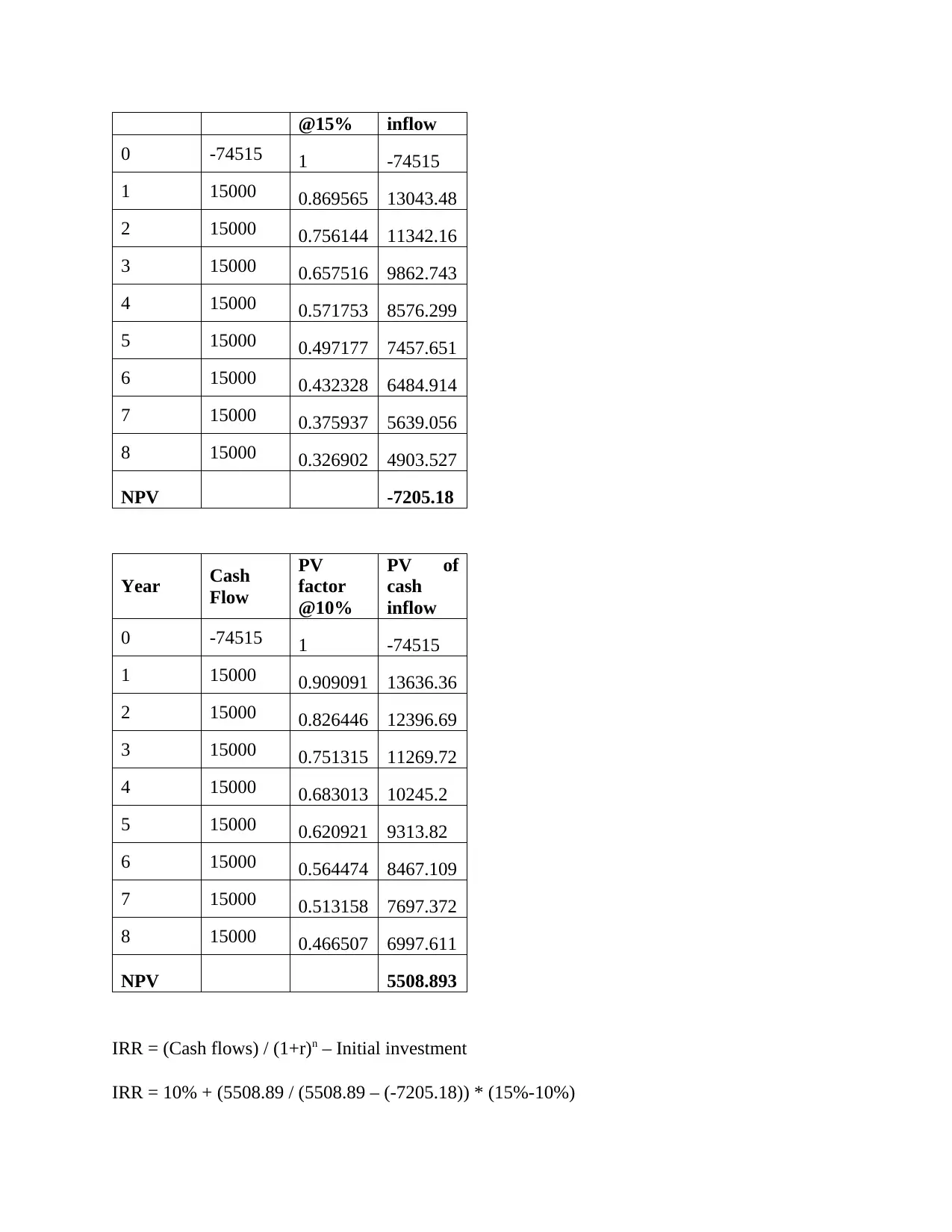

Year Cash

Flow

PV

factor

PV of

cash

@12

% Flow

0 -1200 1 -1200 -1200

1 250 0.8929 223.21 -976.79

2 290 0.7972 231.19 -745.6

3 460 0.7118 327.42 -418.18

4 470 0.6355 298.69 -119.49

5 510 0.5674 289.39 169.9

Payback period = 4 + 119.49/289.39 = 4 years and 4 months

Payback period of project Y

Year

Cash

Flow

Prese

nt

value

factor

@12

%

Prese

nt

value

Net

Discounte

d Cash

Flow

0 -1200 1 -1200 -1200

1 320 0.8929 285.71 -914.29

2 500 0.7972 398.6 -515.69

3 450 0.7118 320.3 -195.39

4 270 0.6355 171.59 -23.798

5 260 0.5674 147.53 123.73

Payback period = 4 + 23.79 / 147.53 = 4 years and 1.6 months

On comparing both the projects, it is better for the company to invest in Project Y as it is

having lower payback period.

Determining the internal rate of return

The IRR is financial analysis metric which is utilized in estimating the profit in association

with the potential investment (Patrick and French, 2016). It is the discounting rate at which the

NPV of the project is equivalent to 0. Basically, higher the IRR, the more desirable it is for

investment.

Year Cash

Flow

PV

factor

PV of

cash

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

@15% inflow

0 -74515 1 -74515

1 15000 0.869565 13043.48

2 15000 0.756144 11342.16

3 15000 0.657516 9862.743

4 15000 0.571753 8576.299

5 15000 0.497177 7457.651

6 15000 0.432328 6484.914

7 15000 0.375937 5639.056

8 15000 0.326902 4903.527

NPV -7205.18

Year Cash

Flow

PV

factor

@10%

PV of

cash

inflow

0 -74515 1 -74515

1 15000 0.909091 13636.36

2 15000 0.826446 12396.69

3 15000 0.751315 11269.72

4 15000 0.683013 10245.2

5 15000 0.620921 9313.82

6 15000 0.564474 8467.109

7 15000 0.513158 7697.372

8 15000 0.466507 6997.611

NPV 5508.893

IRR = (Cash flows) / (1+r)n – Initial investment

IRR = 10% + (5508.89 / (5508.89 – (-7205.18)) * (15%-10%)

0 -74515 1 -74515

1 15000 0.869565 13043.48

2 15000 0.756144 11342.16

3 15000 0.657516 9862.743

4 15000 0.571753 8576.299

5 15000 0.497177 7457.651

6 15000 0.432328 6484.914

7 15000 0.375937 5639.056

8 15000 0.326902 4903.527

NPV -7205.18

Year Cash

Flow

PV

factor

@10%

PV of

cash

inflow

0 -74515 1 -74515

1 15000 0.909091 13636.36

2 15000 0.826446 12396.69

3 15000 0.751315 11269.72

4 15000 0.683013 10245.2

5 15000 0.620921 9313.82

6 15000 0.564474 8467.109

7 15000 0.513158 7697.372

8 15000 0.466507 6997.611

NPV 5508.893

IRR = (Cash flows) / (1+r)n – Initial investment

IRR = 10% + (5508.89 / (5508.89 – (-7205.18)) * (15%-10%)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

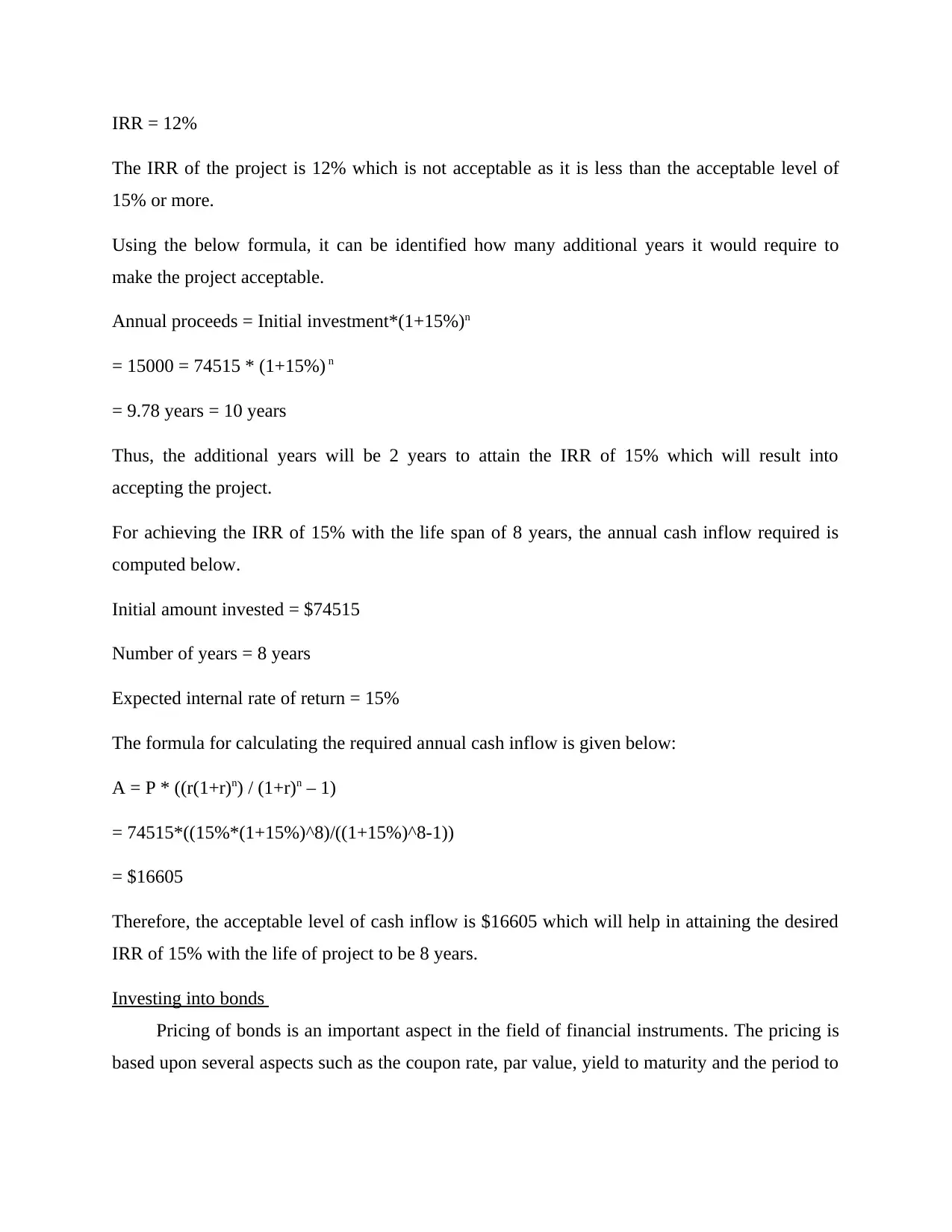

IRR = 12%

The IRR of the project is 12% which is not acceptable as it is less than the acceptable level of

15% or more.

Using the below formula, it can be identified how many additional years it would require to

make the project acceptable.

Annual proceeds = Initial investment*(1+15%)n

= 15000 = 74515 * (1+15%) n

= 9.78 years = 10 years

Thus, the additional years will be 2 years to attain the IRR of 15% which will result into

accepting the project.

For achieving the IRR of 15% with the life span of 8 years, the annual cash inflow required is

computed below.

Initial amount invested = $74515

Number of years = 8 years

Expected internal rate of return = 15%

The formula for calculating the required annual cash inflow is given below:

A = P * ((r(1+r)n) / (1+r)n – 1)

= 74515*((15%*(1+15%)^8)/((1+15%)^8-1))

= $16605

Therefore, the acceptable level of cash inflow is $16605 which will help in attaining the desired

IRR of 15% with the life of project to be 8 years.

Investing into bonds

Pricing of bonds is an important aspect in the field of financial instruments. The pricing is

based upon several aspects such as the coupon rate, par value, yield to maturity and the period to

The IRR of the project is 12% which is not acceptable as it is less than the acceptable level of

15% or more.

Using the below formula, it can be identified how many additional years it would require to

make the project acceptable.

Annual proceeds = Initial investment*(1+15%)n

= 15000 = 74515 * (1+15%) n

= 9.78 years = 10 years

Thus, the additional years will be 2 years to attain the IRR of 15% which will result into

accepting the project.

For achieving the IRR of 15% with the life span of 8 years, the annual cash inflow required is

computed below.

Initial amount invested = $74515

Number of years = 8 years

Expected internal rate of return = 15%

The formula for calculating the required annual cash inflow is given below:

A = P * ((r(1+r)n) / (1+r)n – 1)

= 74515*((15%*(1+15%)^8)/((1+15%)^8-1))

= $16605

Therefore, the acceptable level of cash inflow is $16605 which will help in attaining the desired

IRR of 15% with the life of project to be 8 years.

Investing into bonds

Pricing of bonds is an important aspect in the field of financial instruments. The pricing is

based upon several aspects such as the coupon rate, par value, yield to maturity and the period to

maturity (What is Bond Pricing? 2020). Each bond comes with a price which is required to be

repaid at the maturity. Without the par value or the principle value the bond will be of no use.

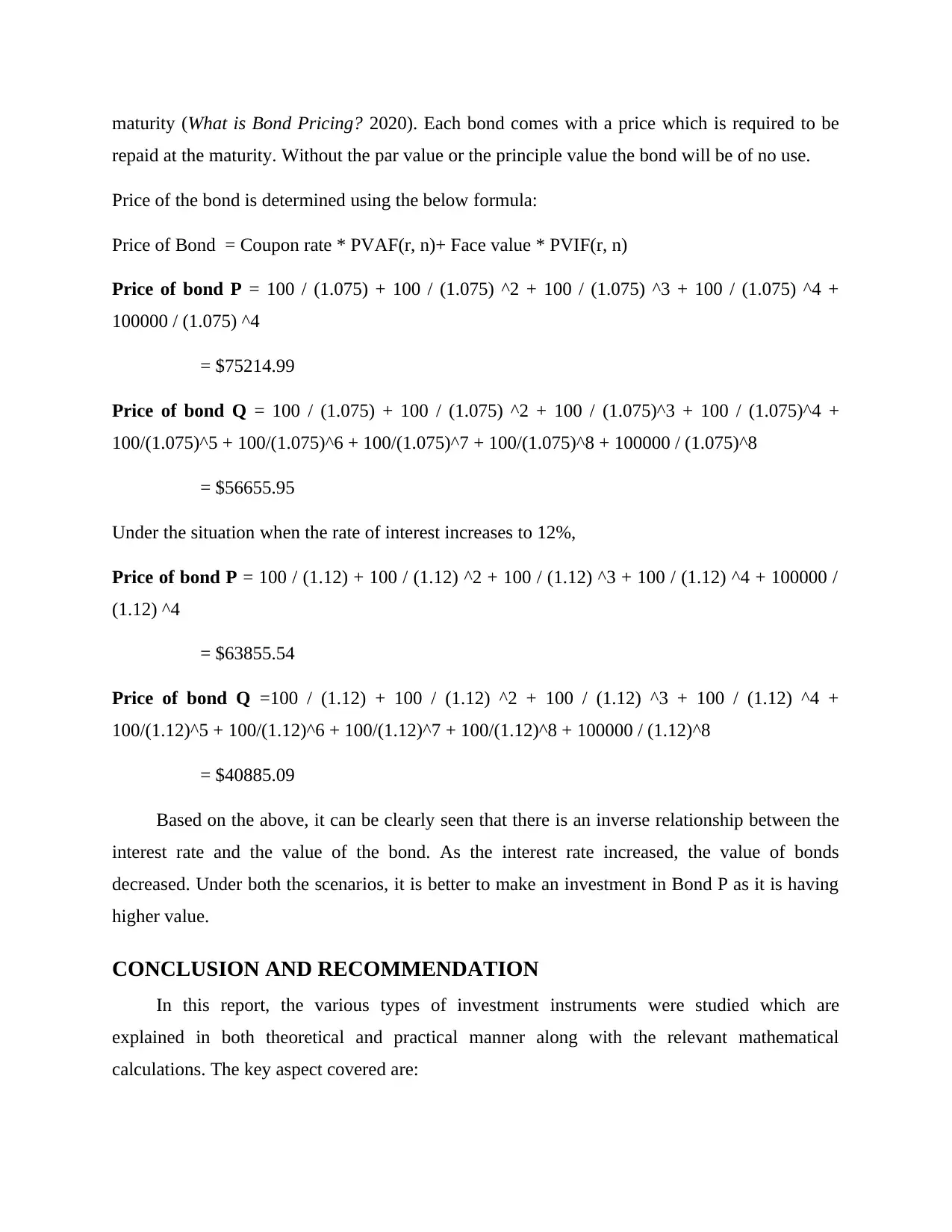

Price of the bond is determined using the below formula:

Price of Bond = Coupon rate * PVAF(r, n)+ Face value * PVIF(r, n)

Price of bond P = 100 / (1.075) + 100 / (1.075) ^2 + 100 / (1.075) ^3 + 100 / (1.075) ^4 +

100000 / (1.075) ^4

= $75214.99

Price of bond Q = 100 / (1.075) + 100 / (1.075) ^2 + 100 / (1.075)^3 + 100 / (1.075)^4 +

100/(1.075)^5 + 100/(1.075)^6 + 100/(1.075)^7 + 100/(1.075)^8 + 100000 / (1.075)^8

= $56655.95

Under the situation when the rate of interest increases to 12%,

Price of bond P = 100 / (1.12) + 100 / (1.12) ^2 + 100 / (1.12) ^3 + 100 / (1.12) ^4 + 100000 /

(1.12) ^4

= $63855.54

Price of bond Q =100 / (1.12) + 100 / (1.12) ^2 + 100 / (1.12) ^3 + 100 / (1.12) ^4 +

100/(1.12)^5 + 100/(1.12)^6 + 100/(1.12)^7 + 100/(1.12)^8 + 100000 / (1.12)^8

= $40885.09

Based on the above, it can be clearly seen that there is an inverse relationship between the

interest rate and the value of the bond. As the interest rate increased, the value of bonds

decreased. Under both the scenarios, it is better to make an investment in Bond P as it is having

higher value.

CONCLUSION AND RECOMMENDATION

In this report, the various types of investment instruments were studied which are

explained in both theoretical and practical manner along with the relevant mathematical

calculations. The key aspect covered are:

repaid at the maturity. Without the par value or the principle value the bond will be of no use.

Price of the bond is determined using the below formula:

Price of Bond = Coupon rate * PVAF(r, n)+ Face value * PVIF(r, n)

Price of bond P = 100 / (1.075) + 100 / (1.075) ^2 + 100 / (1.075) ^3 + 100 / (1.075) ^4 +

100000 / (1.075) ^4

= $75214.99

Price of bond Q = 100 / (1.075) + 100 / (1.075) ^2 + 100 / (1.075)^3 + 100 / (1.075)^4 +

100/(1.075)^5 + 100/(1.075)^6 + 100/(1.075)^7 + 100/(1.075)^8 + 100000 / (1.075)^8

= $56655.95

Under the situation when the rate of interest increases to 12%,

Price of bond P = 100 / (1.12) + 100 / (1.12) ^2 + 100 / (1.12) ^3 + 100 / (1.12) ^4 + 100000 /

(1.12) ^4

= $63855.54

Price of bond Q =100 / (1.12) + 100 / (1.12) ^2 + 100 / (1.12) ^3 + 100 / (1.12) ^4 +

100/(1.12)^5 + 100/(1.12)^6 + 100/(1.12)^7 + 100/(1.12)^8 + 100000 / (1.12)^8

= $40885.09

Based on the above, it can be clearly seen that there is an inverse relationship between the

interest rate and the value of the bond. As the interest rate increased, the value of bonds

decreased. Under both the scenarios, it is better to make an investment in Bond P as it is having

higher value.

CONCLUSION AND RECOMMENDATION

In this report, the various types of investment instruments were studied which are

explained in both theoretical and practical manner along with the relevant mathematical

calculations. The key aspect covered are:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The different between the return on debt and equity.

Reason why yield change and coupon rate being constant.

Identifying various types of risks and its impact.

Use of CAPM model to price the risky securities.

It is recommended that for the purpose of investment, it is better to gain more knowledge and

understanding along with important calculations in order to make a right decision pertaining to

the investment to be made.

Reason why yield change and coupon rate being constant.

Identifying various types of risks and its impact.

Use of CAPM model to price the risky securities.

It is recommended that for the purpose of investment, it is better to gain more knowledge and

understanding along with important calculations in order to make a right decision pertaining to

the investment to be made.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

BARKLEY, T., 2019. Interest Rate Risk, Measurement, and Management. Debt Markets and

Investments, p.41.

Cheung, W. M., and et.al.,2017, April. The effect of stock liquidity on debt-equity choices.

In China International Conference in Finance.

Frank, M. Z. and Shen, T., 2016. Investment and the weighted average cost of capital. Journal of

Financial Economics. 119(2). pp.300-315.

GHALIBAF, A. H. and Salmalian, S., 2019. A comparison of fundamental and historical beta in

assessment of systematic risk Evidence from Tehran Security Exchange.

Grundy, B. D. and Verwijmeren, P., 2020. The external financing of investment. Journal of

Corporate Finance. p.101745.

Hassas, Y. Y. and Sattari, H., 2017. Studing the relationship between unsystematic risk

fluctuations and noise trading.

Patrick, M. and French, N., 2016. The internal rate of return (IRR): projections, benchmarks and

pitfalls. Journal of Property Investment & Finance.

Rossi, M., 2016. The capital asset pricing model: a critical literature review. Global Business

and Economics Review. 18(5). pp.604-617.

Online

What is Bond Pricing? 2020. [Online]. Available Through:<

https://corporatefinanceinstitute.com/resources/knowledge/trading-investing/bond-

pricing/ >.

Books and Journals

BARKLEY, T., 2019. Interest Rate Risk, Measurement, and Management. Debt Markets and

Investments, p.41.

Cheung, W. M., and et.al.,2017, April. The effect of stock liquidity on debt-equity choices.

In China International Conference in Finance.

Frank, M. Z. and Shen, T., 2016. Investment and the weighted average cost of capital. Journal of

Financial Economics. 119(2). pp.300-315.

GHALIBAF, A. H. and Salmalian, S., 2019. A comparison of fundamental and historical beta in

assessment of systematic risk Evidence from Tehran Security Exchange.

Grundy, B. D. and Verwijmeren, P., 2020. The external financing of investment. Journal of

Corporate Finance. p.101745.

Hassas, Y. Y. and Sattari, H., 2017. Studing the relationship between unsystematic risk

fluctuations and noise trading.

Patrick, M. and French, N., 2016. The internal rate of return (IRR): projections, benchmarks and

pitfalls. Journal of Property Investment & Finance.

Rossi, M., 2016. The capital asset pricing model: a critical literature review. Global Business

and Economics Review. 18(5). pp.604-617.

Online

What is Bond Pricing? 2020. [Online]. Available Through:<

https://corporatefinanceinstitute.com/resources/knowledge/trading-investing/bond-

pricing/ >.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.