Comparison of Payback Period and Net Present Value for Business Finance Projects

VerifiedAdded on 2023/06/16

|19

|3950

|285

AI Summary

This report discusses the importance of business finance and how to compare different projects based on their payback period and net present value. It includes a detailed analysis of seven different projects and their rankings based on these two factors. The report also highlights the concept of mutually exclusive projects and how to choose between them.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Business Finance

1

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

TASK A:.................................................................................................................................3

TASK B................................................................................................................................12

TASK C................................................................................................................................13

TASK 4

Comparison between centralised and decentralised procurement and their benefits. 15

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................18

2

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

TASK A:.................................................................................................................................3

TASK B................................................................................................................................12

TASK C................................................................................................................................13

TASK 4

Comparison between centralised and decentralised procurement and their benefits. 15

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................18

2

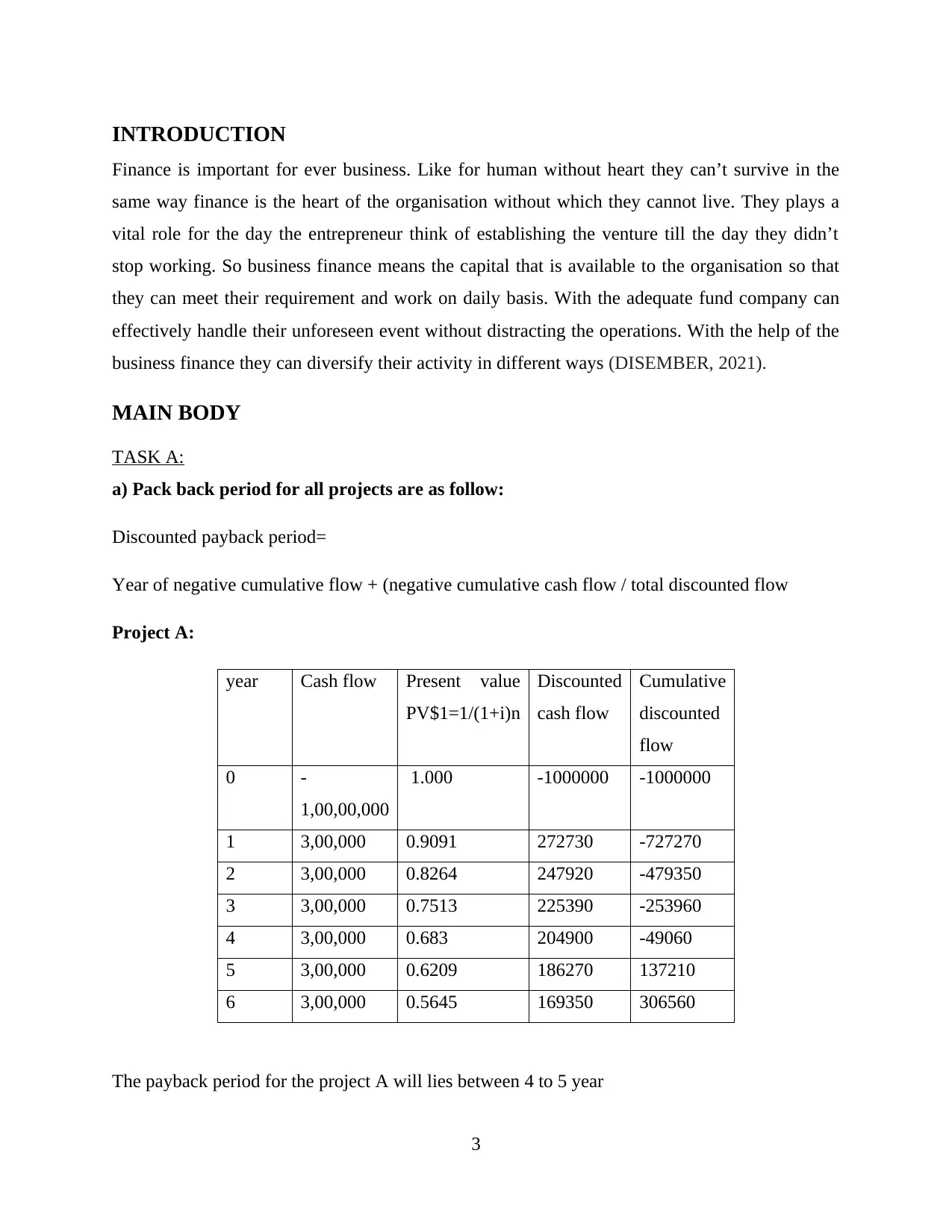

INTRODUCTION

Finance is important for ever business. Like for human without heart they can’t survive in the

same way finance is the heart of the organisation without which they cannot live. They plays a

vital role for the day the entrepreneur think of establishing the venture till the day they didn’t

stop working. So business finance means the capital that is available to the organisation so that

they can meet their requirement and work on daily basis. With the adequate fund company can

effectively handle their unforeseen event without distracting the operations. With the help of the

business finance they can diversify their activity in different ways (DISEMBER, 2021).

MAIN BODY

TASK A:

a) Pack back period for all projects are as follow:

Discounted payback period=

Year of negative cumulative flow + (negative cumulative cash flow / total discounted flow

Project A:

year Cash flow Present value

PV$1=1/(1+i)n

Discounted

cash flow

Cumulative

discounted

flow

0 -

1,00,00,000

1.000 -1000000 -1000000

1 3,00,000 0.9091 272730 -727270

2 3,00,000 0.8264 247920 -479350

3 3,00,000 0.7513 225390 -253960

4 3,00,000 0.683 204900 -49060

5 3,00,000 0.6209 186270 137210

6 3,00,000 0.5645 169350 306560

The payback period for the project A will lies between 4 to 5 year

3

Finance is important for ever business. Like for human without heart they can’t survive in the

same way finance is the heart of the organisation without which they cannot live. They plays a

vital role for the day the entrepreneur think of establishing the venture till the day they didn’t

stop working. So business finance means the capital that is available to the organisation so that

they can meet their requirement and work on daily basis. With the adequate fund company can

effectively handle their unforeseen event without distracting the operations. With the help of the

business finance they can diversify their activity in different ways (DISEMBER, 2021).

MAIN BODY

TASK A:

a) Pack back period for all projects are as follow:

Discounted payback period=

Year of negative cumulative flow + (negative cumulative cash flow / total discounted flow

Project A:

year Cash flow Present value

PV$1=1/(1+i)n

Discounted

cash flow

Cumulative

discounted

flow

0 -

1,00,00,000

1.000 -1000000 -1000000

1 3,00,000 0.9091 272730 -727270

2 3,00,000 0.8264 247920 -479350

3 3,00,000 0.7513 225390 -253960

4 3,00,000 0.683 204900 -49060

5 3,00,000 0.6209 186270 137210

6 3,00,000 0.5645 169350 306560

The payback period for the project A will lies between 4 to 5 year

3

Project A = 4 + (-49060 / 169350)

= 4.24 years.

Project B:

Year Cash

flow

Present value

PV$1=1/(1+i)

n

Discounted

cash flow

Cumulative

discounted

flow

0 -

400000

1 -400000 -400000

1 100000 0.9091 90910 -309090

2 100000 0.8264 82640 -226450

3 100000 0.7513 75130 -151320

4 100000 0.683 68300 -83020

Discounted payback period= cannot be determine because the project end before the income

receive.

Project C:

Year Cash

flow

Present value

PV$1=1/(1+i)

n

Discounted

cash flow

Cumulative

discounted

flow

0 -

700000

1 -700000 -700000

1 200000 0.9091 181820 -518180

2 200000 0.8264 165280 -352900

3 200000 0.7513 150260 -202640

4 200000 0.683 136600 -66040

5 200000 0.6209 124180 58140

Payback period = 4 + (-66040 /124180)

= 4.53

Project D:

4

= 4.24 years.

Project B:

Year Cash

flow

Present value

PV$1=1/(1+i)

n

Discounted

cash flow

Cumulative

discounted

flow

0 -

400000

1 -400000 -400000

1 100000 0.9091 90910 -309090

2 100000 0.8264 82640 -226450

3 100000 0.7513 75130 -151320

4 100000 0.683 68300 -83020

Discounted payback period= cannot be determine because the project end before the income

receive.

Project C:

Year Cash

flow

Present value

PV$1=1/(1+i)

n

Discounted

cash flow

Cumulative

discounted

flow

0 -

700000

1 -700000 -700000

1 200000 0.9091 181820 -518180

2 200000 0.8264 165280 -352900

3 200000 0.7513 150260 -202640

4 200000 0.683 136600 -66040

5 200000 0.6209 124180 58140

Payback period = 4 + (-66040 /124180)

= 4.53

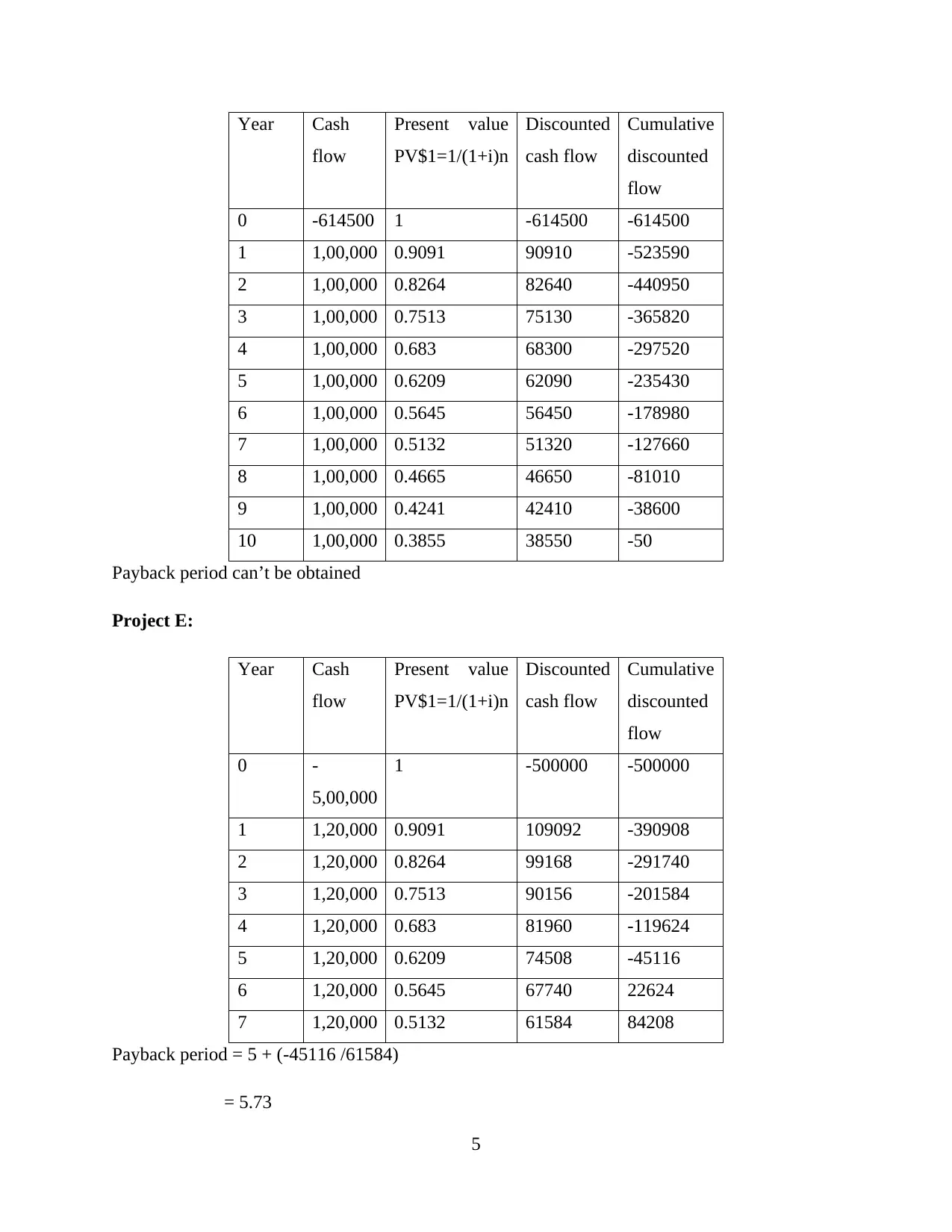

Project D:

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Year Cash

flow

Present value

PV$1=1/(1+i)n

Discounted

cash flow

Cumulative

discounted

flow

0 -614500 1 -614500 -614500

1 1,00,000 0.9091 90910 -523590

2 1,00,000 0.8264 82640 -440950

3 1,00,000 0.7513 75130 -365820

4 1,00,000 0.683 68300 -297520

5 1,00,000 0.6209 62090 -235430

6 1,00,000 0.5645 56450 -178980

7 1,00,000 0.5132 51320 -127660

8 1,00,000 0.4665 46650 -81010

9 1,00,000 0.4241 42410 -38600

10 1,00,000 0.3855 38550 -50

Payback period can’t be obtained

Project E:

Year Cash

flow

Present value

PV$1=1/(1+i)n

Discounted

cash flow

Cumulative

discounted

flow

0 -

5,00,000

1 -500000 -500000

1 1,20,000 0.9091 109092 -390908

2 1,20,000 0.8264 99168 -291740

3 1,20,000 0.7513 90156 -201584

4 1,20,000 0.683 81960 -119624

5 1,20,000 0.6209 74508 -45116

6 1,20,000 0.5645 67740 22624

7 1,20,000 0.5132 61584 84208

Payback period = 5 + (-45116 /61584)

= 5.73

5

flow

Present value

PV$1=1/(1+i)n

Discounted

cash flow

Cumulative

discounted

flow

0 -614500 1 -614500 -614500

1 1,00,000 0.9091 90910 -523590

2 1,00,000 0.8264 82640 -440950

3 1,00,000 0.7513 75130 -365820

4 1,00,000 0.683 68300 -297520

5 1,00,000 0.6209 62090 -235430

6 1,00,000 0.5645 56450 -178980

7 1,00,000 0.5132 51320 -127660

8 1,00,000 0.4665 46650 -81010

9 1,00,000 0.4241 42410 -38600

10 1,00,000 0.3855 38550 -50

Payback period can’t be obtained

Project E:

Year Cash

flow

Present value

PV$1=1/(1+i)n

Discounted

cash flow

Cumulative

discounted

flow

0 -

5,00,000

1 -500000 -500000

1 1,20,000 0.9091 109092 -390908

2 1,20,000 0.8264 99168 -291740

3 1,20,000 0.7513 90156 -201584

4 1,20,000 0.683 81960 -119624

5 1,20,000 0.6209 74508 -45116

6 1,20,000 0.5645 67740 22624

7 1,20,000 0.5132 61584 84208

Payback period = 5 + (-45116 /61584)

= 5.73

5

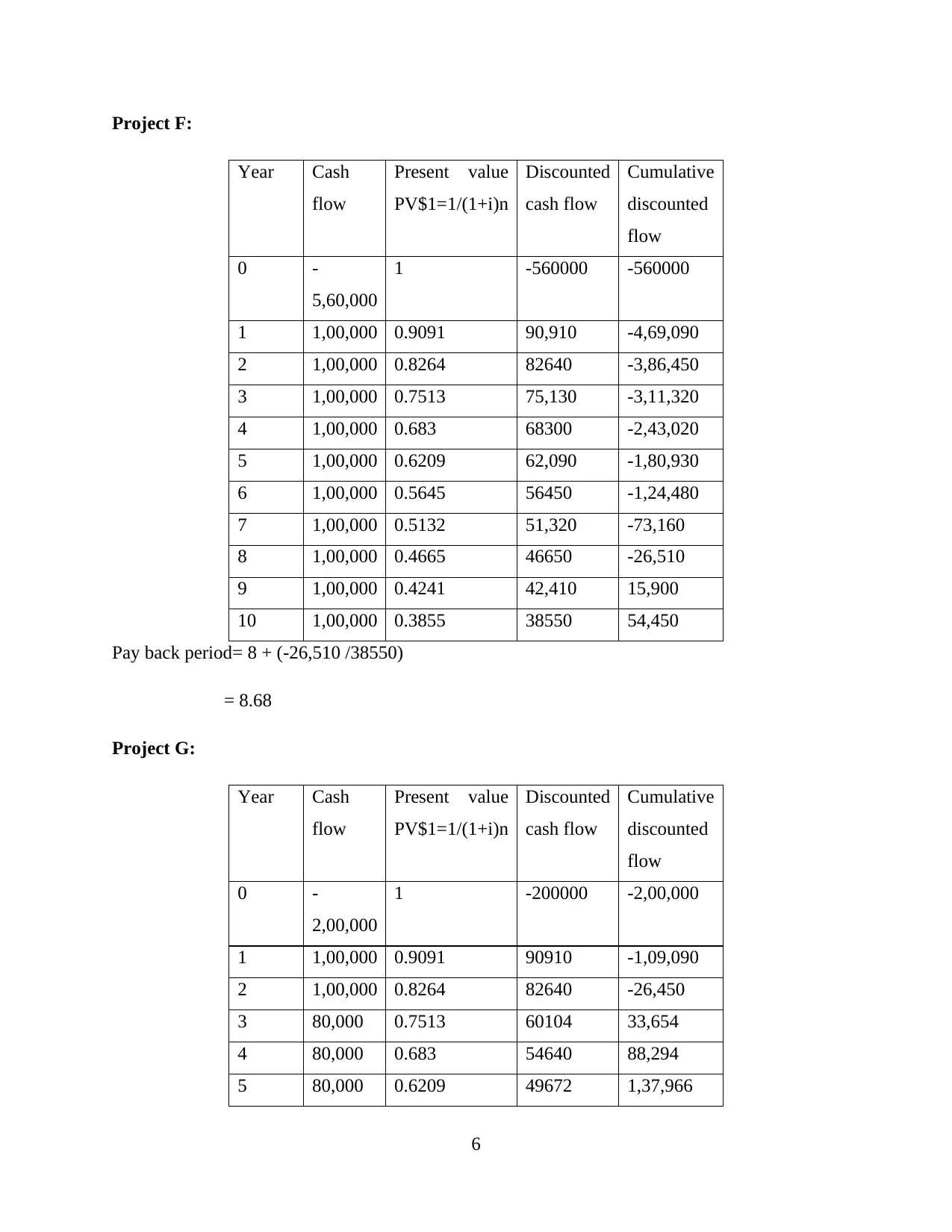

Project F:

Year Cash

flow

Present value

PV$1=1/(1+i)n

Discounted

cash flow

Cumulative

discounted

flow

0 -

5,60,000

1 -560000 -560000

1 1,00,000 0.9091 90,910 -4,69,090

2 1,00,000 0.8264 82640 -3,86,450

3 1,00,000 0.7513 75,130 -3,11,320

4 1,00,000 0.683 68300 -2,43,020

5 1,00,000 0.6209 62,090 -1,80,930

6 1,00,000 0.5645 56450 -1,24,480

7 1,00,000 0.5132 51,320 -73,160

8 1,00,000 0.4665 46650 -26,510

9 1,00,000 0.4241 42,410 15,900

10 1,00,000 0.3855 38550 54,450

Pay back period= 8 + (-26,510 /38550)

= 8.68

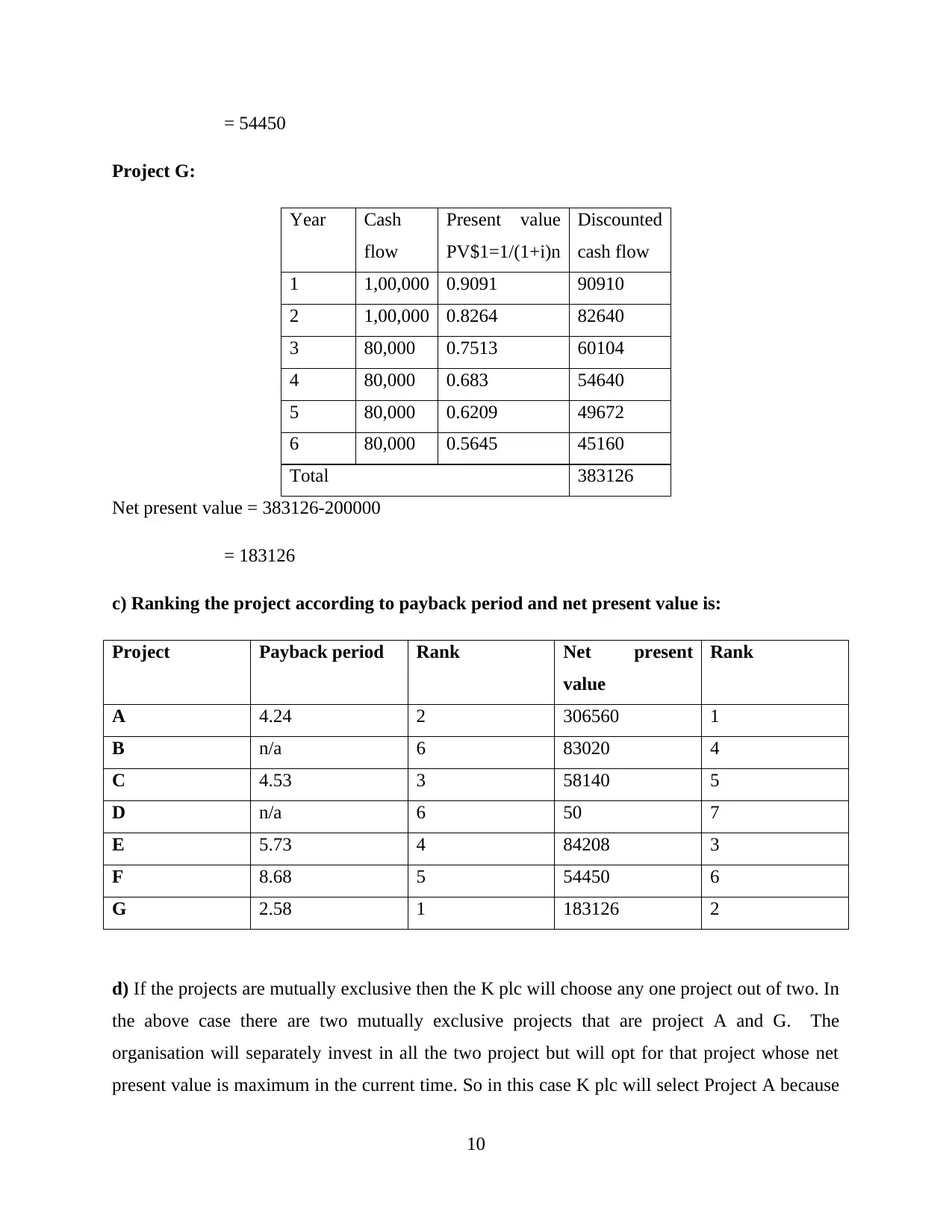

Project G:

Year Cash

flow

Present value

PV$1=1/(1+i)n

Discounted

cash flow

Cumulative

discounted

flow

0 -

2,00,000

1 -200000 -2,00,000

1 1,00,000 0.9091 90910 -1,09,090

2 1,00,000 0.8264 82640 -26,450

3 80,000 0.7513 60104 33,654

4 80,000 0.683 54640 88,294

5 80,000 0.6209 49672 1,37,966

6

Year Cash

flow

Present value

PV$1=1/(1+i)n

Discounted

cash flow

Cumulative

discounted

flow

0 -

5,60,000

1 -560000 -560000

1 1,00,000 0.9091 90,910 -4,69,090

2 1,00,000 0.8264 82640 -3,86,450

3 1,00,000 0.7513 75,130 -3,11,320

4 1,00,000 0.683 68300 -2,43,020

5 1,00,000 0.6209 62,090 -1,80,930

6 1,00,000 0.5645 56450 -1,24,480

7 1,00,000 0.5132 51,320 -73,160

8 1,00,000 0.4665 46650 -26,510

9 1,00,000 0.4241 42,410 15,900

10 1,00,000 0.3855 38550 54,450

Pay back period= 8 + (-26,510 /38550)

= 8.68

Project G:

Year Cash

flow

Present value

PV$1=1/(1+i)n

Discounted

cash flow

Cumulative

discounted

flow

0 -

2,00,000

1 -200000 -2,00,000

1 1,00,000 0.9091 90910 -1,09,090

2 1,00,000 0.8264 82640 -26,450

3 80,000 0.7513 60104 33,654

4 80,000 0.683 54640 88,294

5 80,000 0.6209 49672 1,37,966

6

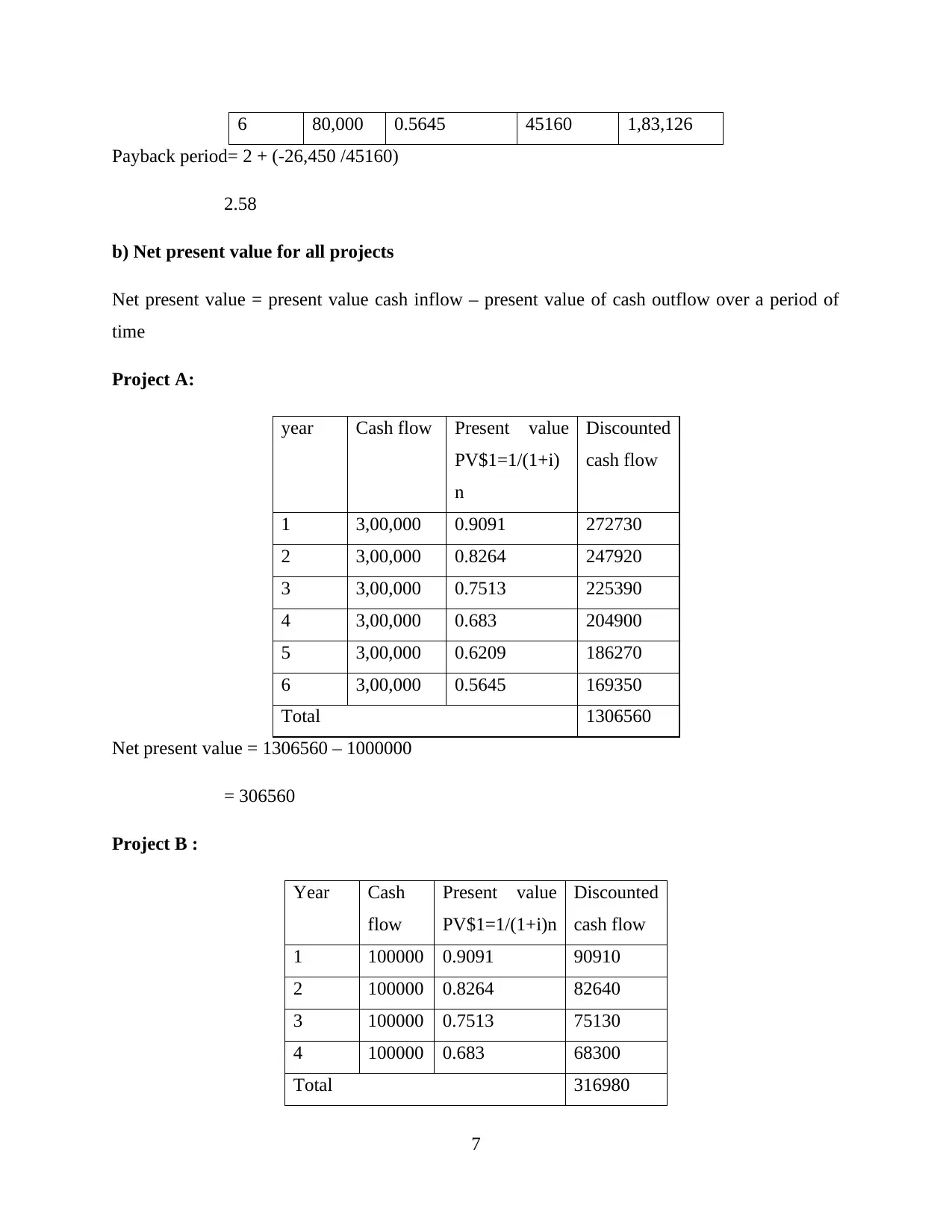

6 80,000 0.5645 45160 1,83,126

Payback period= 2 + (-26,450 /45160)

2.58

b) Net present value for all projects

Net present value = present value cash inflow – present value of cash outflow over a period of

time

Project A:

year Cash flow Present value

PV$1=1/(1+i)

n

Discounted

cash flow

1 3,00,000 0.9091 272730

2 3,00,000 0.8264 247920

3 3,00,000 0.7513 225390

4 3,00,000 0.683 204900

5 3,00,000 0.6209 186270

6 3,00,000 0.5645 169350

Total 1306560

Net present value = 1306560 – 1000000

= 306560

Project B :

Year Cash

flow

Present value

PV$1=1/(1+i)n

Discounted

cash flow

1 100000 0.9091 90910

2 100000 0.8264 82640

3 100000 0.7513 75130

4 100000 0.683 68300

Total 316980

7

Payback period= 2 + (-26,450 /45160)

2.58

b) Net present value for all projects

Net present value = present value cash inflow – present value of cash outflow over a period of

time

Project A:

year Cash flow Present value

PV$1=1/(1+i)

n

Discounted

cash flow

1 3,00,000 0.9091 272730

2 3,00,000 0.8264 247920

3 3,00,000 0.7513 225390

4 3,00,000 0.683 204900

5 3,00,000 0.6209 186270

6 3,00,000 0.5645 169350

Total 1306560

Net present value = 1306560 – 1000000

= 306560

Project B :

Year Cash

flow

Present value

PV$1=1/(1+i)n

Discounted

cash flow

1 100000 0.9091 90910

2 100000 0.8264 82640

3 100000 0.7513 75130

4 100000 0.683 68300

Total 316980

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

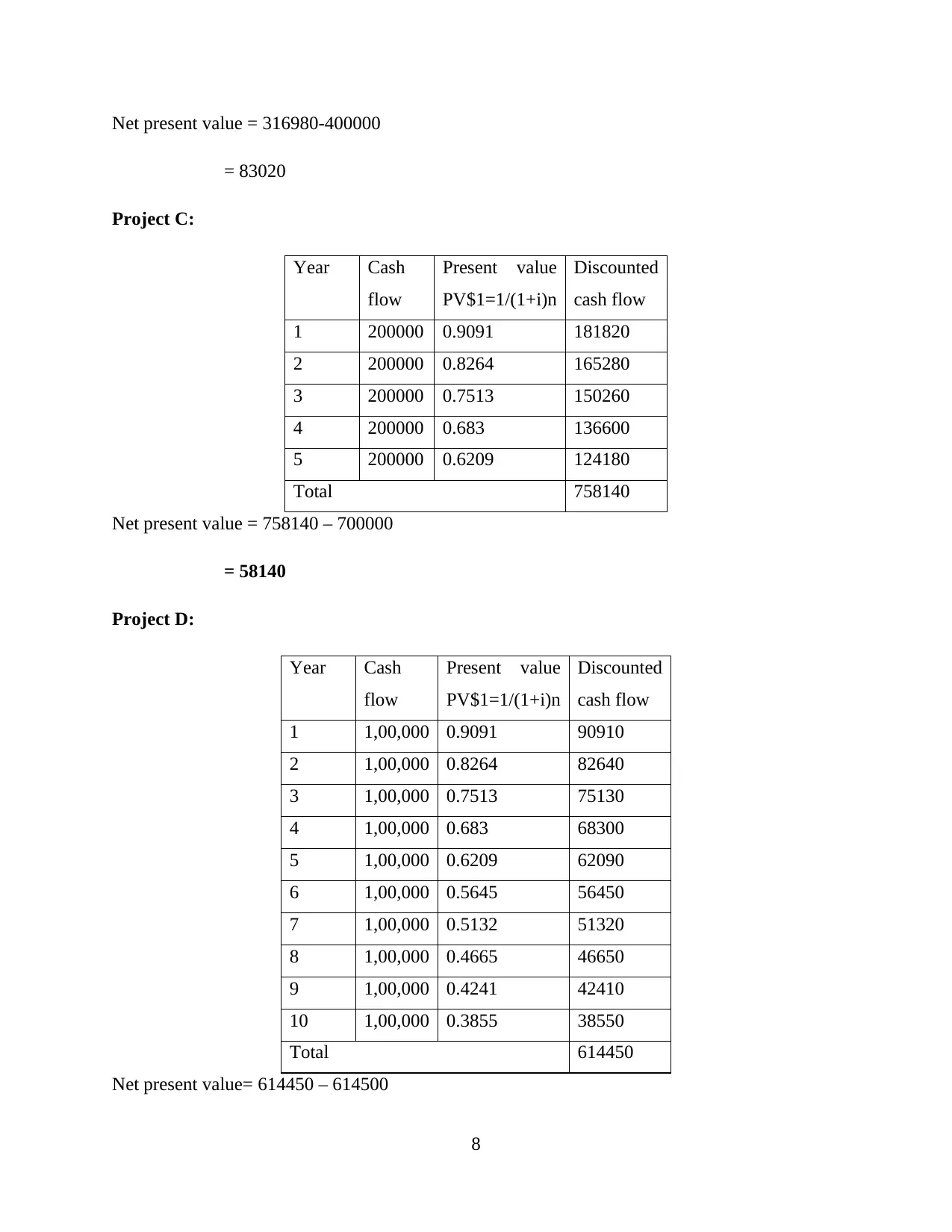

Net present value = 316980-400000

= 83020

Project C:

Year Cash

flow

Present value

PV$1=1/(1+i)n

Discounted

cash flow

1 200000 0.9091 181820

2 200000 0.8264 165280

3 200000 0.7513 150260

4 200000 0.683 136600

5 200000 0.6209 124180

Total 758140

Net present value = 758140 – 700000

= 58140

Project D:

Year Cash

flow

Present value

PV$1=1/(1+i)n

Discounted

cash flow

1 1,00,000 0.9091 90910

2 1,00,000 0.8264 82640

3 1,00,000 0.7513 75130

4 1,00,000 0.683 68300

5 1,00,000 0.6209 62090

6 1,00,000 0.5645 56450

7 1,00,000 0.5132 51320

8 1,00,000 0.4665 46650

9 1,00,000 0.4241 42410

10 1,00,000 0.3855 38550

Total 614450

Net present value= 614450 – 614500

8

= 83020

Project C:

Year Cash

flow

Present value

PV$1=1/(1+i)n

Discounted

cash flow

1 200000 0.9091 181820

2 200000 0.8264 165280

3 200000 0.7513 150260

4 200000 0.683 136600

5 200000 0.6209 124180

Total 758140

Net present value = 758140 – 700000

= 58140

Project D:

Year Cash

flow

Present value

PV$1=1/(1+i)n

Discounted

cash flow

1 1,00,000 0.9091 90910

2 1,00,000 0.8264 82640

3 1,00,000 0.7513 75130

4 1,00,000 0.683 68300

5 1,00,000 0.6209 62090

6 1,00,000 0.5645 56450

7 1,00,000 0.5132 51320

8 1,00,000 0.4665 46650

9 1,00,000 0.4241 42410

10 1,00,000 0.3855 38550

Total 614450

Net present value= 614450 – 614500

8

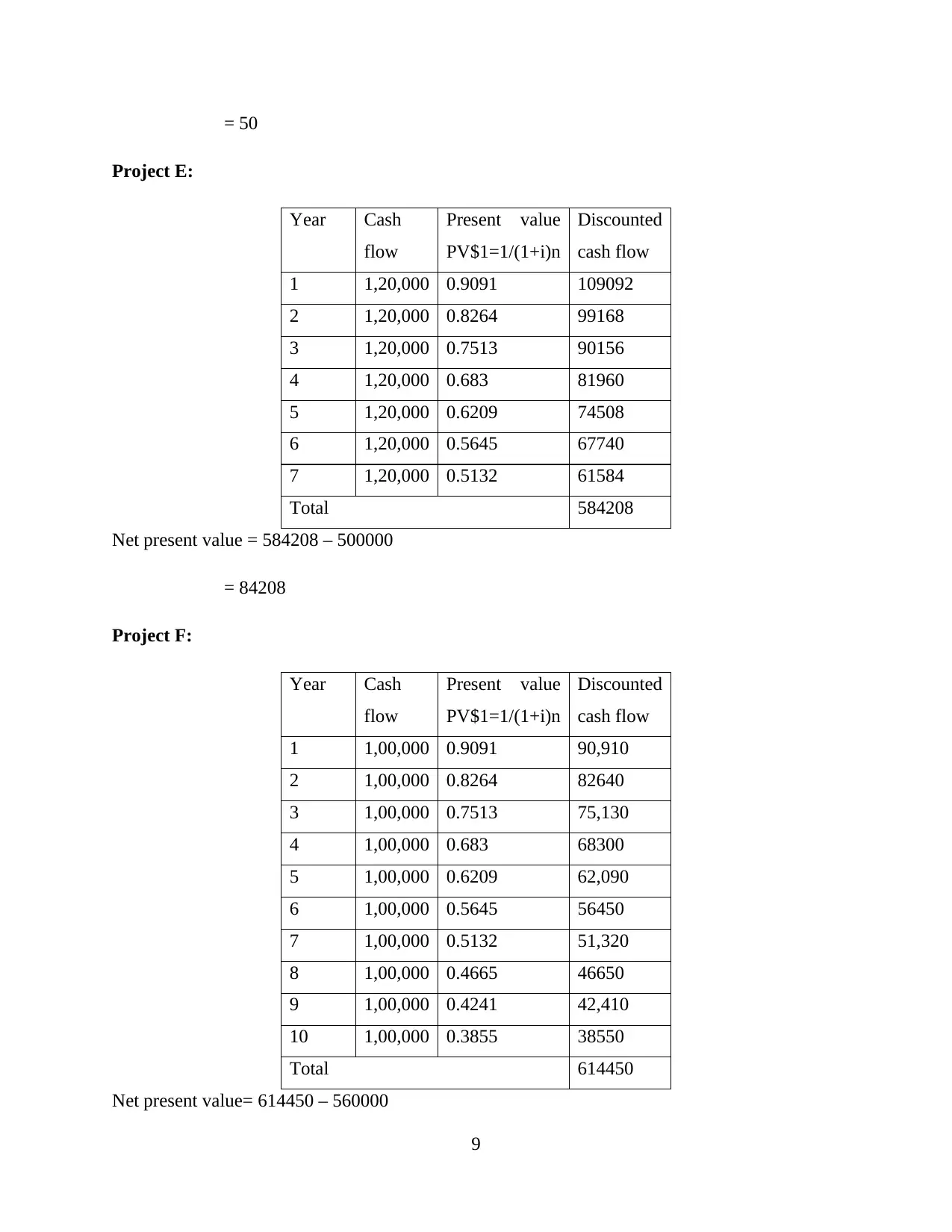

= 50

Project E:

Year Cash

flow

Present value

PV$1=1/(1+i)n

Discounted

cash flow

1 1,20,000 0.9091 109092

2 1,20,000 0.8264 99168

3 1,20,000 0.7513 90156

4 1,20,000 0.683 81960

5 1,20,000 0.6209 74508

6 1,20,000 0.5645 67740

7 1,20,000 0.5132 61584

Total 584208

Net present value = 584208 – 500000

= 84208

Project F:

Year Cash

flow

Present value

PV$1=1/(1+i)n

Discounted

cash flow

1 1,00,000 0.9091 90,910

2 1,00,000 0.8264 82640

3 1,00,000 0.7513 75,130

4 1,00,000 0.683 68300

5 1,00,000 0.6209 62,090

6 1,00,000 0.5645 56450

7 1,00,000 0.5132 51,320

8 1,00,000 0.4665 46650

9 1,00,000 0.4241 42,410

10 1,00,000 0.3855 38550

Total 614450

Net present value= 614450 – 560000

9

Project E:

Year Cash

flow

Present value

PV$1=1/(1+i)n

Discounted

cash flow

1 1,20,000 0.9091 109092

2 1,20,000 0.8264 99168

3 1,20,000 0.7513 90156

4 1,20,000 0.683 81960

5 1,20,000 0.6209 74508

6 1,20,000 0.5645 67740

7 1,20,000 0.5132 61584

Total 584208

Net present value = 584208 – 500000

= 84208

Project F:

Year Cash

flow

Present value

PV$1=1/(1+i)n

Discounted

cash flow

1 1,00,000 0.9091 90,910

2 1,00,000 0.8264 82640

3 1,00,000 0.7513 75,130

4 1,00,000 0.683 68300

5 1,00,000 0.6209 62,090

6 1,00,000 0.5645 56450

7 1,00,000 0.5132 51,320

8 1,00,000 0.4665 46650

9 1,00,000 0.4241 42,410

10 1,00,000 0.3855 38550

Total 614450

Net present value= 614450 – 560000

9

= 54450

Project G:

Year Cash

flow

Present value

PV$1=1/(1+i)n

Discounted

cash flow

1 1,00,000 0.9091 90910

2 1,00,000 0.8264 82640

3 80,000 0.7513 60104

4 80,000 0.683 54640

5 80,000 0.6209 49672

6 80,000 0.5645 45160

Total 383126

Net present value = 383126-200000

= 183126

c) Ranking the project according to payback period and net present value is:

Project Payback period Rank Net present

value

Rank

A 4.24 2 306560 1

B n/a 6 83020 4

C 4.53 3 58140 5

D n/a 6 50 7

E 5.73 4 84208 3

F 8.68 5 54450 6

G 2.58 1 183126 2

d) If the projects are mutually exclusive then the K plc will choose any one project out of two. In

the above case there are two mutually exclusive projects that are project A and G. The

organisation will separately invest in all the two project but will opt for that project whose net

present value is maximum in the current time. So in this case K plc will select Project A because

10

Project G:

Year Cash

flow

Present value

PV$1=1/(1+i)n

Discounted

cash flow

1 1,00,000 0.9091 90910

2 1,00,000 0.8264 82640

3 80,000 0.7513 60104

4 80,000 0.683 54640

5 80,000 0.6209 49672

6 80,000 0.5645 45160

Total 383126

Net present value = 383126-200000

= 183126

c) Ranking the project according to payback period and net present value is:

Project Payback period Rank Net present

value

Rank

A 4.24 2 306560 1

B n/a 6 83020 4

C 4.53 3 58140 5

D n/a 6 50 7

E 5.73 4 84208 3

F 8.68 5 54450 6

G 2.58 1 183126 2

d) If the projects are mutually exclusive then the K plc will choose any one project out of two. In

the above case there are two mutually exclusive projects that are project A and G. The

organisation will separately invest in all the two project but will opt for that project whose net

present value is maximum in the current time. So in this case K plc will select Project A because

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

the net present value of that project is 306560 although the Project G has the pay period which is

less than that of other one. If organisation need to select mutually exclusive project than the

decision are made by seeing the net present value(Watkins, 2020).

e) Strength and weakness of pay back periods and Net present value are (Gorshkov, and et. al,

2018):

Payback period:

Strengths Weakness

Speedy solution Ignore the time and money value.

Helpful in case of uncertainty Neglect cash flow receive after

payback period

Give preference to liquidity Not based on realistic approach

Simple to use Ignore profit

Net present value:

Strength Weakness

Verify investing value Future forecasting Error

Compute profitability Ignore the sunk cost

Identify the risk involved Depends upon the rate of discount

Can be adjusted according to the

condition

Cannot be used to evaluate projects of

dissimilar sizes.

e) The five qualitative factor that keeps in mind while making a firm decision are:

Customers: Clients perception regarding the organization when they buy the goods and

services plays a very important role when the directors of the company made any

decision. How their problem is getting solved, the time taken to resolve the problem etc.

(Elliott, 2018).

11

less than that of other one. If organisation need to select mutually exclusive project than the

decision are made by seeing the net present value(Watkins, 2020).

e) Strength and weakness of pay back periods and Net present value are (Gorshkov, and et. al,

2018):

Payback period:

Strengths Weakness

Speedy solution Ignore the time and money value.

Helpful in case of uncertainty Neglect cash flow receive after

payback period

Give preference to liquidity Not based on realistic approach

Simple to use Ignore profit

Net present value:

Strength Weakness

Verify investing value Future forecasting Error

Compute profitability Ignore the sunk cost

Identify the risk involved Depends upon the rate of discount

Can be adjusted according to the

condition

Cannot be used to evaluate projects of

dissimilar sizes.

e) The five qualitative factor that keeps in mind while making a firm decision are:

Customers: Clients perception regarding the organization when they buy the goods and

services plays a very important role when the directors of the company made any

decision. How their problem is getting solved, the time taken to resolve the problem etc.

(Elliott, 2018).

11

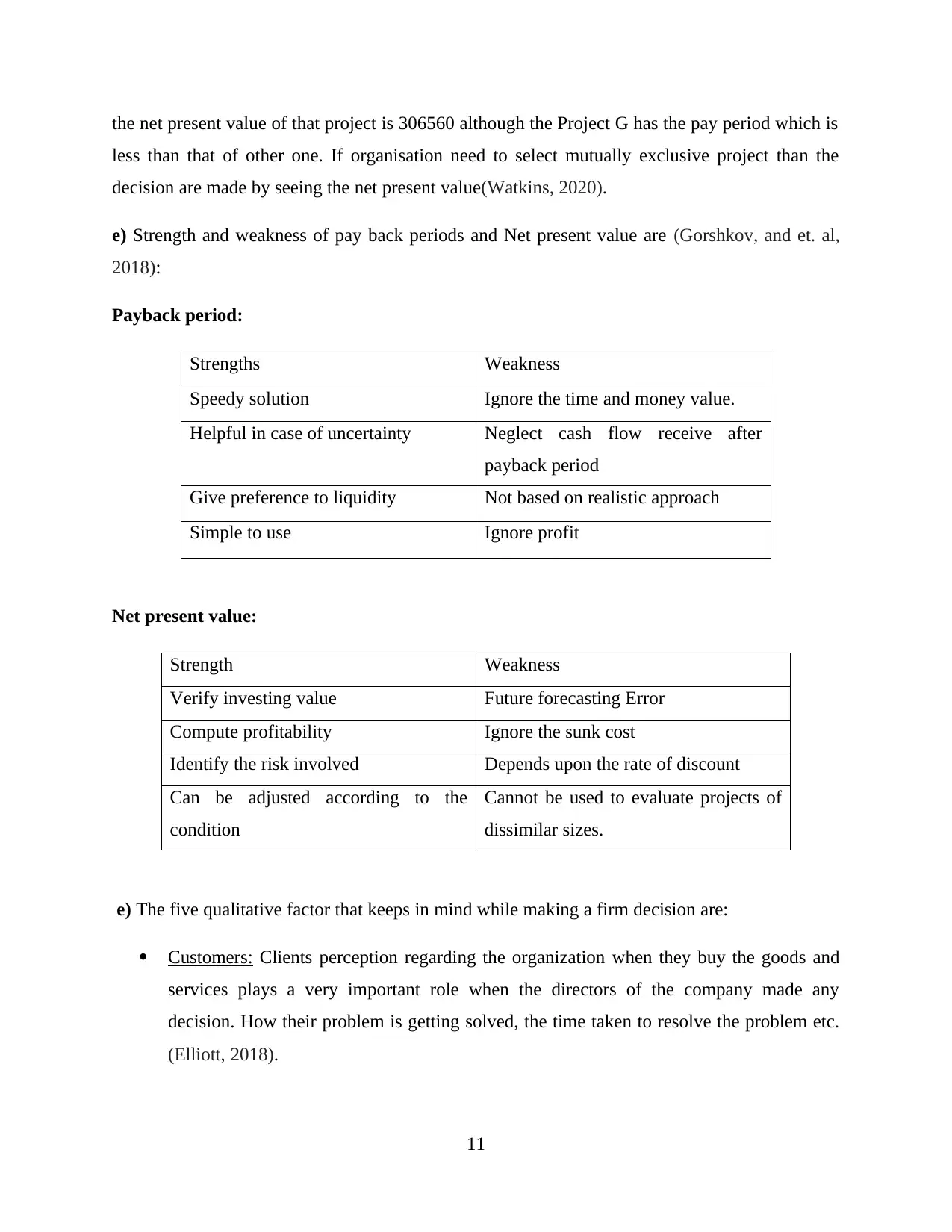

External image: The top managers need to take in mind that hoe their decision will affect

the reputation of the company in outside the business environment.

Employee relation: this is the most important factor. For all the organisation it is very

important to make any decision while seeing their engagement with the workforce

because they are the people who actual put efforts to enhance the production (Pinto,

2020).

Technology outbreaks: technological advancement is one of the important factors. Before

passing any judgment the supervisor need to look after the technology so that they can

see if there is any outbreak because of this.

Market share: Top managers need to properly analysis the market so that they can get to

know whether there is any market growth for the business and invest is made on this

factor Elwakil and Hegab, 2020).

TASK B

a) Three alternatives to raise capital for external sources are:

Debt capital: Debt financing is that source to raise fund where the borrower issue some

debt securities from the bank. In this K plc will borrow some money from the bank in

exchange of some security. This source should be used as this one of the secure external

source through which capital can be gained in cheaper rate (Sohaib and et. al, 2019).

Trade credit: This is nothing but a short term financing source were the credit is grant

by the creditors for certain period of time. This source should be suitable for K plc as it

will help them to delay their payment for certain period. The period of repayment

depends upon the agreement between the organisation and the provider.

Factoring: This external source of funding will be best for K plc as it will help them to

raise the capital in short period. In this the debtors of K plc will be sealed to the third

party. The account receivables are being sale at the discount price. In this the purchased

that is also known as factor will accumulate the amount from the K plc debtors on behalf

of the organisation Lane and Milesi-Ferretti, 2018).

b) A link between the investment choice and the financial decision is called as Financial

planning. This planning process aims to identify the choice of the company in respect to the

12

the reputation of the company in outside the business environment.

Employee relation: this is the most important factor. For all the organisation it is very

important to make any decision while seeing their engagement with the workforce

because they are the people who actual put efforts to enhance the production (Pinto,

2020).

Technology outbreaks: technological advancement is one of the important factors. Before

passing any judgment the supervisor need to look after the technology so that they can

see if there is any outbreak because of this.

Market share: Top managers need to properly analysis the market so that they can get to

know whether there is any market growth for the business and invest is made on this

factor Elwakil and Hegab, 2020).

TASK B

a) Three alternatives to raise capital for external sources are:

Debt capital: Debt financing is that source to raise fund where the borrower issue some

debt securities from the bank. In this K plc will borrow some money from the bank in

exchange of some security. This source should be used as this one of the secure external

source through which capital can be gained in cheaper rate (Sohaib and et. al, 2019).

Trade credit: This is nothing but a short term financing source were the credit is grant

by the creditors for certain period of time. This source should be suitable for K plc as it

will help them to delay their payment for certain period. The period of repayment

depends upon the agreement between the organisation and the provider.

Factoring: This external source of funding will be best for K plc as it will help them to

raise the capital in short period. In this the debtors of K plc will be sealed to the third

party. The account receivables are being sale at the discount price. In this the purchased

that is also known as factor will accumulate the amount from the K plc debtors on behalf

of the organisation Lane and Milesi-Ferretti, 2018).

b) A link between the investment choice and the financial decision is called as Financial

planning. This planning process aims to identify the choice of the company in respect to the

12

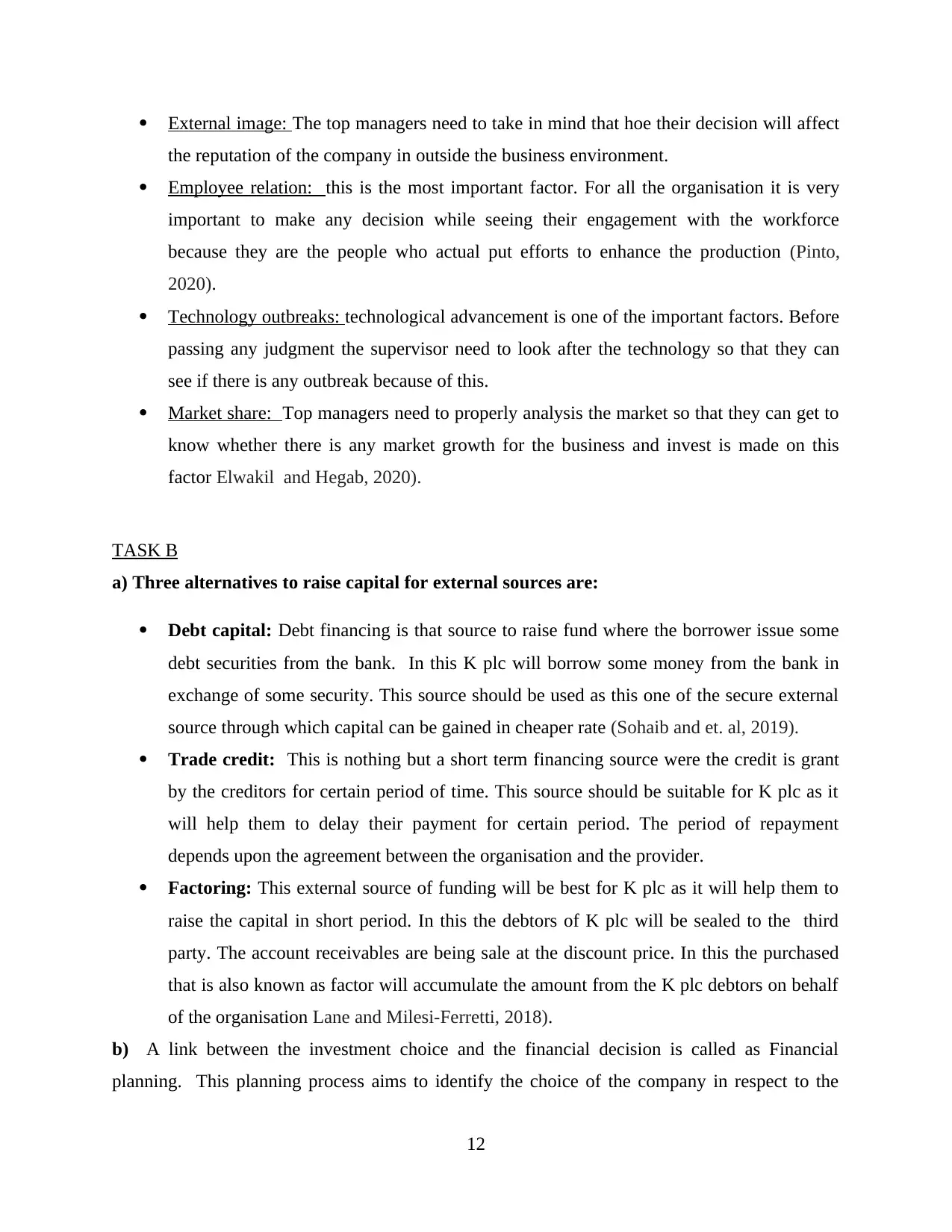

investment and thee sources to raise capital. The relationship between the two with Regard to K

plc is that it will help them to being the capital in the company. As the company in which they

are investing the capital help them to gain market share of that business to so that when they

diversified they will get the customer easily. This will also help to grow in the market and

capture more market share (Rodriguez-Satizabal, 2021).

TASK C

a) Total cost to be incurred for 1 unit = 3+2+30+18= 53

Total units produced in a year is 40000 * 53 = 2120000

To produced 9000 units in a quarter the cost incurred will be

= 9000 * 53 = 477000

Full variance analysis statement of variable cost will be follow:

Standard Actual

Direct labour 8500 *3 25500 29750

Direct material 18000 /2= 9000

*1

9000 18000

Direct labour 28000/3= 9333 *

30

280000 294000

Variable overhead 162500 165000

Total variable

production cost

477000 506750

So in the above table the cost to be incurred will be 477000 but the actual caot is 506750

So the overhead variable cost is 506750- 477000

= £29750

b) So from the above table it is identified that K plc is not utilising their resources effective way

due to which their cost of production in the first quarter is increased.

13

plc is that it will help them to being the capital in the company. As the company in which they

are investing the capital help them to gain market share of that business to so that when they

diversified they will get the customer easily. This will also help to grow in the market and

capture more market share (Rodriguez-Satizabal, 2021).

TASK C

a) Total cost to be incurred for 1 unit = 3+2+30+18= 53

Total units produced in a year is 40000 * 53 = 2120000

To produced 9000 units in a quarter the cost incurred will be

= 9000 * 53 = 477000

Full variance analysis statement of variable cost will be follow:

Standard Actual

Direct labour 8500 *3 25500 29750

Direct material 18000 /2= 9000

*1

9000 18000

Direct labour 28000/3= 9333 *

30

280000 294000

Variable overhead 162500 165000

Total variable

production cost

477000 506750

So in the above table the cost to be incurred will be 477000 but the actual caot is 506750

So the overhead variable cost is 506750- 477000

= £29750

b) So from the above table it is identified that K plc is not utilising their resources effective way

due to which their cost of production in the first quarter is increased.

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The direct cost that will be incurred for 8500 kg of S material will be 25500 but the actual

cost that is incurring is 29750 which means that for every they are paying £ 4250 extra

that means the turnover is high for producing material S.

Next for direct material cost for T will be 9000 for every 2 kg but there are paying £ 1 for

every 1 kg that means actual they are paying £18000. This indicates that they are paying

double to procure material T.

Direct labour cost will be for every 1 hour they will be pay £ 10 so if the labour work for

28000 so they will be paying 280000 but they are paying extra 294000. £ 14000 is being

paying extra for 1400 hour work.

Variable overhead will be £ 162500 but they are incurring cost £165000.

So in total they are paying extra £ 29750 in the first quarter.

14

cost that is incurring is 29750 which means that for every they are paying £ 4250 extra

that means the turnover is high for producing material S.

Next for direct material cost for T will be 9000 for every 2 kg but there are paying £ 1 for

every 1 kg that means actual they are paying £18000. This indicates that they are paying

double to procure material T.

Direct labour cost will be for every 1 hour they will be pay £ 10 so if the labour work for

28000 so they will be paying 280000 but they are paying extra 294000. £ 14000 is being

paying extra for 1400 hour work.

Variable overhead will be £ 162500 but they are incurring cost £165000.

So in total they are paying extra £ 29750 in the first quarter.

14

TASK 4

Comparison between centralised and decentralised procurement and their benefits.

Centralised and decentralised purchasing are two type of organisation composition. These

type can be found in the company, government bodies and even when the procurement are been

made. The term centralised itself says the authority to take decision or plans are only in the hand

of top managers of the company whereas decentralised means authorities are being delegated to

the other department mangers to take decision based on their departmental needs. All the power

in centralised are at apex stage , in other hand Decentralised means diffusion of power to

subordinate also (Oehler, and et. al, 2018).

Centralised purchasing:

Centralised purchasing means all the procurement are been done at the central stage of the

company. If department need any material than they need to inform the fundamental authority

and the purchase is made by them according to the needs. This type of procurement of material is

possible when there is only one plant of the organisation. This will help them to buy in economic

quantity and also avoid of purchasing in the tiny lots. The whole procurement authority is made

in one hand that is the purchasing department. As the material is purchased in large quantity this

will help in favourable price for buying and the economy of scale. This also helps in managing

the raw material in effective and efficient manner(Shah, Ahmad and Mahmood, 2018).

There are some benefits of centralised procurement:

Bulk buying discount: Centralised purchasing help the organisation to bargain in

effective manner as the order is made in large amount which help them to negotiate for

discount as buying is made in bulk.

Wider supplier network: The procurement is made by the purchasing department which

help them to extend their supplier network to the local buyers. This will benefit them by

getting the material at the lowest price will analysing the provider.

Single Centralised store: As the company is situated at small area where operating cost is

incurred on one geographical area so managing one single store is easy. It will also help

the purchasing department to maintain their inventory in effective way rather than

distributing it on several parts. This will also provides access to information about the

15

Comparison between centralised and decentralised procurement and their benefits.

Centralised and decentralised purchasing are two type of organisation composition. These

type can be found in the company, government bodies and even when the procurement are been

made. The term centralised itself says the authority to take decision or plans are only in the hand

of top managers of the company whereas decentralised means authorities are being delegated to

the other department mangers to take decision based on their departmental needs. All the power

in centralised are at apex stage , in other hand Decentralised means diffusion of power to

subordinate also (Oehler, and et. al, 2018).

Centralised purchasing:

Centralised purchasing means all the procurement are been done at the central stage of the

company. If department need any material than they need to inform the fundamental authority

and the purchase is made by them according to the needs. This type of procurement of material is

possible when there is only one plant of the organisation. This will help them to buy in economic

quantity and also avoid of purchasing in the tiny lots. The whole procurement authority is made

in one hand that is the purchasing department. As the material is purchased in large quantity this

will help in favourable price for buying and the economy of scale. This also helps in managing

the raw material in effective and efficient manner(Shah, Ahmad and Mahmood, 2018).

There are some benefits of centralised procurement:

Bulk buying discount: Centralised purchasing help the organisation to bargain in

effective manner as the order is made in large amount which help them to negotiate for

discount as buying is made in bulk.

Wider supplier network: The procurement is made by the purchasing department which

help them to extend their supplier network to the local buyers. This will benefit them by

getting the material at the lowest price will analysing the provider.

Single Centralised store: As the company is situated at small area where operating cost is

incurred on one geographical area so managing one single store is easy. It will also help

the purchasing department to maintain their inventory in effective way rather than

distributing it on several parts. This will also provides access to information about the

15

stock which is in bulk and which required on the urgent basis (Harrison, Rafiq and

Medcalf, 2018).

Effective Quality: One of the important advantages in centralised purchasing is that it

provides quality raw material as organisation will easily contact with those supplier who

gives prime material.

Decentralised purchasing:

This is just the opposite of centralised purchasing. When the company has so many planets in

different location then this type of structure is been followed so that complexity can be increased.

Various purchasing agents are there who buy the raw material according to the need of their

planet. Decentralised purchasing means procuring the material by the subordinate who has assign

the power of delegation. Decentralised purchasing is also known as local purchasing. This is

flexible approach when there is so many subsidiary of the big organisation. Here the authority to

take declension are been delegated by the head department so that complexity of providing stock

to different location can be solved in effective and efficient manner. The raw material

procurement is made by the purchasing department on the basis of the local needs and want and

the planet does not rely to the head to conduct their business activities (Khoukhi, Bojji and

Bensouda, 2021).

Following benefits of centralised purchasing are:

Reduce burden on top mangers: Where there is so many subsidiary of the company

than the burden to top management increases. So decrease that burden the purchasing

agents are being hired for various location so that top executive can perform their

function in effective manner. Decision are made very fastly by the decentralised structure

so that uncertainty can be avoid.

Better control and supervision: Decentralisation purchasing promotes amended control

and supervision as the inferior has the power to take decision independently. They do not

relay on the higher authority for the problem that require immediate solution. This also

boosts the morale of the employee (Moretto and et.al, 2020).

Facilitates diversification: The most important benefits are it promotes diversification.

It will help the variation of goods and services according to the market. This

diversification is not possible in Centralised procurement. They also have the advantage

16

Medcalf, 2018).

Effective Quality: One of the important advantages in centralised purchasing is that it

provides quality raw material as organisation will easily contact with those supplier who

gives prime material.

Decentralised purchasing:

This is just the opposite of centralised purchasing. When the company has so many planets in

different location then this type of structure is been followed so that complexity can be increased.

Various purchasing agents are there who buy the raw material according to the need of their

planet. Decentralised purchasing means procuring the material by the subordinate who has assign

the power of delegation. Decentralised purchasing is also known as local purchasing. This is

flexible approach when there is so many subsidiary of the big organisation. Here the authority to

take declension are been delegated by the head department so that complexity of providing stock

to different location can be solved in effective and efficient manner. The raw material

procurement is made by the purchasing department on the basis of the local needs and want and

the planet does not rely to the head to conduct their business activities (Khoukhi, Bojji and

Bensouda, 2021).

Following benefits of centralised purchasing are:

Reduce burden on top mangers: Where there is so many subsidiary of the company

than the burden to top management increases. So decrease that burden the purchasing

agents are being hired for various location so that top executive can perform their

function in effective manner. Decision are made very fastly by the decentralised structure

so that uncertainty can be avoid.

Better control and supervision: Decentralisation purchasing promotes amended control

and supervision as the inferior has the power to take decision independently. They do not

relay on the higher authority for the problem that require immediate solution. This also

boosts the morale of the employee (Moretto and et.al, 2020).

Facilitates diversification: The most important benefits are it promotes diversification.

It will help the variation of goods and services according to the market. This

diversification is not possible in Centralised procurement. They also have the advantage

16

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

were they can purchase raw material from the diversified suppliers located at different

parts.

The decentralised procurement is better option when they want purchase in localized industry

or when there are different branch mangers (Ellul, 2021).

.

CONCLUSION

From the above report it is been concluded that to run the business it is very important to

manage their finance. Without effective funds company cannot utilise their resources in effective

and efficient manner. This report consist of four task, the first task talks about the payback period

and the net present value for the different project that is adopted by K plc. They also talks about

the strength and weakness about the two. In K plc there is two mutually exclusive projects and

the director will select which has more present value. The second parts tell about the various

external sources that is available to raise capital for diversification. The third task of the report is

all about the variable cost. The K plc has variable overhead which means that company is not

using their capital in effective and efficient manner. The last task is all about the centralised and

decentralised procurement and the benefits of all the two structure. In centralised purchasing the

procurement of the material is done by the central authority whereas in decentralised power is

delegated to various purchasing agents of different subsidies, which means that purchasing is

made according to the store purchasing department of the single organisation.

17

parts.

The decentralised procurement is better option when they want purchase in localized industry

or when there are different branch mangers (Ellul, 2021).

.

CONCLUSION

From the above report it is been concluded that to run the business it is very important to

manage their finance. Without effective funds company cannot utilise their resources in effective

and efficient manner. This report consist of four task, the first task talks about the payback period

and the net present value for the different project that is adopted by K plc. They also talks about

the strength and weakness about the two. In K plc there is two mutually exclusive projects and

the director will select which has more present value. The second parts tell about the various

external sources that is available to raise capital for diversification. The third task of the report is

all about the variable cost. The K plc has variable overhead which means that company is not

using their capital in effective and efficient manner. The last task is all about the centralised and

decentralised procurement and the benefits of all the two structure. In centralised purchasing the

procurement of the material is done by the central authority whereas in decentralised power is

delegated to various purchasing agents of different subsidies, which means that purchasing is

made according to the store purchasing department of the single organisation.

17

REFERENCES

DISEMBER, S., 2021. DPB50113: BUSINESS FINANCE.

Watkins, J.S., 2020. Ethical and Business Finance. In Islamic Finance and Global

Capitalism (pp. 207-255). Palgrave Macmillan, Cham.

Gorshkov, A.S., Vatin, N.I., Rymkevich, P.P. and Kydrevich, O.O., 2018. Payback period of

investments in energy saving. Magazine of Civil Engineering, (2).

Pinto, J.E., 2020. Equity asset valuation. John Wiley & Sons.

Elliott, V., 2018. Thinking about the coding process in qualitative data analysis. The Qualitative

Report, 23(11), pp.2850-2861.

Elwakil, E. and Hegab, M., 2020, April. Toward smart and sustainable infrastructure solution:

Assessment and modelling of qualitative factors affecting productivity in

microtunneling projects. In 2020 IEEE Conference on Technologies for Sustainability

(SusTech) (pp. 1-8). IEEE.

Sohaib, O., Naderpour, M., Hussain, W. and Martinez, L., 2019. Cloud computing model

selection for e-commerce enterprises using a new 2-tuple fuzzy linguistic decision-

making method. Computers & Industrial Engineering, 132, pp.47-58.

Lane, P.R. and Milesi-Ferretti, G.M., 2018. The external wealth of nations revisited:

international financial integration in the aftermath of the global financial crisis. IMF

Economic Review, 66(1), pp.189-222.

Rodriguez-Satizabal, B., 2021. Only one way to raise capital? Colombian business groups and

the dawn of internal markets. Business History, 63(8), pp.1371-1392.

Oehler, A., Wendt, S., Wedlich, F. and Horn, M., 2018. Investors' personality influences

investment decisions: Experimental evidence on extraversion and neuroticism. Journal

of Behavioral Finance, 19(1), pp.30-48.

Shah, S.Z.A., Ahmad, M. and Mahmood, F., 2018. Heuristic biases in investment decision-

making and perceived market efficiency: A survey at the Pakistan stock

exchange. Qualitative Research in Financial Markets.

Harrison, R.P., Rafiq, Q.A. and Medcalf, N., 2018. Centralised versus decentralised

manufacturing and the delivery of healthcare products: A United Kingdom

exemplar. Cytotherapy, 20(6), pp.873-890.

Khoukhi, S., Bojji, C. and Bensouda, Y., 2021. Joint optimisation of replenishment policies on a

downstream multi-echelon, multi-product pharmaceutical supply chain with lost sales,

stochastic demands and storage capacity constraints: centralised vs. decentralised

structure. International Journal of Logistics Systems and Management, 39(1), pp.1-21.

Moretto, A., Patrucco, A.S., Walker, H. and Ronchi, S., 2020. Procurement organisation in

project-based setting: a multiple case study of engineer-to-order companies. Production

Planning & Control, pp.1-16.

Ellul, J., 2021. Blockchain, Decentralisation and the Public Interest: The need for a

Decentralisation Conceptual Framework for dApps. Available at SSRN 3788887.

18

DISEMBER, S., 2021. DPB50113: BUSINESS FINANCE.

Watkins, J.S., 2020. Ethical and Business Finance. In Islamic Finance and Global

Capitalism (pp. 207-255). Palgrave Macmillan, Cham.

Gorshkov, A.S., Vatin, N.I., Rymkevich, P.P. and Kydrevich, O.O., 2018. Payback period of

investments in energy saving. Magazine of Civil Engineering, (2).

Pinto, J.E., 2020. Equity asset valuation. John Wiley & Sons.

Elliott, V., 2018. Thinking about the coding process in qualitative data analysis. The Qualitative

Report, 23(11), pp.2850-2861.

Elwakil, E. and Hegab, M., 2020, April. Toward smart and sustainable infrastructure solution:

Assessment and modelling of qualitative factors affecting productivity in

microtunneling projects. In 2020 IEEE Conference on Technologies for Sustainability

(SusTech) (pp. 1-8). IEEE.

Sohaib, O., Naderpour, M., Hussain, W. and Martinez, L., 2019. Cloud computing model

selection for e-commerce enterprises using a new 2-tuple fuzzy linguistic decision-

making method. Computers & Industrial Engineering, 132, pp.47-58.

Lane, P.R. and Milesi-Ferretti, G.M., 2018. The external wealth of nations revisited:

international financial integration in the aftermath of the global financial crisis. IMF

Economic Review, 66(1), pp.189-222.

Rodriguez-Satizabal, B., 2021. Only one way to raise capital? Colombian business groups and

the dawn of internal markets. Business History, 63(8), pp.1371-1392.

Oehler, A., Wendt, S., Wedlich, F. and Horn, M., 2018. Investors' personality influences

investment decisions: Experimental evidence on extraversion and neuroticism. Journal

of Behavioral Finance, 19(1), pp.30-48.

Shah, S.Z.A., Ahmad, M. and Mahmood, F., 2018. Heuristic biases in investment decision-

making and perceived market efficiency: A survey at the Pakistan stock

exchange. Qualitative Research in Financial Markets.

Harrison, R.P., Rafiq, Q.A. and Medcalf, N., 2018. Centralised versus decentralised

manufacturing and the delivery of healthcare products: A United Kingdom

exemplar. Cytotherapy, 20(6), pp.873-890.

Khoukhi, S., Bojji, C. and Bensouda, Y., 2021. Joint optimisation of replenishment policies on a

downstream multi-echelon, multi-product pharmaceutical supply chain with lost sales,

stochastic demands and storage capacity constraints: centralised vs. decentralised

structure. International Journal of Logistics Systems and Management, 39(1), pp.1-21.

Moretto, A., Patrucco, A.S., Walker, H. and Ronchi, S., 2020. Procurement organisation in

project-based setting: a multiple case study of engineer-to-order companies. Production

Planning & Control, pp.1-16.

Ellul, J., 2021. Blockchain, Decentralisation and the Public Interest: The need for a

Decentralisation Conceptual Framework for dApps. Available at SSRN 3788887.

18

19

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.