MA514 Business Finance Report: Economic, Investment & Finance Analysis

VerifiedAdded on 2023/06/11

|15

|3183

|473

Report

AI Summary

This report provides a comprehensive financial analysis, including property price projections, income growth assessments, and savings calculations, to aid a client in achieving her 'Australian dream.' It evaluates the affordability of property in Melbourne by analyzing historical price data, inflation rates, and income trends. The report calculates the client's potential savings, considering salary, expenses, and tax implications, and determines the maximum property value achievable with and without insurance premiums, assessing loan-to-value ratios. Furthermore, it projects future property prices and income, demonstrating the client's ability to purchase property with different upfront payment scenarios. The analysis incorporates stamp duty and insurance premium costs to provide a realistic financial outlook, concluding with a projection of the client's savings over time and their ability to meet financial goals. This student-contributed document is available on Desklib, offering valuable insights for finance students and professionals.

Running head: BUSINESS FINANCE

Business Finance

Name of the Student:

Name of the University:

Authors Note:

Business Finance

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BUSINESS FINANCE

1

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................3

Answer to question 3:.................................................................................................................5

Answer to question 4:.................................................................................................................6

Answer to question 5:.................................................................................................................8

Answer to question 6:...............................................................................................................11

Answer to question 7:...............................................................................................................11

Reference and Bibliography:....................................................................................................13

1

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................3

Answer to question 3:.................................................................................................................5

Answer to question 4:.................................................................................................................6

Answer to question 5:.................................................................................................................8

Answer to question 6:...............................................................................................................11

Answer to question 7:...............................................................................................................11

Reference and Bibliography:....................................................................................................13

BUSINESS FINANCE

2

Answer to question 1:

Year Price Four Year Average Price change

2002 262

2003 293

2004 309

2005 321 296

2006 345 317 7.07%

2007 372 337 6.20%

2008 389 357 5.93%

2009 419 381 6.88%

2010 494 418 9.76%

2011 492 448 7.21%

2012 488 473 5.52%

2013 517 498 5.18%

2014 543 510 2.47%

2015 587 534 4.61%

2016 633 570 6.78%

2017 684 612 7.34%

Average 4.33%

Inflation rate 1.92%

Year Amount "Million"

Year 0 $ 0.68

Year 1 $ 0.71

Year 2 $ 0.74

Year 3 $ 0.78

Year 4 $ 0.81

Year 5 $ 0.85

Year 6 $ 0.88

Year 7 $ 0.92

Year 8 $ 0.96

Year 9 $ 1.00

Year 10 $ 1.04

Year 11 $ 1.09

Year 12 $ 1.14

Year 13 $ 1.19

Year 14 $ 1.24

Year 15 $ 1.29

Year 16 $ 1.35

Year 17 $ 1.41

Year 18 $ 1.47

Year 19 $ 1.53

2

Answer to question 1:

Year Price Four Year Average Price change

2002 262

2003 293

2004 309

2005 321 296

2006 345 317 7.07%

2007 372 337 6.20%

2008 389 357 5.93%

2009 419 381 6.88%

2010 494 418 9.76%

2011 492 448 7.21%

2012 488 473 5.52%

2013 517 498 5.18%

2014 543 510 2.47%

2015 587 534 4.61%

2016 633 570 6.78%

2017 684 612 7.34%

Average 4.33%

Inflation rate 1.92%

Year Amount "Million"

Year 0 $ 0.68

Year 1 $ 0.71

Year 2 $ 0.74

Year 3 $ 0.78

Year 4 $ 0.81

Year 5 $ 0.85

Year 6 $ 0.88

Year 7 $ 0.92

Year 8 $ 0.96

Year 9 $ 1.00

Year 10 $ 1.04

Year 11 $ 1.09

Year 12 $ 1.14

Year 13 $ 1.19

Year 14 $ 1.24

Year 15 $ 1.29

Year 16 $ 1.35

Year 17 $ 1.41

Year 18 $ 1.47

Year 19 $ 1.53

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BUSINESS FINANCE

3

Year 20 $ 1.60

Year

0

Year

1

Year

2

Year

3

Year

4

Year

5

Year

6

Year

7

Year

8

Year

9

Year

10

Year

11

Year

12

Year

13

Year

14

Year

15

Year

16

Year

17

Year

18

Year

19

Year

20

$0.68$0.71$0.74$0.78$0.81$0.85$0.88$0.92$0.96$1.00$1.04$1.09$1.14$1.19$1.24$1.29$1.35$1.41$1.47$1.53$1.60

Property price for next 20 years "In Million"

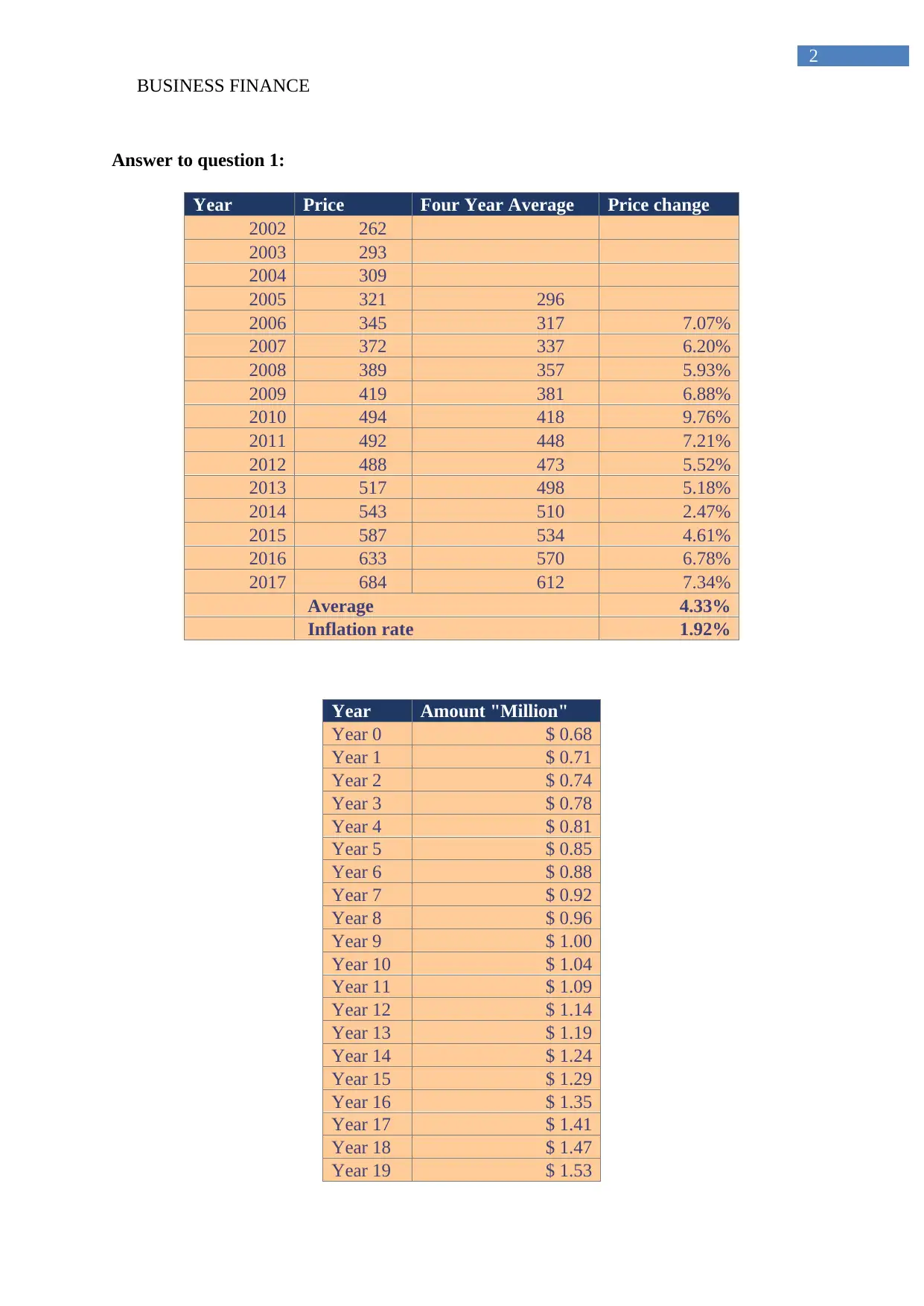

The 4-year average price is a relatively used for detecting the price change of housing

in Melbourne from 2002 to 2017. This relevant measure helps in understanding the relevant

prices of housing in Melbourne which would eventually rice in future. The calculation is

adequately deducted from inflation rate to understand the actual increment in property price.

This would help in detecting the actual price level that is been changed in the housing price.

The above table relatively represents the overall average rate and the 20 year future prices of

houses in Melbourne. The housing price will relatively increased from $0.68 million to $1.60

million in 20 years. The graph relevantly represents of the price increment of property in next

30 years, which is essential to draft the financial plan for the client to achieve her Australian

dream (Randolph & Tice, 2014).

Answer to question 2:

Year Weekly Income Yearly Income Four Year Average Price change

1994–95 $ 1,340 $ 69,680

1995–96 $ 1,297 $ 67,444

1996–97 $ 1,342 $ 69,784

1997–98 $ 1,400 $ 72,800 69,927

1999–2000 $ 1,534 $ 79,768 72,449 3.61%

3

Year 20 $ 1.60

Year

0

Year

1

Year

2

Year

3

Year

4

Year

5

Year

6

Year

7

Year

8

Year

9

Year

10

Year

11

Year

12

Year

13

Year

14

Year

15

Year

16

Year

17

Year

18

Year

19

Year

20

$0.68$0.71$0.74$0.78$0.81$0.85$0.88$0.92$0.96$1.00$1.04$1.09$1.14$1.19$1.24$1.29$1.35$1.41$1.47$1.53$1.60

Property price for next 20 years "In Million"

The 4-year average price is a relatively used for detecting the price change of housing

in Melbourne from 2002 to 2017. This relevant measure helps in understanding the relevant

prices of housing in Melbourne which would eventually rice in future. The calculation is

adequately deducted from inflation rate to understand the actual increment in property price.

This would help in detecting the actual price level that is been changed in the housing price.

The above table relatively represents the overall average rate and the 20 year future prices of

houses in Melbourne. The housing price will relatively increased from $0.68 million to $1.60

million in 20 years. The graph relevantly represents of the price increment of property in next

30 years, which is essential to draft the financial plan for the client to achieve her Australian

dream (Randolph & Tice, 2014).

Answer to question 2:

Year Weekly Income Yearly Income Four Year Average Price change

1994–95 $ 1,340 $ 69,680

1995–96 $ 1,297 $ 67,444

1996–97 $ 1,342 $ 69,784

1997–98 $ 1,400 $ 72,800 69,927

1999–2000 $ 1,534 $ 79,768 72,449 3.61%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BUSINESS FINANCE

4

2000–01 $ 1,475 $ 76,700 74,763 3.19%

2002–03 $ 1,525 $ 79,300 77,142 3.18%

2003–04(a) $ 1,582 $ 82,264 79,508 3.07%

2005–06(a) $ 1,681 $ 87,412 81,419 2.40%

2007–08(a) $ 1,967 $ 102,284 87,815 7.86%

2009–10(a) $ 1,870 $ 97,240 92,300 5.11%

2011–12(a) $ 1,914 $ 99,528 96,616 4.68%

2013–14(a) $ 2,016 $ 104,832 100,971 4.51%

2015–16(a) $ 2,055 $ 106,860 102,115 1.13%

Average 3.87%

Growth in Income 3.87%

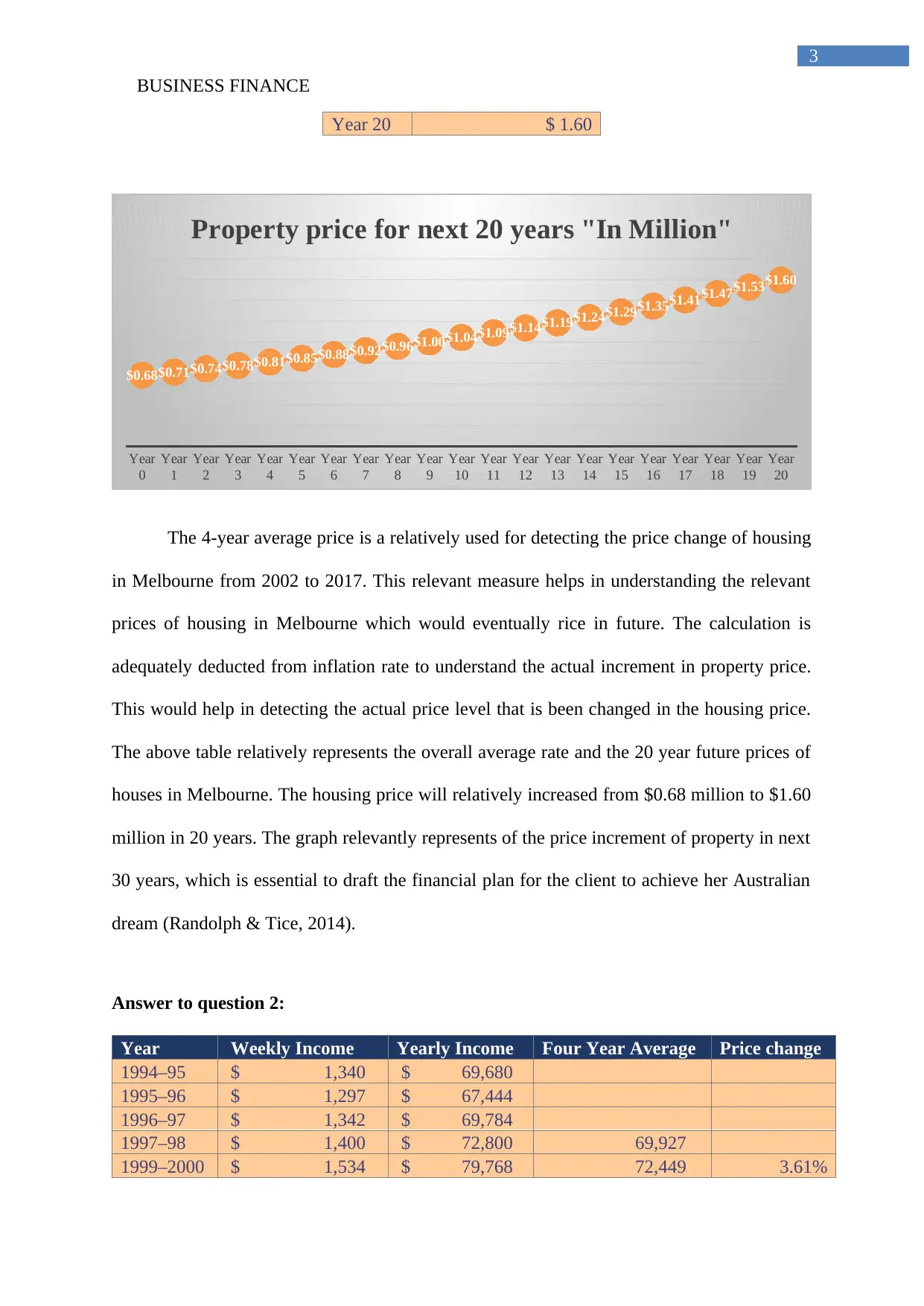

The calculation conducted in the above table mainly helps in understanding the level

of income growth obtained by citizens in Melbourne. The calculations on 4-year average

income of the citizens are relatively conducted to identify the income growth for previous 20

years. This identification of the income growth would eventually help in detecting the future

income that will be generated by salaried person. The average growth rate is relatively

detected by averaging the overall increment in income that is obtained by the individual

citizens of Melbourne (Gauder, Houssard & Orsmond, 2014).

Year Amount "Million"

Amount

"Million"

Year 0 $ 0.68 $ 0.08

Year 1 $ 0.71 $ 0.08

Year 2 $ 0.74 $ 0.09

Year 3 $ 0.78 $ 0.09

Year 4 $ 0.81 $ 0.09

Year 5 $ 0.85 $ 0.10

Year 6 $ 0.88 $ 0.10

Year 7 $ 0.92 $ 0.10

Year 8 $ 0.96 $ 0.11

Year 9 $ 1.00 $ 0.11

Year 10 $ 1.04 $ 0.12

Year 11 $ 1.09 $ 0.12

Year 12 $ 1.14 $ 0.13

Year 13 $ 1.19 $ 0.13

Year 14 $ 1.24 $ 0.14

Year 15 $ 1.29 $ 0.14

4

2000–01 $ 1,475 $ 76,700 74,763 3.19%

2002–03 $ 1,525 $ 79,300 77,142 3.18%

2003–04(a) $ 1,582 $ 82,264 79,508 3.07%

2005–06(a) $ 1,681 $ 87,412 81,419 2.40%

2007–08(a) $ 1,967 $ 102,284 87,815 7.86%

2009–10(a) $ 1,870 $ 97,240 92,300 5.11%

2011–12(a) $ 1,914 $ 99,528 96,616 4.68%

2013–14(a) $ 2,016 $ 104,832 100,971 4.51%

2015–16(a) $ 2,055 $ 106,860 102,115 1.13%

Average 3.87%

Growth in Income 3.87%

The calculation conducted in the above table mainly helps in understanding the level

of income growth obtained by citizens in Melbourne. The calculations on 4-year average

income of the citizens are relatively conducted to identify the income growth for previous 20

years. This identification of the income growth would eventually help in detecting the future

income that will be generated by salaried person. The average growth rate is relatively

detected by averaging the overall increment in income that is obtained by the individual

citizens of Melbourne (Gauder, Houssard & Orsmond, 2014).

Year Amount "Million"

Amount

"Million"

Year 0 $ 0.68 $ 0.08

Year 1 $ 0.71 $ 0.08

Year 2 $ 0.74 $ 0.09

Year 3 $ 0.78 $ 0.09

Year 4 $ 0.81 $ 0.09

Year 5 $ 0.85 $ 0.10

Year 6 $ 0.88 $ 0.10

Year 7 $ 0.92 $ 0.10

Year 8 $ 0.96 $ 0.11

Year 9 $ 1.00 $ 0.11

Year 10 $ 1.04 $ 0.12

Year 11 $ 1.09 $ 0.12

Year 12 $ 1.14 $ 0.13

Year 13 $ 1.19 $ 0.13

Year 14 $ 1.24 $ 0.14

Year 15 $ 1.29 $ 0.14

BUSINESS FINANCE

5

Year 16 $ 1.35 $ 0.15

Year 17 $ 1.41 $ 0.15

Year 18 $ 1.47 $ 0.16

Year 19 $ 1.53 $ 0.16

Year 20 $ 1.60 $ 0.17

Year

0

Year

1

Year

2

Year

3

Year

4

Year

5

Year

6

Year

7

Year

8

Year

9

Year

10

Year

11

Year

12

Year

13

Year

14

Year

15

Year

16

Year

17

Year

18

Year

19

Year

20

$0.08$0.08$0.09$0.09$0.09$0.10$0.10$0.10$0.11$0.11$0.12$0.12$0.13$0.13$0.14$0.14$0.15$0.15$0.16$0.16$0.17

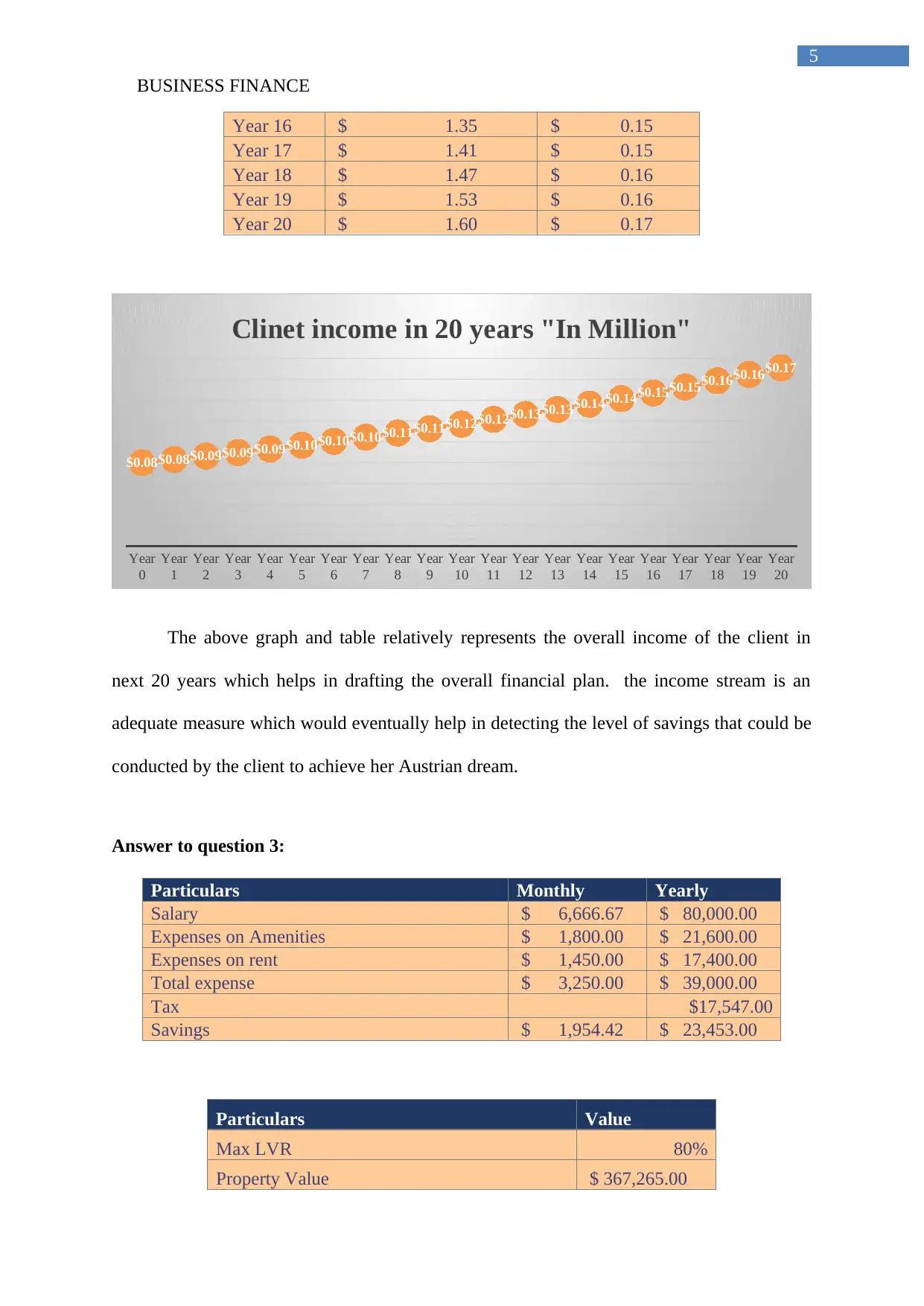

Clinet income in 20 years "In Million"

The above graph and table relatively represents the overall income of the client in

next 20 years which helps in drafting the overall financial plan. the income stream is an

adequate measure which would eventually help in detecting the level of savings that could be

conducted by the client to achieve her Austrian dream.

Answer to question 3:

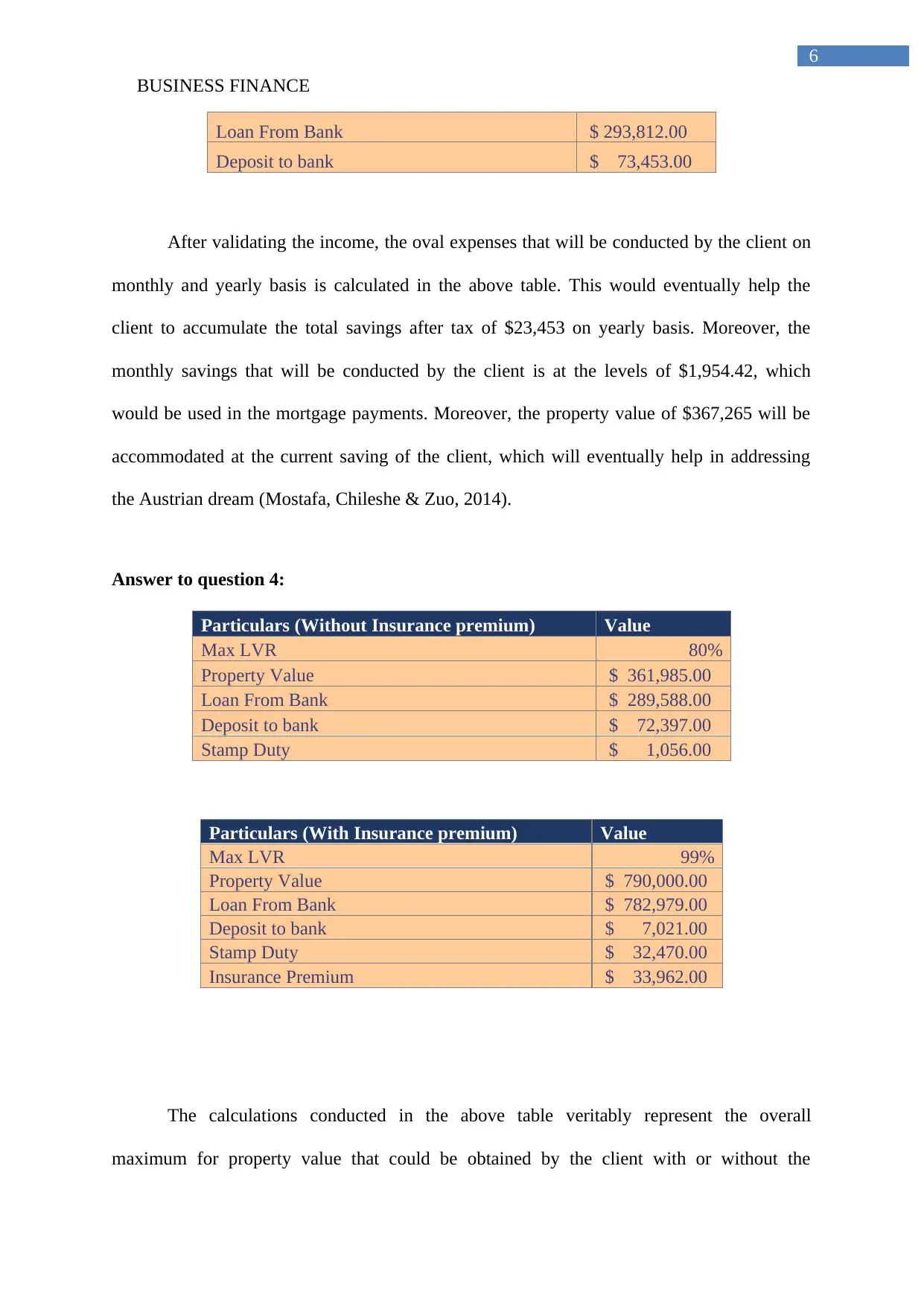

Particulars Monthly Yearly

Salary $ 6,666.67 $ 80,000.00

Expenses on Amenities $ 1,800.00 $ 21,600.00

Expenses on rent $ 1,450.00 $ 17,400.00

Total expense $ 3,250.00 $ 39,000.00

Tax $17,547.00

Savings $ 1,954.42 $ 23,453.00

Particulars Value

Max LVR 80%

Property Value $ 367,265.00

5

Year 16 $ 1.35 $ 0.15

Year 17 $ 1.41 $ 0.15

Year 18 $ 1.47 $ 0.16

Year 19 $ 1.53 $ 0.16

Year 20 $ 1.60 $ 0.17

Year

0

Year

1

Year

2

Year

3

Year

4

Year

5

Year

6

Year

7

Year

8

Year

9

Year

10

Year

11

Year

12

Year

13

Year

14

Year

15

Year

16

Year

17

Year

18

Year

19

Year

20

$0.08$0.08$0.09$0.09$0.09$0.10$0.10$0.10$0.11$0.11$0.12$0.12$0.13$0.13$0.14$0.14$0.15$0.15$0.16$0.16$0.17

Clinet income in 20 years "In Million"

The above graph and table relatively represents the overall income of the client in

next 20 years which helps in drafting the overall financial plan. the income stream is an

adequate measure which would eventually help in detecting the level of savings that could be

conducted by the client to achieve her Austrian dream.

Answer to question 3:

Particulars Monthly Yearly

Salary $ 6,666.67 $ 80,000.00

Expenses on Amenities $ 1,800.00 $ 21,600.00

Expenses on rent $ 1,450.00 $ 17,400.00

Total expense $ 3,250.00 $ 39,000.00

Tax $17,547.00

Savings $ 1,954.42 $ 23,453.00

Particulars Value

Max LVR 80%

Property Value $ 367,265.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BUSINESS FINANCE

6

Loan From Bank $ 293,812.00

Deposit to bank $ 73,453.00

After validating the income, the oval expenses that will be conducted by the client on

monthly and yearly basis is calculated in the above table. This would eventually help the

client to accumulate the total savings after tax of $23,453 on yearly basis. Moreover, the

monthly savings that will be conducted by the client is at the levels of $1,954.42, which

would be used in the mortgage payments. Moreover, the property value of $367,265 will be

accommodated at the current saving of the client, which will eventually help in addressing

the Austrian dream (Mostafa, Chileshe & Zuo, 2014).

Answer to question 4:

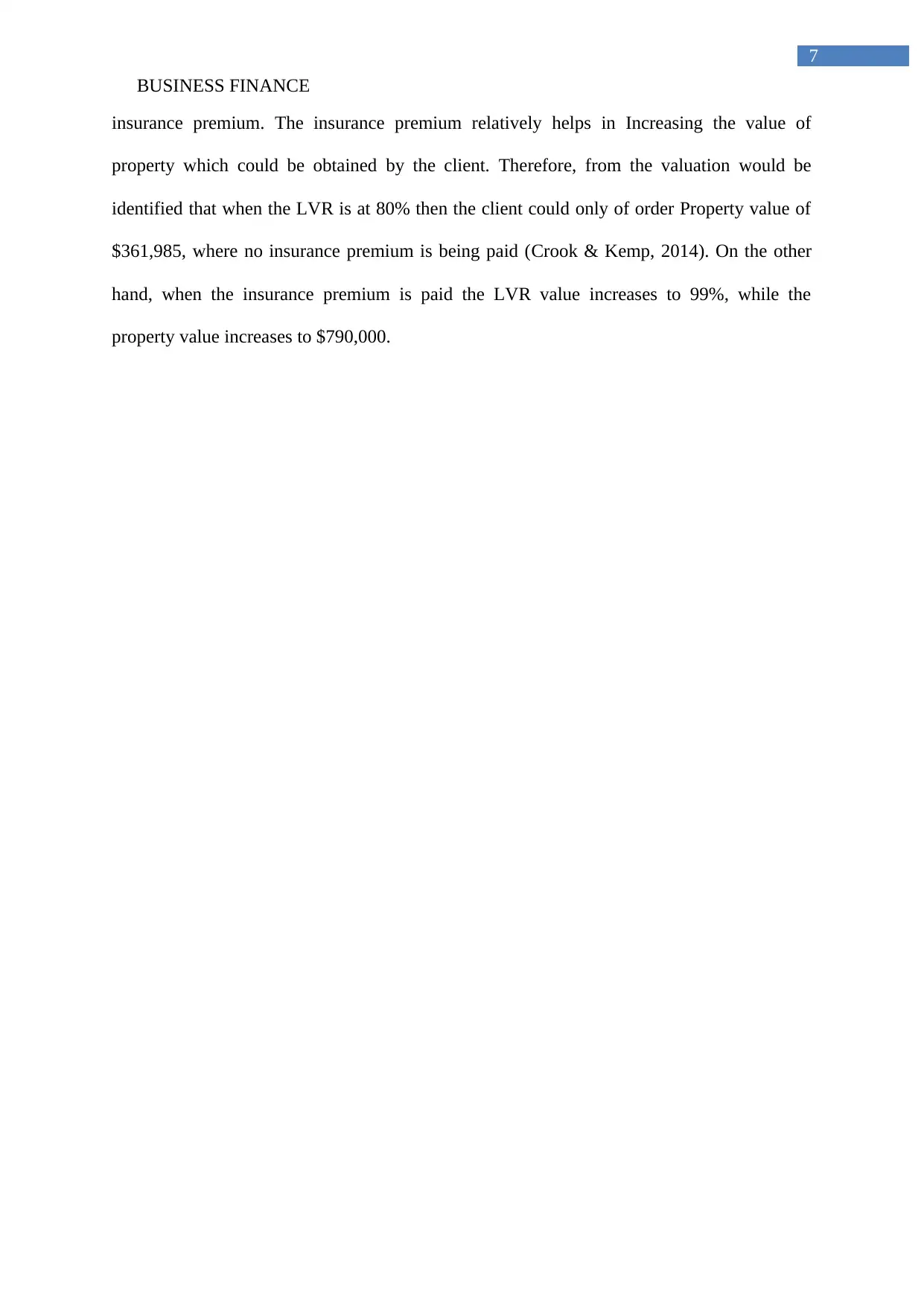

Particulars (Without Insurance premium) Value

Max LVR 80%

Property Value $ 361,985.00

Loan From Bank $ 289,588.00

Deposit to bank $ 72,397.00

Stamp Duty $ 1,056.00

Particulars (With Insurance premium) Value

Max LVR 99%

Property Value $ 790,000.00

Loan From Bank $ 782,979.00

Deposit to bank $ 7,021.00

Stamp Duty $ 32,470.00

Insurance Premium $ 33,962.00

The calculations conducted in the above table veritably represent the overall

maximum for property value that could be obtained by the client with or without the

6

Loan From Bank $ 293,812.00

Deposit to bank $ 73,453.00

After validating the income, the oval expenses that will be conducted by the client on

monthly and yearly basis is calculated in the above table. This would eventually help the

client to accumulate the total savings after tax of $23,453 on yearly basis. Moreover, the

monthly savings that will be conducted by the client is at the levels of $1,954.42, which

would be used in the mortgage payments. Moreover, the property value of $367,265 will be

accommodated at the current saving of the client, which will eventually help in addressing

the Austrian dream (Mostafa, Chileshe & Zuo, 2014).

Answer to question 4:

Particulars (Without Insurance premium) Value

Max LVR 80%

Property Value $ 361,985.00

Loan From Bank $ 289,588.00

Deposit to bank $ 72,397.00

Stamp Duty $ 1,056.00

Particulars (With Insurance premium) Value

Max LVR 99%

Property Value $ 790,000.00

Loan From Bank $ 782,979.00

Deposit to bank $ 7,021.00

Stamp Duty $ 32,470.00

Insurance Premium $ 33,962.00

The calculations conducted in the above table veritably represent the overall

maximum for property value that could be obtained by the client with or without the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BUSINESS FINANCE

7

insurance premium. The insurance premium relatively helps in Increasing the value of

property which could be obtained by the client. Therefore, from the valuation would be

identified that when the LVR is at 80% then the client could only of order Property value of

$361,985, where no insurance premium is being paid (Crook & Kemp, 2014). On the other

hand, when the insurance premium is paid the LVR value increases to 99%, while the

property value increases to $790,000.

7

insurance premium. The insurance premium relatively helps in Increasing the value of

property which could be obtained by the client. Therefore, from the valuation would be

identified that when the LVR is at 80% then the client could only of order Property value of

$361,985, where no insurance premium is being paid (Crook & Kemp, 2014). On the other

hand, when the insurance premium is paid the LVR value increases to 99%, while the

property value increases to $790,000.

8

BUSINESS FINANCE

Answer to question 5:

Yea

r

Property

price Income

Expens

e Tax Saved

Savings

Target Income 20% upfront Stamp duty Difference

0

$

684,000

$

80,000

$

39,000

$

17,547

$

50,000

$

73,453

$

23,453

$

136,800

$

31,868

$

(95,215)

1

$

713,599

$

83,099

$

39,913

$

18,554

$

73,453

$

98,086

$

24,632

$

142,720

$

12,986

$

(57,621)

2

$

744,479

$

86,317

$

40,847

$

19,600

$

98,086

$

123,957

$

25,871

$

148,896

$

13,981

$

(38,920)

3

$

776,694

$

89,661

$

41,802

$

20,806

$

123,957

$

151,009

$

27,052

$

155,339

$

15,019

$

(19,349)

4

$

810,304

$

93,133

$

42,781

$

22,091

$

151,009

$

179,271

$

28,262

$

162,061

$

16,102

$

1,108

5

$

845,369

$

96,741

$

43,782

$

23,426

$

179,271

$

208,804

$

29,533

$

169,074

$

17,231

$

22,499

6

$

881,951

$

100,488

$

44,806

$

24,812

$

208,804

$

239,674

$

30,870

$

176,390

$

18,409

$

44,874

7

$

920,115

$

104,380

$

45,855

$

26,252

$

239,674

$

271,947

$

32,273

$

184,023

$

19,639

$

68,285

8

$

959,932

$

108,423

$

46,928

$

27,748

$

271,947

$

305,694

$

33,747

$

191,986

$

20,921

$

92,786

9

$

1,001,471

$

112,622

$

48,026

$

29,302

$

305,694

$

340,989

$

35,295

$

200,294

$

22,259

$

118,435

10

$

1,044,808

$

116,985

$

49,149

$

30,916

$

340,989

$

377,908

$

36,919

$

208,962

$

23,655

$

145,291

11

$

1,090,020

$

121,516

$

50,300

$

32,592

$

377,908

$

416,532

$

38,624

$

218,004

$

25,112

$

173,416

12

$

1,137,189

$

126,222

$

51,477

$

34,334

$

416,532

$

456,944

$

40,412

$

227,438

$

26,631

$

202,875

BUSINESS FINANCE

Answer to question 5:

Yea

r

Property

price Income

Expens

e Tax Saved

Savings

Target Income 20% upfront Stamp duty Difference

0

$

684,000

$

80,000

$

39,000

$

17,547

$

50,000

$

73,453

$

23,453

$

136,800

$

31,868

$

(95,215)

1

$

713,599

$

83,099

$

39,913

$

18,554

$

73,453

$

98,086

$

24,632

$

142,720

$

12,986

$

(57,621)

2

$

744,479

$

86,317

$

40,847

$

19,600

$

98,086

$

123,957

$

25,871

$

148,896

$

13,981

$

(38,920)

3

$

776,694

$

89,661

$

41,802

$

20,806

$

123,957

$

151,009

$

27,052

$

155,339

$

15,019

$

(19,349)

4

$

810,304

$

93,133

$

42,781

$

22,091

$

151,009

$

179,271

$

28,262

$

162,061

$

16,102

$

1,108

5

$

845,369

$

96,741

$

43,782

$

23,426

$

179,271

$

208,804

$

29,533

$

169,074

$

17,231

$

22,499

6

$

881,951

$

100,488

$

44,806

$

24,812

$

208,804

$

239,674

$

30,870

$

176,390

$

18,409

$

44,874

7

$

920,115

$

104,380

$

45,855

$

26,252

$

239,674

$

271,947

$

32,273

$

184,023

$

19,639

$

68,285

8

$

959,932

$

108,423

$

46,928

$

27,748

$

271,947

$

305,694

$

33,747

$

191,986

$

20,921

$

92,786

9

$

1,001,471

$

112,622

$

48,026

$

29,302

$

305,694

$

340,989

$

35,295

$

200,294

$

22,259

$

118,435

10

$

1,044,808

$

116,985

$

49,149

$

30,916

$

340,989

$

377,908

$

36,919

$

208,962

$

23,655

$

145,291

11

$

1,090,020

$

121,516

$

50,300

$

32,592

$

377,908

$

416,532

$

38,624

$

218,004

$

25,112

$

173,416

12

$

1,137,189

$

126,222

$

51,477

$

34,334

$

416,532

$

456,944

$

40,412

$

227,438

$

26,631

$

202,875

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

BUSINESS FINANCE

13

$

1,186,398

$

131,111

$

52,681

$

36,143

$

456,944

$

499,231

$

42,287

$

237,280

$

28,216

$

233,735

14

$

1,237,737

$

136,190

$

53,914

$

38,022

$

499,231

$

543,485

$

44,254

$

247,547

$

29,870

$

266,067

15

$

1,291,298

$

141,465

$

55,175

$

39,974

$

543,485

$

589,801

$

46,316

$

258,260

$

31,595

$

299,946

16

$

1,347,177

$

146,944

$

56,467

$

42,001

$

589,801

$

638,277

$

48,477

$

269,435

$

33,395

$

335,446

17

$

1,405,473

$

152,635

$

57,788

$

44,107

$

638,277

$

689,018

$

50,741

$

281,095

$

35,273

$

372,650

18

$

1,466,293

$

158,547

$

59,140

$

46,294

$

689,018

$

742,131

$

53,113

$

293,259

$

37,232

$

411,640

19

$

1,529,744

$

164,688

$

60,524

$

48,566

$

742,131

$

797,729

$

55,598

$

305,949

$

39,276

$

452,504

20

$

1,595,941

$

171,067

$

61,940

$

50,927

$

797,729

$

855,930

$

58,201

$

319,188

$

41,408

$

495,333

Ye

ar

Property

price Income

Expen

se Tax Saved

Savings

Target

5%

upfront

Insurance

premium

Stamp

duty

Total

payment Amount

0

$

684,000

$

80,000

$

39,000

$

17,547

$

50,000

$

73,453

$

34,200

$

20,222

$

31,868

$

86,290

$

(12,837)

1

$

713,599

$

83,099

$

39,913

$

18,554

$

73,453

$

98,086

$

35,680

$

21,097

$

12,986

$

69,763

$

28,322

2

$

744,479

$

86,317

$

40,847

$

19,600

$

98,086

$

123,957

$

37,224

$

22,010

$

13,981

$

73,215

$

50,741

3

$

776,694

$

89,661

$

41,802

$

20,806

$

123,957

$

151,009

$

38,835

$

22,962

$

15,019

$

76,816

$

74,193

4

$

810,304

$

93,133

$

42,781

$

22,091

$

151,009

$

179,271

$

40,515

$

23,956

$

16,102

$

80,573

$

98,698

5 $ $ $ $ $ $ $ $ $ $ $

BUSINESS FINANCE

13

$

1,186,398

$

131,111

$

52,681

$

36,143

$

456,944

$

499,231

$

42,287

$

237,280

$

28,216

$

233,735

14

$

1,237,737

$

136,190

$

53,914

$

38,022

$

499,231

$

543,485

$

44,254

$

247,547

$

29,870

$

266,067

15

$

1,291,298

$

141,465

$

55,175

$

39,974

$

543,485

$

589,801

$

46,316

$

258,260

$

31,595

$

299,946

16

$

1,347,177

$

146,944

$

56,467

$

42,001

$

589,801

$

638,277

$

48,477

$

269,435

$

33,395

$

335,446

17

$

1,405,473

$

152,635

$

57,788

$

44,107

$

638,277

$

689,018

$

50,741

$

281,095

$

35,273

$

372,650

18

$

1,466,293

$

158,547

$

59,140

$

46,294

$

689,018

$

742,131

$

53,113

$

293,259

$

37,232

$

411,640

19

$

1,529,744

$

164,688

$

60,524

$

48,566

$

742,131

$

797,729

$

55,598

$

305,949

$

39,276

$

452,504

20

$

1,595,941

$

171,067

$

61,940

$

50,927

$

797,729

$

855,930

$

58,201

$

319,188

$

41,408

$

495,333

Ye

ar

Property

price Income

Expen

se Tax Saved

Savings

Target

5%

upfront

Insurance

premium

Stamp

duty

Total

payment Amount

0

$

684,000

$

80,000

$

39,000

$

17,547

$

50,000

$

73,453

$

34,200

$

20,222

$

31,868

$

86,290

$

(12,837)

1

$

713,599

$

83,099

$

39,913

$

18,554

$

73,453

$

98,086

$

35,680

$

21,097

$

12,986

$

69,763

$

28,322

2

$

744,479

$

86,317

$

40,847

$

19,600

$

98,086

$

123,957

$

37,224

$

22,010

$

13,981

$

73,215

$

50,741

3

$

776,694

$

89,661

$

41,802

$

20,806

$

123,957

$

151,009

$

38,835

$

22,962

$

15,019

$

76,816

$

74,193

4

$

810,304

$

93,133

$

42,781

$

22,091

$

151,009

$

179,271

$

40,515

$

23,956

$

16,102

$

80,573

$

98,698

5 $ $ $ $ $ $ $ $ $ $ $

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

BUSINESS FINANCE

845,369 96,741 43,782 23,426 179,271 208,804 42,268 24,993 17,231 84,492 124,312

6

$

881,951

$

100,48

8

$

44,806

$

24,812

$

208,804

$

239,674

$

44,098

$

26,074

$

18,409

$

88,581

$

151,092

7

$

920,115

$

104,38

0

$

45,855

$

26,252

$

239,674

$

271,947

$

46,006

$

27,203

$

19,639

$

92,847

$

179,100

8

$

959,932

$

108,42

3

$

46,928

$

27,748

$

271,947

$

305,694

$

47,997

$

28,380

$

20,921

$

97,298

$

208,396

9

$

1,001,471

$

112,62

2

$

48,026

$

29,302

$

305,694

$

340,989

$

50,074

$

29,608

$

22,259

$

101,941

$

239,048

10

$

1,044,808

$

116,98

5

$

49,149

$

30,916

$

340,989

$

377,908

$

52,240

$

30,889

$

23,655

$

106,785

$

271,123

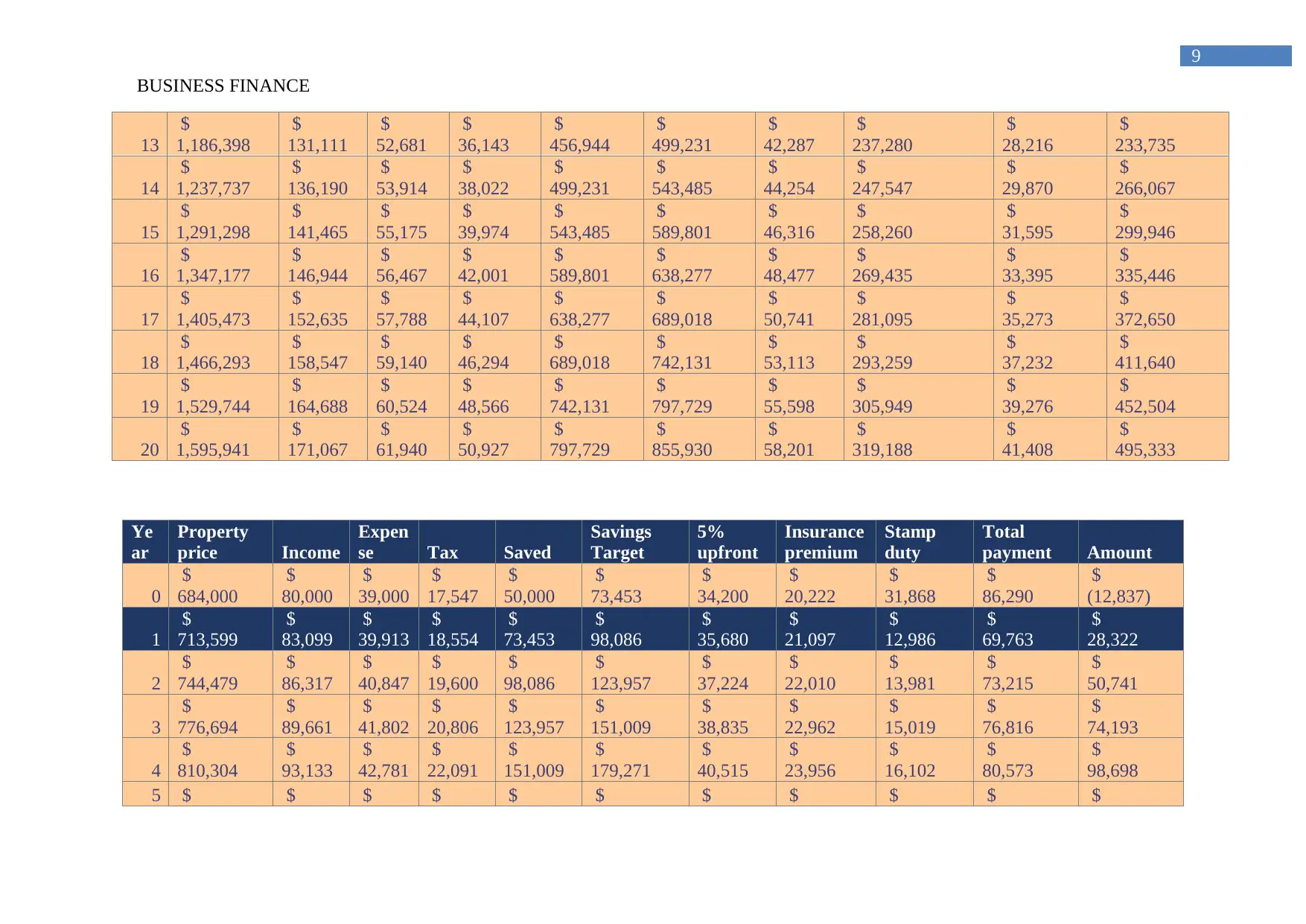

The calculations conducted in the above table relatively represents the ability of the client to purchase the property when the upfront

payment is at the levels of 5% and 20%. from the evaluation it is detected that within a friend payment of 20% the client could purchase house

in year 4, while within a friend payment of 5% the property can be purchased in year 1.

BUSINESS FINANCE

845,369 96,741 43,782 23,426 179,271 208,804 42,268 24,993 17,231 84,492 124,312

6

$

881,951

$

100,48

8

$

44,806

$

24,812

$

208,804

$

239,674

$

44,098

$

26,074

$

18,409

$

88,581

$

151,092

7

$

920,115

$

104,38

0

$

45,855

$

26,252

$

239,674

$

271,947

$

46,006

$

27,203

$

19,639

$

92,847

$

179,100

8

$

959,932

$

108,42

3

$

46,928

$

27,748

$

271,947

$

305,694

$

47,997

$

28,380

$

20,921

$

97,298

$

208,396

9

$

1,001,471

$

112,62

2

$

48,026

$

29,302

$

305,694

$

340,989

$

50,074

$

29,608

$

22,259

$

101,941

$

239,048

10

$

1,044,808

$

116,98

5

$

49,149

$

30,916

$

340,989

$

377,908

$

52,240

$

30,889

$

23,655

$

106,785

$

271,123

The calculations conducted in the above table relatively represents the ability of the client to purchase the property when the upfront

payment is at the levels of 5% and 20%. from the evaluation it is detected that within a friend payment of 20% the client could purchase house

in year 4, while within a friend payment of 5% the property can be purchased in year 1.

BUSINESS FINANCE

11

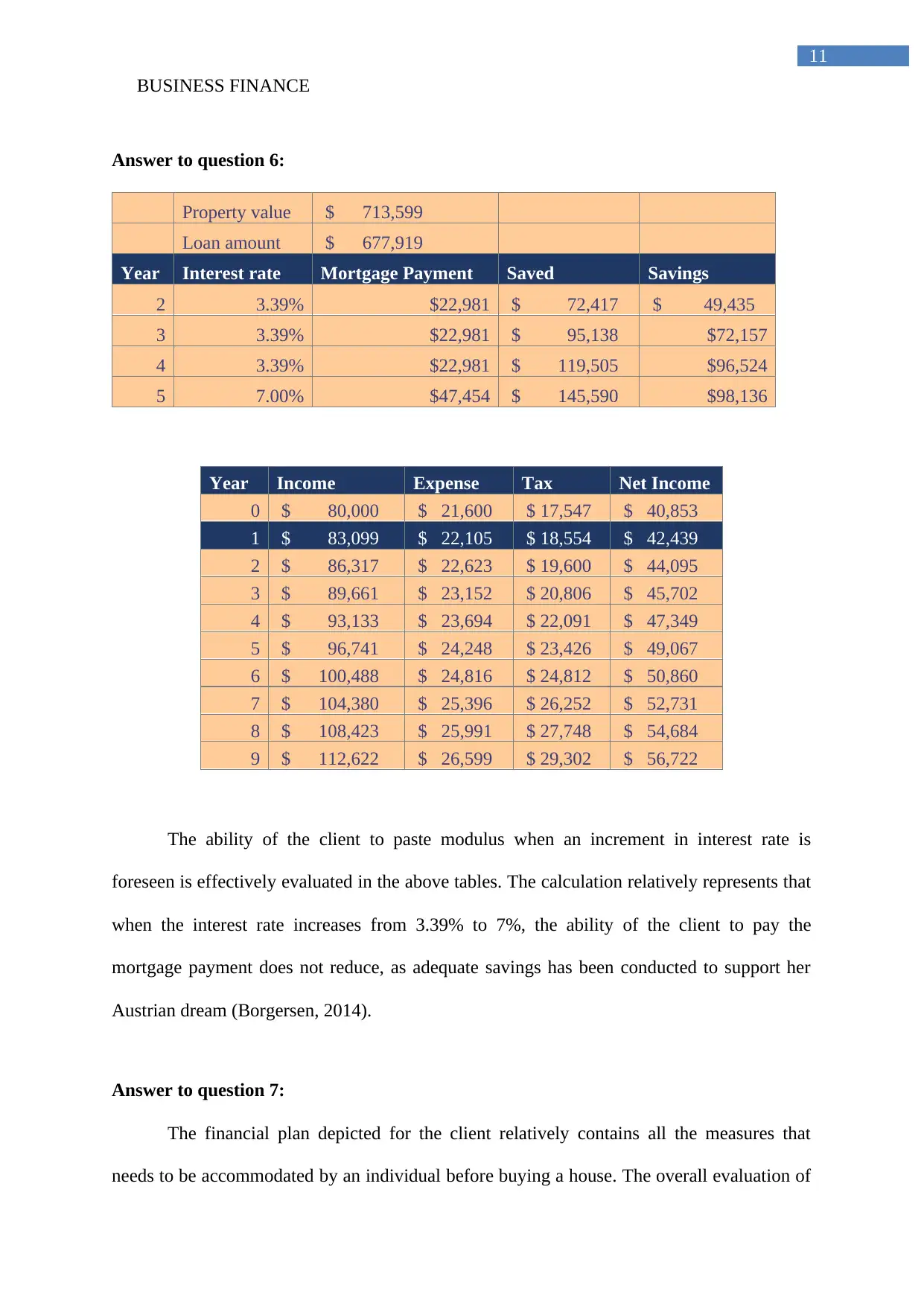

Answer to question 6:

Property value $ 713,599

Loan amount $ 677,919

Year Interest rate Mortgage Payment Saved Savings

2 3.39% $22,981 $ 72,417 $ 49,435

3 3.39% $22,981 $ 95,138 $72,157

4 3.39% $22,981 $ 119,505 $96,524

5 7.00% $47,454 $ 145,590 $98,136

Year Income Expense Tax Net Income

0 $ 80,000 $ 21,600 $ 17,547 $ 40,853

1 $ 83,099 $ 22,105 $ 18,554 $ 42,439

2 $ 86,317 $ 22,623 $ 19,600 $ 44,095

3 $ 89,661 $ 23,152 $ 20,806 $ 45,702

4 $ 93,133 $ 23,694 $ 22,091 $ 47,349

5 $ 96,741 $ 24,248 $ 23,426 $ 49,067

6 $ 100,488 $ 24,816 $ 24,812 $ 50,860

7 $ 104,380 $ 25,396 $ 26,252 $ 52,731

8 $ 108,423 $ 25,991 $ 27,748 $ 54,684

9 $ 112,622 $ 26,599 $ 29,302 $ 56,722

The ability of the client to paste modulus when an increment in interest rate is

foreseen is effectively evaluated in the above tables. The calculation relatively represents that

when the interest rate increases from 3.39% to 7%, the ability of the client to pay the

mortgage payment does not reduce, as adequate savings has been conducted to support her

Austrian dream (Borgersen, 2014).

Answer to question 7:

The financial plan depicted for the client relatively contains all the measures that

needs to be accommodated by an individual before buying a house. The overall evaluation of

11

Answer to question 6:

Property value $ 713,599

Loan amount $ 677,919

Year Interest rate Mortgage Payment Saved Savings

2 3.39% $22,981 $ 72,417 $ 49,435

3 3.39% $22,981 $ 95,138 $72,157

4 3.39% $22,981 $ 119,505 $96,524

5 7.00% $47,454 $ 145,590 $98,136

Year Income Expense Tax Net Income

0 $ 80,000 $ 21,600 $ 17,547 $ 40,853

1 $ 83,099 $ 22,105 $ 18,554 $ 42,439

2 $ 86,317 $ 22,623 $ 19,600 $ 44,095

3 $ 89,661 $ 23,152 $ 20,806 $ 45,702

4 $ 93,133 $ 23,694 $ 22,091 $ 47,349

5 $ 96,741 $ 24,248 $ 23,426 $ 49,067

6 $ 100,488 $ 24,816 $ 24,812 $ 50,860

7 $ 104,380 $ 25,396 $ 26,252 $ 52,731

8 $ 108,423 $ 25,991 $ 27,748 $ 54,684

9 $ 112,622 $ 26,599 $ 29,302 $ 56,722

The ability of the client to paste modulus when an increment in interest rate is

foreseen is effectively evaluated in the above tables. The calculation relatively represents that

when the interest rate increases from 3.39% to 7%, the ability of the client to pay the

mortgage payment does not reduce, as adequate savings has been conducted to support her

Austrian dream (Borgersen, 2014).

Answer to question 7:

The financial plan depicted for the client relatively contains all the measures that

needs to be accommodated by an individual before buying a house. The overall evaluation of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.