MA514 Business Finance: Applying Financial Concepts to Investment

VerifiedAdded on 2023/06/11

|12

|2584

|227

Report

AI Summary

This report provides a comprehensive financial analysis, focusing on property price forecasting in Sydney, income growth projections, and mortgage payment evaluations. It assesses a client's capability to achieve their 'Australian dream' by examining savings, loan options, and the impact of insurance premiums on property purchases. The analysis includes calculations for monthly savings, maximum loan amounts, and the effect of varying interest rates on mortgage payments. The report evaluates two loan scenarios: a 20% upfront payment without insurance and a 5% upfront payment with insurance, determining the timeline for property purchase under each condition. It also considers potential risks, such as income changes and government policy shifts, while highlighting the overall effectiveness of the financial plan. Desklib offers similar solved assignments and resources for students.

Running head: BUSINESS FINANCE

Business Finance

Name of the Student:

Name of the University:

Authors Note:

Business Finance

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BUSINESS FINANCE

1

Table of Contents

Answer: (Question 1).................................................................................................................2

Answer: (Question 2).................................................................................................................2

Answer: (Question 3).................................................................................................................3

Answer: (Question 4).................................................................................................................4

Answer: (Question 5).................................................................................................................5

Answer: (Question 6).................................................................................................................7

Answer: (Question 7).................................................................................................................8

Reference and Bibliography:......................................................................................................9

1

Table of Contents

Answer: (Question 1).................................................................................................................2

Answer: (Question 2).................................................................................................................2

Answer: (Question 3).................................................................................................................3

Answer: (Question 4).................................................................................................................4

Answer: (Question 5).................................................................................................................5

Answer: (Question 6).................................................................................................................7

Answer: (Question 7).................................................................................................................8

Reference and Bibliography:......................................................................................................9

BUSINESS FINANCE

2

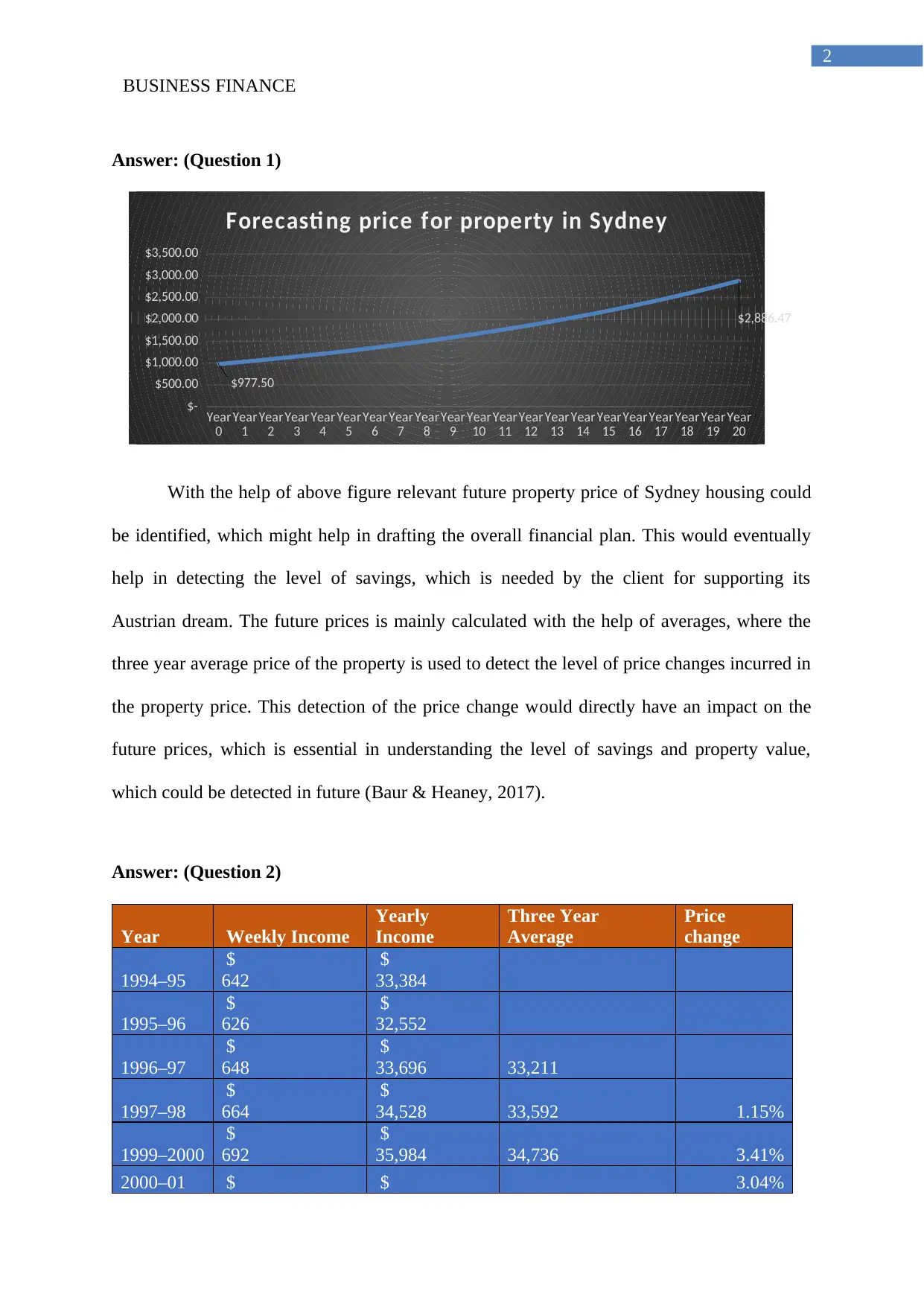

Answer: (Question 1)

Year

0 Year

1 Year

2 Year

3 Year

4 Year

5 Year

6 Year

7 Year

8 Year

9 Year

10 Year

11 Year

12 Year

13 Year

14 Year

15 Year

16 Year

17 Year

18 Year

19 Year

20

$-

$500.00

$1,000.00

$1,500.00

$2,000.00

$2,500.00

$3,000.00

$3,500.00

$977.50

$2,886.47

Forecasti ng price for property in Sydney

With the help of above figure relevant future property price of Sydney housing could

be identified, which might help in drafting the overall financial plan. This would eventually

help in detecting the level of savings, which is needed by the client for supporting its

Austrian dream. The future prices is mainly calculated with the help of averages, where the

three year average price of the property is used to detect the level of price changes incurred in

the property price. This detection of the price change would directly have an impact on the

future prices, which is essential in understanding the level of savings and property value,

which could be detected in future (Baur & Heaney, 2017).

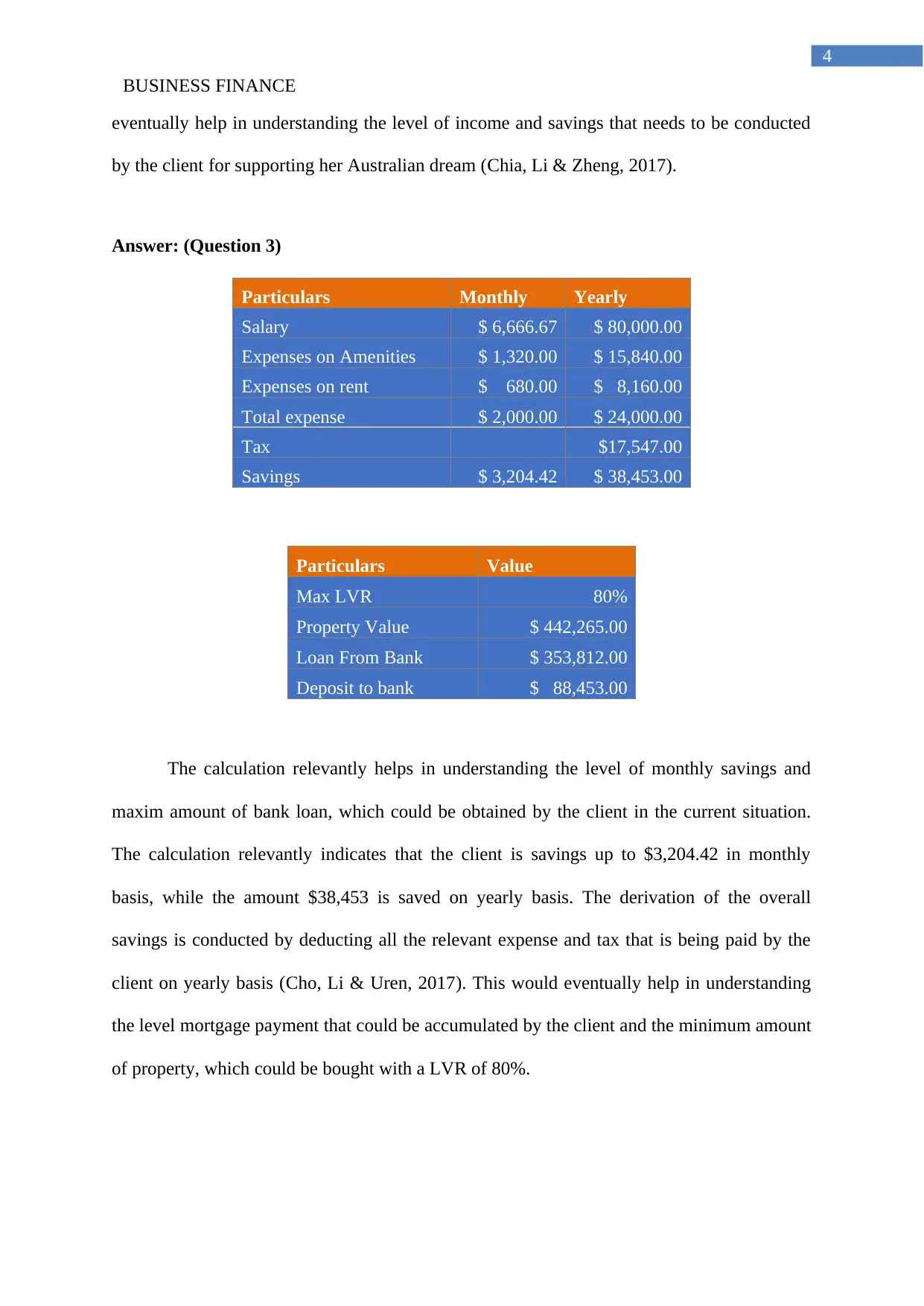

Answer: (Question 2)

Year Weekly Income

Yearly

Income

Three Year

Average

Price

change

1994–95

$

642

$

33,384

1995–96

$

626

$

32,552

1996–97

$

648

$

33,696 33,211

1997–98

$

664

$

34,528 33,592 1.15%

1999–2000

$

692

$

35,984 34,736 3.41%

2000–01 $ $ 3.04%

2

Answer: (Question 1)

Year

0 Year

1 Year

2 Year

3 Year

4 Year

5 Year

6 Year

7 Year

8 Year

9 Year

10 Year

11 Year

12 Year

13 Year

14 Year

15 Year

16 Year

17 Year

18 Year

19 Year

20

$-

$500.00

$1,000.00

$1,500.00

$2,000.00

$2,500.00

$3,000.00

$3,500.00

$977.50

$2,886.47

Forecasti ng price for property in Sydney

With the help of above figure relevant future property price of Sydney housing could

be identified, which might help in drafting the overall financial plan. This would eventually

help in detecting the level of savings, which is needed by the client for supporting its

Austrian dream. The future prices is mainly calculated with the help of averages, where the

three year average price of the property is used to detect the level of price changes incurred in

the property price. This detection of the price change would directly have an impact on the

future prices, which is essential in understanding the level of savings and property value,

which could be detected in future (Baur & Heaney, 2017).

Answer: (Question 2)

Year Weekly Income

Yearly

Income

Three Year

Average

Price

change

1994–95

$

642

$

33,384

1995–96

$

626

$

32,552

1996–97

$

648

$

33,696 33,211

1997–98

$

664

$

34,528 33,592 1.15%

1999–2000

$

692

$

35,984 34,736 3.41%

2000–01 $ $ 3.04%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BUSINESS FINANCE

3

709 36,868 35,793

2002–03

$

726

$

37,752 36,868 3.00%

2003–

04(a)

$

806

$

41,912 38,844 5.36%

2005–

06(a)

$

870

$

45,240 41,635 7.18%

2007–

08(a)

$

994

$

51,688 46,280 11.16%

2009–

10(a)

$

981

$

51,012 49,313 6.55%

2011–

12(a)

$

1,015

$

52,780 51,827 5.10%

2013–

14(a)

$

1,046

$

54,392 52,728 1.74%

2015–

16(a)

$

1,070

$

55,640 54,271 2.93%

Average 4.60%

Year

0 Year

1 Year

2 Year

3 Year

4 Year

5 Year

6 Year

7 Year

8 Year

9 Year

10 Year

11 Year

12 Year

13 Year

14 Year

15 Year

16 Year

17 Year

18 Year

19 Year

20

$-

$50.00

$100.00

$150.00

$200.00

$250.00

$80.00

$196.72

Forecasting growth of Clinet

The evaluation of above graph helps in understanding the level of income growth

which will incur by the client in 20 years’ time. The income growth calculation is mainly

valued with the help of average valuation, which is obtained by the salaried persons in

Sydney. Therefore, the calculation is mainly conducted with the help of previous 20 years of

income that is generated by salaried person in Sydney, which could help in understanding the

level of income. The income of client is anticipated to increase from $80,000 to 196,720 in

20 years’ time, which will be helpful in drafting the financial plan. This financial plan would

3

709 36,868 35,793

2002–03

$

726

$

37,752 36,868 3.00%

2003–

04(a)

$

806

$

41,912 38,844 5.36%

2005–

06(a)

$

870

$

45,240 41,635 7.18%

2007–

08(a)

$

994

$

51,688 46,280 11.16%

2009–

10(a)

$

981

$

51,012 49,313 6.55%

2011–

12(a)

$

1,015

$

52,780 51,827 5.10%

2013–

14(a)

$

1,046

$

54,392 52,728 1.74%

2015–

16(a)

$

1,070

$

55,640 54,271 2.93%

Average 4.60%

Year

0 Year

1 Year

2 Year

3 Year

4 Year

5 Year

6 Year

7 Year

8 Year

9 Year

10 Year

11 Year

12 Year

13 Year

14 Year

15 Year

16 Year

17 Year

18 Year

19 Year

20

$-

$50.00

$100.00

$150.00

$200.00

$250.00

$80.00

$196.72

Forecasting growth of Clinet

The evaluation of above graph helps in understanding the level of income growth

which will incur by the client in 20 years’ time. The income growth calculation is mainly

valued with the help of average valuation, which is obtained by the salaried persons in

Sydney. Therefore, the calculation is mainly conducted with the help of previous 20 years of

income that is generated by salaried person in Sydney, which could help in understanding the

level of income. The income of client is anticipated to increase from $80,000 to 196,720 in

20 years’ time, which will be helpful in drafting the financial plan. This financial plan would

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BUSINESS FINANCE

4

eventually help in understanding the level of income and savings that needs to be conducted

by the client for supporting her Australian dream (Chia, Li & Zheng, 2017).

Answer: (Question 3)

Particulars Monthly Yearly

Salary $ 6,666.67 $ 80,000.00

Expenses on Amenities $ 1,320.00 $ 15,840.00

Expenses on rent $ 680.00 $ 8,160.00

Total expense $ 2,000.00 $ 24,000.00

Tax $17,547.00

Savings $ 3,204.42 $ 38,453.00

Particulars Value

Max LVR 80%

Property Value $ 442,265.00

Loan From Bank $ 353,812.00

Deposit to bank $ 88,453.00

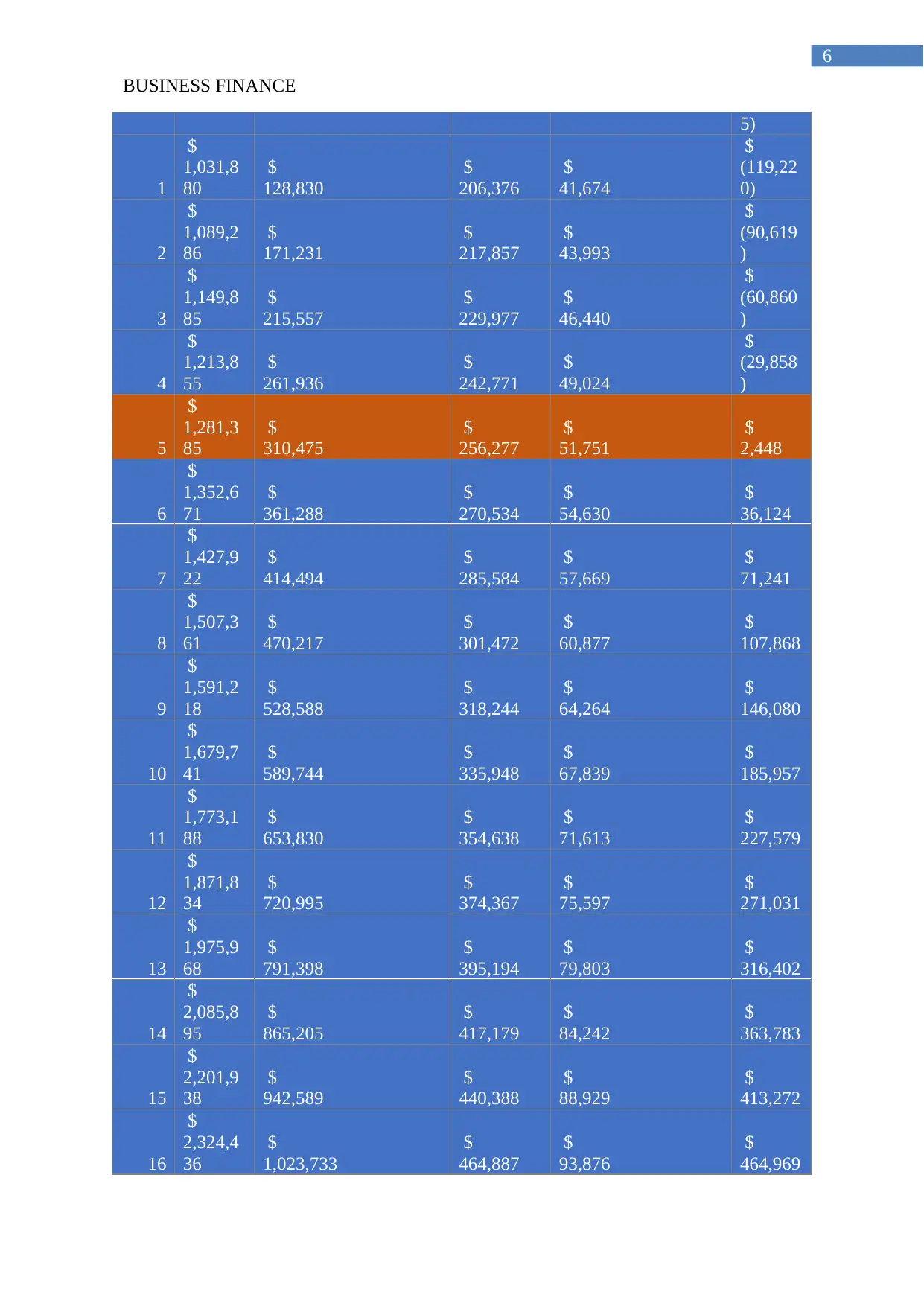

The calculation relevantly helps in understanding the level of monthly savings and

maxim amount of bank loan, which could be obtained by the client in the current situation.

The calculation relevantly indicates that the client is savings up to $3,204.42 in monthly

basis, while the amount $38,453 is saved on yearly basis. The derivation of the overall

savings is conducted by deducting all the relevant expense and tax that is being paid by the

client on yearly basis (Cho, Li & Uren, 2017). This would eventually help in understanding

the level mortgage payment that could be accumulated by the client and the minimum amount

of property, which could be bought with a LVR of 80%.

4

eventually help in understanding the level of income and savings that needs to be conducted

by the client for supporting her Australian dream (Chia, Li & Zheng, 2017).

Answer: (Question 3)

Particulars Monthly Yearly

Salary $ 6,666.67 $ 80,000.00

Expenses on Amenities $ 1,320.00 $ 15,840.00

Expenses on rent $ 680.00 $ 8,160.00

Total expense $ 2,000.00 $ 24,000.00

Tax $17,547.00

Savings $ 3,204.42 $ 38,453.00

Particulars Value

Max LVR 80%

Property Value $ 442,265.00

Loan From Bank $ 353,812.00

Deposit to bank $ 88,453.00

The calculation relevantly helps in understanding the level of monthly savings and

maxim amount of bank loan, which could be obtained by the client in the current situation.

The calculation relevantly indicates that the client is savings up to $3,204.42 in monthly

basis, while the amount $38,453 is saved on yearly basis. The derivation of the overall

savings is conducted by deducting all the relevant expense and tax that is being paid by the

client on yearly basis (Cho, Li & Uren, 2017). This would eventually help in understanding

the level mortgage payment that could be accumulated by the client and the minimum amount

of property, which could be bought with a LVR of 80%.

BUSINESS FINANCE

5

Answer: (Question 4)

Particulars (Without Insurance

premium) Value

Max LVR 80%

Property Value $ 440,877.00

Loan From Bank $ 352,701.60

Deposit to bank $ 88,175.40

Stamp Duty $ 277.60

Particulars (With Insurance

premium) Value

Max LVR 99%

Property Value $ 985,000.00

Loan From Bank $ 974,120.00

Deposit to bank $ 10,880.00

Stamp Duty $ 39,815.00

Insurance Premium $ 37,758.00

The calculation conducted on the above tables relevantly helps in drafting an adequate

financial plan for the client, where mortgage loan is with and without the insurance pre.

Under the insurance premium method, individuals can accumulate high end LVR mortgages,

which could reduce the overall deposit amount. Therefore, from the evaluation it could be

identified that without the insurance premium the client could only purchase property of

$440,877, while using the insurance premium the property value increases to $985,000. The

evaluation of the calculation relevantly indicates that without the insurance premium the

overall LVR is at the level of 80%, while it increases to a max of 99% if insurance premium

is included in the loan process (Easthope, Stone & Cheshire, 2017).

Answer: (Question 5)

Year

Propert

y price Savings Target

20%

upfront Stamp duty

Differe

nce

0 $

977,500

$

88,453

$

195,500

$

41,868

$

(148,91

5

Answer: (Question 4)

Particulars (Without Insurance

premium) Value

Max LVR 80%

Property Value $ 440,877.00

Loan From Bank $ 352,701.60

Deposit to bank $ 88,175.40

Stamp Duty $ 277.60

Particulars (With Insurance

premium) Value

Max LVR 99%

Property Value $ 985,000.00

Loan From Bank $ 974,120.00

Deposit to bank $ 10,880.00

Stamp Duty $ 39,815.00

Insurance Premium $ 37,758.00

The calculation conducted on the above tables relevantly helps in drafting an adequate

financial plan for the client, where mortgage loan is with and without the insurance pre.

Under the insurance premium method, individuals can accumulate high end LVR mortgages,

which could reduce the overall deposit amount. Therefore, from the evaluation it could be

identified that without the insurance premium the client could only purchase property of

$440,877, while using the insurance premium the property value increases to $985,000. The

evaluation of the calculation relevantly indicates that without the insurance premium the

overall LVR is at the level of 80%, while it increases to a max of 99% if insurance premium

is included in the loan process (Easthope, Stone & Cheshire, 2017).

Answer: (Question 5)

Year

Propert

y price Savings Target

20%

upfront Stamp duty

Differe

nce

0 $

977,500

$

88,453

$

195,500

$

41,868

$

(148,91

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BUSINESS FINANCE

6

5)

1

$

1,031,8

80

$

128,830

$

206,376

$

41,674

$

(119,22

0)

2

$

1,089,2

86

$

171,231

$

217,857

$

43,993

$

(90,619

)

3

$

1,149,8

85

$

215,557

$

229,977

$

46,440

$

(60,860

)

4

$

1,213,8

55

$

261,936

$

242,771

$

49,024

$

(29,858

)

5

$

1,281,3

85

$

310,475

$

256,277

$

51,751

$

2,448

6

$

1,352,6

71

$

361,288

$

270,534

$

54,630

$

36,124

7

$

1,427,9

22

$

414,494

$

285,584

$

57,669

$

71,241

8

$

1,507,3

61

$

470,217

$

301,472

$

60,877

$

107,868

9

$

1,591,2

18

$

528,588

$

318,244

$

64,264

$

146,080

10

$

1,679,7

41

$

589,744

$

335,948

$

67,839

$

185,957

11

$

1,773,1

88

$

653,830

$

354,638

$

71,613

$

227,579

12

$

1,871,8

34

$

720,995

$

374,367

$

75,597

$

271,031

13

$

1,975,9

68

$

791,398

$

395,194

$

79,803

$

316,402

14

$

2,085,8

95

$

865,205

$

417,179

$

84,242

$

363,783

15

$

2,201,9

38

$

942,589

$

440,388

$

88,929

$

413,272

16

$

2,324,4

36

$

1,023,733

$

464,887

$

93,876

$

464,969

6

5)

1

$

1,031,8

80

$

128,830

$

206,376

$

41,674

$

(119,22

0)

2

$

1,089,2

86

$

171,231

$

217,857

$

43,993

$

(90,619

)

3

$

1,149,8

85

$

215,557

$

229,977

$

46,440

$

(60,860

)

4

$

1,213,8

55

$

261,936

$

242,771

$

49,024

$

(29,858

)

5

$

1,281,3

85

$

310,475

$

256,277

$

51,751

$

2,448

6

$

1,352,6

71

$

361,288

$

270,534

$

54,630

$

36,124

7

$

1,427,9

22

$

414,494

$

285,584

$

57,669

$

71,241

8

$

1,507,3

61

$

470,217

$

301,472

$

60,877

$

107,868

9

$

1,591,2

18

$

528,588

$

318,244

$

64,264

$

146,080

10

$

1,679,7

41

$

589,744

$

335,948

$

67,839

$

185,957

11

$

1,773,1

88

$

653,830

$

354,638

$

71,613

$

227,579

12

$

1,871,8

34

$

720,995

$

374,367

$

75,597

$

271,031

13

$

1,975,9

68

$

791,398

$

395,194

$

79,803

$

316,402

14

$

2,085,8

95

$

865,205

$

417,179

$

84,242

$

363,783

15

$

2,201,9

38

$

942,589

$

440,388

$

88,929

$

413,272

16

$

2,324,4

36

$

1,023,733

$

464,887

$

93,876

$

464,969

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BUSINESS FINANCE

7

17

$

2,453,7

49

$

1,108,827

$

490,750

$

99,099

$

518,979

18

$

2,590,2

56

$

1,198,073

$

518,051

$

104,612

$

575,410

19

$

2,734,3

57

$

1,291,679

$

546,871

$

110,432

$

634,376

20

$

2,886,4

75

$

1,389,865

$

577,295

$

116,575

$

695,995

Yea

r Property price

Savings

Target

5%

upfront

Insurance

premium

Stam

p

duty

Amoun

t

0

$

977,500

$

88,453

$

48,875

$

37,532

$

41,86

8

$

(39,822

)

1

$

1,031,880

$

128,830

$

51,594

$

39,620

$

41,67

4

$

(4,058)

2

$

1,089,286

$

171,231

$

54,464

$

41,824

$

43,99

3

$

30,950

3

$

1,149,885

$

215,557

$

57,494

$

44,151

$

46,44

0

$

67,472

4

$

1,213,855

$

261,936

$

60,693

$

46,607

$

49,02

4

$

105,61

3

5

$

1,281,385

$

310,475

$

64,069

$

49,200

$

51,75

1

$

145,45

5

6

$

1,352,671

$

361,288

$

67,634

$

51,937

$

54,63

0

$

187,08

8

7

$

1,427,922

$

414,494

$

71,396

$

54,826

$

57,66

9

$

230,60

3

8

$

1,507,361

$

470,217

$

75,368

$

57,876

$

60,87

7

$

276,09

5

9

$

1,591,218

$

528,588

$

79,561

$

61,096

$

64,26

4

$

323,66

7

10 $

1,679,741

$

589,744

$

83,987

$

64,495

$

67,83

$

373,42

7

17

$

2,453,7

49

$

1,108,827

$

490,750

$

99,099

$

518,979

18

$

2,590,2

56

$

1,198,073

$

518,051

$

104,612

$

575,410

19

$

2,734,3

57

$

1,291,679

$

546,871

$

110,432

$

634,376

20

$

2,886,4

75

$

1,389,865

$

577,295

$

116,575

$

695,995

Yea

r Property price

Savings

Target

5%

upfront

Insurance

premium

Stam

p

duty

Amoun

t

0

$

977,500

$

88,453

$

48,875

$

37,532

$

41,86

8

$

(39,822

)

1

$

1,031,880

$

128,830

$

51,594

$

39,620

$

41,67

4

$

(4,058)

2

$

1,089,286

$

171,231

$

54,464

$

41,824

$

43,99

3

$

30,950

3

$

1,149,885

$

215,557

$

57,494

$

44,151

$

46,44

0

$

67,472

4

$

1,213,855

$

261,936

$

60,693

$

46,607

$

49,02

4

$

105,61

3

5

$

1,281,385

$

310,475

$

64,069

$

49,200

$

51,75

1

$

145,45

5

6

$

1,352,671

$

361,288

$

67,634

$

51,937

$

54,63

0

$

187,08

8

7

$

1,427,922

$

414,494

$

71,396

$

54,826

$

57,66

9

$

230,60

3

8

$

1,507,361

$

470,217

$

75,368

$

57,876

$

60,87

7

$

276,09

5

9

$

1,591,218

$

528,588

$

79,561

$

61,096

$

64,26

4

$

323,66

7

10 $

1,679,741

$

589,744

$

83,987

$

64,495

$

67,83

$

373,42

BUSINESS FINANCE

8

9 3

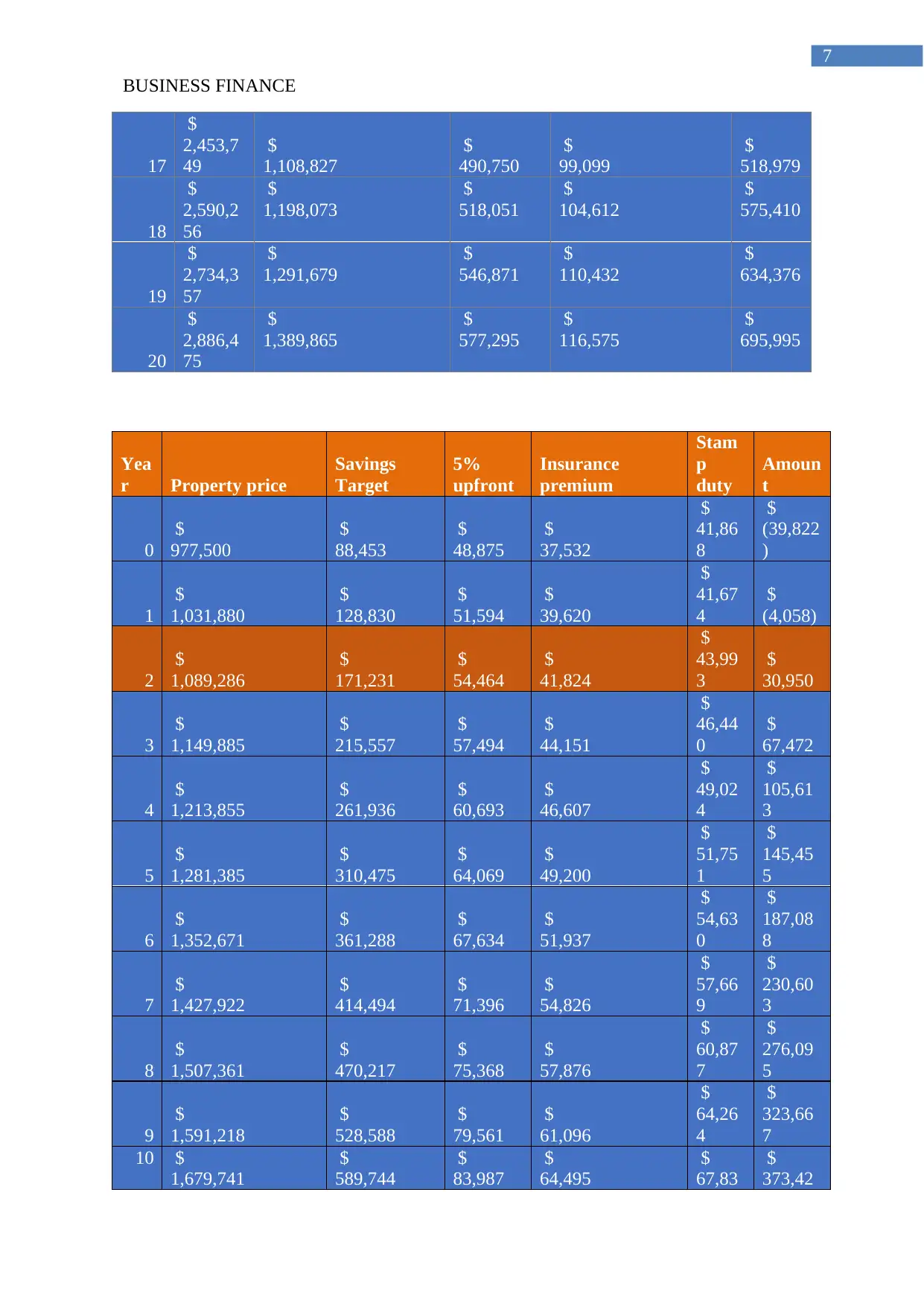

The above calculation relevantly indicates two type of loan process, which could be

used by the client, where 20% and 8% upfront payment needs to be conducted. From the

valuation it could be identified that with the upfront payment of 20% the client could buy the

house within 5th year, while using the 5% upfront payment reduction in property purchase

time could be seen to the level of year 2. In addition, from the valuation it could be detected

that the upfront payment of 20% calculation does not include any kind of insurance premium.

On the other hand, the calculation of 5% upfront payment mainly has an expense of

insurance, which needs to be conducted for minimising any kind of risk involved in

investment. This has allowed the client to purchase the property quickly without waiting to

accumulate the required savings for supporting her purchase of house (Gurran, & Bramley,

2017).

Answer: (Question 6)

Property value $ 1,089,286

Loan amount $ 1,034,822

Yea

r

Interest

rate

Mortgage

Payment Saved Savings

3 3.42% $35,391

$

84,023

$

48,632

4 3.42% $35,391

$

103,962 $68,571

5 3.42% $35,391

$

126,270 $90,880

6 7.00% $72,438

$

151,067 $78,630

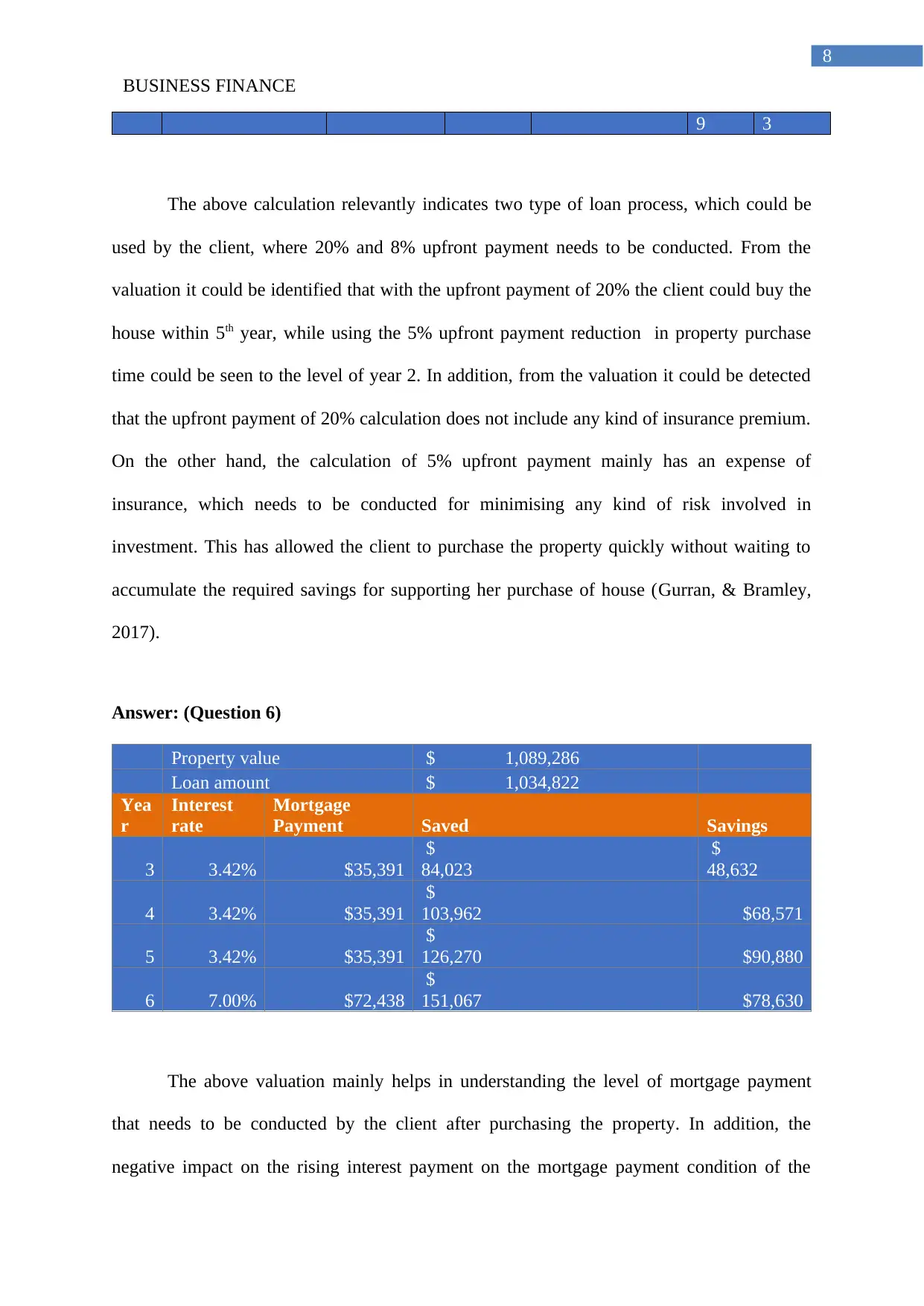

The above valuation mainly helps in understanding the level of mortgage payment

that needs to be conducted by the client after purchasing the property. In addition, the

negative impact on the rising interest payment on the mortgage payment condition of the

8

9 3

The above calculation relevantly indicates two type of loan process, which could be

used by the client, where 20% and 8% upfront payment needs to be conducted. From the

valuation it could be identified that with the upfront payment of 20% the client could buy the

house within 5th year, while using the 5% upfront payment reduction in property purchase

time could be seen to the level of year 2. In addition, from the valuation it could be detected

that the upfront payment of 20% calculation does not include any kind of insurance premium.

On the other hand, the calculation of 5% upfront payment mainly has an expense of

insurance, which needs to be conducted for minimising any kind of risk involved in

investment. This has allowed the client to purchase the property quickly without waiting to

accumulate the required savings for supporting her purchase of house (Gurran, & Bramley,

2017).

Answer: (Question 6)

Property value $ 1,089,286

Loan amount $ 1,034,822

Yea

r

Interest

rate

Mortgage

Payment Saved Savings

3 3.42% $35,391

$

84,023

$

48,632

4 3.42% $35,391

$

103,962 $68,571

5 3.42% $35,391

$

126,270 $90,880

6 7.00% $72,438

$

151,067 $78,630

The above valuation mainly helps in understanding the level of mortgage payment

that needs to be conducted by the client after purchasing the property. In addition, the

negative impact on the rising interest payment on the mortgage payment condition of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BUSINESS FINANCE

9

client is also evaluated. From the valuation, the financial capability of the client is mainly

detected, which could help in understanding her level of supporting the interest increment

from 3.42% to 7% in 4th year of loan. The client could effectively support the rising interest

rate, as her savings and income are adequate for supporting the mortgage payments (Hulse &

Yates, 2017).

Answer: (Question 7)

The financial plan mainly indicates a positive attribute of the client, which could help

in supporting her Australian dream. However, from the valuation it could be detected that any

kind of adverse action in her income would directly have a negative impact on her capability

to support the Sydney house. Any kind of problems related to the change in government

policy would also have negative impact on savings capability of the client, which would

directly impact her mortgage payment capability. Regardless of the drawback the overall

financial plan would be effective for the client in allowing her to achieve the Australian

dream.

9

client is also evaluated. From the valuation, the financial capability of the client is mainly

detected, which could help in understanding her level of supporting the interest increment

from 3.42% to 7% in 4th year of loan. The client could effectively support the rising interest

rate, as her savings and income are adequate for supporting the mortgage payments (Hulse &

Yates, 2017).

Answer: (Question 7)

The financial plan mainly indicates a positive attribute of the client, which could help

in supporting her Australian dream. However, from the valuation it could be detected that any

kind of adverse action in her income would directly have a negative impact on her capability

to support the Sydney house. Any kind of problems related to the change in government

policy would also have negative impact on savings capability of the client, which would

directly impact her mortgage payment capability. Regardless of the drawback the overall

financial plan would be effective for the client in allowing her to achieve the Australian

dream.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BUSINESS FINANCE

10

Reference and Bibliography:

Abs.gov.au. (2018). Ato.gov.au. Retrieved 29 May 2018, from

https://www.ato.gov.au/calculators-and-tools/simple-tax-calculator/

Baur, D. G., & Heaney, R. (2017). Bubbles in the Australian housing market. Pacific-Basin

Finance Journal, 44, 113-126.

Chia, W. M., Li, M., & Zheng, H. (2017). Behavioral heterogeneity in the Australian housing

market. Applied Economics, 49(9), 872-885.

Cho, Y., Li, S. M., & Uren, L. (2017). Negative Gearing and Welfare: A Quantitative Study

for the Australian Housing Market.

Easthope, H., Stone, W., & Cheshire, L. (2017). The decline of ‘advantageous

disadvantage’in gateway suburbs in Australia: The challenge of private housing market

settlement for newly arrived migrants. Urban Studies, 0042098017700791.

Gurran, N., & Bramley, G. (2017). Relationships Between Planning and the Housing Market.

In Urban Planning and the Housing Market (pp. 85-120). Palgrave Macmillan, London.

Hulse, K., & Yates, J. (2017). A private rental sector paradox: unpacking the effects of urban

restructuring on housing market dynamics. Housing studies, 32(3), 253-270.

Leal, H., Parsons, S., White, G., & Zurawski, A. (2017). Housing Market Turnover. RBA

Bulletin, March, 21-30.

Lee, C. L. (2017). An examination of the risk-return relation in the Australian housing

market. International Journal of Housing Markets and Analysis, 10(3), 431-449.\

10

Reference and Bibliography:

Abs.gov.au. (2018). Ato.gov.au. Retrieved 29 May 2018, from

https://www.ato.gov.au/calculators-and-tools/simple-tax-calculator/

Baur, D. G., & Heaney, R. (2017). Bubbles in the Australian housing market. Pacific-Basin

Finance Journal, 44, 113-126.

Chia, W. M., Li, M., & Zheng, H. (2017). Behavioral heterogeneity in the Australian housing

market. Applied Economics, 49(9), 872-885.

Cho, Y., Li, S. M., & Uren, L. (2017). Negative Gearing and Welfare: A Quantitative Study

for the Australian Housing Market.

Easthope, H., Stone, W., & Cheshire, L. (2017). The decline of ‘advantageous

disadvantage’in gateway suburbs in Australia: The challenge of private housing market

settlement for newly arrived migrants. Urban Studies, 0042098017700791.

Gurran, N., & Bramley, G. (2017). Relationships Between Planning and the Housing Market.

In Urban Planning and the Housing Market (pp. 85-120). Palgrave Macmillan, London.

Hulse, K., & Yates, J. (2017). A private rental sector paradox: unpacking the effects of urban

restructuring on housing market dynamics. Housing studies, 32(3), 253-270.

Leal, H., Parsons, S., White, G., & Zurawski, A. (2017). Housing Market Turnover. RBA

Bulletin, March, 21-30.

Lee, C. L. (2017). An examination of the risk-return relation in the Australian housing

market. International Journal of Housing Markets and Analysis, 10(3), 431-449.\

BUSINESS FINANCE

11

Lee, M. T., Lee, C. L., Lee, M. L., & Liao, C. Y. (2017). Price linkages between Australian

housing and stock markets: Wealth effect, credit effect or capital switching?. International

Journal of Housing Markets and Analysis, 10(2), 305-323.

Liu, S., & Gurran, N. (2017). Chinese investment in Australian housing: push and pull factors

and implications for understanding international housing demand. International Journal of

Housing Policy, 17(4), 489-511.

Stampduty.calculatorsaustralia.com.au. (2014). Stamp Duty Calculator. Retrieved 29 May

2018, from https://stampduty.calculatorsaustralia.com.au/

Wang, J., Koblyakova, A., Tiwari, P., & Croucher, J. S. (2018). Is the Australian housing

market in a bubble?. International Journal of Housing Markets and Analysis.

Warren-Myers, G., & Heywood, C. (2018). A New Demand-Supply Model to Enable

Sustainability in New Australian Housing. Sustainability, 10(2), 376.

Wong, S. Y., Susilawati, C., Miller, W., & Mardiasmo, D. (2018). Improving information

gathering and distribution on sustainability features in the Australian residential property

market. Journal of Cleaner Production, 184, 342-352.

Wood, G. A., & Ong, R. (2017). The Australian housing system: a quiet

revolution?. Australian Economic Review, 50(2), 197-204.

11

Lee, M. T., Lee, C. L., Lee, M. L., & Liao, C. Y. (2017). Price linkages between Australian

housing and stock markets: Wealth effect, credit effect or capital switching?. International

Journal of Housing Markets and Analysis, 10(2), 305-323.

Liu, S., & Gurran, N. (2017). Chinese investment in Australian housing: push and pull factors

and implications for understanding international housing demand. International Journal of

Housing Policy, 17(4), 489-511.

Stampduty.calculatorsaustralia.com.au. (2014). Stamp Duty Calculator. Retrieved 29 May

2018, from https://stampduty.calculatorsaustralia.com.au/

Wang, J., Koblyakova, A., Tiwari, P., & Croucher, J. S. (2018). Is the Australian housing

market in a bubble?. International Journal of Housing Markets and Analysis.

Warren-Myers, G., & Heywood, C. (2018). A New Demand-Supply Model to Enable

Sustainability in New Australian Housing. Sustainability, 10(2), 376.

Wong, S. Y., Susilawati, C., Miller, W., & Mardiasmo, D. (2018). Improving information

gathering and distribution on sustainability features in the Australian residential property

market. Journal of Cleaner Production, 184, 342-352.

Wood, G. A., & Ong, R. (2017). The Australian housing system: a quiet

revolution?. Australian Economic Review, 50(2), 197-204.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.