Business Finance Report: Capital Structure and Valuation

VerifiedAdded on 2020/01/16

|11

|1896

|188

Report

AI Summary

This finance report delves into the valuation of JB Hi Fi Ltd, examining its cost of capital, capital structure, and investment recommendations. The report begins with a re-estimation of the cost of capital, including the cost of bonds, cost of equity, and weighted average cost of capital (WACC). It then proceeds to the valuation of JB Hi Fi Ltd's shares using dividend growth and discounted cash flow models, providing an updated valuation based on provided financial data. Finally, it provides recommendations regarding the company's capital structure using the trade-off theory, analyzing the debt-equity ratio and suggesting strategies for financial improvement. The report includes several tables with calculations and interpretations to support its findings and recommendations.

Business Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

QUESTION 1..................................................................................................................................3

A Re-estimation of the cost of capital.........................................................................................3

B Cost of bond.............................................................................................................................3

QUESTION 2..................................................................................................................................6

A. Valuation of shares of JB Hi Fi Ltd..................................................................................6

b. Updating the valuation of JB Hi Fi Ltd...................................................................................7

c. Giving recommendations in relation to make investment in the company’s shares................9

QUESTION 3................................................................................................................................10

Giving recommendations to JB Hi Fi Ltd regarding capital structure by using trade-off theory

...................................................................................................................................................10

Table 1Current value of bond..........................................................................................................4

Table 2 Calculation of weighted average cost of capital.................................................................6

Table 3 Free cash flow and data of cash, debt and shares outstanding...........................................7

Table 4 Cost of equity......................................................................................................................7

Table 5Computation of enterprise value..........................................................................................8

Table 6Input for WACC..................................................................................................................8

Table 7Calculaiton of WACC.........................................................................................................8

Table 8Input table for valuation of shares.......................................................................................8

Table 9Second input sheet of valuation...........................................................................................9

Table 10 Calculation of fair value of shares....................................................................................9

QUESTION 1..................................................................................................................................3

A Re-estimation of the cost of capital.........................................................................................3

B Cost of bond.............................................................................................................................3

QUESTION 2..................................................................................................................................6

A. Valuation of shares of JB Hi Fi Ltd..................................................................................6

b. Updating the valuation of JB Hi Fi Ltd...................................................................................7

c. Giving recommendations in relation to make investment in the company’s shares................9

QUESTION 3................................................................................................................................10

Giving recommendations to JB Hi Fi Ltd regarding capital structure by using trade-off theory

...................................................................................................................................................10

Table 1Current value of bond..........................................................................................................4

Table 2 Calculation of weighted average cost of capital.................................................................6

Table 3 Free cash flow and data of cash, debt and shares outstanding...........................................7

Table 4 Cost of equity......................................................................................................................7

Table 5Computation of enterprise value..........................................................................................8

Table 6Input for WACC..................................................................................................................8

Table 7Calculaiton of WACC.........................................................................................................8

Table 8Input table for valuation of shares.......................................................................................8

Table 9Second input sheet of valuation...........................................................................................9

Table 10 Calculation of fair value of shares....................................................................................9

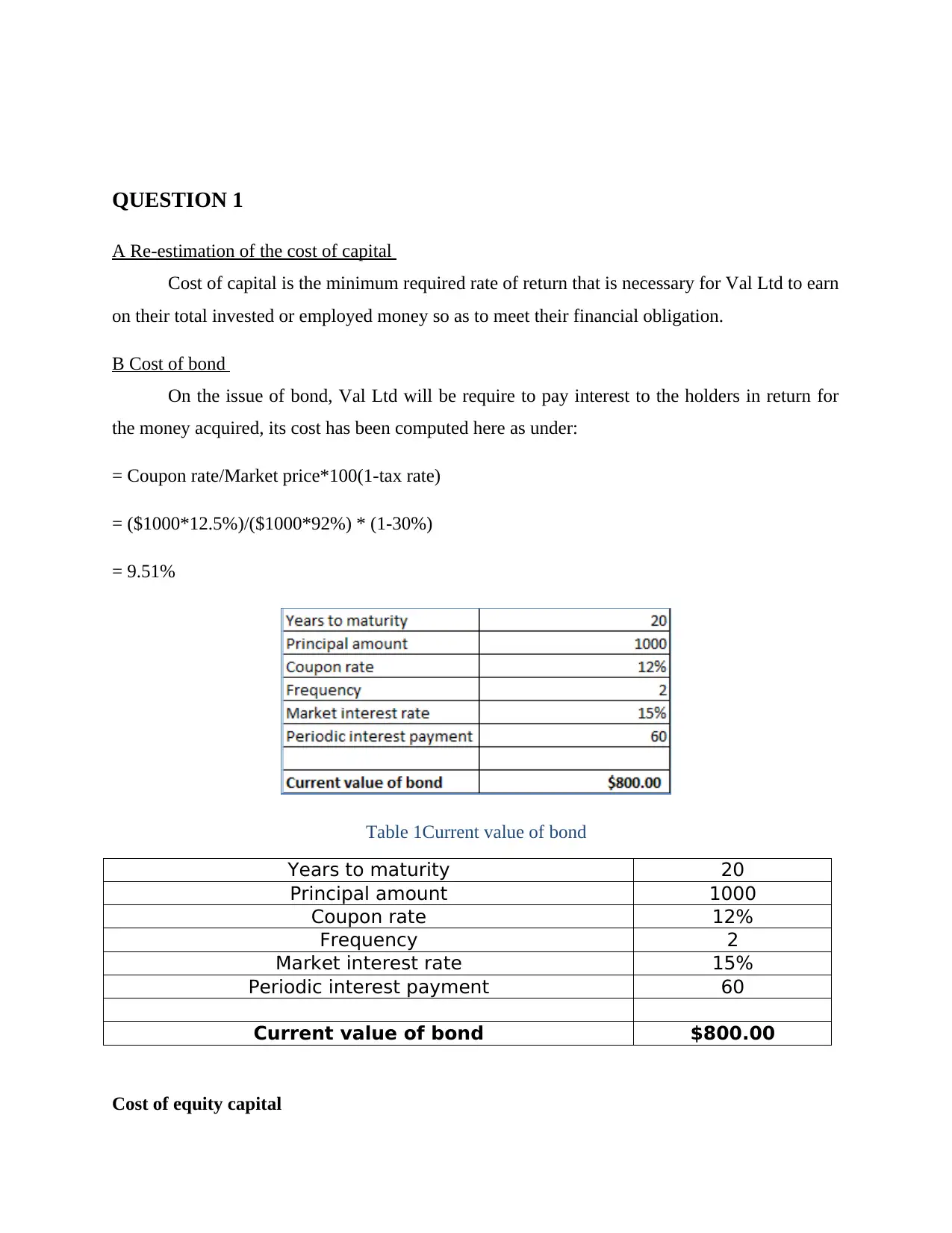

QUESTION 1

A Re-estimation of the cost of capital

Cost of capital is the minimum required rate of return that is necessary for Val Ltd to earn

on their total invested or employed money so as to meet their financial obligation.

B Cost of bond

On the issue of bond, Val Ltd will be require to pay interest to the holders in return for

the money acquired, its cost has been computed here as under:

= Coupon rate/Market price*100(1-tax rate)

= ($1000*12.5%)/($1000*92%) * (1-30%)

= 9.51%

Table 1Current value of bond

Years to maturity 20

Principal amount 1000

Coupon rate 12%

Frequency 2

Market interest rate 15%

Periodic interest payment 60

Current value of bond $800.00

Cost of equity capital

A Re-estimation of the cost of capital

Cost of capital is the minimum required rate of return that is necessary for Val Ltd to earn

on their total invested or employed money so as to meet their financial obligation.

B Cost of bond

On the issue of bond, Val Ltd will be require to pay interest to the holders in return for

the money acquired, its cost has been computed here as under:

= Coupon rate/Market price*100(1-tax rate)

= ($1000*12.5%)/($1000*92%) * (1-30%)

= 9.51%

Table 1Current value of bond

Years to maturity 20

Principal amount 1000

Coupon rate 12%

Frequency 2

Market interest rate 15%

Periodic interest payment 60

Current value of bond $800.00

Cost of equity capital

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

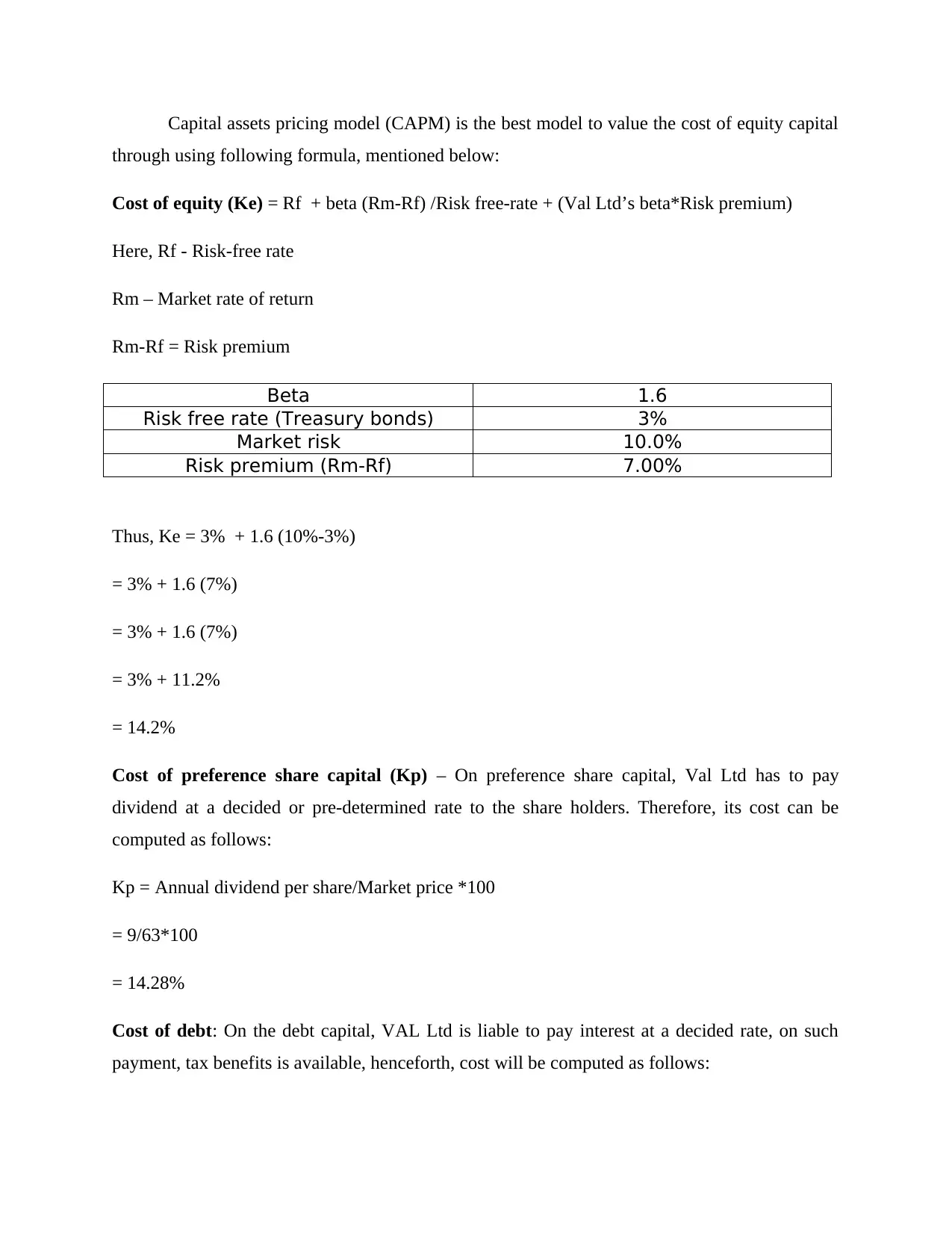

Capital assets pricing model (CAPM) is the best model to value the cost of equity capital

through using following formula, mentioned below:

Cost of equity (Ke) = Rf + beta (Rm-Rf) /Risk free-rate + (Val Ltd’s beta*Risk premium)

Here, Rf - Risk-free rate

Rm – Market rate of return

Rm-Rf = Risk premium

Beta 1.6

Risk free rate (Treasury bonds) 3%

Market risk 10.0%

Risk premium (Rm-Rf) 7.00%

Thus, Ke = 3% + 1.6 (10%-3%)

= 3% + 1.6 (7%)

= 3% + 1.6 (7%)

= 3% + 11.2%

= 14.2%

Cost of preference share capital (Kp) – On preference share capital, Val Ltd has to pay

dividend at a decided or pre-determined rate to the share holders. Therefore, its cost can be

computed as follows:

Kp = Annual dividend per share/Market price *100

= 9/63*100

= 14.28%

Cost of debt: On the debt capital, VAL Ltd is liable to pay interest at a decided rate, on such

payment, tax benefits is available, henceforth, cost will be computed as follows:

through using following formula, mentioned below:

Cost of equity (Ke) = Rf + beta (Rm-Rf) /Risk free-rate + (Val Ltd’s beta*Risk premium)

Here, Rf - Risk-free rate

Rm – Market rate of return

Rm-Rf = Risk premium

Beta 1.6

Risk free rate (Treasury bonds) 3%

Market risk 10.0%

Risk premium (Rm-Rf) 7.00%

Thus, Ke = 3% + 1.6 (10%-3%)

= 3% + 1.6 (7%)

= 3% + 1.6 (7%)

= 3% + 11.2%

= 14.2%

Cost of preference share capital (Kp) – On preference share capital, Val Ltd has to pay

dividend at a decided or pre-determined rate to the share holders. Therefore, its cost can be

computed as follows:

Kp = Annual dividend per share/Market price *100

= 9/63*100

= 14.28%

Cost of debt: On the debt capital, VAL Ltd is liable to pay interest at a decided rate, on such

payment, tax benefits is available, henceforth, cost will be computed as follows:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

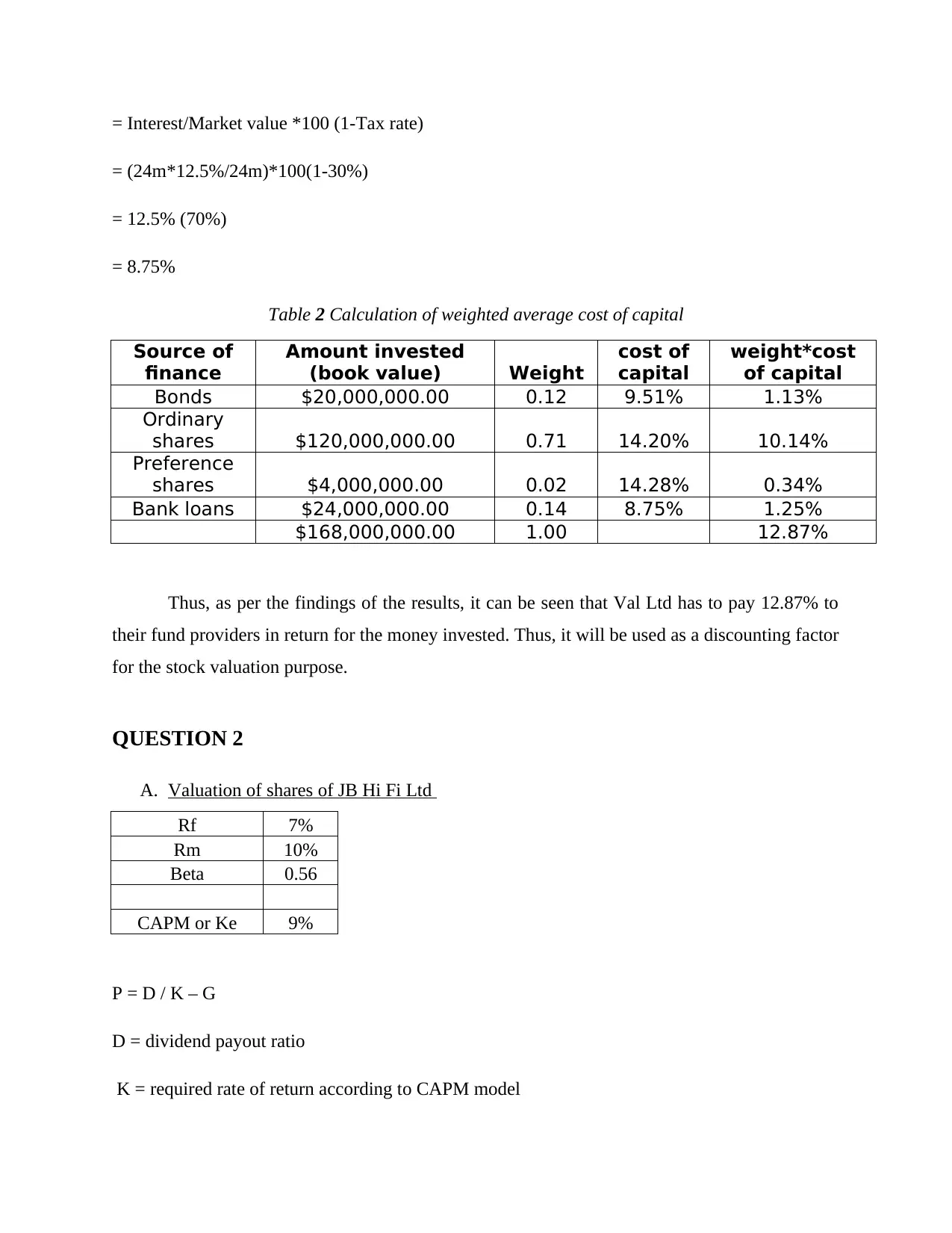

= Interest/Market value *100 (1-Tax rate)

= (24m*12.5%/24m)*100(1-30%)

= 12.5% (70%)

= 8.75%

Table 2 Calculation of weighted average cost of capital

Source of

finance

Amount invested

(book value) Weight

cost of

capital

weight*cost

of capital

Bonds $20,000,000.00 0.12 9.51% 1.13%

Ordinary

shares $120,000,000.00 0.71 14.20% 10.14%

Preference

shares $4,000,000.00 0.02 14.28% 0.34%

Bank loans $24,000,000.00 0.14 8.75% 1.25%

$168,000,000.00 1.00 12.87%

Thus, as per the findings of the results, it can be seen that Val Ltd has to pay 12.87% to

their fund providers in return for the money invested. Thus, it will be used as a discounting factor

for the stock valuation purpose.

QUESTION 2

A. Valuation of shares of JB Hi Fi Ltd

Rf 7%

Rm 10%

Beta 0.56

CAPM or Ke 9%

P = D / K – G

D = dividend payout ratio

K = required rate of return according to CAPM model

= (24m*12.5%/24m)*100(1-30%)

= 12.5% (70%)

= 8.75%

Table 2 Calculation of weighted average cost of capital

Source of

finance

Amount invested

(book value) Weight

cost of

capital

weight*cost

of capital

Bonds $20,000,000.00 0.12 9.51% 1.13%

Ordinary

shares $120,000,000.00 0.71 14.20% 10.14%

Preference

shares $4,000,000.00 0.02 14.28% 0.34%

Bank loans $24,000,000.00 0.14 8.75% 1.25%

$168,000,000.00 1.00 12.87%

Thus, as per the findings of the results, it can be seen that Val Ltd has to pay 12.87% to

their fund providers in return for the money invested. Thus, it will be used as a discounting factor

for the stock valuation purpose.

QUESTION 2

A. Valuation of shares of JB Hi Fi Ltd

Rf 7%

Rm 10%

Beta 0.56

CAPM or Ke 9%

P = D / K – G

D = dividend payout ratio

K = required rate of return according to CAPM model

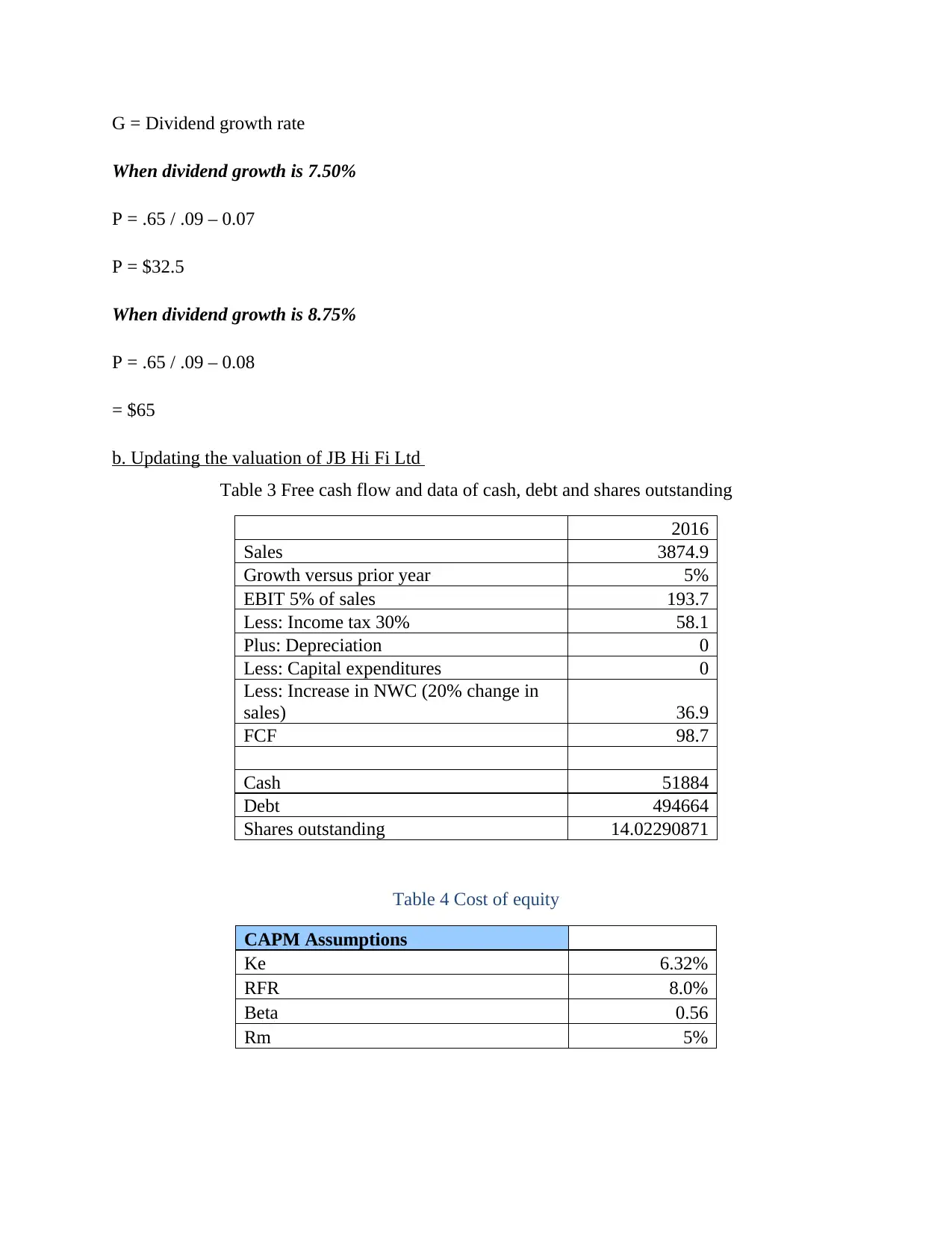

G = Dividend growth rate

When dividend growth is 7.50%

P = .65 / .09 – 0.07

P = $32.5

When dividend growth is 8.75%

P = .65 / .09 – 0.08

= $65

b. Updating the valuation of JB Hi Fi Ltd

Table 3 Free cash flow and data of cash, debt and shares outstanding

2016

Sales 3874.9

Growth versus prior year 5%

EBIT 5% of sales 193.7

Less: Income tax 30% 58.1

Plus: Depreciation 0

Less: Capital expenditures 0

Less: Increase in NWC (20% change in

sales) 36.9

FCF 98.7

Cash 51884

Debt 494664

Shares outstanding 14.02290871

Table 4 Cost of equity

CAPM Assumptions

Ke 6.32%

RFR 8.0%

Beta 0.56

Rm 5%

When dividend growth is 7.50%

P = .65 / .09 – 0.07

P = $32.5

When dividend growth is 8.75%

P = .65 / .09 – 0.08

= $65

b. Updating the valuation of JB Hi Fi Ltd

Table 3 Free cash flow and data of cash, debt and shares outstanding

2016

Sales 3874.9

Growth versus prior year 5%

EBIT 5% of sales 193.7

Less: Income tax 30% 58.1

Plus: Depreciation 0

Less: Capital expenditures 0

Less: Increase in NWC (20% change in

sales) 36.9

FCF 98.7

Cash 51884

Debt 494664

Shares outstanding 14.02290871

Table 4 Cost of equity

CAPM Assumptions

Ke 6.32%

RFR 8.0%

Beta 0.56

Rm 5%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

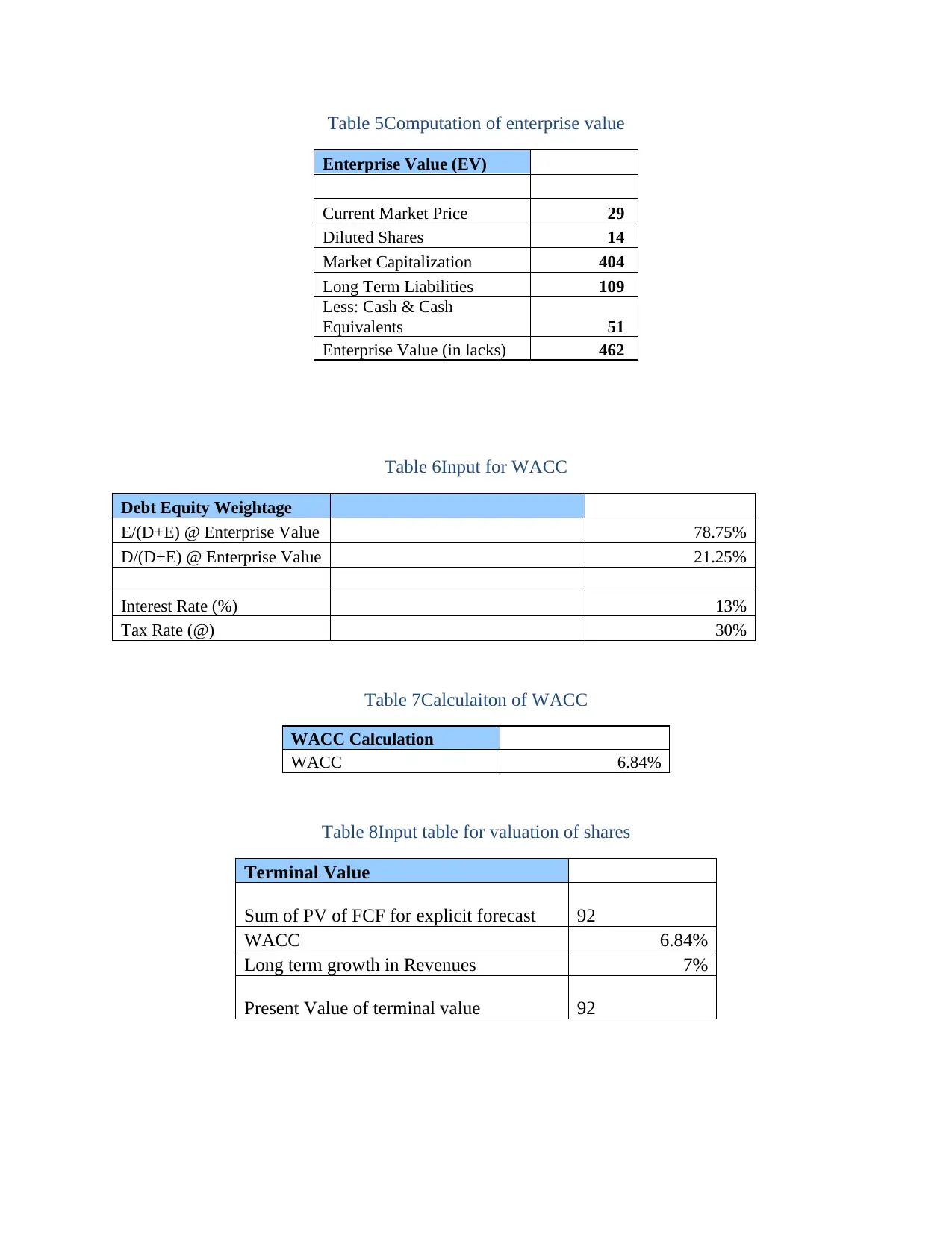

Table 5Computation of enterprise value

Enterprise Value (EV)

Current Market Price 29

Diluted Shares 14

Market Capitalization 404

Long Term Liabilities 109

Less: Cash & Cash

Equivalents 51

Enterprise Value (in lacks) 462

Table 6Input for WACC

Debt Equity Weightage

E/(D+E) @ Enterprise Value 78.75%

D/(D+E) @ Enterprise Value 21.25%

Interest Rate (%) 13%

Tax Rate (@) 30%

Table 7Calculaiton of WACC

WACC Calculation

WACC 6.84%

Table 8Input table for valuation of shares

Terminal Value

Sum of PV of FCF for explicit forecast 92

WACC 6.84%

Long term growth in Revenues 7%

Present Value of terminal value 92

Enterprise Value (EV)

Current Market Price 29

Diluted Shares 14

Market Capitalization 404

Long Term Liabilities 109

Less: Cash & Cash

Equivalents 51

Enterprise Value (in lacks) 462

Table 6Input for WACC

Debt Equity Weightage

E/(D+E) @ Enterprise Value 78.75%

D/(D+E) @ Enterprise Value 21.25%

Interest Rate (%) 13%

Tax Rate (@) 30%

Table 7Calculaiton of WACC

WACC Calculation

WACC 6.84%

Table 8Input table for valuation of shares

Terminal Value

Sum of PV of FCF for explicit forecast 92

WACC 6.84%

Long term growth in Revenues 7%

Present Value of terminal value 92

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

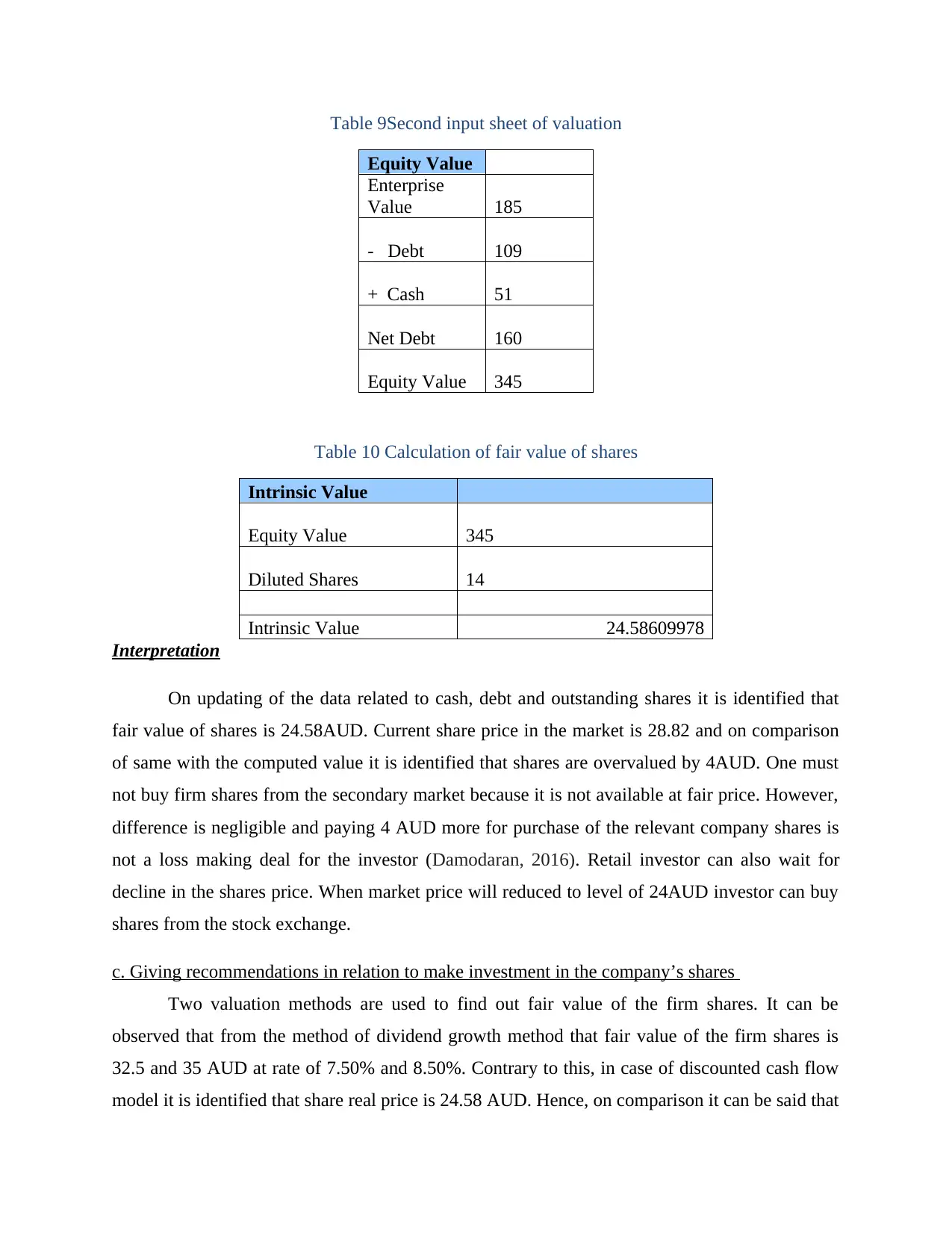

Table 9Second input sheet of valuation

Equity Value

Enterprise

Value 185

- Debt 109

+ Cash 51

Net Debt 160

Equity Value 345

Table 10 Calculation of fair value of shares

Intrinsic Value

Equity Value 345

Diluted Shares 14

Intrinsic Value 24.58609978

Interpretation

On updating of the data related to cash, debt and outstanding shares it is identified that

fair value of shares is 24.58AUD. Current share price in the market is 28.82 and on comparison

of same with the computed value it is identified that shares are overvalued by 4AUD. One must

not buy firm shares from the secondary market because it is not available at fair price. However,

difference is negligible and paying 4 AUD more for purchase of the relevant company shares is

not a loss making deal for the investor (Damodaran, 2016). Retail investor can also wait for

decline in the shares price. When market price will reduced to level of 24AUD investor can buy

shares from the stock exchange.

c. Giving recommendations in relation to make investment in the company’s shares

Two valuation methods are used to find out fair value of the firm shares. It can be

observed that from the method of dividend growth method that fair value of the firm shares is

32.5 and 35 AUD at rate of 7.50% and 8.50%. Contrary to this, in case of discounted cash flow

model it is identified that share real price is 24.58 AUD. Hence, on comparison it can be said that

Equity Value

Enterprise

Value 185

- Debt 109

+ Cash 51

Net Debt 160

Equity Value 345

Table 10 Calculation of fair value of shares

Intrinsic Value

Equity Value 345

Diluted Shares 14

Intrinsic Value 24.58609978

Interpretation

On updating of the data related to cash, debt and outstanding shares it is identified that

fair value of shares is 24.58AUD. Current share price in the market is 28.82 and on comparison

of same with the computed value it is identified that shares are overvalued by 4AUD. One must

not buy firm shares from the secondary market because it is not available at fair price. However,

difference is negligible and paying 4 AUD more for purchase of the relevant company shares is

not a loss making deal for the investor (Damodaran, 2016). Retail investor can also wait for

decline in the shares price. When market price will reduced to level of 24AUD investor can buy

shares from the stock exchange.

c. Giving recommendations in relation to make investment in the company’s shares

Two valuation methods are used to find out fair value of the firm shares. It can be

observed that from the method of dividend growth method that fair value of the firm shares is

32.5 and 35 AUD at rate of 7.50% and 8.50%. Contrary to this, in case of discounted cash flow

model it is identified that share real price is 24.58 AUD. Hence, on comparison it can be said that

there is not a big difference between the share prices that is computed by using both methods.

DCF method is assumed to be best method then dividend growth model. This is because in the

discounted cash flow model first of all cash flow is computed and present value of same is

computed (Shen, Firth and Poon, 2016). Thereafter, relevant cash flows are added and divided by

the issued shares. In this way intrinsic value of shares is computed. In this method overall

business performance and current capital structure is taken in to account. Thus, it can be said that

in the discounted cash flow model shares are valued in very systematic manner. On other hand,

in case of dividend discount model only cost of equity dividend growth rate are considered. Cash

flows are not taken in to account. Hence, DCF model is assumed better then growth model. On

30 June 2016 share price was 24.10 AUD which is almost equal to DCF model result 24.58AUD.

Hence, it is recommended that investment must be made in the firm shares.

QUESTION 3

Giving recommendations to JB Hi Fi Ltd regarding capital structure by using trade-off theory

Debt: AU$110 (in millions)

Shareholders’ equity: AU$405 (in millions)

Debt-equity ratio = Debt / equity

= 110 / 405

= .27

Hence, by considering the above ratio it has been analyzed that solvency position of Hi Fi

Ltd was not sound in the year of 2016. Moreover, in accounting period 2016, debt-equity ratio of

the firm was not sound because it is far from the ideal ratio. According to the ideal ratio

company needs to maintain the ratio of .5:1 for strengthening its liquidity position or

performance (Wilson, 2016). According to such aspect Hi Fi Ltd needs to make focus on issue 1

debt instrument in against to 2 equity shares. Trade off theory also helps in determining the fund

which business unit needs to enhance from debt and equity for making proper balance in the

financial structure. Hence, by considering such theoretical framework it can be said that in the

DCF method is assumed to be best method then dividend growth model. This is because in the

discounted cash flow model first of all cash flow is computed and present value of same is

computed (Shen, Firth and Poon, 2016). Thereafter, relevant cash flows are added and divided by

the issued shares. In this way intrinsic value of shares is computed. In this method overall

business performance and current capital structure is taken in to account. Thus, it can be said that

in the discounted cash flow model shares are valued in very systematic manner. On other hand,

in case of dividend discount model only cost of equity dividend growth rate are considered. Cash

flows are not taken in to account. Hence, DCF model is assumed better then growth model. On

30 June 2016 share price was 24.10 AUD which is almost equal to DCF model result 24.58AUD.

Hence, it is recommended that investment must be made in the firm shares.

QUESTION 3

Giving recommendations to JB Hi Fi Ltd regarding capital structure by using trade-off theory

Debt: AU$110 (in millions)

Shareholders’ equity: AU$405 (in millions)

Debt-equity ratio = Debt / equity

= 110 / 405

= .27

Hence, by considering the above ratio it has been analyzed that solvency position of Hi Fi

Ltd was not sound in the year of 2016. Moreover, in accounting period 2016, debt-equity ratio of

the firm was not sound because it is far from the ideal ratio. According to the ideal ratio

company needs to maintain the ratio of .5:1 for strengthening its liquidity position or

performance (Wilson, 2016). According to such aspect Hi Fi Ltd needs to make focus on issue 1

debt instrument in against to 2 equity shares. Trade off theory also helps in determining the fund

which business unit needs to enhance from debt and equity for making proper balance in the

financial structure. Hence, by considering such theoretical framework it can be said that in the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

near future business unit needs to place emphasis on raising fund through the means of debt

instrument rather than equity shares.

By keeping all such aspects in mind it can be said company can make improvement in its

solvency aspect. Moreover, when business unit generates more funds from debt instruments then

it is obliged to make interest payment. This in turn imposes high financial burden in front of firm

and affects the profitability aspect in a negative manner (Jacob, Johan Schweizer and Zhan,

2016). Further, in the case of shares company offers dividend to the shareholders only when it

earns enough amount of profit margin. In this way, shares do not impose high financial burden in

front of firm. Hence, in accordance with trade off theory company needs to issue debt instrument

of AU$100 for enhancing fund. In this way, by raising fund through the means of debt Hi Fi Ltd

can make significant improvement in its liquidity position or aspects.

instrument rather than equity shares.

By keeping all such aspects in mind it can be said company can make improvement in its

solvency aspect. Moreover, when business unit generates more funds from debt instruments then

it is obliged to make interest payment. This in turn imposes high financial burden in front of firm

and affects the profitability aspect in a negative manner (Jacob, Johan Schweizer and Zhan,

2016). Further, in the case of shares company offers dividend to the shareholders only when it

earns enough amount of profit margin. In this way, shares do not impose high financial burden in

front of firm. Hence, in accordance with trade off theory company needs to issue debt instrument

of AU$100 for enhancing fund. In this way, by raising fund through the means of debt Hi Fi Ltd

can make significant improvement in its liquidity position or aspects.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Damodaran, A., 2016. Damodaran on valuation: security analysis for investment and corporate

finance (Vol. 324). John Wiley & Sons.

Jacob, M. and et.al., 2016. Corporate finance and the governance implications of removing

government support programs.Journal of Banking & Finance, 63, pp.35-47.

Shen, J., Firth, M. and Poon, W.P., 2016. Credit Expansion, Corporate Finance and

Overinvestment:

Wilson, N., 2016. ESOPs: their role in corporate finance and performance. Springer.

Books and Journals

Damodaran, A., 2016. Damodaran on valuation: security analysis for investment and corporate

finance (Vol. 324). John Wiley & Sons.

Jacob, M. and et.al., 2016. Corporate finance and the governance implications of removing

government support programs.Journal of Banking & Finance, 63, pp.35-47.

Shen, J., Firth, M. and Poon, W.P., 2016. Credit Expansion, Corporate Finance and

Overinvestment:

Wilson, N., 2016. ESOPs: their role in corporate finance and performance. Springer.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.