Capital Budgeting Analysis: Booli Electronics Investment Project

VerifiedAdded on 2023/06/12

|12

|2307

|436

Report

AI Summary

This report provides a comprehensive analysis of Booli Electronics' potential investment in a new 'smart speaker and home assistant (SSHA)' product, utilizing capital budgeting techniques to determine project viability. It calculates and interprets the non-discounted payback period, profitability index, internal rate of return (IRR), and net present value (NPV) to assess whether the company should proceed with the investment. The report also examines the sensitivity of NPV to price changes and discusses the implications for project management. Ultimately, based on the positive financial indicators, the report recommends that Booli Electronics pursue the SSHA product expansion, with considerations for managing potential impacts on existing product sales. Desklib provides similar solved assignments for students.

qwertyuiopasdfghjklzxcvbnmqw

ertyuiopasdfghjklzxcvbnmqwert

yuiopasdfghjklzxcvbnmqwertyui

opasdfghjklzxcvbnmqwertyuiop

asdfghjklzxcvbnmqwertyuiopasd

fghjklzxcvbnmqwertyuiopasdfgh

jklzxcvbnmqwertyuiopasdfghjkl

zxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvb

nmqwertyuiopasdfghjklzxcvbnm

qwertyuiopasdfghjklzxcvbnmqw

ertyuiopasdfghjklzxcvbnmqwert

yuiopasdfghjklzxcvbnmqwertyui

opasdfghjklzxcvbnmqwertyuiop

asdfghjklzxcvbnmqwertyuiopasd

fghjklzxcvbnmqwertyuiopasdfgh

jklzxcvbnmrtyuiopasdfghjklzxcv

Business Finance

Report

5/24/2018

Student Name

ertyuiopasdfghjklzxcvbnmqwert

yuiopasdfghjklzxcvbnmqwertyui

opasdfghjklzxcvbnmqwertyuiop

asdfghjklzxcvbnmqwertyuiopasd

fghjklzxcvbnmqwertyuiopasdfgh

jklzxcvbnmqwertyuiopasdfghjkl

zxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvb

nmqwertyuiopasdfghjklzxcvbnm

qwertyuiopasdfghjklzxcvbnmqw

ertyuiopasdfghjklzxcvbnmqwert

yuiopasdfghjklzxcvbnmqwertyui

opasdfghjklzxcvbnmqwertyuiop

asdfghjklzxcvbnmqwertyuiopasd

fghjklzxcvbnmqwertyuiopasdfgh

jklzxcvbnmrtyuiopasdfghjklzxcv

Business Finance

Report

5/24/2018

Student Name

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1 | P a g e Business Finance

Contents

Introduction...........................................................................................................................................2

Questions...............................................................................................................................................2

Q1......................................................................................................................................................2

Q2......................................................................................................................................................2

Q3......................................................................................................................................................3

Q4......................................................................................................................................................3

Q5......................................................................................................................................................4

Q6......................................................................................................................................................5

Q7......................................................................................................................................................5

Q8......................................................................................................................................................6

Conclusion.............................................................................................................................................6

References.............................................................................................................................................7

Appendices............................................................................................................................................9

Appendix 1.........................................................................................................................................9

Appendix 2.........................................................................................................................................9

Appendix 3.........................................................................................................................................9

Appendix 4.......................................................................................................................................10

Contents

Introduction...........................................................................................................................................2

Questions...............................................................................................................................................2

Q1......................................................................................................................................................2

Q2......................................................................................................................................................2

Q3......................................................................................................................................................3

Q4......................................................................................................................................................3

Q5......................................................................................................................................................4

Q6......................................................................................................................................................5

Q7......................................................................................................................................................5

Q8......................................................................................................................................................6

Conclusion.............................................................................................................................................6

References.............................................................................................................................................7

Appendices............................................................................................................................................9

Appendix 1.........................................................................................................................................9

Appendix 2.........................................................................................................................................9

Appendix 3.........................................................................................................................................9

Appendix 4.......................................................................................................................................10

2 | P a g e Business Finance

Introduction

The report highlights the fact related to the Booli Electronics. The business is going to

diversify its activities to have a large market share by using some innovation in its strategy.

The report discusses the fact and figures whether the business should expand or not. The

report focuses on the various techniques of capital budgeting to know whether the proposal is

accepted or not. The business decisions based on the capital budgeting techniques are used in

the report. The project acceptance and rejection are based on the cost and profitability of the

project (Sayadi, Tavassoli, Monjezi and Rezaei, 2014). The Booli electronics have to decide

whether to go for the new introduction of product or not. The Booli Company profitability,

payback period, internal rate of return is discussed in the report.

Questions

Q1

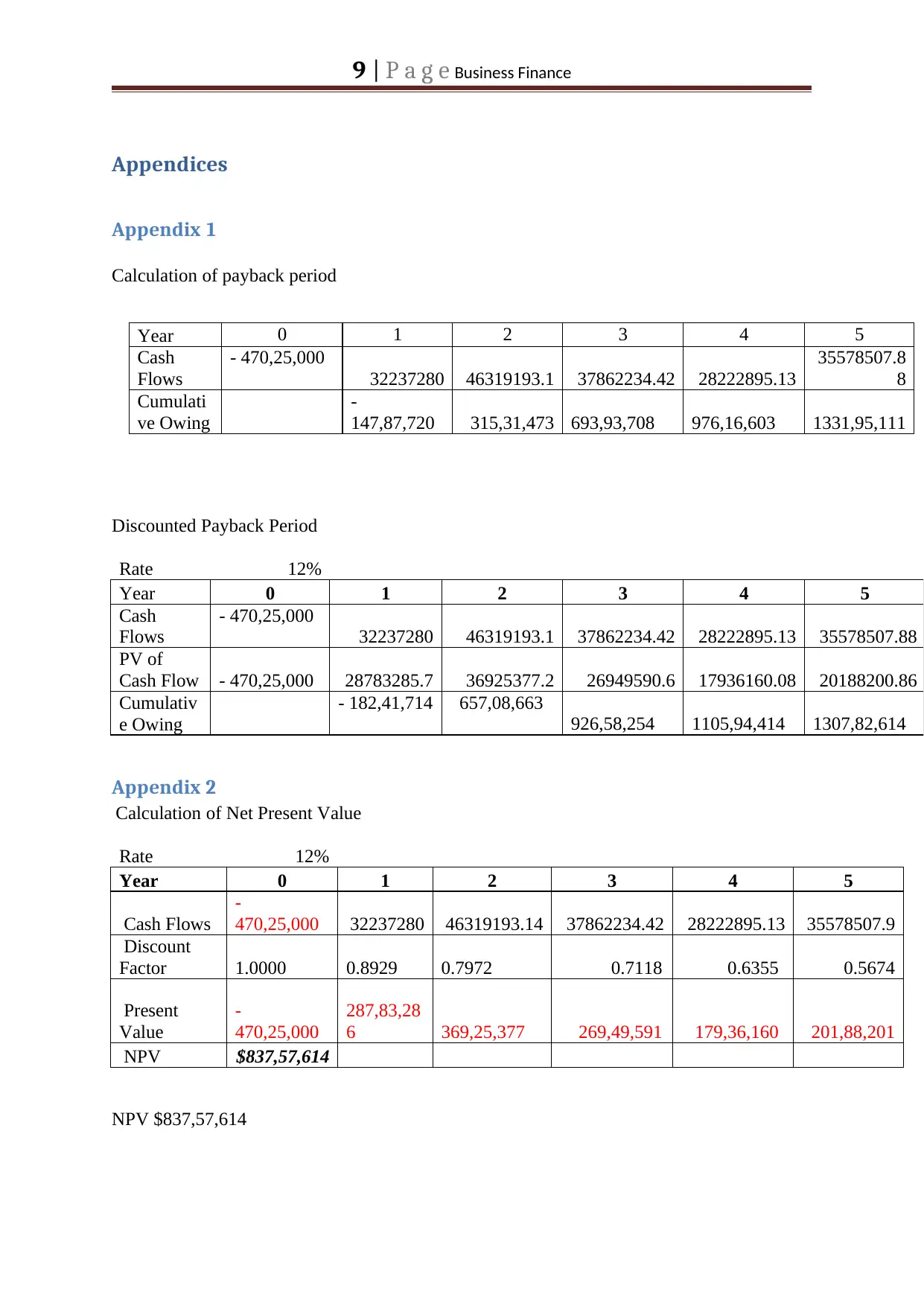

Non-discounted payback period

The non-discounted payback period can be defined as the period in which the time value of

money has been ignored. This technique assumes that there will be no revenues after the

project is completed (Peng and Yang, 2013). In the case of Booli electronic, the payback

period comes out to be 1.7 years (Refer Appendix 1). This indicates that the company can

recover its capital in years and 7 months only.

Q2.

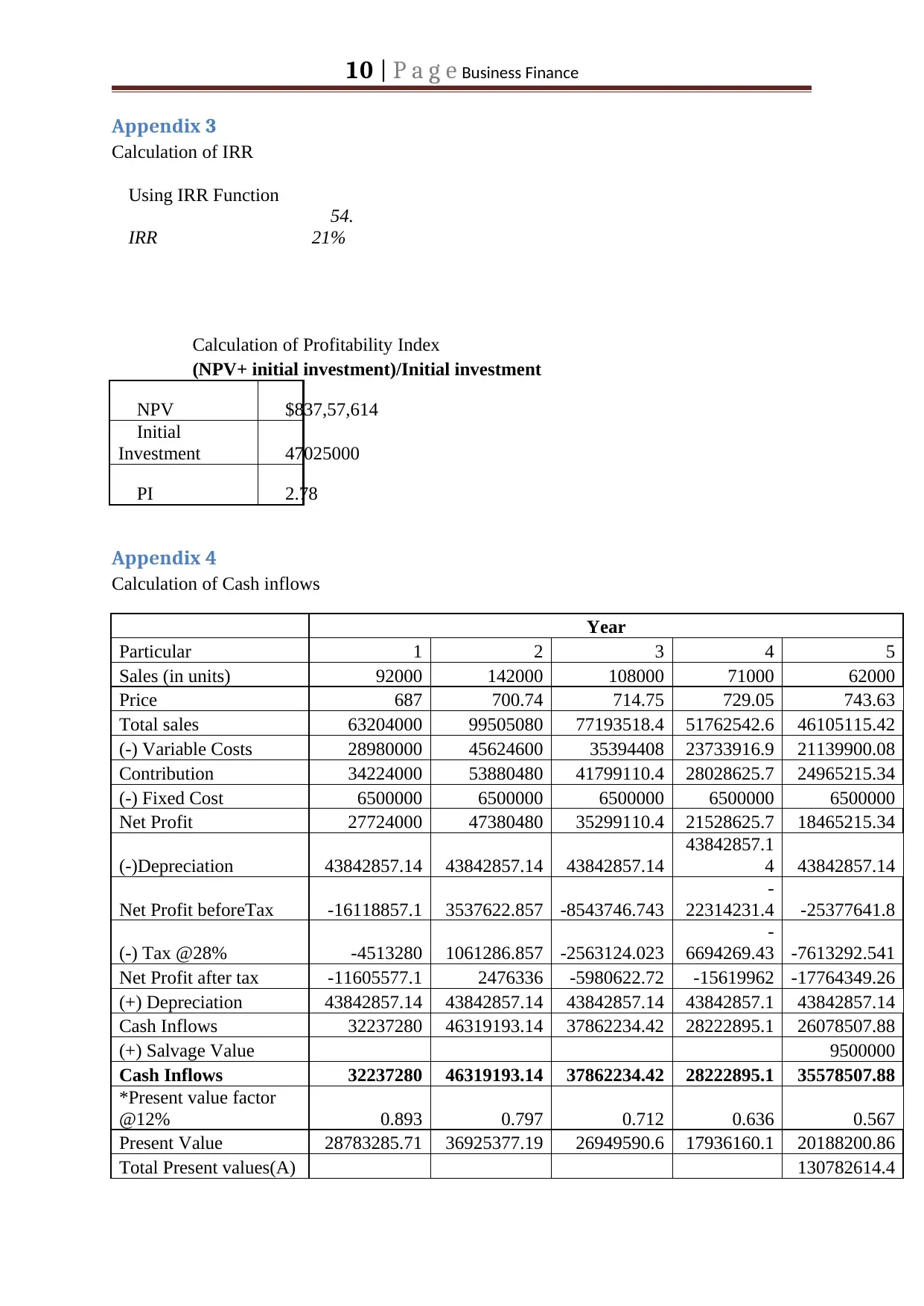

Profitability Index

Profitability index can be defined as the index which shows the profit earning capacity of the

business. If the profitability index is more than 1 then the project will be accepted and if it

Introduction

The report highlights the fact related to the Booli Electronics. The business is going to

diversify its activities to have a large market share by using some innovation in its strategy.

The report discusses the fact and figures whether the business should expand or not. The

report focuses on the various techniques of capital budgeting to know whether the proposal is

accepted or not. The business decisions based on the capital budgeting techniques are used in

the report. The project acceptance and rejection are based on the cost and profitability of the

project (Sayadi, Tavassoli, Monjezi and Rezaei, 2014). The Booli electronics have to decide

whether to go for the new introduction of product or not. The Booli Company profitability,

payback period, internal rate of return is discussed in the report.

Questions

Q1

Non-discounted payback period

The non-discounted payback period can be defined as the period in which the time value of

money has been ignored. This technique assumes that there will be no revenues after the

project is completed (Peng and Yang, 2013). In the case of Booli electronic, the payback

period comes out to be 1.7 years (Refer Appendix 1). This indicates that the company can

recover its capital in years and 7 months only.

Q2.

Profitability Index

Profitability index can be defined as the index which shows the profit earning capacity of the

business. If the profitability index is more than 1 then the project will be accepted and if it

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3 | P a g e Business Finance

comes out to be less than 1 then the proposal is rejected (Brunzell, Liljeblom and Vaihekoski,

2013).

Profitability Index = Present value of Future cash flow

Initial Investment

OR

= (NPV+ initial investment)/Initial investment

Net present value is directly related to the maximizing the wealth and earnings of the

business (Faccio, Marchica and Mura, 2016). The profitability index comes out to be

2.78(Refer Appendix 2) which is greater than 1. The project should be accepted as it is

greater than 1.

Q3.

IRR of the project

Internal Rate of return is the rate at which the business calculates its returns. This rate will not

be influenced by the external factors. The acceptance criterion for IRR is that if the internal

rate of return is come out to be more than the cost of capital then the proposal will be

accepted otherwise rejected (Rossi, 2014). In Booli Company, the IRR comes out to be ----

which is more than the cost of capital. The Internal rate of return comes out to be 54.21%

(Refer Appendix 3) which is much more than the cost of capital of the company. According

to the criterion, the project should be accepted by the Booli Electronics.

Q4.

NPV of the project

comes out to be less than 1 then the proposal is rejected (Brunzell, Liljeblom and Vaihekoski,

2013).

Profitability Index = Present value of Future cash flow

Initial Investment

OR

= (NPV+ initial investment)/Initial investment

Net present value is directly related to the maximizing the wealth and earnings of the

business (Faccio, Marchica and Mura, 2016). The profitability index comes out to be

2.78(Refer Appendix 2) which is greater than 1. The project should be accepted as it is

greater than 1.

Q3.

IRR of the project

Internal Rate of return is the rate at which the business calculates its returns. This rate will not

be influenced by the external factors. The acceptance criterion for IRR is that if the internal

rate of return is come out to be more than the cost of capital then the proposal will be

accepted otherwise rejected (Rossi, 2014). In Booli Company, the IRR comes out to be ----

which is more than the cost of capital. The Internal rate of return comes out to be 54.21%

(Refer Appendix 3) which is much more than the cost of capital of the company. According

to the criterion, the project should be accepted by the Booli Electronics.

Q4.

NPV of the project

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4 | P a g e Business Finance

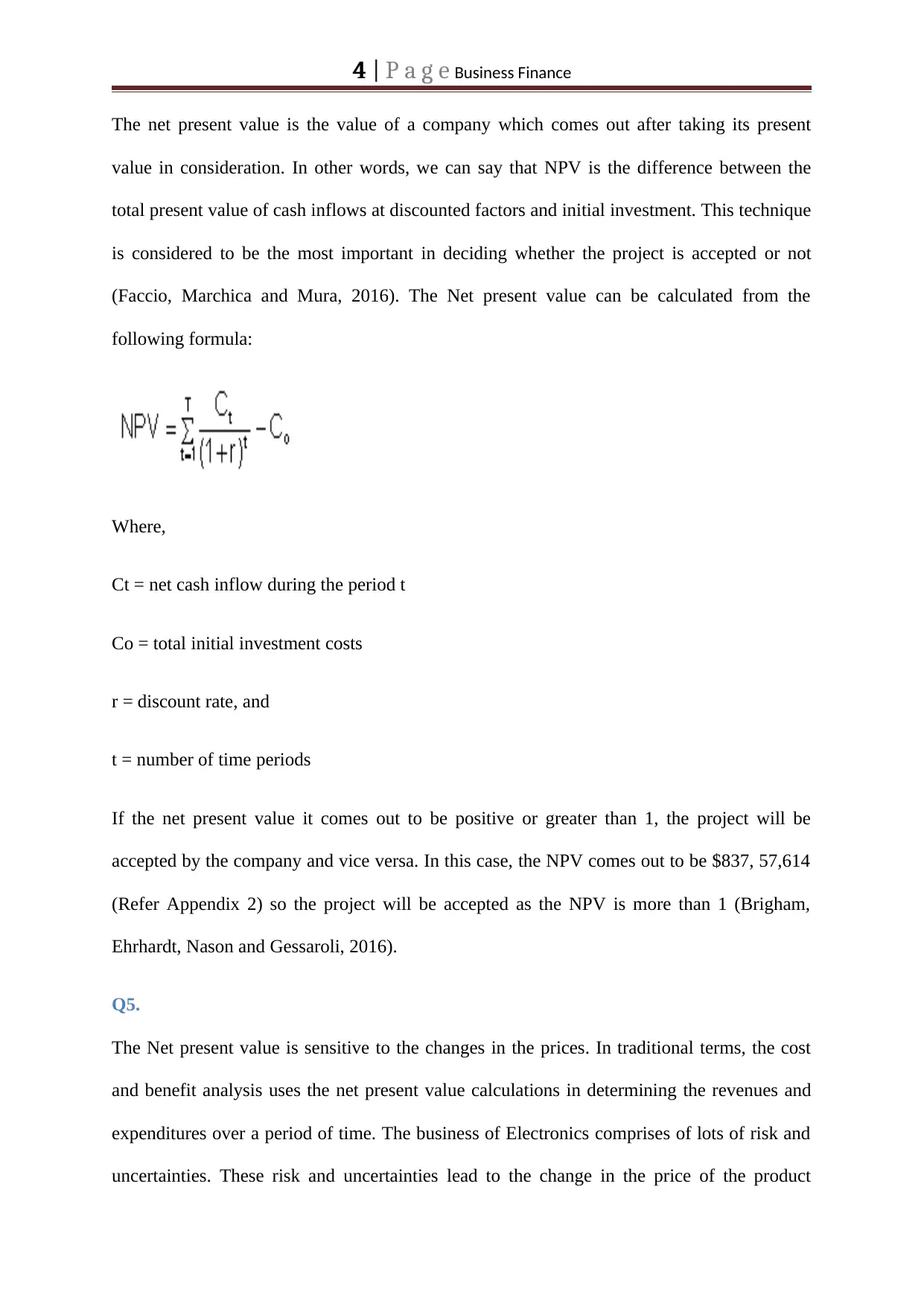

The net present value is the value of a company which comes out after taking its present

value in consideration. In other words, we can say that NPV is the difference between the

total present value of cash inflows at discounted factors and initial investment. This technique

is considered to be the most important in deciding whether the project is accepted or not

(Faccio, Marchica and Mura, 2016). The Net present value can be calculated from the

following formula:

Where,

Ct = net cash inflow during the period t

Co = total initial investment costs

r = discount rate, and

t = number of time periods

If the net present value it comes out to be positive or greater than 1, the project will be

accepted by the company and vice versa. In this case, the NPV comes out to be $837, 57,614

(Refer Appendix 2) so the project will be accepted as the NPV is more than 1 (Brigham,

Ehrhardt, Nason and Gessaroli, 2016).

Q5.

The Net present value is sensitive to the changes in the prices. In traditional terms, the cost

and benefit analysis uses the net present value calculations in determining the revenues and

expenditures over a period of time. The business of Electronics comprises of lots of risk and

uncertainties. These risk and uncertainties lead to the change in the price of the product

The net present value is the value of a company which comes out after taking its present

value in consideration. In other words, we can say that NPV is the difference between the

total present value of cash inflows at discounted factors and initial investment. This technique

is considered to be the most important in deciding whether the project is accepted or not

(Faccio, Marchica and Mura, 2016). The Net present value can be calculated from the

following formula:

Where,

Ct = net cash inflow during the period t

Co = total initial investment costs

r = discount rate, and

t = number of time periods

If the net present value it comes out to be positive or greater than 1, the project will be

accepted by the company and vice versa. In this case, the NPV comes out to be $837, 57,614

(Refer Appendix 2) so the project will be accepted as the NPV is more than 1 (Brigham,

Ehrhardt, Nason and Gessaroli, 2016).

Q5.

The Net present value is sensitive to the changes in the prices. In traditional terms, the cost

and benefit analysis uses the net present value calculations in determining the revenues and

expenditures over a period of time. The business of Electronics comprises of lots of risk and

uncertainties. These risk and uncertainties lead to the change in the price of the product

5 | P a g e Business Finance

(Bierman and Smidt, 2014). The market is dynamic in nature and gives the opportunity to the

businessman to have the advantage and opportunity from the market. So the changes in the

price of the project affect the cash flows and earnings of the project. Change in price leads to

knowing the present value of the company at which the company is offering the product to its

customers.

Q6.

The change in the net present value also changes the quantity demanded in the market. From

the data, we can analyse that in initial years the quantity sold by the company is high when

compared to the fifth year. If the cash flows of the company are high that means the company

is selling more units and earning high revenue also. Change in the cash flow leads to the

change in the NPV of the project as there is the direct relationship between the cash inflows

and NPV of the project. If the cash inflows are increasing then the NPV will also increase and

vice versa (Graham, Harvey and Puri, 2015).

Q7.

Yes, the Booli electronics Company should go for the SSHA product. This product will give

the benefit to the company in revenue terms. From the data given, it can be analysed that the

sales are increasing in the initial years but after sometimes the sale of the company goes on

decreasing. This is the reason that the company should go for the implementation of the new

product in the market so to have a share in the market (Baker, Jabbouri, and Dyaz, 2017).

This new product has new and exciting features which will influence the customers and

company can able to gain more revenues. The product SSHA includes the features like Wi-Fi

tethering and access to a large number of music streaming services including Amazon,

Spotify etc. The proposal should be accepted as the project found to be good and high.

(Bierman and Smidt, 2014). The market is dynamic in nature and gives the opportunity to the

businessman to have the advantage and opportunity from the market. So the changes in the

price of the project affect the cash flows and earnings of the project. Change in price leads to

knowing the present value of the company at which the company is offering the product to its

customers.

Q6.

The change in the net present value also changes the quantity demanded in the market. From

the data, we can analyse that in initial years the quantity sold by the company is high when

compared to the fifth year. If the cash flows of the company are high that means the company

is selling more units and earning high revenue also. Change in the cash flow leads to the

change in the NPV of the project as there is the direct relationship between the cash inflows

and NPV of the project. If the cash inflows are increasing then the NPV will also increase and

vice versa (Graham, Harvey and Puri, 2015).

Q7.

Yes, the Booli electronics Company should go for the SSHA product. This product will give

the benefit to the company in revenue terms. From the data given, it can be analysed that the

sales are increasing in the initial years but after sometimes the sale of the company goes on

decreasing. This is the reason that the company should go for the implementation of the new

product in the market so to have a share in the market (Baker, Jabbouri, and Dyaz, 2017).

This new product has new and exciting features which will influence the customers and

company can able to gain more revenues. The product SSHA includes the features like Wi-Fi

tethering and access to a large number of music streaming services including Amazon,

Spotify etc. The proposal should be accepted as the project found to be good and high.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6 | P a g e Business Finance

Q8.

If the overall sales of the Booli Electronics have been decreased because of the introduction

of SSHA in the product line then the project should be offered in the market in such a way

that the other product sale will not be affected. The company should try for the method which

will enhance the sale of SSHA while maintaining the sale of an existing product. The

analysis would affect a lot as there will be fewer cash flows earned by the company which

will affect the profitability and cash flows of the business. This decrease in the sale of the

company also affects the cash inflows of the company which ultimately affect the price and

quantity of the product (Walden and Kitts, 2014).

Conclusion

From the above discussion, we can conclude that the Booli electronics should go for Opting

the expansion in the product range by introducing the SSHA. According to the analysis, it is

visible that the company is earning is well at present and can increase it's earning from the

new product expansion the cash flows calculated are come out to be positive and showing the

increasing trends. The profitability index is come out to be more than which indicates that the

project should be accepted by the company. The company can also able to recover its cost in

fewer years. The internal rate of return of the company is also coming out to be more than the

cost of capital. The price and quantity are also favouring the company strategy in the market.

From all the calculations and discussion, it can be stated that the proposal of the new project

should be accepted.

Q8.

If the overall sales of the Booli Electronics have been decreased because of the introduction

of SSHA in the product line then the project should be offered in the market in such a way

that the other product sale will not be affected. The company should try for the method which

will enhance the sale of SSHA while maintaining the sale of an existing product. The

analysis would affect a lot as there will be fewer cash flows earned by the company which

will affect the profitability and cash flows of the business. This decrease in the sale of the

company also affects the cash inflows of the company which ultimately affect the price and

quantity of the product (Walden and Kitts, 2014).

Conclusion

From the above discussion, we can conclude that the Booli electronics should go for Opting

the expansion in the product range by introducing the SSHA. According to the analysis, it is

visible that the company is earning is well at present and can increase it's earning from the

new product expansion the cash flows calculated are come out to be positive and showing the

increasing trends. The profitability index is come out to be more than which indicates that the

project should be accepted by the company. The company can also able to recover its cost in

fewer years. The internal rate of return of the company is also coming out to be more than the

cost of capital. The price and quantity are also favouring the company strategy in the market.

From all the calculations and discussion, it can be stated that the proposal of the new project

should be accepted.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7 | P a g e Business Finance

References

Baker, H.K., Jabbouri, I. and Dyaz, C. (2017). Corporate finance practices in

Morocco. Managerial Finance, 43(8), pp.865-880.

Bierman Jr, H. and Smidt, S. (2014). Advanced capital budgeting: Refinements in the

economic analysis of investment projects. Oxon: Routledge.

Brigham, E.F., Ehrhardt, M.C., Nason, R.R. and Gessaroli, J. (2016) Financial Managment:

Theory And Practice, Canadian Edition. Ontario: Nelson Education.

Brunzell, T., Liljeblom, E. and Vaihekoski, M. (2013) Determinants of capital budgeting

methods and hurdle rates in Nordic firms. Accounting and Finance, 53(1), pp.85-110.

Faccio, M., Marchica, M.T. and Mura, R. (2016) CEO gender, corporate risk-taking, and the

efficiency of capital allocation. Journal of Corporate Finance, 39, pp.193-209.

Graham, J.R., Harvey, C.R. and Puri, M. (2015) Capital allocation and delegation of

decision-making authority within firms. Journal of Financial Economics, 115(3), pp.449-470.

Peng, J., Lu, L. and Yang, H. (2013) Review on life cycle assessment of energy payback and

greenhouse gas emission of solar photovoltaic systems. Renewable and Sustainable Energy

Reviews, 19, pp.255-274.

Rossi, M. (2014) Capital budgeting in Europe: confronting theory with practice. International

Journal of Managerial and Financial Accounting, 6(4), pp.341-356.

References

Baker, H.K., Jabbouri, I. and Dyaz, C. (2017). Corporate finance practices in

Morocco. Managerial Finance, 43(8), pp.865-880.

Bierman Jr, H. and Smidt, S. (2014). Advanced capital budgeting: Refinements in the

economic analysis of investment projects. Oxon: Routledge.

Brigham, E.F., Ehrhardt, M.C., Nason, R.R. and Gessaroli, J. (2016) Financial Managment:

Theory And Practice, Canadian Edition. Ontario: Nelson Education.

Brunzell, T., Liljeblom, E. and Vaihekoski, M. (2013) Determinants of capital budgeting

methods and hurdle rates in Nordic firms. Accounting and Finance, 53(1), pp.85-110.

Faccio, M., Marchica, M.T. and Mura, R. (2016) CEO gender, corporate risk-taking, and the

efficiency of capital allocation. Journal of Corporate Finance, 39, pp.193-209.

Graham, J.R., Harvey, C.R. and Puri, M. (2015) Capital allocation and delegation of

decision-making authority within firms. Journal of Financial Economics, 115(3), pp.449-470.

Peng, J., Lu, L. and Yang, H. (2013) Review on life cycle assessment of energy payback and

greenhouse gas emission of solar photovoltaic systems. Renewable and Sustainable Energy

Reviews, 19, pp.255-274.

Rossi, M. (2014) Capital budgeting in Europe: confronting theory with practice. International

Journal of Managerial and Financial Accounting, 6(4), pp.341-356.

8 | P a g e Business Finance

Sayadi, A.R., Tavassoli, S.M.M., Monjezi, M. and Rezaei, M. (2014) Application of neural

networks to predict net present value in mining projects. Arabian Journal of

Geosciences, 7(3), pp.1067-1072.

Walden, J.B. and Kitts, N. (2014) Measuring fishery profitability: An index number

approach. Marine Policy, 43, pp.321-326.

Sayadi, A.R., Tavassoli, S.M.M., Monjezi, M. and Rezaei, M. (2014) Application of neural

networks to predict net present value in mining projects. Arabian Journal of

Geosciences, 7(3), pp.1067-1072.

Walden, J.B. and Kitts, N. (2014) Measuring fishery profitability: An index number

approach. Marine Policy, 43, pp.321-326.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9 | P a g e Business Finance

Appendices

Appendix 1

Calculation of payback period

Year 0 1 2 3 4 5

Cash

Flows

- 470,25,000

32237280 46319193.1 37862234.42 28222895.13

35578507.8

8

Cumulati

ve Owing

-

147,87,720 315,31,473 693,93,708 976,16,603 1331,95,111

Discounted Payback Period

Rate 12%

Year 0 1 2 3 4 5

Cash

Flows

- 470,25,000

32237280 46319193.1 37862234.42 28222895.13 35578507.88

PV of

Cash Flow - 470,25,000 28783285.7 36925377.2 26949590.6 17936160.08 20188200.86

Cumulativ

e Owing

- 182,41,714 657,08,663

926,58,254 1105,94,414 1307,82,614

Appendix 2

Calculation of Net Present Value

Rate 12%

Year 0 1 2 3 4 5

Cash Flows

-

470,25,000 32237280 46319193.14 37862234.42 28222895.13 35578507.9

Discount

Factor 1.0000 0.8929 0.7972 0.7118 0.6355 0.5674

Present

Value

-

470,25,000

287,83,28

6 369,25,377 269,49,591 179,36,160 201,88,201

NPV $837,57,614

NPV $837,57,614

Appendices

Appendix 1

Calculation of payback period

Year 0 1 2 3 4 5

Cash

Flows

- 470,25,000

32237280 46319193.1 37862234.42 28222895.13

35578507.8

8

Cumulati

ve Owing

-

147,87,720 315,31,473 693,93,708 976,16,603 1331,95,111

Discounted Payback Period

Rate 12%

Year 0 1 2 3 4 5

Cash

Flows

- 470,25,000

32237280 46319193.1 37862234.42 28222895.13 35578507.88

PV of

Cash Flow - 470,25,000 28783285.7 36925377.2 26949590.6 17936160.08 20188200.86

Cumulativ

e Owing

- 182,41,714 657,08,663

926,58,254 1105,94,414 1307,82,614

Appendix 2

Calculation of Net Present Value

Rate 12%

Year 0 1 2 3 4 5

Cash Flows

-

470,25,000 32237280 46319193.14 37862234.42 28222895.13 35578507.9

Discount

Factor 1.0000 0.8929 0.7972 0.7118 0.6355 0.5674

Present

Value

-

470,25,000

287,83,28

6 369,25,377 269,49,591 179,36,160 201,88,201

NPV $837,57,614

NPV $837,57,614

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10 | P a g e Business Finance

Appendix 3

Calculation of IRR

Using IRR Function

IRR

54.

21%

Calculation of Profitability Index

(NPV+ initial investment)/Initial investment

NPV $837,57,614

Initial

Investment 47025000

PI 2.78

Appendix 4

Calculation of Cash inflows

Year

Particular 1 2 3 4 5

Sales (in units) 92000 142000 108000 71000 62000

Price 687 700.74 714.75 729.05 743.63

Total sales 63204000 99505080 77193518.4 51762542.6 46105115.42

(-) Variable Costs 28980000 45624600 35394408 23733916.9 21139900.08

Contribution 34224000 53880480 41799110.4 28028625.7 24965215.34

(-) Fixed Cost 6500000 6500000 6500000 6500000 6500000

Net Profit 27724000 47380480 35299110.4 21528625.7 18465215.34

(-)Depreciation 43842857.14 43842857.14 43842857.14

43842857.1

4 43842857.14

Net Profit beforeTax -16118857.1 3537622.857 -8543746.743

-

22314231.4 -25377641.8

(-) Tax @28% -4513280 1061286.857 -2563124.023

-

6694269.43 -7613292.541

Net Profit after tax -11605577.1 2476336 -5980622.72 -15619962 -17764349.26

(+) Depreciation 43842857.14 43842857.14 43842857.14 43842857.1 43842857.14

Cash Inflows 32237280 46319193.14 37862234.42 28222895.1 26078507.88

(+) Salvage Value 9500000

Cash Inflows 32237280 46319193.14 37862234.42 28222895.1 35578507.88

*Present value factor

@12% 0.893 0.797 0.712 0.636 0.567

Present Value 28783285.71 36925377.19 26949590.6 17936160.1 20188200.86

Total Present values(A) 130782614.4

Appendix 3

Calculation of IRR

Using IRR Function

IRR

54.

21%

Calculation of Profitability Index

(NPV+ initial investment)/Initial investment

NPV $837,57,614

Initial

Investment 47025000

PI 2.78

Appendix 4

Calculation of Cash inflows

Year

Particular 1 2 3 4 5

Sales (in units) 92000 142000 108000 71000 62000

Price 687 700.74 714.75 729.05 743.63

Total sales 63204000 99505080 77193518.4 51762542.6 46105115.42

(-) Variable Costs 28980000 45624600 35394408 23733916.9 21139900.08

Contribution 34224000 53880480 41799110.4 28028625.7 24965215.34

(-) Fixed Cost 6500000 6500000 6500000 6500000 6500000

Net Profit 27724000 47380480 35299110.4 21528625.7 18465215.34

(-)Depreciation 43842857.14 43842857.14 43842857.14

43842857.1

4 43842857.14

Net Profit beforeTax -16118857.1 3537622.857 -8543746.743

-

22314231.4 -25377641.8

(-) Tax @28% -4513280 1061286.857 -2563124.023

-

6694269.43 -7613292.541

Net Profit after tax -11605577.1 2476336 -5980622.72 -15619962 -17764349.26

(+) Depreciation 43842857.14 43842857.14 43842857.14 43842857.1 43842857.14

Cash Inflows 32237280 46319193.14 37862234.42 28222895.1 26078507.88

(+) Salvage Value 9500000

Cash Inflows 32237280 46319193.14 37862234.42 28222895.1 35578507.88

*Present value factor

@12% 0.893 0.797 0.712 0.636 0.567

Present Value 28783285.71 36925377.19 26949590.6 17936160.1 20188200.86

Total Present values(A) 130782614.4

11 | P a g e Business Finance

(-)Cash Outflows

Additional expenses 1175000

(+)Marketing expenses 650000

(+)Cost Of equipment 45200000

Total(B) 47025000

Net Present Value(A-B) 83757614.44

Working Notes

Variable cost Units $

315 92000 28980000

321.30 142000 45624600

327.73 108000 35394408

334.28 71000

23733916.9

2

340.97 62000

21139900.0

8

(-)Cash Outflows

Additional expenses 1175000

(+)Marketing expenses 650000

(+)Cost Of equipment 45200000

Total(B) 47025000

Net Present Value(A-B) 83757614.44

Working Notes

Variable cost Units $

315 92000 28980000

321.30 142000 45624600

327.73 108000 35394408

334.28 71000

23733916.9

2

340.97 62000

21139900.0

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12