UGB 223 Business Finance: Financial Statement Analysis & Decisions

VerifiedAdded on 2023/06/10

|10

|2636

|443

Homework Assignment

AI Summary

This assignment provides a comprehensive analysis of various financial concepts and their application to business decision-making. It includes calculations and explanations related to the cash conversion cycle, evaluating the benefits and costs of factoring, and assessing the implications of a rights issue. The document also delves into dividend policy, examining factors influencing dividend decisions and evaluating different dividend payout alternatives. Furthermore, it discusses the limitations of the dividend growth model in stock valuation. The solutions presented offer insights into financial statement analysis, investment appraisal, and the impact of financial decisions on shareholder wealth. Desklib offers a platform to explore this and similar assignments, providing students with valuable resources for their studies.

Business finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

QUESTION 1..................................................................................................................................1

Calculate the following:...............................................................................................................1

a) Calculating the Cash Conversion Cycle and write down its significance...............................1

b. State whether to accept the factoring decision and also state whether the amount saved can

be utilised.....................................................................................................................................2

QUESTION 3..................................................................................................................................3

(a) The theoretical ex-rights price per share................................................................................3

(b) The net cash raised.................................................................................................................3

(c) The value of the rights............................................................................................................3

d) The benefits and drawbacks of the right issue........................................................................4

QUESTION 5..................................................................................................................................4

a)..................................................................................................................................................4

b)..................................................................................................................................................5

c) Evaluate the disadvantages of utilising the dividend growth model to value stocks..............5

QUESTION 6..................................................................................................................................6

The size of the annual dividend to return to its shareholders for the factors which needs to be

considered....................................................................................................................................6

The realistic considerations which must be made while determining the amount of the

dividend payout...........................................................................................................................6

b) Make a calculation for each of the 3 alternatives....................................................................6

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

QUESTION 1..................................................................................................................................1

Calculate the following:...............................................................................................................1

a) Calculating the Cash Conversion Cycle and write down its significance...............................1

b. State whether to accept the factoring decision and also state whether the amount saved can

be utilised.....................................................................................................................................2

QUESTION 3..................................................................................................................................3

(a) The theoretical ex-rights price per share................................................................................3

(b) The net cash raised.................................................................................................................3

(c) The value of the rights............................................................................................................3

d) The benefits and drawbacks of the right issue........................................................................4

QUESTION 5..................................................................................................................................4

a)..................................................................................................................................................4

b)..................................................................................................................................................5

c) Evaluate the disadvantages of utilising the dividend growth model to value stocks..............5

QUESTION 6..................................................................................................................................6

The size of the annual dividend to return to its shareholders for the factors which needs to be

considered....................................................................................................................................6

The realistic considerations which must be made while determining the amount of the

dividend payout...........................................................................................................................6

b) Make a calculation for each of the 3 alternatives....................................................................6

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

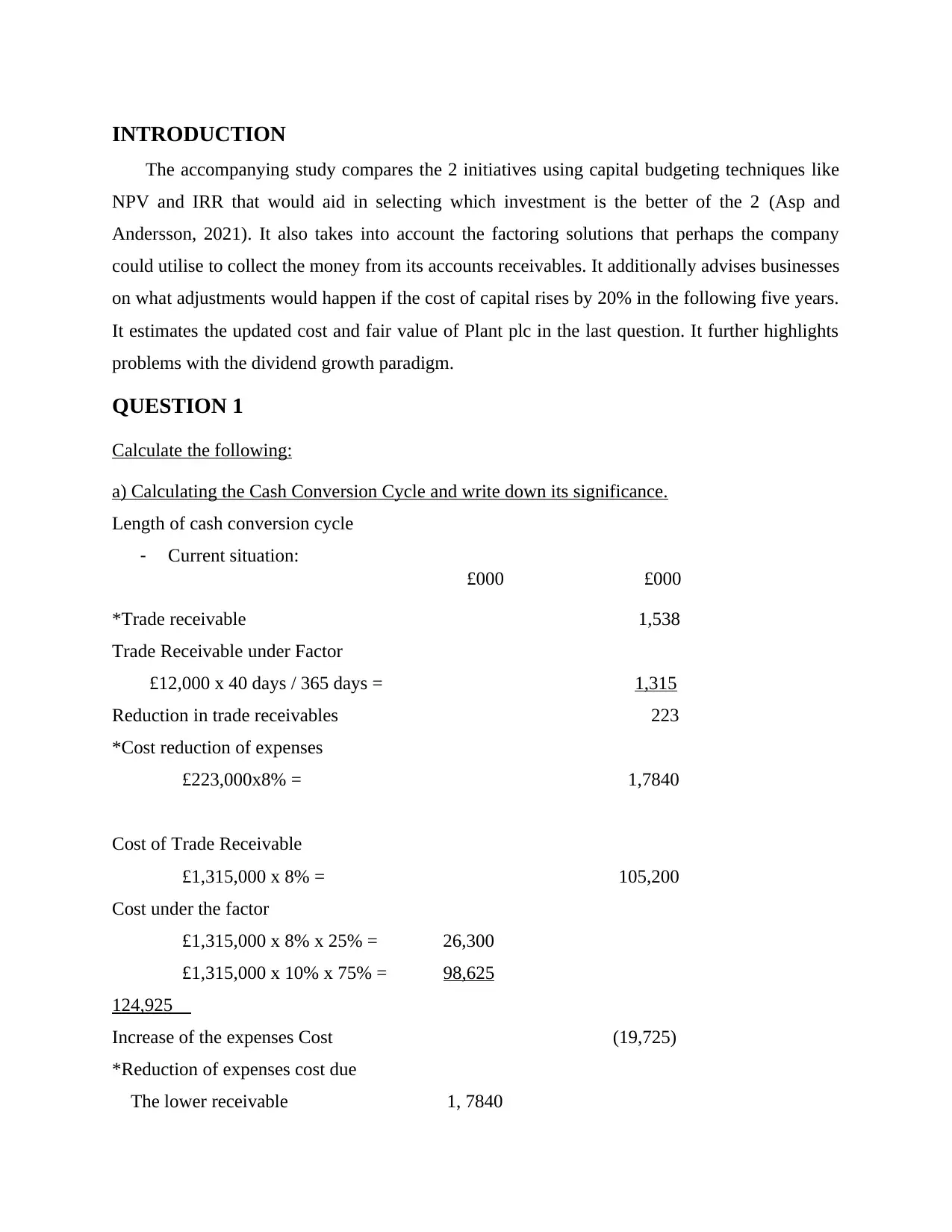

INTRODUCTION

The accompanying study compares the 2 initiatives using capital budgeting techniques like

NPV and IRR that would aid in selecting which investment is the better of the 2 (Asp and

Andersson, 2021). It also takes into account the factoring solutions that perhaps the company

could utilise to collect the money from its accounts receivables. It additionally advises businesses

on what adjustments would happen if the cost of capital rises by 20% in the following five years.

It estimates the updated cost and fair value of Plant plc in the last question. It further highlights

problems with the dividend growth paradigm.

QUESTION 1

Calculate the following:

a) Calculating the Cash Conversion Cycle and write down its significance.

Length of cash conversion cycle

- Current situation:

£000 £000

*Trade receivable 1,538

Trade Receivable under Factor

£12,000 x 40 days / 365 days = 1,315

Reduction in trade receivables 223

*Cost reduction of expenses

£223,000x8% = 1,7840

Cost of Trade Receivable

£1,315,000 x 8% = 105,200

Cost under the factor

£1,315,000 x 8% x 25% = 26,300

£1,315,000 x 10% x 75% = 98,625

124,925

Increase of the expenses Cost (19,725)

*Reduction of expenses cost due

The lower receivable 1, 7840

The accompanying study compares the 2 initiatives using capital budgeting techniques like

NPV and IRR that would aid in selecting which investment is the better of the 2 (Asp and

Andersson, 2021). It also takes into account the factoring solutions that perhaps the company

could utilise to collect the money from its accounts receivables. It additionally advises businesses

on what adjustments would happen if the cost of capital rises by 20% in the following five years.

It estimates the updated cost and fair value of Plant plc in the last question. It further highlights

problems with the dividend growth paradigm.

QUESTION 1

Calculate the following:

a) Calculating the Cash Conversion Cycle and write down its significance.

Length of cash conversion cycle

- Current situation:

£000 £000

*Trade receivable 1,538

Trade Receivable under Factor

£12,000 x 40 days / 365 days = 1,315

Reduction in trade receivables 223

*Cost reduction of expenses

£223,000x8% = 1,7840

Cost of Trade Receivable

£1,315,000 x 8% = 105,200

Cost under the factor

£1,315,000 x 8% x 25% = 26,300

£1,315,000 x 10% x 75% = 98,625

124,925

Increase of the expenses Cost (19,725)

*Reduction of expenses cost due

The lower receivable 1, 7840

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

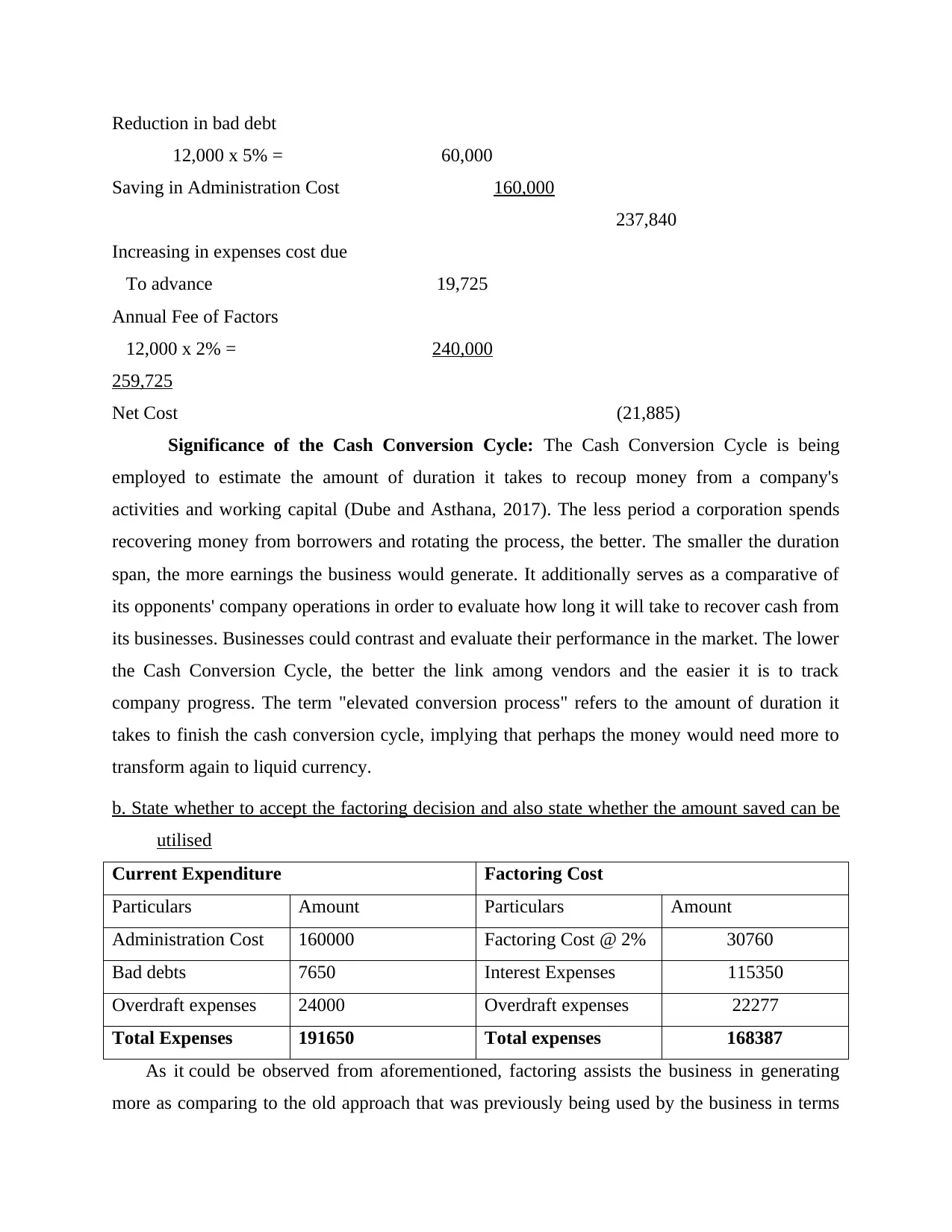

Reduction in bad debt

12,000 x 5% = 60,000

Saving in Administration Cost 160,000

237,840

Increasing in expenses cost due

To advance 19,725

Annual Fee of Factors

12,000 x 2% = 240,000

259,725

Net Cost (21,885)

Significance of the Cash Conversion Cycle: The Cash Conversion Cycle is being

employed to estimate the amount of duration it takes to recoup money from a company's

activities and working capital (Dube and Asthana, 2017). The less period a corporation spends

recovering money from borrowers and rotating the process, the better. The smaller the duration

span, the more earnings the business would generate. It additionally serves as a comparative of

its opponents' company operations in order to evaluate how long it will take to recover cash from

its businesses. Businesses could contrast and evaluate their performance in the market. The lower

the Cash Conversion Cycle, the better the link among vendors and the easier it is to track

company progress. The term "elevated conversion process" refers to the amount of duration it

takes to finish the cash conversion cycle, implying that perhaps the money would need more to

transform again to liquid currency.

b. State whether to accept the factoring decision and also state whether the amount saved can be

utilised

Current Expenditure Factoring Cost

Particulars Amount Particulars Amount

Administration Cost 160000 Factoring Cost @ 2% 30760

Bad debts 7650 Interest Expenses 115350

Overdraft expenses 24000 Overdraft expenses 22277

Total Expenses 191650 Total expenses 168387

As it could be observed from aforementioned, factoring assists the business in generating

more as comparing to the old approach that was previously being used by the business in terms

12,000 x 5% = 60,000

Saving in Administration Cost 160,000

237,840

Increasing in expenses cost due

To advance 19,725

Annual Fee of Factors

12,000 x 2% = 240,000

259,725

Net Cost (21,885)

Significance of the Cash Conversion Cycle: The Cash Conversion Cycle is being

employed to estimate the amount of duration it takes to recoup money from a company's

activities and working capital (Dube and Asthana, 2017). The less period a corporation spends

recovering money from borrowers and rotating the process, the better. The smaller the duration

span, the more earnings the business would generate. It additionally serves as a comparative of

its opponents' company operations in order to evaluate how long it will take to recover cash from

its businesses. Businesses could contrast and evaluate their performance in the market. The lower

the Cash Conversion Cycle, the better the link among vendors and the easier it is to track

company progress. The term "elevated conversion process" refers to the amount of duration it

takes to finish the cash conversion cycle, implying that perhaps the money would need more to

transform again to liquid currency.

b. State whether to accept the factoring decision and also state whether the amount saved can be

utilised

Current Expenditure Factoring Cost

Particulars Amount Particulars Amount

Administration Cost 160000 Factoring Cost @ 2% 30760

Bad debts 7650 Interest Expenses 115350

Overdraft expenses 24000 Overdraft expenses 22277

Total Expenses 191650 Total expenses 168387

As it could be observed from aforementioned, factoring assists the business in generating

more as comparing to the old approach that was previously being used by the business in terms

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

of intended to facilitate in retrieving the accounts receivables of the corporation and

thus business could employ factoring facilities. On an annual basis, the company would save

23263 by adopting factoring. The money gained through applying factoring in the firm would go

toward reducing the firm's overdraft charges, which are needed to supplement the firm's cash

flow. The money might be put to good use by the company in its commercial dealings (Esmaeili

and Golpayegani, 2021).

QUESTION 3

Calculate and explain the following:

(a) The theoretical ex-rights price per share

2 million ordinary shares issued to raise £1,000,000

Issue cost= £50,000

A Theoretical Ex-Right price per share = £2.64

Issue price at 20% discount

2.75 x 0.80 = £2.20 (Right issue price)

Ex-right price

(2.75 x 4 shares) + (2.20 x 1 new share) / 5 = £2.64

(b) The net cash raised

Net Cash raised = fund raised – issue cost

Net cash raised = £1,050,000

2 million ordinary shares = 500,000 new shares

500,000 new shares x 2.20 = £1,100,000

Net Cash raised = fund raised – issue cost

Net cash raised = £1,100,000 – £50,000 = £1,050,000

Net cash raised = £1,050,000

(c) The value of the rights.

Value of the right = T. ex-right price – right issue

Value of the right = 2.64 -2.20

Value of the right = £0.44

thus business could employ factoring facilities. On an annual basis, the company would save

23263 by adopting factoring. The money gained through applying factoring in the firm would go

toward reducing the firm's overdraft charges, which are needed to supplement the firm's cash

flow. The money might be put to good use by the company in its commercial dealings (Esmaeili

and Golpayegani, 2021).

QUESTION 3

Calculate and explain the following:

(a) The theoretical ex-rights price per share

2 million ordinary shares issued to raise £1,000,000

Issue cost= £50,000

A Theoretical Ex-Right price per share = £2.64

Issue price at 20% discount

2.75 x 0.80 = £2.20 (Right issue price)

Ex-right price

(2.75 x 4 shares) + (2.20 x 1 new share) / 5 = £2.64

(b) The net cash raised

Net Cash raised = fund raised – issue cost

Net cash raised = £1,050,000

2 million ordinary shares = 500,000 new shares

500,000 new shares x 2.20 = £1,100,000

Net Cash raised = fund raised – issue cost

Net cash raised = £1,100,000 – £50,000 = £1,050,000

Net cash raised = £1,050,000

(c) The value of the rights.

Value of the right = T. ex-right price – right issue

Value of the right = 2.64 -2.20

Value of the right = £0.44

d) The benefits and drawbacks of the right issue

Current shareholders of the business are invited to participate in the rights issue and buy

extra shares. If there had been an opportunity to acquire more units at a cheaper cost than

competitors, existing shareholders will have a security cushion. Hanging Valley Plc requires

monetary assistance, therefore they give raw goods to allow companies to build up operations

and meet responsibilities effectively. Evaluating rights issues does have advantages and

drawbacks and thus they are explained below in detail:

Benefits:

Raise promoters equity as perhaps the most strong statements would be that it encourages

business people to expand their ownership. Monetary supporters could seek the fund's

"limit investing part," thus bolstering existing positions (Kaindl, Hoch and Popp, 2017).

The simplest way to increase investment is to issue equity, which has less regulations and

standards than community contributions because it is a more autonomous component.

Because the distribution of more shares, the fundamental approach for a suitable issuing

is for the authorized endeavour to file a deal statement to the Board of Control for these

assets and the operation phase for general review and authorization should be done before

it.

Drawbacks:

Whenever an organisation offers a valuation proposal to generate funds, the participation

of present finance supporters might well be lowered, lowering the worth of every

component. Whenever new shareholders come in and reduce equity ownership, property

investment financing supporters have a difficult time.

Increasing income to a certain level as an evident drawback would be that an organisation

could not obtain a specified quantity in an urgent initial public offer mindset. How much

money a group could generate with it is always not certain and thus add as a drawback to

this approach (Kaowiwattanakul, 2016)(Shishkov and Janssen, 2017).

QUESTION 5

a)

Shares’ Fair price

Dividends for the past 4 years = 13p, 14p, 17p and 18p

Current shareholders of the business are invited to participate in the rights issue and buy

extra shares. If there had been an opportunity to acquire more units at a cheaper cost than

competitors, existing shareholders will have a security cushion. Hanging Valley Plc requires

monetary assistance, therefore they give raw goods to allow companies to build up operations

and meet responsibilities effectively. Evaluating rights issues does have advantages and

drawbacks and thus they are explained below in detail:

Benefits:

Raise promoters equity as perhaps the most strong statements would be that it encourages

business people to expand their ownership. Monetary supporters could seek the fund's

"limit investing part," thus bolstering existing positions (Kaindl, Hoch and Popp, 2017).

The simplest way to increase investment is to issue equity, which has less regulations and

standards than community contributions because it is a more autonomous component.

Because the distribution of more shares, the fundamental approach for a suitable issuing

is for the authorized endeavour to file a deal statement to the Board of Control for these

assets and the operation phase for general review and authorization should be done before

it.

Drawbacks:

Whenever an organisation offers a valuation proposal to generate funds, the participation

of present finance supporters might well be lowered, lowering the worth of every

component. Whenever new shareholders come in and reduce equity ownership, property

investment financing supporters have a difficult time.

Increasing income to a certain level as an evident drawback would be that an organisation

could not obtain a specified quantity in an urgent initial public offer mindset. How much

money a group could generate with it is always not certain and thus add as a drawback to

this approach (Kaowiwattanakul, 2016)(Shishkov and Janssen, 2017).

QUESTION 5

a)

Shares’ Fair price

Dividends for the past 4 years = 13p, 14p, 17p and 18p

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Rate Return = 14% = 0.14

Number of Years (n) = 4

Ordinary dividend per share = 20p

13p x (1 + = 20p

(1 + ) =

Growth = 1.1137 – 1

Growth = 0.1137

Growth = 11.37%

P = = 846.92p = £8.47

Fair price share is £8.47.

b)

Calculation of new price shares when the rate of returns changes to 15.4%

P =(20 (1+0.1137))/(0.154-0.1137) = 552.70p = £5.53

c) Evaluate the disadvantages of utilising the dividend growth model to value stocks

When small capital shares are contrasted to large capital shares, local companies

outperform larger companies in the big scheme of things. Because many independent

businesses do not have that profit-driven attitude, such evaluation methodology could

not be utilised to estimate their worth (van Meerkerk, 2017). It should only be utilised for

highly successful companies. If monetary supporters concentrate solely on this strategy,

they might miss out on other chances to diversify their investments.

The reality is that a group's revenues do not expand at a fixed value throughout presently

and in the future in the venture capital sector. In the big scheme of things, several

businesses have boosted their profitability and others might have to cut back on existing

earnings. A few even went so far as to cut the prices of the competitors that they lowered

their prices so that the competition can be increased and the other firm would have less of

the profits and more of the losses. Such actions are not included in the assessment

Number of Years (n) = 4

Ordinary dividend per share = 20p

13p x (1 + = 20p

(1 + ) =

Growth = 1.1137 – 1

Growth = 0.1137

Growth = 11.37%

P = = 846.92p = £8.47

Fair price share is £8.47.

b)

Calculation of new price shares when the rate of returns changes to 15.4%

P =(20 (1+0.1137))/(0.154-0.1137) = 552.70p = £5.53

c) Evaluate the disadvantages of utilising the dividend growth model to value stocks

When small capital shares are contrasted to large capital shares, local companies

outperform larger companies in the big scheme of things. Because many independent

businesses do not have that profit-driven attitude, such evaluation methodology could

not be utilised to estimate their worth (van Meerkerk, 2017). It should only be utilised for

highly successful companies. If monetary supporters concentrate solely on this strategy,

they might miss out on other chances to diversify their investments.

The reality is that a group's revenues do not expand at a fixed value throughout presently

and in the future in the venture capital sector. In the big scheme of things, several

businesses have boosted their profitability and others might have to cut back on existing

earnings. A few even went so far as to cut the prices of the competitors that they lowered

their prices so that the competition can be increased and the other firm would have less of

the profits and more of the losses. Such actions are not included in the assessment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

model's appraisal process. This implies that the approach is better placed for a variety of

businesses which consistently generate revenue increases year after year.

QUESTION 6

The size of the annual dividend to return to its shareholders for the factors which needs to be

considered

Liquidity: Especially if the company requires deposits, the smaller profitability level is

preferred since the asset provides a means of financing and therefore does not require

exterior acquisition at a relatively constant level.

Efficiency and growth: The smaller the payout, the greater the predicted growth and

efficiency, since finance traders would underestimate the group's return on capital,

increasing the theoretical worth along with the firm's valuation.

The realistic considerations which must be made while determining the amount of the dividend

payout

Return payment deadlines as the corporation must determine if it has too many holdings

to pay returns. Accessibility is not the same as efficiency. As a result, the amount of the

payout is limited by the existing resources (Von Peinen, Böhmer and Lindemann, 2018).

The income moving conditions laid forth in the Companies Act must be fulfilled prior

earnings can be declared. The amount is limited by the provisions of the corporate

legislation (Weller, 2019).

Produce the desired marketplace expectations as if a company reports unusually large

earnings in a given period, the marketplace might anticipate the business to maintain pace

with the earnings. As a result, it's critical to overlook the dividend's amount (Yu, 2018).

b) Make a calculation for each of the 3 alternatives

Wealth of Shareholder = Market value of Shares held + Dividend received + Market value of

Shares newly allotted - Loss in value of shares due to dividend / scrip dividend

Because no worth is created in any of the three circumstances, the income of the

shareholders stays unchanged as the income that already exists.

= 432 * 1250 = 540,000

businesses which consistently generate revenue increases year after year.

QUESTION 6

The size of the annual dividend to return to its shareholders for the factors which needs to be

considered

Liquidity: Especially if the company requires deposits, the smaller profitability level is

preferred since the asset provides a means of financing and therefore does not require

exterior acquisition at a relatively constant level.

Efficiency and growth: The smaller the payout, the greater the predicted growth and

efficiency, since finance traders would underestimate the group's return on capital,

increasing the theoretical worth along with the firm's valuation.

The realistic considerations which must be made while determining the amount of the dividend

payout

Return payment deadlines as the corporation must determine if it has too many holdings

to pay returns. Accessibility is not the same as efficiency. As a result, the amount of the

payout is limited by the existing resources (Von Peinen, Böhmer and Lindemann, 2018).

The income moving conditions laid forth in the Companies Act must be fulfilled prior

earnings can be declared. The amount is limited by the provisions of the corporate

legislation (Weller, 2019).

Produce the desired marketplace expectations as if a company reports unusually large

earnings in a given period, the marketplace might anticipate the business to maintain pace

with the earnings. As a result, it's critical to overlook the dividend's amount (Yu, 2018).

b) Make a calculation for each of the 3 alternatives

Wealth of Shareholder = Market value of Shares held + Dividend received + Market value of

Shares newly allotted - Loss in value of shares due to dividend / scrip dividend

Because no worth is created in any of the three circumstances, the income of the

shareholders stays unchanged as the income that already exists.

= 432 * 1250 = 540,000

i) cash dividend payment A cash dividend payment of 15p per share = 15 * 1250 + (432

- 15) * 1250 = 18,750 + 521,250 = 540,000

(Cash per share * shares held) + (shares held * new market value per share)

ii) A 5% scrip dividend = 1250 * 105% * (540,000 / (1250 * 105%) = 540,000

(New total shares * new Market value per share)

iii) A repurchase of 15 % of ordinary share capital at the current market price = 187.5 *

432 + 1062.5 * 432 = 540,000

(Cash for 187.5 shares + Market value of remaining shares)

CONCLUSION

It could be concluded from the foregoing given study that it investigates which initiative

strategy will be more useful and appropriate for the Better plc organization. It will be beneficial

to analyze using methods like NPV and IRR. It also suggests that the company's cost of capital

will change by more than 20% in the next five years. In a subsequent phase, the cost of

each share, net income, and worth of rights issue of the hanging plc firm would've been

determined, together with the advantages and restrictions, to solve the appropriate issue.

Furthermore, this could establish the firm's fresh and reasonable value, as well as the issue that is

increasing owing to the dividend plus growth approach.

- 15) * 1250 = 18,750 + 521,250 = 540,000

(Cash per share * shares held) + (shares held * new market value per share)

ii) A 5% scrip dividend = 1250 * 105% * (540,000 / (1250 * 105%) = 540,000

(New total shares * new Market value per share)

iii) A repurchase of 15 % of ordinary share capital at the current market price = 187.5 *

432 + 1062.5 * 432 = 540,000

(Cash for 187.5 shares + Market value of remaining shares)

CONCLUSION

It could be concluded from the foregoing given study that it investigates which initiative

strategy will be more useful and appropriate for the Better plc organization. It will be beneficial

to analyze using methods like NPV and IRR. It also suggests that the company's cost of capital

will change by more than 20% in the next five years. In a subsequent phase, the cost of

each share, net income, and worth of rights issue of the hanging plc firm would've been

determined, together with the advantages and restrictions, to solve the appropriate issue.

Furthermore, this could establish the firm's fresh and reasonable value, as well as the issue that is

increasing owing to the dividend plus growth approach.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and journals

Asp, L. and Andersson, J., 2021. Marketing Communication in the Context of Selling a

Business: Business Brokers and how They Communicate Value of a Business.

Dube, V.S. and Asthana, P.K., 2017. A comparative study on Financial Literacy of Uttar Pradesh

with Central Zone states in India. IOSR Journal of Business and Management (IOSR-

JBM), 19(10), pp.22-27.

Esmaeili, L. and Golpayegani, A.H., 2021. A novel method for discovering process based on the

network analysis approach in the context of social commerce systems. Journal of

theoretical and applied electronic commerce research, 16(2), pp.34-62.

Kaindl, H., Hoch, R. and Popp, R., 2017, May. Semantic task specification in business process

context. In 2017 11th International Conference on Research Challenges in Information

Science (RCIS) (pp. 286-291). IEEE.

Kaowiwattanakul, S., 2016. Role of International Study Experiences in the Personal and

Professional Development of University Lecturers in the Humanities and Social

Sciences Fields in Thailand. International Education Journal: Comparative

Perspectives, 15(2), pp.58-71.

Shishkov, B. and Janssen, M., 2017, May. Enforcing context-awareness and privacy-by-design in

the specification of information systems. In International Symposium on Business

Modeling and Software Design (pp. 87-111). Springer, Cham.

van Meerkerk, E., 2017. Teacher logbooks and professional development: A tool for assessing

transformative learning processes. International Journal of Qualitative Methods, 16(1),

p.1609406917735255.

Von Peinen, A., Böhmer, A.I. and Lindemann, U., 2018, June. System Dynamics as a Tool for

Data Driven Business Model Design in the Context of Autonomous Ride Hailing. In

2018 IEEE International Conference on Engineering, Technology and Innovation

(ICE/ITMC) (pp. 1-6). IEEE.

Weller, J., 2019. Critical reflection through personal pronoun analysis (critical analysis) to

identify and individualise teacher professional development. Teacher

Development, 23(1), pp.139-154.

Yu, W.M., 2018. Critical incidents as a reflective tool for professional development: An

experience with in-service teachers. Reflective Practice, 19(6), pp.763-776.

Books and journals

Asp, L. and Andersson, J., 2021. Marketing Communication in the Context of Selling a

Business: Business Brokers and how They Communicate Value of a Business.

Dube, V.S. and Asthana, P.K., 2017. A comparative study on Financial Literacy of Uttar Pradesh

with Central Zone states in India. IOSR Journal of Business and Management (IOSR-

JBM), 19(10), pp.22-27.

Esmaeili, L. and Golpayegani, A.H., 2021. A novel method for discovering process based on the

network analysis approach in the context of social commerce systems. Journal of

theoretical and applied electronic commerce research, 16(2), pp.34-62.

Kaindl, H., Hoch, R. and Popp, R., 2017, May. Semantic task specification in business process

context. In 2017 11th International Conference on Research Challenges in Information

Science (RCIS) (pp. 286-291). IEEE.

Kaowiwattanakul, S., 2016. Role of International Study Experiences in the Personal and

Professional Development of University Lecturers in the Humanities and Social

Sciences Fields in Thailand. International Education Journal: Comparative

Perspectives, 15(2), pp.58-71.

Shishkov, B. and Janssen, M., 2017, May. Enforcing context-awareness and privacy-by-design in

the specification of information systems. In International Symposium on Business

Modeling and Software Design (pp. 87-111). Springer, Cham.

van Meerkerk, E., 2017. Teacher logbooks and professional development: A tool for assessing

transformative learning processes. International Journal of Qualitative Methods, 16(1),

p.1609406917735255.

Von Peinen, A., Böhmer, A.I. and Lindemann, U., 2018, June. System Dynamics as a Tool for

Data Driven Business Model Design in the Context of Autonomous Ride Hailing. In

2018 IEEE International Conference on Engineering, Technology and Innovation

(ICE/ITMC) (pp. 1-6). IEEE.

Weller, J., 2019. Critical reflection through personal pronoun analysis (critical analysis) to

identify and individualise teacher professional development. Teacher

Development, 23(1), pp.139-154.

Yu, W.M., 2018. Critical incidents as a reflective tool for professional development: An

experience with in-service teachers. Reflective Practice, 19(6), pp.763-776.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.