Detailed Business Finance Report: Investment, Factoring, and Rights

VerifiedAdded on 2023/06/09

|12

|2687

|395

Report

AI Summary

This report provides a comprehensive analysis of investment decisions, factoring, and rights issues in the context of business finance. It evaluates two projects using Net Present Value (NPV) and Internal Rate of Return (IRR) to determine the most profitable investment. The report also assesses the feasibility of using factoring services to improve cash flow and analyzes the impact of a potential increase in the cost of capital. Furthermore, it calculates the theoretical ex-rights price per share, net cash raised, and the value of rights in a rights issue scenario. The analysis extends to share valuation, using the dividend growth model, and identifies its limitations. The report concludes by recommending the most suitable project for investment and highlighting the strategic financial considerations for Better plc and Hanging Valley Plc.

Business Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

QUESTION 1..................................................................................................................................3

Calculate the following:...............................................................................................................3

a) Calculating the Cash Conversion Cycle and write down its significance...............................3

b. State whether to accept the factoring decision and also state whether the amount saved can

be utilised.....................................................................................................................................4

QUESTION 2..................................................................................................................................5

a) Compute NPV and suggest which project should be accepted...............................................5

b) Calculate IRR and on the basis of this which project should be accepted..............................6

c) If the cost of capital increase to 20 % in year 5, then does the changes would be advisable..7

QUESTION 3..................................................................................................................................8

(a). the theoretical ex-rights price per share................................................................................8

(b). the net cash raised.................................................................................................................8

(c). the value of the rights............................................................................................................8

d) Pros and cons of right issue.....................................................................................................9

QUESTION 5..................................................................................................................................9

a)..................................................................................................................................................9

b)................................................................................................................................................10

c) Identify the drawbacks of using dividend growth model as part of valuing shares..............10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................3

QUESTION 1..................................................................................................................................3

Calculate the following:...............................................................................................................3

a) Calculating the Cash Conversion Cycle and write down its significance...............................3

b. State whether to accept the factoring decision and also state whether the amount saved can

be utilised.....................................................................................................................................4

QUESTION 2..................................................................................................................................5

a) Compute NPV and suggest which project should be accepted...............................................5

b) Calculate IRR and on the basis of this which project should be accepted..............................6

c) If the cost of capital increase to 20 % in year 5, then does the changes would be advisable..7

QUESTION 3..................................................................................................................................8

(a). the theoretical ex-rights price per share................................................................................8

(b). the net cash raised.................................................................................................................8

(c). the value of the rights............................................................................................................8

d) Pros and cons of right issue.....................................................................................................9

QUESTION 5..................................................................................................................................9

a)..................................................................................................................................................9

b)................................................................................................................................................10

c) Identify the drawbacks of using dividend growth model as part of valuing shares..............10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

INTRODUCTION

In the following project it states about the two projects on the basis of capital budgeting

methods such as Net present value and internal rate of return which will help in determining the

best project among the two projects. It also considers the factoring services that can be used by

the organisation to recover the amount from its trade receivables. It also advices company as

what changes will occur if cost of capital will increase by 20% in the next 5 years. In last

question it calculates the new price and fair price of the Plant plc. It also identifies the issues

which are related to the dividend growth model (Alakaleek and Cooper, 2018).

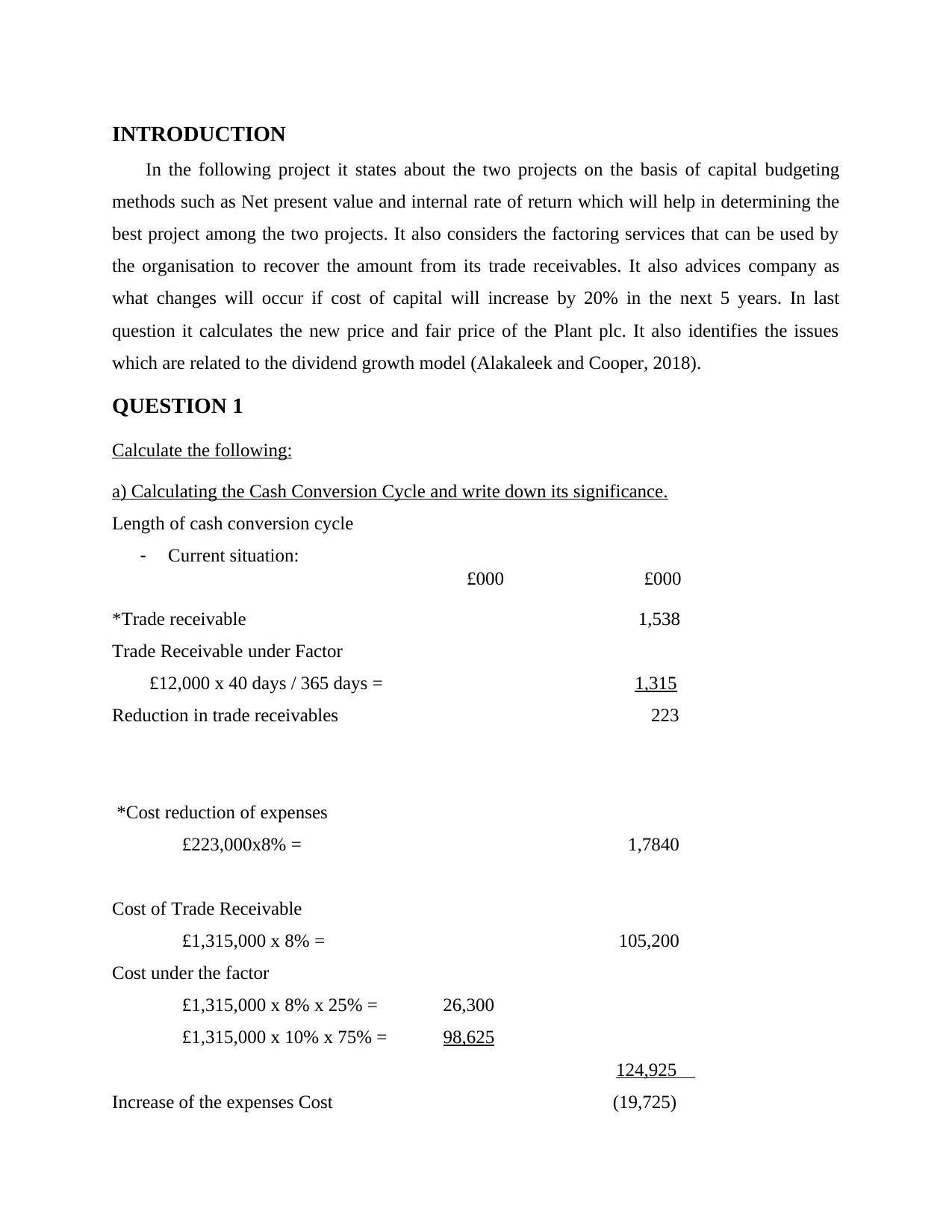

QUESTION 1

Calculate the following:

a) Calculating the Cash Conversion Cycle and write down its significance.

Length of cash conversion cycle

- Current situation:

£000 £000

*Trade receivable 1,538

Trade Receivable under Factor

£12,000 x 40 days / 365 days = 1,315

Reduction in trade receivables 223

*Cost reduction of expenses

£223,000x8% = 1,7840

Cost of Trade Receivable

£1,315,000 x 8% = 105,200

Cost under the factor

£1,315,000 x 8% x 25% = 26,300

£1,315,000 x 10% x 75% = 98,625

124,925

Increase of the expenses Cost (19,725)

In the following project it states about the two projects on the basis of capital budgeting

methods such as Net present value and internal rate of return which will help in determining the

best project among the two projects. It also considers the factoring services that can be used by

the organisation to recover the amount from its trade receivables. It also advices company as

what changes will occur if cost of capital will increase by 20% in the next 5 years. In last

question it calculates the new price and fair price of the Plant plc. It also identifies the issues

which are related to the dividend growth model (Alakaleek and Cooper, 2018).

QUESTION 1

Calculate the following:

a) Calculating the Cash Conversion Cycle and write down its significance.

Length of cash conversion cycle

- Current situation:

£000 £000

*Trade receivable 1,538

Trade Receivable under Factor

£12,000 x 40 days / 365 days = 1,315

Reduction in trade receivables 223

*Cost reduction of expenses

£223,000x8% = 1,7840

Cost of Trade Receivable

£1,315,000 x 8% = 105,200

Cost under the factor

£1,315,000 x 8% x 25% = 26,300

£1,315,000 x 10% x 75% = 98,625

124,925

Increase of the expenses Cost (19,725)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

*Reduction of expenses cost due

the lower receivable 1,7840

Reduction in bad debt

12,000 x 5% = 60,000

Saving in Admin. Cost 160,000

237,840

Increasing in expenses cost due

To advance 19,725

Annual Fee of Factors

12,000 x 2% = 240,000

259,725

Net Cost (21,885)

Significance of Cash Conversion Cycle:

Cash Conversion cycle is used to determine the time period it requires to recover cash

from the business operations activity and Cash flow of the business. The shorter time business

takes to recover its amount from the debtors and rotates the cycle more it will be beneficial for

the business. The shorter the time period the more will be revenue for the organisation. It also

works as a comparison of the business activities from its competitors to determine the time

period it requires to recall its money from its business operations. Business can compare and

check how they are performing in the industry (Alemany and Andreoli, 2018).

The shorter the Cash Conversion Cycle it will improve the relationship between the

suppliers and also helps in knowing the performance of the business. High conversion cycle

states that the time period it requires to complete the cash conversion cycle which means that it

will take longer for the cash to convert back to liquid form.

b. State whether to accept the factoring decision and also state whether the amount saved can be

utilised.

the lower receivable 1,7840

Reduction in bad debt

12,000 x 5% = 60,000

Saving in Admin. Cost 160,000

237,840

Increasing in expenses cost due

To advance 19,725

Annual Fee of Factors

12,000 x 2% = 240,000

259,725

Net Cost (21,885)

Significance of Cash Conversion Cycle:

Cash Conversion cycle is used to determine the time period it requires to recover cash

from the business operations activity and Cash flow of the business. The shorter time business

takes to recover its amount from the debtors and rotates the cycle more it will be beneficial for

the business. The shorter the time period the more will be revenue for the organisation. It also

works as a comparison of the business activities from its competitors to determine the time

period it requires to recall its money from its business operations. Business can compare and

check how they are performing in the industry (Alemany and Andreoli, 2018).

The shorter the Cash Conversion Cycle it will improve the relationship between the

suppliers and also helps in knowing the performance of the business. High conversion cycle

states that the time period it requires to complete the cash conversion cycle which means that it

will take longer for the cash to convert back to liquid form.

b. State whether to accept the factoring decision and also state whether the amount saved can be

utilised.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

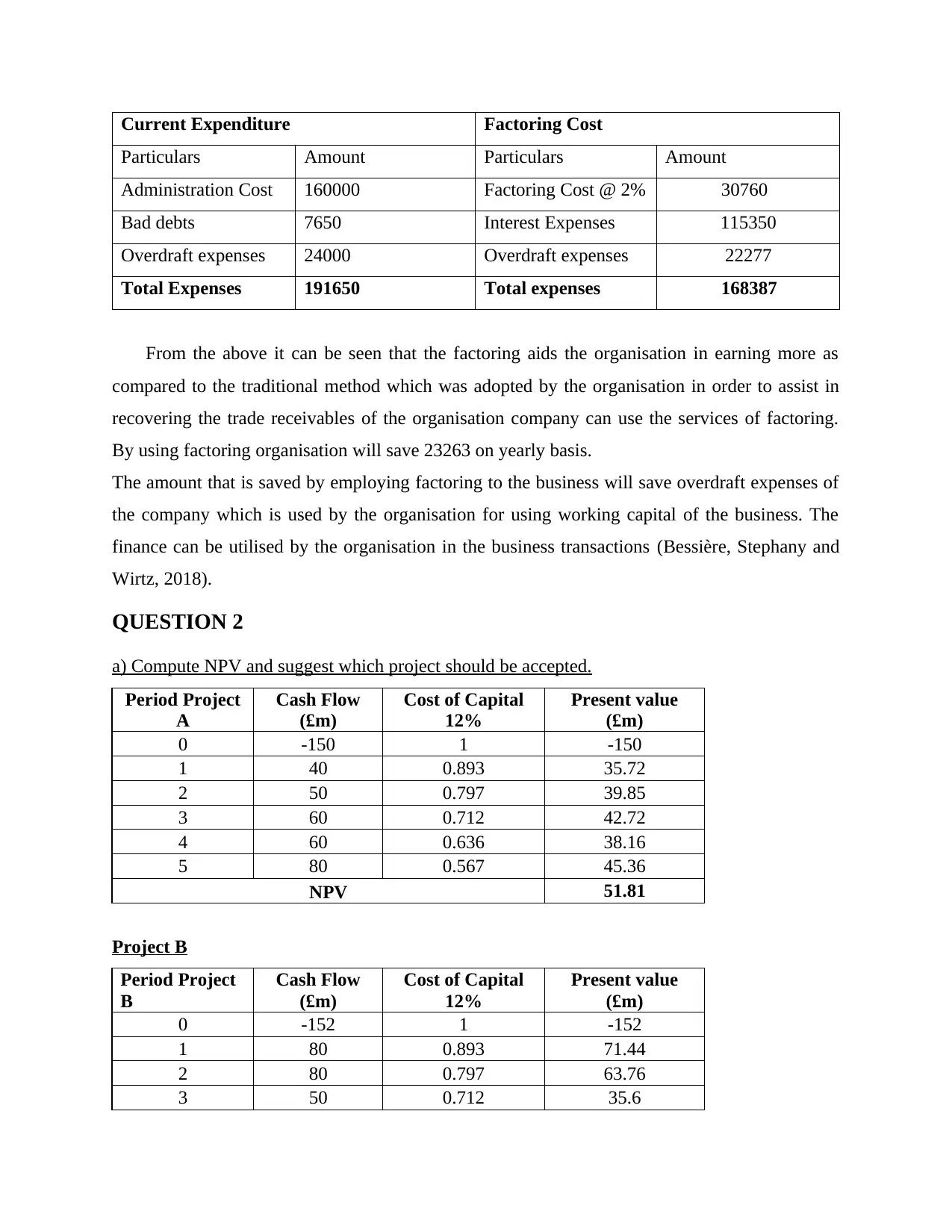

Current Expenditure Factoring Cost

Particulars Amount Particulars Amount

Administration Cost 160000 Factoring Cost @ 2% 30760

Bad debts 7650 Interest Expenses 115350

Overdraft expenses 24000 Overdraft expenses 22277

Total Expenses 191650 Total expenses 168387

From the above it can be seen that the factoring aids the organisation in earning more as

compared to the traditional method which was adopted by the organisation in order to assist in

recovering the trade receivables of the organisation company can use the services of factoring.

By using factoring organisation will save 23263 on yearly basis.

The amount that is saved by employing factoring to the business will save overdraft expenses of

the company which is used by the organisation for using working capital of the business. The

finance can be utilised by the organisation in the business transactions (Bessière, Stephany and

Wirtz, 2018).

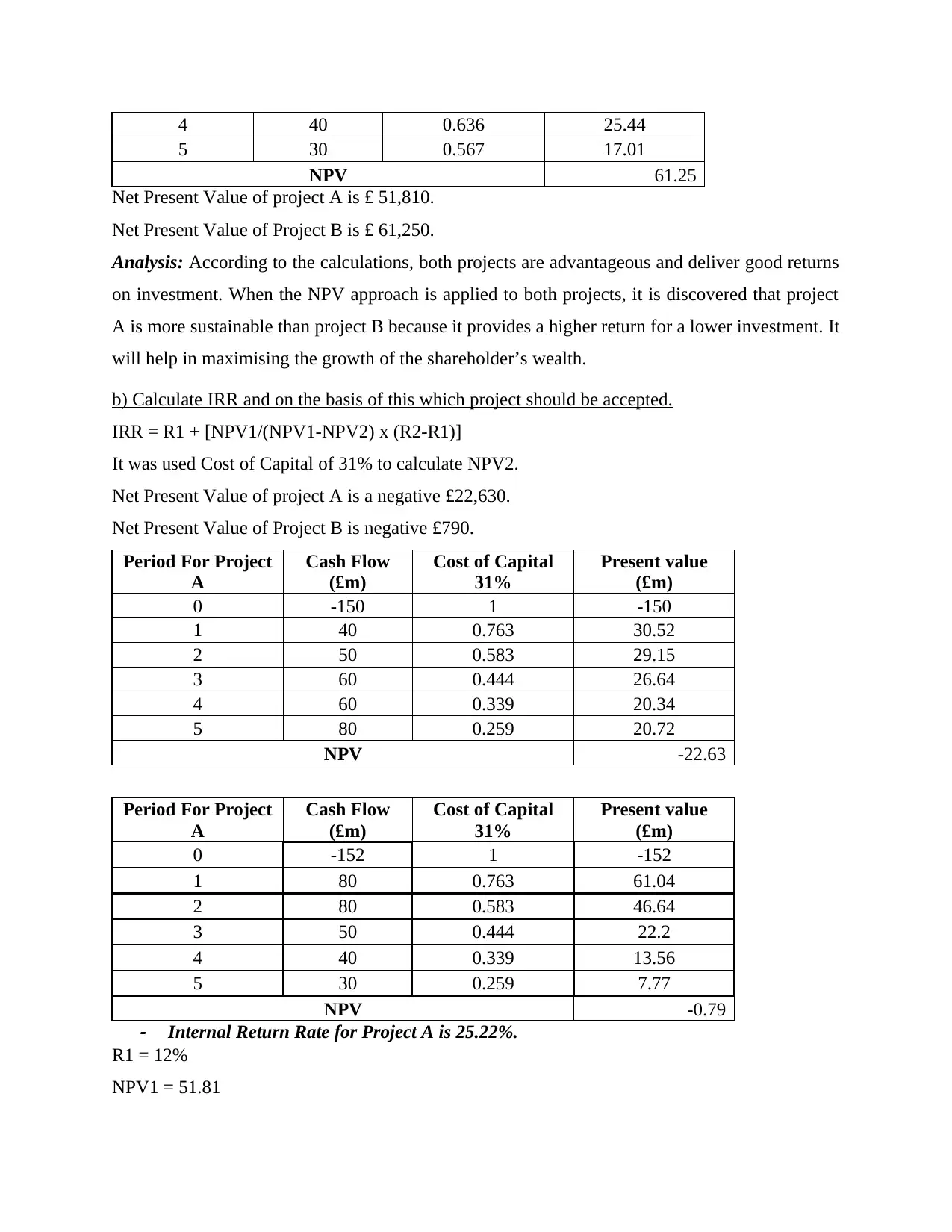

QUESTION 2

a) Compute NPV and suggest which project should be accepted.

Period Project

A

Cash Flow

(£m)

Cost of Capital

12%

Present value

(£m)

0 -150 1 -150

1 40 0.893 35.72

2 50 0.797 39.85

3 60 0.712 42.72

4 60 0.636 38.16

5 80 0.567 45.36

NPV 51.81

Project B

Period Project

B

Cash Flow

(£m)

Cost of Capital

12%

Present value

(£m)

0 -152 1 -152

1 80 0.893 71.44

2 80 0.797 63.76

3 50 0.712 35.6

Particulars Amount Particulars Amount

Administration Cost 160000 Factoring Cost @ 2% 30760

Bad debts 7650 Interest Expenses 115350

Overdraft expenses 24000 Overdraft expenses 22277

Total Expenses 191650 Total expenses 168387

From the above it can be seen that the factoring aids the organisation in earning more as

compared to the traditional method which was adopted by the organisation in order to assist in

recovering the trade receivables of the organisation company can use the services of factoring.

By using factoring organisation will save 23263 on yearly basis.

The amount that is saved by employing factoring to the business will save overdraft expenses of

the company which is used by the organisation for using working capital of the business. The

finance can be utilised by the organisation in the business transactions (Bessière, Stephany and

Wirtz, 2018).

QUESTION 2

a) Compute NPV and suggest which project should be accepted.

Period Project

A

Cash Flow

(£m)

Cost of Capital

12%

Present value

(£m)

0 -150 1 -150

1 40 0.893 35.72

2 50 0.797 39.85

3 60 0.712 42.72

4 60 0.636 38.16

5 80 0.567 45.36

NPV 51.81

Project B

Period Project

B

Cash Flow

(£m)

Cost of Capital

12%

Present value

(£m)

0 -152 1 -152

1 80 0.893 71.44

2 80 0.797 63.76

3 50 0.712 35.6

4 40 0.636 25.44

5 30 0.567 17.01

NPV 61.25

Net Present Value of project A is £ 51,810.

Net Present Value of Project B is £ 61,250.

Analysis: According to the calculations, both projects are advantageous and deliver good returns

on investment. When the NPV approach is applied to both projects, it is discovered that project

A is more sustainable than project B because it provides a higher return for a lower investment. It

will help in maximising the growth of the shareholder’s wealth.

b) Calculate IRR and on the basis of this which project should be accepted.

IRR = R1 + [NPV1/(NPV1-NPV2) x (R2-R1)]

It was used Cost of Capital of 31% to calculate NPV2.

Net Present Value of project A is a negative £22,630.

Net Present Value of Project B is negative £790.

Period For Project

A

Cash Flow

(£m)

Cost of Capital

31%

Present value

(£m)

0 -150 1 -150

1 40 0.763 30.52

2 50 0.583 29.15

3 60 0.444 26.64

4 60 0.339 20.34

5 80 0.259 20.72

NPV -22.63

Period For Project

A

Cash Flow

(£m)

Cost of Capital

31%

Present value

(£m)

0 -152 1 -152

1 80 0.763 61.04

2 80 0.583 46.64

3 50 0.444 22.2

4 40 0.339 13.56

5 30 0.259 7.77

NPV -0.79

- Internal Return Rate for Project A is 25.22%.

R1 = 12%

NPV1 = 51.81

5 30 0.567 17.01

NPV 61.25

Net Present Value of project A is £ 51,810.

Net Present Value of Project B is £ 61,250.

Analysis: According to the calculations, both projects are advantageous and deliver good returns

on investment. When the NPV approach is applied to both projects, it is discovered that project

A is more sustainable than project B because it provides a higher return for a lower investment. It

will help in maximising the growth of the shareholder’s wealth.

b) Calculate IRR and on the basis of this which project should be accepted.

IRR = R1 + [NPV1/(NPV1-NPV2) x (R2-R1)]

It was used Cost of Capital of 31% to calculate NPV2.

Net Present Value of project A is a negative £22,630.

Net Present Value of Project B is negative £790.

Period For Project

A

Cash Flow

(£m)

Cost of Capital

31%

Present value

(£m)

0 -150 1 -150

1 40 0.763 30.52

2 50 0.583 29.15

3 60 0.444 26.64

4 60 0.339 20.34

5 80 0.259 20.72

NPV -22.63

Period For Project

A

Cash Flow

(£m)

Cost of Capital

31%

Present value

(£m)

0 -152 1 -152

1 80 0.763 61.04

2 80 0.583 46.64

3 50 0.444 22.2

4 40 0.339 13.56

5 30 0.259 7.77

NPV -0.79

- Internal Return Rate for Project A is 25.22%.

R1 = 12%

NPV1 = 51.81

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

R2 = 31%

NPV2 = (22.68)

IRR = 12 + [(51.81 / (51.81+22.63) x (31-12)]

IRR = 25.22%

Conclusion: Cost of Capital more than 25.22% will turn NPV negative and less than 25.22% will

show a NPV positive.

- Internal Return Rate for Project B is

R1 = 12%

NPV1 = 61.25

R2 = 31%

NPV2 = (0.79)

IRR = 12 + [(61.25 / (61.25+0.79) x (31-12)]

IRR = 30.76%

Conclusion: Cost of Capital more than 25.22% will turn NPV negative and less than 25.22% will

show a NPV positive.

c) If the cost of capital increase to 20 % in year 5, then does the changes would be advisable.

Period For Project

A

Cash Flow

(£m)

Cost of Capital

31%

Present value

(£m)

0 -150 1 -150

1 40 0.893 35.72

2 50 0.797 39.85

3 60 0.712 42.72

4 60 0.636 38.16

5 80 0.833 66.67

NPV 73.12

Period For Project

B

Cash Flow

(£m)

Cost of Capital

31%

Present value

(£m)

0 -152 1 -152

1 80 0.893 71.44

2 80 0.797 63.76

3 50 0.712 35.6

4 40 0.636 25.44

NPV2 = (22.68)

IRR = 12 + [(51.81 / (51.81+22.63) x (31-12)]

IRR = 25.22%

Conclusion: Cost of Capital more than 25.22% will turn NPV negative and less than 25.22% will

show a NPV positive.

- Internal Return Rate for Project B is

R1 = 12%

NPV1 = 61.25

R2 = 31%

NPV2 = (0.79)

IRR = 12 + [(61.25 / (61.25+0.79) x (31-12)]

IRR = 30.76%

Conclusion: Cost of Capital more than 25.22% will turn NPV negative and less than 25.22% will

show a NPV positive.

c) If the cost of capital increase to 20 % in year 5, then does the changes would be advisable.

Period For Project

A

Cash Flow

(£m)

Cost of Capital

31%

Present value

(£m)

0 -150 1 -150

1 40 0.893 35.72

2 50 0.797 39.85

3 60 0.712 42.72

4 60 0.636 38.16

5 80 0.833 66.67

NPV 73.12

Period For Project

B

Cash Flow

(£m)

Cost of Capital

31%

Present value

(£m)

0 -152 1 -152

1 80 0.893 71.44

2 80 0.797 63.76

3 50 0.712 35.6

4 40 0.636 25.44

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

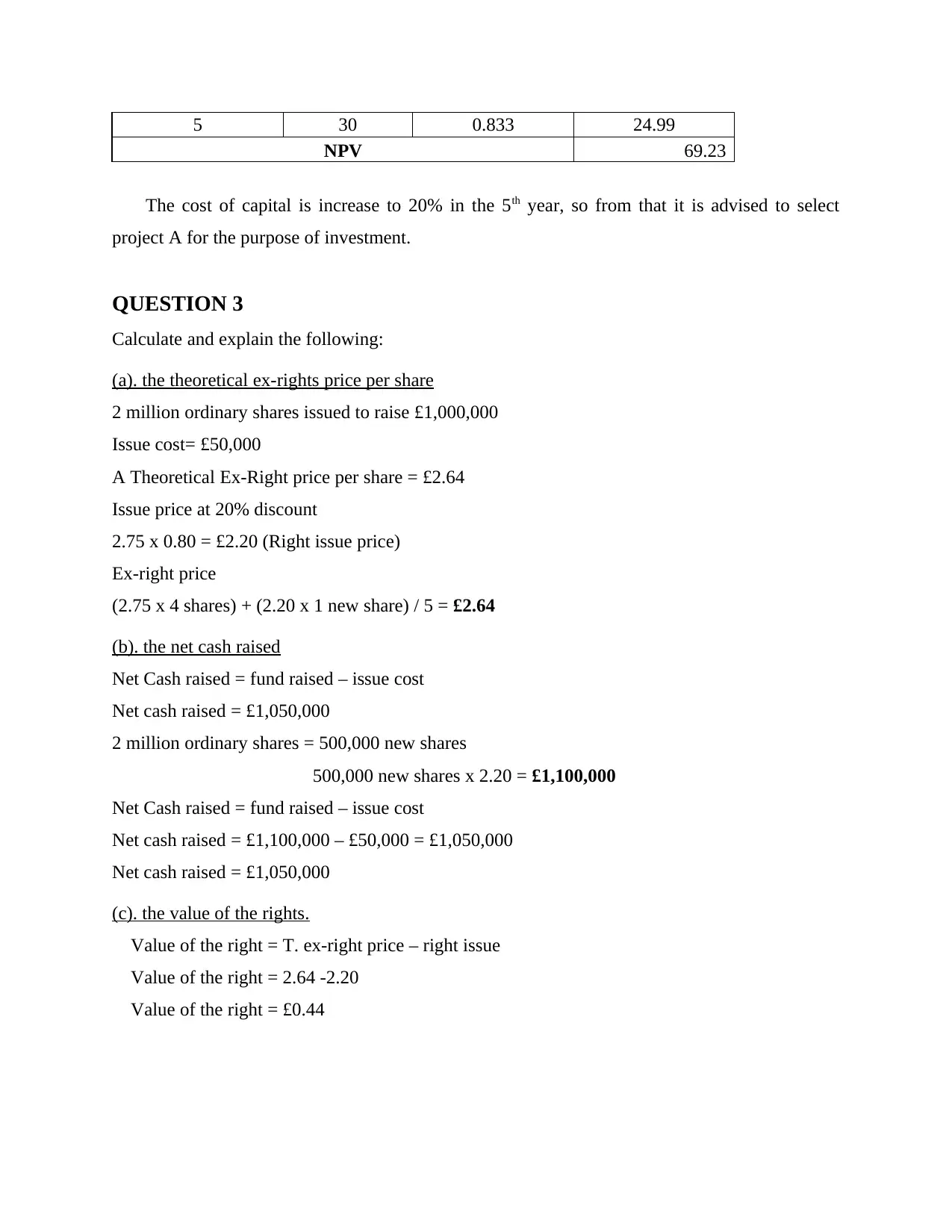

5 30 0.833 24.99

NPV 69.23

The cost of capital is increase to 20% in the 5th year, so from that it is advised to select

project A for the purpose of investment.

QUESTION 3

Calculate and explain the following:

(a). the theoretical ex-rights price per share

2 million ordinary shares issued to raise £1,000,000

Issue cost= £50,000

A Theoretical Ex-Right price per share = £2.64

Issue price at 20% discount

2.75 x 0.80 = £2.20 (Right issue price)

Ex-right price

(2.75 x 4 shares) + (2.20 x 1 new share) / 5 = £2.64

(b). the net cash raised

Net Cash raised = fund raised – issue cost

Net cash raised = £1,050,000

2 million ordinary shares = 500,000 new shares

500,000 new shares x 2.20 = £1,100,000

Net Cash raised = fund raised – issue cost

Net cash raised = £1,100,000 – £50,000 = £1,050,000

Net cash raised = £1,050,000

(c). the value of the rights.

Value of the right = T. ex-right price – right issue

Value of the right = 2.64 -2.20

Value of the right = £0.44

NPV 69.23

The cost of capital is increase to 20% in the 5th year, so from that it is advised to select

project A for the purpose of investment.

QUESTION 3

Calculate and explain the following:

(a). the theoretical ex-rights price per share

2 million ordinary shares issued to raise £1,000,000

Issue cost= £50,000

A Theoretical Ex-Right price per share = £2.64

Issue price at 20% discount

2.75 x 0.80 = £2.20 (Right issue price)

Ex-right price

(2.75 x 4 shares) + (2.20 x 1 new share) / 5 = £2.64

(b). the net cash raised

Net Cash raised = fund raised – issue cost

Net cash raised = £1,050,000

2 million ordinary shares = 500,000 new shares

500,000 new shares x 2.20 = £1,100,000

Net Cash raised = fund raised – issue cost

Net cash raised = £1,100,000 – £50,000 = £1,050,000

Net cash raised = £1,050,000

(c). the value of the rights.

Value of the right = T. ex-right price – right issue

Value of the right = 2.64 -2.20

Value of the right = £0.44

d) Pros and cons of right issue.

Existing investors of the company are welcome to purchase additional offers through the rights

issue. Current investors would have the safety net if there was an option to buy additional

apartments at a lower price than opponents. Hanging Valley Plc needs financial help, so they

provide basic stock to enable them to efficiently set up processes or fulfill obligations. There are

benefits and burdens of reviewing rights issues such as:

Advantages:

The quickest strategy to improve capital is to issue equity: since it is a freer element than

public donations, there are fewer rules and guidelines for equity. The main strategy for a

proper issuance is that since the delivery of more units, the registered effort should

submit a transaction letter to SEBI and the transaction stage for public consideration and

approval.

Increase promoter equity: One of the most powerful claims of traditionalism is that it

urges businessmen to increase their holdings. Financial backers can pursue the "stop

investment portion" of the stock, thereby supporting their holdings.

Cons:

Raising revenue to a specific amount An undeniable disadvantage is that in an emergency

(IPO) mentality, an organization cannot get a specific amount. How much cash an

organization can raise

The value of each unit may be diminished When an organization issues a value

proposition to raise capital, the stake of current financial backers may be reduced. Real

estate finance backers face a tough time when the entry of investors leads to a reduction

in stock holdings.

QUESTION 5

a)

Shares’ Fair price

Dividends for the past 4 years = 13p, 14p, 17p and 18p

Rate Return = 14% = 0.14

Number of Years (n) = 4

Ordinary dividend per share = 20p

Existing investors of the company are welcome to purchase additional offers through the rights

issue. Current investors would have the safety net if there was an option to buy additional

apartments at a lower price than opponents. Hanging Valley Plc needs financial help, so they

provide basic stock to enable them to efficiently set up processes or fulfill obligations. There are

benefits and burdens of reviewing rights issues such as:

Advantages:

The quickest strategy to improve capital is to issue equity: since it is a freer element than

public donations, there are fewer rules and guidelines for equity. The main strategy for a

proper issuance is that since the delivery of more units, the registered effort should

submit a transaction letter to SEBI and the transaction stage for public consideration and

approval.

Increase promoter equity: One of the most powerful claims of traditionalism is that it

urges businessmen to increase their holdings. Financial backers can pursue the "stop

investment portion" of the stock, thereby supporting their holdings.

Cons:

Raising revenue to a specific amount An undeniable disadvantage is that in an emergency

(IPO) mentality, an organization cannot get a specific amount. How much cash an

organization can raise

The value of each unit may be diminished When an organization issues a value

proposition to raise capital, the stake of current financial backers may be reduced. Real

estate finance backers face a tough time when the entry of investors leads to a reduction

in stock holdings.

QUESTION 5

a)

Shares’ Fair price

Dividends for the past 4 years = 13p, 14p, 17p and 18p

Rate Return = 14% = 0.14

Number of Years (n) = 4

Ordinary dividend per share = 20p

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

13p x (1 + Growth ¿ ¿4 = 20p

(1 + Growth) = 4

√20/13

Growth = 1.1137 – 1

Growth = 0.1137

Growth = 11.37%

P = 20(1+0.1137)

0.14−0.1137 = 846.92p = £8.47

Fair price share is £8.47.

b)

Calculation of new price shares when the rate of returns changes to 15.4%

P = (20 (1 + 0.1137)) / (0.154 - 0.1137) = 552.70p = £ 5.53

c) Identify the drawbacks of using dividend growth model as part of valuing shares.

The truth of the venture capital world is that an organization's profits don't grow at a

specific rate between now and eternity. Some organizations have increased their profits in

the long run. Others may reduce their profits. Some even decided to kill them outright.

These activities are not part of the valuation cycle of the valuation model. This means

that the model is best suited for several organizations that reliably provide profit growth

rates each year.

While small-cap stocks are compared to large-cap stocks, it is smaller organizations that

perform better over the long term. Most private companies don't have this mindset to

deliver profits, which means this valuation model cannot be used to determine their

value. It has to be used for stocks that are really profitable. If financial backers focus only

on this particular model, they may pass up various opportunities to enhance their

portfolios.

CONCLUSION

It can be asserted from the above prepared report, it examines as which project plan would

be more beneficial and suitable for the organization named as Better plc. It would help to

(1 + Growth) = 4

√20/13

Growth = 1.1137 – 1

Growth = 0.1137

Growth = 11.37%

P = 20(1+0.1137)

0.14−0.1137 = 846.92p = £8.47

Fair price share is £8.47.

b)

Calculation of new price shares when the rate of returns changes to 15.4%

P = (20 (1 + 0.1137)) / (0.154 - 0.1137) = 552.70p = £ 5.53

c) Identify the drawbacks of using dividend growth model as part of valuing shares.

The truth of the venture capital world is that an organization's profits don't grow at a

specific rate between now and eternity. Some organizations have increased their profits in

the long run. Others may reduce their profits. Some even decided to kill them outright.

These activities are not part of the valuation cycle of the valuation model. This means

that the model is best suited for several organizations that reliably provide profit growth

rates each year.

While small-cap stocks are compared to large-cap stocks, it is smaller organizations that

perform better over the long term. Most private companies don't have this mindset to

deliver profits, which means this valuation model cannot be used to determine their

value. It has to be used for stocks that are really profitable. If financial backers focus only

on this particular model, they may pass up various opportunities to enhance their

portfolios.

CONCLUSION

It can be asserted from the above prepared report, it examines as which project plan would

be more beneficial and suitable for the organization named as Better plc. It would help to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

evaluate with the help of calculations carried out such as net present value and internal rate of

return. Furthermore, it recommends the business to alter in cost of capital in upcoming 5 years

would be more than 20%. In another step, it would determine the price per share, net cash and

value of rights of the hanging plc company with the benefits and limitations so right problem.

Finally, it would determine the new and fair price of the planet plc company and would search

the issue which is rising due to dividend growth model.

return. Furthermore, it recommends the business to alter in cost of capital in upcoming 5 years

would be more than 20%. In another step, it would determine the price per share, net cash and

value of rights of the hanging plc company with the benefits and limitations so right problem.

Finally, it would determine the new and fair price of the planet plc company and would search

the issue which is rising due to dividend growth model.

REFERENCES

Books and Journals

Alakaleek, W. and Cooper, S.Y., 2018. The female entrepreneur’s financial networks: accessing

finance for the emergence of technology-based firms in Jordan. Venture Capital, 20(2),

pp.137-157.

Alemany, L. and Andreoli, J.J., 2018. Entrepreneurial Finance. Cambridge University Press.

Bessière, V., Stephany, E. and Wirtz, P., 2018, March. Crowdfunding, business angels, and

venture capital: new funding trajectories for start-ups?. In 2nd Emerging Trends in

Entrepreneurial Finance Conference.

Gietzmann, M. and Wang, Y., 2020. Goodwill valuations certified by independent experts:

Bigger and cleaner impairments?. Journal of Business Finance & Accounting, 47(1-2),

pp.27-51.

Hui, H.W., Manaf, A.W.A. and Shakri, A.K., 2019. Fintech and the transformation of the Islamic

finance regulatory framework in Malaysia. In Emerging issues in Islamic finance law

and practice in Malaysia. Emerald Publishing Limited.

Kuhn, B.M., 2022. Sustainable finance in Germany: mapping discourses, stakeholders, and

policy initiatives. Journal of Sustainable Finance & Investment, 12(2), pp.497-524.

Liu, X., 2020. A visualization analysis on researches of internet finance credit risk in coastal

area. Journal of Coastal Research, 103(SI), pp.85-89.

Shen, D. and Chen, S.H., 2018. Big data finance and financial markets. In Big Data in

Computational Social Science and Humanities (pp. 235-248). Springer, Cham.

Tian, X. and et.al., 2020. Rural finance, scale management and rural industrial integration. China

Agricultural Economic Review.

Youssef, J.A., 2021. Investigating consumer finance in Lebanon: an empirical study of ATM and

virtual currency. In Impact of Globalization and Advanced Technologies on Online

Business Models (pp. 32-54). IGI Global.

Books and Journals

Alakaleek, W. and Cooper, S.Y., 2018. The female entrepreneur’s financial networks: accessing

finance for the emergence of technology-based firms in Jordan. Venture Capital, 20(2),

pp.137-157.

Alemany, L. and Andreoli, J.J., 2018. Entrepreneurial Finance. Cambridge University Press.

Bessière, V., Stephany, E. and Wirtz, P., 2018, March. Crowdfunding, business angels, and

venture capital: new funding trajectories for start-ups?. In 2nd Emerging Trends in

Entrepreneurial Finance Conference.

Gietzmann, M. and Wang, Y., 2020. Goodwill valuations certified by independent experts:

Bigger and cleaner impairments?. Journal of Business Finance & Accounting, 47(1-2),

pp.27-51.

Hui, H.W., Manaf, A.W.A. and Shakri, A.K., 2019. Fintech and the transformation of the Islamic

finance regulatory framework in Malaysia. In Emerging issues in Islamic finance law

and practice in Malaysia. Emerald Publishing Limited.

Kuhn, B.M., 2022. Sustainable finance in Germany: mapping discourses, stakeholders, and

policy initiatives. Journal of Sustainable Finance & Investment, 12(2), pp.497-524.

Liu, X., 2020. A visualization analysis on researches of internet finance credit risk in coastal

area. Journal of Coastal Research, 103(SI), pp.85-89.

Shen, D. and Chen, S.H., 2018. Big data finance and financial markets. In Big Data in

Computational Social Science and Humanities (pp. 235-248). Springer, Cham.

Tian, X. and et.al., 2020. Rural finance, scale management and rural industrial integration. China

Agricultural Economic Review.

Youssef, J.A., 2021. Investigating consumer finance in Lebanon: an empirical study of ATM and

virtual currency. In Impact of Globalization and Advanced Technologies on Online

Business Models (pp. 32-54). IGI Global.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.