Business Finance Report: Profitability, Cash Flow, and Ratio Analysis

VerifiedAdded on 2020/10/23

|11

|3649

|74

Report

AI Summary

This report delves into the core concepts of business finance, focusing on profit, cash flow, and working capital management. It begins by defining profit and cash flow, highlighting their differences, and then examines working capital components like inventory, receivables, and payables. The report assesses how changes in working capital impact cash flow and analyzes the financial performance of UberTools Ltd. and Madagascar Industries Limited. It includes financial ratio calculations for each year, provides interpretations, and offers recommendations for financial performance improvement. The report also explores how companies can manage their financial results effectively, and proposes steps for improving cash flow through better working capital management, emphasizing the importance of budgeting, forecasting, and efficient debt collection.

BUSINESS FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

PART – 1.........................................................................................................................................1

1. Explaining:..............................................................................................................................1

a. Meaning of Profit and Cash flow and how they differs..........................................................1

b. Meaning of Working capital along with inventory, receivables and payable.........................2

c. Changes in working capital affect Cash flow. ........................................................................3

2. Company manage is affecting its financial results..................................................................3

3. Steps taken for improving the cash flow of company through better working capital ..........3

management................................................................................................................................3

PART – 2.........................................................................................................................................4

1. Explaining financial ratio........................................................................................................4

b. Calculating ratio of each year.................................................................................................6

c. Interpretation...........................................................................................................................7

2. Recommendations for financial performance improvement...................................................8

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................1

PART – 1.........................................................................................................................................1

1. Explaining:..............................................................................................................................1

a. Meaning of Profit and Cash flow and how they differs..........................................................1

b. Meaning of Working capital along with inventory, receivables and payable.........................2

c. Changes in working capital affect Cash flow. ........................................................................3

2. Company manage is affecting its financial results..................................................................3

3. Steps taken for improving the cash flow of company through better working capital ..........3

management................................................................................................................................3

PART – 2.........................................................................................................................................4

1. Explaining financial ratio........................................................................................................4

b. Calculating ratio of each year.................................................................................................6

c. Interpretation...........................................................................................................................7

2. Recommendations for financial performance improvement...................................................8

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

Business finance is a term which refers to cash, funds, money, capital and credit amount

employed in the business organization for carrying on any business operations. Business finance

is related to procurement and effective utilization of money or funds resources to carry out

business operations effectively and efficiently. The report will discuss about UberTools Ltd. And

Madagascar Industries Limited. UberTools Ltd. Is a company which is engaged in producing

power tools and is thinking of expanding its business to produce chainsaws. The report will

further discuss about the meaning of profit and cash flow and the way in which differs form each

other. Further, the report will discuss meaning of working capital along with inventory,

receivables and payables. The report will emphasize on assessing the impact of changes in

working capital on cash flow. It will also provide financial ratio calculation and how it is

interpreted. At last the report will discuss how financial performance of Madagascar Industries

Limited can be assessed and improved.

PART – 1

1. Explaining:

a. Meaning of Profit and Cash flow and how they differs.

Profit – The word profit is also known as Gaining. Profit is thus a defined as the

monetary or financial gain which is considered as the difference between the amount of money

earned and the expenses incurred. Profit is the income or gain which is earned from trade or

business activity remaining after total costs and expenses are deducted from the total sales

revenue of the business. It is used as a measure for assessing the success and growth of a

business organization (Reid and Myddelton, 2017).

Cash Flow -The term Cash flow is defined as the amount of cash, money, funds that is

moving in and out of a business organization. Thus, the term cash flow is the difference between

the amount of cash, funds available with the company at the beginning of a period and the

amount available at the end of a specified period (Reid and Myddelton, 2017). The cash flow

helps in preparation of cash flow statement which depicts about the cash uses by the operating,

investing and financing activities of the business organization for the specified period of time

(Reid and Myddelton, 2017).

1

Business finance is a term which refers to cash, funds, money, capital and credit amount

employed in the business organization for carrying on any business operations. Business finance

is related to procurement and effective utilization of money or funds resources to carry out

business operations effectively and efficiently. The report will discuss about UberTools Ltd. And

Madagascar Industries Limited. UberTools Ltd. Is a company which is engaged in producing

power tools and is thinking of expanding its business to produce chainsaws. The report will

further discuss about the meaning of profit and cash flow and the way in which differs form each

other. Further, the report will discuss meaning of working capital along with inventory,

receivables and payables. The report will emphasize on assessing the impact of changes in

working capital on cash flow. It will also provide financial ratio calculation and how it is

interpreted. At last the report will discuss how financial performance of Madagascar Industries

Limited can be assessed and improved.

PART – 1

1. Explaining:

a. Meaning of Profit and Cash flow and how they differs.

Profit – The word profit is also known as Gaining. Profit is thus a defined as the

monetary or financial gain which is considered as the difference between the amount of money

earned and the expenses incurred. Profit is the income or gain which is earned from trade or

business activity remaining after total costs and expenses are deducted from the total sales

revenue of the business. It is used as a measure for assessing the success and growth of a

business organization (Reid and Myddelton, 2017).

Cash Flow -The term Cash flow is defined as the amount of cash, money, funds that is

moving in and out of a business organization. Thus, the term cash flow is the difference between

the amount of cash, funds available with the company at the beginning of a period and the

amount available at the end of a specified period (Reid and Myddelton, 2017). The cash flow

helps in preparation of cash flow statement which depicts about the cash uses by the operating,

investing and financing activities of the business organization for the specified period of time

(Reid and Myddelton, 2017).

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

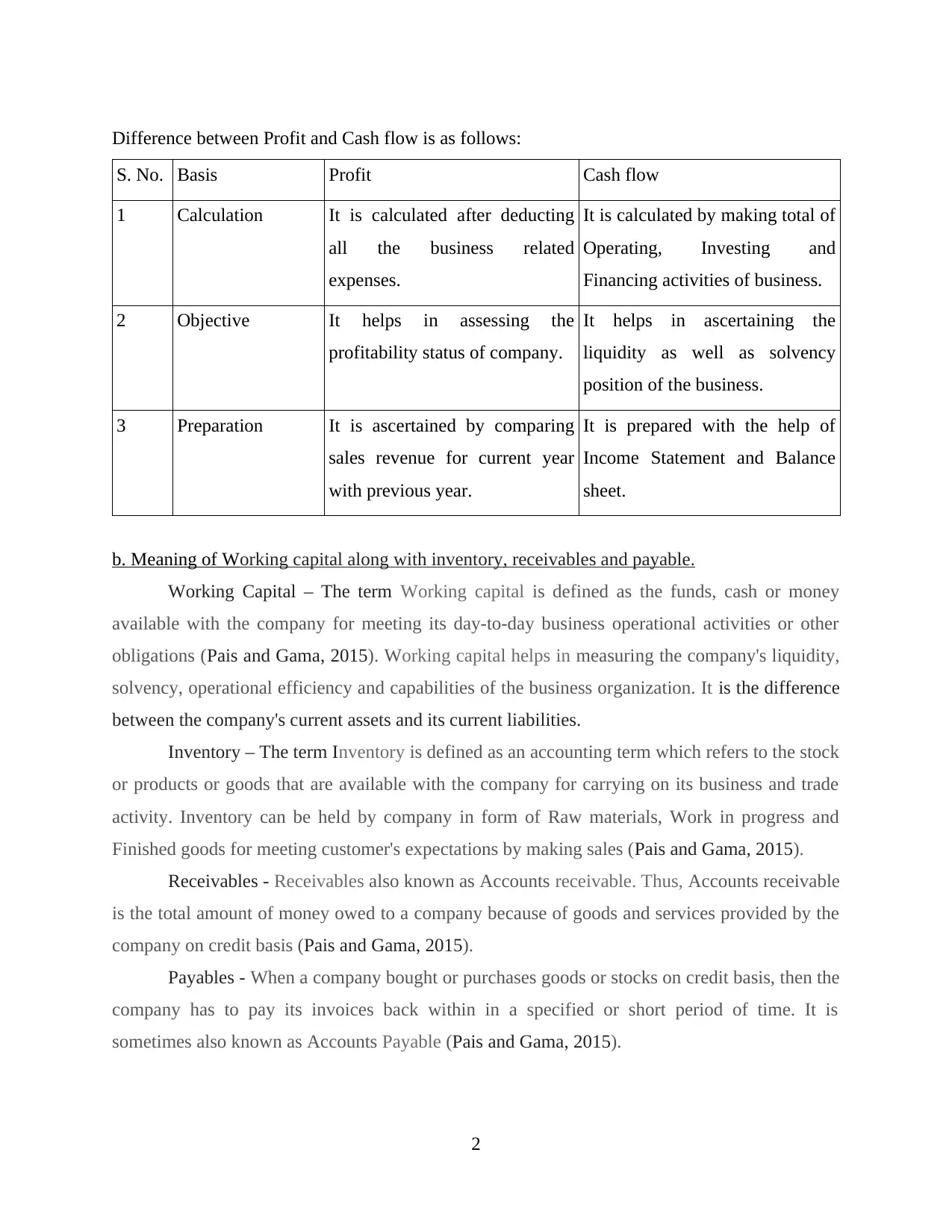

Difference between Profit and Cash flow is as follows:

S. No. Basis Profit Cash flow

1 Calculation It is calculated after deducting

all the business related

expenses.

It is calculated by making total of

Operating, Investing and

Financing activities of business.

2 Objective It helps in assessing the

profitability status of company.

It helps in ascertaining the

liquidity as well as solvency

position of the business.

3 Preparation It is ascertained by comparing

sales revenue for current year

with previous year.

It is prepared with the help of

Income Statement and Balance

sheet.

b. Meaning of Working capital along with inventory, receivables and payable.

Working Capital – The term Working capital is defined as the funds, cash or money

available with the company for meeting its day-to-day business operational activities or other

obligations (Pais and Gama, 2015). Working capital helps in measuring the company's liquidity,

solvency, operational efficiency and capabilities of the business organization. It is the difference

between the company's current assets and its current liabilities.

Inventory – The term Inventory is defined as an accounting term which refers to the stock

or products or goods that are available with the company for carrying on its business and trade

activity. Inventory can be held by company in form of Raw materials, Work in progress and

Finished goods for meeting customer's expectations by making sales (Pais and Gama, 2015).

Receivables - Receivables also known as Accounts receivable. Thus, Accounts receivable

is the total amount of money owed to a company because of goods and services provided by the

company on credit basis (Pais and Gama, 2015).

Payables - When a company bought or purchases goods or stocks on credit basis, then the

company has to pay its invoices back within in a specified or short period of time. It is

sometimes also known as Accounts Payable (Pais and Gama, 2015).

2

S. No. Basis Profit Cash flow

1 Calculation It is calculated after deducting

all the business related

expenses.

It is calculated by making total of

Operating, Investing and

Financing activities of business.

2 Objective It helps in assessing the

profitability status of company.

It helps in ascertaining the

liquidity as well as solvency

position of the business.

3 Preparation It is ascertained by comparing

sales revenue for current year

with previous year.

It is prepared with the help of

Income Statement and Balance

sheet.

b. Meaning of Working capital along with inventory, receivables and payable.

Working Capital – The term Working capital is defined as the funds, cash or money

available with the company for meeting its day-to-day business operational activities or other

obligations (Pais and Gama, 2015). Working capital helps in measuring the company's liquidity,

solvency, operational efficiency and capabilities of the business organization. It is the difference

between the company's current assets and its current liabilities.

Inventory – The term Inventory is defined as an accounting term which refers to the stock

or products or goods that are available with the company for carrying on its business and trade

activity. Inventory can be held by company in form of Raw materials, Work in progress and

Finished goods for meeting customer's expectations by making sales (Pais and Gama, 2015).

Receivables - Receivables also known as Accounts receivable. Thus, Accounts receivable

is the total amount of money owed to a company because of goods and services provided by the

company on credit basis (Pais and Gama, 2015).

Payables - When a company bought or purchases goods or stocks on credit basis, then the

company has to pay its invoices back within in a specified or short period of time. It is

sometimes also known as Accounts Payable (Pais and Gama, 2015).

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

c. Changes in working capital affect Cash flow.

Working Capital is defined as the net amount of funds, cash or money which is available

with the company to meet or for paying its short-term expenses related to business operations

(Pais and Gama, 2015).

Cash flow depicts the movement of cash and funds in and out of the business organization for a

specified period of time.

Changes in working capital affect Cash flow in following way:

1. The positive working capital is a situation when the company is having current assets more

than current liabilities which depicts that the company is financially sound and strong as a result

it will bring Positive impact on cash flow (Pais and Gama, 2015). It indicates that the liquid

assets of company are increasing enabling it to cover its short-term liabilities, pay expenses and

provide a good return to its shareholders.

2. Negative working capital means the current liabilities exceeds the current assets of the

company. It can be due to company having a large cash payment related to purchase of products

from its suppliers, vendors. It indicates company has to struggle for making payment and also

has negative cash flow because of low profit generation (Pais and Gama, 2015).

2. Company manage is affecting its financial results.

In case of UberTolos Ltd. The company is producing power tools and is thinking of

expanding its business in new product development i.e. chainsaws for which it has acquired a 3

year license and has make an investment of £20 million with an advance fees of £18 million to

design company. Here the company after making payment and investment, is not able to generate

gain or return on capital employed.

Also, the inventory management of the company is not effectively managed. The

company should adopt good inventory valuation method for valuing its inventory and assessing

the level of stock held by company (Pais and Gama, 2015).

3. Steps taken for improving the cash flow of company through better working capital

management.

The company should adopt following measures for improving the cash flow of company

through better working capital management:

3

Working Capital is defined as the net amount of funds, cash or money which is available

with the company to meet or for paying its short-term expenses related to business operations

(Pais and Gama, 2015).

Cash flow depicts the movement of cash and funds in and out of the business organization for a

specified period of time.

Changes in working capital affect Cash flow in following way:

1. The positive working capital is a situation when the company is having current assets more

than current liabilities which depicts that the company is financially sound and strong as a result

it will bring Positive impact on cash flow (Pais and Gama, 2015). It indicates that the liquid

assets of company are increasing enabling it to cover its short-term liabilities, pay expenses and

provide a good return to its shareholders.

2. Negative working capital means the current liabilities exceeds the current assets of the

company. It can be due to company having a large cash payment related to purchase of products

from its suppliers, vendors. It indicates company has to struggle for making payment and also

has negative cash flow because of low profit generation (Pais and Gama, 2015).

2. Company manage is affecting its financial results.

In case of UberTolos Ltd. The company is producing power tools and is thinking of

expanding its business in new product development i.e. chainsaws for which it has acquired a 3

year license and has make an investment of £20 million with an advance fees of £18 million to

design company. Here the company after making payment and investment, is not able to generate

gain or return on capital employed.

Also, the inventory management of the company is not effectively managed. The

company should adopt good inventory valuation method for valuing its inventory and assessing

the level of stock held by company (Pais and Gama, 2015).

3. Steps taken for improving the cash flow of company through better working capital

management.

The company should adopt following measures for improving the cash flow of company

through better working capital management:

3

1. Perform Budgeting and Forecasting function – The company should always prepare a

budget or forecasting function by making strong business strategies and plans for meeting

future business operations.

2. Debtors collection period – The company should focus on the efficient, effective and

timely collection of customer debts to remain liquid and solvent. It should focus on

decreasing the debtors' collection period by getting easy collection of money due form its

customers (Pais and Gama, 2015).

3. Payable period – The company should always emphasizes on increasing the payable

period so as to keep cash or cash-equivalents with itself for meeting day-to-day expenses

(Pais and Gama, 2015).

PART – 2

1. Explaining financial ratio.

1. Sales growth – The term Sales growth is defined as a measure which defines the ability of

company and its employee to increase sales of its product and services over a fixed

period of time. It is defined as the amount of sales increased in terms of revenue as

compared to a previous year. Sales growth is always considered as a positive factor for

every business organization as it depicts the company's survival and profitability.

Because of sales growth it has impact on increase in dividends for shareholders & high

share price (Lakshan and Wijekoon, 2017).

2. Gross profit margin – The Gross profit margin helps in evaluating the company's

financial performance, position as well as health. It is calculated as the amount of money

remaining after making all deduction related to the cost of production & cost of goods

sold. It is the profit amount which is left after meeting all business and cost expenses

(Lakshan and Wijekoon, 2017).

3. Operating profit margin – The Operating profit margin defines the way of measuring the

company's profitability position. It indicates that how much revenue amount is left after

making all the expenses related to costs of goods sold and operation of business. The

operating profit margin is thus that amount of revenue which a business earns by

conducting its business related operating activities (Lakshan and Wijekoon, 2017).

4

budget or forecasting function by making strong business strategies and plans for meeting

future business operations.

2. Debtors collection period – The company should focus on the efficient, effective and

timely collection of customer debts to remain liquid and solvent. It should focus on

decreasing the debtors' collection period by getting easy collection of money due form its

customers (Pais and Gama, 2015).

3. Payable period – The company should always emphasizes on increasing the payable

period so as to keep cash or cash-equivalents with itself for meeting day-to-day expenses

(Pais and Gama, 2015).

PART – 2

1. Explaining financial ratio.

1. Sales growth – The term Sales growth is defined as a measure which defines the ability of

company and its employee to increase sales of its product and services over a fixed

period of time. It is defined as the amount of sales increased in terms of revenue as

compared to a previous year. Sales growth is always considered as a positive factor for

every business organization as it depicts the company's survival and profitability.

Because of sales growth it has impact on increase in dividends for shareholders & high

share price (Lakshan and Wijekoon, 2017).

2. Gross profit margin – The Gross profit margin helps in evaluating the company's

financial performance, position as well as health. It is calculated as the amount of money

remaining after making all deduction related to the cost of production & cost of goods

sold. It is the profit amount which is left after meeting all business and cost expenses

(Lakshan and Wijekoon, 2017).

3. Operating profit margin – The Operating profit margin defines the way of measuring the

company's profitability position. It indicates that how much revenue amount is left after

making all the expenses related to costs of goods sold and operation of business. The

operating profit margin is thus that amount of revenue which a business earns by

conducting its business related operating activities (Lakshan and Wijekoon, 2017).

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4. Gearing - Gearing is used to measure the level of financial leverage a company has

employed into its business organization. It also represents the funding amount as

contributed by the lenders in comparison with funds contributed by shareholders. It is a

fundamental analysis ratio of a firm's level of long-term debt as compared to its equity

capital. Gearing ratio measures the extent by which it can be assess how much business is

funded by equity capital in comparison with debt funds (Lakshan and Wijekoon, 2017).

5. Interest coverage ratio- The interest coverage ratio helps in determining that how easily

the company's ability to pay its interest related expenses arises because of the outstanding

debt with the available earnings of business. The interest coverage ratio is type of

financial ratio which measures the company's ability in meeting it expenses related to

interest payments on time (Lakshan and Wijekoon, 2017).

6. Liquidity ratio – The word Liquidity describes the extent of a company by which the

current assets can be easily bought from the market or converted into cash without having

any impact on the price of asset. The liquidity factor measures the ability of every

company that how it will meet the short term financial obligations or other obligation due

within one year with the amount of liquid assets available (Lakshan and Wijekoon,

2017).

7. Return on equity – The word Return on Equity basically means the normal rate of return

that the shareholders or other stakeholders holding company's shares or stock receives on

the part of their shareholdings. A Return on Equity is a measure which assess the ability

of business organization in generating income or profit from the equity capital available

(Lakshan and Wijekoon, 2017).

8. Return on capital employed – It measures the company's operational efficiency and

profitability with the amount of capital employed. In simple meaning it measures that

how much a company is able to generate profit from capital invested (Lakshan and

Wijekoon, 2017).

b. Calculating ratio of each year.

Particulars Formula 2019 2020 2021

5

employed into its business organization. It also represents the funding amount as

contributed by the lenders in comparison with funds contributed by shareholders. It is a

fundamental analysis ratio of a firm's level of long-term debt as compared to its equity

capital. Gearing ratio measures the extent by which it can be assess how much business is

funded by equity capital in comparison with debt funds (Lakshan and Wijekoon, 2017).

5. Interest coverage ratio- The interest coverage ratio helps in determining that how easily

the company's ability to pay its interest related expenses arises because of the outstanding

debt with the available earnings of business. The interest coverage ratio is type of

financial ratio which measures the company's ability in meeting it expenses related to

interest payments on time (Lakshan and Wijekoon, 2017).

6. Liquidity ratio – The word Liquidity describes the extent of a company by which the

current assets can be easily bought from the market or converted into cash without having

any impact on the price of asset. The liquidity factor measures the ability of every

company that how it will meet the short term financial obligations or other obligation due

within one year with the amount of liquid assets available (Lakshan and Wijekoon,

2017).

7. Return on equity – The word Return on Equity basically means the normal rate of return

that the shareholders or other stakeholders holding company's shares or stock receives on

the part of their shareholdings. A Return on Equity is a measure which assess the ability

of business organization in generating income or profit from the equity capital available

(Lakshan and Wijekoon, 2017).

8. Return on capital employed – It measures the company's operational efficiency and

profitability with the amount of capital employed. In simple meaning it measures that

how much a company is able to generate profit from capital invested (Lakshan and

Wijekoon, 2017).

b. Calculating ratio of each year.

Particulars Formula 2019 2020 2021

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sales 360 396 459

Sales growth (Sales Y2- Sales Y1)/

Sales Y1 - 10% 15.91%

Gross profit 230 252 272

Sales 360 396 459

Gross profit margin Gross Profit/ Sales 63.89% 63.64% 59.26%

Operating profit 108 101 49

Sales 360 396 459

Operating profit

margin

Operating Profit/

Sales 30.00% 25.51% 10.68%

Total debt 29 48 102

Shareholders fund 304 347 344

Gearing

Total debt/ (Total

debt + shareholder

funds)

8.71% 12.15% 22.87%

Operating profit 108 101 49

Finance expenses 9 12 16

Interest coverage ratio Operating profit/

Finance expenses 12 8.42 3.06

Current assets 65 114 94

Current liabilities 29 48 102

Liquidity ratio Current assets/

Current Liabilities 2.24 2.38 0.92

Net Profit 79 72 26

6

Sales growth (Sales Y2- Sales Y1)/

Sales Y1 - 10% 15.91%

Gross profit 230 252 272

Sales 360 396 459

Gross profit margin Gross Profit/ Sales 63.89% 63.64% 59.26%

Operating profit 108 101 49

Sales 360 396 459

Operating profit

margin

Operating Profit/

Sales 30.00% 25.51% 10.68%

Total debt 29 48 102

Shareholders fund 304 347 344

Gearing

Total debt/ (Total

debt + shareholder

funds)

8.71% 12.15% 22.87%

Operating profit 108 101 49

Finance expenses 9 12 16

Interest coverage ratio Operating profit/

Finance expenses 12 8.42 3.06

Current assets 65 114 94

Current liabilities 29 48 102

Liquidity ratio Current assets/

Current Liabilities 2.24 2.38 0.92

Net Profit 79 72 26

6

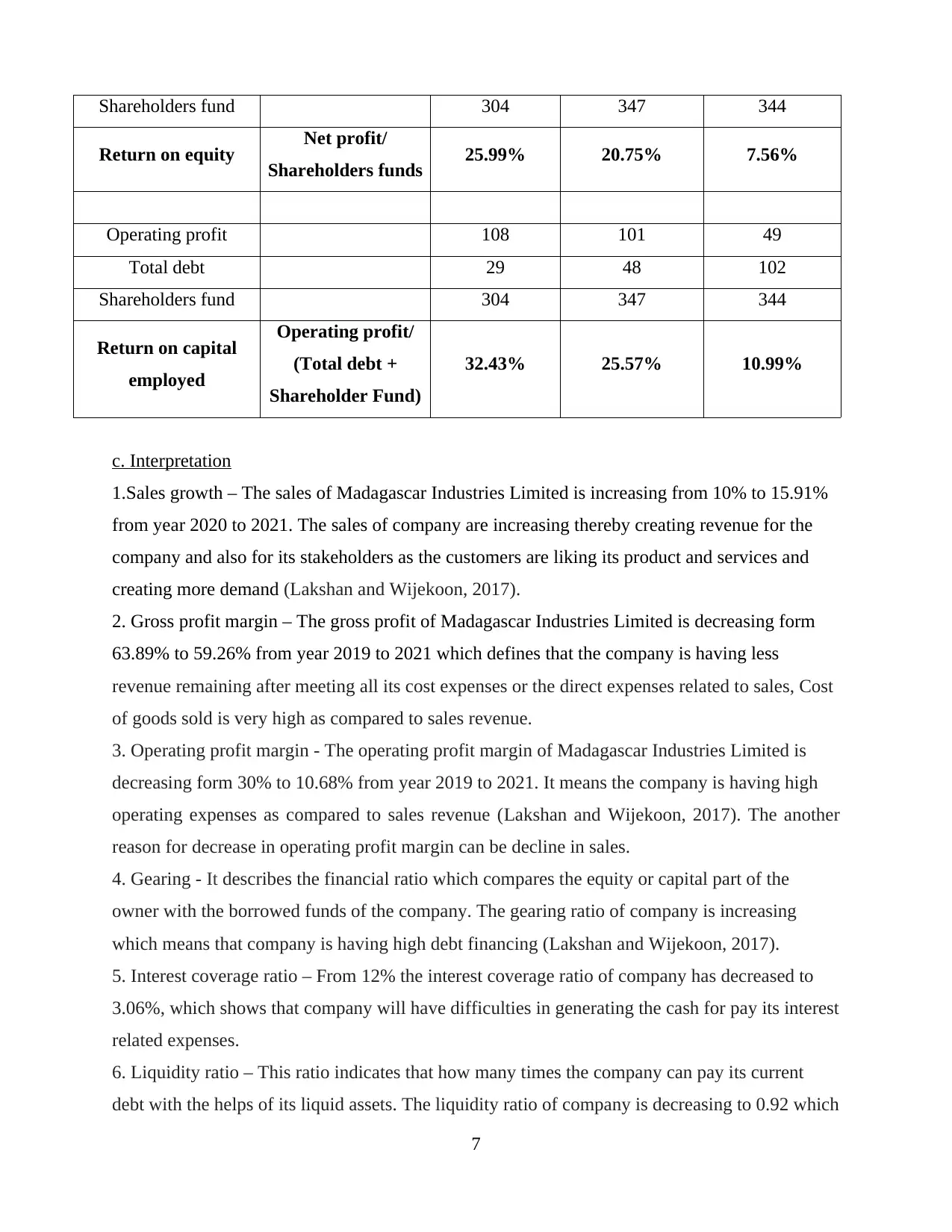

Shareholders fund 304 347 344

Return on equity Net profit/

Shareholders funds 25.99% 20.75% 7.56%

Operating profit 108 101 49

Total debt 29 48 102

Shareholders fund 304 347 344

Return on capital

employed

Operating profit/

(Total debt +

Shareholder Fund)

32.43% 25.57% 10.99%

c. Interpretation

1.Sales growth – The sales of Madagascar Industries Limited is increasing from 10% to 15.91%

from year 2020 to 2021. The sales of company are increasing thereby creating revenue for the

company and also for its stakeholders as the customers are liking its product and services and

creating more demand (Lakshan and Wijekoon, 2017).

2. Gross profit margin – The gross profit of Madagascar Industries Limited is decreasing form

63.89% to 59.26% from year 2019 to 2021 which defines that the company is having less

revenue remaining after meeting all its cost expenses or the direct expenses related to sales, Cost

of goods sold is very high as compared to sales revenue.

3. Operating profit margin - The operating profit margin of Madagascar Industries Limited is

decreasing form 30% to 10.68% from year 2019 to 2021. It means the company is having high

operating expenses as compared to sales revenue (Lakshan and Wijekoon, 2017). The another

reason for decrease in operating profit margin can be decline in sales.

4. Gearing - It describes the financial ratio which compares the equity or capital part of the

owner with the borrowed funds of the company. The gearing ratio of company is increasing

which means that company is having high debt financing (Lakshan and Wijekoon, 2017).

5. Interest coverage ratio – From 12% the interest coverage ratio of company has decreased to

3.06%, which shows that company will have difficulties in generating the cash for pay its interest

related expenses.

6. Liquidity ratio – This ratio indicates that how many times the company can pay its current

debt with the helps of its liquid assets. The liquidity ratio of company is decreasing to 0.92 which

7

Return on equity Net profit/

Shareholders funds 25.99% 20.75% 7.56%

Operating profit 108 101 49

Total debt 29 48 102

Shareholders fund 304 347 344

Return on capital

employed

Operating profit/

(Total debt +

Shareholder Fund)

32.43% 25.57% 10.99%

c. Interpretation

1.Sales growth – The sales of Madagascar Industries Limited is increasing from 10% to 15.91%

from year 2020 to 2021. The sales of company are increasing thereby creating revenue for the

company and also for its stakeholders as the customers are liking its product and services and

creating more demand (Lakshan and Wijekoon, 2017).

2. Gross profit margin – The gross profit of Madagascar Industries Limited is decreasing form

63.89% to 59.26% from year 2019 to 2021 which defines that the company is having less

revenue remaining after meeting all its cost expenses or the direct expenses related to sales, Cost

of goods sold is very high as compared to sales revenue.

3. Operating profit margin - The operating profit margin of Madagascar Industries Limited is

decreasing form 30% to 10.68% from year 2019 to 2021. It means the company is having high

operating expenses as compared to sales revenue (Lakshan and Wijekoon, 2017). The another

reason for decrease in operating profit margin can be decline in sales.

4. Gearing - It describes the financial ratio which compares the equity or capital part of the

owner with the borrowed funds of the company. The gearing ratio of company is increasing

which means that company is having high debt financing (Lakshan and Wijekoon, 2017).

5. Interest coverage ratio – From 12% the interest coverage ratio of company has decreased to

3.06%, which shows that company will have difficulties in generating the cash for pay its interest

related expenses.

6. Liquidity ratio – This ratio indicates that how many times the company can pay its current

debt with the helps of its liquid assets. The liquidity ratio of company is decreasing to 0.92 which

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

has to be improved to above 1, so that it don't have to sell assets for meeting its short-term debt

expenses (Lakshan and Wijekoon, 2017).

7. Return on equity – The ratio of return on equity is decreasing from 25.99% to 7.56%.

Decreasing return is because low profit generation because of low sales turnover.

8. Return on capital employed – The return is decreasing against which the company has to take

preventive measures for improving return on capital employed by reducing its cost expenses,

increasing sales and sales revenue (Lakshan and Wijekoon, 2017).

2. Recommendations for financial performance improvement.

1. Increase in Revenue – Madagascar Industries Limited should focus on increasing its sales

thereby increasing the sales revenue (Epstein, M.J., Buhovac, and et.al., 2015). The

company has to focus on improving the quality of its product, services as well as

performance of business operations.

2. Debt Ratio remain low – The debt is considered as one of the most important aspect of

company. The company should maintain a mix of debt equity and should be financial

leveraged (Epstein, M.J., Buhovac, and et.al., 2015).

3. Profitability ratio – The company should always focus on maximization of profit and

customer satisfaction along with minimum cost of production. The company should

always emphasize on increasing profit with better quality product.

4. Current ratio & liquidity – The company should have more current as well as liquid

assets in comparison with the current liabilities (Epstein, M.J., Buhovac, and et.al., 2015).

It helps in assessing the liquidity and solvency position of the company.

5. Operating expenses – The term expense related to cost incurred for carrying on any

business or trade activity. Every company should focus on minimizing its cost expenses

related to business operation and cost of goods sold (Epstein, M.J., Buhovac, and et.al.,

2015).

CONCLUSION

From the above report it can be concluded that finance is considered as important factor

for every business organization in carrying on any business operations. The report has discussed

about the concept of profit and cash flow statement. It has also provided the comparison between

profit and cash flow. The report has also discussed the importance of working capital

8

expenses (Lakshan and Wijekoon, 2017).

7. Return on equity – The ratio of return on equity is decreasing from 25.99% to 7.56%.

Decreasing return is because low profit generation because of low sales turnover.

8. Return on capital employed – The return is decreasing against which the company has to take

preventive measures for improving return on capital employed by reducing its cost expenses,

increasing sales and sales revenue (Lakshan and Wijekoon, 2017).

2. Recommendations for financial performance improvement.

1. Increase in Revenue – Madagascar Industries Limited should focus on increasing its sales

thereby increasing the sales revenue (Epstein, M.J., Buhovac, and et.al., 2015). The

company has to focus on improving the quality of its product, services as well as

performance of business operations.

2. Debt Ratio remain low – The debt is considered as one of the most important aspect of

company. The company should maintain a mix of debt equity and should be financial

leveraged (Epstein, M.J., Buhovac, and et.al., 2015).

3. Profitability ratio – The company should always focus on maximization of profit and

customer satisfaction along with minimum cost of production. The company should

always emphasize on increasing profit with better quality product.

4. Current ratio & liquidity – The company should have more current as well as liquid

assets in comparison with the current liabilities (Epstein, M.J., Buhovac, and et.al., 2015).

It helps in assessing the liquidity and solvency position of the company.

5. Operating expenses – The term expense related to cost incurred for carrying on any

business or trade activity. Every company should focus on minimizing its cost expenses

related to business operation and cost of goods sold (Epstein, M.J., Buhovac, and et.al.,

2015).

CONCLUSION

From the above report it can be concluded that finance is considered as important factor

for every business organization in carrying on any business operations. The report has discussed

about the concept of profit and cash flow statement. It has also provided the comparison between

profit and cash flow. The report has also discussed the importance of working capital

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

management with inventory, accounts receivables and accounts payables meaning. This report

has provided that how any change in the business item of working capital has impact on cash

flow of the company. Furthermore, the report has provided calculation of financial ratios of

Madagascar Industries Limited along with its interpretation and meaning. Also, the report has

disclosed that how a company can manage and assess its financial performance with the help of

financial statement and financial ratios.

REFERENCES

Books and Journals

Epstein, M.J., Buhovac, and et.al., 2015. Managing social, environmental and financial

performance simultaneously. Long range planning. 48(1). pp.35-45.

Kraemer-Eis, H., Botsari, and et.al., 2018. European Small Business Finance Outlook: June

2018 (No. 2018/50). EIF Working Paper.

Lakshan, A.I. and Wijekoon, W.M.H.N., 2017. The use of financial ratios in predicting corporate

failure in Sri Lanka. GSTF Journal on Business Review (GBR). 2(4).

Mathuva, D., 2015. The Influence of working capital management components on corporate

profitability.

Pais, M.A. and Gama, P.M., 2015. Working capital management and SMEs profitability:

Portuguese evidence. International Journal of Managerial Finance. 11(3). pp.341-358.

Reid, W. and Myddelton, D.R., 2017. Cash flow statement. In The Meaning of Company

Accounts (pp. 16-16). Routledge.

Rodrigues, L. and Rodrigues, L., 2018. Economic-financial performance of the Brazilian

sugarcane energy industry: An empirical evaluation using financial ratio, cluster and

discriminant analysis. Biomass and bioenergy. 108. pp.289-296.

Shackle, G.L.S., 2017. Expectation, enterprise and profit: The theory of the firm. Routledge.

Stripling, E. and Baesens, B., 2018. Building profit-sensitive classifiers for maximum profit. In

European Conference on Operational Research (EURO 2018), Date: 2018/07/08-

2018/07/11, Location: Valencia (Spain).

Williams, E.E. and Dobelman, J.A., 2017. Financial statement analysis. World Scientific Book

Chapters. pp.109-169.

9

has provided that how any change in the business item of working capital has impact on cash

flow of the company. Furthermore, the report has provided calculation of financial ratios of

Madagascar Industries Limited along with its interpretation and meaning. Also, the report has

disclosed that how a company can manage and assess its financial performance with the help of

financial statement and financial ratios.

REFERENCES

Books and Journals

Epstein, M.J., Buhovac, and et.al., 2015. Managing social, environmental and financial

performance simultaneously. Long range planning. 48(1). pp.35-45.

Kraemer-Eis, H., Botsari, and et.al., 2018. European Small Business Finance Outlook: June

2018 (No. 2018/50). EIF Working Paper.

Lakshan, A.I. and Wijekoon, W.M.H.N., 2017. The use of financial ratios in predicting corporate

failure in Sri Lanka. GSTF Journal on Business Review (GBR). 2(4).

Mathuva, D., 2015. The Influence of working capital management components on corporate

profitability.

Pais, M.A. and Gama, P.M., 2015. Working capital management and SMEs profitability:

Portuguese evidence. International Journal of Managerial Finance. 11(3). pp.341-358.

Reid, W. and Myddelton, D.R., 2017. Cash flow statement. In The Meaning of Company

Accounts (pp. 16-16). Routledge.

Rodrigues, L. and Rodrigues, L., 2018. Economic-financial performance of the Brazilian

sugarcane energy industry: An empirical evaluation using financial ratio, cluster and

discriminant analysis. Biomass and bioenergy. 108. pp.289-296.

Shackle, G.L.S., 2017. Expectation, enterprise and profit: The theory of the firm. Routledge.

Stripling, E. and Baesens, B., 2018. Building profit-sensitive classifiers for maximum profit. In

European Conference on Operational Research (EURO 2018), Date: 2018/07/08-

2018/07/11, Location: Valencia (Spain).

Williams, E.E. and Dobelman, J.A., 2017. Financial statement analysis. World Scientific Book

Chapters. pp.109-169.

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.