Business Finance: Cash Budget, Accounting Equation and Stakeholders

VerifiedAdded on 2023/06/17

|13

|3320

|366

Report

AI Summary

This report delves into business finance, beginning with a practical cash budget example spanning January to March, demonstrating favorable ending balances and highlighting the importance of cash flow management. It explains the fundamental accounting equation (Assets = Liabilities + Equity) and its balancing nature through double-entry bookkeeping, using examples to illustrate its application. Furthermore, the report outlines the benefits a company like Marks and Spencer can gain from listing its shares on the stock exchange, including increased access to capital, enhanced visibility, and improved liquidity. Finally, it identifies and discusses the various stakeholders in a large listed company, differentiating between internal (employees, managers) and external stakeholders (customers, suppliers, investors) and emphasizing their roles in ensuring effective corporate governance. Desklib offers this and many more solved assignments for students.

Business Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................................3

TASK 1..........................................................................................................................................................3

Cash budget for the business..................................................................................................................3

TASK 2..........................................................................................................................................................5

2.1 Explaining accounting equation and reason for its always balancing with example.........................5

2.2 Benefits which company can gain by having its shares listed on stock exchange..............................7

2.3 Stakeholders in large listed company like Marks and Spencer..........................................................8

2.4 Profit as a reliable indicator of cash balance and difference within profit and cash..........................9

CONCLUSION.............................................................................................................................................11

REFERENCES..............................................................................................................................................11

INTRODUCTION...........................................................................................................................................3

TASK 1..........................................................................................................................................................3

Cash budget for the business..................................................................................................................3

TASK 2..........................................................................................................................................................5

2.1 Explaining accounting equation and reason for its always balancing with example.........................5

2.2 Benefits which company can gain by having its shares listed on stock exchange..............................7

2.3 Stakeholders in large listed company like Marks and Spencer..........................................................8

2.4 Profit as a reliable indicator of cash balance and difference within profit and cash..........................9

CONCLUSION.............................................................................................................................................11

REFERENCES..............................................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

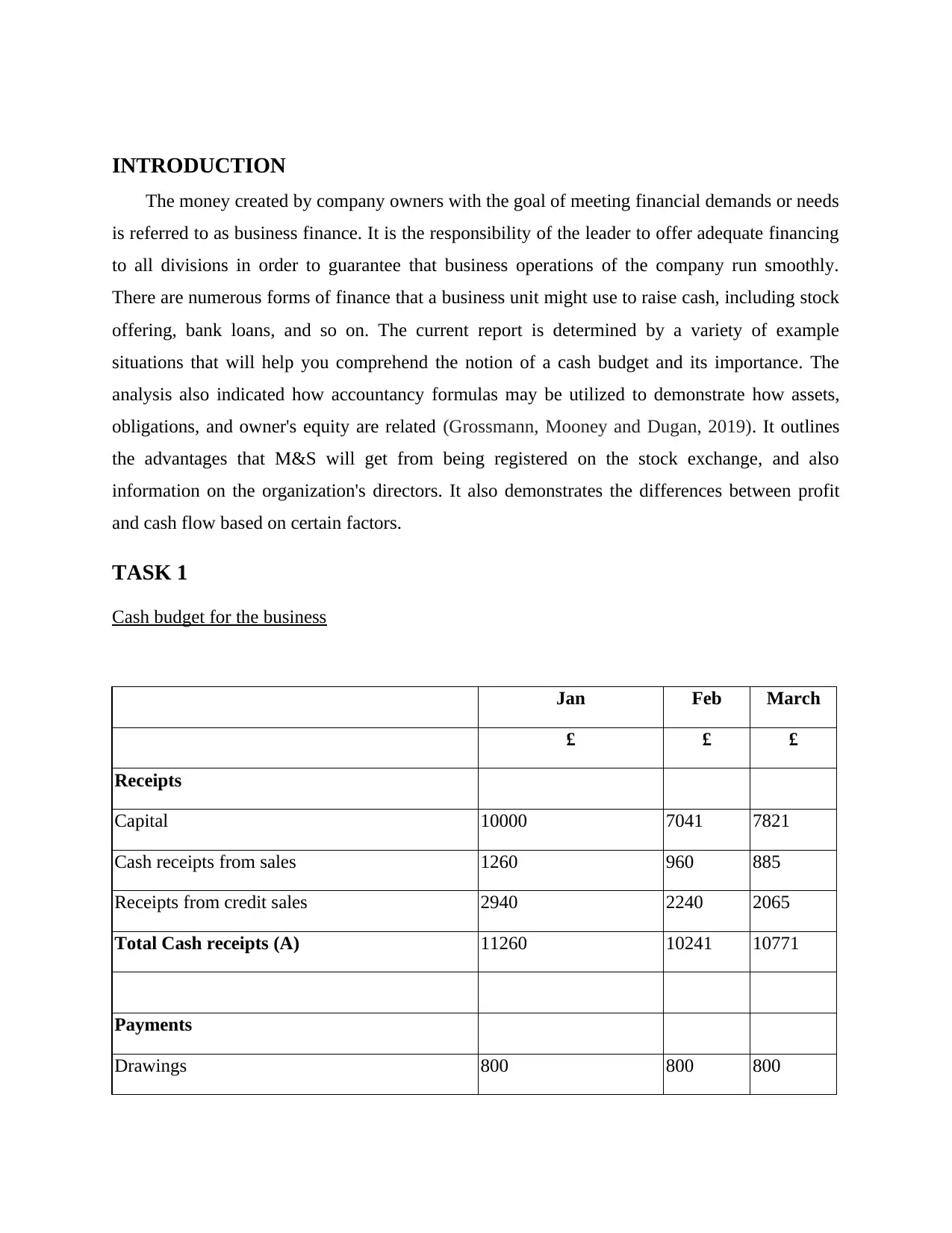

INTRODUCTION

The money created by company owners with the goal of meeting financial demands or needs

is referred to as business finance. It is the responsibility of the leader to offer adequate financing

to all divisions in order to guarantee that business operations of the company run smoothly.

There are numerous forms of finance that a business unit might use to raise cash, including stock

offering, bank loans, and so on. The current report is determined by a variety of example

situations that will help you comprehend the notion of a cash budget and its importance. The

analysis also indicated how accountancy formulas may be utilized to demonstrate how assets,

obligations, and owner's equity are related (Grossmann, Mooney and Dugan, 2019). It outlines

the advantages that M&S will get from being registered on the stock exchange, and also

information on the organization's directors. It also demonstrates the differences between profit

and cash flow based on certain factors.

TASK 1

Cash budget for the business

Jan Feb March

£ £ £

Receipts

Capital 10000 7041 7821

Cash receipts from sales 1260 960 885

Receipts from credit sales 2940 2240 2065

Total Cash receipts (A) 11260 10241 10771

Payments

Drawings 800 800 800

The money created by company owners with the goal of meeting financial demands or needs

is referred to as business finance. It is the responsibility of the leader to offer adequate financing

to all divisions in order to guarantee that business operations of the company run smoothly.

There are numerous forms of finance that a business unit might use to raise cash, including stock

offering, bank loans, and so on. The current report is determined by a variety of example

situations that will help you comprehend the notion of a cash budget and its importance. The

analysis also indicated how accountancy formulas may be utilized to demonstrate how assets,

obligations, and owner's equity are related (Grossmann, Mooney and Dugan, 2019). It outlines

the advantages that M&S will get from being registered on the stock exchange, and also

information on the organization's directors. It also demonstrates the differences between profit

and cash flow based on certain factors.

TASK 1

Cash budget for the business

Jan Feb March

£ £ £

Receipts

Capital 10000 7041 7821

Cash receipts from sales 1260 960 885

Receipts from credit sales 2940 2240 2065

Total Cash receipts (A) 11260 10241 10771

Payments

Drawings 800 800 800

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

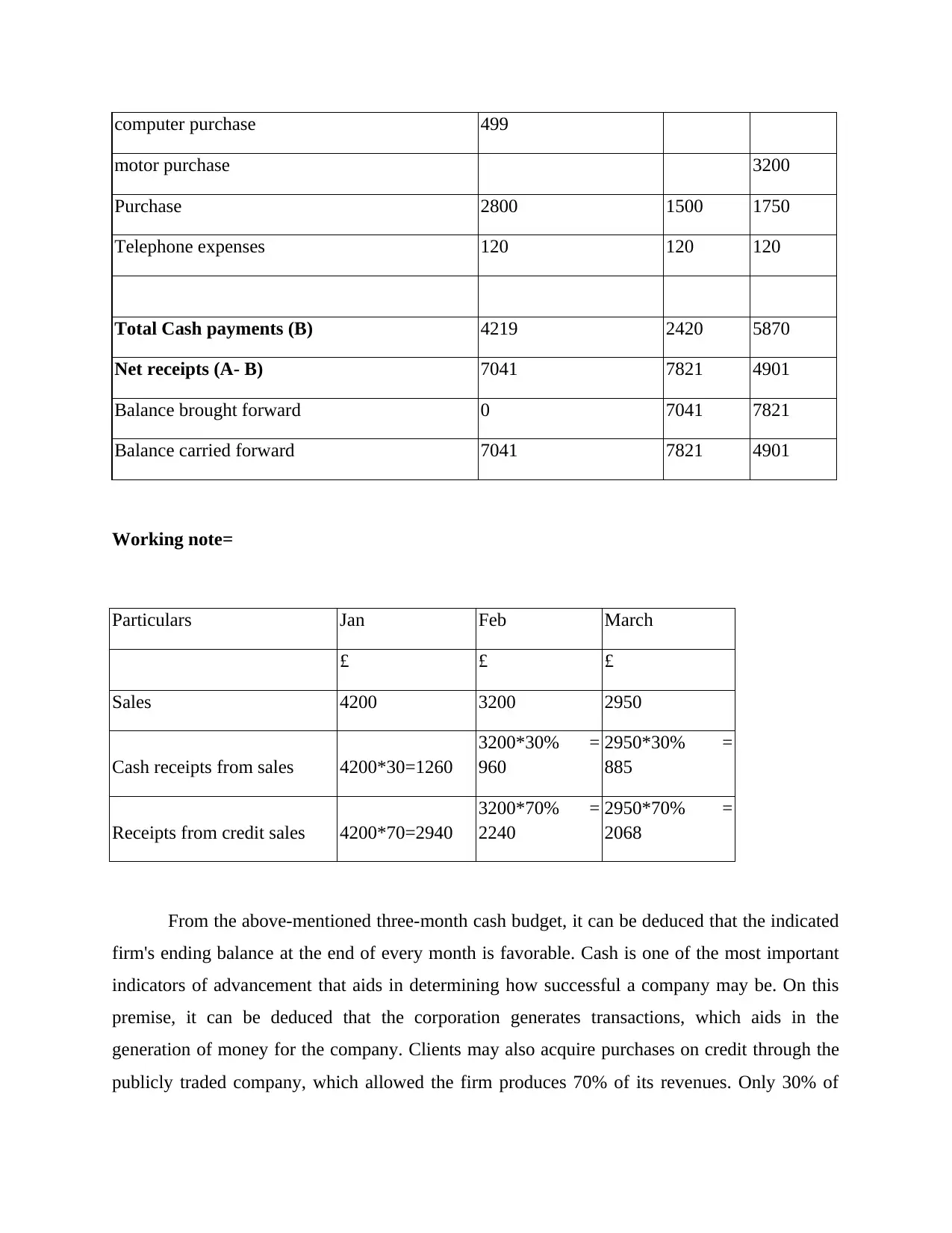

computer purchase 499

motor purchase 3200

Purchase 2800 1500 1750

Telephone expenses 120 120 120

Total Cash payments (B) 4219 2420 5870

Net receipts (A- B) 7041 7821 4901

Balance brought forward 0 7041 7821

Balance carried forward 7041 7821 4901

Working note=

Particulars Jan Feb March

£ £ £

Sales 4200 3200 2950

Cash receipts from sales 4200*30=1260

3200*30% =

960

2950*30% =

885

Receipts from credit sales 4200*70=2940

3200*70% =

2240

2950*70% =

2068

From the above-mentioned three-month cash budget, it can be deduced that the indicated

firm's ending balance at the end of every month is favorable. Cash is one of the most important

indicators of advancement that aids in determining how successful a company may be. On this

premise, it can be deduced that the corporation generates transactions, which aids in the

generation of money for the company. Clients may also acquire purchases on credit through the

publicly traded company, which allowed the firm produces 70% of its revenues. Only 30% of

motor purchase 3200

Purchase 2800 1500 1750

Telephone expenses 120 120 120

Total Cash payments (B) 4219 2420 5870

Net receipts (A- B) 7041 7821 4901

Balance brought forward 0 7041 7821

Balance carried forward 7041 7821 4901

Working note=

Particulars Jan Feb March

£ £ £

Sales 4200 3200 2950

Cash receipts from sales 4200*30=1260

3200*30% =

960

2950*30% =

885

Receipts from credit sales 4200*70=2940

3200*70% =

2240

2950*70% =

2068

From the above-mentioned three-month cash budget, it can be deduced that the indicated

firm's ending balance at the end of every month is favorable. Cash is one of the most important

indicators of advancement that aids in determining how successful a company may be. On this

premise, it can be deduced that the corporation generates transactions, which aids in the

generation of money for the company. Clients may also acquire purchases on credit through the

publicly traded company, which allowed the firm produces 70% of its revenues. Only 30% of

real cash sales are used to help the company fulfill its costs. Enterprise incurs minimum costs in

order to achieve its company objectives. This covers the cost of a laptop, a transport, graphics,

and phone calls, among other things.

On this basis, it can be determined that the firm has favorable results in January,

February, and March, with 7041, 7821, and 4901, respectively. As can be observed from the

budgetary control, the stated organisation is putting up significant attempt to accomplish a better

liquidity position. In order to maintain a solid financial competitive advantage, modifications in

the proprietor's individual withdrawal habit are required (Al Rahahleh and et.al, 2019). It may be

concluded that a firm can reap a variety of advantages by creating a cash budget in order to

increase profitability and long-term viability. These advantages include precise cash available

statistics, determination of necessary level finances, efficient management, and maximum asset

utilization. This assists in making strategic decisions about the use and allocation of cash,

allowing for increased production by overcoming unanticipated events. Process of creating a

cash budget can help to get the necessary abilities to create a competitive edge by ensuring long

term sustainability.

This also enables the business to resist going into debt since it becomes more creative,

and the truth of the company can be determined by examining at its financial condition.

Assessment of weak regions may be done efficiently, allowing for the correct and equitable

communication of financial information.

TASK 2

2.1 Explaining accounting equation and reason for its always balancing with example

The Accounting Equation (AE) is a key notion that aids in the comprehension of the balance

sheet's essential tenets.

Assets equal liabilities + shareholder equity is the equation in question.

It is a widely acknowledged formula for balancing a balance sheet. This is now the

foundation of the double entry system, which assists in obtaining reliable data for judgments.

The main motivation for this is because information is verified in different accounts since both

sides are considered (Bellavitis and et.al, 2017). Here on premise, it can be stated that the major

order to achieve its company objectives. This covers the cost of a laptop, a transport, graphics,

and phone calls, among other things.

On this basis, it can be determined that the firm has favorable results in January,

February, and March, with 7041, 7821, and 4901, respectively. As can be observed from the

budgetary control, the stated organisation is putting up significant attempt to accomplish a better

liquidity position. In order to maintain a solid financial competitive advantage, modifications in

the proprietor's individual withdrawal habit are required (Al Rahahleh and et.al, 2019). It may be

concluded that a firm can reap a variety of advantages by creating a cash budget in order to

increase profitability and long-term viability. These advantages include precise cash available

statistics, determination of necessary level finances, efficient management, and maximum asset

utilization. This assists in making strategic decisions about the use and allocation of cash,

allowing for increased production by overcoming unanticipated events. Process of creating a

cash budget can help to get the necessary abilities to create a competitive edge by ensuring long

term sustainability.

This also enables the business to resist going into debt since it becomes more creative,

and the truth of the company can be determined by examining at its financial condition.

Assessment of weak regions may be done efficiently, allowing for the correct and equitable

communication of financial information.

TASK 2

2.1 Explaining accounting equation and reason for its always balancing with example

The Accounting Equation (AE) is a key notion that aids in the comprehension of the balance

sheet's essential tenets.

Assets equal liabilities + shareholder equity is the equation in question.

It is a widely acknowledged formula for balancing a balance sheet. This is now the

foundation of the double entry system, which assists in obtaining reliable data for judgments.

The main motivation for this is because information is verified in different accounts since both

sides are considered (Bellavitis and et.al, 2017). Here on premise, it can be stated that the major

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

cause for the balance sheet's balancing is due to the use of the dual entry book. Accounting

equations is completing the task of delivering relevant, dependable and other data via preparing

the financial statements. It is critical for the business to provide comprehensive information to

financial planning users in order to prevent unnecessary legal obligations. It assists in

maintaining good operations in the sector in order to accomplish the firm's stated goals by

referencing to the financial statements and comparing to the summary supplied in the form of a

balance sheet.

Regardless of the size, nature, kind, or other characteristics of the organisation, the focus

is on constructing a position financially statement using accounting equations. This enables us to

obtain advantages in a variety of forms, allowing us to satisfy the high computation needs of the

organisation in a more effective manner. For example, a corporation may buy 500-dollar

equipment with cash to complete its operations. Cash will be credited when it leaves the

company and the machine will be deducted in this operation. This activity aids in the

comprehension of a total transaction twofold impact, allowing the financial state report to be

balanced (Adebiyi and Banjo, 2017).

Let's take a look at a few real-world activities to see how they affect the accounting equation.

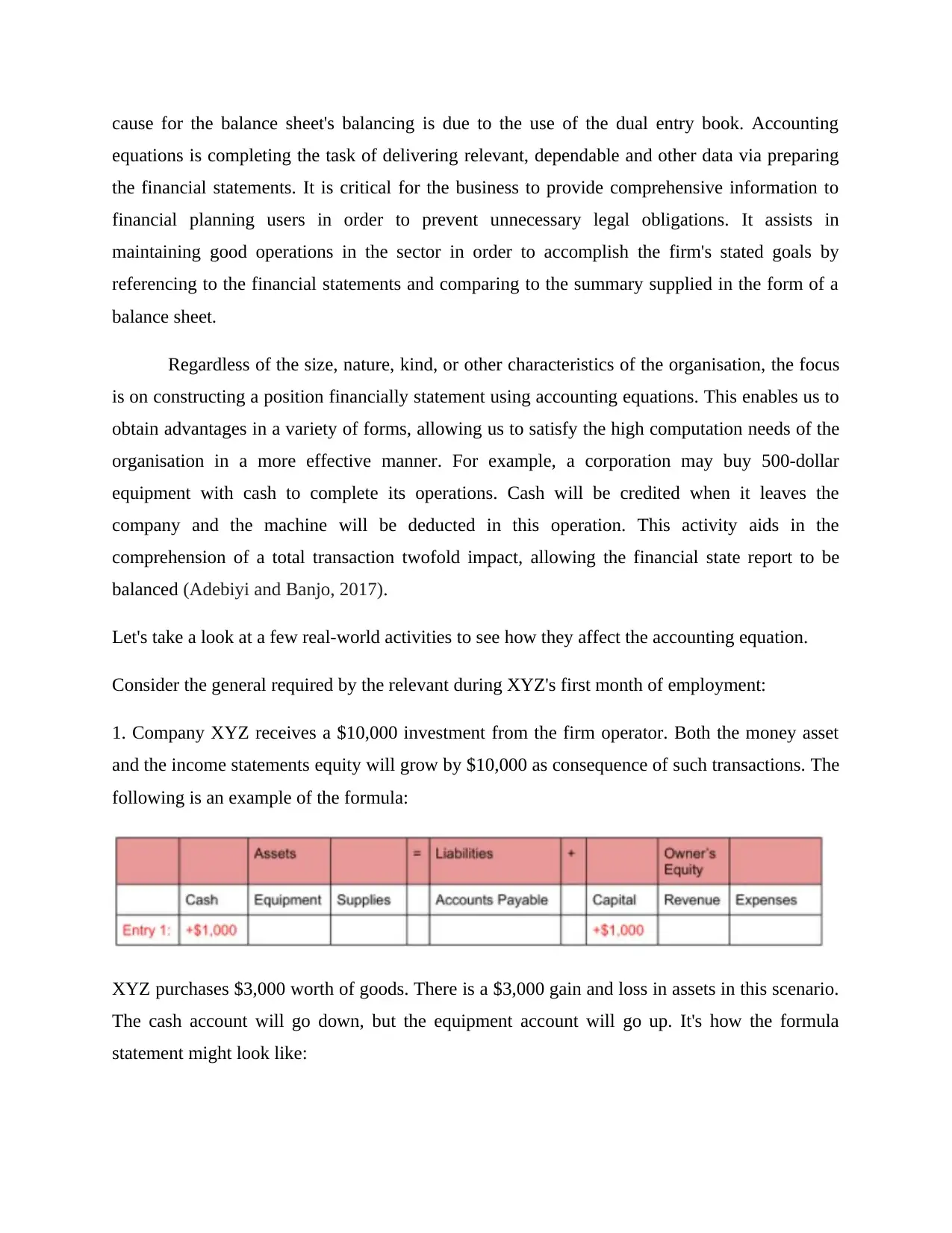

Consider the general required by the relevant during XYZ's first month of employment:

1. Company XYZ receives a $10,000 investment from the firm operator. Both the money asset

and the income statements equity will grow by $10,000 as consequence of such transactions. The

following is an example of the formula:

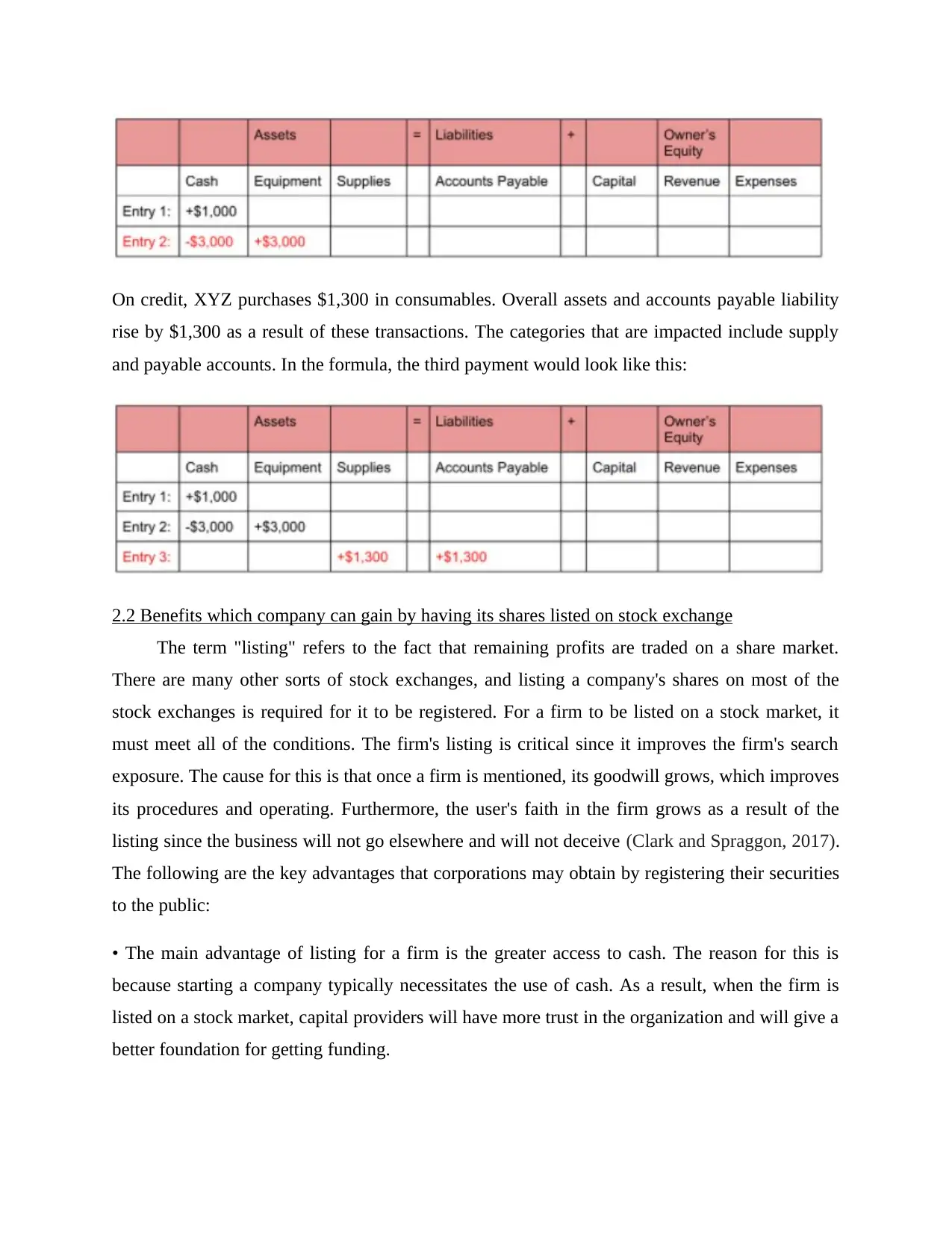

XYZ purchases $3,000 worth of goods. There is a $3,000 gain and loss in assets in this scenario.

The cash account will go down, but the equipment account will go up. It's how the formula

statement might look like:

equations is completing the task of delivering relevant, dependable and other data via preparing

the financial statements. It is critical for the business to provide comprehensive information to

financial planning users in order to prevent unnecessary legal obligations. It assists in

maintaining good operations in the sector in order to accomplish the firm's stated goals by

referencing to the financial statements and comparing to the summary supplied in the form of a

balance sheet.

Regardless of the size, nature, kind, or other characteristics of the organisation, the focus

is on constructing a position financially statement using accounting equations. This enables us to

obtain advantages in a variety of forms, allowing us to satisfy the high computation needs of the

organisation in a more effective manner. For example, a corporation may buy 500-dollar

equipment with cash to complete its operations. Cash will be credited when it leaves the

company and the machine will be deducted in this operation. This activity aids in the

comprehension of a total transaction twofold impact, allowing the financial state report to be

balanced (Adebiyi and Banjo, 2017).

Let's take a look at a few real-world activities to see how they affect the accounting equation.

Consider the general required by the relevant during XYZ's first month of employment:

1. Company XYZ receives a $10,000 investment from the firm operator. Both the money asset

and the income statements equity will grow by $10,000 as consequence of such transactions. The

following is an example of the formula:

XYZ purchases $3,000 worth of goods. There is a $3,000 gain and loss in assets in this scenario.

The cash account will go down, but the equipment account will go up. It's how the formula

statement might look like:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

On credit, XYZ purchases $1,300 in consumables. Overall assets and accounts payable liability

rise by $1,300 as a result of these transactions. The categories that are impacted include supply

and payable accounts. In the formula, the third payment would look like this:

2.2 Benefits which company can gain by having its shares listed on stock exchange

The term "listing" refers to the fact that remaining profits are traded on a share market.

There are many other sorts of stock exchanges, and listing a company's shares on most of the

stock exchanges is required for it to be registered. For a firm to be listed on a stock market, it

must meet all of the conditions. The firm's listing is critical since it improves the firm's search

exposure. The cause for this is that once a firm is mentioned, its goodwill grows, which improves

its procedures and operating. Furthermore, the user's faith in the firm grows as a result of the

listing since the business will not go elsewhere and will not deceive (Clark and Spraggon, 2017).

The following are the key advantages that corporations may obtain by registering their securities

to the public:

• The main advantage of listing for a firm is the greater access to cash. The reason for this is

because starting a company typically necessitates the use of cash. As a result, when the firm is

listed on a stock market, capital providers will have more trust in the organization and will give a

better foundation for getting funding.

rise by $1,300 as a result of these transactions. The categories that are impacted include supply

and payable accounts. In the formula, the third payment would look like this:

2.2 Benefits which company can gain by having its shares listed on stock exchange

The term "listing" refers to the fact that remaining profits are traded on a share market.

There are many other sorts of stock exchanges, and listing a company's shares on most of the

stock exchanges is required for it to be registered. For a firm to be listed on a stock market, it

must meet all of the conditions. The firm's listing is critical since it improves the firm's search

exposure. The cause for this is that once a firm is mentioned, its goodwill grows, which improves

its procedures and operating. Furthermore, the user's faith in the firm grows as a result of the

listing since the business will not go elsewhere and will not deceive (Clark and Spraggon, 2017).

The following are the key advantages that corporations may obtain by registering their securities

to the public:

• The main advantage of listing for a firm is the greater access to cash. The reason for this is

because starting a company typically necessitates the use of cash. As a result, when the firm is

listed on a stock market, capital providers will have more trust in the organization and will give a

better foundation for getting funding.

• Other advantage of putting a firm on a stock exchange is the increased visibility in a

competitive industry. The rationale for this is because whenever a firm is listed on a marketplace,

additional individuals and institutions may obtain data about it. As a result, the firm's reputation

and exposure in the international markets will improve.

• Another advantage of putting the firm on the stock exchange is availability. This is due to the

fact that if the firm requires funds, it can decisions and actions and receive funds. Investors also

benefit from liquidity since they can move their money at any time and receive a return on their

investment.

• Another advantage of going public is that it renders the company's activities better accessible

and productive. The rationale for this is because whenever a firm is publicly listed exchanges, it

must comply with a series of things and rules. In addition, the corporation is required to disclose

a variety of reports and other data with stockholders as well as others. As a result, when a firm is

publicly traded, the business requirements are more transparent and efficient (Cumming and

et.al, 2019).

• Additionally, a firm's listing on a stock market gives it a level playing field when it comes to

pricing. The value of goods is judged on the basis of producers and consumers with the aid of the

stock market, and customers pay fair costs as a result.

2.3 Stakeholders in large listed company like Marks and Spencer

Stakeholders are individuals or groups of customers who are interested in the company's

business and are influenced by all of the firm's operations. There are numerous sorts of

shareholders in either organization that want the firm to run more smoothly. All of the personnel

involved with the organisation and its activities contribute to the successful completion of the

task. For a firm to succeed, all parties must be particularly pleased in order for corporate

objectives to be conducted properly and effectively. A big publicly traded firm, such as Marks

and Spencer, is required to have shareholder inside the corporation. The basis for this is that if a

firm has strong stakeholder trust, it will be able to function and operate more efficiently. There

are two sorts of shareholder in a major publicly traded corporation: internally and externally

(Zimmermann, 2020).

competitive industry. The rationale for this is because whenever a firm is listed on a marketplace,

additional individuals and institutions may obtain data about it. As a result, the firm's reputation

and exposure in the international markets will improve.

• Another advantage of putting the firm on the stock exchange is availability. This is due to the

fact that if the firm requires funds, it can decisions and actions and receive funds. Investors also

benefit from liquidity since they can move their money at any time and receive a return on their

investment.

• Another advantage of going public is that it renders the company's activities better accessible

and productive. The rationale for this is because whenever a firm is publicly listed exchanges, it

must comply with a series of things and rules. In addition, the corporation is required to disclose

a variety of reports and other data with stockholders as well as others. As a result, when a firm is

publicly traded, the business requirements are more transparent and efficient (Cumming and

et.al, 2019).

• Additionally, a firm's listing on a stock market gives it a level playing field when it comes to

pricing. The value of goods is judged on the basis of producers and consumers with the aid of the

stock market, and customers pay fair costs as a result.

2.3 Stakeholders in large listed company like Marks and Spencer

Stakeholders are individuals or groups of customers who are interested in the company's

business and are influenced by all of the firm's operations. There are numerous sorts of

shareholders in either organization that want the firm to run more smoothly. All of the personnel

involved with the organisation and its activities contribute to the successful completion of the

task. For a firm to succeed, all parties must be particularly pleased in order for corporate

objectives to be conducted properly and effectively. A big publicly traded firm, such as Marks

and Spencer, is required to have shareholder inside the corporation. The basis for this is that if a

firm has strong stakeholder trust, it will be able to function and operate more efficiently. There

are two sorts of shareholder in a major publicly traded corporation: internally and externally

(Zimmermann, 2020).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The organization's corporate stakeholders are those who are directly involved in the

firm's management and are concerned in the firm's management. Workers, owners, and managers

are often included in these inner key stakeholders. The outside shareholder of the firm, on the

other extreme, is made up of individuals who are engaged in the firm's earnings though not in a

straightforward manner. However, the company's success is extremely important to various

parties. Clients, suppliers, the administration, culture, investors, organized labor, and a variety of

other interests make up Marks and Spencer's various customers (Waleczek, Zehren and Flatten,

2018).

All of these different stakeholders have a vested interest and authority in the organisation.

This passion and power inspires people to work efficiently and effectively, resulting in improved

company governance. Whenever interest is strong, they will operate much more efficiently and

effectively. As a consequence, company operations will be expanded. This is due to the fact that

when stakeholders complete all of their responsibilities in an efficient and productive manner; it

leads to more efficient and productive performance. For example, whenever workers, who are

internal stakeholders in the firm, operate properly and effectively, the financial value improves.

As a consequence, the firm's work productivity will enhance, and as revenues rise, employees

will be given bonuses. Additionally, Marks & Spencer's stockholders, who are exterior to the

corporation, are stakeholders.

Shareholders are primarily concerned with improving the corporate accounting success.

As a result, they encourage the firm and its workers to work harder and more efficiently in order

to boost profits. Whenever sales revenue rises, so does the dividend given to the existing shares.

Furthermore, other illustration is the government, which is an outside investor in the firm but has

a strong interest in it. The rationale for this is that if a firm earns a fortune, the government was

able to collect more taxes. As a result, the government has little control inside the corporation but

a strong stake in its prosperity (Gunawan and Chairani, 2019).

2.4 Profit as a reliable indicator of cash balance and difference within profit and cash

Once all expenditures have been deducted from the overall sales received by the firm, the

profitability is the amount remaining. Any company exists to make money. It is believed that the

more the revenue, the better the firm. As a result, a larger level of profit must be made by the

firm in order for it to invest in growth. This is critical because profit is the grand total even after

firm's management and are concerned in the firm's management. Workers, owners, and managers

are often included in these inner key stakeholders. The outside shareholder of the firm, on the

other extreme, is made up of individuals who are engaged in the firm's earnings though not in a

straightforward manner. However, the company's success is extremely important to various

parties. Clients, suppliers, the administration, culture, investors, organized labor, and a variety of

other interests make up Marks and Spencer's various customers (Waleczek, Zehren and Flatten,

2018).

All of these different stakeholders have a vested interest and authority in the organisation.

This passion and power inspires people to work efficiently and effectively, resulting in improved

company governance. Whenever interest is strong, they will operate much more efficiently and

effectively. As a consequence, company operations will be expanded. This is due to the fact that

when stakeholders complete all of their responsibilities in an efficient and productive manner; it

leads to more efficient and productive performance. For example, whenever workers, who are

internal stakeholders in the firm, operate properly and effectively, the financial value improves.

As a consequence, the firm's work productivity will enhance, and as revenues rise, employees

will be given bonuses. Additionally, Marks & Spencer's stockholders, who are exterior to the

corporation, are stakeholders.

Shareholders are primarily concerned with improving the corporate accounting success.

As a result, they encourage the firm and its workers to work harder and more efficiently in order

to boost profits. Whenever sales revenue rises, so does the dividend given to the existing shares.

Furthermore, other illustration is the government, which is an outside investor in the firm but has

a strong interest in it. The rationale for this is that if a firm earns a fortune, the government was

able to collect more taxes. As a result, the government has little control inside the corporation but

a strong stake in its prosperity (Gunawan and Chairani, 2019).

2.4 Profit as a reliable indicator of cash balance and difference within profit and cash

Once all expenditures have been deducted from the overall sales received by the firm, the

profitability is the amount remaining. Any company exists to make money. It is believed that the

more the revenue, the better the firm. As a result, a larger level of profit must be made by the

firm in order for it to invest in growth. This is critical because profit is the grand total even after

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

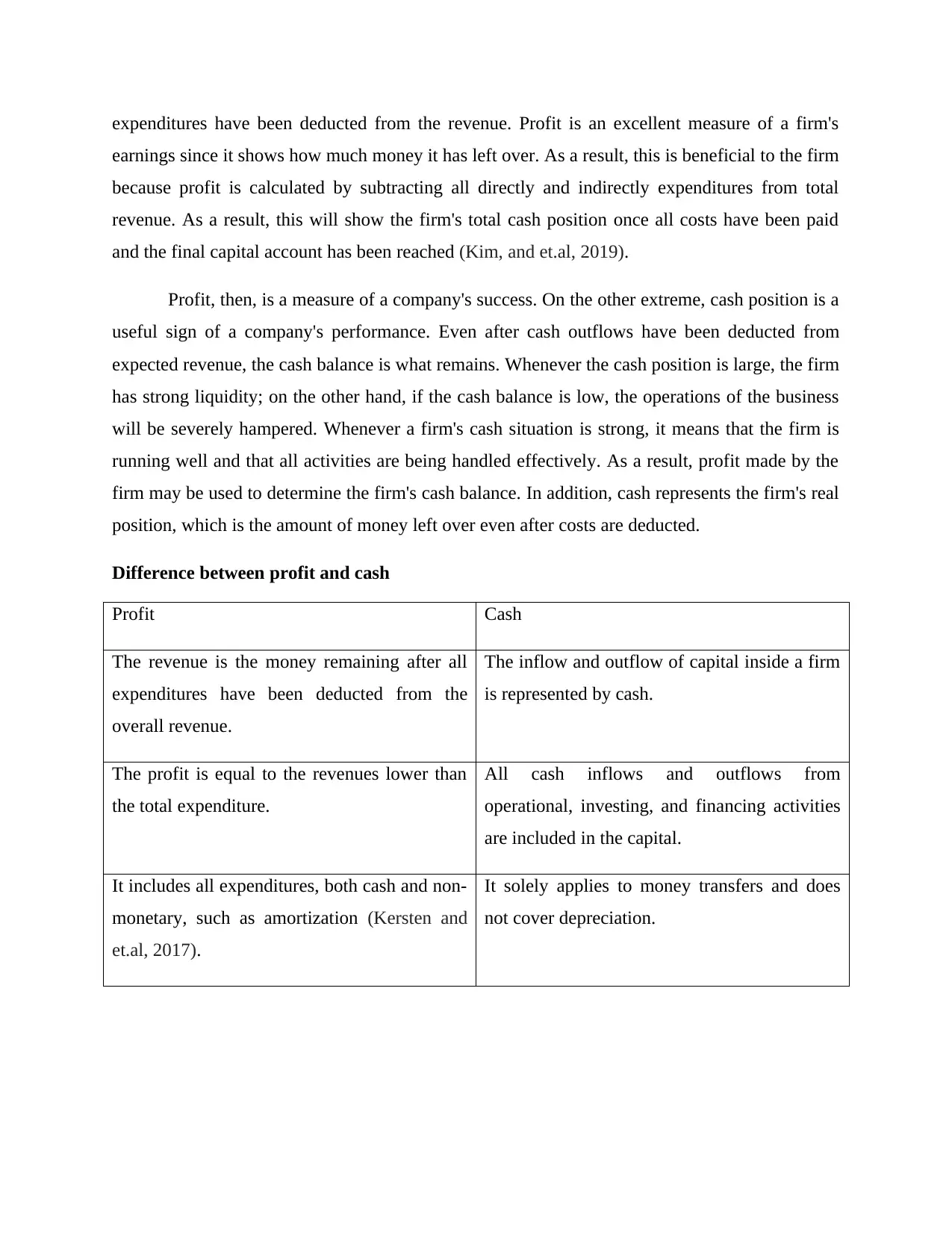

expenditures have been deducted from the revenue. Profit is an excellent measure of a firm's

earnings since it shows how much money it has left over. As a result, this is beneficial to the firm

because profit is calculated by subtracting all directly and indirectly expenditures from total

revenue. As a result, this will show the firm's total cash position once all costs have been paid

and the final capital account has been reached (Kim, and et.al, 2019).

Profit, then, is a measure of a company's success. On the other extreme, cash position is a

useful sign of a company's performance. Even after cash outflows have been deducted from

expected revenue, the cash balance is what remains. Whenever the cash position is large, the firm

has strong liquidity; on the other hand, if the cash balance is low, the operations of the business

will be severely hampered. Whenever a firm's cash situation is strong, it means that the firm is

running well and that all activities are being handled effectively. As a result, profit made by the

firm may be used to determine the firm's cash balance. In addition, cash represents the firm's real

position, which is the amount of money left over even after costs are deducted.

Difference between profit and cash

Profit Cash

The revenue is the money remaining after all

expenditures have been deducted from the

overall revenue.

The inflow and outflow of capital inside a firm

is represented by cash.

The profit is equal to the revenues lower than

the total expenditure.

All cash inflows and outflows from

operational, investing, and financing activities

are included in the capital.

It includes all expenditures, both cash and non-

monetary, such as amortization (Kersten and

et.al, 2017).

It solely applies to money transfers and does

not cover depreciation.

earnings since it shows how much money it has left over. As a result, this is beneficial to the firm

because profit is calculated by subtracting all directly and indirectly expenditures from total

revenue. As a result, this will show the firm's total cash position once all costs have been paid

and the final capital account has been reached (Kim, and et.al, 2019).

Profit, then, is a measure of a company's success. On the other extreme, cash position is a

useful sign of a company's performance. Even after cash outflows have been deducted from

expected revenue, the cash balance is what remains. Whenever the cash position is large, the firm

has strong liquidity; on the other hand, if the cash balance is low, the operations of the business

will be severely hampered. Whenever a firm's cash situation is strong, it means that the firm is

running well and that all activities are being handled effectively. As a result, profit made by the

firm may be used to determine the firm's cash balance. In addition, cash represents the firm's real

position, which is the amount of money left over even after costs are deducted.

Difference between profit and cash

Profit Cash

The revenue is the money remaining after all

expenditures have been deducted from the

overall revenue.

The inflow and outflow of capital inside a firm

is represented by cash.

The profit is equal to the revenues lower than

the total expenditure.

All cash inflows and outflows from

operational, investing, and financing activities

are included in the capital.

It includes all expenditures, both cash and non-

monetary, such as amortization (Kersten and

et.al, 2017).

It solely applies to money transfers and does

not cover depreciation.

CONCLUSION

It may be stated from the foregoing research that analysis is critical for creating strategic

decisions. The latest report includes data on the budget period, which indicates a favorable

outcome. Additionally, there are a numerous benefits to developing a cash budget, including

reliable and efficient access to the company's finances. The accounting equation and the

justification for always rebalancing the balance sheet are covered in this paper. The present

research examined at the benefits that a firm may get from having its shares publicly traded

companies, including such increased access to credit and so on. Internally and externally

investors are separate in major publicly traded companies like Marks and Spencer. The

discrepancy between cash and profit has been properly calculated and reported in the report.

REFERENCES

Books and Journal

Grossmann, A., Mooney, L. and Dugan, M., 2019. Inclusion fairness in accounting, finance, and

management: An investigation of A-star publications on the ABDC journal list. Journal

of Business Research. 95. pp.232-241.

Al Rahahleh, N. and et.al, 2019. Developments in risk management in Islamic finance: A

review. Journal of Risk and Financial Management. 12(1). p.37.

Bellavitis, C. and et.al, 2017. Entrepreneurial finance: new frontiers of research and practice:

Editorial for the special issue Embracing entrepreneurial funding innovations.

Adebiyi, A. J. and Banjo, H. A., 2017. Performance of small and medium enterprises in Lagos

State: The implications of finance. Acta Universitatis Danubius. Œconomica. 13(5).

Clark, J. and Spraggon, J., 2017. The Applicability of Micro Finance to Higher Risk Business

Ventures: An Experimental Study (No. 17/20).

Cumming, D. and et.al, 2019. New directions in entrepreneurial finance. Journal of Banking &

Finance. 100. pp.252-260.

Waleczek, P., Zehren, T. and Flatten, T. C., 2018. Start‐up financing: How founders finance their

ventures' early stage. Managerial and Decision Economics. 39(5). pp.535-549.

Gunawan, A. and Chairani, C., 2019. Effect of Financial Literacy and Lifestyle of Finance

Student Behavior. International Journal of Business Economics (IJBE). 1(1). pp.76-86.

It may be stated from the foregoing research that analysis is critical for creating strategic

decisions. The latest report includes data on the budget period, which indicates a favorable

outcome. Additionally, there are a numerous benefits to developing a cash budget, including

reliable and efficient access to the company's finances. The accounting equation and the

justification for always rebalancing the balance sheet are covered in this paper. The present

research examined at the benefits that a firm may get from having its shares publicly traded

companies, including such increased access to credit and so on. Internally and externally

investors are separate in major publicly traded companies like Marks and Spencer. The

discrepancy between cash and profit has been properly calculated and reported in the report.

REFERENCES

Books and Journal

Grossmann, A., Mooney, L. and Dugan, M., 2019. Inclusion fairness in accounting, finance, and

management: An investigation of A-star publications on the ABDC journal list. Journal

of Business Research. 95. pp.232-241.

Al Rahahleh, N. and et.al, 2019. Developments in risk management in Islamic finance: A

review. Journal of Risk and Financial Management. 12(1). p.37.

Bellavitis, C. and et.al, 2017. Entrepreneurial finance: new frontiers of research and practice:

Editorial for the special issue Embracing entrepreneurial funding innovations.

Adebiyi, A. J. and Banjo, H. A., 2017. Performance of small and medium enterprises in Lagos

State: The implications of finance. Acta Universitatis Danubius. Œconomica. 13(5).

Clark, J. and Spraggon, J., 2017. The Applicability of Micro Finance to Higher Risk Business

Ventures: An Experimental Study (No. 17/20).

Cumming, D. and et.al, 2019. New directions in entrepreneurial finance. Journal of Banking &

Finance. 100. pp.252-260.

Waleczek, P., Zehren, T. and Flatten, T. C., 2018. Start‐up financing: How founders finance their

ventures' early stage. Managerial and Decision Economics. 39(5). pp.535-549.

Gunawan, A. and Chairani, C., 2019. Effect of Financial Literacy and Lifestyle of Finance

Student Behavior. International Journal of Business Economics (IJBE). 1(1). pp.76-86.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.