Business Finance Report: RCL Working Capital and Capital Budgeting

VerifiedAdded on 2020/07/23

|10

|3307

|85

Report

AI Summary

This report provides a comprehensive analysis of Root and Cook Ltd.'s (RCL) financial performance, focusing on working capital management and capital budgeting. Part 1 examines the differences between profit and cash flow, emphasizing the impact of receivables, inventory, and payables on cash flow. It also discusses various management concepts and their implications on the company's financial status, offering recommendations for improving working capital management. Part 2 delves into capital budgeting, outlining its purpose, key steps, and the advantages and disadvantages of investment appraisal methods. The report analyzes two potential investment projects, Reading and Bristol, and provides recommendations for decision-making. The report highlights the importance of timely collection of receivables, improved payables, price negotiation, and expense reduction to enhance RCL's financial stability and profitability. The executive summary encapsulates the key findings and emphasizes the need for effective working capital management to avoid insolvency and ensure sufficient cash flow for operational activities.

BUSINESS FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

PART 1............................................................................................................................................1

i (a) Difference of Profit and Cash flow of RCL........................................................................1

i (b) Theory of working capital, receivables, inventory and payables........................................1

i (c) Impact of Working Capital affect Cash flow.......................................................................1

ii) Various management concepts and their implication on company's financial status.............2

iii) Analysis and recommendations for improving Working Capital Management....................3

PART 2............................................................................................................................................4

i (a)Purpose and Key steps of Capital Budgeting.......................................................................4

i (b) Advantages and disadvantages of Investment Appraisal Methods....................................5

ii Comparison of the alternative investment options..................................................................6

iii Analysis and recommendations..............................................................................................6

..........................................................................................................................................................7

REFERENCES................................................................................................................................8

PART 1............................................................................................................................................1

i (a) Difference of Profit and Cash flow of RCL........................................................................1

i (b) Theory of working capital, receivables, inventory and payables........................................1

i (c) Impact of Working Capital affect Cash flow.......................................................................1

ii) Various management concepts and their implication on company's financial status.............2

iii) Analysis and recommendations for improving Working Capital Management....................3

PART 2............................................................................................................................................4

i (a)Purpose and Key steps of Capital Budgeting.......................................................................4

i (b) Advantages and disadvantages of Investment Appraisal Methods....................................5

ii Comparison of the alternative investment options..................................................................6

iii Analysis and recommendations..............................................................................................6

..........................................................................................................................................................7

REFERENCES................................................................................................................................8

PART 1

i (a) Difference of Profit and Cash flow of RCL

The term profit is defined as financial gain which is distributed at end of the year to

shareholders. On other hand, cash refers to physical money. A business may have a profit but

cannot have cash because profit is calculated by using revenues and expenses which is different

from company's cash receipts and cash payments. Cash flow is termed as the difference of cash

amount that a company receives and pays whereas, profit is determined by the evaluation of

revenues and expenses in a given year. Profitability is a concept which cannot be measured in

terms of cash rather depends on the results of accumulated cash (Bierman and Smidt, 2012).

The 2 prime customers of RCL are D&R DIY and BricoFrance. The company generated

its major operating profit as a result of an order placed by D&R last year of 12 million pounds.

It's major revenue was stuck as a result of the increasing debts and the irregularity of payments

from its customers. Most of the company's amount is also involved in disputes with

BricoFinance which has stopped payment of 20 million pounds and Robocut had an 8 million

pound advance payment for manufacturing automatic grass cut machines.

i (b) Theory of working capital, receivables, inventory and payables

Working capital is a broader concept which includes receivable’s inventory and payables.

The working capital of a company is calculated by subtracting current liabilities from its current

assets. A deficit in working capital implies that company has less value of current assets as

compared to its current liabilities. It measures the ability of a company to repay its short term

loans and debts as well as provide funds for company's operations (Gervais, 2010).

RCL has a deficit in net working capital as an inventory is lined up in the warehouses and

payables are generating with no cash receivables. Steve, the owner of RCL, is pushing up

customers for making immediate payments as the shareholders are worried about company's

operations. Steve is showing concern for other shareholders to invest in company as it's debts

have increased from last year to 157 million pounds.

i (c) Impact of Working Capital affect Cash flow

The impact of inventory, receivables and payables have an effect on company's cash

flow. The operating cash flow includes all those transactions which are occurring irrespective of

generating any cash transactions for company. The deficit in working capital implies that

1

i (a) Difference of Profit and Cash flow of RCL

The term profit is defined as financial gain which is distributed at end of the year to

shareholders. On other hand, cash refers to physical money. A business may have a profit but

cannot have cash because profit is calculated by using revenues and expenses which is different

from company's cash receipts and cash payments. Cash flow is termed as the difference of cash

amount that a company receives and pays whereas, profit is determined by the evaluation of

revenues and expenses in a given year. Profitability is a concept which cannot be measured in

terms of cash rather depends on the results of accumulated cash (Bierman and Smidt, 2012).

The 2 prime customers of RCL are D&R DIY and BricoFrance. The company generated

its major operating profit as a result of an order placed by D&R last year of 12 million pounds.

It's major revenue was stuck as a result of the increasing debts and the irregularity of payments

from its customers. Most of the company's amount is also involved in disputes with

BricoFinance which has stopped payment of 20 million pounds and Robocut had an 8 million

pound advance payment for manufacturing automatic grass cut machines.

i (b) Theory of working capital, receivables, inventory and payables

Working capital is a broader concept which includes receivable’s inventory and payables.

The working capital of a company is calculated by subtracting current liabilities from its current

assets. A deficit in working capital implies that company has less value of current assets as

compared to its current liabilities. It measures the ability of a company to repay its short term

loans and debts as well as provide funds for company's operations (Gervais, 2010).

RCL has a deficit in net working capital as an inventory is lined up in the warehouses and

payables are generating with no cash receivables. Steve, the owner of RCL, is pushing up

customers for making immediate payments as the shareholders are worried about company's

operations. Steve is showing concern for other shareholders to invest in company as it's debts

have increased from last year to 157 million pounds.

i (c) Impact of Working Capital affect Cash flow

The impact of inventory, receivables and payables have an effect on company's cash

flow. The operating cash flow includes all those transactions which are occurring irrespective of

generating any cash transactions for company. The deficit in working capital implies that

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

company has more cash liquidity which could be used to fund other operational projects. On the

other hand, an increase in working capital shows that company is financing its resources for

shorter period of time. Thus, expressing a reduction in the accessible cash flow from the

financing, investment and operating activities.

Root and Cook Ltd. in the current year at the Manchester site is experiencing an increase

in working capital as cash receivables are late, inventory is held in go-downs and payments are

done in advance. Such activities of company put a direct impact on its share value in the market

which is a major concern for it's shareholders who might withdraw their money. Steve needs to

take decisions to contemplate the company's position (Bierman and Smidt, 2012).

ii) Various management concepts and their implication on company's financial status

The availability of short term assets for meeting its financial operations is an important

factor for any company. Most of the manufacturing units face challenges of low cash availability

as it requires future payments for acquiring various machineries for producing goods. The deficit

in working capital implies that company has more cash liquidity which could be used to fund

other operational projects. On the other hand, an increase in working capital shows that company

is financing its resources for shorter period. For instance: a company buy reams for 100 x 10

pounds (1000 pounds) and uses only 50 reams in a year. The company pays 1000 pounds in cash

though had only made an expense of 500 pounds implies a negative cash outflow of 500 pounds.

On the other hand, same company generates a sales revenue of 1000 pounds out of which 50 %

of its customers take goods on credit which implies earnings of 500 pounds. Thus, the profit and

cash flow figures are:

Cash flow: = Cash inflow (500 pounds of cash sales) minus cash outflow (1,000 pounds

reams) => - 500 pounds cash flow

Profit = Income earned (1,000 pounds of sales) minus cost incurred (500 pounds utilized

for reams) => +500 pounds of total profit

Root and Cook Ltd is experiencing a good profitability figure in current year though the

cash amount is nil as company's cash receivables and payables have a huge difference. Both;

cash and profit are the measures of accounting. The profit is measured in terms of company's

prolong ability while cash depends on its receiving and paying ability. Steve is working on how

to increase firm’s liquidity by maintaining profitability position. The inventory of raw materials

2

other hand, an increase in working capital shows that company is financing its resources for

shorter period of time. Thus, expressing a reduction in the accessible cash flow from the

financing, investment and operating activities.

Root and Cook Ltd. in the current year at the Manchester site is experiencing an increase

in working capital as cash receivables are late, inventory is held in go-downs and payments are

done in advance. Such activities of company put a direct impact on its share value in the market

which is a major concern for it's shareholders who might withdraw their money. Steve needs to

take decisions to contemplate the company's position (Bierman and Smidt, 2012).

ii) Various management concepts and their implication on company's financial status

The availability of short term assets for meeting its financial operations is an important

factor for any company. Most of the manufacturing units face challenges of low cash availability

as it requires future payments for acquiring various machineries for producing goods. The deficit

in working capital implies that company has more cash liquidity which could be used to fund

other operational projects. On the other hand, an increase in working capital shows that company

is financing its resources for shorter period. For instance: a company buy reams for 100 x 10

pounds (1000 pounds) and uses only 50 reams in a year. The company pays 1000 pounds in cash

though had only made an expense of 500 pounds implies a negative cash outflow of 500 pounds.

On the other hand, same company generates a sales revenue of 1000 pounds out of which 50 %

of its customers take goods on credit which implies earnings of 500 pounds. Thus, the profit and

cash flow figures are:

Cash flow: = Cash inflow (500 pounds of cash sales) minus cash outflow (1,000 pounds

reams) => - 500 pounds cash flow

Profit = Income earned (1,000 pounds of sales) minus cost incurred (500 pounds utilized

for reams) => +500 pounds of total profit

Root and Cook Ltd is experiencing a good profitability figure in current year though the

cash amount is nil as company's cash receivables and payables have a huge difference. Both;

cash and profit are the measures of accounting. The profit is measured in terms of company's

prolong ability while cash depends on its receiving and paying ability. Steve is working on how

to increase firm’s liquidity by maintaining profitability position. The inventory of raw materials

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

is lined up and slow payments from customers are key points to be look into to improve the

overall cash generation of company (Nazir and Afza, 2009).

iii) Analysis and recommendations for improving Working Capital Management.

Various practices are adopted by companies to manage their working capital efficiently.

The working capital is calculated as current assets minus current liabilities. The ideal ratio in

between the two is 2:1 which implies 2 portion of assets while 1 portion of liabilities must be

preserved in a business enterprise. To ensure that company has sufficient monetary value to

execute its regular financial activities as well as to fund daily business activities, it should

manage its working capital both efficiently and effectively. Too much of working capital leads to

decreased profits and shareholder’s value as well as little working capital may lead to insolvency

of company (Bierman and Smidt, 2012). The various methods that could be used to bring

stability in working capital are:

Timely collection of receivables: Company should have a check on timely collection of

payments from its customers. It could be done by motivating collection teams by

providing incentives for early collection of payments. RCL’s major issue was lack of

collection of payments which has reduced company's liquidity and thereby, preventing it

to fund other financial operations.

Improved account payables: This will lock up cash in company for funding other

projects. There should always be a balance in between cash receivables and cash payables

of a company. Procuring of raw materials from suppliers on credit basis also help

companies in locking up cash.

Price negotiation: Procurement of raw materials should always be done by evaluating

prices of various suppliers and negotiating with them. Suppliers could be changed

keeping the cost incurred on the company. Best type of raw material should be bought so

as to gain maximum profitability(Bierman and Smidt, 2012).

Less expenses: Company should curtail its expenses both fixed and variable to improve

its overall cash flow. RCL has a major task of decreasing its expenses for the firm to gain

cash accessibility for meeting its short term debts and operational projects.

EXECUTIVE SUMMARY

3

overall cash generation of company (Nazir and Afza, 2009).

iii) Analysis and recommendations for improving Working Capital Management.

Various practices are adopted by companies to manage their working capital efficiently.

The working capital is calculated as current assets minus current liabilities. The ideal ratio in

between the two is 2:1 which implies 2 portion of assets while 1 portion of liabilities must be

preserved in a business enterprise. To ensure that company has sufficient monetary value to

execute its regular financial activities as well as to fund daily business activities, it should

manage its working capital both efficiently and effectively. Too much of working capital leads to

decreased profits and shareholder’s value as well as little working capital may lead to insolvency

of company (Bierman and Smidt, 2012). The various methods that could be used to bring

stability in working capital are:

Timely collection of receivables: Company should have a check on timely collection of

payments from its customers. It could be done by motivating collection teams by

providing incentives for early collection of payments. RCL’s major issue was lack of

collection of payments which has reduced company's liquidity and thereby, preventing it

to fund other financial operations.

Improved account payables: This will lock up cash in company for funding other

projects. There should always be a balance in between cash receivables and cash payables

of a company. Procuring of raw materials from suppliers on credit basis also help

companies in locking up cash.

Price negotiation: Procurement of raw materials should always be done by evaluating

prices of various suppliers and negotiating with them. Suppliers could be changed

keeping the cost incurred on the company. Best type of raw material should be bought so

as to gain maximum profitability(Bierman and Smidt, 2012).

Less expenses: Company should curtail its expenses both fixed and variable to improve

its overall cash flow. RCL has a major task of decreasing its expenses for the firm to gain

cash accessibility for meeting its short term debts and operational projects.

EXECUTIVE SUMMARY

3

The above report incorporates how different accounting factors affect working of a

company. Steve, one of the shareholders of company, is engaged in taking crucial decisions so as

to bring stability in the inflow and outflow of cash. Insufficiency of working capital may have an

impact on company's liquidity status. To ensure that company has sufficient monetary value to

execute its regular financial activities as well as to fund daily business activities, it should

manage the working capital both efficiently and effectively. Too much of working capital leads

to decreased profits and shareholder’s value as well as little working capital may lead to

insolvency of company.

PART 2

i (a)Purpose and Key steps of Capital Budgeting.

The term capital budgeting is known as the investment of capital in long term projects

which will generate cash in a period of one year. It incorporates decisions to make investment in

buildings, plants, heavy machines etc. It is an aspect of financial management. Financial

managers should see capital budgeting methods if they want to plan long term investment of its

profits. The process of capital budgeting involves three crucial steps to be undertaken. Capital

budgeting enhances company's competitive position thereby accumulating profits and allocation

of excess profits to shareholders (Storey and Greene, 2010).

To decide the amount of expenditure needed to make an investment: It involves

taking vital decisions as to how much an investment will cost and how much the

company will earn in the coming years.

Determine the possible sources of capital availability: This step involves searching for

various possible sources of inflow and making the best possible use of it. Ascertaining

the sources from which capital could be raised for funding the investments.

Allocate the capital available in different investment aspects: This aspect focuses on

which projects among the ones shortlisted should be preferred for funding and why. The

why concept is an important question every manger should look into before investing.

Steve at RCL is concerned about investing in two new manufacturing projects with

Reading or Bristol. Both the projects involves huge investment to be undertaken. The Reading

venture involves construction on an abandoned site which will cost £20 million and would

operate for 9-10 years. The other project with Bristol involves £16 million investment and will

4

company. Steve, one of the shareholders of company, is engaged in taking crucial decisions so as

to bring stability in the inflow and outflow of cash. Insufficiency of working capital may have an

impact on company's liquidity status. To ensure that company has sufficient monetary value to

execute its regular financial activities as well as to fund daily business activities, it should

manage the working capital both efficiently and effectively. Too much of working capital leads

to decreased profits and shareholder’s value as well as little working capital may lead to

insolvency of company.

PART 2

i (a)Purpose and Key steps of Capital Budgeting.

The term capital budgeting is known as the investment of capital in long term projects

which will generate cash in a period of one year. It incorporates decisions to make investment in

buildings, plants, heavy machines etc. It is an aspect of financial management. Financial

managers should see capital budgeting methods if they want to plan long term investment of its

profits. The process of capital budgeting involves three crucial steps to be undertaken. Capital

budgeting enhances company's competitive position thereby accumulating profits and allocation

of excess profits to shareholders (Storey and Greene, 2010).

To decide the amount of expenditure needed to make an investment: It involves

taking vital decisions as to how much an investment will cost and how much the

company will earn in the coming years.

Determine the possible sources of capital availability: This step involves searching for

various possible sources of inflow and making the best possible use of it. Ascertaining

the sources from which capital could be raised for funding the investments.

Allocate the capital available in different investment aspects: This aspect focuses on

which projects among the ones shortlisted should be preferred for funding and why. The

why concept is an important question every manger should look into before investing.

Steve at RCL is concerned about investing in two new manufacturing projects with

Reading or Bristol. Both the projects involves huge investment to be undertaken. The Reading

venture involves construction on an abandoned site which will cost £20 million and would

operate for 9-10 years. The other project with Bristol involves £16 million investment and will

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

have an expected useful life of 5-6 years. Steve need to undertake a crucial capital budgeting

process and decide which project will benefit the company in the long run by generating profit as

well as maintaining sufficient cash for the short term operations.

(Source: The capital budgeting, 2017)

i (b) Advantages and disadvantages of Investment Appraisal Methods

The Investment appraisal of new projects involves deciding whether the new machines,

set up new plant, procuring of buildings or replacement of tools are worth to fund or not. These

methods incorporates payback period, net present value and internal rate of return which is

calculated to decide whether the investment decision should be taken or not (Preve and Allende,

2010).

b. i Net present value: The term NPV is a method used for calculating the investment

appraisal which focuses on surplus or shortage of cash inflow. A positive NPV states that

the investment will have a good impact on the company. There is an inverse relationship

between NPV and the discount rate. It states that a low discount increases the NPV result

whereas the high rate of discount reduces the capital's net present value.

b. ii. Internal rate of return: The internal rate of return or the discount rate which is

used in NPV is another method of calculating the appraisal of capital budgeting. The IRR

is responsible for measuring the efficiency of the capital investment in a project. If the

cost of capital invested is lower than the IRR the project is accepted whereas if the capital

invested cost is more than IRR the project has more possibility to get rejected.

b. iii. Payback period: It is measured to calculate the time taken to get the principal

investment amount back.

5

Illustration 1: Capital Budgeting

process and decide which project will benefit the company in the long run by generating profit as

well as maintaining sufficient cash for the short term operations.

(Source: The capital budgeting, 2017)

i (b) Advantages and disadvantages of Investment Appraisal Methods

The Investment appraisal of new projects involves deciding whether the new machines,

set up new plant, procuring of buildings or replacement of tools are worth to fund or not. These

methods incorporates payback period, net present value and internal rate of return which is

calculated to decide whether the investment decision should be taken or not (Preve and Allende,

2010).

b. i Net present value: The term NPV is a method used for calculating the investment

appraisal which focuses on surplus or shortage of cash inflow. A positive NPV states that

the investment will have a good impact on the company. There is an inverse relationship

between NPV and the discount rate. It states that a low discount increases the NPV result

whereas the high rate of discount reduces the capital's net present value.

b. ii. Internal rate of return: The internal rate of return or the discount rate which is

used in NPV is another method of calculating the appraisal of capital budgeting. The IRR

is responsible for measuring the efficiency of the capital investment in a project. If the

cost of capital invested is lower than the IRR the project is accepted whereas if the capital

invested cost is more than IRR the project has more possibility to get rejected.

b. iii. Payback period: It is measured to calculate the time taken to get the principal

investment amount back.

5

Illustration 1: Capital Budgeting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

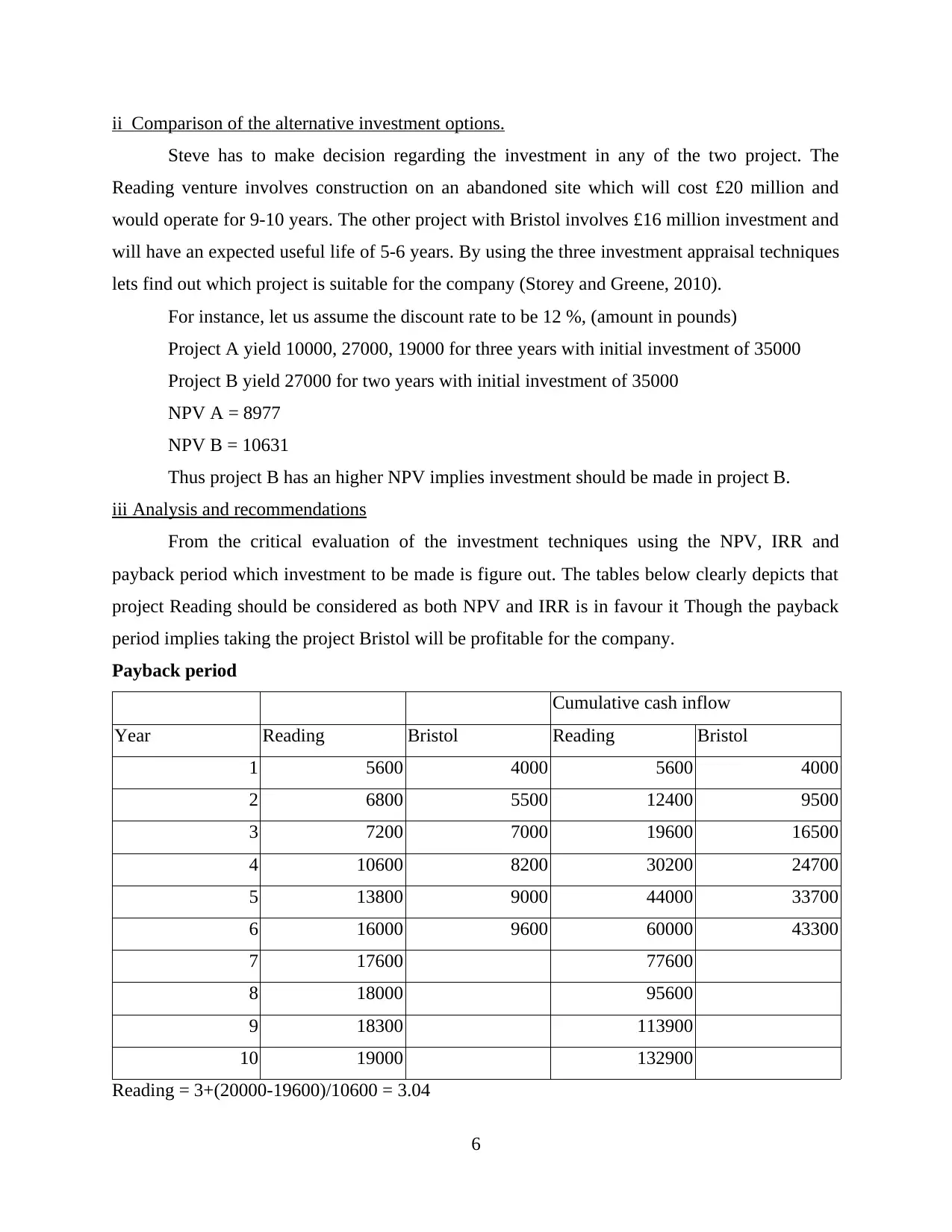

ii Comparison of the alternative investment options.

Steve has to make decision regarding the investment in any of the two project. The

Reading venture involves construction on an abandoned site which will cost £20 million and

would operate for 9-10 years. The other project with Bristol involves £16 million investment and

will have an expected useful life of 5-6 years. By using the three investment appraisal techniques

lets find out which project is suitable for the company (Storey and Greene, 2010).

For instance, let us assume the discount rate to be 12 %, (amount in pounds)

Project A yield 10000, 27000, 19000 for three years with initial investment of 35000

Project B yield 27000 for two years with initial investment of 35000

NPV A = 8977

NPV B = 10631

Thus project B has an higher NPV implies investment should be made in project B.

iii Analysis and recommendations

From the critical evaluation of the investment techniques using the NPV, IRR and

payback period which investment to be made is figure out. The tables below clearly depicts that

project Reading should be considered as both NPV and IRR is in favour it Though the payback

period implies taking the project Bristol will be profitable for the company.

Payback period

Cumulative cash inflow

Year Reading Bristol Reading Bristol

1 5600 4000 5600 4000

2 6800 5500 12400 9500

3 7200 7000 19600 16500

4 10600 8200 30200 24700

5 13800 9000 44000 33700

6 16000 9600 60000 43300

7 17600 77600

8 18000 95600

9 18300 113900

10 19000 132900

Reading = 3+(20000-19600)/10600 = 3.04

6

Steve has to make decision regarding the investment in any of the two project. The

Reading venture involves construction on an abandoned site which will cost £20 million and

would operate for 9-10 years. The other project with Bristol involves £16 million investment and

will have an expected useful life of 5-6 years. By using the three investment appraisal techniques

lets find out which project is suitable for the company (Storey and Greene, 2010).

For instance, let us assume the discount rate to be 12 %, (amount in pounds)

Project A yield 10000, 27000, 19000 for three years with initial investment of 35000

Project B yield 27000 for two years with initial investment of 35000

NPV A = 8977

NPV B = 10631

Thus project B has an higher NPV implies investment should be made in project B.

iii Analysis and recommendations

From the critical evaluation of the investment techniques using the NPV, IRR and

payback period which investment to be made is figure out. The tables below clearly depicts that

project Reading should be considered as both NPV and IRR is in favour it Though the payback

period implies taking the project Bristol will be profitable for the company.

Payback period

Cumulative cash inflow

Year Reading Bristol Reading Bristol

1 5600 4000 5600 4000

2 6800 5500 12400 9500

3 7200 7000 19600 16500

4 10600 8200 30200 24700

5 13800 9000 44000 33700

6 16000 9600 60000 43300

7 17600 77600

8 18000 95600

9 18300 113900

10 19000 132900

Reading = 3+(20000-19600)/10600 = 3.04

6

Bristol= 2+(16000-9500)/7000 =2.93

Project Bristol should be adopted.

Net present value

Discounted

cash flows

Year A B

Discounting

factor @ 10% A B

1 5600 4000 0.9091 5090.91 3636.36

2 6800 5500 0.8264 5619.83 4545.45

3 7200 7000 0.7513 5409.47 5259.20

4 10600 8200 0.6830 7239.94 5600.71

5 13800 9000 0.6209 8568.71 5588.29

6 16000 9600 0.5645 9031.58 5418.95

7 17600 0.5132 9031.58

8 18000 0.4665 8397.13

9 18300 0.4241 7760.99

10 19000 0.3855 7325.32

66150.15 30048.97

Less: Initial investment 20000 16000

Net present Value 46150.15 14048.97

According to NPV project Reading should be adopted

Internal rate of return

Year A B

Initial investment -20000 -16000

1 5600 4000

2 6800 5500

3 7200 7000

4 10600 8200

5 13800 9000

6 16000 9600

7

Project Bristol should be adopted.

Net present value

Discounted

cash flows

Year A B

Discounting

factor @ 10% A B

1 5600 4000 0.9091 5090.91 3636.36

2 6800 5500 0.8264 5619.83 4545.45

3 7200 7000 0.7513 5409.47 5259.20

4 10600 8200 0.6830 7239.94 5600.71

5 13800 9000 0.6209 8568.71 5588.29

6 16000 9600 0.5645 9031.58 5418.95

7 17600 0.5132 9031.58

8 18000 0.4665 8397.13

9 18300 0.4241 7760.99

10 19000 0.3855 7325.32

66150.15 30048.97

Less: Initial investment 20000 16000

Net present Value 46150.15 14048.97

According to NPV project Reading should be adopted

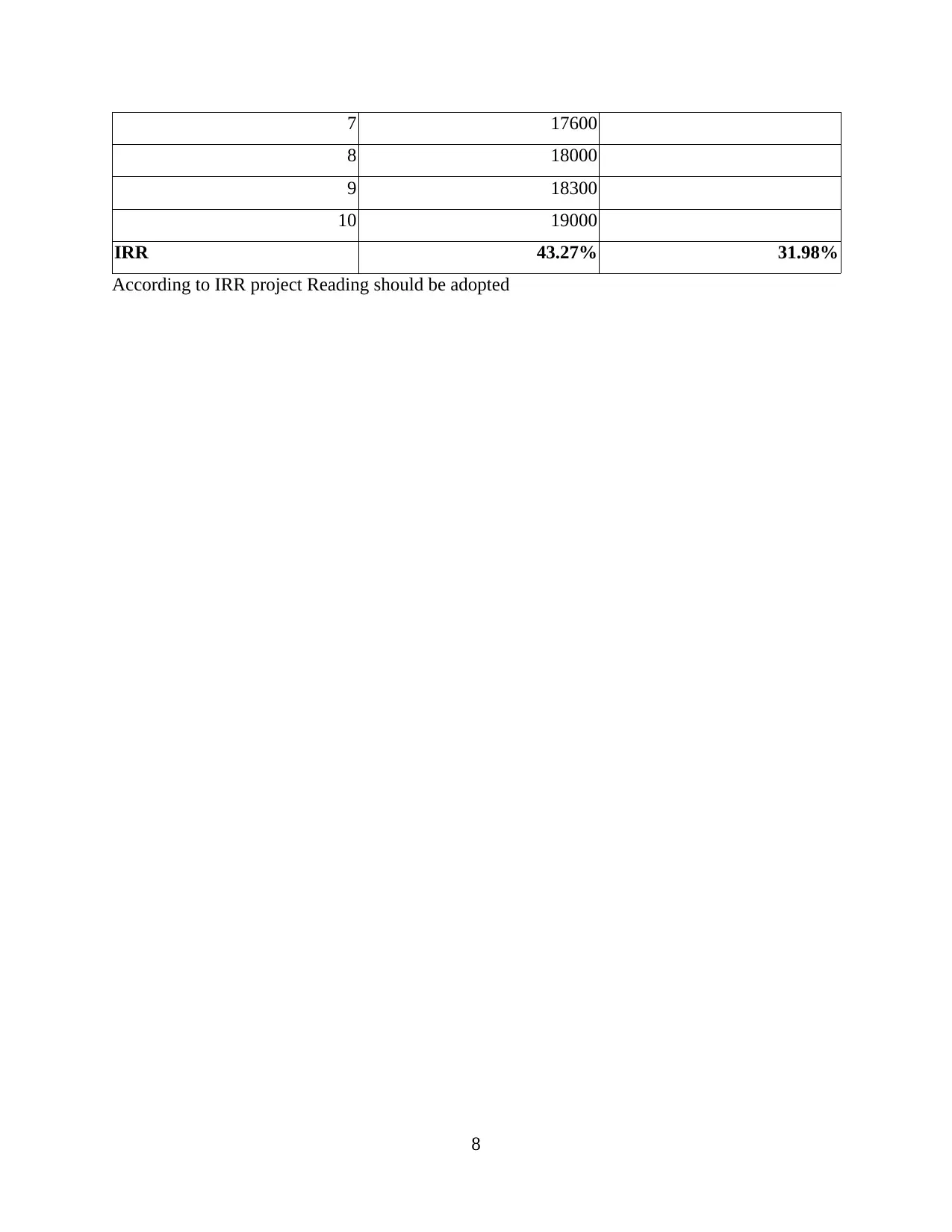

Internal rate of return

Year A B

Initial investment -20000 -16000

1 5600 4000

2 6800 5500

3 7200 7000

4 10600 8200

5 13800 9000

6 16000 9600

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7 17600

8 18000

9 18300

10 19000

IRR 43.27% 31.98%

According to IRR project Reading should be adopted

8

8 18000

9 18300

10 19000

IRR 43.27% 31.98%

According to IRR project Reading should be adopted

8

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.